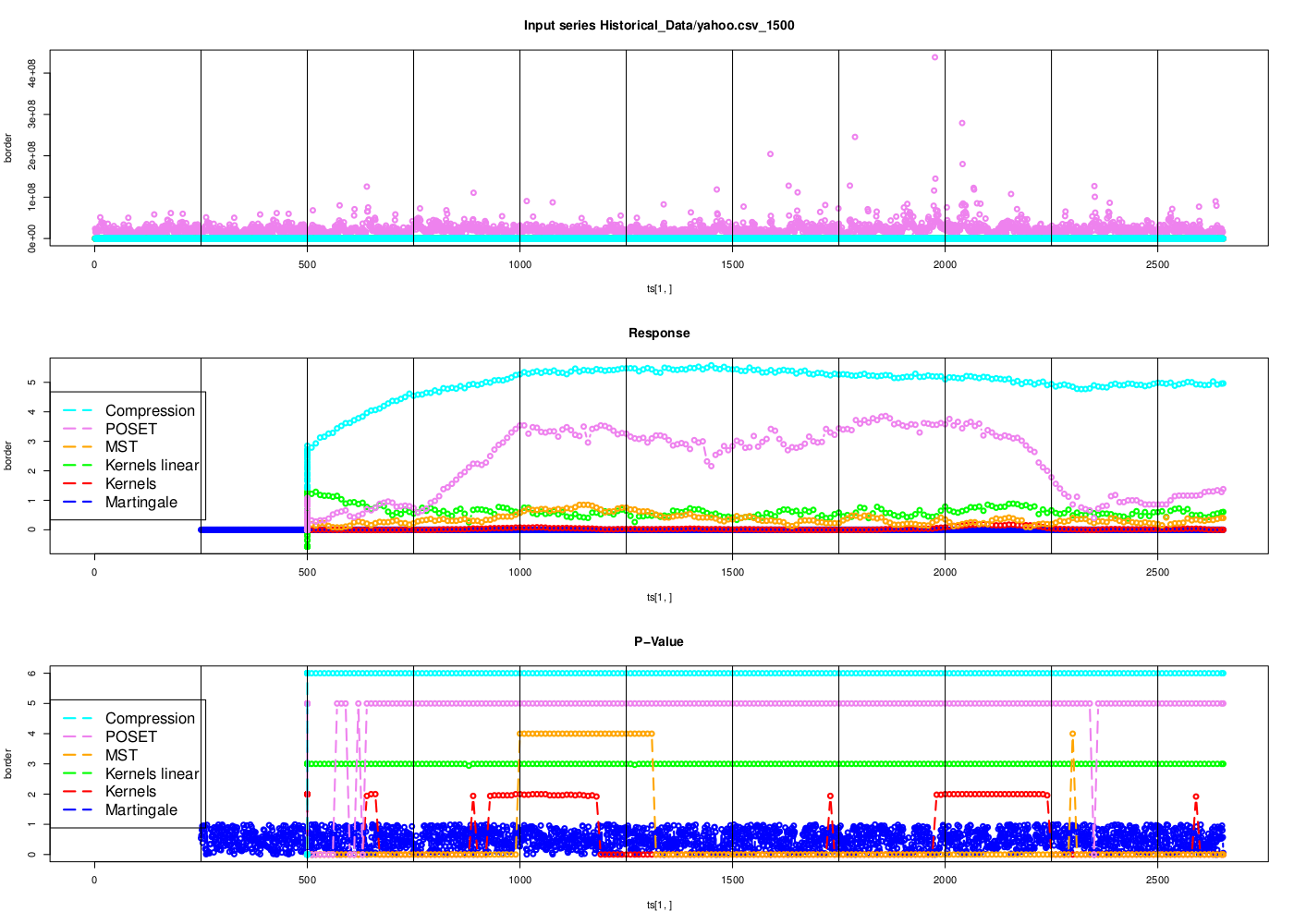

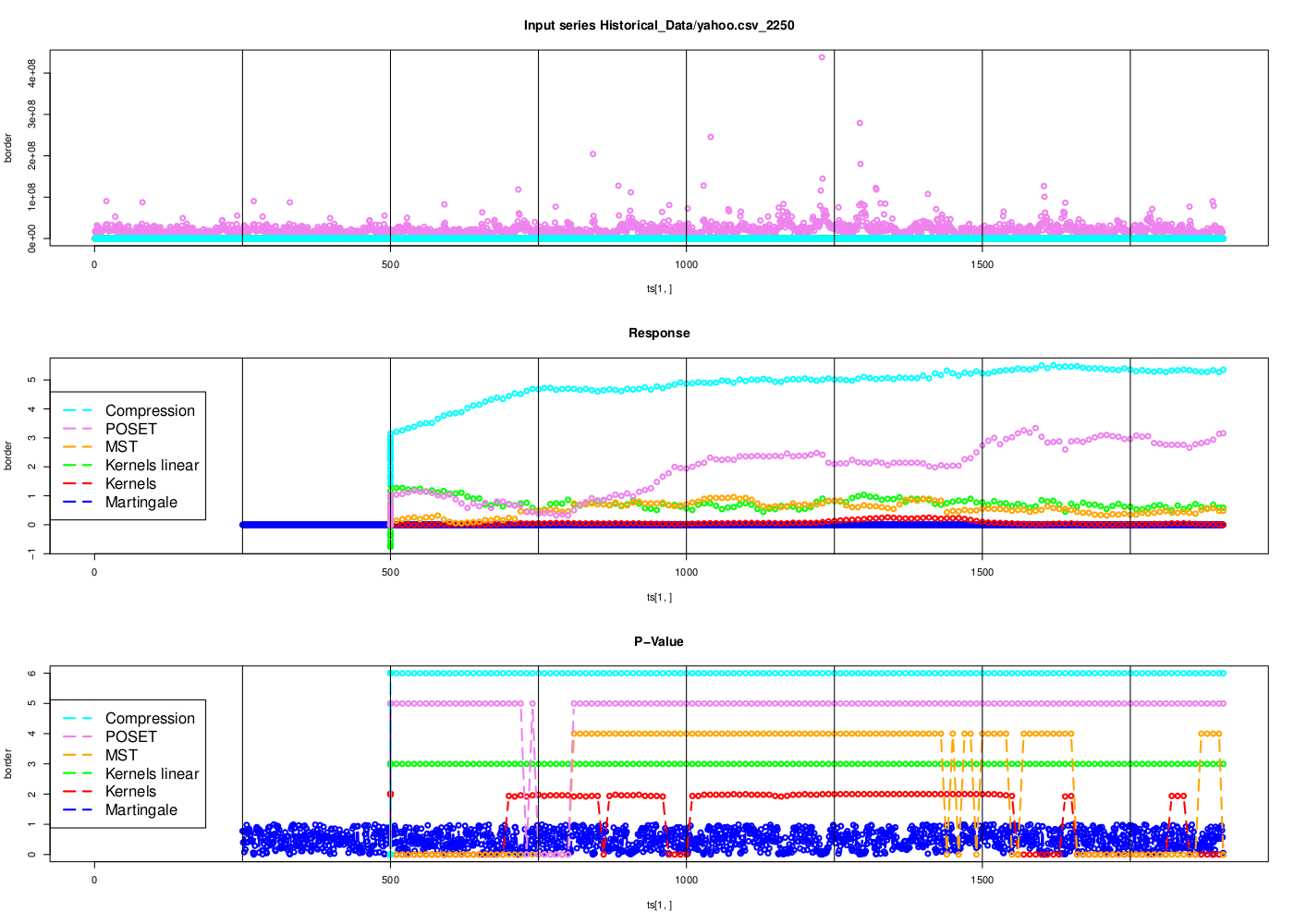

Non-Parametric Methods Applied to the N-Sample Series Comparison

Abstract

Anomaly and similarity detection in multidimensional series have a long history and have found practical usage in many different fields such as medicine, networks, and finance. Anomaly detection is of great appeal for many different disciplines; for example, mathematicians searching for a unified mathematical formulation based on probability, statisticians searching for error bound estimates, and computer scientists who are trying to design fast algorithms, to name just a few.

In summary, we have two contributions: First, we present a self-contained survey of the most promising methods being used in the fields of machine learning, statistics, and bio-informatics today. Included we present discussions about conformal prediction, kernels in the Hilbert space, Kolmogorov’s information measure, and non-parametric cumulative distribution function comparison methods (NCDF). Second, building upon this foundation, we provide a powerful NCDF method for series with small dimensionality. Through a combination of data organization and statistical tests, we describe extensions that scale well with increased dimensionality.

category:

G.3 Probability and Statistics Nonparametric statistics, Statistical software, Time series analysiskeywords:

N-Sample, series, distribution comparisonsP. D’Alberto, A. Dasdan, and C. Dromen 2012. Non-Parametric Methods Applied to the N-Sample Series Comparison

Author’s addresses: P. D’Alberto paolo@FastMMW.com, A. Dasdan ali_dasdan@yahoo.com, and C. Drome cdrome@yahoo-inc.com

1 Introduction

Let us begin by exploring what change detection in a multidimensional series is through a couple of examples. If we are investigating whether cheating is happening at a game of chance, we could try to find a bias or pattern in a single game or a set of games, which would constitute a single dimensional series and a multi-dimensional series respectively. We may look for a statistically significant difference from the expected win-loss pattern. As another example, an Internet search company may collect hundreds of annotation features for a host, then the search engine will monitor the feature changes over time in order to identify potential service outages or other issues with that host. In both cases, a variation from the norm can only be identified and understood after it happens, which may prompt further investigations into the cause.

The question of why one should be concerned about change detection should be obvious even when considering what is at stake from the two previous examples. Although it is true that we may be able to identify a change only after it has already occurred, one important goal of change detection is to minimize the amount of delay required to identify such a change, and thereby, hopefully, minimize the impact or effects of the change.

In this paper, we consider change detection, and consequently similarity detection, as a data mining problem on a large volume of data. In particular we are interested in optimizing the early response, recall, cost, and sensibility with respect to a change:

-

•

for the early response, we try to minimize the number of events or data points that pass by undetected before a change is identified;

-

•

for the recall, we try to increase the accuracy of identifying real changes versus perceived changes;

-

•

for the cost, we try to reduce the cost and increase the speed at which the required computations are performed;

-

•

for the sensibility, we try to minimize the number of data points required to declare a significant difference (early response and sensibility are related: we will need a fast response to have a sensible response, but we will need some confidence associated with the variation to improve the recall).

We organized this work into three parts: In the first part, we present a review of a variety of existing methods using a unified and concise notation. Each method is described in detail with an emphasis on pointing out their relative advantages and disadvantages. In the second part, we propose a new method and compare it against the previously described methods. In the third part, we present experimental results for the various methods. To this end, we have produced a self-contained work which can be understood by others who do not have an in-depth knowledge of this field111A comparable understanding of the topics contained herein would require the reader to comprehend half a dozen papers covering just the statistical aspects. A similar amount of papers would be required to understand the implementation details, and another handful to cover experimental results. Furthermore, each paper would be presented in its own notation making comparison between methods challenging..

In summary, our goals for this work are as follows: The first goal is to introduce the reader to six methods spanning four different non-parametric method families. We do this in the context of a unified framework which easily facilitates comparison between methods. This framework is designed to be flexible enough that adding new methods is easy. Our work is similar to the work by Siegle in 1959 [Siegel (1959)], in which he focused on explaining the power and usage of non-parametric methods. Rather, our work focuses on the computational aspects of the methods in order to create a useful statistical tool set.

A secondary goal, arising from the first, is to show that there is no single best method; rather, the most appropriate method is a function of the data. That said, each method does contribute insights into understanding the data better. Hence, we propose that the methods should be used in conjunction, thus enhancing the set of statistical tools available to the reader.

The third goal is to build upon this knowledge to propose a new method based on works of Bickel [Bickel (1969)] and Friedman–Rafsky [Friedman and Rafsky (1979)]. We have extended these works in two original ways, by sorting the data in topological order, and then applying a robust, non-parametric test set based on empirical cumulative distribution functions.

The fourth goal is to contribute an implementation of our proposed framework, which includes codes of the methods described herein. The library is implemented in C and optimized to reduce the computational costs of each method. We supply wrappers to allow the use of the library to be called from within such languages as Java, Python, Perl, and R.

The final goal is to demonstrate the application of our framework through a series of experiments on a variety of data sets, including well-known, classified data sets, and synthetically generated data sets.

Section by section, we have organized the paper as follows: In Section 2, we build a foundation for later sections by defining necessary terms and explaining the motivation for analyzing multi-dimensional series and the need to develop appropriate tools. In Section 3, we present details of the statistical methods that can be applied to the two-sample problem in multi-dimensional space and presents the theoretical background of those methods. This includes the following known methods: conformal prediction in Section 3.1, Kolmogorov’s information in Section 3.2, kernels methods in Section 3.3, as well as our proposed non-parametric method in Section 3.4. In Section 3.5, we introduce non-parametric statistics that are suitable for single- and multi-dimensional series. Finally, in Section 6, we provide an overview of the experimental results. In Section 7, we start with the results obtained by the application of methods for multi-dimensional series. Finally, in Section 8, we follow with the performance of our non-parametric statistics, which are based upon cumulative distribution functions (CDF), and we compare them against the classical probability–distribution-function (PDF) statistics.

2 Change Detection in Series

This section addresses two topics: we present our notation to describe a series, and we present examples of change in series. The notation is used throughout the work; in the experimental results, we are going to present the analysis for most of the examples introduced in this section.

2.1 Terminology

A series is composed of elements where is a strictly increasing, non-negative integer, called an epoch, which represents time. The epoch helps ensure a global ordering of the elements of , . We identify the most recent or the last element of by .

The term , the natural positive number set, is a time stamp where the epoch is always in order and increasing. Note: the time stamp of a sample does not necessarily have this constraint. The distinction between epoch and time stamp is made because there are instances where the order of the time stamp does not coincide with the order of the epoch. For example, the epoch could describe when a process finishes and data was collected; in contrast, the time stamp is when the process started. In such cases, we want to reorder the sequence accordingly, because the processing time is not under consideration. The term with is the sample vector (e.g., a single value when ).

We define the reference window and test window as the ordered set of successive elements of . We shall present methods for which the length of the two windows need not be equal. When reduced to vectors, these windows are represented as and . In practice, these windows typically do not overlap, and either one can be made more recent or closer to “now” depending on the need for defining a new reference. In this work, we will use the time stamp to build intervals that are ordered sets of points in time; thus we do not use the epoch. We explicitly use the epoch only when we need to handle the last sample point to compare it against a set of points that were collected in the past.

To simplify the presentation, we will overlook the difference between epoch and time stamp. In fact, we can interchangeably use , in , and in without loss of information, because the original order should not matter once the intervals have been created.

A change occurs any time when is different from . In the following section by using examples, we present an intuitive explanation of change.

2.2 Examples of Series and Change

Hardware Clusters. One can measure the read–write latency of the four disks on each machine in a 1000-node cluster during a stress test. Each disk is considered independent of the others; therefore, each disk latency measure is an independent data point. Over time, a multi-variate series is generated: 1,000 independent series each with four dimensions, for a total of 4,000 series. Alternatively this could be viewed as one series with 4,000 dimensions.

Any variation in the average latency could indicate a mechanical defect and thus a possible rejection of the disk lot. Any variation in the variance of the latency, an increasing deviation in the latency, could indicate the possibility of a pending failure or data inconsistency.

