Simulation of BSDEs by Wiener chaos expansion

Abstract

We present an algorithm to solve BSDEs based on Wiener chaos expansion and Picard’s iterations. We get a forward scheme where the conditional expectations are easily computed thanks to chaos decomposition formulas. We use the Malliavin derivative to compute . Concerning the error, we derive explicit bounds with respect to the number of chaos and the discretization time step. We also present numerical experiments. We obtain very encouraging results in terms of speed and accuracy.

doi:

10.1214/13-AAP943keywords:

[class=AMS]keywords:

and

1 Introduction

In this paper, we are interested in the numerical approximation of solutions to backward stochastic differential equations (BSDEs for short in the sequel). BSDEs were introduced by Bismut in Bis73 in the linear case, whereas the nonlinear case was considered later by Pardoux and Peng in PP90 . A BSDE is an equation of the following form:

| (1) |

where is a -dimensional standard Brownian motion, the terminal condition is a real-valued -measurable random variable where stands for the augmented filtration of the Brownian motion and the generator is a map from into . A solution to this equation is a pair of processes which is required to be adapted to the filtration . We will assume the conditions of Pardoux and Peng to ensure existence and uniqueness of solutions.

Our main objective in this study is the numerical approximation of the solution to BSDE (1) (even though there exists a large literature on this subject). The first two contributions to this topic are due to Chevance Che97 , who considered generators independent of and Bally Bal97 , who used a random time mesh. Ma and Yong MY99 proposed numerical schemes based on the link between Markovian BSDEs and semilinear partial differential equations (PDEs). Another approach, based on Donsker’s theorem and close to Che97 , was proposed by Coquet, Mackevicius and Mémin CMM99 in the case of a generator independent of ; the general case was treated by Briand, Delyon and Mémin in BDM01 , who later extended it to a more general framework BDM02 , including the case of a “stepwise constant Brownian motion.” This extension led to the formulas

known as the dynamic programming algorithm. Even though the convergence was proved in the case of path-dependent terminal condition , the rate of convergence was left as an open question in BDM02 . This problem was solved by Zhang Zha04 and Bouchard and Touzi BT04 in the case of Markovian BSDE, namely in the case of a terminal condition where is the solution to a stochastic differential equation; in Zha04 , the author considers the path-dependent case as well. Their result was generalized by Gobet and Labart GL07 and also by Gobet and Makhlouf GM10 .

From a numerical point of view, the main difficulty in solving BSDEs is to efficiently compute conditional expectations. Several approaches have been proposed using various tools: the Malliavin calculus BT04 , regression methods GLW05 , GLW06 and quantization technics BP03 .

Finally, let us mention that there exist some works dealing with the discretization of solutions to BSDEs in a more general framework: forward–backward SDEs DM06 and quadratic BSDEs Ric11 .

Let us now describe briefly the main points of our approach in the case of a real-valued Brownian motion. Already used in several quoted papers (see also BD07 , GL10 , BS11 ), our starting point is the use of Picard’s iterations, and for ,

It is well known that the sequence converges exponentially fast toward the solution to BSDE (1). We write this Picard scheme in a forward way,

where stands for the Malliavin derivative of the random variable .

In order to compute the previous conditional expectation, we use a Wiener chaos expansion of the random variable

More precisely, we use the following orthogonal decomposition of the random variable :

where denotes the Hermite polynomial of degree , is an orthonormal basis of and, if is a sequence of integers, . is the sequence of coefficients ensuing from the decomposition of . Of course, from a practical point of view, we only keep a finite number of terms in this expansion:

-

•

we work with a finite number of chaos, ;

-

•

we choose a finite number of functions .

This leads to the following approximation with :

One of the key points in using such a decomposition is that, for choices of simple functions , …, , there exist explicit formulas for both

| (2) |

this plays a crucial role in our algorithm. Using these formulas and starting from trajectories of the underlying Brownian motion, we are able to construct trajectories of the solution to the BSDE.

