Risk estimation for matrix recovery with spectral regularization

Abstract

In this paper, we develop an approach to recursively estimate the quadratic risk for matrix recovery problems regularized with spectral functions. Toward this end, in the spirit of the SURE theory, a key step is to compute the (weak) derivative and divergence of a solution with respect to the observations. As such a solution is not available in closed form, but rather through a proximal splitting algorithm, we propose to recursively compute the divergence from the sequence of iterates. A second challenge that we unlocked is the computation of the (weak) derivative of the proximity operator of a spectral function. To show the potential applicability of our approach, we exemplify it on a matrix completion problem to objectively and automatically select the regularization parameter.

1 Introduction

Consider the problem of estimating a matrix from noisy observations , where . The linear bounded operator entails loss of information such that the problem is ill-posed. This problem arises in various research fields. Because of ill-posedness, side information through a regularizing term is necessary. We thus consider the problem

| (1) |

where the set of minimizers is assumed non-empty, is a regularization parameter and is a proper lower semi-continuous (lsc) convex regularizing function that imposes the desired structure on . In this paper, we focus on the case where is a convex spectral function, that is a symmetric convex function of the singular values of its argument. Spectral regularization can account for prior knowledge on the spectrum of , typically low-rank (see e.g. Fazel, 2002).

In practice, the choice of the regularization parameter in (1) remains an important problem largely unexplored. Typically, we want to select minimizing the quadratic risk . Since is unknown and is non-unique, one can instead consider an unbiased estimate of the prediction risk , where it can be easily shown that is a single-valued mapping. With the proviso that is weakly differentiable, the SURE (for Stein unbiased risk estimator, Stein, 1981)

| (2) |

is an unbiased estimate of the prediction risk, where , and stands for the (weak) Jacobian of . The SURE depends solely on , without prior knowledge of and then can prove very useful as a basis for automatic ways to choose the regularization parameters .

Contributions.

Our main contribution is to provide the derivative of matrix-valued spectral functions where the matrices have distinct singular values which extends the result of Lewis & Sendov (2001) to non-symmetric square matrices. This result is used to recursively compute the derivative of any solution of spectrally regularized inverse problems by solving (1). This is achieved by computing the derivatives of the iterates provided by a proximal splitting algorithm. In particular, this provides an estimate of in (2) which allows to compute . A Numerical example on a matrix completion problem is given to support our findings.

2 Recursive risk estimation

Proximal splitting

Proximal splitting algorithms have become extremely popular to solve non-smooth convex optimization problems that arise often in inverse problems, e.g. (1). These algorithms provide a sequence of iterates that provably converges to a solution . A practical way to compute , hence , as initiated by Vonesch et al. (2008), and that we pursue here, consists in differentiating this sequence of iterates. This methodology has been extended to a wide class of proximal splitting schemes in (Deledalle et al., 2012). For the sake of clarity, and without loss of generality, we focus on the case of the forward-backward (FB) splitting algorithm (Combettes & Wajs, 2005).

The FB scheme is a good candidate to solve (1) if is simple, meaning that its proximity operator has a closed-form. Recall that the proximity operator of a lsc proper convex function on is

The FB algorithm iteration reads

| (3) |

where denotes the adjoint operator of , is chosen such that , the dependency of the iterate to is dropped to lighten the notation.

Risk estimation

The divergence term is obtained by differentiating formula (3), which allows, for any vector to compute iteratively (the derivative of at in the direction ) as

| where | |||

| and |

Using the Jacobian trace formula of the divergence, it can be easily seen that

| (4) |

where and are realizations of . The can in turn be iteratively estimated by plugging in (4).

3 Local behavior of spectral functions

This section studies the local behavior of real- and matrix-valued spectral functions. We write the (full) singular value decomposition (SVD) of a matrix

(which might not be in general unique), where is the vector of singular values of with , denotes the rectangular matrix with entries on its main diagonal and 0 otherwise, and and are the unitary matrices of left and right singular vectors.

3.1 Scalar-valued Spectral Functions

A real-valued spectral function can by definition be written as

| (5) |

where is a symmetric function of its argument, meaning for any permutation matrix and in the domain of . We extend to the negative half-line as .

We then consider a scalar-valued spectral function as defined in (5). From subdifferential calculus on spectral functions Lewis (1995), we get the following.

Proposition 1.

