Parrondo games with spatial dependence, II

Abstract

Let game be Toral’s cooperative Parrondo game with (one-dimensional) spatial dependence, parameterized by and , and let game be the special case . In previous work we investigated and , the mean profits per turn to the ensemble of players always playing game and always playing the randomly mixed game . These means were computable for , at least, and appeared to converge as , suggesting that the Parrondo region (i.e., the region in which and ) has nonzero volume in the limit. The convergence was established under certain conditions, and the limits were expressed in terms of a parameterized spin system on the one-dimensional integer lattice. In this paper we replace the random mixture with the nonrandom periodic pattern , where and are positive integers. We show that , the mean profit per turn to the ensemble of players repeatedly playing the pattern , is computable for and , at least, and appears to converge as , albeit more slowly than in the random-mixture case. Again this suggests that the Parrondo region ( and ) has nonzero volume in the limit. Moreover, we can prove this convergence under certain conditions and identify the limits.

Keywords: Parrondo’s paradox; cooperative Parrondo games; Markov chain; stationary distribution; equivalence class; dihedral group; nonrandom periodic patterns; strong law of large numbers.

1 Introduction

Toral [1] introduced what he called cooperative Parrondo games, in which there are players labeled from 1 to and arranged in a circle in clockwise order. At each turn, one player is chosen at random to play. Call him player . He plays either game or game . In game he tosses a fair coin. In game , he tosses a -coin (i.e., is the probability of heads) if his neighbors and are both losers, a -coin if is a loser and is a winner, a -coin if is a winner and is a loser, and a -coin if and are both winners. (Because of the circular arrangement, player 0 is player and player is player 1.) A player’s status as winner or loser depends on the result of his most recent game. The player of either game wins one unit with heads and loses one unit with tails. Under these assumptions, the model has an integer parameter, , and four probability parameters, , , , and . See Figure 1.

Toral used computer simulation to show that, with , 100, or 200, , , and , game is fair, game is losing, but both the random mixture (toss a fair coin, play game if heads, game if tails) and the nonrandom periodic pattern (i.e., ), also denoted by , are winning, providing new examples of Parrondo’s paradox (Harmer and Abbott [2], Abbott [3]). Ethier and Lee [4] investigated and , the mean profits per turn to the ensemble of players always playing game and always playing the randomly mixed game . These means were computable for , at least, and appeared to converge as , suggesting that the Parrondo region (i.e., the region in which and ) has nonzero volume in the limit. In [5] this convergence was established under certain conditions on , and the limits were expressed in terms of a parameterized spin system on the one-dimensional integer lattice. In addition, assuming , explicit formulas for the means were derived for , and this allowed us to visualize the Parrondo region in these cases. Incidentally, we note that the results can easily be extended to the more general random mixture , in which case the mean profit per turn is denoted by .

In this paper we replace the random mixture with the nonrandom periodic pattern , also denoted by , where and are positive integers. We show that , the mean profit per turn to the ensemble of players repeatedly playing the pattern , is computable for and , at least, and appears to converge as , albeit more slowly than in the random-mixture case. Again this suggests that the Parrondo region ( and ) has nonzero volume in the limit. Elsewhere [6] we establish this convergence under certain conditions on (see Appendix A herein for the conditions), and show that the limit as coincides with , where . In addition, assuming , explicit formulas for can be derived for and , and this allows us to visualize the Parrondo region in these cases.