In the following, the functions are chosen as step functions:

and the previous formulas are really simple; see (2.3)–(11) and Proposition 2.7. Eventually, the main advantage of this method is that only one decomposition has to be computed per Picard iteration: the decomposition of . Therein lies the main difference between our approach and the approach based on regression technique developed by Bender and Denk in BD07 . In their paper, for a given Picard iteration and for each time of the mesh grid, two projections have to be computed, one for and one for . The second difference comes from the way of computing . In our method, once the decomposition of is computed, is given explicitly as the Malliavin derivative of . Let us also point out that our algorithm can handle fully path dependent terminal conditions.

The rest of the paper is organized as follows. Section 2 contains the notation and the preliminary results, Section 3 describes precisely the algorithm, Section 4 is devoted to the study of the convergence of the algorithm and finally Section 5 contains some numerical experiments. Some technical proofs are postponed to the Appendix.

2 Preliminaries

2.1 Definitions and notation

Given a probability space and an -valued Brownian motion , we consider:

-

•

, the filtration generated by the Brownian motion and augmented.

-

•

, , the space of all -measurable random variables (r.v. in the following) satisfying .

-

•

denotes for any in .

-

•

, , the space of all càdlàg predictable processes such that .

-

•

, , the space of all predictable processes such that .

-

•

, the space of all square integrable functions on .

-

•

, the set of continuously differentiable functions with continuous derivatives w.r.t. (resp., w.r.t. ) up to order (resp., up to order ).

-

•

, the set of continuously differentiable functions with continuous and uniformly bounded derivatives w.r.t. (resp., w.r.t. ) up to order (resp., up to order ). The function is also bounded.

-

•

, the norm of the derivatives of w.r.t. all the space variables which sum equals : , where .

-

•

, the set of smooth functions with partial derivatives of polynomial growth.

-

•

, , the norm on the space defined by

(3)

We also recall some useful definitions related to Malliavin calculus. We use the notation of nualart06 .

-

•

denotes the class of random variables of the form , where , for all and for all .

-

•

denotes the closure of w.r.t. the following norm on

where is a multi-index , and represents the multi-index Malliavin derivative operator. We recall .

Remark 2.1.

When , .

Let and . We also introduce the following notation:

-

•

denotes the space of all -measurable r.v. such that

where means .

-

•

denotes the space of all couple of processes belonging to and such that

We recall

We also denote .

2.2 Wiener chaos expansion

2.2.1 Notation and useful results

We refer to nualart06 for more details on this section. Let us briefly recall the Wiener chaos expansion in the simple case of a real-valued Brownian motion. It is well known that every random variable has an expansion of the following form:

where the functions are deterministic functions. There is an ambiguity for the definition of these functions . We adopt in this paper the following point of view: the function is defined on the simplex

We define the iterated integral for a deterministic function as

Due to the Itô isometry, and . Then .

Let be a random variable in whose chaos expansion is given by (2.2.1). We introduce:

-

•

the Wiener chaos of order of .

-

•

the chaos decomposition of up to order , that is,

We state two lemmas useful for the sequel.

Lemma 2.2 ((Nualart))

if and only if . In this case, we have

From Lemma 2.2, we deduce the following:

Lemma 2.3

Let . We have

The following lemma gives some useful properties of the chaos decomposition.

Lemma 2.4

-

•

Let be a r.v. in . , we have . If belongs to , , .

-

•

Let be in . We have .

-

•

For all and for all , .

The first result ensues from the fact that for ; see nualart06 , page 63.

2.2.2 Wiener chaos expansion and Hermite polynomials

Another approach to Wiener chaos expansion uses Hermite polynomials. This approach can be easily generalized when considering -dimensional Brownian motions, and so this is the one we consider in the following. We present it for . Let be an orthonormal basis of . The Wiener chaos of order , , is the -closure of the vector field spanned by

where is the Hermite polynomial of order defined by the expansion

with the convention . With this normalization, we have for any integer . It is well known that is a sequence of orthogonal polynomials in , where denotes the reduced centered Gaussian measure. Moreover, we have

Every square integrable random variable , measurable with respect to , admits the following orthogonal decomposition:

| (6) |

where is a sequence of positive integers, and where stands for . Taking into account the normalization of the Hermite polynomials we use, we get

where . Before describing the chaos decomposition formulas we use in the algorithm, we give a lemma useful in the sequel.

