Estimating Unknown Sparsity in Compressed Sensing

Miles E. Lopes

mlopes@stat.berkeley.edu

Department of Statistics

University of California, Berkeley

Abstract

In the theory of compressed sensing (CS), the sparsity of the unknown signal is commonly assumed to be a known parameter. However, it is typically unknown in practice. Due to the fact that many aspects of CS depend on knowing , it is important to estimate this parameter in a data-driven way. A second practical concern is that is a highly unstable function of . In particular, for real signals with entries not exactly equal to 0, the value is not a useful description of the effective number of coordinates. In this paper, we propose to estimate a stable measure of sparsity , which is a sharp lower bound on . Our estimation procedure uses only a small number of linear measurements, does not rely on any sparsity assumptions, and requires very little computation. A confidence interval for is provided, and its width is shown to have no dependence on the signal dimension . Moreover, this result extends naturally to the matrix recovery setting, where a soft version of matrix rank can be estimated with analogous guarantees. Finally, we show that the use of randomized measurements is essential to estimating . This is accomplished by proving that the minimax risk for estimating with deterministic measurements is large when .

1 Introduction

The central problem of compressed sensing (CS) is to estimate an unknown signal from linear measurements given by

| (1) |

where is a user-specified measurement matrix, is a random noise vector, and is much smaller than the signal dimension . During the last several years, the theory of CS has drawn widespread attention to the fact that this seemingly ill-posed problem can be solved reliably when is sparse — in the sense that the parameter is much less than . For instance, if is approximately , then accurate recovery can be achieved with high probability when is drawn from a Gaussian ensemble Donoho (2006); Candès et al. (2006). Along these lines, the value of the parameter is commonly assumed to be known in the analysis of recovery algorithms — even though it is typically unknown in practice. Due to the fundamental role that sparsity plays in CS, this issue has been recognized as a significant gap between theory and practice by several authors Ward (2009); Eldar (2009); Malioutov et al. (2008). Nevertheless, the literature has been relatively quiet about the problems of estimating this parameter and quantifying its uncertainty.

1.1 Motivations and the role of sparsity

At a conceptual level, the problem of estimating is quite different from the more well-studied problems of estimating the full signal or its support set . The difference arises from sparsity assumptions. On one hand, a procedure for estimating should make very few assumptions about sparsity (if any). On the other hand, methods for estimating or often assume that a sparsity level is given, and then impose this value on the solution or . Consequently, a simple plug-in estimate of , such as or , may fail when the sparsity assumptions underlying or are invalid.

To emphasize that there are many aspects of CS that depend on knowing , we provide several examples below. Our main point here is that a method for estimating is valuable because it can help to address a broad range of issues.

-

•

Modeling assumptions. One of the core modeling assumptions invoked in applications of CS is that the signal of interest has a sparse representation. Likewise, the problem of checking whether or not this assumption is supported by data has been an active research topic, particularly in in areas of face recognition and image classification Rigamonti et al. (2011); Shi et al. (2011). In this type of situation, an estimate that does not rely on any sparsity assumptions is a natural device for validating the use of sparse representations.

-

•

The number of measurements. If the choice of is too small compared to the “critical” number , then there are known information-theoretic barriers to the accurate reconstruction of Arias-Castro et al. (2011). At the same time, if is chosen to be much larger than , then the measurement process is wasteful (since there are known algorithms that can reliably recover with approximately measurements Davenport et al. (2011)).

To deal with the selection of , a sparsity estimate may be used in two different ways, depending on whether measurements are collected sequentially, or in a single batch. In the sequential case, an estimate of can be computed from a set of “preliminary” measurements, and then the estimated value determines how many additional measurements should be collected to recover the full signal. Also, it is not always necessary to take additional measurements, since the preliminary set may be re-used to compute (as discussed in Section 5). Alternatively, if all of the measurements must be taken in one batch, the value can be used to certify whether or not enough measurements were actually taken.

-

•

The measurement matrix. Two of the most well-known design characteristics of the matrix are defined explicitly in terms of sparsity. These are the restricted isometry property of order (RIP-), and the restricted null-space property of order (NSP-), where is a presumed upper bound on the sparsity level of the true signal. Since many recovery guarantees are closely tied to RIP- and NSP-, a growing body of work has been devoted to certifying whether or not a given matrix satisfies these properties d’Aspremont and El Ghaoui (2011); Juditsky and Nemirovski (2011); Tang and Nehorai (2011). When is treated as given, this problem is already computationally difficult. Yet, when the sparsity of is unknown, we must also remember that such a “certificate” is not meaningful unless we can check that is consistent with the true signal.