Sites and URLs. In the process of generating a web graph, sites, hosts, and URLs are annotated with hundreds of features. Each feature can be considered orthogonal and independent. Consecutive builds of a web graph will generate billions of series composed of hundreds of dimensions.

A sudden change in the measure space may occur as a result of an internal or external error. Similarly, a change in variance could hint at potential issues.

Hardware Counters. With the increased complexity of modern hardware components, it is becoming more common to embed a variety of hardware counters to monitor performance statistics. These counters can be used to monitor the performance of software running on the underlying hardware. Multi-dimensional series can be generated by polling these counters over time.

Quantifying the stochastic distance between series generated by different software allows the grouping of software with similar hardware processing profiles. We could match applications with specific hardware accordingly. This example uses the magnitude of the difference between series to identify similarity.

Histograms in Time. Selection rank algorithms, such as PageRank, attempt to order URLs by ranking them. These ranking methods are useful in generating histograms, which are valuable inputs for machine learning and self-adjusting ranking tools. A histogram can be thought of as a vector or a multi-dimensional point.

The histograms evolution over time results in a series which can be used to monitor for internal or external failures in the collection system.

Stock Index. A stock index is a set of stocks which act as an indicator for a specific sector of the market. Again, a stock index can be thought of as a multi-dimensional series; although it should be noted that the individual stocks may not necessarily be independent. Also note that the historical data about a specific stock can also be thought of as a multi-dimensional series composed of such attributes as average price, volume, opening price, closing price, high, and low.

The benefits of quickly identifying changes should be readily apparent.

Multi-Dimensional Series. Instead of analyzing a multitude of single- dimension series, it is sometimes easier and more natural to join sets of single-dimension series into one multi-dimensional series. This is important to consider, because we will show that certain feature changes are easier to detect when looking at a multi-dimensional series, as opposed to considering each dimension individually.

In general, given a sample of points from the reference interval and a sample from the moving interval , we are able to quantify the degree to which the two intervals originate from the same stochastic process, and hence are indistinguishable and independent. Note that we have not mentioned the correlation between dimensions or the independence of samples. These topics raise such questions as determining the important dimensions of a series, and whether certain dimensions can be ignored without loss of information. We will touch on these issues in the context of this paper.

In summary, given a series and a change, we would like to have a quantitative and automatic method to detect the change. What follows is a description of tests that are available in the literature, for which we will provide experimental results. Finally, our original contribution will be presented in Section 3.4

3 Methods for Multidimensional Series

The literature is rich and spans many disciplines. There is a wealth of statistical tests and methods for organizing data in sets, and numerous approaches for identifying relations across different features or dimensions.

A recent work by Sriperumbudur et al. [Sriperumbudur et al. (2009)], clearly attempts to classify and understand the power of different families of measures. For example, the authors draws a connection between -divergence based methods, such as those of Kullback-Leibler [Kullback and Leibler (1951)] and Jensen-Shannon [Jensen (1906), Shannon (1948)] (Section 4.1), and integral probability based measures, such as reproducing kernel Hilbert space methods [Borgwardt et al. (2006)] and Kolmogorov-Smirnov’s [Kolmogorov (1933)] method. The authors find only one metric, the variation distance [Pinsker (1960), Ali and Silvey (1966)], which is common to both types of methods. Others have found further commonality, such as Jensen-Shannon’s distance being embedded into a Hilbert space [Fuglede and Topsoe (2004)], resulting in the application of -divergence into a space where integral probabilities are more common. Interestingly, the authors in [Sriperumbudur et al. (2009)] suggest that -divergence methods are difficult to estimate in high dimensions; either being too expensive computationally or not powerful enough. We will show that this is not the case.

Borgwardt et al. and Gretton et al. [Borgwardt et al. (2006), Gretton et al. (2006), Gretton et al. (2008)] provide the first extensive comparison of the same family of measures that we use in this work 222We introduce compression methods.. Their test results show that kernel methods and conformal prediction are insensitive to the dimensionality of the series, while previous tests based on [Biau and Gyorfi (2005), Friedman and Rafsky (1979)] show a loss of discriminative power as the number of dimensions increase.

What distinguishes our work from others is the focus on the computational aspects of implementing each method in the context of a set of statistical tools. A clear understanding of the computational requirements of a method lead to insights about the method itself. As we are building a set of tools, our target audience are those researchers who may be familiar with one or two methods and want to explore the effectiveness of other methods 333Novice users may find that this work is lacking explanatory examples, while advanced users may find this work too verbose.. We feel that we have taken the works of Bickel [Bickel (1969)] and Friedman–Rafsky [Friedman and Rafsky (1979)] and succeeded in extracting the common features, combining the data sorting algorithms, and deploying non-parametric statistical tests that are independent of the data ordering.

With respect to our original contribution, we show that the -divergence measures can be generalized, extended, and applied to multi-dimensional series (i.e., with ) in a manner that makes them as discriminative as other measures. We show that the complexity of -divergence methods is where and by using spanning trees in conjunction with all-to-all distance computations. The complexity becomes by using sorting poset algorithms, where is the dimensionality of the series and is the number of parallel points where comparison is undefined. If , then the complexity becomes , which means that the sample is not large enough to represent the probability sufficiently. Note: this complexity is comparable to the other methods (e.g., kernels methods).

In Section 3.1, we present conformal prediction methods along with the implementation details. This is followed by a discussion about the similarity measure based on Kolmogorov’s information complexity measure in Section 3.2. We describe the minimum mean discrepancy measure as computed from reproducing kernels in a Hilbert space in Section 3.3. In Section 3.4 we introduce our extension of the distribution comparison using a poset-based and a minimum–spanning-tree topological ordering. We complete the extension of our method to multi-dimensional series with a look at methods of applying single-dimensional distribution function comparison measures to the topological ordering in Section 3.5.

3.1 Conformal Prediction

We present the following methods under the assumption that the series is composed of independent samples. Consider the series , where is an integer , and where . The event should be independent of previous and successive events. The importance of the independence condition lies with the ability to fully count the contribution of a single event towards the description of the process that generated the event. In absence of this condition, it is possible that the event is redundant and could be ignore entirely.

In this section we explain what an independence test is. This is followed by a discussion of how different change detection methods are designed to capture both independence and change.

The hypothesis of independence states that can be described by a distribution function where = . Alternatively, this could be expressed as . The hypothesis of exchangeability is based on the idea that the sequence of is generated with a probability . Thus we could obtain a probability under , such that, the permutation is distributed as the original ; that is, for any permutation . Independence implies exchangeability, although the reverse is not true.

We are interested in exploring on-line independence–interchangeability tests. For each new data point, where , we determine whether or not belongs to the series based on the information that has been seen so far. If not, then a change has occurred. In other words, if the probability of a data point occurring is similar to that of the points already seen, and if independent of the sequence of events, then truly there is no detectable change.

3.1.1 Individual Strangeness Measure

Consider a particular interval of a series where , a multi-dimensional space, such that and .

Now consider, a family of measurable functions , where . More specifically, is an individual strangeness measure when for any of any permutation of the time stamps in , and for any and and any

| (1) |

is equal to

| (2) |

Example. With the term we identify a distance function, such that for every it returns a real number , which quantifies the strangeness of the point with respect to or (the interval without the point in consideration). This becomes the means by which we can represent a multi-dimensional series, , as a single vector in , for which we can estimate a distribution function. In the next step, we shall show how to reduce it to a single real number.

3.1.2 Transducers:

A deterministic transducer is a function , where is a strangeness measure. We define the transducer as

| (3) |

where

| (4) |

The transducer takes an interval and a new data point, for which a measure of strangeness is computed, and it returns the number of points that are of equal or greater strangeness.

There is another type of transducer, the randomized transducer, which introduces a randomized multiplicative term, uniformly generated from the real interval , to break ties (i.e., ). The randomized transducer is used to ensure that, in the case of no change, the output of the transducer will be uniformly distributed over .

This is an important concept and we should clarify the meaning and the power of a randomized transducer. In other words, if we have a set of samples that have the same strangeness and we use a deterministic method, the transducer is going to produce a sequence of ones. Equality of strangeness is a strong signal that the new points belong to the set but the output value will be skew towards the value one. It will not be uniform. The randomization has no effect if there is no ties, and the transducer’s distribution will be evident. The randomization has effect only with a lot of ties, and the distribution of the output will be artificially uniform.

Very briefly, in case of no change, the output of the random transducer will be uniformly distributed. In case of change, the distribution should be skewed. The type of transducer will determine the extent of skewness.

We deploy deterministic transducers only, because they are easy to understand. Furthermore, we propose an alternative to coping with an output that is non-uniformly distributed.

Example. The transducer–strangeness pair is an attempt to estimate the distribution function of the process that generates the series. If we knew the distribution of the process, it would provide a direct method for the computation of the transducer–strangeness pair.

Although we implemented a few transducers, we shall turn our attention to transducers based on a minimum distance measure (i.e., nearest neighbor) or an average distance measure, as either can be computed in linear time for each new point. In fact, with space to store an adjacent matrix, we can compute the update of the minimum and average distance between points with comparisons.

If we apply the transducer to the series, we compute a different series . This transforms the problem from one using multi-dimensional series data to single-dimension series data.

The question now becomes one of how we can use the output series of a transducer in such a way to detect change in a series. To this end, we present two approaches: the Martingale method and a non-parametric method (and we can use them separately or together). The Martingale method simulates gambling to exploit a consecutive sequence of lucky or unlucky bets: skewed distribution to specific discrete points. The non-parametric method measure the change of distribution in its entirety: change of the type of distribution from uniform to exponential. One approach does not subsume the other. Both methods are aimed at detecting variations in the transducer’s output. At the time of writing this paper, we have started experimenting with kernel methods as well.

3.1.3 Martingale Methods

We know that the transducer provides an estimate of the distribution function . As such, the series is an approximation of the probability that the sample belongs to the series as seen so far. The Martingale method is based on the idea that successful bets result in exponential gains if a long enough sequence of successes is found. An example of a sequence of successes would be a sufficiently long sequence of , which consists of points determined to be strange with respect to the reference interval.

The Martingale measure is defined as

| (5) |

where and . The Martingale measure will increase exponentially if for a sufficiently long sequence of points. In the literature, we found two tests related to the Martingale measure and its maximum increase.

Property, Without Proof [Ho and Wechsler (2010)]. Given the hypothesis that there is no change, we can accept the hypothesis as long as

and reject the hypothesis when . In fact, for any and bounded we have

| (6) |

If , that is, if we take an interval of time where the Martingale starts and finishes with a steady point, then

.

Property, Without Proof [Ho (2005)]. We can use the derivative of the Martingale measure to reject the test in the case of when

| (7) |

In fact, we have

where is a difference Martingale and is a proper constant.

The parameter and are set according to the recommendations in the literature by Ho et al. ([Ho and Wechsler (2005), Ho (2005), Ho and Wechsler (2010)]); hence and .

Property. The Martingale test approximates the sequential probability ratio test ([Wald (1947)]), which can be used in combination with to form a more robust test. This is not investigated further.

In addition to the values for and mentioned above, we set ; however, all three of these parameters should be tuned accordingly with the size of the reference interval .

3.1.4 Non-Parametric Distance Application

In this section, we present our contribution to the Martingale method by taking a fresh look at as a series.

In the original works on the Martingale method, the transducers provides an estimate of a probability function. If this is truly a distribution function, we expect that is uniformly distributed on . Let us assume we know the nature of the process that generates the sequence ; that is, we know the distribution function and therefore we also know . All of the above properties hold true if we use .

In practice, and, in the work by Vovk [Vovk (1993)], the author defines the power of transducers and rigorously demonstrates how they can be used instead of the distribution function.

We make only one assumption about the sequence , that is, if there is a change in the original series , there is a corresponding change in the series, and vice versa. Instead of making assumptions about the distribution of , such as being uniformly distributed on , we create a reference sequence by running the system on a series for which there is no change. We also create a moving window consisting of as the system evolves in time. This creates a two–-samples problem for which we can apply all the stochastic distance measures in the literature. In practice, we will apply our generalized measures as described in Section 3.5.

Remark. We will show that this test, which is built in parallel with the Martingale method, will have more than a supporting role. We will also show that it is orthogonal to the Martingale method, capturing global variations of the series , not just temporal variations (i.e., lucky/unlucky bets). This test can also be used to reset the Martingale measure to 1, resulting in a faster response to changes. For example, at steady state where there are no changes, the Martingale measure will tend to decrease (the result of consecutive losing bets) to a value as small as . A side effect of this small value, is that the method requires a longer string of changes before it can recognize a changes has occurred, because it takes more effort to recover. A periodic check of the sequence will allow us to safely restart the Martingale method from a value of 1, where it will be more responsive to change.

Remark. Resetting the value to 1 is beneficial only when the Martingale value becomes extremely large or small, hence the Martingale value is slow to return to a steady state. It is also very important to carefully choose the moment of the reset. If there is a temporal change in with no corresponding change in the distribution, it may be disruptive to reset the value at this time as a change is just being detected. We will return to this topic in the experimental results section.

This section’s references are [Vovk et al. (2003), Shafer and Vovk (2008), Vovk et al. (2005), Ho (2005), Ho and Wechsler (2010), Vovk (1993), Wald (1947), Einmahl and Khmaladze (2001), Kulldorf (1997)]

3.2 Normalized Compression Distance

The measure that we discuss in this section is known by several names in the literature, including the similarity metric describing the universal nature of the measure, the algorithmic information distance, and the information distance. We feel the term normalized Kolmogorov’s information measure is more precise and distinguishes it from the Kolmogorov-Smirnov measure and other information-theoretic measures like Jensen-Shannon or Kullback-Leiber measures.

To describe Kolmogorov’s information measure we need to introduce Kolmogorov’s complexity. Consider a descriptive process as a set of pairs where is the description of and both are binary strings such that can be described by a chain of descriptions s. can be seen as an algorithm.

The complexity of an object is the minimum length of the description such that :

| (8) |

Let us fix the , and thus the string set we need to describe. Let us also consider a family of processes that describe and are associated with algorithms such that Kolmogorov’s hypotheses apply as follows: for all there exists an optimum such that . For the sake of brevity, we can drop the specifier so the complexity of is denoted simply as . Thus, we have found an optimal algorithm capable of using a shorter key to retrieve the output , while maintaining a simple mapping .

Armed with these concepts, Kolmogorov was able to provide the first, widely-accepted, and formal definition of a random sequence: a sequence is random, if

| (9) |

where is a constant and is independent of .

The details of the computability of [Terwijn et al. (2010)] are outside the scope of this paper. Instead, we will use the compression algorithm from zlib, referred to as for compression, to approximate the Kolmogorov’s measure. The compression algorithm takes a binary string as input and produces a shorter string as output. A loss-less compression creates the mapping . Hence, we can measure the complexity of by the length of as generated by the compression algorithm.

Now the question arises as to how we compute the distance between two intervals and in a series?

In practice, the intervals and are two arrays of double precision numbers stored consecutively in memory. We can simply represent the encoded data as and .

The Normalized Compression Distance is defined as

| (10) |

where is the concatenation of and . We have where is a small term function of the compression algorithm, which represents an artifact of the compression algorithm. If , then () is similar to (); conversely, if , then is different from .

Intuitively, is an estimate of , or the complexity of under the condition that has already been seen. We interpret as the independent complexity of with respect to (or with respect to ).

Assume that is generated by a stochastic normal process with a distribution, is generated by either or , and they are of the same length . Because of the characteristics of the compression algorithm and the nature of the input, the compression measure will be very close to 1, independent of the choice of ( or ). However, there will be a difference, regardless of how small it is. To handle the cases we are interested in, we must provide a confidence level, or p-value, and take advantage of this difference.

