copyrightbox

Forecastable Component Analysis (ForeCA)111Appears in Proceedings of ICML 2013.

Abstract

I introduce Forecastable Component Analysis (ForeCA), a novel dimension reduction technique for temporally dependent signals. Based on a new forecastability measure, ForeCA finds an optimal transformation to separate a multivariate time series into a forecastable and an orthogonal white noise space. I present a converging algorithm with a fast eigenvector solution. Applications to financial and macro-economic time series show that ForeCA can successfully discover informative structure, which can be used for forecasting as well as classification.

The R package ForeCA accompanies this work and is publicly available on CRAN.

1 Introduction

With the rise of high-dimensional datasets it has become important to perform dimension reduction (DR) to a lower dimensional representation of the data. For simplicity we consider linear transformations , which map an -dimensional to a dimensional . Typically, the transformed data should be somewhat “interesting”; there is no point in transforming to an arbitrary that is less useful, meaningful, etc. Let measure “interestingness” of . DR can then be set up as an optimization problem

| (1) | ||||

| subject to | (2) |

where (2) is a common DR constraint, which makes orthogonal (uncorrelated) to previously obtained signals.

For example, principal component analysis (PCA) keeps large variance signals (Jolliffe, 2002) – in (1); independent component analysis (ICA) recovers statistically independent signals (Hyvärinen and Oja, 2000); slow feature analysis (SFA) (Wiskott and Sejnowski, 2002) finds “slow” signals and is equivalent to maximizing the lag autocorrelation coefficient.

DR techniques are often applied to multivariate time series , hoping that forecasting on the lower-dimensional space is more accurate, simpler, more efficient, etc. Standard DR techniques such as PCA or ICA, however, do not explicitly address forecastability of the sources. For example, just because a signal has high variance does not mean it is easy to forecast.

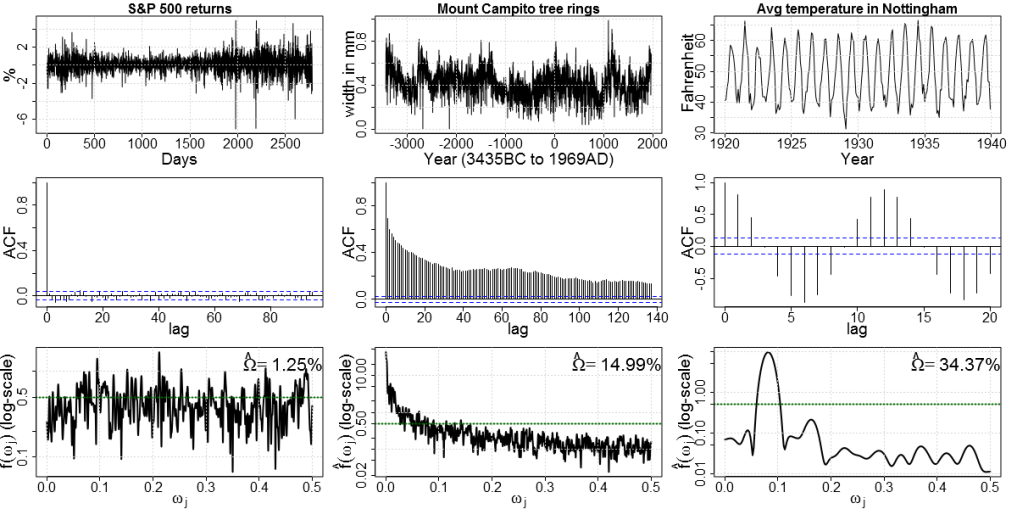

Thus let’s define interesting as being predictable. Forecasting is not only good for its own sake (finance, economics), but even when future values are not immediately interesting, signals that do have predictive power exhibit non-trivial structure by definition – and are thus easier to interpret. For example, the time series in Fig. 1 are ordered from least (S&P500 daily returns) to most forecastable (monthly temperature in Nottingham) according to the ForeCA forecastability measure I propose in Definition 3.1 below. And indeed moving from left to right they exhibit more structure.

The main contributions of this work are i) a model-free, comparable measure of forecastability for (stationary) time series (Section 3), ii) a novel data-driven DR technique, ForeCA, that finds forecastable signals, iii) an iterative algorithm that provably converges to (local) optima using fast eigenvector solutions (Section 4), and iv) applications showing that ForeCA outperforms traditional DR techniques in finding low-dimensional, forecastable subspaces, and that it can also be used for time series classification (Section 5). Related work will be reviewed in Section 6.

All computations and simulations were done in R (R Development Core Team, 2010).

2 Time Series Preliminaries

Let be a univariate, second-order stationary time series with mean , variance , and autocovariance function (ACVF)

| (3) |

The ACVF for univariate processes is symmetric in , . Let be the autocorrelation function (ACF). A large means that the process time steps ago is highly correlated with the present . The sample ACFs in Fig. 1 show that, e.g., S&P 500 daily returns are uncorrelated with their own past (stock market efficiency); yearly tree ring growth is highly correlated over time with significant lags even for years; and intuitively temperature in month is highly correlated with the temperature (cold warm) and (cold cold; warm warm) months ago (or in the future).

The building block of time series models is white noise , which has zero mean, finite variance, and is uncorrelated over time: iff222Iff will be used as an abbreviation for if and only if. i) , ii) , and iii) if . Only if is a Gaussian process, then it is also independent.

For multivariate second-order stationary with mean333Without loss of generality (WLOG) assume . and covariance matrix the ACVF

| (4) |

is a matrix-valued function of . In particular, . The diagonal of contains the ACVF of each ; the off-diagonal element is the cross-covariance between the th and th series at lag :

| (5) |

Contrary to , is not symmetric, but

| (6) |

2.1 Spectrum and Spectral Density

The spectrum of a univariate stationary process can be defined as the Fourier transform of its ACVF,

| (7) |

where is the imaginary unit. Since is symmetric, the spectrum is a real-valued, non-negative function, . For white noise all if , thus is constant for all . When for the spectrum has peaks at the corresponding frequencies. For example, the spectral density of monthly temperature series (right in Fig. 1) has large peaks at and , which represent the half- and one-year cycle.444Frequencies are often scaled by , . This does not change results qualitatively, but simplifies interpretation since the corresponding cycle length equals .

Vice versa, the ACVF can be recovered from the spectrum using the inverse Fourier transform

| (8) |

In particular, for . Let

| (9) |

be the spectral density of . As and , the spectral density can be interpreted as a probability density function (pdf) of an (unobserved) random variable (RV) that “lives” on the unit circle. For white noise , which represents the uniform distribution .