Nonrandom patterns of the form have been part of the Parrondo paradox literature from its inception (Harmer and Abbott [7]). The reason is clear. The flashing Brownian ratchet (Ajdari and Prost [8]), which motivated the formulation of Parrondo’s games, is most closely related to the pattern (i.e., ). But this pattern is not winning for the original capital-dependent games, so Parrondo considered instead. Analysis of these patterns was initially based on simulation. Analytical formulas for the mean profit per turn were found by Ekhad and Zeilberger [9] and Velleman and Wagon [10], and in the history-dependent setting by Kay and Johnson [11]. Behrends [12] generalized Parrondo’s games in such a way that the random-mixture case and the nonrandom-pattern case could be studied simultaneously, and he too found an expression for the mean profit per turn. Ethier and Lee [13] proved a strong law of large numbers and showed that the Parrondo effect appears (in the capital-dependent setting with the so-called bias parameter equal to 0) for the pattern for all integers except . The problem of finding the most profitable pattern (not restricted to patterns of the form ) was investigated in [9] and [10] and eventually solved by Dinis [14], the winning pattern being (and its cyclic permutations) in the case of Parrondo’s original parameters. In Toral’s [15] nonspatial -player model with redistribution of wealth, Ethier and Lee [16] showed that the mean profit per turn for the pattern converges, as , to the mean profit per turn for the random mixture with , which does not depend on . This foreshadowed the results of the present paper and [6].

2 The Markov Chain and its Reduction

The Markov chain formalized by Mihailović and Rajković [17] keeps track of the status (loser or winner, 0 or 1) of each of the players. Its state space is the product space

with states. Let ; in other words, is the integer (0, 1, 2, or 3) whose binary representation is ; of course and . Also, let be the element of equal to except at the th component; for example, .

The one-step transition matrix for this Markov chain depends not only on but on the four probability parameters , , , and , which we assume satisfy for . (This rules out Toral’s choice of the probability parameters, at least for now, but we will return to this point in Sec. 4. We do not assume that until Sec. 5.) It has the form

| (1) |

| (2) |

where for and empty sums are 0, and otherwise.

The description of the model suggests that its long-term behavior should be invariant under rotation (and, if , reflection) of the players. In order to maximize the value of for which exact computations are feasible, we will use the following lemma from [4] to make this precise.

Lemma 1.

Fix , let be a subgroup of the symmetric group . For and , write . Let be the one-step transition matrix for a Markov chain in with a unique stationary distribution . Assume that

| (3) |

Then for all and .

Let us say that is equivalent to (written ) if there exists such that , and let us denote the equivalence class containing by . Then, in addition, induces a one-step transition matrix for a Markov chain in the quotient set (i.e., the set of equivalence classes) defined by the formula

| (4) |

the second sum extending over only those for which the various are distinct. Furthermore, if has a unique stationary distribution , then the unique stationary distribution is given by , where denotes the cardinality of the equivalence class .

As we saw in [4], Lemma 1 applies to of (1) and (2) with being the subgroup of cyclic permutations (or rotations) of . If , then Lemma 1 also applies to with being the subgroup generated by the cyclic permutations and the order-reversing permutation (rotations and/or reflections) of , the dihedral group of order . The resulting one-step transition matrix has smaller dimension than (see Table 1 of [4]), thereby making matrix computations feasible for larger .

If , we denote by . Of course the same conclusions apply to . We would like to argue that they also apply to for each . For this we need to show that the mapping has a certain multiplicative property.

Given a subgroup of , let us say that a square matrix (not necessarily stochastic) with rows and columns indexed by is -invariant if (3) holds. If is -invariant, then we can define as in (4).

Lemma 2.

Let be a subgroup of . If the square matrices and are -invariant, then is -invariant, and .

Proof.

The first assertion follows from the identity

The second is a consequence of

so the proof is complete. ∎

With being the subgroup of cyclic permutations or (if ) the dihedral group of order , and are of course -invariant. Consequently, for each , Lemma 2 tells us that is -invariant as well. This fact will be needed in the next section.

3 Strong Law of Large Numbers

We will need the following version of the SLLN.

Theorem 3 (Ethier and Lee [13]).

Let and be one-step transition matrices for Markov chains in a finite state space . Fix . Assume that , as well as all cyclic permutations of , are irreducible and aperiodic, and let the row vector be the unique stationary distribution of . Given a real-valued function on , define the payoff matrix . Define and , where denotes the Hadamard (entrywise) product, and put

where denotes a column vector of s with entries indexed by . Let be a nonhomogeneous Markov chain in with one-step transition matrices , , , , and so on, and let the initial distribution be arbitrary. For each , define and . Then a.s.