A spectral function is convex if and only if is convex, and then

3.2 Matrix-valued Spectral Functions

We now turn to matrix-valued spectral functions

| (6) |

where is symmetric in its arguments, meaning for any permutation matrix . We extend to negative numbers as and is the entry-wise matrix multiplication. One can observe that for with , the proximity operator of a convex scalar-valued spectral function is a matrix-valued spectral function.

The following theorem provides a closed-form expression of the derivative of when is square, i.e. , with distinct singular values.

Theorem 1.

For any matrix-valued spectral function in (6), let the quantity

where , the symmetric and anti-symmetric parts are defined, for and , as

| and |

and is

The matrices and are defined, for all and , as

where for we have extended and as

and .

Assume that is a square matrix, i.e. ,

and with distinct singular values, such that

for all .

Then, a matrix-valued spectral function is differentiable at

if and only if is differentiable at .

Moreover,

The proof is given in Appendix A.

Theorem 1 generalizes the result of Lewis & Sendov (2001) to square matrices that are not necessarily symmetric, and we recover their formula when and are symmetric matrices and has distinct singular values. Regularity properties and expression of the directional derivative of symmetric matrix-valued separable spectral functions (possibly non-smooth) over non-necessarily symmetric matrices were also derived in Sun & Sun (2003). Before revising the previous version of this manuscript, Candès et al. (2012) brought to our attention their recent work on the SURE framework for parameter selection in denoising low-rank matrix data. Towards this goal, they provided closed-form expressions for the directional derivative and divergence of matrix-valued spectral functions over rectangular matrices with distinct singular values. They also addressed the case of complex-valued matrices.

Although our proof of Theorem 1 is rigorously valid only for square matrices with distinct singular values, we conjecture that the formula of the directional derivative holds for rectangular matrices with repeated singular values. For the symmetric case with repeated eigenvalues, this assertion was formally proved in Lewis & Sendov (2001). As stated above, the full-rank rectangular case with distinct singular values was proved in Candès et al. (2012), where it was also shown that the divergence formula has a continuous extension to all matrices.

4 Numerical applications

4.1 Nuclear norm regularization

We here consider the problem of recovering a low-rank matrix . To this end, is taken as the nuclear norm (a.k.a., trace or Schatten -norm) which is in some sense the tightest convex relaxation to the NP-hard rank minimization problem (Candès & Recht, 2009). The nuclear norm is defined by

| (7) |

Taking as and as in Proposition 1 gives:

Corollary 1.

The proximal operator of is

| (8) |

where is the component-wise soft-thresholding, defined for as

We now turn to the derivative of . A straightforward attempt is to take and apply Theorem 1 with

| (11) |

However, strictly speaking, Theorem 1 does not apply since a proximity mapping is 1-Lipschitz in general, hence not necessarily differentiable everywhere. Thus, its derivative may be set-valued, as is the case for soft-thresholding at .

4.2 Application to matrix completion

We now exemplify the proposed SURE computation approach on a matrix completion problem encountered in recommendation systems such as the popular Netflix problem. We therefore consider the forward model , , where is a dense but low-rank (or approximately so) matrix and is binary masking operator.

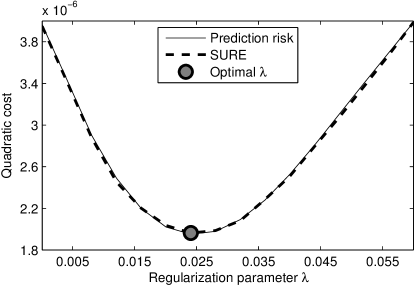

We have taken and observed entries (i.e., ). The underlying dense matrix has been chosen to be approximately low-rank with a rapidly decaying spectrum . The standard deviation has been set such that the resulting minimum least-square estimate has a relative error . Figure 1 depicts the prediction risk and its estimate as a function of . For each value of in the tested range, in (2) has been computed for a single realization of with realizations in (4)111Without impacting the optimal choice of , the two curves have been vertically shifted for visualization.. At the optimal value, has a rank of with a relative error of (i.e., a gain of about a factor w.r.t. the least-square estimator).

5 Conclusion

The core theoretical contribution of this paper is the derivative of square matrix-valued spectral functions. This was a key step to compute the derivative of the proximal operator associated to the nuclear norm, and finally to use the to recursively estimate the quadratic prediction risk of matrix recovery problems involving the nuclear norm regularization. The was also used to automatically select the optimal regularization parameter.