Remark 2.1 (Spectrum and spectral density).

In the time series literature “spectrum” and “spectral density” are often used interchangeably. Here I reserve “spectral density” for in (9), as it integrates to one such as standard probability density functions.

3 Measuring Forecastability

Forecasting is inherently tied to the time domain. Yet, since Eqs. (7) & (8) provide a one-to-one mapping between the time and frequency domain, we can use frequency domain properties to measure forecastability.

The intuition for the proposed measure of forecastability is as follows. Consider

| (10) | ||||

One can show that (Gibson, 1994).

If we have to predict the future of , then uncertainty about , , is only manifested in uncertainty about , since is a deterministic function of : less uncertainty about means less uncertainty about . We can measure this uncertainty using the Shannon entropy of (Shannon, 1948). It is thus natural to measure uncertainty about the future as (differential) entropy of ,

| (11) |

where is the logarithm base.

On a finite support the maximum entropy occurs for the uniform distribution ; thus a flat spectrum should indicate the least predictable sequence. And indeed, a flat spectrum corresponds to white noise, which is unpredictable by definition (using linear predictors). Consequently, for any stationary

with equality iff is white noise.

Definition 3.1 (Forecastability of a stationary process).

For a second-order stationary process , let

| (12) | ||||

be the forecastability of .

Contrary to other measures in the signal processing and time series literature, does not require actual forecasts, but is a characteristic of the process . It is therefore not biased to a particular – perhaps sub-optimal – model, forecast horizon, or loss function; as used in e.g., Stone (2001); Box and Tiao (1977).

Properties 3.2.

satisfies:

-

a)

iff is white noise.

-

b)

invariant to scaling and shifting:

-

c)

max sub-additivity for uncorrelated processes:

(13) if ; equality iff .

The three series in Fig. 1 are ordered (left to right) by increasing forecastability and indeed larger correspond to intuitively more predictable real-world events: stock returns are in general not predictable; average monthly temperature is.

We can thus use (12) to guide the search for optimal that make as forecastable as possible.

3.1 Plug-in Estimator for

To estimate , we first estimate , normalize it, and then plug it in (11).

An unbiased estimator of is the periodogram

| (14) |

where , are the (scaled) Fourier frequencies, and is a sample of . It is well known that (14) is not a good estimate (e.g., periodograms are not consistent). In the numerical examples we therefore use weighted overlapping segment averaging (WOSA) (Nuttal and Carter, 1982) from the R package sapa: SDF(y, ’’wosa’’).

The bottom row of Figure 1 shows the normalized along with the plug-in estimate

| (15) |

Remark 3.3.

Typically, to estimate for (here: ) the sample average is solely over without multiplicative terms. This however assumes that each is sampled from (and thus by the strong law of large numbers). While this is true in a standard sampling framework, here the “data” are the Fourier frequencies and the fast Fourier transform (FFT) samples them uniformly (and deterministically) from and not according to the “true” spectral density .555Advances in “compressed sensing” (Jacques and Vandergheynst, 2010) might improve estimates; see also “non-uniform FFT” (Fessler and Sutton, 2003).

Eq. (15) can be improved by a better spectral density (Fryzlewicz et al., 2008; Trobs and Heinzel, 2006; Lees and Park, 1995) and entropy estimation (Paninski, 2003). Future research can also address direct estimation of (11) – as is common for classic entropy estimates (Sricharan et al., 2011; Stowell and Plumbley, 2009). However, since neither spectrum nor entropy estimation are the primary focus of this work, we use standard estimators for and then the plug-in estimator of (15).

It must be noted though that in (15) is based on discrete rather than differential entropy. It still has the intuitive property that white noise has zero estimated forecastability, but now ; iff the sample is a perfect sinusoid. Applications show that (15) yields reasonable estimates and we do not expect the results to change qualitatively for other estimators. We leave differential entropy estimates of to future work.

Notice that relies on Gaussianity as only then captures all the temporal dependence structure of . While time series are often non-Gaussian, is a computationally and algebraically manageable forecastability measure – similarly to the importance of variance in PCA for iid data, even though they are rarely Gaussian.

4 ForeCA: Maximizing Forecastability

Recall from Eq. (1) that we want to find a linear combination of a multivariate that makes as forecastable as possible. Based on the forecastability measure in Section 3, we can now formally define the ForeCA optimization problem:

| (16) | ||||

| subject to | (17) |

where (17) must hold since (11) uses the spectral density of , i.e. we need .

Property 3.2c seems to let (16) only have a trivial boundary solution. However, it is intuitively clear that combining uncorrelated series makes forecasting (in general) more difficult, e.g., signal noise. But if for some then combining them can make it simpler: for some it holds .

To optimize the right hand side of (16) we need to evaluate for various and do this efficiently. We now show how to obtain by simple matrix-vector multiplication from .

4.1 Spectrum of Multivariate Time Series and Their Linear Combinations

For multivariate the spectrum equals

| (18) |

Contrary to the univariate case, (18) is in general complex-valued. Yet, since , is Hermitian for every , , where is the complex conjugate of (Brockwell and Davis, 1991, p. 436).

For dimension reduction we consider linear combinations , . By assumption and . In particular, . The spectrum of can be quickly computed via and consequently

| (19) |

Since for every , for all ; thus is positive semi-definite.

4.2 Solving the Optimization Problem

Since is invariant to shift and scale (Property 3.2b), we shall not only assume zero mean, but also contemporaneously uncorrelated observed signals with unit variance in each component. WLOG consider ; thus . Given for , the transformation for becomes . Problem (16) is then equivalent to

| (20) |

where

| (21) |

is the spectral entropy (Eq. (11)) of as a function of . We use for better readability.

In practice we approximate (21) with and thus obtain666We use ‘‘wosa’’ estimates (sapa R package). However, any other estimate of can be used.

| (22) |

Here

| (23) |

is the discretized version of (20), where . Notice that varies with while is fixed over all frequencies, which makes it difficult to obtain an analytic, closed-form solution. However, (22) can be solved iteratively borrowing ideas from the expectation maximization (EM) algorithm (Dempster et al., 1977).

4.2.1 A Convergent EM-like Algorithm

For every , , has the form of a mixture model with weights and “log-likelihood” . Since , is indeed a discrete probability distribution over .

Just as in an EM algorithm, the objective can be optimized iteratively by first fixing in , and then minimizing the quadratic form

| (24) |

where .

Proposition 4.1.

is positive semi-definite.

Thus (24) can be solved analytically by the last eigenvector of – automatically guaranteeing . The procedure iterates until for some tolerance level . For initialization we sample from an -dimensional uniform hyper-cube, , and normalize to .

