Sparse projections onto the simplex

Abstract

Most learning methods with rank or sparsity constraints use convex relaxations, which lead to optimization with the nuclear norm or the -norm. However, several important learning applications cannot benefit from this approach as they feature these convex norms as constraints in addition to the non-convex rank and sparsity constraints. In this setting, we derive efficient sparse projections onto the simplex and its extension, and illustrate how to use them to solve high-dimensional learning problems in quantum tomography, sparse density estimation and portfolio selection with non-convex constraints.

1 Introduction

We study the following sparse Euclidean projections:

Problem 1.

(Simplex) Given , find a Euclidean projection of onto the intersection of -sparse vectors and the simplex :

| (1) |

Problem 2.

(Hyperplane) Replace in (1) with the hyperplane constraint .

We prove that it is possible to compute such projections in quasilinear time via simple greedy algorithms.

Our motivation with these projectors is to address important learning applications where the standard sparsity/low-rank heuristics based on the /nuclear-norm are either given as a constraint or conflicts with the problem constraints. For concreteness, we highlight quantum tomography, density learning, and Markowitz portfolio design problems as running examples. We then illustrate provable non-convex solutions to minimize quadratic loss functions

| (2) |

subject to the constraints in Problem 1 and 2 with our projectors. In (2), we assume that is given and the (known) operator is linear.

For simplicity of analysis, our minimization approach is based on the projected gradient descent algorithm:

| (3) |

where is the -th iterate, is the gradient of the loss function, is a step-size, and is based on Problem 1 or 2. When the linear map in (2) provides bi-Lipschitz embedding for the constraint sets, we can derive rigorous approximation guarantees for the algorithm (3); cf., (Garg & Khandekar, 2009).111Surprisingly, a recent analysis of this algorithm along with similar assumptions indicates that rigorous guarantees can be obtained for minimization of general loss functions other than the quadratic (Bahmani et al., 2011).

To the best of our knowledge, explicitly sparse Euclidean projections onto the simplex and hyperplane constraints have not been considered before. The closest work to ours is the paper (Kyrillidis & Cevher, 2012). In (Kyrillidis & Cevher, 2012), the authors propose an alternating projection approach in regression where the true vector is already sparse and within a convex norm-ball constraint. In contrast, we consider the problem of projecting an arbitrary given vector onto convex-based and sparse constraints jointly.

At the time of this submission, we become aware of (Pilanci et al., 2012), which considers cardinality regularized loss function minimization subject to simplex constraints. Their convexified approach relies on solving a lower-bound to the objective function and has complexity, which is not scalable. We also note that regularizing with the cardinality constraints is generally easier: e.g., our projectors become simpler.

Notation:

Plain and boldface lowercase letters represent scalars and vectors, resp. The -th entry of a vector is , and , while is the model estimate at the -th iteration of an algorithm. Given a set , the complement is defined with respect to , and the cardinality is . The support set of is . Given a vector , is the projection (in ) of onto , i.e. , whereas is limited to entries. The all-ones column vector is , with dimensions apparent from the context. We define as the set of all -sparse subsets of , and we sometimes write to mean . The trace of a matrix is written .

2 Preliminaries

Basic definitions:

Without loss of generality, assume is sorted in descending order, so is the largest element. We denote for the (convex) Euclidean projector onto the standard simplex , and for its extension to . The (non-convex) Euclidean projector onto the set is , which retains the -largest in magnitude elements. In contrast to , the projection need not be unique.

Definition 2.1 (Operator ).

We define as the operator that keeps the -largest entries of (not in magnitude) and sets the rest to zero. This operation can be computed in -time.

Definition 2.2 (Euclidean projection ).

The projector onto the simplex is given by

for

Definition 2.3 (Euclidean projection ).

The projector onto the extended simplex is given by

Definition 2.4 (Restricted isometry property (RIP) (Candès et al., 2006)).

A linear operator satisfies the -RIP with constant if

| (4) |

Guarantees of the gradient scheme (3):

Let , , be a generative model where is an additive perturbation term and is the -sparse true model generating . If the RIP assumption (4) is satisfied, then the projected gradient descent algorithm in (3) features the following invariant on the objective (Garg & Khandekar, 2009):

| (5) |

for and stepsize . Hence, for , the iterations of the algorithm are contractive and (3) obtains a good approximation on the loss function. In addition, (Foucart, 2010) shows that we can guarantee approximation on the true model via

| (6) |

for and . Similarly, when , the iterations of the algorithm are contractive. Different step size strategies result in different guarantees; c.f., (Garg & Khandekar, 2009; Foucart, 2010; Kyrillidis & Cevher, 2011) for a more detailed discussion. Note that to satisfy a given RIP constant , random matrices with sub-Gaussian entries require . In low rank matrix cases, similar RIP conditions for (3) can be derived with approximation guarantees; cf., (Meka et al., 2010).