3.2.1 Bootstrap

Consider the intervals and , generated by the same process, as a sequence composed of points each. Applying a series of swaps between the original series (i.e., ), two new sequences and can be created to generate . The distance values are sorted, so that a distribution and a p-value can be determined. In computing , the distance value can be used to obtain a significance level. Then, can be used as a minimum threshold, in combination with the p-value, to provide a measure of the significance of the difference.

This bootstrapping process tunes the sensitivity of the NCD measure to the training set. For example, if we are working with intervals which are very similar, then the range of possible distance values will be small, and the p-value will be sensitive to small variations; thus, we have a measure for the process that is quick to reject the equality hypothesis. For most of the synthetic series in the experimental results section, this sensitivity is a powerful discriminating feature. However, if the measure becomes too sensitive, every interval will be considered different, and the measure will fail to give useful information.

The section’s references are [Martin-Lof (1969), Kolmogorov and Uspenskii (1987), Bennett et al. (1998), Li et al. (2004), Cilibrasi and Vitányi (2005), Terwijn et al. (2010), Keogh et al. (2004)].

3.3 Kernel Methods

The following distance measure is called integral probability metric (IPM) [Müller (1997)],

| (11) |

where is the class of real-value bounded measureable functions in , and and are probability functions.

If , , and , then because

Furthermore, if , then , that is,

thus, with probability 1.

For example, if we restrict the class to the step function (i.e., when , otherwise), then

that is the Kolmogorov-Smirnov test.

In the remainder of this section, we examine the class of bounded continuous functions where represents a reproducing kernel Hilbert space with as its reproducing kernel. This measure is called the maximum mean discrepancy (MMD), and is defined as:

| (12) |

We will explain the concepts of Hilbert space and kernels, and then examine how to transform a multi-dimensional problem into a covariance matrix computation, and then into a single-dimension problem.

3.3.1 MMD, Kernels and Notations

In discussing a Hilbert space, let us consider as a class of real-valued functions forming a real vector space and restricting multiplication to real constants only; that is, the addition of functions is a function in , given a and any , then . Such a class of functions is called a real Hilbert space if the following two conditions are met: First, the norm in is given by where is a scalar product so that for any real and any function :

| (13) |

second, is complete. Complete means that any Cauchy sequence such that , then every function .

Notice that the inner product is a vector norm and it is also a distance measure for a functions space. The linearity property in Equation 13 states that the domain is well behaved; the completeness property makes the domain closed for infinite series and their linear combinations.

Now that we have a definition of a Hilbert space, let us introduce what is a kernel. Assume that is a Hilbert space defined in ; that is, with . The function with and in is called a reproducing kernel if the following two conditions hold: First, for every fixed , then ; second, and , then we have

In other words, is a valid function, and, in combination with the inner product, we can reproduce the original function. It is important that be continuous, as this will ensure the existence of a reproducing kernel that will be unique. Any one familiar with the Fourier transform will recognize the previous two properties, thus the ability to reconstruct the original signal/function. We have stated now the definition of kernels in a Hilbert space.

There are occasions where finding the witness function, the function that minimizes Equation 12, is useful to shed a light to the data. For our purposes, we do not really need the witness function and in this work we do not pursue it any further. In practice, once the reproducing kernel is set, the computation can be simplified by directly finding the MMD bound, without the witness function. Indeed, the kernels are a powerful tool set.

Now, we explore how to transform the problem from the multi-dimensional space, in which the series is defined, to a single-dimensional space, where is defined by the scalar product into the Hilbert space.

The first problem is how to transform a multi-dimensional space into a single-dimension space. As suggested in [Gretton et al. (2008)], the authors in [Schölkopf and Smola (2002)] found the existence of a mapping from the original domain to a feature domain in such that is in the Hilbert space. Using the kernel , where and are defined in the original space, results in . This is a single dimensional space.

The existence of assures the existence of . Unfortunately, this property does not really provide a constructive description about the kernel that can be used.

The second problem is how to simplify the computation such that it is using kernels only. The authors in [Gretton et al. (2008)] suggest using expectations to rewrite the MMD as follows,

| (14) |

We report the original proof in the following as

In the Hilbert space, the right-hand norm can be computed in terms of kernels only:

For finite samples and in and where this can be estimated by

| (15) |

Notice that, once the kernel is known, it is not necessary to compute: the witness function , the scalar product , nor the mapping 444In practice, how to choose the right kernel is often a art. We followed the suggestions of the original authors as we will explain in the following section..

3.3.2 MMD in Practice

Based upon the theoretical understanding of MMDs and the process of transforming a multi-dimensional space into a single-dimensional space, we will examine the details of the methods used in this paper. This includes a discussion of what is computed in practice, how the significance measure is determined, and which kernel to use.

MMD Computation. We shall consider two MMD measures. The has already been described in Equation 15 and has a computation complexity of ; instead, is a linear approximation of .

Assuming that and is even, then is defined as follows:

| (16) |

Consider to be the product

where the matrix is a semi-definite covariance matrix, that is for any , which is a proper difference measure. Therefore, the linear approximation considers the contribution of the one upper diagonal only, which should also be the dominant one. Now, consider to be a covariance matrix consisting of only those consecutive points in the series at a distance of 1 from each other. Notice that the comparison reduces to a localized pair-wise comparison of and and their direct neighbors and , without requiring an all-to-all comparison.

Significance Level. Having examined the computation of the MMDs, we consider the question of determining whether the two samples are similar or different.

For we followed the practical approach outlined in [Borgwardt et al. (2006)] Algorithm 1 555In [Gretton et al. (2008)], the authors present a better way of computing the significance level for than in [Borgwardt et al. (2006)].. Particular care must be taken in the computation of , because for even moderate values of the denominator can grow so large that it cancels the overall contribution. This results in an incorrect estimate of the variance.

For we use the method described in [Gretton et al. (2008)] Corollary 22, and present the results here as well. The variance is computed at the same time as the distance for both methods. This shows that the variance has a normal distribution with 0 mean and a parametric variance of . Knowledge of the distribution of the variance () along with the actual variance permits the generation of a confidence level.

With the mild conditions presented in [Gretton et al. (2008)],

| (17) |

We show that, for a stochastic process composed of independent variables with an obvious simplicity and speed, the linear method for computing provides a very good approximation for . Among the methods presented, the linear method is the fastest, having a complexity of where is the number of points and is the number of dimensions of the series.

Kernels. In this paper, we use the Gaussian kernel as per [Borgwardt et al. (2006), Gretton et al. (2008)]

| (18) |

Note that this kernel function is parametric, where must be estimated from the data before the kernel can be used to compute the MMDs. Here we describe the process of computing . For all we first compute , , , . We compute the median for that will be the . Then, we compute the sum of the terms such as and thus the kernel value.

Having chosen a Gaussian method means that the kernel methods are very similar to Fourier methods and the Parseval–Plancharel theorem as described in [Meintanis and Iliopoulos (2008)].

The Section’s references are [Aronszajn (1950), Gretton et al. (2007), Borgwardt et al. (2006), Zhang et al. (2008), Biau and Gyorfi (2005), Gretton et al. (2006), Gretton et al. (2008), Meintanis and Iliopoulos (2008)].

3.4 Sorting and Distribution Functions in

This section introduces our original contribution to the field. It is based on the idea of creating a topological ordering of the data, generating an empirical cumulative distribution function, and then applying our statistical test. Given two arbitrary, empirical CDFs and , the test will generate a distance and a confidence level for said distance. These pairs allow us to quantify how similar or different the two distributions are. If is true, the two intervals have the same distributions, and that there is a high probability that they are instances of the same stochastic process. Section 3.5 contains a formal introduction.

Let us pose the questions of what means, and how a test can measure such a difference.

Recall that an empirical cumulative distribution function (CDF) for an interval means that for a given point , , where the ordering is satisfied for all components of the vectors y and x. Here, it is not necessary that belongs to interval or . Notice that means that for any we have the same number of points from each and , which is proportional to the size of each interval when creating the larger interval . This is the same idea proposed by the Mann–Whitney U statistics for testing whether one random variable is stochastically larger than another random variable [Mann and Whitney (1947)]. Our goal is to extend this idea to a multi-dimensional series.

In principle, if we can compute and , we can also apply the Kolmogorov-Smirnov test as is (see Section 4.2 and Equation 32), such that

| (19) |

This is possible because the Kolmogorov-Smirnov test is based on the image of the distance function, or the maximum difference of the distribution functions, and is independent of the domain dimensions. The weakness of this direct approach is intrinsic in the density of the domains and our ability to estimate the distribution functions. Simply, the larger the space is, the more points are required to estimate the real distributions to ensure that the test can discriminate properly between different distributions. In other words, if and do not have enough points to provide a good sample of the distribution function domains, then the test results are often inconclusive and the intervals are stochastically indistinguishable. This is often referred as the curse of dimensionality.

In the literature, there are new tests being developed to handle the case of multi-dimensional data. For these tests, we use the term statistical solutions to differentiate them from the methods we propose here. Instead, we will use the term algorithmic solutions to refer to our methods. We make a clear distinction of these methods in the following sections. In the following sections, we shall describe two methods that are designed to circumvent the problem of sparse samples by building on our understanding of single-dimension series anomaly detection without requiring the introduction of new tests. The first method is completely original, and based on the poset-sorting algorithm (Section 3.4.1), while the second method is based on the minimum-spanning-tree (Section 3.4.2). From our observations, we have noticed that CDF measures used for single-dimension series are easily applied, and build upon well established statistical and computational grounds.

3.4.1 Partial Ordered Topological Ordering

In the previous sections, we introduced the definition of distribution functions and showed methods for comparing two empirical distributions. Recall, that the definition of a distribution function is based on the concept of order among the points in the interval. In other words, , where this condition is true for all components when a point is actually a vector with .

For , the condition is always defined as either true or false. For , cases may exist whereby the inequalities and are both not defined. In this case, the two points are parallel and denoted as . This is a partial ordered set or poset.

The computation of the empirical distribution function turns out to be exactly the same computation as the length of all the paths in the poset (without repetition). It should be clear that building the poset from and is based on a poset sorting algorithm which creates links between those points for which the relation ’’ is defined. Once the poset is generated, given a point, we can compute the number of points satisfying the relation ’’ (i.e., the distribution function). We should emphasize that the parallel points, those for which ’’ is not defined, are not used in the distribution comparison.

Given two intervals and with points of dimension , a poset-based sorting algorithm can be used to build a poset directed acyclic graph (DAG). We implemented a variant of the sorting algorithm in [Faigle and Turán (1988)] as described by [Daskalakis et al. (2009)], which has a complexity of where is the maximum number of parallel points. In practice, we take advantage of the lexicographical order of the points to further reduce the complexity by a constant. We did not implement or test the faster version suggested in [Daskalakis et al. (2009)].

Given the set of points in and , a source point always exists from which all other points in the DAG can be reached; also, a sink point always exists that can be reached from all other points. In fact, each dimension of a vector can be defined as such that , and each dimension of a vector can be defined as such that . Such points can always be added to the poset above.

Remarks. Once the poset DAG is generated, the computation of the empirical distribution is trivial, as the points that satisfy the relation ’’ can be easily computed for each point in the DAG. Unfortunately, the use of these distribution are not practical, because for points close to a large variation may occur as a result of the ordering method chosen. Let us explain this problem: from any point in the DAG we can always reach , this implies that the distribution value of ; if we reach from above the cluster of points, the distribution will likely increase in small steps because we are counting also parallel node, but if we reach from below the cluster, the increase will be much faster because parallel nodes will counted only very close to ; it implies that the distribution may have large variation as a function how we approach in its close neighborhood. This would result in the method falsely identifying all intervals as different, even for processes with small dimensions. This problem can be resolved by taking into account the neighboring parallel points.

The question becomes one of how we can derive a strong order from a partial order. This would permit the use all points and thus the parallel points for the comparison as well.

We create a topological ordering by using a breadth-first search algorithm to traverse the points from to . The topological ordering is an ordered and unique partition of the graph (the union of both intervals with a possible intersection):

The topological ordering infers a strong order between points in and where . Furthermore, a strong order within can be inferred by using a lexicographical ordering because points in are parallel points, and thus the strong order extension is arbitrary and harmless as long as is small, having few points666If is large, any predefined order will skew the comparison. Let us associate the color red with the points from and the color white with the points from . Using the topological ordering of the graph, we can perform another breadth-first search to compute the empirical distributions for and such that and . Then is the number of red points that appear before in the breadth-first search divided by the total number of red points. is similarly defined for the white points.

To perform the breadth-first search, we visit each edge of the poset DAG, which theoretically takes , but on average is closer to . Notice that this approach to ordering can be applied, without modification, for an arbitrary number of intervals.

By using a topological ordering, the construction of a density function is circumvented; thus our data partition is implicit within the ordering. As the sample space is not explicitly partitioned (as the authors recommend in [Wang et al. (2005)]), bins may contain just a single point. This is not a problem, as we are interested only in their cumulative contribution. Now, we can apply any single-dimension non-parametric approach, including those describe in Section 3.5.

Remarks. Given a poset derived from and , the topological ordering is also known, and the partition is unique as will be explained shortly. We can identify the sets as bins, and can think of the partition as a histogram induced by the topological ordering of the data. Each bin contains parallel points, where the maximum number of parallel points, or the height of the bins, is referred to as the parallelism of the poset. We do not differentiate between the points in based on the ordering when considering the bins. Hence, we consider this partition representative of, and unique across all partitions that can be obtained by any point permutation of the bin .

In other words, if and are obtained from the same stochastic process, then the set in the topological ordering should have an even mix of red and white points. For this partition to be effective, the parallelism of the poset should be small and the number of bins large. Otherwise, each bin will not have an even mix of points and we will end up with a few bins with high parallelism. This result is undesirable, because it means that the ordering within each bin will be based on the lexicographical order, which is arbitrary and provides no real information. This discussion is not restricted to the lexicographical ordering, but extends to any fixed ordering of the points performed without any prior knowledge of the data.

The main limitation of this method is the inverse relationship between the number of points and the number of dimensions. For example, if we study 20-point intervals from a series with 500 dimensions, then the probability of building a meaningful poset is very slim indeed, with a high probability that all 40 points are parallel. As a result of the high degree of parallelism, it is not possible to infer any ’’ relations amount the points. We will show that this poset approach is ideal for series with less than 10 dimensions, if the intervals consist of about 200 points each.

Remark. A natural extension of this method would use the dominant direction of the data instead of the fixed one used by the poset sorting algorithm, and then define the ’’ ordering accordingly. For example, one could use the direction of the dominant eigenvector to describe a new ordering, or to perform a domain rotation, which would facilitate the use of the regular sorting method. Where possible, the easiest solution is to increase the number of samples accordingly.

Remark. A multi-dimension problem is reduced to a single-dimension problem by using comparisons and counting. The capability of this method can be extended by using the quantitative contribution of each dimension distance instead of a bare comparison. In the next section, we will introduce an approach that extends the poset-based method to work on series with thousands of dimensions by quantifying the distance between points based upon the contribution of each vector component.

Remark. The appeal of the poset-based topological ordering is that poset ordering reduces to the usual ordering when applied to a single dimension series.

3.4.2 Minimum-Spanning-Tree Based Topological Order

In this section, we examine the use of a well known approach used in the determination of clusters: the minimum-spanning tree (MST) as proposed by Friedman and Rafsky [Friedman and Rafsky (1979)].

