∎

Tel.: +380-44-259-03-92

Fax: +380-44-259-03-92

22email: shklyar@univ.kiev.ua 33institutetext: G. Shevchenko 44institutetext: Kyiv National Taras Shevchenko University, Faculty of Mechanics and Mathematics, Volodymyrska 64, 01601 Kyiv, Ukraine

Tel.: +380-44-259-03-92

Fax: +380-44-259-03-92

44email: zhora@univ.kiev.ua 55institutetext: Yu. Mishura 66institutetext: Kyiv National Taras Shevchenko University, Faculty of Mechanics and Mathematics, Volodymyrska 64, 01601 Kyiv, Ukraine

Tel.: +380-44-259-03-92

Fax: +380-44-259-03-92

66email: myus@univ.kiev.ua 77institutetext: V. Doroshenko 88institutetext: Kyiv National Taras Shevchenko University, Faculty of Mechanics and Mathematics, Volodymyrska 64, 01601 Kyiv, Ukraine

Tel.: +380-44-259-03-92

Fax: +380-44-259-03-92

88email: vadym.doroshenko@univ.kiev.ua 99institutetext: O. Banna 1010institutetext: Kyiv National Taras Shevchenko University, Economics Faculty, Volodymyrska 64, 01601 Kyiv, Ukraine

Tel.: +380-44-259-03-92

Fax: +380-44-259-03-92

1010email: okskot@ukr.net

Approximation of fractional Brownian motion by martingales

Abstract

We study the problem of optimal approximation of a fractional Brownian motion by martingales. We prove that there exist a unique martingale closest to fractional Brownian motion in a specific sense. It shown that this martingale has a specific form. Numerical results concerning the approximation problem are given.

Keywords:

Fractional Brownian motion Martingale ApproximationConvex functionalMSC:

60G22 60G44 90C251 Introduction

Let be a fractional Brownian motion with Hurst index . It means that is a centered Gaussian process with a covariance function . It is well known that a fractional Brownian motion is neither a semimartingale nor a Markov process unless . So a simple and natural question is how far is Brownian motion from being a martingale? That is, in a sense, we look for the projection of fractional Brownian motion on the space of (square integrable) martingales. Thus, initially, the problem is formulated in such a way: we are looking for a square integrable -martingale that minimizes the value

To proceed with the solution of this problem, we can use the representation of the fractional Brownian motion via the standard Brownian motion on the finite interval (Norros ). Introduce the kernel

where , is the Gamma function, . Then there exists -Wiener process such that admits the representation

| (1) | |||

In what follows we consider fractional Brownian motion with , and in this case the kernel has a simpler form:

| (2) |

Turning back to our problem, we observe first that and generate the same filtration, so any square integrable -martingale admits a representation

| (3) |

where is an -adapted square integrable process. Hence we can write

Consequently, it is enough to minimize over Gaussian martingales, i.e. those having representation (3) with a non-random .

So, the main problem reduces to the following one:

-

(A)

Find

and a minimizing element if the infimum is attained.

Note that the expression being minimized does not involve neither the fractional Brownian motion nor the Wiener process, so the problem becomes purely analytic.

The paper is organized as follows. Sections 2 and 3 are devoted to the general problem of minimization of the functional on that has the following form

| (4) |

with arbitrary kernel satisfying condition

-

(B)

for any the kernel and

(5)

We shall call this functional the principal functional. It is proved in Section 2 that the principal functional is convex, continuous and unbounded on infinity, consequently, the minimum is attained. Section 3 gives an example of kernel where a minimizing function for principal functional is not unique (moreover, being convex, the set of minimizing functions is infinite). Sections 4–6 are devoted to the problem of minimization of principal functional with the kernel corresponding to fractional Brownian motion, i.e., with the kernel from (2). It is proved in Section 4 that in this case the minimizing function for the principal functional is unique. In Section 5 it is proved that the minimizing function has a special form. Section 6 contains some numerical results.

2 The existence of minimizing function for the principal functional

In this section we consider arbitrary kernel satisfying assumption (B), which implies that the functional is well defined for any .

Lemma 1

For any

| (6) |

Proof

Evidently, for any and

Therefore

which is clearly equivalent to the inequality

Swapping and , we get the proof.

Corollary 1

The functional is continuous on .

Lemma 2

The following inequalities hold for any function :

| (7) |

Proof

Lemma 3

Functional is convex on .