3 Underlying discrete problems

Let be a projection of onto or . We now make the following elementary observation:

Remark 1.

The Problem 1 and 2 statements can be equivalently transformed into the following nested minimization problem:

where and or .

Therefore, given , we can find by projecting onto or within the -dimensional space. Thus, the difficulty is finding . Hence, we split the problem into the task of finding the support and then finding the values on the support.

3.1 Problem 1

Given any support , the unique corresponding estimator is . We conclude that satisfies and , and

| (7) |

where .

Lemma 1.

Let where . Then, for all . Furthermore, .

Proof.

Directly from the definition of in Definition 2.2. The intuition is quite simple: the “threshold” should be smaller than the smallest entry in the selected support, or we unnecessarily shrink the coefficients that are larger without introducing any new support to the solution. Same arguments apply to inflating the coefficients to meet the simplex budget.∎

3.2 Problem 2

Similar to above, we conclude that satisfies and , where

| (9) |

where with and and .

4 Sparse projections onto and

Algorithm 1 below suggests an obvious greedy approach for the projection onto . We select the set by naively projecting as . Remarkably, this gives the correct support set for Problem 1, as we prove in Section 5.1. We call this algorithm the greedy selector and simplex projector (GSSP). The overall complexity of GSSP is dominated by the sort operation in -dimensions.

Unfortunately, the GSSP fails for Problem 2. As a result, we propose Algorithm 2 for the case which is non-obvious. The algorithm first selects the index of the largest element that has the same sign as . It then grows the index set one at a time by finding the farthest element from the current mean, as adjusted by lambda. Surprisingly, the algorithm finds the correct support set, as we prove in Section 5.2. We call this algorithm the greedy selector and hyperplane projector (GSHP), whose overall complexity is similar to GSSP.

5 Main results

Remark 2.

When the symbol is used as for any , then if , we enlarge until it has elements by taking the first elements that are not already in , and setting on these elements. The lexicographic approach is used to break ties when there are multiple solutions.

5.1 Correctness of GSSP

Proof.

Intuitively, the -largest coordinates should be in the solution. To see this, suppose that is the projection of . Let be one of the -(most positive) coordinates of and . Also, let such that . We can then construct a new vector where and . Therefore, satisfies the constraints, and it is closer to , i.e., . Hence, cannot be the projection.

To be complete in the proof, we also need to show that the cardinality solutions are as good as any other solution with cardinality less than . Suppose there exists a solution with support . Now add any elements to to form with size . Then consider restricted to , and let be its projection onto the simplex. Because this is a projection, , hence . ∎

5.2 Correctness of GSHP

Proof.

To motivate the support selection of GSHP, we now identify a key relation that holds for any :

| (10) |

By its left-hand side, this relation is invariant under permutation of . Moreover, the summands in the sum over are certainly non-negative for , so without loss of generality the solution sparsity of the original problem is . For , is maximized by picking an index that maximizes , which is what the algorithm does.

For the sake of clarity (and space), we first describe the proof of the case for and then explain how it generalizes for . In the sequel, let us use the shortcut .

Let be an optimal solution index set and let be the result computed by the algorithm. For a proof (of the case ) by contradiction, assume that and differ. Let be the first element of in the order of insertion into by the algorithm. Let be the element of that lies closest to . Without loss of generality, we may assume that , otherwise we could have chosen rather than as solution in the first place. Let be the indices added to by the algorithm before . Assume that is nonempty. We will later see how to ensure this.

Let and . There are three ways in which , and can be ordered relative to each other:

-

1.

lies between and , thus since .

-

2.

lies between and . But then, since there are no elements of between and , moves the average beyond away from towards , so and . But we know that since by the choice of the greedy algorithm and . Thus .

-

3.

, i.e., lies between and . But this case is impossible: compared to , averages over additional values that are closer to than , and is one of them. So must be on the same side as relative to , not the opposite side.

So is assured in all cases. Note in particular that if , , then

| (11) |

where is either ‘’ or ‘’. By inequality (11), . But this means that is not a solution: contradiction.