Given two intervals, and , in a series with dimension , an MST can be built using Dijkstra’s algorithm. This method involves computing the distances between each of the points in and (i.e., distances or edges for points), sorting the edges in increasing order according to their distance, and then attempting to insert each edge into the tree provided it does not create a loop. If the introduction of an edge would result in a loop, it is ignored. This process is continued until all points have been added to the tree, which produces the MST.

The most expensive part of the computation is the computation of the distances, which takes .

In general, an MST is not necessarily unique, but it is the minimum-cost tree connecting all points. The leaves of the MST are easily recognizable because these are all the points with only a single edge. By conducting a breadth-first search from the leaves it is possible to build a topological ordering and the partition :

Because the search is started from the leaves, it is possible to end up with either one or two roots. Notice that the partition can be determined in steps, as the tree is a DAG with edges.

The partition that is generated from the MST derives a strong ordering among the points, but without a fixed orientation, which makes it more resilient to the dimensionality of the space than the poset topological ordering. In our implementation points in a bin are parallel and ordered lexicographically, instead of in decreasing order of the distance from the root [Friedman and Rafsky (1979)]. This choice simplifies the computation at the expense of possibly biasing the comparison.

With a partition, and thus a strong order, the empirical distribution functions can be inferred. The distributions allow us to perform the statistic tests that we will explain in the following section.

Remark. The MST-based topological ordering derives its order from the data points and adapts to them; ordering the points from the outskirts of the cluster towards the center. As noted, the poset-ordering method is positively correlated to the number of points and negatively correlated to the number of dimensions. In other words, it is more sensitive to series with a small number of dimensions and a large number of points. In contrast, the MST-based ordering method is less sensitive to the number of points and more sensitive to the number of dimensions. This difference arises from the fact that an increase in dimensions contributes to the distance between points; thus, the ability to differentiate between points becomes more sensitive.

In [Friedman and Rafsky (1979)], the authors deployed the Wald–Wolfowitz test and the Smirnov test on MST data. Briefly, the Wald–Wolfowitz use a coin based test: head, we visit a node in and tail, a node in ; a path in the DAG should have the distribution of a sequence of coin tosses. The Smirnov test is basically the comparison of distribution using the Kolmogorov-Smirnov’s test. In this section we will describe the Radial Smirnov test, for which the original authors showed evidence of its power in finding changes in the variance, as opposed to tests which can identify changes in the average. We have chosen to postpone the implementation of the Wald–Wolfowitz test because of contradicting evidence of its effectiveness. Early literature [Siegel (1959)] suggests that the Kolmogorov–Smirnov method is preferable to the Wald–Wolfowitz method; while more recent works [Magel and Wibowo (1997)] paint a more complex picture (even for very small samples of up to ). Finally, the [Gretton et al. (2008)] manuscript suggests that both methods tend to break down for large dimensions. We are aware that the original implementation using MST and the Wald–Wolfowitz test may provide better discriminative power due to its sensitivity of changes of the average (see Section 7.1).