Theorem 4.2 (Convergence).

The sequence obtained via (24) converges to a local minimum , where and is the smallest eigenvalue of .

Corollary 4.3.

The transformed data satisfies

| (25) |

Proof of Theorem 4.2.

The entropy of a RV taking values in a finite alphabet is bounded: for all . For convergence it remains to be shown that with equality iff . First,

| (26) |

since is the last eigenvector of . Second,

| (27) | ||||

where (27) holds as for any . ∎

To lower the chance of landing in local optima we repeat (24) for several random starting positions and then select the best solution.

4.3 Obtaining a -dimensional Subspace

To obtain all loadings that give uncorrelated series , we iteratively (starting at ) i) compute , ii) project onto the null space of , iii) apply the EM-type algorithm on to obtain , and finally iv) transform back to loadings of .

Doing this for gives loadings . Loadings for are given by .

5 Applications

Here we demonstrate the usefulness of ForeCA to find informative, forecastable signals, but also as a tool for time series classification.

5.1 Improving Portfolio Forecasts

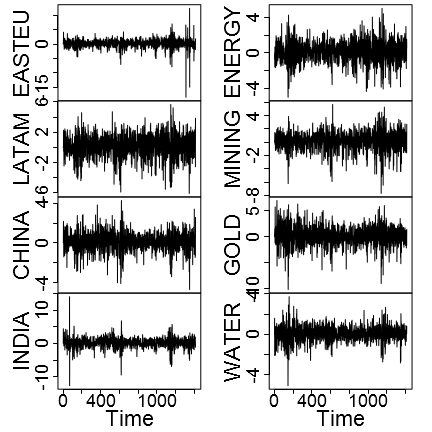

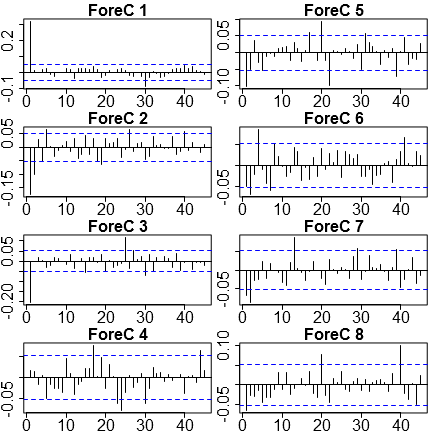

Figure 2(a) shows daily returns of eight equity funds from to (). In the financial context finding forecastable series is an important goal by itself, not just for structure discovery. In particular, we can interpret a linear combination as a portfolio of stocks. The with the highest gives the most forecastable portfolio.

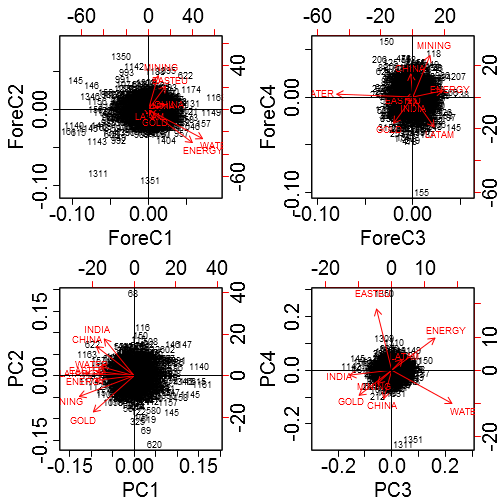

Figure 2(b) shows a bi-plot for PCA and ForeCA for and . As PC weighs all funds almost equally, it represents the average market movement; the second component contrasts Gold & Mining with the rest and we can therefore label PC as the “commodity” index. The third and fourth PC indicate energy/infrastructure and geographic regions.

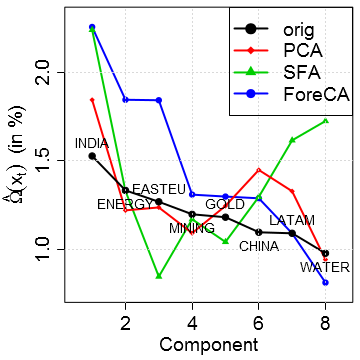

However, even though PC is also the most predictable PC, it has only a slightly larger than the most forecastable fund, India (Fig. 2(c)). On the other hand, combining Water (weight ) with Energy () is almost twice as forecastable as India (weights are from ForeC in Fig. 2(b)). ForeC also has high forecastability by selling Energy & Water ( & ) and buying Mining & Eastern Europe ( & ). The third and fourth ForeCs seem to be hedging strategies (ForeC : Water vs. Energy; ForeC : Latin America & Gold vs. China & Mining).

As financial data only has very small autocorrelation – and usually at lag , if any –, SFA and ForeCA yield overall very similar results, except for a “wrong” ranking by SFA (Fig. 2(c)): SF is the fastest feature (large, but negative lag autocorrelation), yet it is the second most forecastable component. While it is true that white noise is slower than an auto-regressive process of order () with negative autocorrelation, the latter is still more forecastable. Since we want to reveal intertemporal structure, white noise must be ranked lowest; and ForeCA indeed does so (Fig. 2(d)).

ForeC and detect the day lag (one trading month), but correlations are too low to achieve much higher forecastability than – simpler and faster – SFA.

In the next example I study quarterly income data, where ForeCA can leverage its nonparametric power and detect important dependencies at various frequencies automatically from the data.