Here “a.s.” stands for “almost surely,” meaning “with probability 1.”

Our original Markov chain has state space and its one-step transition matrix is given by (1) and (2), but Theorem 3 does not apply directly. Instead, we augment the state space, letting and keeping track not only of the status of each player as described by but also of the label of the next player to play, say . The new one-step transition matrix has the form

where for , and otherwise. If , we denote by . The one-step transition matrix , as well as all cyclic permutations of , are irreducible and aperiodic, so let be the unique stationary distribution of . The payoff matrix now has each nonzero entry equal to , so Theorem 3 applies. Since , we have

| (5) |

where denotes a column vector of s with entries indexed by . Here is the Hadamard (entrywise) product , where is the matrix each of whose entries is , , or according to whether the corresponding entry of is of the form , , or .

Lemma 4.

Fix and let be the unique stationary distribution of . Then has unique stationary distribution and

| (6) |

for .

Proof.

Let be stationary for . We will show that it has the form stated in the lemma. Let be a nonhomogeneous Markov chain in with one-step transition matrices ( times), ( times), and initial distribution . Then has distribution . Let be the projections of onto , and let be the marginal of on . Then is a nonhomogeneous Markov chain in with one-step transition matrices ( times), ( times), and initial distribution . Furthermore, has distribution as well as distribution . So is the unique stationary distribution of , as assumed in the statement of the lemma. On the other hand, writing , is independent of and uniform. So the distribution of must have the stated form.

It follows from (5) and Lemma 4 that

| (7) |

where is obtained from by replacing each by (prior to any simplification using ) and denotes a column vector of s with entries indexed by . This expresses the mean profit in terms of the original one-step transition matrices and and the unique stationary distribution of . However, for computational purposes, we would like to express it in terms of the reduced one-step transition matrices and and the unique stationary distribution of . The subgroup implicit in the notation is either the subgroup of cyclic permutations of or (if ) the dihedral group of order .

Theorem 5.

Given , let be the nonhomogeneous Markov chain in with one-step transition matrices , , , , and so on, and arbitrary initial distribution. Define

where the payoff function is for a win and for a loss, determined by whether the corresponding entry of is of the form or . Let for each . Then a.s., where

| (8) |

is obtained from by replacing each by (prior to any simplification using ), and denotes a column vector of s with entries indexed by .

Proof.

This is an application of Theorem 3. To show that the right sides of (7) and (8) are equal, we note that, for any -invariant square matrix , we have, using Lemma 1,

| (9) | |||||

where denotes a column vector of s of the appropriate dimension. Now if is -invariant, then so too is , and likewise for by Lemma 2; using (9) and Lemma 2,

for . (Note that .) ∎

We conclude with an application of the SLLN for this model.

Let us denote , the mean profit per turn to the ensemble of players always playing game , by to emphasize its dependence on the parameter vector. As shown in [4],

| (10) |

Corollary 6.

In particular, if and , then .

4 Reducible Cases

We have assumed that for , which ensures that the Markov chain for game is irreducible and aperiodic. This assumption was weakened to some extent in [4]. We can derive the results obtained here under analogous conditions by noticing that the irreducibility and aperiodicity assumptions of Theorem 3 can be weakened to simply ergodicity, which requires a unique stationary distribution and convergence of the distribution at time to that stationary distribution as , regardless of the initial distribution.

Fix . We first notice that the Markov chain in with one-step transition matrix , , …, or is ergodic (in fact, irreducible and aperiodic) for all choices of the parameters . It remains to check the ergodicity of the Markov chain in with one-step transition matrix , , …, or . We denote by the state consisting of all 0s, and by the state consisting of all s.

-

1.