We have assumed that is nonempty; this is ensured because any solution must contain at least an index . Otherwise, we could replace a maximal index w.r.t. in by this and get, by (11), a larger value. This would be a contradiction with our assumption that is a solution. Note that this maximal index is also picked (first) by the algorithm. This completes the proof for the case . Let us now consider the general case where is unrestricted.

We reduce the general problem to the case that . Let us write to make the parameters and explicit when talking of . Let for one for which is maximal, and let for all other . We use the fact that, by the definition of ,

when contains such an element . Clearly, is an extremal element w.r.t. and has maximum distance from , so

By (10), must be in the optimal solution for . Also, and are maximized by the same index sets when is required. Thus,

Now observe that our previous proof for the case also works if one adds a constraint that one or more indices be part of the solution: If the algorithm computes these elements as part of its result , they are in . But this is what the algorithm does on input ; it chooses in its first step and then proceeds as if maximizing . Thus we have established the algorithm’s correctness. ∎

6 Application: Quantum tomography

Problem:

In quantum tomography (QT), we aim to learn a density matrix , which is Hermitian (i.e., ), positive semi-definite (i.e., ) and has and . The QT measurements are , where , and is zero-mean Gaussian. The operators ’s are the tensor product of the Pauli matrices (Liu, 2011).

Recently, (Liu, 2011) showed that almost all such tensor constructions of Pauli measurements satisfy the so-called rank- restricted isometry property (RIP) for all :

| (12) |

where is the nuclear norm (i.e., the sum of singular values), which reduces to since . This key observation enables us to leverage the recent theoretical and algorithmic advances in low-rank matrix recovery from a few affine measurements.

The standard matrix-completion based approach to recover from is the following convex relaxation:

| (13) |

This convex approach is both tractable and amenable to theoretical analysis (Gross et al., 2010; Liu, 2011). As a result, we can provably reduce the number of samples from to (Liu, 2011).

Unfortunately, this convex approach fails to account for the physical constraint . To overcome this difficulty, the relaxation parameter is tuned to obtain solutions with the desired rank followed by normalization to heuristically meet the trace constraint.

In this section, we demonstrate that one can do significantly better via the non-convex algorithm based on (3). A key ingredient then is the following projection:

| (14) |

for a given Hermitian matrix . Since the RIP assumption holds here, we can obtain rigorous guarantees based on a similar analysis to (Garg & Khandekar, 2009; Foucart, 2010; Meka et al., 2010).

To obtain the solution, we compute the eigenvalue decomposition and then use the unitary invariance of the problem to solve subject to and , and from form to obtain a solution. In fact, we can constrain to be diagonal, and thus reduce the matrix problem to the vector version for , where the projector in Problem 1 applies. This reduction follows from the well-known result:

Proposition 6.1 ((Mirsky, 1960)).

Let and . Let be the singular values of in descending order (similarly for ). Then,

Equation (14) has a solution if since the constraint set is non-empty and compact (Weierstrass’s theorem). As the vector reduction achieves the lower bound, it is an optimal projection.

Numerical experiments:

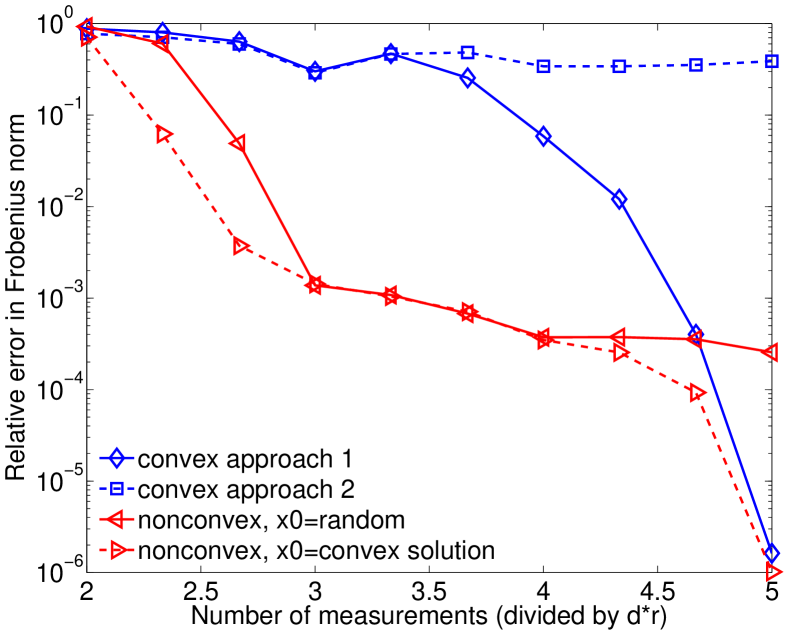

We numerically demonstrate that the ability to project onto trace and rank constraints jointly can radically improve recovery even with the simple gradient descent algorithm as in (3). We follow the same approach in (Gross et al., 2010): we generate random Pauli measurements and add white noise. The experiments that follow use a qubit system () with noise SNR at dB (so the absolute noise level changes depending on the number of measurements), and a qubit noiseless system.

The measurements are generated using a random real-valued matrix with rank , although the algorithms also work with complex-valued matrices. A rank real-valued matrix has degrees of freedom, hence we need at least number of measurements to recover from noiseless measurements (due to the null-space of the linear map). To test the various approaches, we vary the number of measurements between and . We assume is known, though other computational experience suggests that estimates of return good answers as well.

The convex problem (13) depends on a parameter . We solve the problem for different in a bracketing search until we find the first that provides a solution with numerical rank . Like (Flammia et al., 2012), we normalize the final estimate to ensure the trace is . Additionally, we test the following convex approach:

| (15) |

Compared to (13), no parameters are needed since we exploit prior knowledge of the trace, but there is no guarantee on the rank. Both convex approaches can be solved with proximal gradient descent; we use the TFOCS package (Becker et al., 2011) since it uses a sophisticated line search and Nesterov acceleration.

To illustrate the power of the combinatorial projections, we solve the following non-convex formulation:

| (16) |

Within the projected gradient algorithm (3), we use the GSSP algorithm as described above. The stepsize is where is the operator norm; we can also apply Nesterov acceleration to speed convergence, but we use (3) for simplicity. Due to the non-convexity, the algorithm depends on the starting value . We try two strategies: random initialization, and initializing with the solution from (15). Both initializations often lead to the same stationary point.

Figure 1 shows the relative error of the different approaches. All approaches do poorly when there are only measurements since this is near the noiseless information-theoretic limit. For higher numbers of measurements, the non-convex approach substantially outperforms both convex approaches. For measurements, it helps to start with the convex solution, but otherwise the two non-convex approaches are nearly identical.

Between the two convex solutions, (13) outperforms (15) since it tunes to achieve a rank solution. Neither convex approach is competitive with the non-convex approaches since they do not take advantage of the prior knowledge on trace and rank.

Figure 2 shows more results on a qubit problem without noise. Again, the non-convex approach gives better results, particularly when there are fewer measurements. As expected, both approaches approach perfect recovery as the number of measurements increases.

| Approach | mean time | standard deviation |

|---|---|---|

| convex | s. | s. |

| non-convex | s. | s. |

Here we highlight another key benefit of the non-convex approach: since the number of eigenvectors needed in the partial eigenvalue decomposition is at most , it is quite scalable. In general, the convex approach has intermediate iterates which require eigenvalue decompositions close to the full dimension, especially during the first few iterations. Table 1 shows average time per iteration for the convex and non-convex approach (overall time is more complicated, since the number of iterations depends on linesearch and other factors). Even using Matlab’s dense eigenvalue solver eig, the iterations of the non-convex approach are faster; problems that used an iterative Krylov subspace solver would show an even larger discrepancy.222Quantum state tomography does not easily benefit from iterative eigenvalue solvers, since the range of is not sparse.

7 Application: Measure learning

Problem:

We study the kernel density learning setting: Let be an -size corpus of -dimensional samples, drawn from an unknown probability density function (pdf) . Here, we will form an estimator , where is a Gaussian kernel with parameter . Let us choose to minimize the integrated squared error criterion: . As a result, we can introduce a density learning problem as estimating a weight vector . The objective can then be written as follows (Kim, 1995; Bunea et al., 2010)

| (17) |

where with , and

| (18) |

While the combination of the term and the non-negativity constraint induces some sparsity, it may not be enough. To avoid overfitting or obtain interpretable results, one might control the level of solution sparsity (Bunea et al., 2010). In this context, we extend (17) to include cardinality constraints, i.e. .