3.4.3 Single Dimension, Poset, and MST

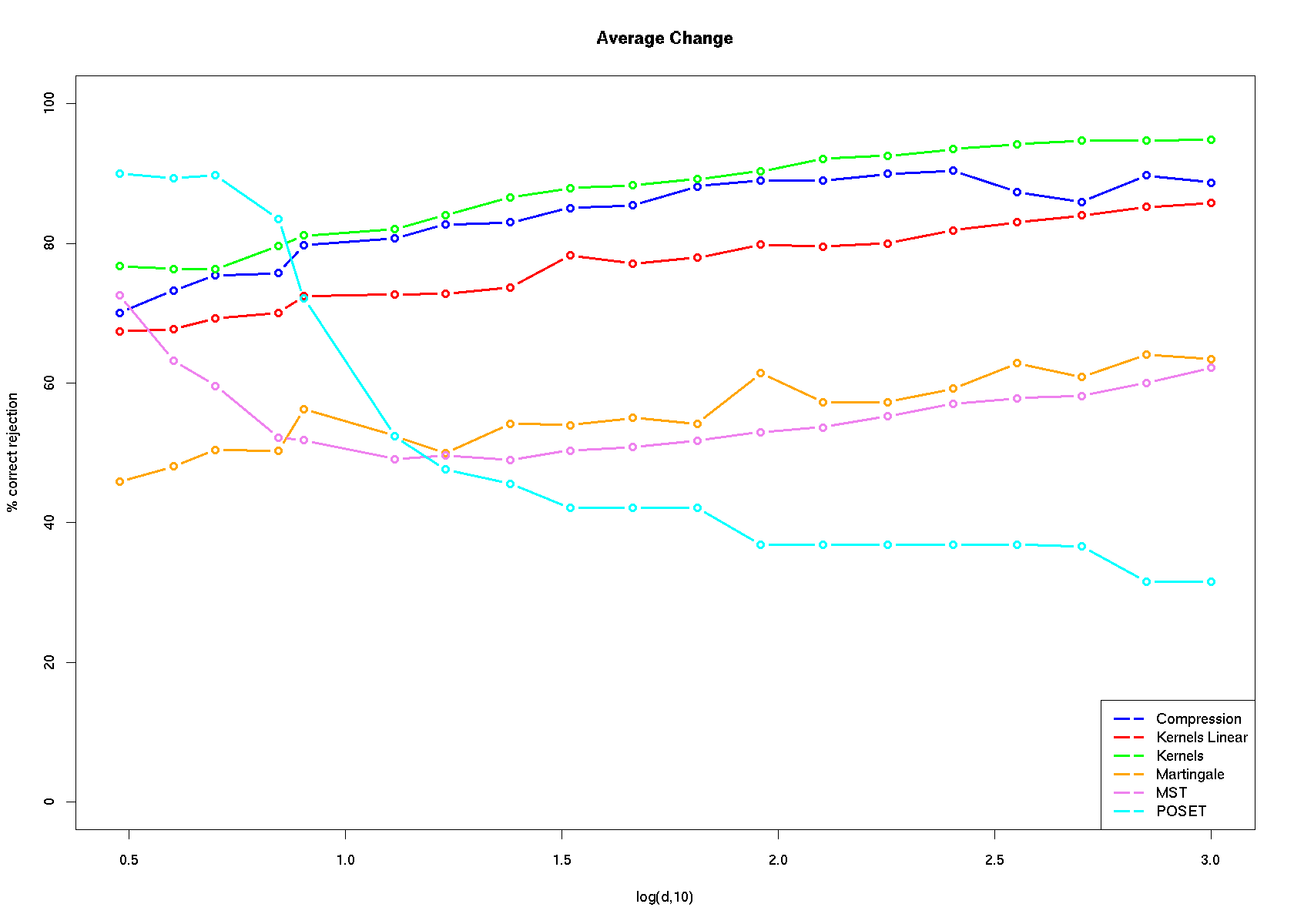

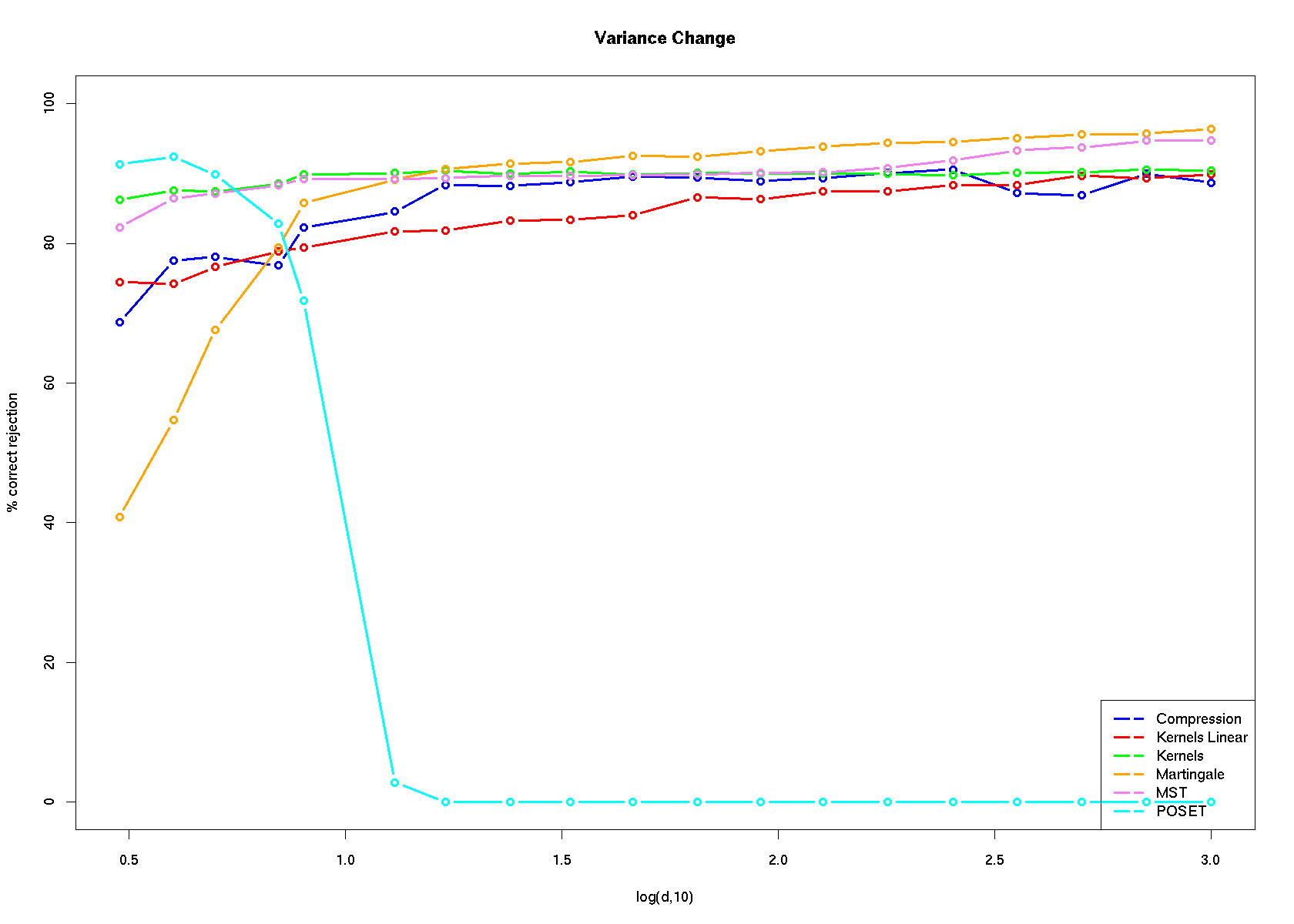

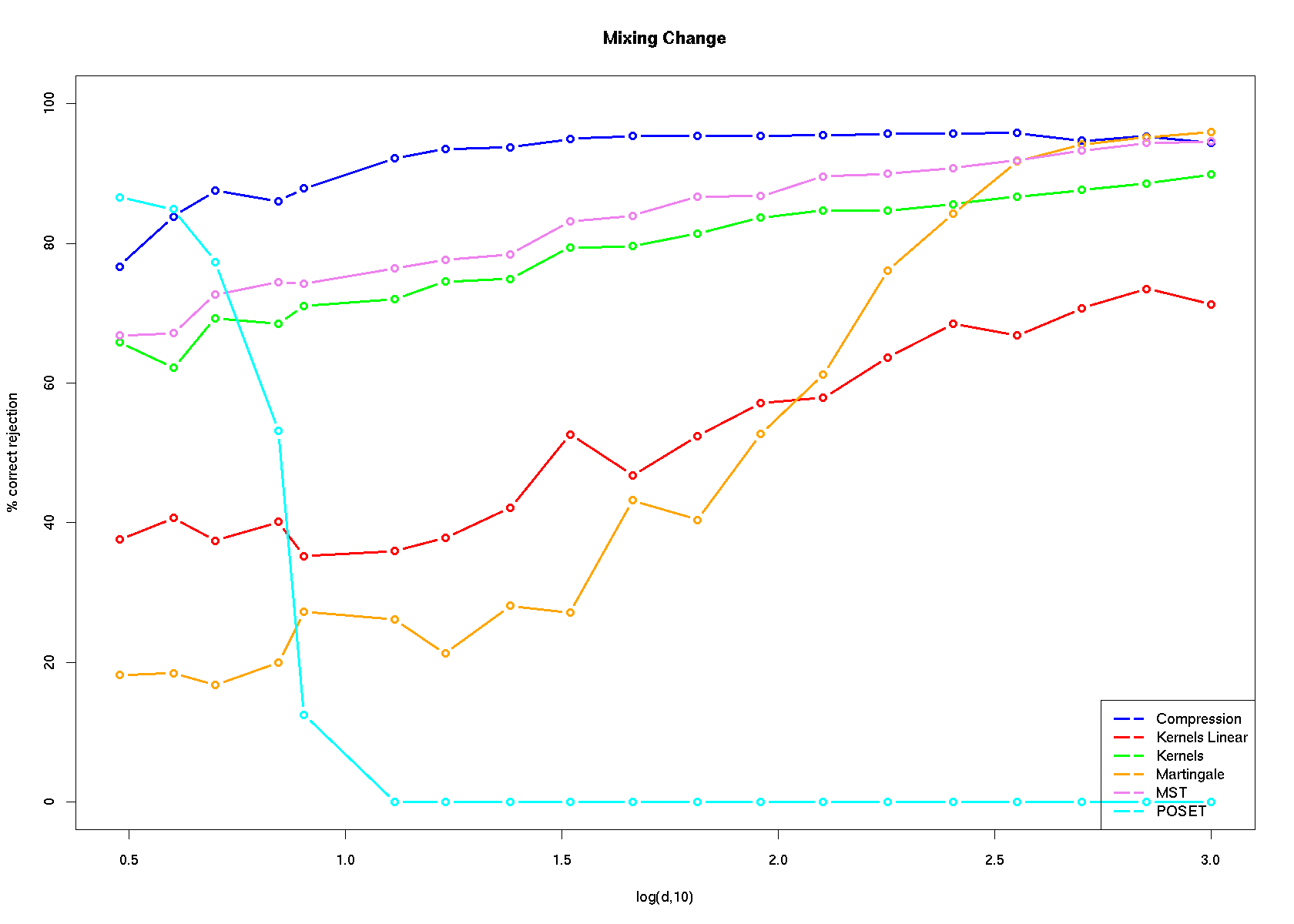

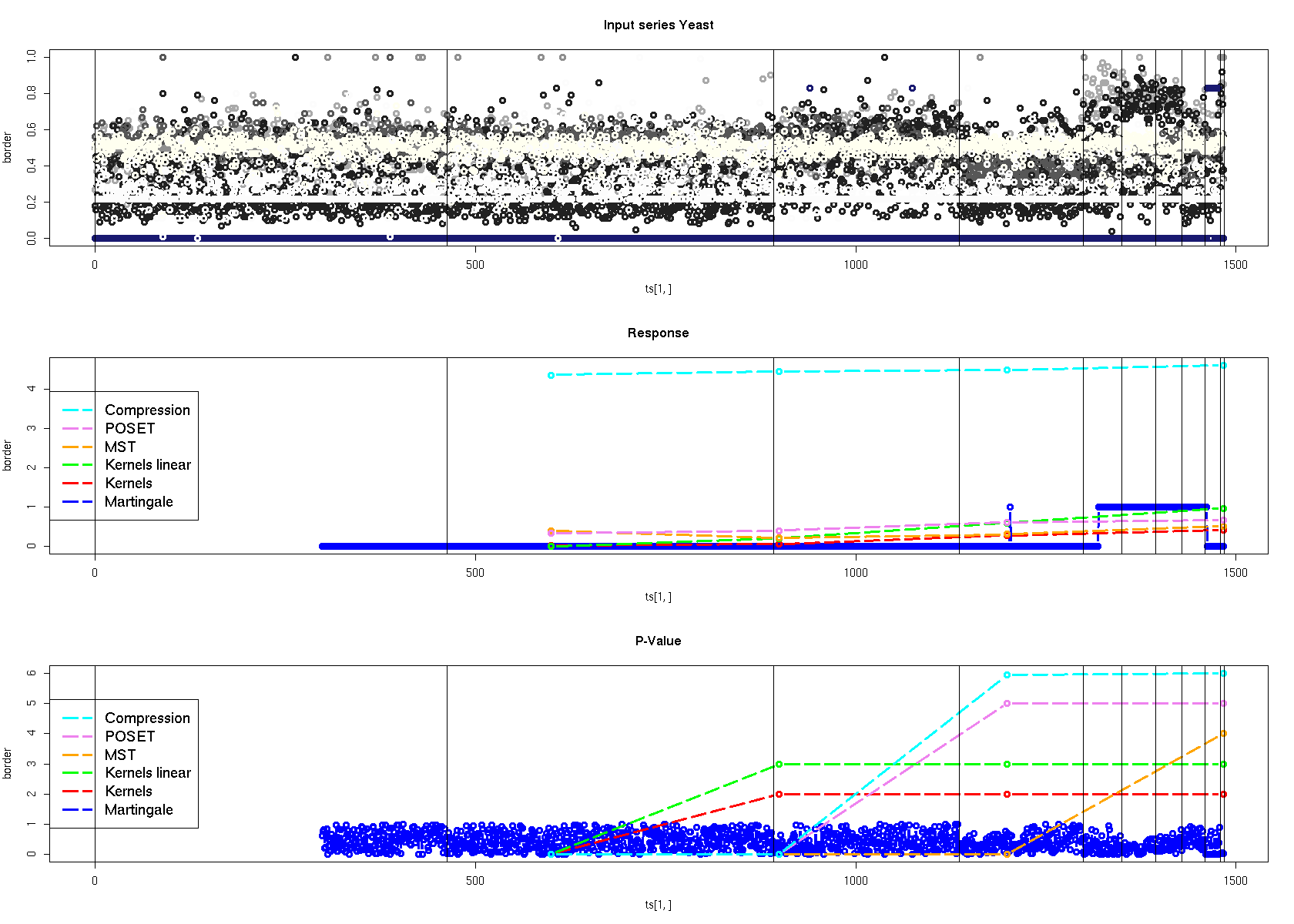

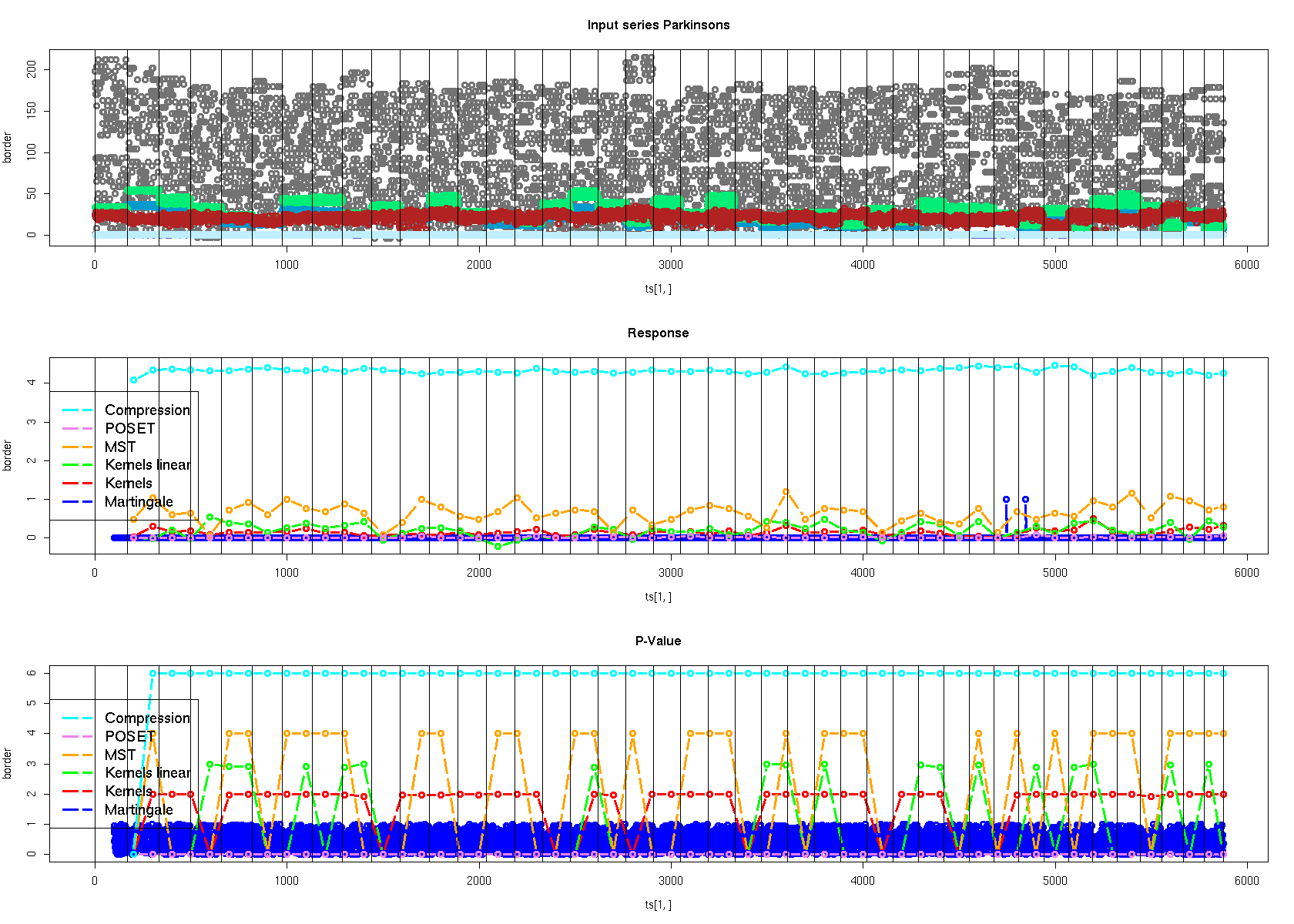

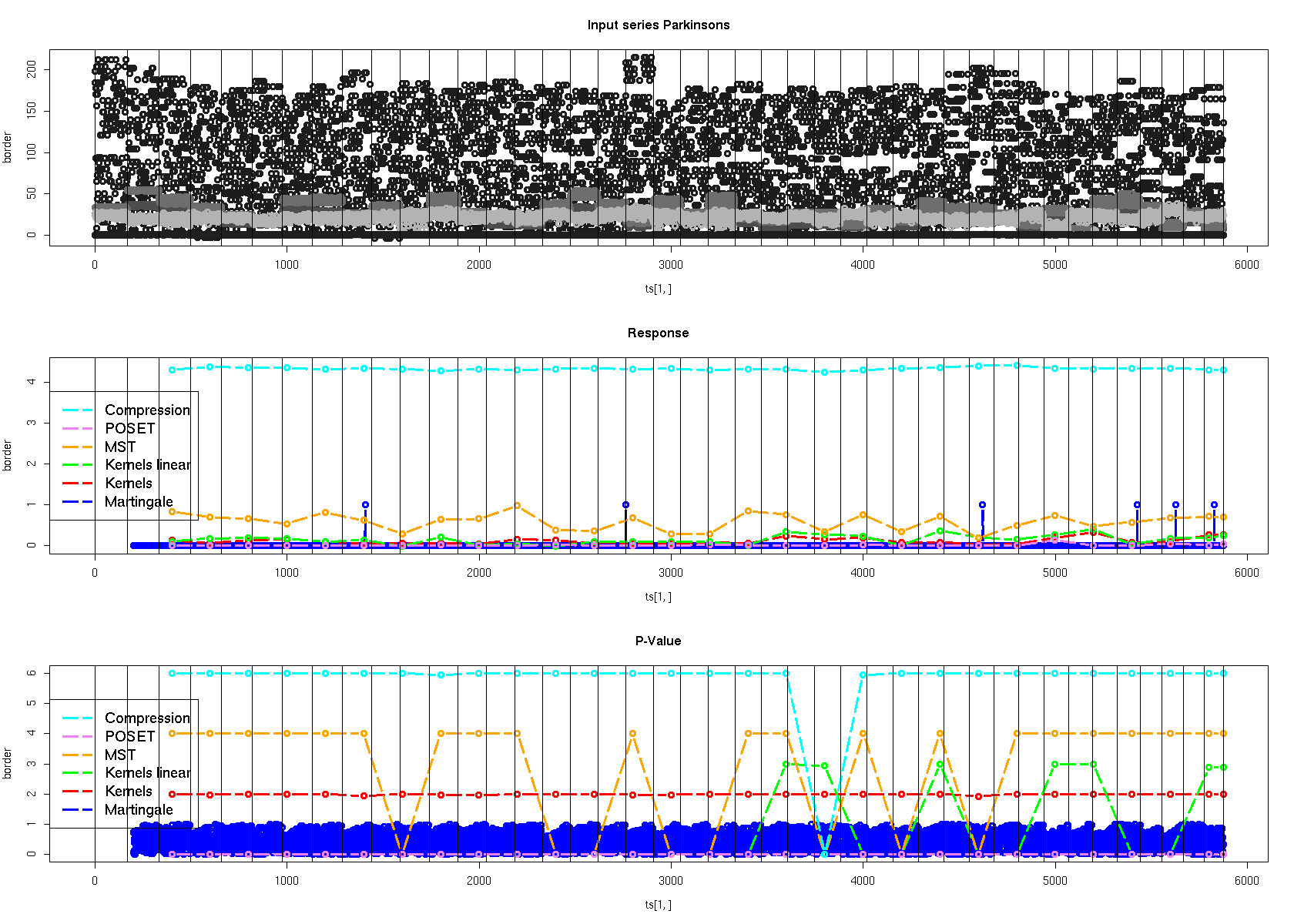

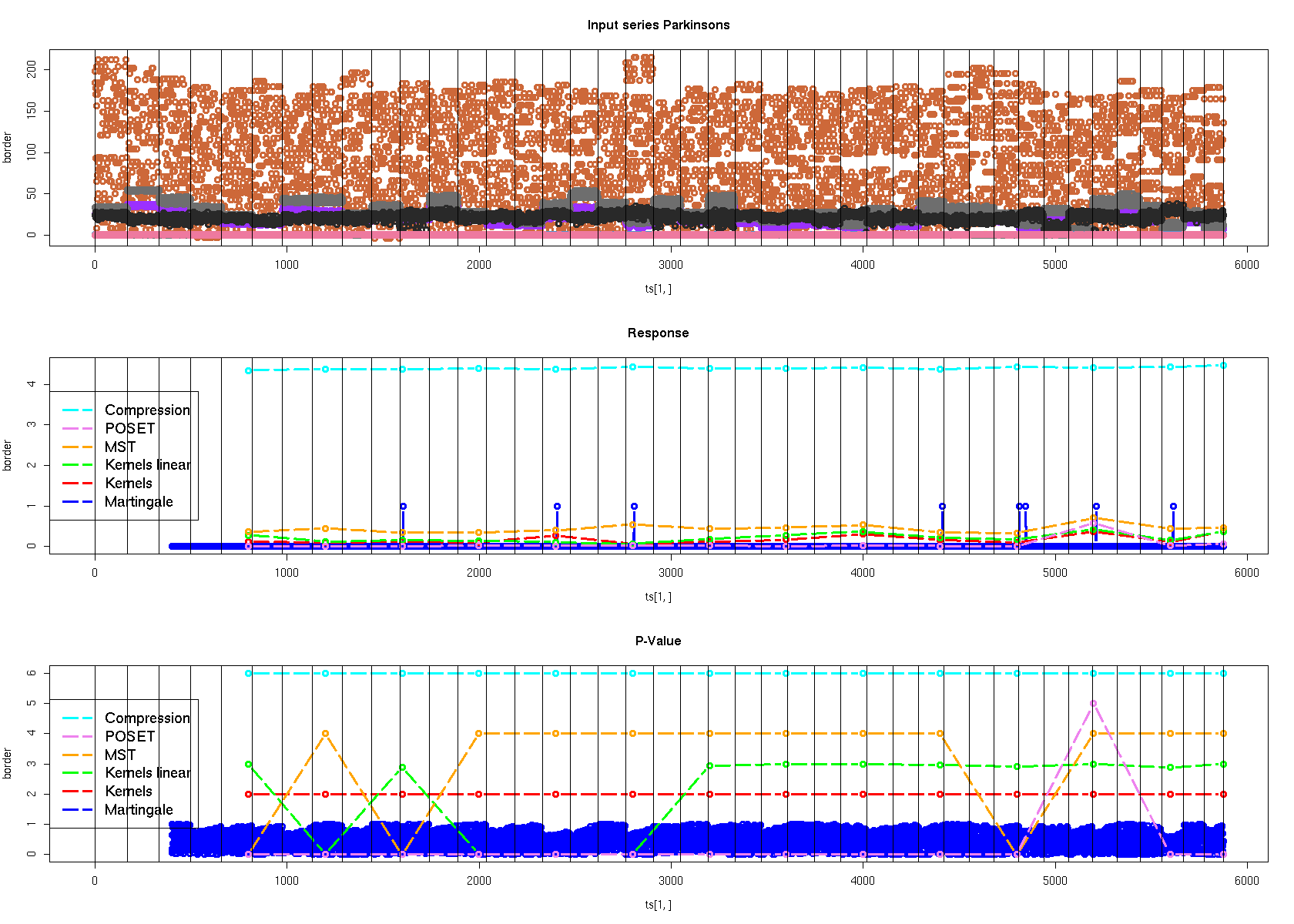

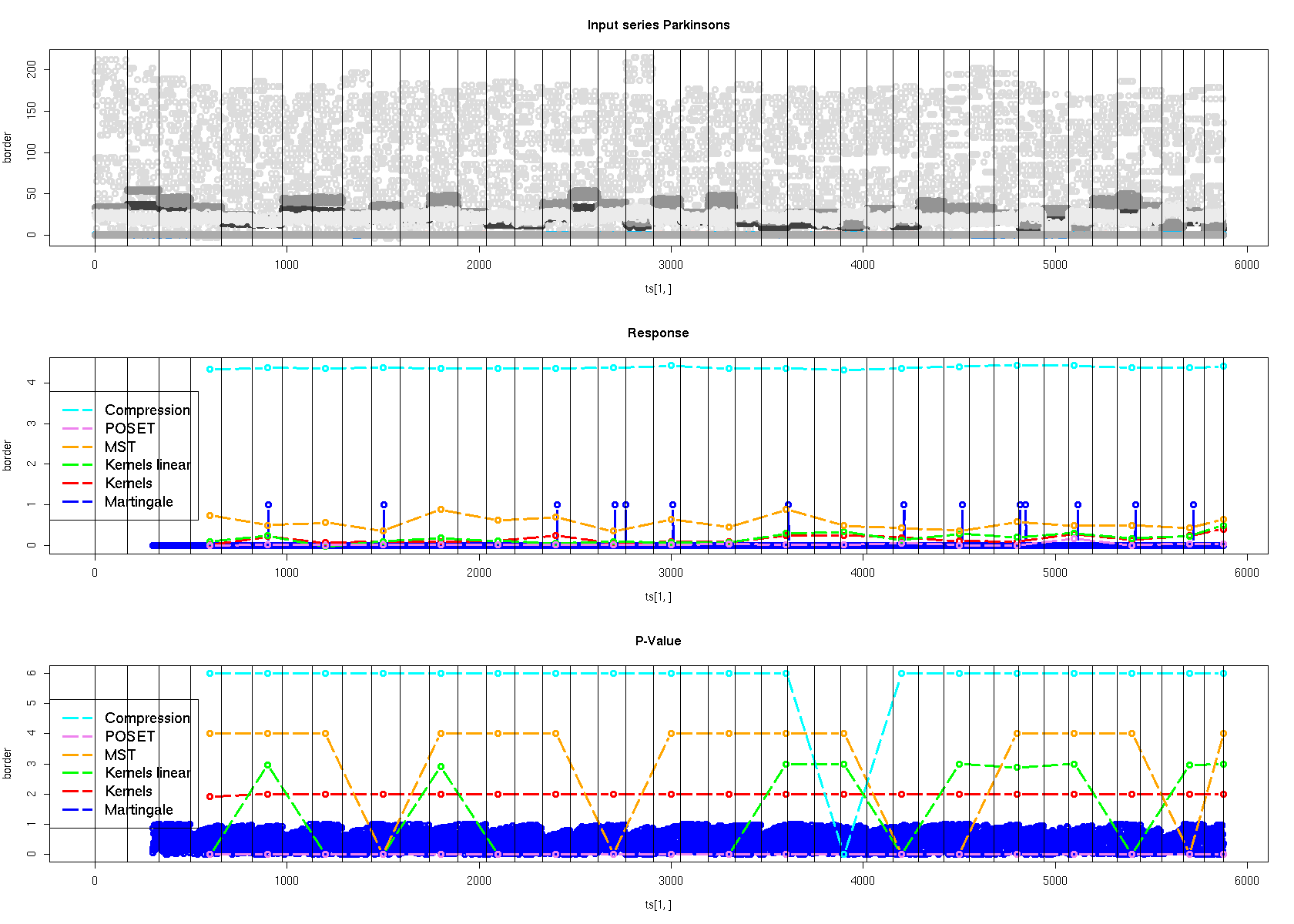

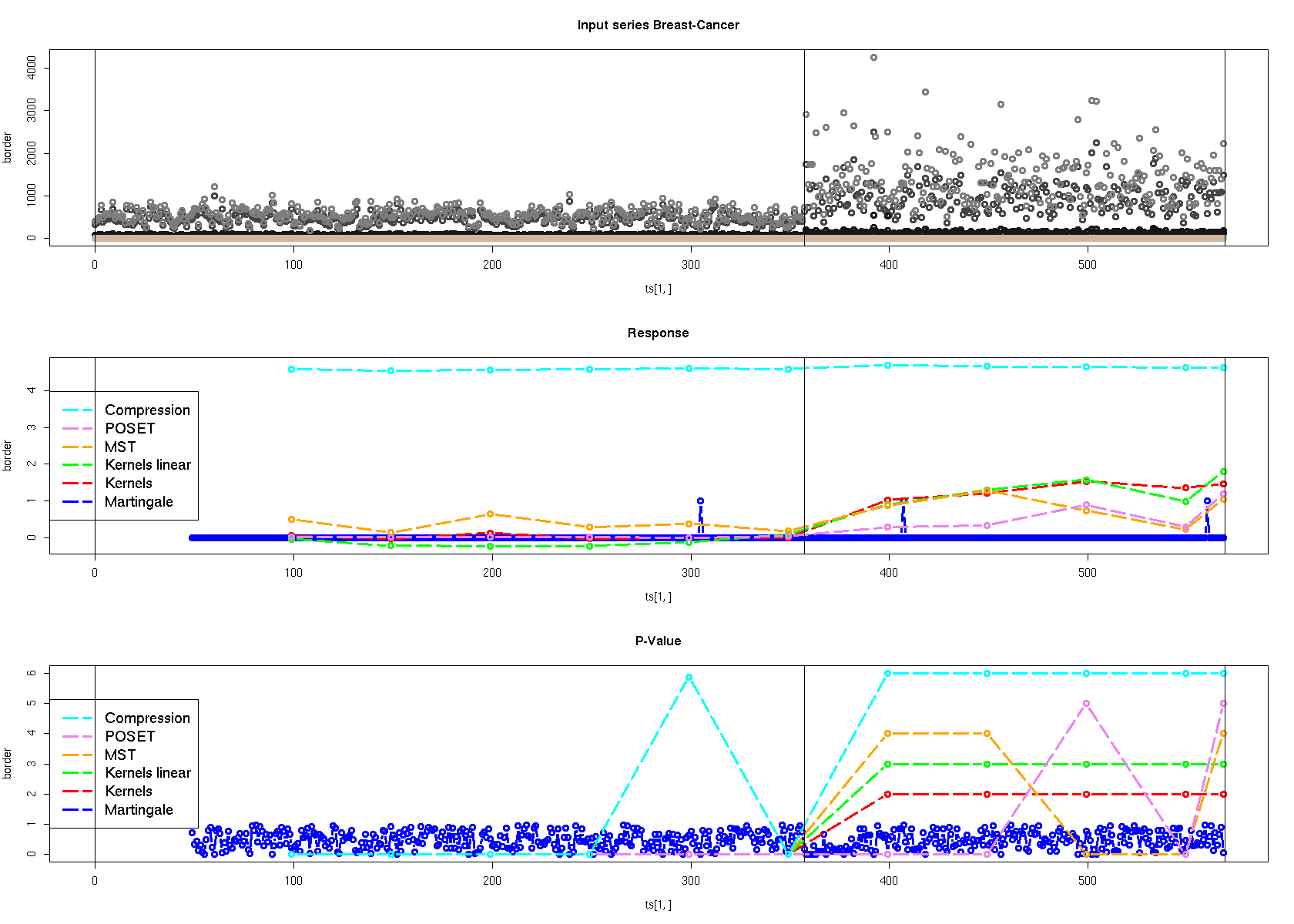

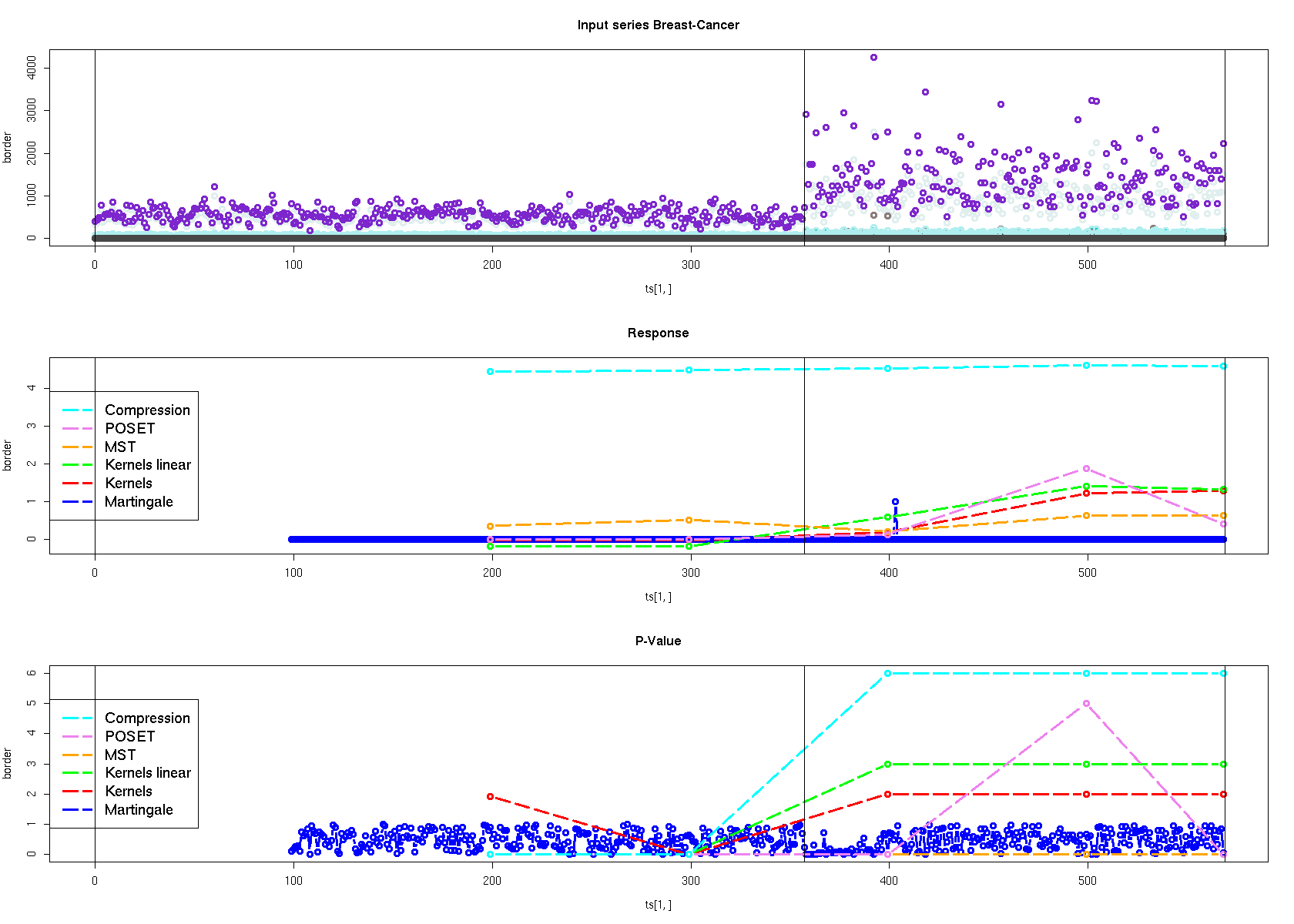

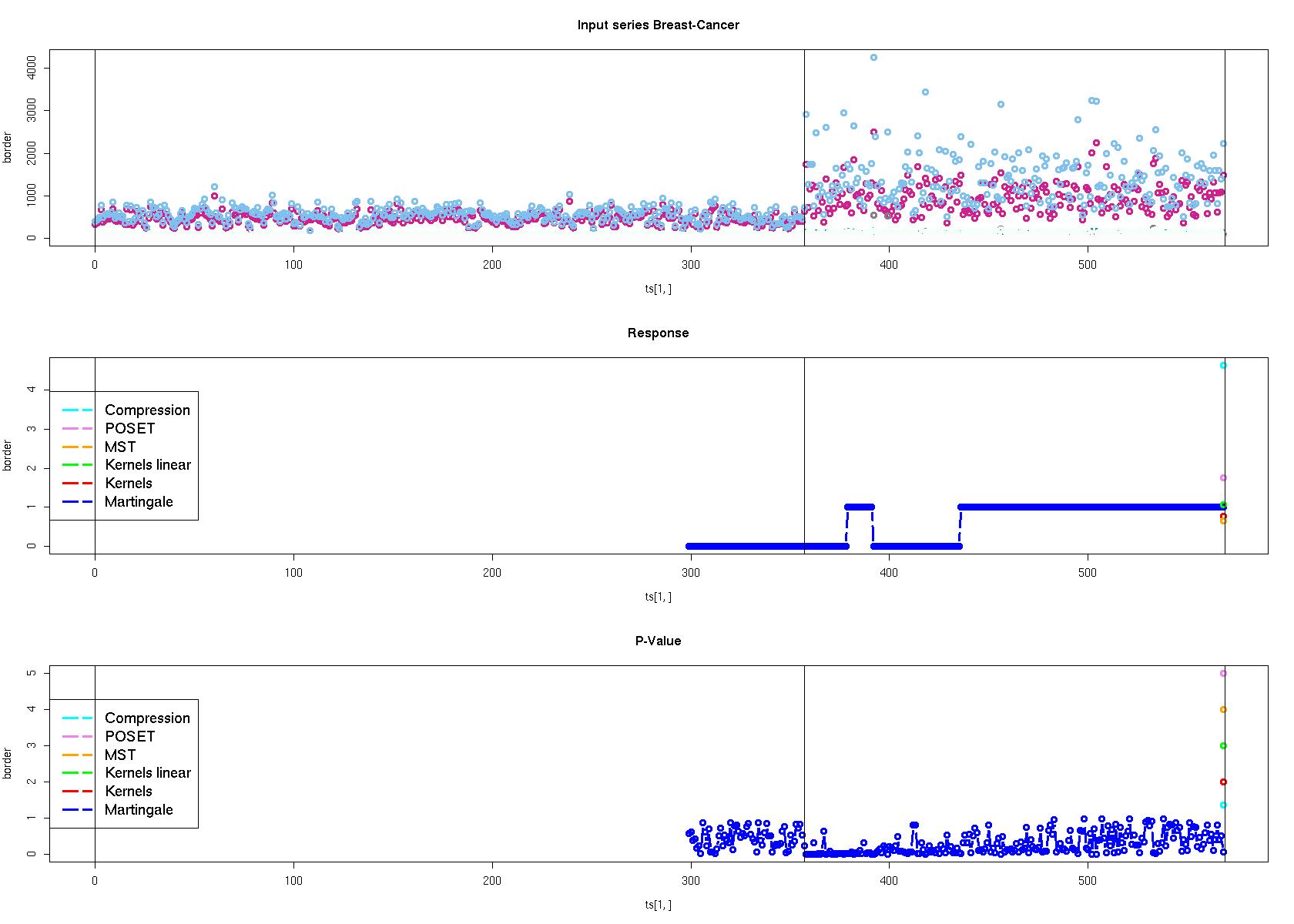

In the experimental results Section 7, we will compare the discriminative powers of all these methods. We will show that the poset-based method performs better than any other method on data with 10 or fewer dimensions, excelling in speed and discriminative power with respect to changes in both the average and variance. The MST-based method performs better on data with 10 or more dimensions and when detecting changes in variance. We will show that for changes in the average, we are better off using other methods.

This section’s references are [Friedman and Rafsky (1979), Hall and Tajvidi (2002), Kim and Foutz (1987), Bickel (1969)].

This Section’s reference are [Müller (1997), Song et al. (2007), Dasu et al. (2006), Sriperumbudur et al. (2009), Kulldorff et al. (2007), Bickel (1969), Bickel et al. (2006)].

3.5 Single-Dimensional Series: Statistical Test, Unified Measure, and Notations

We start by introducing the terminology and definitions used from hereafter.

Given two arbitrary empirical CDFs and , a non-parametric statistical test is composed of the following three components:

-

1.

The null hypothesis : the assumption that the distributions are the same.

-

2.

The measure : it quantifies the distance between the distributions. Here, the term “measure” is used after the same fashion as [Ali and Silvey (1966)].

-

3.

The statistical significance: it is the probability of judging the CDFs as different but they are similar; typically, we will consider significance levels at 0.05 but we can make it closer to zero in order to make the comparison stronger.

In the following, we shall work with measures that are suitable to capture similarity, thus designed to confirm the null hypothesis. In the literature there are available measures that are more suitable to capture difference and thus to confirm the complementary null hypothesis (). These difference measures can be always added but for now they are beyond the purpose of this work. We shall show that similarity measures are more suitable for the framework we are going to build.

Unified Measure. We present a generalized measure that unifies all the measures in this paper. It also helps us to abstract the components of a measure and provides a notation for them.

| (20) |

In Equation 20, the measure takes in the -element vectors and , which represent the input distributions and respectively. It produces the final output by performing these four steps:

-

1.