Suppose and for , as Toral [1] originally assumed. Then state cannot be reached from by and therefore by , , …, and . For these one-step transition matrices, is irreducible and aperiodic while is transient. Thus, the required ergodicity holds. Theorem 3 (modified as noted above) and Theorem 5 apply.

- 2.

-

3.

Suppose and for . This is analogous to case 1 but with the role of played by .

-

4.

Suppose and for . This is analogous to case 2, except that state is absorbing for game and .

- 5.

-

6.

Suppose , , and for . Then both and are absorbing for , and absorption occurs with probability 1. However, the Markov chain with one-step transition matrix , , …, or has different behavior. If is odd, it is irreducible and aperiodic in , whereas if is even, is irreducible and aperiodic and and are transient. Again, Theorem 3 (as stated if is odd, modified if is even) and Theorem 5 apply.

5 The Parrondo Region

In this section we assume that , so that the coin tossed in game depends only on the number of winners among the two nearest neighbors. For fixed and , we have three free probability parameters, and , so our parameter space is the unit cube . With caution (see Sec. 4), we can also include parts of the boundary. Of interest are the Parrondo region, the subset of the parameter space in which the Parrondo effect (i.e., and ) appears, and the anti-Parrondo region, the subset of the parameter space in which the anti-Parrondo effect (i.e., and ) appears.

Theorem 7.

Fix and . With for , the parameter vector belongs to the Parrondo region if and only if the parameter vector belongs to the anti-Parrondo region. In particular, the Parrondo region and the anti-Parrondo region have the same (three-dimensional) volume.

Proof.

We can therefore focus our attention in what follows on the Parrondo region.

Using the mean formula (8) in terms of the reduced Markov chains, together with the assumption that , when we find that

Since

(see [4]), the Parrondo region for the pattern is described by and , or, equivalently,

Similarly, the Parrondo region for the pattern is described by

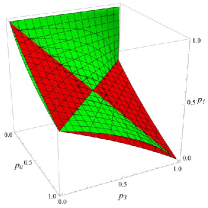

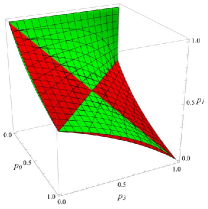

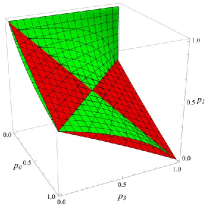

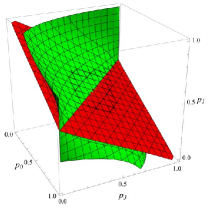

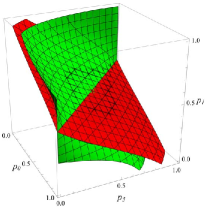

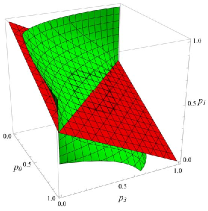

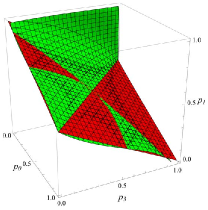

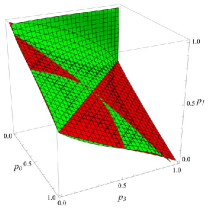

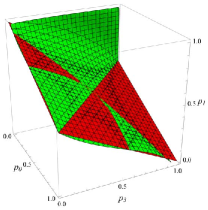

With the parameter space being the unit cube, the Parrondo region is the union of two connected components. See row 1 of Figure 2. For the pattern, integration yields its exact volume, . For the pattern, numerical integration gives its approximate volume, 0.0166398. For the pattern, integration results in its exact volume (rounded), 0.0268219.

In [4] we pointed out a close relationship between the spatially dependent Parrondo games with and the history-dependent Parrondo games of Parrondo, Harmer, and Abbott [18]. Specifically, the Parrondo regions for the equally weighted random mixtures were shown to be equal in the two models. The analogous result for the nonrandom pattern fails, however.