-

•

Recovery algorithms. When recovery algorithms are implemented, the sparsity level of is often treated as a tuning parameter. For example, if is a conjectured bound on , then the Orthogonal Matching Pursuit algorithm (OMP) is typically initialized to run for iterations. A second example is the Lasso algorithm, which computes the solution , for some choice of . The sparsity of is determined by the size of , and in order to select the appropriate value, a family of solutions is examined over a range of values Efron et al. (2004). In the case of either OMP or Lasso, a sparsity estimate would reduce computation by restricting the possible choices of or , and it would also ensure that the chosen values conform to the true signal.

1.2 An alternative measure of sparsity

Despite the important theoretical role of the parameter in many aspects of CS, it has the practical drawback of being a highly unstable function of . In particular, for real signals whose entries are not exactly equal to 0, the value is not a useful description of the effective number of coordinates.

In order to estimate sparsity in a way that accounts for the instability of , it is desirable to replace the norm with a “soft” version. More precisely, we would like to identify a function of that can be interpreted like , but remains stable under small perturbations of . A natural quantity that serves this purpose is the numerical sparsity

| (2) |

which always satisfies for any non-zero . Although the ratio appears sporadically in different areas Tang and Nehorai (2011); Hurley and Rickard (2009); Hoyer (2004); Lopes et al. (2011), it does not seem to be well known as a sparsity measure in CS. Our terminology derives from the so-called numerical rank of a matrix , which is a soft version of the rank function, coined by Rudelson and Vershynin (2007).

A key property of is that it is a sharp lower bound on for all non-zero ,

| (3) |

which follows from applying the Cauchy-Schwarz inequality to the relation . (Equality in (3) is attained iff the non-zero coordinates of are equal in magnitude.) We also note that this inequality is invariant to scaling of , since and are individually scale invariant. In the opposite direction, it is easy to see that the only continuous upper bound on is the trivial one: If a continuous function satisfies for all in some open subset of , then must be identically equal to . Therefore, we must be content with a continuous lower bound.

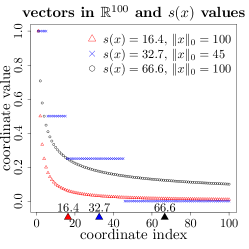

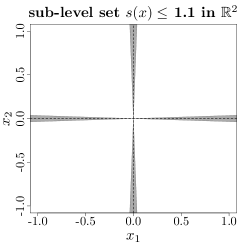

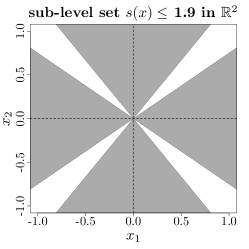

The fact that is a sensible measure of sparsity for non-idealized signals is illustrated in Figure 1. In essence, if has large coordinates and small coordinates, then , whereas . In the left panel, the sorted coordinates of three different vectors in are plotted. The value of for each vector is marked with a triangle on the x-axis, which shows that adapts well to the decay profile. This idea can be seen in a more geometric way in the middle and right panels, which plot the the sub-level sets with . When , the vectors in are closely aligned with the coordinate axes, and hence contain one effective coordinate. As , the set expands to include less sparse vectors until .

1.3 Related work.

Some of the challenges described in Section 1.1 can be approached with the general tools of cross-validation (CV) and empirical risk minimization (ERM). This approach has been used to select various parameters, such as the number of measurements Malioutov et al. (2008); Ward (2009), the number of OMP iterations Ward (2009), or the Lasso regularization parameter Eldar (2009). At a high level, these methods consider a collection of (say ) solutions obtained from different values of some tuning parameter of interest. For each solution, an empirical error estimate is computed, and the value corresponding to the smallest is chosen.

Although methods based on CV/ERM share common motivations with our work here, these methods differ from our approach in several ways. In particular, the problem of estimating a soft measure of sparsity, such as , has not been considered from that angle. Also, the cited methods do not give any theoretical guarantees to ensure that the estimated sparsity level is close to the true one. Note that even if an estimate has small risk , it is not necessary for to be close to . This point is relevant in contexts where one is interested in identifying a set of important variables or interpreting features.

From a computational point view, the CV/ERM approaches can also be costly — since must often be computed from a separate optimization problem for for each choice of the tuning parameter. By contrast, our method for estimating requires no optimization and can be computed easily from just a small set of preliminary measurements.

1.4 Our contributions.

The primary contributions of this paper consist in identifying a stable measure of sparsity that is relevant to CS, and proposing an efficient estimator with with provable guarantees. Secondly, we are not aware of any other papers that have identified a distinction between random and deterministic measurements with regard to estimating unknown sparsity (as in Section 4).