Proof

We have to prove that for any and any

applying the triangle inequality, we have for any

whence

and the proof follows.

Theorem 2.1

Functional attains its minimal value on .

3 An example of the principal functional with infinite set of minimizing functions

Note that the set of minimizing functions for functional is convex. In this section we consider an example of kernel for which contains more than one point, consequently, is infinite. At first, establish the following lower bound for functional .

Lemma 4

1. Let the kernel of functional defined by (4) satisfy assumption . Then for any and the following inequality holds

| (8) |

2. The equality in (8) implies that

| (9) | |||

| (10) |

Proof

1. Following inequalities are evident:

| (11) |

From we immediately get

| (12) |

Setting , and in this inequality, we get from (11)

| (13) |

Thus, inequality (8) is proved.

Remark 1

Example 1 (Functional with infinite set .)

Take the kernel of the form , , where

and

Then

| (15) |

and consists of functions satisfying the conditions

| (16) |

and

| (17) |

Remark 2

1. Since and , we have that is continuous in , therefore we can replace with in inequality (15).

To establish a lower bound on the left-hand side of (15), note that Therefore, applying Lemma 4 with and we obtain that

| (18) |

Moreover, functions satisfying and transform (18) into equality.

To establish an upper bound of the left-hand side of (15), consider functions satisfying conditions (16) and (17). Then for we have that

since on and . For , we take into account the values of and on this interval and obtain that

| (19) |

Hence, if function satisfies (16) and (17), we have that

Summing up, we obtain (15).

Now we prove that any minimizing function satisfies and .

Indeed, let

Then inequality (18) is transformed into equality, therefore

| (20) |

It follows from (20) and from the 2nd part of Lemma 4 that

a.e. on because , ; we obtain also the equality

a.e. on because for . Therefore, function satisfies condition (16). Then we can get similarly to (19) that

and it follows from inequality that

It means that function satisfies condition (17).

4 Uniqueness of the minimizing function for the kernel connected to fractional Brownian motion

Now we return to the main problem of approximation of fractional Brownian motion by martingales.

First we prove some simple but useful properties of the fractional Brownian kernel defined by (2).

Lemma 5 (Properties of the fractional Brownian kernel)

1. Kernel satisfies condition .

2. Kernel increases in the first argument and decreases in the second argument.

3. Kernel is continuous on the set .

4. For any and we have that with

Proof

Theorem 4.1

For any function there exists such function that and a.e.

Proof

Let . Consider the function . Since the kernel is nonnegative, then

and this inequality is strict on a set of positive Lebesgue measure if on a set of positive Lebesgue measure. Moreover, since the kernel is increasing in the first argument, we have that

and this inequality is strict on the set of positive Lebesgue measure if on a set of positive Lebesgue measure. Therefore, and this inequality is strict if or on a set of positive Lebesgue measure. Therefore,

Since the kernel is continuous in the first argument, there exists a function , such that .

Corollary 2

Functions in the set are nonnegative.

Now we are in position to establish the uniqueness of minimizing function for the principal functional corresponding to the kernel of fractional Brownian motion. In order to do this, prove at first the auxiliary statement concerning any minimizing function for this functional. For , denote

Then we have from the definition of the principal functional that It follows from Lemma 5 that for any . Using self-similarity property 4) of the kernel , it is easy to see that

| (21) |

Lemma 6

Let . Then the maximal value of is attained at the point , i.e. .

Proof

Set for . Suppose that . Since is continuous in , there exists such that for . It means that . Set . It follows from equation (21) that , . We get immediately that , which leads to a contradiction.

Theorem 4.2 (Uniqueness of minimizing function)

Proof

Denote the minimal value of functional . Recall that the set is nonempty and convex. Let It follows from Lemma 6 that for any function the following equality holds:

For any we have that

For arbitrary vectors and in a Hilbert space the equality implies that and differ by a non-negative multiple. Therefore, the functions and differ by a non-negative multiple, but since , we have . Therefore, , as required.

5 Representation of the minimizing function

In this section we consider principal functional corresponding to fractional Brownian motion and establish that the minimizing function has some special form. We start by proving several auxiliary results of the fractional Brownian kernel and the minimizing function.

5.1 Auxiliary results

Lemma 7

The fractional Brownian kernel for any satisfies

| (22) |

The following statement will be essentially generalized in what follows. However, we prove it because its proof clarifies the main ideas and, moreover, it has the interesting consequences concerning the properties of the minimizing function. In the remainder of this section denotes the minimizing function, i.e. the unique element of .