When or , we have explicit, albeit very complicated, formulas for with . It would be impractical to state those formulas here. Instead, we plot the Parrondo regions and the anti-Parrondo regions for these cases in rows 2 and 3 of Figure 2. They are surprisingly similar to the regions for the random-mixture cases depicted in [4].

Table 1 displays the mean profits for and the six choices of with for Toral’s choice of the probability parameters . Computations were done using Mathematica 8 and a minor modification of the program displayed in Appendix A of [4]. By Table 3 of [4], for except for , so the Parrondo effect is present except in 22 of the 96 cases. Furthermore this calculation suggests that each mean converges to a limit as , although the rate of convergence is much slower than in the random-mixture case.

In fact, in [6] we proved that, under certain conditions (see Appendix A herein), converges to the same limit that , the mean profit of the randomly mixed game , converges to, where . The last row of Table 1 shows this limit. Tables 2 and 3 analyze two other examples, a second point on the boundary of the unit cube and a point in the interior. These are the same examples as the ones studied in [4].

To illustrate the slower convergence rate, let us consider the example , , and . By , matches its limiting value to only two significant digits. On the other hand, by (the largest for which computations have been done in the random-mixture case), has stabilized to four significant digits and has stabilized to 11 significant digits.

For , , , or , and , evaluation of the stationary distribution of is computationally intensive because 32.4% of the entries of this one-step transition matrix are nonzero. This is the reason we stopped with . On the other hand, only 0.236% of the entries of the one-step transition matrix are nonzero, so it is relatively easy to calculate its stationary distribution. Furthermore, the faster convergence in the random-mixture case allows us to obtain six significant digits of using only the computed values for .

| 3 | 0.00067249 | 0.00179203 | ||||

|---|---|---|---|---|---|---|

| 4 | 0.00877041 | 0.02345828 | 0.03569464 | 0.00352220 | 0.01011944 | 0.00244238 |

| 5 | 0.00466232 | 0.00501198 | 0.00434917 | 0.00320648 | 0.00465517 | 0.00240873 |

| 6 | 0.00497503 | 0.00590528 | 0.00513509 | 0.00325099 | 0.00498178 | 0.00241857 |

| 7 | 0.00496767 | 0.00621483 | 0.00637676 | 0.00326314 | 0.00497331 | 0.00242540 |

| 8 | 0.00494802 | 0.00604194 | 0.00599064 | 0.00327193 | 0.00495138 | 0.00243115 |

| 9 | 0.00493507 | 0.00598135 | 0.00588386 | 0.00327802 | 0.00493728 | 0.00243582 |

| 10 | 0.00492347 | 0.00593756 | 0.00584200 | 0.00328237 | 0.00492494 | 0.00243961 |

| 11 | 0.00491339 | 0.00589846 | 0.00578690 | 0.00328558 | 0.00491438 | 0.00244272 |

| 12 | 0.00490464 | 0.00586697 | 0.00574489 | 0.00328800 | 0.00490531 | 0.00244529 |

| 13 | 0.00489699 | 0.00584063 | 0.00571065 | 0.00328986 | 0.00489744 | 0.00244745 |

| 14 | 0.00489026 | 0.00581820 | 0.00568131 | 0.00329133 | 0.00489056 | 0.00244927 |

| 15 | 0.00488431 | 0.00579891 | 0.00565623 | 0.00329249 | 0.00488449 | 0.00245083 |

| 16 | 0.00487900 | 0.00578213 | 0.00563452 | 0.00329343 | 0.00487912 | 0.00245217 |

| 17 | 0.00487426 | 0.00576740 | 0.00561552 | 0.00329420 | 0.00487432 | 0.00245334 |

| 18 | 0.00486999 | 0.00575438 | 0.00559876 | 0.00329483 | 0.00487001 | 0.00245437 |

| 0.00479089 | 0.00554084 | 0.00532972 | 0.00329853 | 0.00479089 | 0.00246903 | |