The remainder of the paper is organized as follows. In Section 2, we show that a principled choice of can be made if is known. This is accomplished by formulating a recovery condition for the Basis Pursuit algorithm directly in terms of . Next, in Section 3, we propose an estimator , and derive a dimension-free confidence interval for . The procedure is also shown to extend to the problem of estimating a soft measure of rank for matrix-valued signals. In Section 4 we show that the use of randomized measurements is essential to estimating in a minimax sense. Finally, we present simulations in Section 5 to validate the consequences of our theoretical results. We defer all of our proofs to the appendix.

Notation.

We define for any and , which only corresponds to a genuine norm for . For sequences of numbers and , we write or if there is an absolute constant such that for all large . If , we write . For a matrix , we define the Frobenius norm , the matrix -norm . Finally, for two matrices and of the same size, we define the inner product .

2 Recovery conditions in terms of

The purpose of this section is to present a simple proposition that links with recovery conditions for the Basis Pursuit algorithm (BP). This is an important motivation for studying , since it implies that if can be estimated well, then can be chosen appropriately.

In order to explain the connection between and recovery, we first recall a standard result Candès et al. (2006) that describes the error rate of the BP algorithm. Informally, the result assumes that the noise is bounded as for some constant , the matrix is drawn from a suitable ensemble, and the number of measurements satisfies for some . The conclusion is that with high probability, the solution satisfies

| (4) |

where is the best -term approximation111The vector is obtained by setting to 0 all coordinates of except the largest ones (in magnitude). to , and are constants. This bound is a fundamental point of reference, since it matches the minimax optimal rate under certain conditions, and applies to all signals (rather than just -sparse signals). Additional details may be found in Cai et al. (2010) [Theorem 3.3], Vershynin (2010) [Theorem 5.65].

We now aim to answer the question, “If were known, how large must be in order for to be small?”. To make the choice of independent of the scale of , we consider the relative error

| (5) |

so that the approximation error term is invariant to the transformation with . Also, since the noise-to-signal ratio is a fixed feature of the problem, the choice of is determined only by the approximation error. Since the bound (4) assumes , our question is reduced to determining how large must be relative to in order for to be small. Proposition 1 shows that the condition is necessary for the approximation error to be small, and the condition is sufficient.

Proposition 1.

Let , and . The following statements hold for any

-

(i)

If the -term approximation error satisfies , then

-

(ii)

If , then the -term approximation error satisfies

In particular, if with , then

Remarks.

A notable feature of these bounds is that they hold for all non-zero signals. In our simulations in Section 5, we show that choosing based on an estimate leads to accurate reconstruction across many sparsity levels.

3 Estimation results for

In this section, we present a simple procedure to estimate for any . The procedure uses a small number of measurements, makes no sparsity assumptions, and requires very little computation. The measurements we prescribe may also be re-used to recover the full signal after the parameter has been estimated.

The results in this section are are based on the measurement model (1), which may be written in scalar notation as

| (6) |

We assume the noise variables are independent, and bounded by , for some constant . No additional structure on the noise is needed.

3.1 Sketching with stable laws

Our estimation procedure derives from a technique known as sketching in the streaming computation literature Indyk (2006). Although this area deals with problems that are mathematically similar to CS, the connections between the two areas do not seem to be fully developed. One reason for this may be that measurement noise does not usually play a role in the context of sketching.

For any , the sketching technique offers a way to estimate from a set of randomized linear measurements. In our approach, we estimate by estimating and from separate sets of measurements. The core idea is to generate the measurement vectors using stable laws Zolotarev (1986); Indyk (2006).

Definition 1.

A random variable has a symmetric stable distribution if its characteristic function is of the form for some and some . We denote the distribution by , and is referred to as the scale parameter.

The most well-known examples of symmetric stable laws are the cases of , namely the Gaussian distribution , and the Cauchy distribution . To fix some notation, if a vector has i.i.d. entries drawn from , we write . The connection with norms hinges on the following property of stable distributions Zolotarev (1986).

Fact 1.

Suppose , and with parameters and . Then, the random variable is distributed according to

Using this fact, if we generate a set of i.i.d. vectors from and let , then is an i.i.d. sample from . Hence, in the special case of noiseless linear measurements, the task of estimating is equivalent to a well-studied univariate problem: estimating the scale parameter of a stable law from an i.i.d. sample.222It is worth pointing out that the norm can be estimated as the limit of with . This can be useful in the streaming computation context where often represents a sparse stream of integers Cormode (2003). However, we do not pursue this approach, since less meaningful for natural signals.