Compare the elements of the input vectors on a one-to-one basis using the function .

-

2.

Aggregate the results using a vector -norm .

-

3.

Scale the result using the function .

-

4.

Normalize the result using the function so that the final result will be independent of for large .

Each of the functions in the definition of takes different forms for different measures, as shown in Table 3.5. The only exception is the vector -norm, which is defined as follows:

Notice that the definition of is not standardized in the literature. For example, in [Golub and Loan (1996)] is ; while some other sources refer to as the number of non-zero elements of . Our vector norm helps simplify the definition of .

We compute the distance between the two windows and using , as defined in Equation 20. To compute the distance, we can use the input vectors for these windows to represent an empirical PDF or an empirical CDF.

4 Distance Measure Specification

For a finite number of samples, a measure is the quantitative comparison of the distance of two vectors. For example, the Euclidean distance of two -dimension vectors is a norm and a metric; that is, , and . In this spirit, we can extend the measures commonly used for vectors —i.e., the Euclidean distance— or for PDFS —i.e., information-theoretic measures— and apply them to CDFs as inputs.

Let us consider the case when we want to compare two series in . We can always define intervals using CDFs, which means we can always compare two CDFs as vectors, or without any arbitrary determination of buckets or reduction to discrete values. Moreover, two series drawn from the same process will converge to the same CDF (to the same vectors or PDFs), and all the measures will converge to zero.

However, the measure output for different CDFs can be literally bounded only by the number of points in the comparison, and, certainly larger than in the case of PDFs; for example, for the measure in [Lin (1991)] otherwise most PDFs measures are always smaller than one.

Symmetric measures, such as the Kullback–Leibler–J Equation 22, the Jensen–Shannon Equation 24, or the Variational Equation 28, are more suitable for our needs. In fact, the symmetry property ensures that the measure is not biased by the reference window and both windows can be interchanged if necessary. Nonetheless, we can find applications for positive asymmetric measures, such as in Equation 25, because these measures offer better discriminative power when applied to empirical distributions, especially when observations are few or when the reference is more trustworthy than the running window [Lee (1999)].

We show that 17 of the measures in Table 3.5 generate output CDFs that are independent of the input CDFs. For example, the Kolmogorov–Smirnov measure has a limit distribution that is normal, independent of the input stochastic processes. In Section 5.3 we explore this independence, explain the reason for using the Kolmogorov–Smirnov measure and present experimental evidence. Unfortunately, we found that the generalized functions , , and , used by the PDFs (Equation 30, 29, and 31), tend not to work for the CDFs, because we cannot find a CDF for their output measures (see Section 5.2).

Finally, we must clarify that there are several measures which we chose not to investigate, these include the geometric measure, the relative frequency model, and the resistor distance. We did not use the geometric measure [Wang et al. (1992)], [Jones and Furnas (1987)], because the measure only compares the direction of two vectors without considering their magnitude, which we consider important. [Shivakumar and García-Molina (1995)] proposed the relative frequency model to overcome the drawbacks of the cosine measure when used with histograms built from a set of discrete entities that are easily classified into buckets, such as a bag of words. The resistor distance is described in [(41)] and is an alternative symmetric version of the Kullback–Leibler measure.

4.1 Information-Theoretic Measure Extensions

In this section, we present our contributions to the field of information- theoretic measures. We will detail how we have extended these measures and applied them to CDFs.

Kullback–Leibler-I (KLI) [Kullback and Leibler (1951)]. KLI is an asymmetric measure where , which assumes that undefined values have no contributions. Notice that iff ; however if , can be arbitrarily large.

| (21) |

Kullback–Leibler-J (KLJ) [Kullback and Leibler (1951)], [Ali and Silvey (1966)]. KLJ is a symmetric measure where . The KLJ measure is similar to the KLI measure in that iff , and if then can be arbitrarily large.

| (22) |

An alternative example of a symmetric adaptation of KLI is described in [(41)].

Jin-L (JinL) [Lin (1991)]. JinL is a symmetric measure that is always defined, assuming that . iff ; otherwise, will not be larger than if .

| (23) |

Jensen–Shannon (JS) [Jensen (1906), Shannon (1948)]. We describe JS using the Kullback–Leibler measure; however, the JS has historically been formulated using the entropy measure (i.e., ). We use Kullback–Leibler as the generalization of this entropy.

| (24) |

() [Kagan (1963), Vajda (1972), Hope (1968)]. is an asymmetric measure that is defined for ; again, the contribution is not considered when . Notice that iff ; however, if , can be arbitrarily large.

| (25) |

Hellinger (H) [Hahn (1912), Vajda (1972)], [Ali and Silvey (1966)]. H is a symmetric measure that is always defined. The square root operation normalizes the component values to ensure that the component-wise comparison is less biased. The value of all components are between 0 and 1, but components near the extremes (0 or 1) are moved closer to . Notice that iff .

| (26) |

Bhattacharyya (B) [Bhattacharyya (1943), Kailath (1967)]. B is a symmetric measure that is always defined. Notice that iff , and will tend towards 0 if , . Also, if applied to the PDFs and , Bhattacharyya and Hellinger measures are related in following manner: . However, for CDFs, Hellinger is more suitable because we can determine a significance measure. Bhattacharyya is presented for completeness.

| (27) |

Variational Distance (V) [Pinsker (1960), Ali and Silvey (1966)]. V is a symmetric measure that is always defined. Notice that iff ; however, if then will be no larger than . This measure is also known as the Manhattan measure or Kolmogorov’s variance distance [Ali and Silvey (1966)].

| (28) |

For the remaining measures, we use the following notation [Chernoff (1952)] to refer to the sum .

Generalized () [Taneja and Kumar (2004)]. is a generalization of measures that are based on the Kullback–Leibler methodology.

| (29) |

Generalized () [Taneja and Kumar (2004)]. For specific values of with PDFs, can generate Bhattacharyya, Hellinger and Kullback–Leibler.

| (30) |

Generalized () [Taneja and Kumar (2004)]. For specific values of with PDFs, can generate Bhattacharyya, Hellinger, Kullback–Leibler and .

| (31) |

Notice the equivalence relations and , where and are PDFs. Although we present , , and for completeness, we could not find a significance measure for most methods, excepting and a few others.

4.2 Classic Distribution-Function Measures

Here we present the set of measures from the literature that already use CDFs.

Kolmogorov–Smirnov (KS) [Kolmogorov (1933), Kendall (1991), Feller (1971)]. KS is a symmetric measure that is always defined. Notice that iff ; and if then is no larger than 1.

| (32) |

() [Kifer et al. (2004)]. is a symmetric measure that is always defined. Notice that iff ; and if then is no larger than 2.

| (33) |

() [Kifer et al. (2004)]. The is a symmetric measure that is always defined. Notice that iff ; and if then is no larger than 2.

| (34) |

Cramér–von Mises () [Melucci (2007)]. is a symmetric measure that represents the Euclidean distance of a vector. Notice that iff ; and if then will be no larger than (the number of samples in the window). Recently, a new definition has been proposed [Melucci (2007)] that does not follow the original definition by Anderson[Anderson (1962)] exactly.

| (35) |

Minkowsky () [Batchelor (1978), Wilson and Martinez (1997)]. is a symmetric, parametrized measure that generalizes both the Euclidean () and Variational () distance of a vector. Notice that iff . In our experiments, we set .

| (36) |

Camberra (C) [Diday (1974), Wilson and Martinez (1997)]. C is symmetric, and a relative measure of the Euclidean distance, in the same fashion that is a relative measure of the Kolmogorov–Smirnov distance. Notice that iff ;

| (37) |

4.3 Rank Function Measures

For the sake of completeness, we discuss a few other measures which are based on rank measures for a single-dimensional series. These methods are used for the comparison of experimental results to show that our measures have comparable discriminative powers. That being the case, it means that we could use them instead of, or in combination with the following measures. Of course, these measures are not clearly defined in the case of multi-dimensional series.

Wilcoxon-Mann-Whitney (Wilcox) [Wilcoxon (1945), Mann and Whitney (1947)]. Wilcox is a symmetric test that is based on the rank of the events that occur in each series. This is a standard test that is available in R. We also used the t-test.

5 Significance or -value of a Measure

For some measures , the distribution of the measure values is well studied. Some examples include for CDFs generated from windows with points, or for PDFs with buckets. For others, the distribution can be determined by simulation, as in the case of or . Our goal is to pre-determine the measure distribution and thus the measure significance through the use of tables or simulations. We could use bootstrapping instead; bootstrapping is a powerful approach, computable on the fly, and adaptable to any series; however, it requires a training set and, therefore, an a priori knowledge of the series. This extra knowledge makes bootstrapping inconvenient for the final user of these statistical measures; the final user simply wants the measures to describe the data.

We have found, through empirical testing, that simulations are sufficient in determining a simplified distribution and thus the significance for most of the measures used in this paper. However, we were not able to find a distribution function for the following measures:

-

1.

KLI, because it produces negative measures.

-

2.

Bhattacharyya, generalized , , and , because we could not find a normalizing function (see Table 3.5), and thus a CDF.

5.1 Simulation, , and its CDF

Simulation of the expectation for the null hypothesis measure(i.e., ). 100 1000 10000 100000 1000000 E[] 0.28269 0.09925 0.03391 0.01141 0.00374 E[] 0.30643 0.10466 0.03523 0.01169 0.00383 E[KS] 0.11867 0.03830 0.01227 0.00383 0.00124 [Feller (1971)] E[KLI] 1.95563 1.00179 1.76800 -0.10939 51.66521 N/A E[KLJ] 2.87245 2.84168 2.94492 2.81301 3.06639 constant E[JnK] 0.63525 0.14532 0.51653 -0.40636 25.44923 N/A E[JinL] 0.74388 0.71258 0.73634 0.70326 0.76659 constant E[JS] 0.37194 0.35629 0.36817 0.35163 0.38329 constant E[] 2.11921 2.00276 2.04105 1.95051 2.12593 constant E[V] 8.88756 28.09942 89.08333 272.74629 915.27286 E[H] 0.26507 0.24784 0.25529 0.24374 0.26568 constant E[B] 100.23492 1000.25215 10000.24470 100000.25625 1000000.23429 E[W] 0.67146 0.66599 0.67193 0.63212 0.71241 constant E[E] 0.76166 0.75571 0.75984 0.73908 0.77774 constant E[] 0.35486 0.23930 0.16416 0.10910 0.07781 E[C] 16.74404 54.79298 177.49281 557.46331 1809.98318

The simulation process can be described as follows. We select a measure , choose the number of samples , and then randomly generate pairs of samples each, as taken from the same stochastic process. One example of a simulation run might use the following parameters: , , .

We generate a CDF from the measure values , which is denoted as . Repeating the simulation times results in different CDFs for , which produces a cloud of functions . By extension, changing the number of samples , results in clouds of functions, . For any number of samples , we want to determine the normalizing function that makes it possible to compare the measures with respect to other sample sizes, . In Figure 1, we show the simulation results of , where , for different sample sizes , and the resulting cloud of distributions.

To rationalize the deterministic nature of with the stochastic nature of the measure values, it is necessary to estimate . To do so, we use . This is the average distance for the different measures when no normalizing factor is applied, see Table 5.1. Then, we apply the values to the measure . Before proceeding further, a bibliographic note about how to estimate the average is in order. The estimate boils down to the properties of a random walk and the area beneath its path. Even though there is no clear and complete treatment for all the measures, our experiments confirm the results in the literature for the variational distance , see [Harel (1993), Takács (1991)].

The simulations generate CDF clouds as a function of . We define a representation of the behavior of the CDF of the measure as a stochastic function

| (38) |

where is an estimate of the representative CDF and is a function representing the confidence about the representative function.

We assume that we have found a representative distribution when at least 90% of are included in the intervals , giving empirical justification of the claim that the CDF functions have a normal distribution. Moreover, the empirical should be a smooth function, not exhibiting anomaly accumulations or steps because of the merging of with different . That being the case, we may take as the representative distribution function of the measure.