Lemma 2.5

Let , and let . For , let us define

Then is a martingale and

2.3 Chaos decomposition formulas

These formulas are based on the decomposition (6). To get tractable formulas, we consider a finite number of chaos and a finite number of functions . The functions are chosen such that we can quickly compute and [as required in (2)]. We develop in this section the case , and we refer to Section B.2 when .

The first step consists in considering a finite number of chaos. In order to approximate the random variable , we consider its projection onto the first chaos, namely

| (7) |

Of course, we still have an infinite number of terms in the previous sum and the second step consists in working with only the first functions of an orthonormal basis of .

Let us consider a regular mesh grid of time steps and the step functions

| (8) |

We complete these functions into an orthonormal basis of , . For instance, one can consider the Haar basis on each interval , . We implicitly assume that . This leads to the following approximation:

| (9) |

where and . Due to the simplicity of the functions , , we can compute explicitly

Roughly speaking this means that , the th chaos, is generated by

Thus the approximation we will use for the random variable is

where the coefficients and are given by

| (11) |

The following lemma, similar to Lemma 2.4, gives some useful properties of the operator .

Lemma 2.6

Let be a r.v. in and be in . Then:

-

•

.

-

•

.

-

•

For all , .

From (2.3), we deduce the expressions of and , useful for the approximation of by the chaos decomposition; see (2).

Proposition 2.7

Let be a real random variable in , and let be an integer in . For all , we have

where, if and , stands for .

Remark 2.8.

For and , Proposition 2.7 leads to

When , we get , and we define [which is the limit of when tends to ].

Let us end this subsection by some examples.

3 Description of the algorithm

The algorithm is based on four types of approximations: Picard’s iterations, a Wiener chaos expansion up to a finite order, the truncation of an basis in order to apply formulas of Proposition 2.7, and a Monte Carlo method to approximate the coefficients and defined in (11). We present the first three steps of the approximation procedure in Section 3.1. The Monte Carlo method and the practical implementation are presented in Section 3.2.

3.1 Approximation procedure

3.1.1 Picard’s iterations

The first step consists in approximating —the solution to (1)—by Picard’s sequence , built as follows: and for all

| (12) |

From (12), under the assumptions that and , we express as a function of the processes ,

| (13) |

which can also be written

As we recalled in the Introduction, the computation of the conditional expectation is the cornerstone in the numerical resolution of BSDEs. Chaos decomposition formulas enable us to circumvent this problem.

3.1.2 Wiener Chaos expansion

Computing the chaos decomposition of the r.v. [appearing in (13)] in order to compute is not judicious. depends on , and then the computation of on the grid would require calls to the chaos decomposition function. To build an efficient algorithm, we need to call the chaos decomposition function as infrequently as possible, since each call is computationally demanding and brings an approximation error due to the truncation and to the Monte Carlo approximation (see next sections). Then we look for a r.v. independent of such that and can be expressed as functions of , and of and . Equation (3.1.1) gives a more tractable expression of . Let be defined by . Then

| (15) |

The second type of approximation consists of computing the chaos decomposition of up to order . Since does not depend on , the chaos decomposition function is called only once per Picard’s iteration.

Let denote the approximation of built at step using a chaos decomposition with order : and

where . In the sequel, we also use the following equality:

| (17) |

3.1.3 Truncation of the basis

The third type of approximation comes from the truncation of the orthonormal basis used in the definition of (7). Instead of considering a basis of , we only keep the first functions defined by (8) to build the chaos decomposition function (9). Proposition 2.7 gives us explicit formulas for and . From (3.1.2), we build in the following way: and

where .

Equation (3.1.3) is tractable as soon as we know closed formulas for thecoefficients of the chaos decomposition of and; see Proposition 2.7. When it is not the case, we need to use a Monte Carlo method to approximate these coefficients. The next section is devoted to this method and to the practical implementation. In particular, we give the pseudo-code of the algorithm.

3.2 Implementation

In this section, we first explain how to practically compute the chaos decomposition of a r.v. . Then we give the pseudo-code of the algorithm.