When the are corrupted with noise, our analysis shows that standard estimators for scale parameters are only moderately affected. The impact of the noise can also be reduced via the choice of when generating . The parameter controls the “energy level” of the measurement vectors . (Note that in the Gaussian case, if , then .) In our results, we leave as a free parameter to show how the effect of noise is reduced as is increased.

3.2 Estimation procedure for

Two sets of measurements are used to estimate , and we write the total number as . The first set is obtained by generating i.i.d. measurement vectors from a Cauchy distribution,

| (7) |

The corresponding values are then used to estimate via the statistic

| (8) |

which is a standard estimator of the scale parameter of the Cauchy distribution Fama and Roll (1971); Li et al. (2007). Next, a second set of i.i.d. measurement vectors are generated from a Gaussian distribution

| (9) |

In this case, the associated values are used to compute an estimate of given by

| (10) |

which is the natural estimator of the scale parameter (variance) of a Gaussian distribution. Combining these two statistics, our estimate of is defined as

| (11) |

3.3 Confidence interval.

The following theorem describes the relative error via an asymptotic confidence interval for . Our result is stated in terms of the noise-to-signal ratio

and the standard Gaussian quantile , which satisfies for any coverage level . In this notation, the following parameters govern the width of the confidence interval,

and we write these simply as and . As is standard in high-dimensional statistics, we allow all of the model parameters and to vary implicitly as functions of , and let . For simplicity, we choose to take measurement sets of equal sizes, , and we place a mild constraint on , namely . (Note that standard algorithms such as Basis Pursuit are not expected to perform well unless , as is clear from the bound (5).) Lastly, we make no restriction on the growth of , which makes well-suited to high-dimensional problems.

Theorem 1.

Let and . Assume that is constructed as above, and that the model (6) holds. Suppose also that and for all . Then as , we have

| (12) |

Remarks.

The most important feature of this result is that the width of the confidence interval does not depend on the dimension or sparsity of the unknown signal. Concretely, this means that the number of measurements needed to estimate to a fixed precision is only with respect to the size of the problem. This conclusion is confirmed our simulations in Section 5. Lastly, when and are small, we note that the relative error is of order with high probability, which follows from the simple Taylor expansion .

3.4 Estimating rank and sparsity of matrices

The framework of CS naturally extends to the problem of recovering an unknown matrix on the basis of the measurement model

| (13) |

where , is a user-specified linear operator from to , and is a vector of noise variables. In recent years, many researchers have explored the recovery of when it is assumed to have sparse or low rank structure. We refer to the papers Candès and Plan (2011); Chandrasekaran et al. (2010) for descriptions of numerous applications. In analogy with the previous section, the parameters or play important theoretical roles, but are very sensitive to perturbations of . Likewise, it is of basic interest to estimate robust measures of rank and sparsity for matrices. Since the sparsity analogue can be estimated as a straightforward extension of Section 3.2, we restrict our attention to the more distinct problem of rank estimation.

3.4.1 The rank of semidefinite matrices

In the context of recovering a low-rank positive semidefinite matrix , the quantity plays the role that the norm does in the recovery of a sparse vector. If we let denote the vector of ordered eigenvalues of , the connection can be made explicit by writing . As in Section 3.2, our approach is to consider a robust alternative to the rank. Motivated by the quantity in the vector case, we now consider

as our measure of the effective rank for non-zero , which always satisfies . The quantity has appeared elsewhere as a measure of rank Lopes et al. (2011); Tang and Nehorai (2010), but is less well known than other rank relaxations, such as the numerical rank Rudelson and Vershynin (2007). The relationship between and is completely analogous to and . Namely, we have a sharp, scale-invariant inequality

with equality holding iff the non-zero eigenvalues of are equal. The quantity is more stable than in the sense that if has large eigenvalues, and small eigenvalues, then , whereas .

Our procedure for estimating is based on estimating and from separate sets of measurements. The semidefinite condition is exploited through the basic relation . To estimate , we use linear measurements of the form

| (14) |

and compute the estimator , where is again the measurement energy parameter. Next, to estimate , we note that if has i.i.d. entries, then . Hence, if we collect additional measurements of the form

| (15) |

where the are independent random matrices with i.i.d. entries, then a suitable estimator of is . Combining these statistics, we propose

as our estimate of . In principle, this procedure can be refined by using the measurements (14) to estimate the noise distribution, but we omit these details. Also for simplicity, we retain the assumptions of the previous section, and assume only that the are independent, and bounded by . The next theorem shows that the estimator mirrors as in Theorem 1, but with being replaced by , and with being replaced by .