| 3 | 0.02224875 | 0.04081923 | 0.04914477 | 0.01124438 | 0.02978942 | 0.00756605 |

|---|---|---|---|---|---|---|

| 4 | 0.00771486 | 0.00053987 | 0.00804643 | 0.00719297 | 0.00668482 | |

| 5 | 0.00959590 | 0.00896406 | 0.00788233 | 0.00808935 | 0.00944220 | 0.00660145 |

| 6 | 0.00883530 | 0.00657582 | 0.00395457 | 0.00787821 | 0.00870056 | 0.00649756 |

| 7 | 0.00866607 | 0.00674014 | 0.00456448 | 0.00774894 | 0.00856648 | 0.00641956 |

| 8 | 0.00847909 | 0.00646246 | 0.00421207 | 0.00764628 | 0.00840151 | 0.00635716 |

| 9 | 0.00834684 | 0.00633835 | 0.00413293 | 0.00756557 | 0.00828507 | 0.00630657 |

| 10 | 0.00824074 | 0.00622264 | 0.00402604 | 0.00750030 | 0.00819047 | 0.00626485 |

| 11 | 0.00815521 | 0.00613328 | 0.00394982 | 0.00744652 | 0.00811356 | 0.00622992 |

| 12 | 0.00808457 | 0.00605892 | 0.00388449 | 0.00740147 | 0.00804952 | 0.00620028 |

| 13 | 0.00802529 | 0.00599680 | 0.00383017 | 0.00736319 | 0.00799540 | 0.00617485 |

| 14 | 0.00797483 | 0.00594398 | 0.00378377 | 0.00733029 | 0.00794905 | 0.00615279 |

| 15 | 0.00793135 | 0.00589853 | 0.00374381 | 0.00730171 | 0.00790890 | 0.00613348 |

| 16 | 0.00789351 | 0.00585901 | 0.00370899 | 0.00727665 | 0.00787378 | 0.00611645 |

| 17 | 0.00786027 | 0.00582433 | 0.00367839 | 0.00725451 | 0.00784280 | 0.00610132 |

| 18 | 0.00783085 | 0.00579365 | 0.00365129 | 0.00723480 | 0.00781528 | 0.00608779 |

| 0.00734784 | 0.00529172 | 0.00320388 | 0.00689768 | 0.00734784 | 0.00584750 | |