5.2 Classification of US State Economies

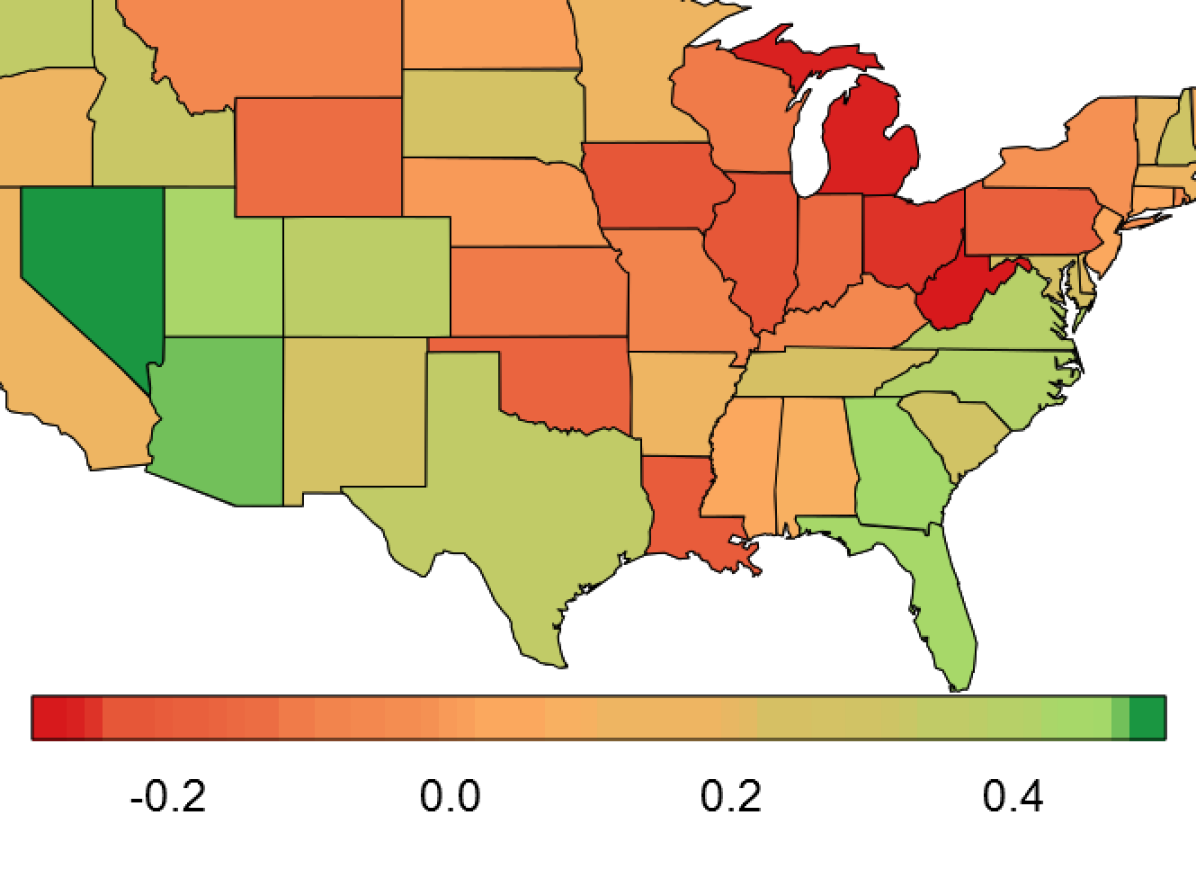

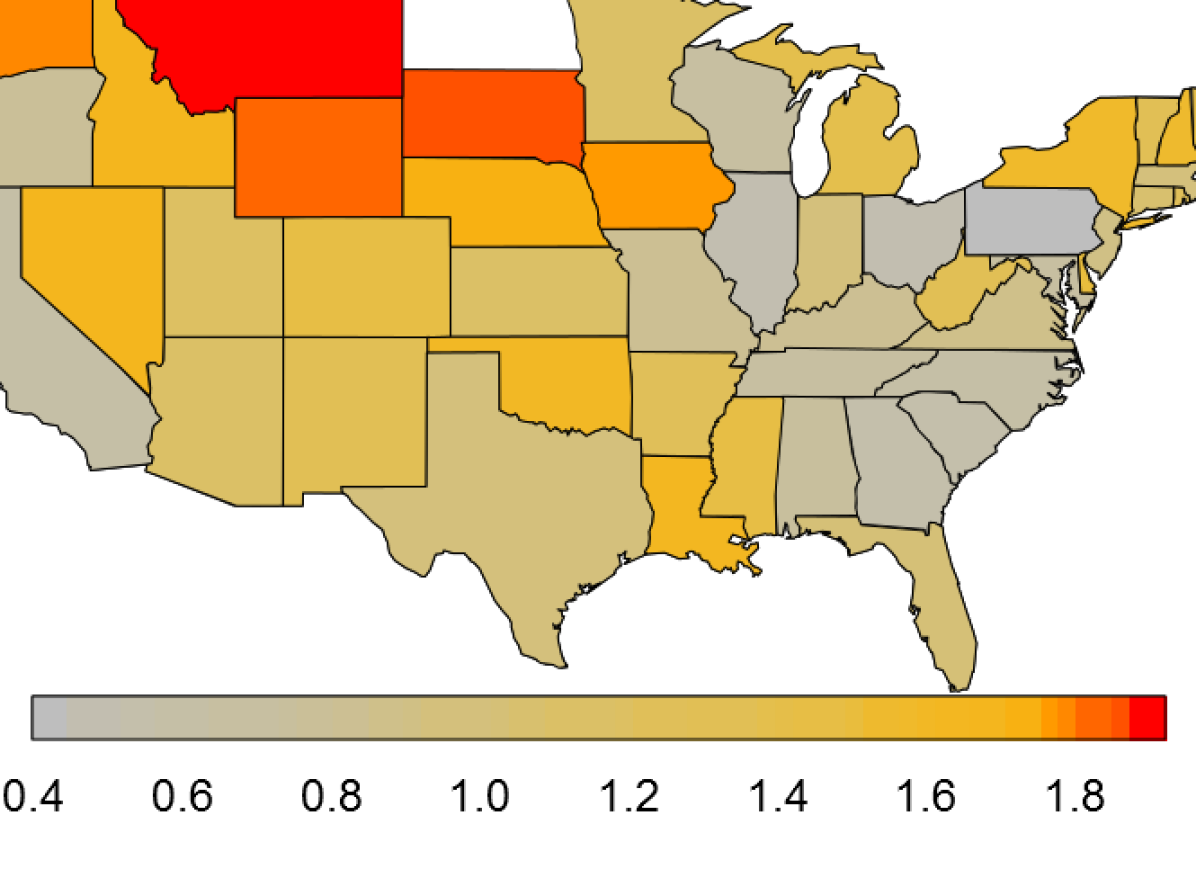

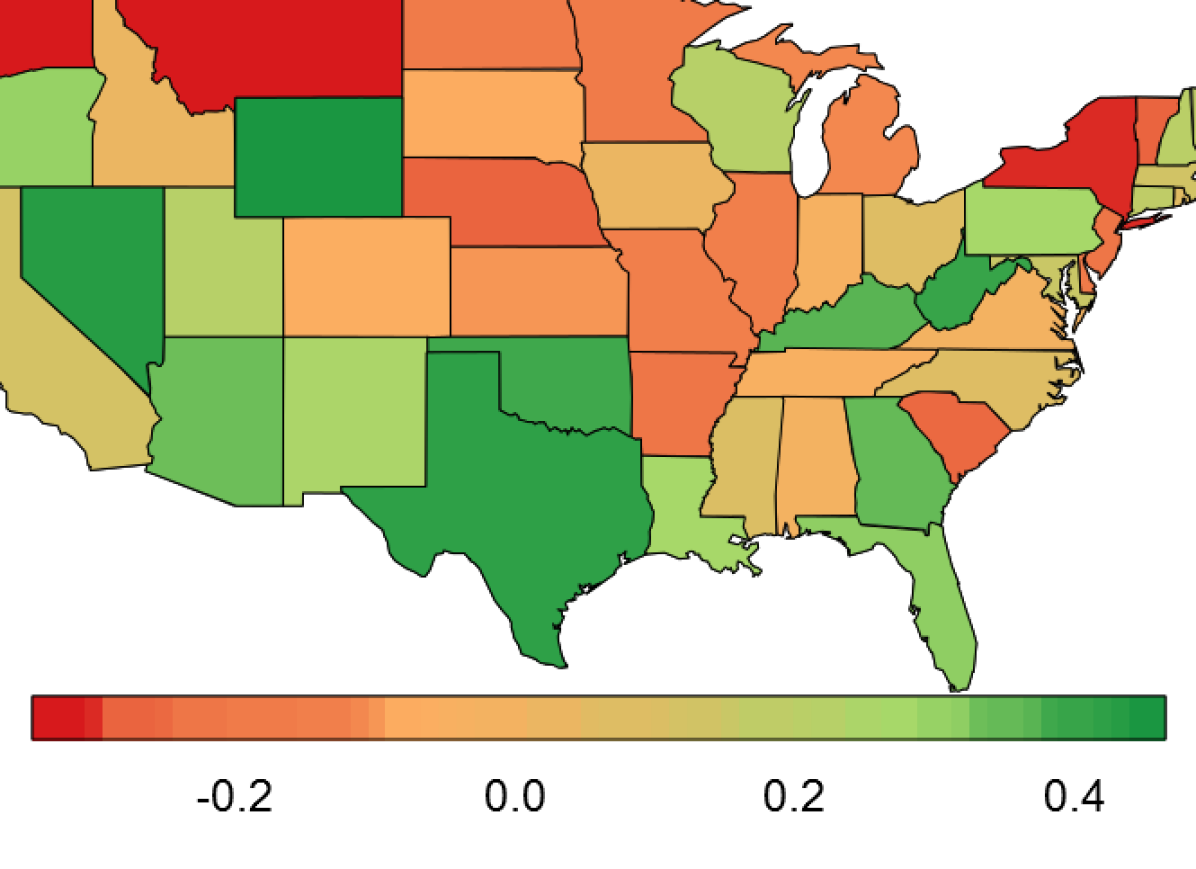

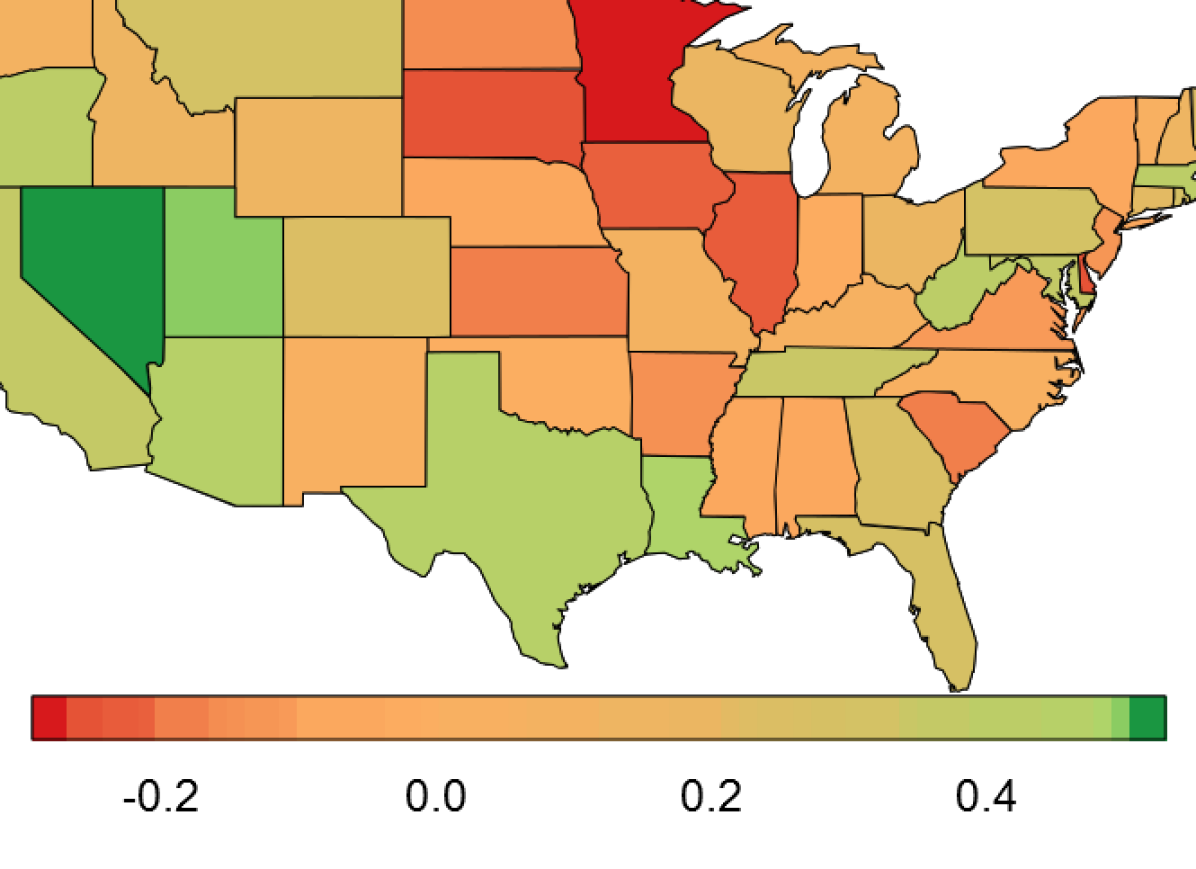

I consider quarterly per-capita income growth rates of the “lower 48” from to (last years)

where is the annual growth rate of region .777Publicly available at www.bea.gov/itable. Interested in finding similar state economies within the US, we subtract the US baseline. Clustering states with similar economic dynamics can help to decide where to provide support when facing difficult economic times. For example, if certain states do not show any important dynamics on a - year scale – also known as the “business cycle” (Hughes Hallett and Richter, 2008) – then it might be better to support states that are affected by these global economy swings.