3.2.1 Monte Carlo simulations of the chaos decomposition

Let denote a r.v. of . Practically, when we are not able to compute exactly and/or the coefficients of the chaos decomposition (2.3)–(11) of , we use Monte Carlo simulations to approximate them. Let be a i.i.d. sample of and be a i.i.d. sample of . We recall that and the coefficients are given by and ; see (11). Then they are solutions of

| (19) |

where . We propose two methods to approximate :

-

•

the first one consists in approximating the expectations of (11) by empirical means where

(20) -

•

the second one is based on a sample average approximation

Remark 3.1.

In terms of computation time, the first method is much faster than the second one.

-

•

The first method requires computations per coefficient. Since we are looking for coefficients, its computational cost is .

-

•

The second method requires computations to evaluate (in fact, it requires the same number of computations as the first method, since the function contains as many additions as coefficients, and each addition contains as many products as the associated coefficient). We still have to compute the argmin, the computational cost of which depends on the method we use.

From a theoretical point of view, the second method gives better convergence results than the first one. For the first method, we only know that converges to a.s. Concerning the second method, we know that converges to a.s., and under regularity assumptions on , the uniform strong law of large numbers gives the a.s. convergence of to .

In the following, denotes the approximation of the chaos decomposition of order of when using the first method to approximate the coefficients :

| (21) |

and denote the conditional expectations obtained in Proposition 2.7 when are replaced by ,

Remark 3.2.

When samples of are needed, we can either use the same samples as the ones used to compute and : , or use new ones. In the first case, we only require samples of and . The coefficients and are not independent of . The notation introduced above cannot be linked to . In the second case, the coefficients and are independent of , and we have . This second approach requires samples of and , and its variance increases with . Practically, we use the first technique.

We introduce the processes , which is useful in the following. It corresponds to the approximation of when we use instead of , that is, when we use a Monte Carlo procedure to compute the coefficients .

where and .

3.2.2 Pseudo-code of the algorithm

In this section, we describe in details the algorithm. We aim at computing trajectories of an approximation of on the grid . Starting from , (3.2.1) enables to get for each of Picard’s iterations on . Practically, we discretize the integral which leads to approximated values of computed on a grid.

Let us introduce , defined by and for all

where . Here is the notation we use in the algorithm:

-

•

: dimension of the Brownian motion;

-

•

: index of Picard’s iteration;

-

•

: number of Picard’s iterations;

-

•

: number of Monte Carlo samples;

-

•

: number of time steps used for the discretization of and ;

-

•

: order of the chaos decomposition;

-

•

represents paths of computed on the grid ;

-

•

for all , represents paths of computed on the grid .

Since , can be written as a measurable function of the Brownian path. Then one gets one sample of from one sample of (where represents ).

For the sake of clarity, we detail the algorithm for .

Let us now deal with the complexity of the algorithm:

For each :

-

•

the computation of the vector (loop line 5) requires computations;

- •

- •

The complexity of the algorithm is then .

4 Convergence results

We aim at bounding the error between —the solution of (1)—and defined by (3.2.1). Before stating the main result of the paper, we introduce some hypotheses.

In the following, and denote two vectors such that

Hypothesis 4.1 ((Hypothesis ))

Let . We say that satisfies Hypothesis if satisfies the two following hypotheses:

-

•

: , that is, ;

-

•

: , , , , and for all multi-indices and such that and , there exist two positive constants and such that

where . In the following, we denote .

Remark 4.2.

If satisfies , for all multi-index such that , we have

| (24) |

where is a constant.

Hypothesis 4.3 ((Hypothesis ))

Let . We say that an r.v. satisfies if

Remark 4.4.

If is bounded by , we get . Then every bounded r.v. satisfies .

This remark ensues from .

Remark 4.5.

Let be the -valued process solution of

where is a -dimensional Brownian motion and and are two functions uniformly Lipschitz w.r.t. and Hölder continuous of parameter w.r.t. , with linear growth in and with bounded derivatives. Then, every random variable of type or with in satisfies and , for all and .

Theorem 4.6

Let be an integer s.t. . Assume that satisfies and and . We have

where is given in Section 4.1, is given in Proposition 4.11, is given in Proposition 4.15, and is given in Proposition 4.17.