Theorem 2.

Let and . Assume that is constructed as above, and that the model (13) holds. Suppose also that and for all . Then as , we have

| (16) |

Remarks.

In parallel with Theorem 1, this confidence interval has the valuable property that its width does not depend on the rank or dimension of , but merely on the noise-to-signal ratio . The relative error is again of order with high probability when is small.

4 Deterministic measurement matrices

The problem of constructing deterministic matrices with good recovery properties (e.g. RIP- or NSP-) has been a longstanding topic within CS. Since our procedure in Section 3.2 selects at random, it is natural to ask if randomization is essential to the estimation of unknown sparsity. In this section, we show that estimating with a deterministic matrix leads to results that are inherently different from our randomized procedure.

At an informal level, the difference between random and deterministic matrices makes sense if we think of the estimation problem as a game between nature and a statistician. Namely, the statistician first chooses a matrix and an estimation rule . (The function takes as input and returns an estimate of .) In turn, nature chooses a signal , with the goal of maximizing the statistician’s error. When the statistician chooses deterministically, nature has the freedom to adversarially select an that is ill-suited to the fixed matrix . By contrast, if the statistician draws at random, then nature does not know what value will take, and therefore has less knowledge to choose a bad signal.

In the case of noiseless random measurements, Theorem 1 implies that our particular estimation rule can achieve a relative error on the order of with high probability for any non-zero . (cf. Remarks for Theorem 1.) Our aim is now to show that for noiseless deterministic measurements, all estimation rules have a worst-case relative error that is much larger than than . In other words, there is always a choice of that can defeat a deterministic procedure, whereas is likely to succeed under any choice of .

In stating the following result, we note that it involves no randomness whatsoever — since we assume that the observed measurements are noiseless and obtained from a deterministic matrix .

Theorem 3.

The minimax relative error for estimating from noiseless deterministic measurements satisfies

Remarks.

Under the typical high-dimensional scenario where there is some for which as , we see that which is indeed much larger than .

5 Simulations

Relative error of .

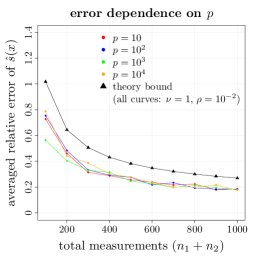

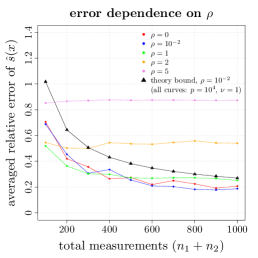

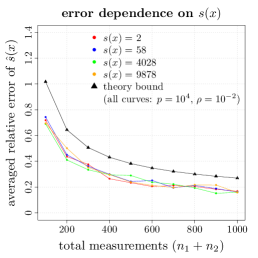

To validate the consequences of Theorem 1, we study how the decay of the relative error depends on the parameters , , and . We generated measurements under a broad range of parameter settings, with in most cases. Note that although is a very large dimension, it is not at all extreme from the viewpoint of applications (e.g. a megapixel image with ). Additional details regarding parameters are given below. As anticipated by Theorem 1, the left and right panels in Figure 2 show that the relative error has no noticeable dependence on or . The middle panel shows that for fixed , the relative error grows moderately with . Lastly, our theoretical bounds on conform well with the empirical curves in the case of low noise ().

Reconstruction of based on .

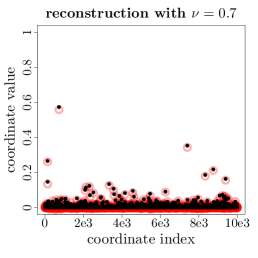

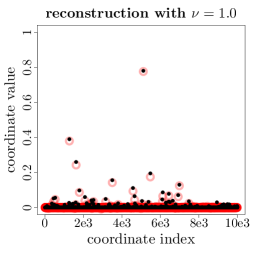

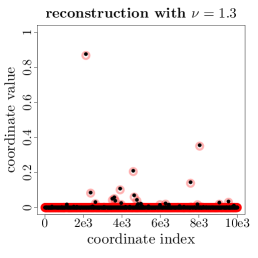

For the problem of choosing the number of measurements for reconstructing , we considered the choice of . First, to compute , we followed Section 3.2, and drew initial measurement sets of Cauchy and Gaussian vectors with and . If it happened to be the case that , then reconstruction was performed using only the initial 500 Gaussian measurements. Alternatively, if , then additional Gaussian measurements were drawn for reconstruction. Specific details of the implementation with the Basis Pursuit algorithm are given below. Figure 3 illustrates the results for three power-law signals in with , and (corresponding to ). In each panel, the coordinates of are plotted in black, and those of are plotted in red. Clearly, there is good qualitative agreement in all three cases. From left to right, the value of was 4108, 590, and 150. Altogether, the simulation indicates that takes the structure of the true signal into account, and is sufficiently large for accurate reconstruction.