| 3 | 0.0064599 | 0.00792562 | 0.0013604 | 0.00640450 | ||

|---|---|---|---|---|---|---|

| 4 | 0.0143185 | 0.0137926 | 0.0079878 | 0.00959254 | 0.0141773 | 0.00690030 |

| 5 | 0.0154167 | 0.0187545 | 0.0174399 | 0.00977539 | 0.0153785 | 0.00699045 |

| 6 | 0.0155020 | 0.0197053 | 0.0197681 | 0.00980464 | 0.0154761 | 0.00703029 |

| 7 | 0.0154423 | 0.0197654 | 0.0202208 | 0.00980993 | 0.0154198 | 0.00705342 |

| 8 | 0.0153749 | 0.0196547 | 0.0201990 | 0.00980937 | 0.0153555 | 0.00706817 |

| 9 | 0.0153182 | 0.0195309 | 0.0200777 | 0.00980683 | 0.0153015 | 0.00707811 |

| 10 | 0.0152717 | 0.0194237 | 0.0199518 | 0.00980357 | 0.0152575 | 0.00708508 |

| 11 | 0.0152334 | 0.0193346 | 0.0198414 | 0.00980014 | 0.0152212 | 0.00709014 |

| 12 | 0.0152014 | 0.0192605 | 0.0197479 | 0.00979677 | 0.0151908 | 0.00709392 |

| 13 | 0.0151742 | 0.0191982 | 0.0196688 | 0.00979356 | 0.0151649 | 0.00709679 |

| 14 | 0.0151508 | 0.0191452 | 0.0196013 | 0.00979055 | 0.0151427 | 0.00709903 |

| 15 | 0.0151306 | 0.0190994 | 0.0195432 | 0.00978777 | 0.0151233 | 0.00710080 |

| 16 | 0.0151128 | 0.0190596 | 0.0194927 | 0.00978519 | 0.0151064 | 0.00710221 |

| 17 | 0.0150971 | 0.0190246 | 0.0194483 | 0.00978280 | 0.0150913 | 0.00710337 |

| 18 | 0.0150831 | 0.0189936 | 0.0194090 | 0.00978060 | 0.0150779 | 0.00710431 |

| 0.0148448 | 0.0184829 | 0.0187645 | 0.00973219 | 0.0148448 | 0.00710942 | |

6 Conclusions

We considered the spatially dependent, or cooperative, Parrondo games of Toral [1], which assume players arranged in a circle, and in which the win probability for a player depends on the status of the player’s two nearest neighbors. There are three games, game without spatial dependence, game with spatial dependence, and the nonrandom periodic pattern , or , with . The model is described by a Markov chain with states and parameters . To maximize the value of for which exact computations are feasible, we assumed and regarded states as equivalent if they are equal after a rotation and/or reflection of the players. This allowed us to compute the mean profits per turn, , to the ensemble of players for and and several choices of the parameter vector , including Toral’s choice. The results provide numerical evidence, but not a proof, that converges as and that the Parrondo effect (i.e., and ) persists for all sufficiently large for a set of parameter vectors having nonzero volume. As we noted in [4], this suggests that the spatially-dependent version of Parrondo’s paradox is a robust phenomenon that remains present in the thermodynamic limit.

This is the main conclusion, but there are several other noteworthy findings. We have shown that the sequence of profits to the ensemble of players obeys the strong law of large numbers. This is relevant to defining what is meant by a winning, losing, and fair game. For and , explicit formulas for and are available, so with the help of computer graphics, we have demonstrated that one can visualize the Parrondo region, the region in the three-dimensional parameter space in which the Parrondo effect appears. There is also an anti-Parrondo region, and we have shown that it is symmetric with the Parrondo region, as might be expected.

We have restricted our attention to the one-dimensional version of the model, but our methods may have applicability to the two-dimensional version, already investigated by Mihailović and Rajković [19] using computer simulation. In a separate paper [6] we prove, under conditions that can likely be improved (see Appendix A below), the convergence of as , and we express the limit in terms of a spin system on the one-dimensional integer lattice.

Acknowledgments

The work of S. N. Ethier was partially supported by a grant from the Simons Foundation (209632). It was also supported by a Korean Federation of Science and Technology Societies grant funded by the Korean Government (MEST, Basic Research Promotion Fund). The work of J. Lee was supported by the Basic Science Research Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Education, Science and Technology (2012-0004434).

Appendix A

We have stated (referring to [5] and [6] for details) that, under certain conditions on and , the means and converge as . We would like to briefly describe the conditions and identify the limits.

The limits depend on the spin system in the infinite product space ( being the set of integers) with generator of the form

| (11) |

where

| (12) |

and and for . Intuitively, a “spin,” 0 or 1, is associated with each “site” , and the spin is “flipped” at site at exponential rate . If the sum in (11) were finite, this would define a pure-jump Markov process, but because the sum is infinite, it defines a Markov process with instantaneous states. See Liggett [20] for a thorough account of spin systems.

We have shown in [5] that the spin system with generator is ergodic (i.e., it has a unique stationary distribution and the distribution at time converges weakly to that stationary distribution as , regardless of the initial distribution) if at least one of the following four conditions is satisfied:

| (13) |

| (14) |

| (15) |

| (16) |

Under the assumption that , the (three-dimensional) volumes of the regions described by (13)–(16) are respectively 7/12, 1/3, 7/32, and 2/3. The volume of the union of these four regions is 3323/4032, representing about 82.4% of the parameter space. Of our three examples (Tables 1–3), only the third one belongs to this union.