If and satisfies and , we get

Remark 4.7.

If is a path-dependent generator, Theorem 4.6 still holds true under the following hypotheses: , , for all multi-index in ( is the dimension of the Brownian motion) s.t. means that the Malliavin derivative w.r.t. concerns the path-dependent component, and we assume

where , and and are two positive constants.

Remark 4.8.

Given the complexity of the algorithm (and a given value of ), we can choose the parameters and such that they minimize the error , where . This boilds down to solving the following constrained minimization problem:

The Karush–Kuhn–Tucker theorem gives , , and such that .

Proof of Theorem 4.6 We split the error into terms: {longlist}[(1)]

Picard’s iterations. , where is defined by (12);

the truncation of the chaos decomposition. , where is defined by (3.1.2);

the truncation of the basis. , where is defined by (3.1.3);

the Monte Carlo approximation to compute the expectations., where is defined by (3.2.1). We have

It remains to combine (25), Propositions 4.11, 4.15 and 4.17 to get the first result.

4.1 Picard’s iterations

The first type of error has already been studied in pardoux92 and karoui97 , and we only recall the main result.

Hypothesis 4.9

We assume:

-

•

the generator is Lipschitz continuous: there exists a constant such that for all , and

-

•

.

4.2 Error due to the truncation of the chaos decomposition

We assume that the integrals are computed exactly, as well as expectations. The error is only due to the truncation of the chaos decomposition introduced in (• ‣ 2.2.1).

For the sequel, we also need the following lemma. We postpone its proof to the Appendix A.2.

Lemma 4.10

Assume that satisfies and . Then , , and belong to . Moreover

where is a constant depending on and on.

Proposition 4.11

Let . Assume that satisfies and . We recall . We get

| (26) |

where is a scalar and depends on , , and on .

Remark 4.12.

We deduce from Proposition 4.11 that for all and , we have . When , that is, for small enough, we also get .

Proof of Proposition 4.11 For the sake of clearness, we assume . In the following, one notes , and . First, we deal with. From (15) and (3.1.2) we get

We introduce in the second conditional expectation. This leads to

where we have used the second property of Lemma 2.4 to rewrite the third term.

From the previous equation, we bound by using Doob’s inequality and the Lipschitz property of

To bound the second expectation of the previous inequality, we use the first property of Lemma 2.4 and the Lispchitz property of . Then we bring together this term with the last one to get

4.3 Error due to the truncation of the basis

Before giving an upper bound for the error, we measure the error between and for a r.v. satisfying (24) when .

Remark 4.13.

Let , satisfies and . Then, for all integers and , satisfies (24); that is, for all multi-index such that , we have

where and depends on , , and on .

Lemma 4.14

We refer to Section A.4 for the proof of the lemma.

Proposition 4.15

Assume that satisfies and . We recall . We get

| (29) |

where is a scalar and depends on , , and on .

Since , we deduce from (29) that , where . Then, converges to when tends to in .

Proof of Proposition 4.15 For the sake of clarity, we assume . In the following, we note , and . First, we deal with . From (3.1.2) and (3.1.3) we get

Following the same steps as in the proof of Proposition 4.11, we get

| (30) | |||

Let us now upper bound . Following the same steps as in the proof of Proposition 4.11, we get

| (31) | |||

4.4 Error due to the Monte Carlo approximation

We are now interested in bounding the error between defined by (3.1.3) and defined by (3.2.1). is defined by (20) and (21). In this section, we assume that the coefficients are independent of the vector , which corresponds to the second approach proposed in Remark 3.2.

Before giving an upper bound for the error, we measure the error between and for a r.v. satisfying (see Hypothesis 4.3).

Lemma 4.16

Let be a r.v. satisfying Hypothesis . We have

Moreover, we have .

We refer to Section A.5 for the proof of the lemma.

Proposition 4.17

Let satisfy Hypothesis and be a bounded function. Let . We get

where is a scalar and .

Since , we deduce from the previous inequality that , where . Then converges to when tends to in .