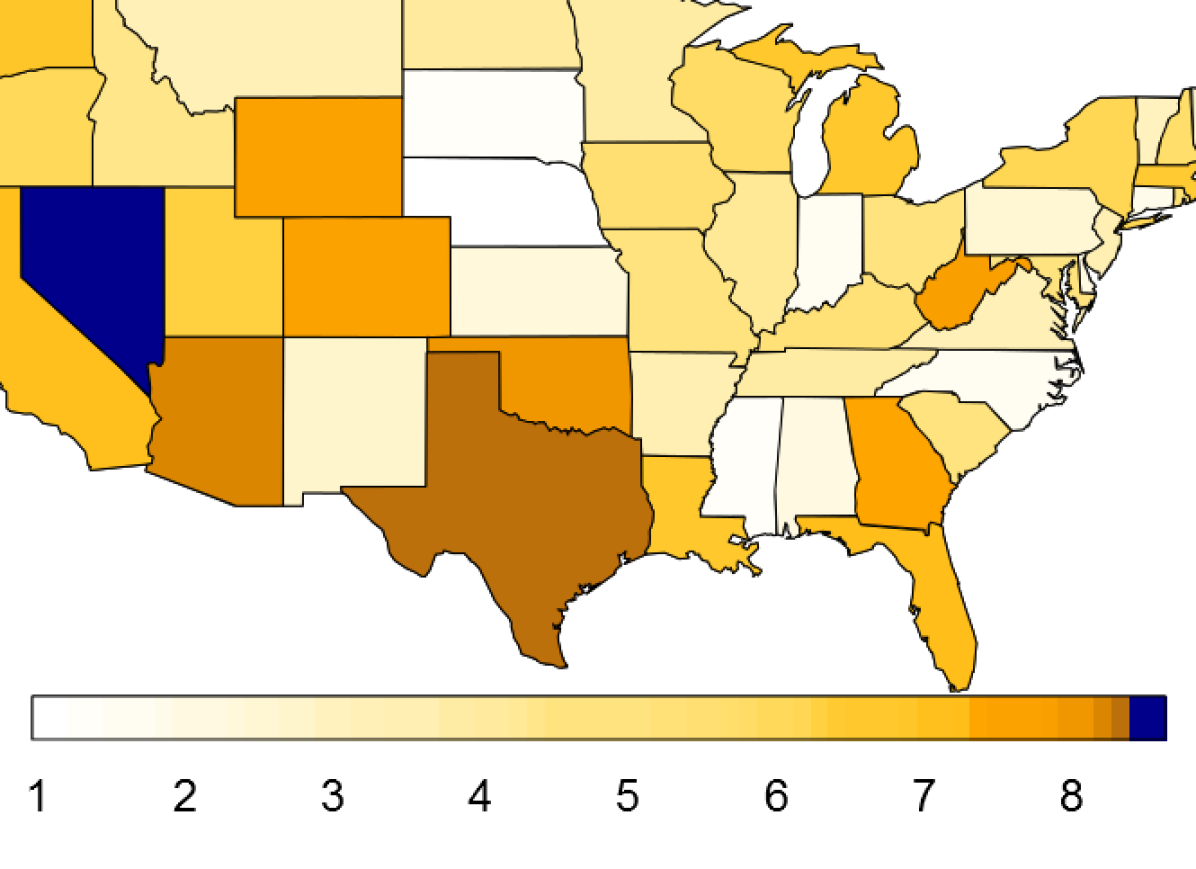

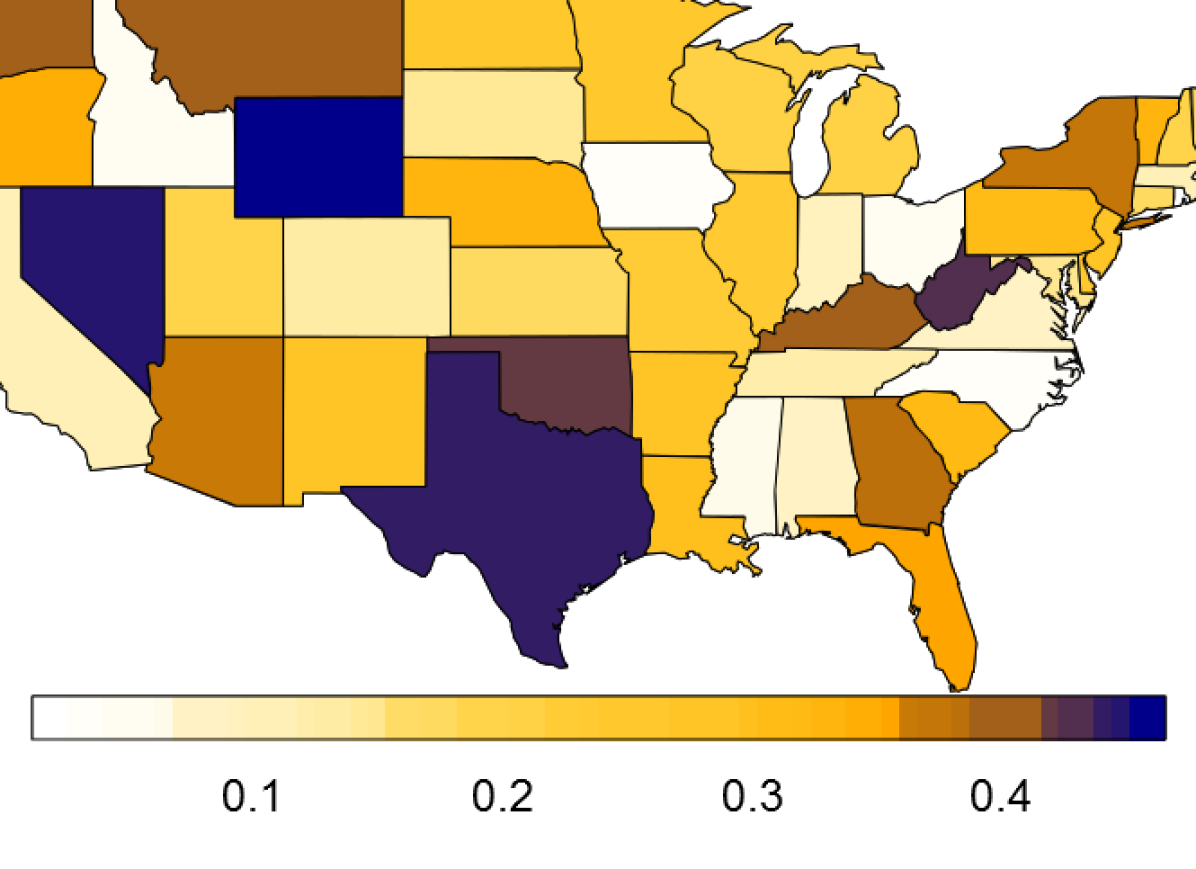

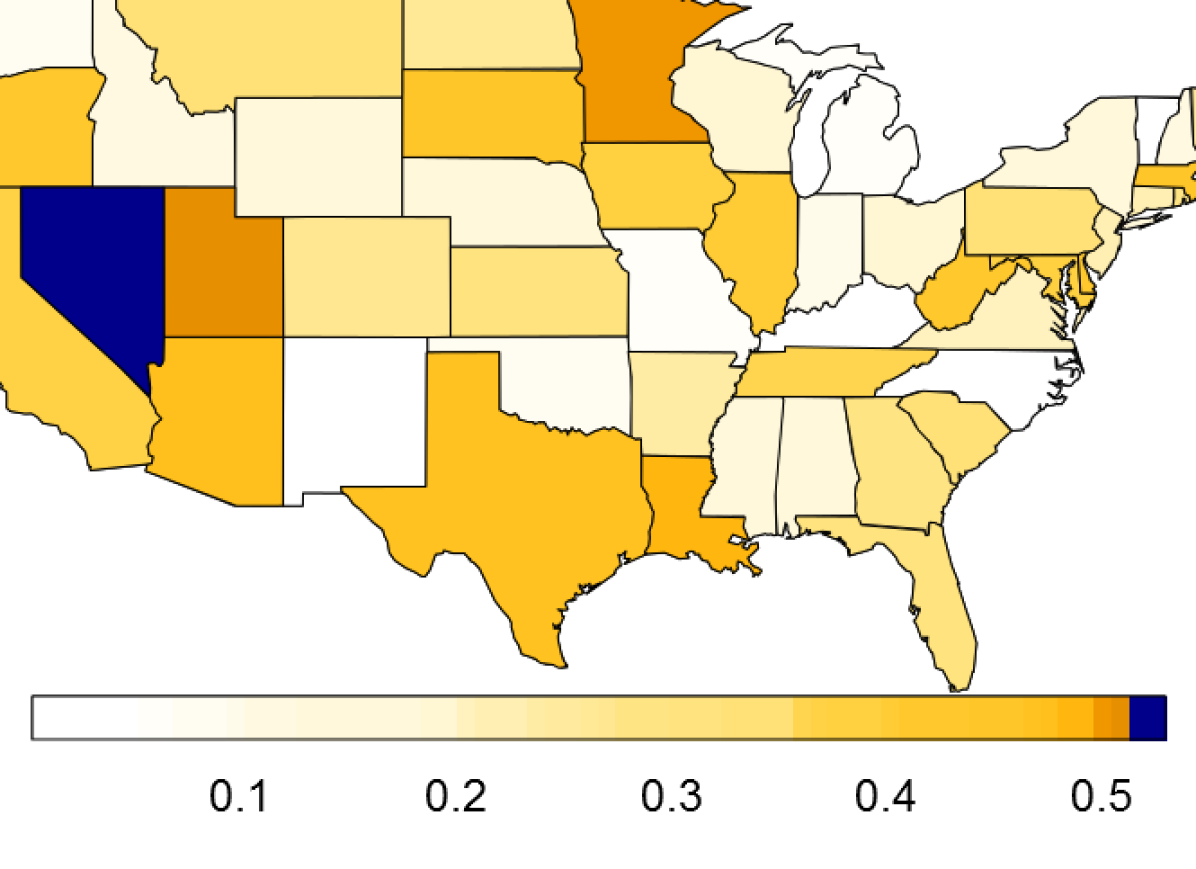

The first row of Fig. 3 displays basic summary statistics: sample average, standard deviation, and first and fourth order autocorrelation. The second row give statistics related to forecastability: Fig. 3(e) shows based on the spectra in Fig. 3(f); Fig. 3(g) shows the absolute lag correlation (analogously for lag in Fig. 3(h)), since two s with a lag coefficient are equivalent in terms of forecasting (compare to SFA ranking in the portfolio example).

The spectral densities of Nevada and Nebraska illustrate the intuitive derivation of from Eq. (10): for Nebraska all frequencies are equally important and it is thus difficult to forecast any better than the sample mean; contrary, Nevada’s income growth rates are mainly driven by a yearly cycle () and low frequencies, thus Nevada is much easier to forecast.

A similar dataset (but annually and for different years) has been analyzed in Dhiral et al. (2001), who fit models to the non-adjusted growth rates for pre-selected states, and then cluster them in the model space. Although they obtain interpretable results, it is unlikely that US state economies only differ in their lag coefficient. In particular, simple models cannot capture the business cycle, which is clearly visible in Fig. 3(f) (even for the adjusted rates).

Similarly, as SFA maximizes lag correlation, it misses the quarterly cycle. ForeCA does not face this model selection bias, but can find forecastability across all frequencies. In particular, only ForeC detects interesting high frequency signals (Fig. 4(b)). The most forecastable PCs are PC , , and ; interestingly PC is least important for forecasting among all PCs. Also note that ForeCs are more interpretable than SFs or PCs (Figs. 4(b) - 4(d)). Particularly, ForeC shows a clear year period (generation cycle), whereas PC looks somewhat arbitrary. Yet, the associated loadings in Fig. 4(a) are quite similar.