It is shown in [5] that, if the spin system with generator is ergodic with unique stationary distribution , then the mean converges as to

| (17) |

where denotes the two-dimensional marginal of .

If , we denote by . A similar argument shows that, if and the spin system with generator is ergodic with unique stationary distribution , then, for the random mixture , the mean converges as to (17) but with replaced by and each replaced by . Notice that is just (11) (with (12)) but with each replaced by (and each replaced by ), so the ergodicity condition holds if at least one of (13)–(16) holds with each replaced by .

Finally, it is shown in [6] that, if the assumption of the preceding paragraph holds with , then the mean converges as to the limit of the preceding paragraph with .

References

- [1] R. Toral, Cooperative Parrondo games, Fluct. Noise Lett. 1 (2001) L7–L12.

- [2] G. P. Harmer and D. Abbott, A review of Parrondo’s paradox, Fluct. Noise Lett. 2 (2002) R71–R107.

- [3] D. Abbott, Asymmetry and disorder: A decade of Parrondo’s paradox, Fluct. Noise Lett. 9 (2010) 129–156.

- [4] S. N. Ethier and J. Lee, Parrondo games with spatial dependence, Fluct. Noise Lett. 11 (2012), to appear, http://arxiv.org/abs/1202.2609.

- [5] S. N. Ethier and J. Lee, Parrondo games with spatial dependence and a related spin system, http://arxiv.org/abs/1203.0818.

- [6] S. N. Ethier and J. Lee, Parrondo games with spatial dependence and a related spin system, II, http://arxiv.org/abs/1206.xxxx.

- [7] G. P. Harmer and D. Abbott, Parrondo’s paradox, Statist. Sci. 14 (1999) 206–213.

- [8] A. Ajdari and J. Prost, Drift induced by a spatially periodic potential of low symmetry: Pulsed dielectrophoresis, C. R. Acad. Sci., Sér. 2 315 (1992) 1635–1639.

- [9] S. B. Ekhad and D. Zeilberger, Remarks on the Parrondo paradox, Personal J. of Ekhad and Zeilberger (2000) http://www.math.rutgers.edu/~zeilberg/pj.html

- [10] D. Velleman and S. Wagon, Parrondo’s paradox, Math. Educ. Res. 9 (2001) 85–90.

- [11] R. J. Kay and N. F. Johnson, Winning combinations of history-dependent games, Phys. Rev. E 67 (2003) 056128.

- [12] E. Behrends, The mathematical background of Parrondo’s paradox, Proc. SPIE Noise in Complex Systems and Stochastic Dynamics II, Maspalomas, Spain, Ed: Z. Gingl, 5471 (2004) 510–517.

- [13] S. N. Ethier and J. Lee, Limit theorems for Parrondo’s paradox, Electron. J. Probab. 14 (2009) 1827–1862.

- [14] L. Dinis, Optimal sequence for Parrondo games, Phys. Rev. E 77 (2008) 021124.

- [15] R. Toral, Capital redistribution brings wealth by Parrondo’s paradox, Fluct. Noise Lett. 2 (2002) L305–L311.

- [16] S. N. Ethier and J. Lee, Parrondo’s paradox via redistribution of wealth, Electron. J. Probab. 17 (2012) (20) 1–21.

- [17] Z. Mihailović and M. Rajković, One dimensional asynchronous cooperative Parrondo’s games, Fluct. Noise Lett. 3 (2003) L389–L398.

- [18] J. M. R. Parrondo, G. P. Harmer, and D. Abbott, New paradoxical games based on Brownian ratchets, Phys. Rev. Lett. 85 (2000) 5226–5229.

- [19] Z. Mihailović and M. Rajković, Cooperative Parrondo’s games on a two-dimensional lattice, Phys. A 365 (2006) 244–251.

- [20] T. M. Liggett, Interacting Particle Systems (Springer-Verlag, New York, 1985).