Proof of Proposition 4.17 For the sake of clarity, we assume . In the following, note that , and . First, we deal with . From (3.1.3) and (3.2.1) we get

By introducing and by using Lemma 2.6, we obtain

From Lemma 4.16, we get . Then

| (32) | |||

Let us now upper bound . Following the same steps as in the proof of Proposition 4.11, we get

| (33) | |||

5 Numerical examples

The computations have been done on a PC INTEL Core 2 Duo P9600 2.53 GHz with 4Gb of RAM.

5.1 Nonlinear driver and path-dependent terminal condition

We consider the case , and .

-

•

Convergence in . Tables 1 and 2 represent the evolution of and w.r.t (Picard’s iteration index), when and . We also give the CPU time needed to get and . We fix and . The seed of the generator is also fixed.

Table 1: Evolution of w.r.t. Picard’s iterations, , and CPU time Iterations 1 2 3 4 5 6 CPU time 1.656357 1.017117 1.237135 1.186691 1.195462 1.194256 14.06 1.656357 1.012091 1.234398 1.183544 1.192367 1.191173 174.09 Table 2: Evolution of w.r.t. Picard’s iterations, , and CPU time Iterations 1 2 3 4 5 6 CPU time 0.969128 0.249148 0.525273 0.459326 0.470069 0.469117 14.06 0.969128 0.242977 0.523846 0.455827 0.466903 0.465939 174.09 Note that the difference between the values of and (resp., and ) does not exceed (resp., ). This is due to the fast convergence of the algorithm in . The CPU time is times higher when than when . Then, the use of order in the chaos decomposition is not necessary. In the following, we take .

-

•

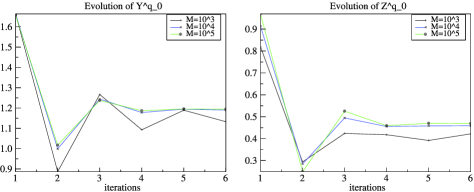

Convergence in . Figure 1 illustrates the evolution of and w.r.t. when and for different values of . The seed of the generator is random. When equals and the algorithm stabilizes after very few iterations. When , there is no convergence.

Figure 1: Evolution of and w.r.t. and when , , .

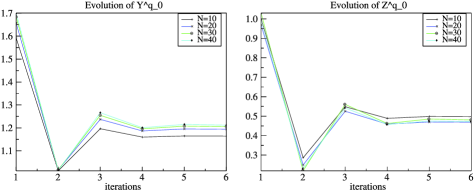

Figure 2: Evolution of and w.r.t. when , , . -

•

Convergence in . Figure 2 illustrates the evolution of and w.r.t. when and for different values of . The seed of the generator is random. The algorithm converges even when , but is quite below .

5.2 Linear driver-financial benchmark

We consider the case of pricing and hedging a discrete down and out barrier call option, that is, and , where represents the Black–Scholes diffusion

The option parameters are , , , , , and ( is also the number of time discretizations of the chaos decomposition).

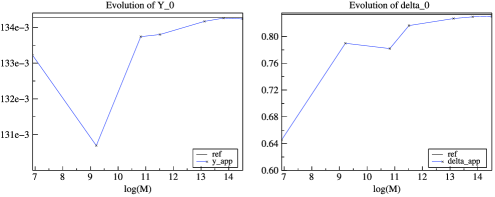

We can get a benchmark for and by using a variance reduction Monte Carlo method. For this set of parameters, the reference values are with a confidence interval and . We compare them with and when , , (we choose the first value of from which the algorithm has converged) for different values of . Figure 3 represents the evolution of and w.r.t. . Notice that for the computed values are very close to the reference values.

5.3 Nonlinear driver in dimension , financial benchmark

We consider the pricing and hedging of a put basket option in dimension , that is, , where

(resp., ) represents the trend (resp., the volatility) of the th asset. is a -dimensional Brownian motion such that . We suppose that , which ensures that the matrix is positive definite. We also assume that the borrowing rate is higher than the bond rate . In such a case, pricing and hedging the put basket option is equivalent to solving a BSDE with terminal condition and with driver defined by , where ( is the vector whose every component is one), and is the matrix defined by ( denote the lower triangular matrix involved in the Cholesky decomposition ). We refer to karoui97 , Example 1.1, for more details.