Appendix A Summary of the proof of Theorem 1

The following lemma derives the expression of the derivative of the SVD mapping . Note that this mapping is not well defined because even if the are distinct, one can apply arbitrary sign changes and permutations to the set of singular vectors. The lemma should thus be interpreted in the sense that one can locally write a Taylor expansion using the given differential for any particular choice of SVD. We point out that a proof of this lemma using wedge products can be found in (Edelman, 2005), but for the sake of completeness, we provide our own proof here.

Lemma 1.

We consider with distinct singular values. For any matrix in a neighborhood of , we can define without ambiguity the SVD mapping by sorting the values in and imposing sign constraints on . The singular value mapping is and for a given matrix , its directional derivative is

where and are defined, for all and , as

| (12) |

and where .

Proof.

Let be the sub-space of Hermitian matrix in . Let , where , be defined for as

We have for any vector

| (14) |

and for any vector

Let have distinct singular values and any of its SVD . We have . Moreover, denoting and , for any , solving is equivalent to solving

| (15) |

where and . Considering and shows that and are antisymmetric. In particular they are zero along the diagonal. Thus applying the operator to both sides of (15) shows . Now considering the entries and of the linear system (15) shows that for any and

| (16) |

Since for , , these symmetric linear systems can be solved. Then is invertible on and for , its inverse is

| (18) |

where and are given by the solutions of the above series of symmetric linear systems.

Since , we can apply the implicit function theorem (Rockafellar & Wets, 2005). Hence, for any in the neighborhood of , there exists a function such that , i.e. admits an SVD. Moreover, this function is in the neighborhood of and its differential is

Injecting (14) and (18) gives the desired formula by solving (16) in closed form. Since is any matrix with distinct singular values, we can conclude. ∎

We now turn to the proof of the theorem.

Proof.

Since the singular values of are all distinct, by composition of differentiable functions, we can derive the relationship (6) that defines which gives

where we have used the notation introduced in Lemma 1. Using the expression (12) for and shows that the matrix is computed as

where . Rearranging this expression using the symmetric and anti-symmetric parts shows the desired formula. ∎

References

- Candès & Recht (2009) Candès, E. J. and Recht, B. Exact matrix completion via convex optimization. Found. Comput. Math., 9(6):717–772, 2009.

- Candès et al. (2012) Candès, E. J., Sing-Long, C. A., and Trzasko, J. D. Unbiased risk estimates for singular value thresholding and spectral estimators. Technical Report arXiv:1210.4139v1, October 2012.

- Combettes & Wajs (2005) Combettes, P. L. and Wajs, V. R. Signal recovery by proximal forward-backward splitting. Math. Mod. Sim., 4(4):1168, 2005.

- Deledalle et al. (2012) Deledalle, C., Vaiter, S., Peyré, G., Fadili, J., and Dossal, C. Proximal splitting derivatives for risk estimation. In Journal of Physics: Conference Series, volume 386, pp. 012003. IOP Publishing, 2012.

- Edelman (2005) Edelman, A. Matrix jacobians with wedge products. MIT Handout for 18.325, 2005.

- Fazel (2002) Fazel, M. Matrix Rank Minimization with Applications. PhD thesis, Stanford University, 2002.

- Lewis (1995) Lewis, A.S. The convex analysis of unitarily invariant matrix functions. Journal of Convex Analysis, 2(1/2):173–183, 1995.

- Lewis & Sendov (2001) Lewis, A.S. and Sendov, H.S. Twice differentiable spectral functions. SIAM Journal on Matrix Analysis on Matrix Analysis and Applications, 23:368–386, 2001.

- Rockafellar & Wets (2005) Rockafellar, R. Tyrrell and Wets, Roger J-B. Variational Analysis. Fundamental Principles of Mathematical Sciences. Berlin: Springer-Verlag, third corrected printing edition, 2005.

- Stein (1981) Stein, C.M. Estimation of the mean of a multivariate normal distribution. The Annals of Statistics, 9(6):1135–1151, 1981.

- Sun & Sun (2003) Sun, D. and Sun, J. Nonsmooth matrix valued functions defined by singular values. Technical report, Department of Decision Sciences, National University of Singapore, 2003.

- Vonesch et al. (2008) Vonesch, C., Ramani, S., and Unser, M. Recursive risk estimation for non-linear image deconvolution with a wavelet-domain sparsity constraint. In ICIP, pp. 665–668. IEEE, 2008.