6 Related Work

Using predictability to separate signals is not new.

In the classic time series literature Box and Tiao (1977) introduced canonical analysis and measure predictive power by the residual variance of fitting vector auto-regression (VAR) models. Recently Matteson and Tsay (2011) propose another DR technique that blends PCA and ICA by separating signals to the extent of fourth moments (but not higher).

Stone (2001) use predictability as a contrast function for blind source separation (BSS). While their approach is similar to ours, it relies on subjective measures of “short” and “long” term moving averages, which are then used to produce actual forecasts.

Much work in BSS (Gomez-Herrero et al., 2010; Li and Adali, 2010), especially ICA, focuses on minimizing entropy rate. The entropy rate of a Gaussian process is related to the spectrum via (Cover and Thomas, 1991, p. 417)

| (28) |

However, these approaches require VAR model fits and/or numerical optimization.

On the contrary, the ForeCA measure is based on information-theoretic uncertainty and is an inherent property of the stochastic process . We believe that this makes a more principled measure of forecastability than model-dependent measures. Furthermore, it can be estimated quickly using data-driven, nonparametric techniques.

It is important to point out that spectral entropy, i.e., differential entropy of (11), is neither equal nor proportional to the entropy rate in (28). For particular processes they coincide (e.g., for an ; Gibson (1994)), but in general they don’t. They measure different properties of the signal. Thus ICA algorithms based on entropy rate minimization do not yield the same results as ForeCA. In fact, the ForeCA measure can be used to rank ICs by decreasing forecastability.