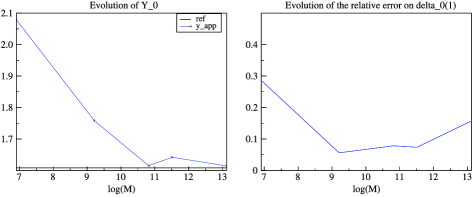

The option parameters are , , , , , and for all , , and . Figure 4 represents the evolution of , the approximated price at time and the relative error on —the quantity of asset to possess at time —w.r.t. . We compare our results with the ones obtained using the Algorithm proposed in GL10 (cited here as reference values). The CPU time needed to compute price and delta when and is s. Notice that the convergence is very fast and quite accurate for .

Conclusion. In this paper, we use Wiener chaos expansions together with the Picard procedure to compute the solution to (1). Once the chaos decomposition of is computed, we get explicit formulas for both conditional expectations and the Malliavin derivative of conditional expectations. This enables us to easily compute . Numerically, we obtain fast and accurate results, which encourage us to extend these results to other type of BSDEs, like 2-BSDEs. It is also possible to couple these Wiener chaos expansions together with the dynamic programming approach. This will be the subject of a forthcoming publication.

Appendix A Technical results of Section 4

In the following, for any regular r.v. , denotes .

A.1 Proof of Remark 4.5

Before proving Remark 4.5, we prove the following lemma.

Lemma A.1

Let be the -valued process solution of

where is a -dimensional Brownian motion and and are two functions uniformly lipschitz w.r.t. and Hölder continuous of parameter w.r.t. , with linear growth in (of constant ) and with bounded derivatives. Then:

-

•

, we have

(34) the upper bound depends on , , and ,

-

•

, , , we have

(35) where and depends on , , , and on .

Proof of Lemma A.1 The first point is proved in nualart06 , Theorem 2.2.2. For the sake of clarity, we prove the second result for . We also assume that the vectors and are such that . We do it by induction on and . We detail the case and only depending on and do the proof for and , . We recall that under these hypotheses on and , we have

where depends on , , and on , and on .

Case . We have

Then

In the following, denotes a generic constant depending only on and , and denotes the Lipschitz contant of .

We introduce . Doob’s inequality and the Burkhölder–Davis–Gundy inequality lead to

Gronwall’s lemma yields the result.

Case . We consider . We have

Then

Doob’s inequality and the Burkhölder–Davis–Gundy inequality lead to

We introduce . The Cauchy–Schwarz inequality yields

Since , and , Gronwall’s lemma ompletes the proof.

Proof of Remark 4.5 We prove the result for . We first prove that belongs to for all , that is,

contains a sum of terms of type , where varies in , and [ denotes the number of nonzero components of ]. Since , and satisfies (34), we get the result.

Let us now prove that satisfies . contains a sum of terms of type , where varies in , , , and . Then, since , satisfies (34) and (35), we get satisfies , with and depends on , on and on .

It remains to prove that satisfies . is bounded by . Since and satisfies for all , we get that is bounded. We prove that is bounded by the same way.

A.2 Proof of Lemma 4.10

We complete the proof for . We prove by induction that , belongs to , that is,

Using (15) gives

where .

Using the definition of and applying Doob’s inequality leads to

where is a generic constant depending on and .

contains a sum of terms of type , where , , and . Then Hölder’s inequality gives

| (36) | |||

and

| (37) | |||

A.3 Proof of Remark 4.13

For the sake of clarity, we assume that , and . Then we show that if satisfies and , then satisfies

Since , we deal with the case . Since we have , it is enough to prove that (we refer to the beginning of Section A for the definition of ).

We introduce , two vectors and , and four integers , , and such that , , and . If , contains a sum of terms of type

where [ denotes the number of nonzero components of ] and and of type

where , . By using the Cauchy–Schwarz inequality, we get that is bounded by

(and the same type of term in ) which leads to

| (38) | |||

where . If , contains the same type of integrals between and plus an integral between and , which is bounded by . Then, since and , it remains to take the supremum over in (A.3) and to apply Lemma A.2 to end the proof. depends on , , and (where is defined in Lemma A.2).