Settings for relative error of (Figure 2).

For each parameter setting labeled in the figures, we let and averaged over 100 problem instances of . In all cases, the matrix chosen according to equations (7) and (9) with and . We always chose the normalization , and so that . (In the left and right panels, .) For the left and middle panels, all signals have the decay profile . For the right panel, the values 2, 58, 4028, and 9878 were obtained using decay profiles with . In the left and right panels, we chose for all curves. The theoretical bound on in black was computed from Theorem 16 with . (This bound holds with probability at least 1/2 equal to and so it may be reasonably be compared with the average of .)

Settings for reconstruction (Figure 3).

Reconstructions were computed using the BP algorithm , with the choice being based on i.i.d. noise variables , with . (As defined above, is the instance-dependent number of Gaussian measurements.) For each choice of , we generated 25 problem instances and plotted the reconstruction corresponding to the median of over the 25 runs (so that the plots reflect typical performance).

6 Appendix

6.1 Proof of Proposition 1

To prove the implication (i), we calculate

| (17) |

Since , and , we obtain the lower bound

Hence, if the left hand side is at most , we must have , proving (i).

To prove the second implication, note that implies

| (18) |

Next, consider the probability vectors defined by and (that is, ). It is a basic fact about the majorization ordering on that is majorized by every probability vector (Marshall et al., 2010, p. 7). In particular, we have for any , which is the same as

Combining this with line (18) proves (ii). ∎

6.2 Proof of Theorem 1.

Define the noiseless version of the measurement to be

and let the noiseless versions of the statistics and be given by

| (19) | ||||

| (20) |

It is convenient to work in terms of these variables, since their limiting distributions may be computed exactly. Due to the fact that is an i.i.d. sample from the standard Cauchy distribution , the asymptotic normality of the sample median implies

| (21) |

where . Additional details may be found in (David, , Theorem 9.2) and (Li et al., 2007, Lemma 3). Similarly, the variables are an i.i.d. sample from the chi-square distribution on one degree of freedom, and so it follows from the delta method that

| (22) |

where . Note that in proving the last two limit statements, we intentionally scaled the variables in such a way that their distributions did not depend on any model parameters. It is for this reason that the limits hold even when the model parameters are allowed to depend on . We conclude from the limits (21) and (22) that for any ,

| (23) |

and

| (24) |

We now relate and in terms of intervals defined by and . Since the noise variables are bounded by , and , it is easy to see that

Consequently, if we note that , then we may write

| (25) |

To derive a similar relationship involving and , if we write in terms of and apply the triangle inequality, it follows that

| (26) |

The proof may now be completed by assembling the last several items. Recall the parameters and , which are given by

| (27) | ||||

| (28) |

Combining the limits (23) and (24) with the intervals (25) and (26), we have the following asymptotic bounds for the statistics and ,

| (29) |

and

| (30) |

Due to the independence of and , and the relation

we conclude that

| (31) |

∎

6.3 Proof of Theorem 2.

The proof of Theorem 2 is almost the same as the proof of Theorem 1 and we omit the details. One point of difference is that in Theorem 1, the bounding probability is , whereas in Theorem 2 it is . The reason is that in the case of Theorem 2, the condition holds with probability 1, whereas the analogous statement holds with probability in the case of Theorem 1.

6.4 Proof of Theorem 3.

The following lemma illustrates the essential reason why estimating is difficult in the deterministic case. The idea is that for any measurement matrix , it is possible to find two signals that are indistinguishable with respect to , and yet have very different sparsity levels in terms of . We prove Theorem 3 after giving the proof of the lemma.

Lemma 1.

Let be an arbitrary matrix, and let be an arbitrary signal. Then, there exists a non-zero vector satisfying , and

| (32) |

Proof of Lemma 1. By Hölder’s inequality, and so it suffices to lower-bound the second ratio. The overall approach to finding a dense vector is to use the probabilistic method. Let be a matrix whose columns are an orthonormal basis for the null space of , where . Also define the scaled matrix . Letting be a standard Gaussian vector, we will consider , which satisfies for all realizations of . We begin the argument by defining the function

| (33) |

where

The proof amounts to showing that the event holds with positive probability. To see this, notice that the event is equivalent to

We will prove that is positive by showing that , and this will be accomplished by lower-bounding the expected value of , and upper-bounding the expected value of .