Lemma 8

Let if this set is empty. If , then for a.e. .

Proof

Fix some and prove that for any the following equality holds:

Evidently, proof follows immediately from this statement.

Assume the contrary. Then, without loss of generality, there exists such that

It follows from the continuity of the last integral w.r.t. upper bound that for some we have

for any . Note also that our assumption implies that

Consider now for . We have that for , and

for . For the following inequality holds,

with the constant that does not depend on . Then for sufficiently small we have that for any .

Furthermore, if , then

Again, for sufficiently small and any we have that . Therefore, for sufficiently small we get that and . We obtain the contradiction with Lemma 6 whence the proof follows.

Corollary 3

There exists such point that .

Proof

Denote , the set of the maximal points of the function . %̳ , , 8, .

Lemma 9

Let point is such that . Then there does not exist function such that for any the inequality holds.

Proof

Assume the contrary, i.e. let for some function we have that for any . The set is closed because . Therefore

Denote

the intersection of -neighborhood of the set with interval . Continuity argument implies that for some it holds that

for any . Similarly to the proof of Lemma 8, denote for any . Then we have that for any , and

for any . It follows from the continuity of that . Therefore we have for that

with the constant that does not depend on and . It follows from the above bounds that for sufficiently small and for any we have the inequality . It means that for sufficiently small we get the equality , and moreover, , which contradicts Lemma 6.

Lemma 9 supplies the form of minimizing function on the part of the interval . All equalities below are considered a.s.

Lemma 10

Let . Then there exist and random variable with the values in such that for we have that , and the equality

holds.

Proof

Consider the set of functions

and let

be the closure of the convex hull of . According to Lemma 9, applied to , there does not exist such that for any . Moreover, there is no such that for any , i.e. the element and the set can not be separated properly. Then, according to the proper separation theorem (see e.g. (convan, , Corollary 4.1.3)), , so there exists such distribution on that

| (23) |

Hence

| (24) |

Note that the equality is impossible because otherwise it follows from equation (24) that for , therefore which contradicts the assumption .

Using the latter statement and , we get the statement of the theorem with and random variable with the distribution .

Conditions on minimizing function from Lemma 10 are sufficient in the following sense.

Lemma 11

Let . Define the kernel for as

Function is the minimizing function of the principal functional if and only if there exists random variable taking values in such that the following conditions hold:

| (25) | |||

| (26) |

Proof

The necessity was proved in Lemma 10. Indeed, take that was obtained in the course of the proof of Lemma 10. Then condition (25) follows from the equality (23), while condition (26) follows from the fact that .

The sufficiency is proved basically by reversing a proper separation argument from Lemma 10: if a function belongs to the convex set , then it cannot be properly separated from this set, which means that it is a minimizer. To make this idea rigorous, assume the contrary: let a function satisfy (25) and (26), but . Then there exists function such that (for example, we can take as the minimizing function). Functional is convex, therefore

It is easy to see that for any function

Therefore for we have that

It means that for sufficiently small

| (27) |

On one hand, choose arbitrary for which the inequality (27) holds, and set . Then

| (28) |

On the other hand,

| (29) |

Inequalities (28) and (5.1) contradict each other. So, assuming that function is not minimizing for principal functional , we get the contradiction. Therefore, .

Lemma 12

5.2 Main properties of the minimizing function

We can refine Lemma 10 in view of Lemma 12. We remind that is the minimizing function for the principal functional and .

Theorem 5.1

There exists a random variable assuming values in such that

| (30) |

Proof

This statement is a straightforward consequence of Lemma 12.

We will assume further (clearly, without loss of generality) that (30) holds for every :

| (31) |

Corollary 4

1. The minimizing function is left-continuous and has right limits.

2. For any

| (32) |

moreover,

on a set of positive Lebesgue measure.

Proof

1. Follows from (31), continuity of and the dominated convergence.

Further we investigate the distribution of .

Lemma 13

There exists such that

Proof

Denote

The function is continuous on and has left and right derivatives (except of ):

where . Hence, by Corollary 4

and the statement easily follows.

The lemma just proved means that is an isolated point of .

As an immediate corollary, we have the following theorem.

Theorem 5.2

There exists such that , and the distribution of has an atom at , i.e. . Consequently, for all .