Cardoso (2004) gives an excellent account of the intertwined relations between Gaussianity, autocorrelation, and dependence in multivariate time series and their effect on objective functions for BSS. Exactly because of this tangle, we only consider frequency properties of the signal and not entropy rate – since for forecasting the distribution itself is of minor importance compared to the temporal dependence.

7 Discussion

I introduce Forecastable Component Analysis (ForeCA), a new dimension reduction technique for multivariate time series. Contrary to other popular methods – such as PCA or ICA – ForeCA takes temporal dependence into account and actively searches for the most forecastable subspace. ForeCA minimizes the entropy of the spectral density: lower entropy implies a more forecastable signal. The optimization problem has an iterative, yet fast analytic solution, and provably leads to a (local) optimum.

While SFA is a good approximation (maximizing lag correlation), real world signals often have more complex correlation structure. The here proposed ForeCA can automatically detect arbitrary autocorrelation structure using nonparametric estimators. Applications to financial and macro-economic data demonstrate that ForeCA is better than PCA and SFA at finding the most predictable signals, and can also be used for time series classifications.

References

- Box and Tiao (1977) Box, G. E. P. and G. C. Tiao (1977). A canonical analysis of multiple time series. Biometrika 64(2), 355–365.

- Brockwell and Davis (1991) Brockwell, P. J. and R. A. Davis (1991). Time Series: Theory and Methods (2 ed.). New York, NY: Springer Series in Statistics.

- Cardoso (2004) Cardoso, J.-F. (2004). Dependence, correlation and gaussianity in independent component analysis. J. Mach. Learn. Res. 4(7-8), 1177–1203.

- Cover and Thomas (1991) Cover, T. M. and J. Thomas (1991). Elements of Information Theory. Wiley.

- Dempster et al. (1977) Dempster, A. P., N. M. Laird, and D. B. Rubin (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society Series B Methodological 39(1), 1–38.

- Dhiral et al. (2001) Dhiral, K. K., K. Kalpakis, D. Gada, and V. Puttagunta (2001). Distance Measures for Effective Clustering of ARIMA Time-Series. In Proceedings of the 2001 IEEE International Conference on Data Mining, pp. 273–280.

- Fessler and Sutton (2003) Fessler, J. A. and B. P. Sutton (2003). Nonuniform fast fourier transforms using min-max interpolation. IEEE Trans. Signal Process 51, 560–574.

- Fryzlewicz et al. (2008) Fryzlewicz, P., G. P. Nason, and R. von Sachs (2008). A wavelet-Fisz approach to spectrum estimation. Journal of Time Series Analysis 29(5), 868–880.

- Gibson (1994) Gibson, J. (1994). What is the interpretation of spectral entropy? In Proceedings of IEEE International Symposium on Information Theory, 1994, pp. 440.

- Gomez-Herrero et al. (2010) Gomez-Herrero, G., K. Rutanen, and K. Egiazarian (2010). Blind source separation by entropy rate minimization. Signal Processing Letters, IEEE 17(2), 153 –156.

- Hughes Hallett and Richter (2008) Hughes Hallett, A. and C. Richter (2008). Have the Eurozone economies converged on a common European cycle? International Economics and Economic Policy 5, 71–101.

- Hyvärinen and Oja (2000) Hyvärinen, A. and E. Oja (2000). Independent Component Analysis: Algorithms and Applications. Neural Networks 13, 411–430.

- Jacques and Vandergheynst (2010) Jacques, L. and P. Vandergheynst (2010). Compressed Sensing: “When sparsity meets sampling”, Chapter 23, pp. 507–528. Wiley-Blackwell.

- Jolliffe (2002) Jolliffe, I. T. (2002). Principal Component Analysis (2 ed.). New York, NY: Springer.

- Lees and Park (1995) Lees, J. M. and J. Park (1995). Multiple-Taper Spectral-Analysis - A Stand-Alone C-Subroutine. Computers & Geosciences 21(2), 199–236.

- Li and Adali (2010) Li, X.-L. and T. Adali (2010). Blind spatiotemporal separation of second and/or higher-order correlated sources by entropy rate minimization. In Acoustics Speech and Signal Processing (ICASSP), 2010 IEEE International Conference on, pp. 1934 –1937.

- Matteson and Tsay (2011) Matteson, D. S. and R. S. Tsay (2011). Dynamic orthogonal components for multivariate time series. Journal of the American Statistical Association 106(496), 1450–1463.

- Nuttal and Carter (1982) Nuttal, A. H. and G. C. Carter (1982). Spectral Estimation and Lag Using Combined Time Weighting. In Proceedings of IEEE, Volume 70, pp. 1111–1125.

- Paninski (2003) Paninski, L. (2003). Estimation of entropy and mutual information. Neural Comput. 15(6), 1191–1253.

- R Development Core Team (2010) R Development Core Team (2010). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing. ISBN 3-900051-07-0.

- Shannon (1948) Shannon, C. E. (1948). A Mathematical Theory of Communication. Bell System Technical Journal 27, 379–23, 623–656.

- Sricharan et al. (2011) Sricharan, K., R. Raich, and A. Hero (2011). K-nearest neighbor estimation of entropies with confidence. In Information Theory Proceedings (ISIT), 2011 IEEE International Symposiumon, pp. 1205 –1209.

- Stone (2001) Stone, J. V. (2001). Blind source separation using temporal predictability. Neural Comput. 13(7), 1559–1574.

- Stowell and Plumbley (2009) Stowell, D. and M. D. Plumbley (2009). Fast Multidimensional Entropy Estimation by k-d Partitioning. IEEE Signal Processing Letters 16, 537–540.

- Trobs and Heinzel (2006) Trobs, M. and G. Heinzel (2006). Improved spectrum estimation from digitized time series on a logarithmic frequency axis. Measurement 39(2), 120–129.

- Wiskott and Sejnowski (2002) Wiskott, L. and T. J. Sejnowski (2002). Slow Feature Analysis: Unsupervised Learning of Invariances. Neural computation 14(4), 715–770.

APPENDIX – SUPPLEMENTARY MATERIAL

Appendix A Proofs

Proof of Properties 3.2c (Max-subadditivity).

Consider the linear combination of two stationary processes and ,

It holds . If and are uncorrelated for all then (if and are both unit-variance processes). To have a unit-variance sum we need :

The spectrum of equals (if they are uncorrelated)

| (29) |

It therefore holds

where the last inequality follows by (29). Plugging in gives

which completes the proof.

∎

Proof of Proposition 4.1.

For every ,

∎