First, to lower-bound we begin by considering the variance of , and use the fact that , obtaining

| (34) |

To upper-bound the variance, we use the Poincaré inequality for the standard Gaussian measure on Beckner (1989). Since the function has a Lipschitz constant equal to with respect to the Euclidean norm, it follows that . Consequently, the Poincaré inequality implies

Using this in conjunction with the inequality (34), and the fact that is at most , we obtain the lower bound

| (35) |

The second main portion of the proof is to upper-bound . Since , it is enough to upper-bound , and we will do this using a version of Slepian’s inequality. If denotes the row of , define , and let be i.i.d. variables. The idea is to compare the Gaussian process with the Gaussian process . By Proposition A.2.6 in van der Vaart and Wellner van der Vaart and Wellner (1996), the inequality

holds as long as the condition is satisfied for all , and this is simple to verify. To finish the proof, we make use of a standard bound for the expectation of Gaussian maxima

which follows from a modification of the proof of Massart’s finite class lemma (Massart, 2000, Lemma 5.2)333The “extra” factor of 2 inside the logarithm arises from taking the absolute value of the .. Combining the last two steps, we obtain

| (36) |

Finally, applying the bounds (35) and (36) to the definition of the function in , we have

| (37) |

which proves , as needed. ∎

We now apply Lemma 3 to prove Theorem 3.

Proof of Theorem 3. We begin by making several reductions. First, it is enough to show that

| (38) |

To see this, note that the general inequality implies

and we can optimize over both sides with being a constant. Next, for any fixed matrix , it is enough to show that

| (39) |

as we may take the infimum over all matrices without affecting the right hand side. To make a third reduction, it is enough to prove the same bound when is replaced with any smaller set, as this can only make the supremum smaller. In particular, we will replace with a two-point subset , where by Lemma 1, we may choose and to satisfy , as well as

We now aim to prove that

| (40) |

and we will accomplish this using the classical technique of constructing a Bayes procedure with constant risk. For any decision rule and any point , define the (deterministic) risk function

Also, for any prior on , define

By Propositions 3.3.1 and 3.3.2 of Bickel and Doksum (2001), the inequality (40) holds if there exists a prior distribution on and a decision rule with the following three properties:

-

1.

The rule is Bayes for , i.e. .

-

2.

The rule has constant risk over , i.e. .

-

3.

The constant value of the risk of is at least .

To exhibit and with these properties, we define to be the two-point prior that puts equal mass at and , and we define to be the trivial decision rule that always returns the average of the two possibilities, namely . It is simple to check the second and third properties, namely that has constant risk equal to , and that this risk is at least . It remains to check that is Bayes for . This follows easily from the triangle inequality, since for any ,

| (41) |

∎

References

- Arias-Castro et al. (2011) E. Arias-Castro, E.J. Candès, and M. Davenport. On the fundamental limits of adaptive sensing. Arxiv preprint arXiv:1111.4646, 2011.

- Beckner (1989) W. Beckner. A generalized Poincaré inequality for Gaussian measures. Proceedings of the American Mathematical Society, 105(2):397–400, 1989.

- Bickel and Doksum (2001) P.J. Bickel and K.A. Doksum. Mathematical Statistics, volume I. Prentice Hall, 2001.

- Cai et al. (2010) T.T. Cai, L. Wang, and G. Xu. New bounds for restricted isometry constants. Information Theory, IEEE Transactions on, 56(9), 2010.

- Candès and Plan (2011) E.J. Candès and Y. Plan. Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. IEEE Transactions on Information Theory, 57(4):2342–2359, 2011.

- Candès et al. (2006) E.J. Candès, J.K. Romberg, and T. Tao. Stable signal recovery from incomplete and inaccurate measurements. Communications on pure and applied mathematics, 59(8):1207–1223, 2006.

- Candès et al. (2006) E.J. Candès, J.K. Romberg, and T. Tao. Stable signal recovery from incomplete and inaccurate measurements. Communications on pure and applied mathematics, 59(8):1207–1223, 2006.

- Chandrasekaran et al. (2010) V. Chandrasekaran, B. Recht, P.A. Parrilo, and A.S. Willsky. The convex algebraic geometry of linear inverse problems. In Communication, Control, and Computing (Allerton), 2010 48th Annual Allerton Conference on, pages 699–703. IEEE, 2010.

- Cormode (2003) G. Cormode. Stable distributions for stream computations: It’s as easy as 0, 1, 2. In Workshop on Management and Processing of Massive Data Streams, 2003.