Further we prove that the distribution of has no other atoms.

Theorem 5.3

For any . Consequently, .

Proof

Remark 3

Due to monotonicity of in the first variable, the right-hand of inequality (8) is maximal for , so we have that

| (34) |

Theorem 5.3 implies in particular that the inequality is strict, i.e. this lower bound is not attained. Indeed, if there were equality in (34), Lemma 4 would imply that the distribution of is , where is the point where the minimum of the right-hand side of (34) is attained, which would contradict Theorem 5.3.

Remark 4

From (31) it is easy to see that decreases on the complement of . The numerical experiments in the following section suggest that is decreasing on (the positive jumps in the graphs are due to atoms, which are, clearly, unavoidable in the discrete case, but there are no atoms in the continuous) case. It seems even that is constant on , which would be a striking property to have. However, we did not manage to prove either of these facts.

6 Approximation of a discrete fBm by martingales

In this section we consider a problem of minimization of the principal functional, but in discrete time. This is an approximation to the original problem, so its solution can be considered as an approximate solution to the original problem.

Let be a natural number, and define . The vector will be called a discrete fBm. It generates a discrete filtration , . For arbitrary random vector with square integrable components denote

Consider the problem of minimization of the functional , where is an -martingale.

Denote by the increments of the discrete fBm. Let be the covariance matrix of the vector . Using the Cholesky decomposition, one can find a lower triangular real matrix such that . Then there exists a sequence of independent standard Gaussian random variables such that is -measurable for and

Define a matrix as follows:

It is clear that

The matrix is therefore can be regarded as a discrete counterpart of a fractional Brownian kernel.

Further, we will show, as in the continuous case, that minimization of over martingales is equivalent to minimization over Gaussian martingales. Indeed, let be arbitrary square integrable -martingale. Owing to the fact that , , we have the following martingale representation:

where is a square integrable -measurable random variable, . Thus,

So we can assume that has a form , , with some non-random . Then

Thus, we have arrived to the following optimization problem:

For fixed and we solve this problem numerically by using the MATLAB fminimax function.

The following table gives the values of the functional for different and .

| H | .55 | .6 | .65 | .7 | .75 | .8 | .85 | .9 | .95 |

|---|---|---|---|---|---|---|---|---|---|

| .0013 | .0051 | .0112 | .0200 | .0320 | .0482 | .0705 | .1023 | .1511 |

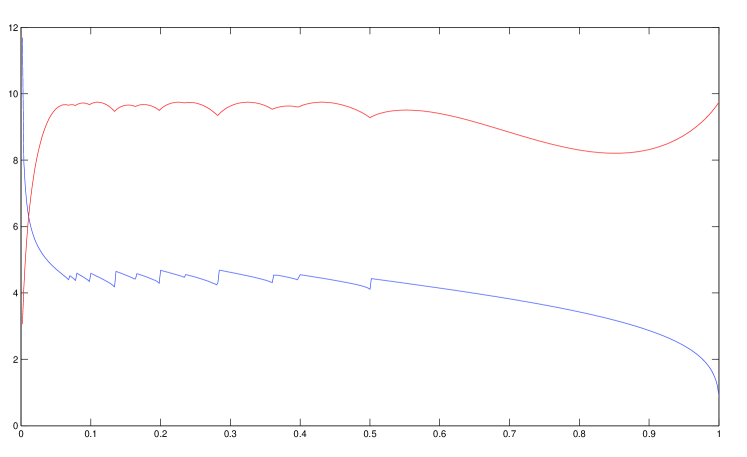

Figure 1 shows the values of for from to with a step for . Figure 2 contain graphs of the minimizing vector (blue) and the scaled “distance” (red), when and . For other values of the picture is similar: is (mainly) decreasing and looks close to constant on the sets of maxima of .

References

- (1) A. E. Bashirov. Partially Observable Linear Systems Under Dependent Noises. — Basel : Birkhäuser, 2003.

- (2) J.-B. Hiriart-Urruty, C. Lemaréchal. Convex analysis and minimization algorithms. Part 1: Fundamentals. Grundlehren der Mathematischen Wissenschaften 305. Berlin: Springer-Verlag.

- (3) I.Norros , E.Valkeila, J.Virtamo. An elementary approach to a Girsanov formula and other analytical results on fractional Brownian motions. Bernoulli. Vol. 5, No. 4, 1999, 571-587.