Numerical experiments:

We consider the following Gaussian mixture: , where and . A sample of points is drawn from . We compare the density estimation performance of: the Parzen method (Parzen, 1962), the quadratic programming formulation in (17), and our cardinality-constrained version of (17) using GSSP. While is constructed by kernels with various widths, we assume a constant width during the kernel estimation. In practice, the width is not known a priori but can be found using cross-validation techniques; for simplicity, we assume kernels with width .

Figure 3(left) depicts the true pdf and the estimated densities using the Parzen method and the quadratic programming approach. Moreover, the figure also includes a scaled plot of , indicating the height of the individual Gaussian mixtures. By default, the Parzen window method estimation interpolates Gaussian kernels with centers around the sampled points to compute the estimate ; unfortunately, neither the quadratic programming approach (as Figure 3 (middle-top) illustrates) nor the Parzen window estimator results are easily interpretable even though both approaches provide a good approximation of the true pdf.

Using our cardinality-constrained approach, we can significantly enhance the interpretability. This is because in the sparsity-constrained approach, we can control the number of estimated Gaussian components. Hence, if the model order is known a priori, the non-convex approach can be extremely useful.

To see this, we first show the coefficient profile of the sparsity based approach for in Figure 3 (middle-bottom). Figure 3 (right) shows the estimated pdf for along with the positions of weight coefficients obtained by our sparsity enforcing approach. Note that most of the weights obtained concentrate around the true means, fully exploiting our prior information about the ingredients of —this happens with rather high frequency in the experiments we conducted. Figure 4 illustrates further estimated pdf’s using our approach for various . Surprisingly, the resulting solutions are still approximately -sparse even if , as the over-estimated coefficients are extremely small, and hence the sparse estimator is reasonably robust to inaccurate estimates of .

8 Application: Portfolio optimization

Problem:

Given a sample covariance matrix and expected mean , the return-adjusted Markowitz mean-variance (MV) framework selects a portfolio such that where encodes the normalized capital constraint, and trades off risk and return (DeMiguel et al., 2009; Brodie et al., 2009). The solution is the distribution of investments over the available assets.

While such solutions construct portfolios from scratch, a more realistic scenario is to incrementally adjust an existing portfolio as the market changes. Due to costs per transaction, we can naturally introduce cardinality constraints. In mathematical terms, let be the current portfolio selection. Given , we seek to adjust the current selection such that . This leads to the following optimization problem:

where is the level of update, and controls the transactions costs. During an update, would keep the portfolio value constant while would increase it.

Numerical experiments:

To clearly highlight the impact of the non-convex projector, we create a synthetic portfolio update problem, where we know the solution. As in (Brodie et al., 2009), we cast this problem as a regression problem and synthetically generate where such that ( is chosen randomly), and for .

Since in general we do not expect RIP assumptions to hold in portfolio optimization, our goal here is to refine the sparse solution of a state-of-the-art convex solver via (3) in order to accommodate the strict sparsity and budget constraints. Hence, we first consider the basis pursuit criterion and solve it using SPGL1 (van den Berg & Friedlander, 2008):

| (19) |

The normalization by in the last equality gives the constraint matrix a better condition number, since otherwise it is too ill-conditioned for a first-order solver.

Almost none of the solutions to (19) return a -sparse solution. Hence, we initialize (3) with the SPGL1 solution to meet the constraints. The update step in (3) uses the GSHP algorithm.

Figure 5 shows the resulting relative errors . We see that not only does (3) return a -sparse solution, but that this solution is also closer to , particularly when the sample size is small. As the sample size increases, the knowledge that is -sparse makes up a smaller percentage of what we know about the signal, so the gap between (19) and (3) diminishes.

9 Conclusions

While non-convexity in learning algorithms is undesirable according to conventional wisdom, avoiding it might be difficult in many problems. In this setting, we show how to efficiently obtain exact sparse projections onto the positive simplex and its hyperplane extension. We empirically demonstrate that our projectors provide substantial accuracy benefits in quantum tomography from fewer measurements and enable us to exploit prior non-convex knowledge in density learning. Moreover, we also illustrate that we can refine the solution of well-established state-of-the-art convex sparse recovery algorithms to enforce non-convex constraints in sparse portfolio updates. The quantum tomography example in particular illustrates that the non-convex solutions can be extremely useful; here, the non-convexity appears milder, since a fixed-rank matrix still has extra degrees of freedom from the choice of its eigenvectors.

10 Acknowledgements

VC and AK’s work was supported in part by the European Commission under Grant MIRG-268398, ERC Future Proof and SNF 200021-132548. SRB is supported by the Fondation Sciences Mathématiques de Paris. CK’s research is funded by ERC ALGILE.