- d’Aspremont and El Ghaoui (2011) A. d’Aspremont and L. El Ghaoui. Testing the nullspace property using semidefinite programming. Mathematical programming, 127(1):123–144, 2011.

- Davenport et al. (2011) M.A. Davenport, M.F. Duarte, YC Eldar, and G. Kutyniok. Introduction to compressed sensing. Preprint, 93, 2011.

- (12) HA David. Order statistics. 1981. J. Wiley.

- Donoho (2006) D.L. Donoho. Compressed sensing. IEEE Transactions on Information Theory, 52(4):1289–1306, 2006.

- Efron et al. (2004) B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least angle regression. The Annals of statistics, 32(2):407–499, 2004.

- Eldar (2009) Y.C. Eldar. Generalized sure for exponential families: Applications to regularization. IEEE Transactions on Signal Processing, 57(2):471–481, 2009.

- Fama and Roll (1971) Eugene F Fama and Richard Roll. Parameter estimates for symmetric stable distributions. Journal of the American Statistical Association, 66(334):331–338, 1971.

- Hoyer (2004) P.O. Hoyer. Non-negative matrix factorization with sparseness constraints. The Journal of Machine Learning Research, 5:1457–1469, 2004.

- Hurley and Rickard (2009) N. Hurley and S. Rickard. Comparing measures of sparsity. IEEE Transactions on Information Theory, 55(10):4723–4741, 2009.

- Indyk (2006) P. Indyk. Stable distributions, pseudorandom generators, embeddings, and data stream computation. Journal of the ACM (JACM), 53(3):307–323, 2006.

- Juditsky and Nemirovski (2011) A. Juditsky and A. Nemirovski. On verifiable sufficient conditions for sparse signal recovery via minimization. Mathematical programming, 127(1):57–88, 2011.

- Li et al. (2007) P. Li, T. Hastie, and K. Church. Nonlinear estimators and tail bounds for dimension reduction in l 1 using cauchy random projections. Journal of Machine Learning Research, pages 2497–2532, 2007.

- Lopes et al. (2011) M. Lopes, L. Jacob, and M.J. Wainwright. A more powerful two-sample test in high dimensions using random projection. In NIPS 24, pages 1206–1214. 2011.

- Malioutov et al. (2008) D.M. Malioutov, S. Sanghavi, and A.S. Willsky. Compressed sensing with sequential observations. In IEEE International Conference on Acoustics, Speech and Signal Processing, 2008., pages 3357–3360. IEEE, 2008.

- Marshall et al. (2010) A.W. Marshall, I. Olkin, and B.C. Arnold. Inequalities: theory of majorization and its applications. Springer, 2010.

- Massart (2000) P. Massart. Some applications of concentration inequalities to statistics. In Annales-Faculte des Sciences Toulouse Mathematiques, volume 9, pages 245–303. Université Paul Sabatier, 2000.

- Rigamonti et al. (2011) R. Rigamonti, M.A. Brown, and V. Lepetit. Are sparse representations really relevant for image classification? In Computer Vision and Pattern Recognition (CVPR), 2011 IEEE Conference on, pages 1545–1552. IEEE, 2011.

- Rudelson and Vershynin (2007) M. Rudelson and R. Vershynin. Sampling from large matrices: An approach through geometric functional analysis. Journal of the ACM (JACM), 54(4):21, 2007.

- Shi et al. (2011) Q. Shi, A. Eriksson, A. van den Hengel, and C. Shen. Is face recognition really a compressive sensing problem? In Computer Vision and Pattern Recognition (CVPR), 2011 IEEE Conference on, pages 553–560. IEEE, 2011.

- Tang and Nehorai (2010) G. Tang and A. Nehorai. The stability of low-rank matrix reconstruction: a constrained singular value view. arXiv:1006.4088, submitted to IEEE Transactions on Information Theory, 2010.

- Tang and Nehorai (2011) G. Tang and A. Nehorai. Performance analysis of sparse recovery based on constrained minimal singular values. IEEE Transactions on Signal Processing, 59(12):5734–5745, 2011.

- van der Vaart and Wellner (1996) A.W. van der Vaart and J.A. Wellner. Weak convergence and empirical processes. Springer Verlag, 1996.

- Vershynin (2010) R. Vershynin. Introduction to the non-asymptotic analysis of random matrices. Arxiv preprint arxiv:1011.3027, 2010.

- Ward (2009) R. Ward. Compressed sensing with cross validation. IEEE Transactions on Information Theory, 55(12):5773–5782, 2009.

- Zolotarev (1986) V.M. Zolotarev. One-dimensional stable distributions, volume 65. Amer Mathematical Society, 1986.