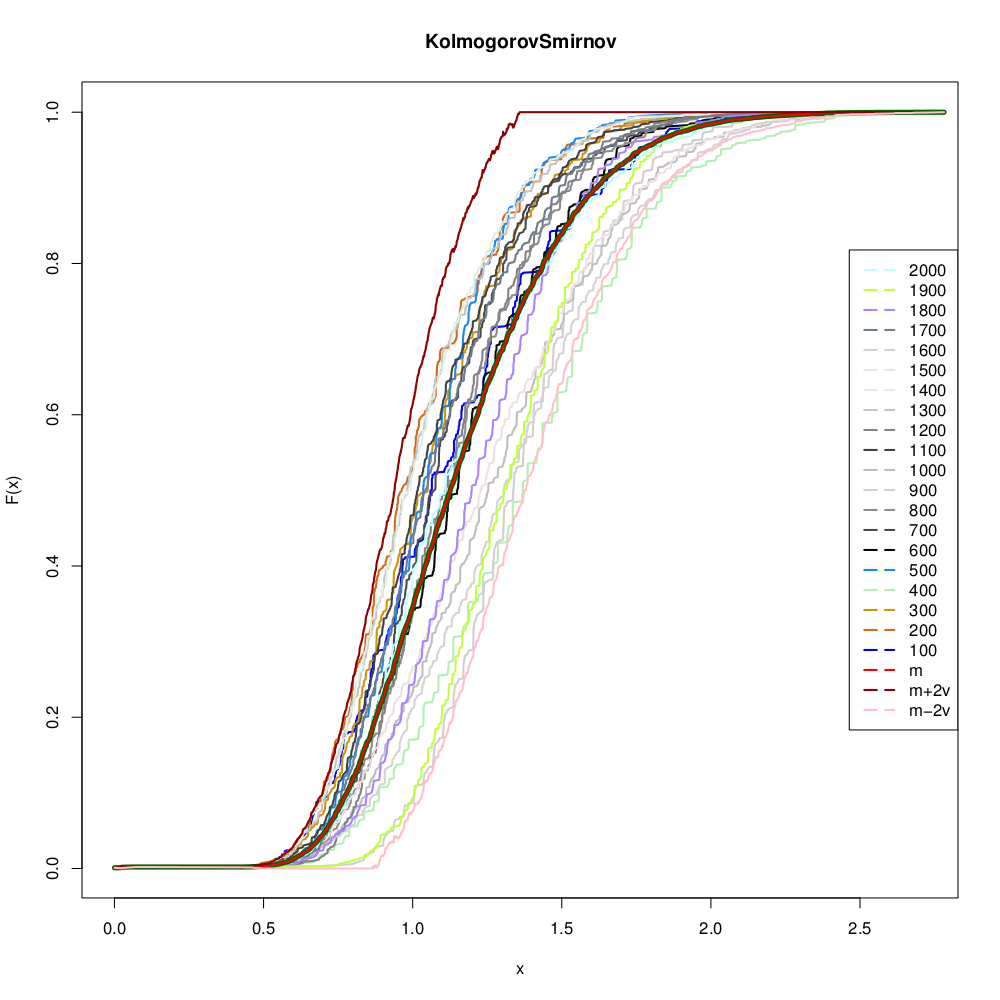

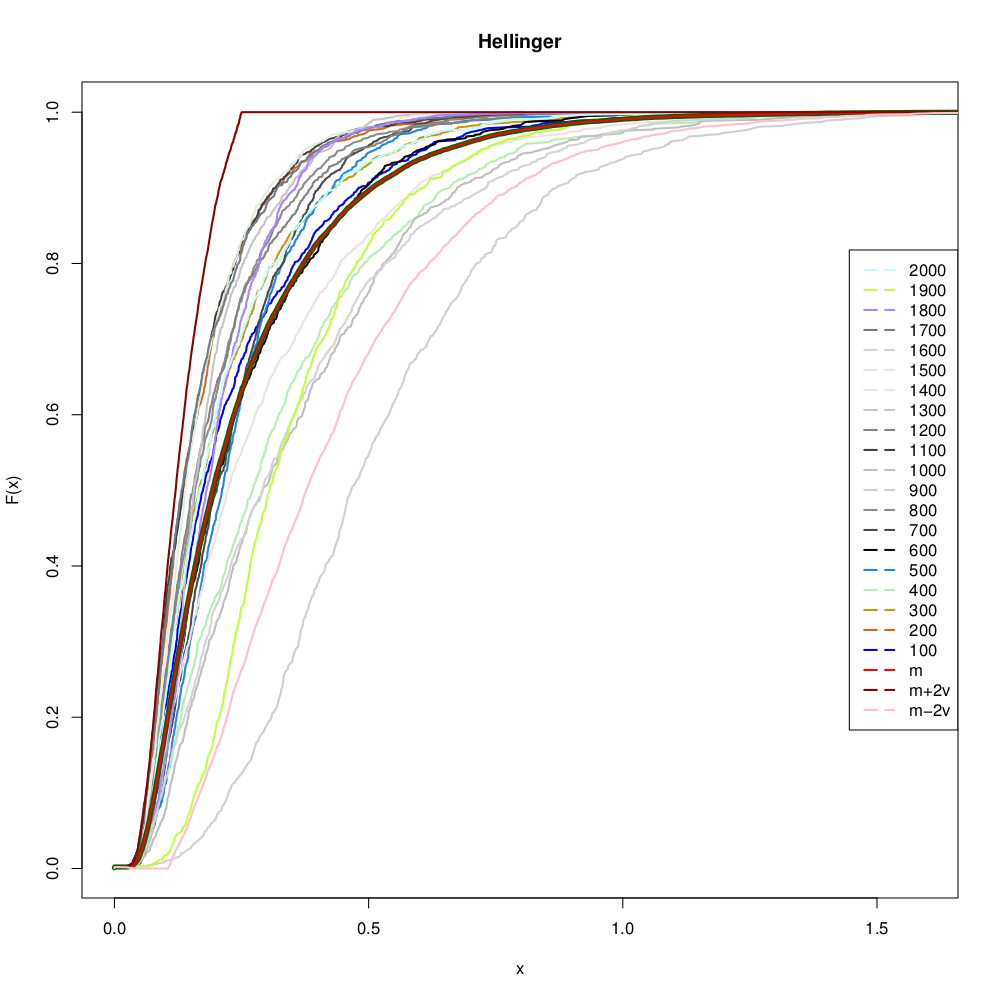

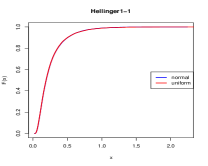

5.2 Window-Size Independence

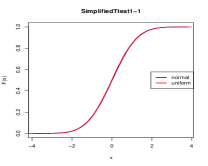

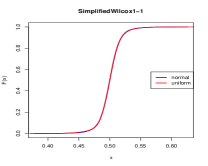

We present the results of the simulation of the Kolmogorov–Smirnov () and Hellinger (H) measures in Figure 1 and 2, respectively. For window sizes between 100 and 2000, at increments of 100, we generated 1000 intervals drawn from the same normal distribution . Then we computed the value of the measures to determine the CDF that supports the similarity assumption .

In Figure 1 and 2, for window sizes (dark blue) and (azure), both measures have CDFs that are similar. This is made possible because of .

Average . For each window size, we have a different CDF . We define the average of the distribution as,

| (39) |

Notice that is still a distribution and it could be considered as representative of the family of distributions (e.g., even though is not a valid distribution, is). In Figure 1, we draw the average in red. With our assumption about the nature of the distribution function, should tend to .

Variance . A natural definition of distribution variance is

| (40) |

In general, is not a distribution. Furthermore, the use of subtraction and power prevents the result from being a valid distribution, because the resulting can be negative for some . In Figure 1, we plot in dark-red, and in pink.

We assume that we have found a representative distribution when at least 19 of the 20 CDFs, 90% of them, are included in the intervals . This suggests that the CDF functions have a normal distribution . So, as gets larger, this should converge to our assumption . Recall that empirically, should be a smooth function that does not exhibit any anomaly accumulations or steps because of the merging of with different . Thus, we may consider to be the representative distribution function of the measure. 777Note that in practice, we could not find a CDF for the Bhattacharyya measure because we could not find a smooth CDF.

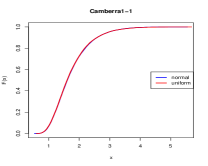

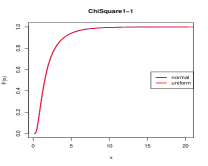

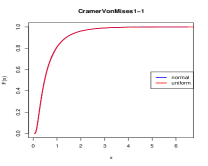

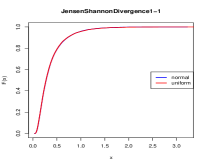

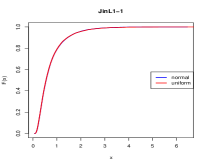

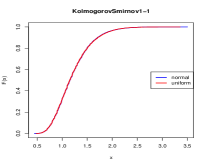

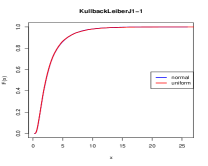

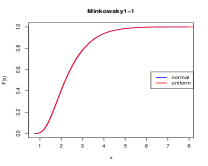

5.3 Input Distribution Independence

Let us consider the output of a CDF to be a stochastic variable and refer to as . Now, assume that is the inverse function of , properly defined for a finite number of samples . Then the event is identical to the event , which has the probability . This leads to for (see [Feller (1971)] Ch.1 Section 12). Thus, when we consider the input , we actually obtain a measure for which the distribution of the input should not affect the distribution of the measure, because is uniformly distributed independent of .

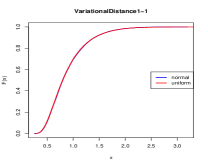

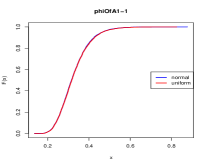

What we have found experimentally is that is independent of the distribution of the inputs and , as we show in Figure 3. Moreover, the distribution function can be used as a representative distribution.

We repeat the simulation described in Section 5.2 for window sizes 100–2000, collecting 1000, 2000, 5000, and 10000 samples per window size, while using two different stochastic processes, a normal distribution () and a uniform distribution (). For each stochastic process, we obtain four representative distribution functions. We then compare the results in a table (by size and input distribution), and report the first tile only (1000 samples per window size) in Figure 3 due to space restrictions.

By applying the standard measures, the same measure described in this work, and by simple visual inspection, we can say that these new stochastic distance measures have a distribution that is independent of the window sizes and the distribution of the process we compare. This gives us compelling evidence that our measures, such as JS, have a measure distribution that need to be pre-computed by simulation and only once.

We use the larger set (with 10,000 samples) to determine different -values, and then determine the measure thresholds for each -value. For example, we determine the threshold value having a -value of 95% for each measure. In practice, this means that if we generate and from two intervals and , and apply the measure , then if that measure has a value that is larger than the threshold, we know that only 5% of intervals drawn from the same stochastic process will have the same or larger measure. However, we may still decide to reject the assumption that and are similar because the probability is too small.

In the following experiments, we use the simulation distributions to tabulate the -values and the significance for each measure.

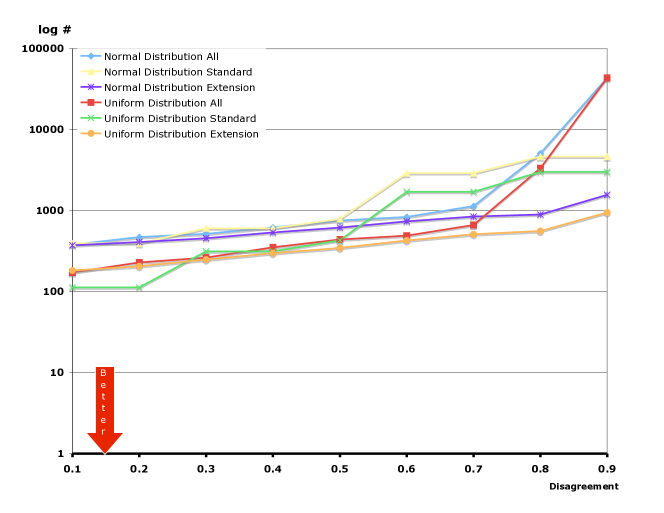

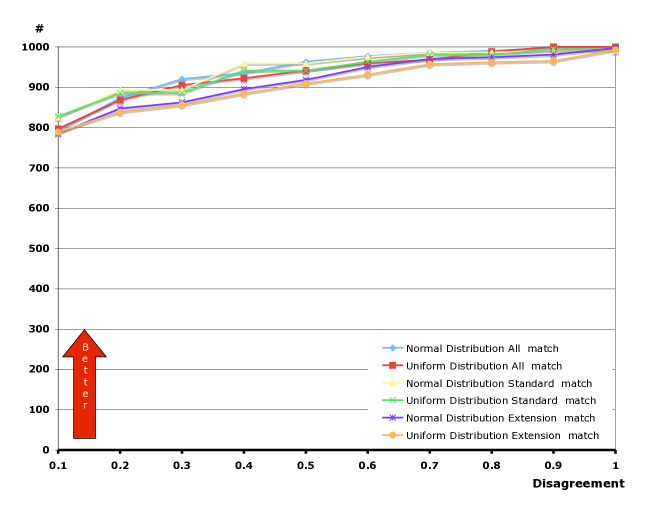

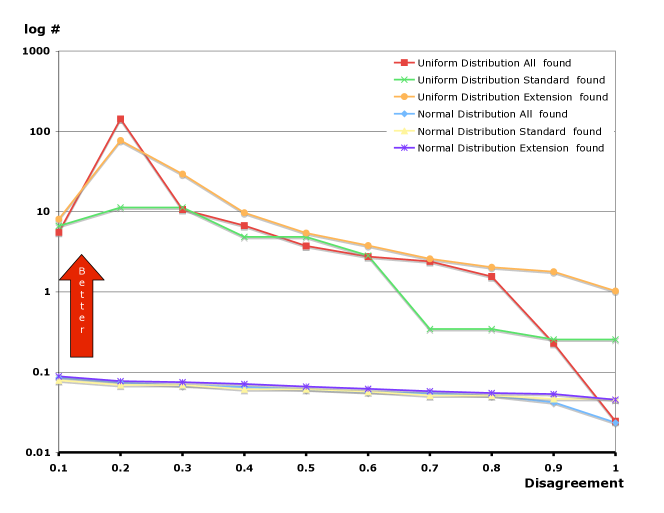

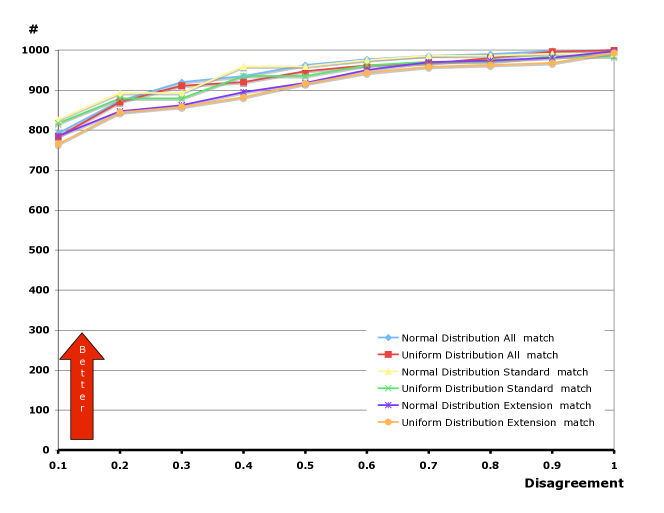

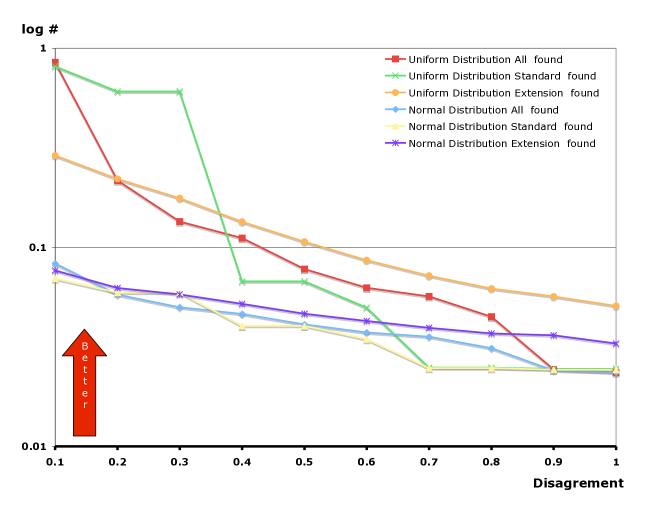

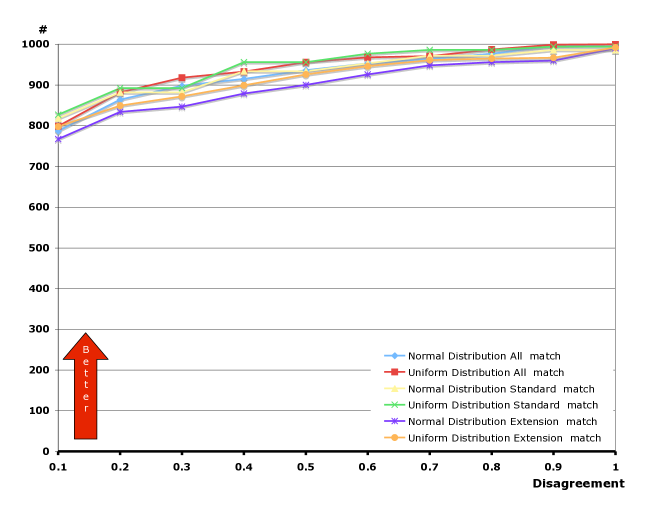

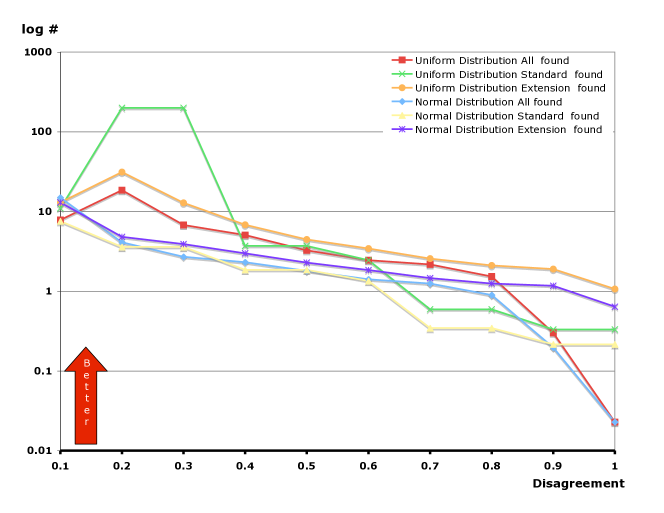

5.3.1 Disagreement (with Multiple Measures)