References

- Bahmani et al. (2011) Bahmani, S., Boufounos, P., and Raj, B. Greedy sparsity-constrained optimization. In Signals, Systems and Computers (ASILOMAR), 2011 Conference Record of the Forty Fifth Asilomar Conference on, pp. 1148–1152. IEEE, 2011.

- Becker et al. (2011) Becker, Stephen, Candès, Emmanuel, and Grant, Michael. Templates for convex cone problems with applications to sparse signal recovery. Mathematical Programming Computation, pp. 1–54, 2011. ISSN 1867-2949. URL http://dx.doi.org/10.1007/s12532-011-0029-5. 10.1007/s12532-011-0029-5.

- Brodie et al. (2009) Brodie, J., Daubechies, I., De Mol, C., Giannone, D., and Loris, I. Sparse and stable Markowitz portfolios. Proceedings of the National Academy of Sciences, 106(30):12267–12272, 2009.

- Bunea et al. (2010) Bunea, F., Tsybakov, A.B., Wegkamp, M.H., and Barbu, A. SPADES and mixture models. The Annals of Statistics, 38(4):2525–2558, 2010.

- Candès et al. (2006) Candès, E., Romberg, J., and Tao, T. Robust uncertainty principles: Exact signal reconstruction from highly incomplete frequency information. IEEE Trans. on Information Theory, 52(2):489 – 509, February 2006.

- DeMiguel et al. (2009) DeMiguel, V., Garlappi, L., Nogales, F.J., and Uppal, R. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55(5):798–812, 2009.

- Flammia et al. (2012) Flammia, S.T., Gross, D., Liu, Y.K., and Eisert, J. Quantum tomography via compressed sensing: error bounds, sample complexity and efficient estimators. New Journal of Physics, 14(9):095022, 2012. URL http://stacks.iop.org/1367-2630/14/i=9/a=095022.

- Foucart (2010) Foucart, S. Sparse recovery algorithms: sufficient conditions in terms of restricted isometry constants. Proceedings of the 13th International Conference on Approximation Theory, 2010.

- Garg & Khandekar (2009) Garg, R. and Khandekar, R. Gradient descent with sparsification: an iterative algorithm for sparse recovery with restricted isometry property. In ICML. ACM, 2009.

- Gross et al. (2010) Gross, D., Liu, Y.-K., Flammia, S. T., Becker, S., and Eisert, J. Quantum state tomography via compressed sensing. Phys. Rev. Lett., 105(15):150401, Oct 2010. doi: 10.1103/PhysRevLett.105.150401.

- Kim (1995) Kim, D. Least squares mixture decomposition estimation. PhD thesis, 1995.

- Kyrillidis & Cevher (2011) Kyrillidis, A. and Cevher, V. Recipes on hard thresholding methods. Dec. 2011.

- Kyrillidis & Cevher (2012) Kyrillidis, A. and Cevher, V. Combinatorial selection and least absolute shrinkage via the Clash algorithm. In IEEE International Symposium on Information Theory, July 2012.

- Liu (2011) Liu, Y.K. Universal low-rank matrix recovery from Pauli measurements. In NIPS, pp. 1638–1646, 2011.

- Meka et al. (2010) Meka, Raghu, Jain, Prateek, and Dhillon, Inderjit S. Guaranteed rank minimization via singular value projection. In NIPS Workshop on Discrete Optimization in Machine Learning, 2010.

- Mirsky (1960) Mirsky, L. Symmetric gauge functions and unitarily invariant norms. The quarterly journal of mathematics, 11(1):50–59, 1960.

- Nemhauser & Wolsey (1988) Nemhauser, G.L. and Wolsey, L.A. Integer and combinatorial optimization, volume 18. Wiley New York, 1988.

- Parzen (1962) Parzen, E. On estimation of a probability density function and mode. The annals of mathematical statistics, 33(3):1065–1076, 1962.

- Pilanci et al. (2012) Pilanci, M., El Ghaoui, L., and Chandrasekaran, V. Recovery of sparse probability measures via convex programming. In Advances in Neural Information Processing Systems 25, pp. 2429–2437, 2012.

- van den Berg & Friedlander (2008) van den Berg, E. and Friedlander, M. P. Probing the Pareto frontier for basis pursuit solutions. SIAM J. Sci. Comput., 31(2):890–912, 2008.