Lemma A.2

Assume satisfies and . Then , , and

where and depends on , , and on .

We complete the proof by induction on . We distinguishcases and . We first consider . Let be in and (if , the first term on the right-hand side of the following equality vanishes). From (3.1.2) and Lemma 2.4, we get . Using the definition of [see (3.1.2)], Doob’s inequality and Lemma 2.4 yields

| (39) | |||

where denotes a generic constant depending on , and .

Let us now upper bound . Using (17) and the Clark–Ocone formula gives . Hence, for , we have . Then, we get

The left-hand side of the Burkhölder–Davis–Gundy inequality gives

where denotes a generic constant depending on and . Adding (A.3) to the previous equation leads to

We introduce two vectors and , and four integers , , and such that , , and . contains a sum of terms of type

where and and of type

where , .

By using Cauchy–Schwarz inequality, we get that is bounded by

(and the same type of term in ) which leads to

It remains to plug this result into (A.3), to take the supremum in and to apply the induction hypothesis to obtain

and the result follows. If , we get

When bounding , we deal with the first two terms as we did before, we bound the term by

which completes the proof.

A.4 Proof of Lemma 4.14

We prove the result by induction. Lemma 4.14 is true for , since . Assume that . Since we have

it remains to show that . We recall

| (43) |

where

| (44) |

where Let us rewrite as a sum of stochastic integrals. Let . Applying Lemma 2.5 to yields is a martingale and . Then, . For and , we get

For , we obtain

To compare and , we split the integrals in (43),

Combining (44), (A.4), (A.4) and (A.4) yields

| (48) | |||

Moreover,

Since satisfies Hypothesis 4.1, we get . Then . Plugging this result into (A.4) completes the proof.

A.5 Proof of Lemma 4.16

Appendix B Wiener chaos expansion formulas

B.1 Proof of Proposition 2.7

B.2 Wiener chaos expansion formulas in

We want to approximate using its chaos decomposition up to order . We assume . We consider the following truncated basis of :

where is a regular mesh grid, and represents the canonical basis of . , the th chaos, is generated by

For , , one notes , , and for , . , , and . Since the r.v. are orthogonal ones, the projection of is given by

where the coefficients are given by

Proposition B.1

For , we have

and for ,

Remark B.2.

In particular, for , and ,

When , we get , and we define , where is a matrix of size whose component equals and the other ones are null.

Proof of Proposition B.1 We first compute for . We have

Since Brownian motions and their increments are independents, we get

which is null as soon as . Then nested conditional expectations give

From Lemma 2.5, for is a martingale and . Then is also a martingale, and the first result follows. Since, we get the second result.

References

- (1) {bincollection}[mr] \bauthor\bsnmBally, \bfnmV.\binitsV. (\byear1997). \btitleApproximation scheme for solutions of BSDE. In \bbooktitleBackward Stochastic Differential Equations (Paris, 1995–1996) (\beditor\binitsN.\bfnmN. \bsnmEl Karoui and \beditor\binitsL.\bfnmL. \bsnmMazliak, eds.) \bseriesPitman Res. Notes Math. Ser. \bvolume364 \bpages177–191. \bpublisherLongman, \blocationHarlow. \bidmr=1752682 \bptokimsref \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmBally, \bfnmVlad\binitsV. and \bauthor\bsnmPagès, \bfnmGilles\binitsG. (\byear2003). \btitleA quantization algorithm for solving multi-dimensional discrete-time optimal stopping problems. \bjournalBernoulli \bvolume9 \bpages1003–1049. \biddoi=10.3150/bj/1072215199, issn=1350-7265, mr=2046816 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmBender, \bfnmChristian\binitsC. and \bauthor\bsnmDenk, \bfnmRobert\binitsR. (\byear2007). \btitleA forward scheme for backward SDEs. \bjournalStochastic Process. Appl. \bvolume117 \bpages1793–1812. \biddoi=10.1016/j.spa.2007.03.005, issn=0304-4149, mr=2437729 \bptokimsref \endbibitem

- (4) {bmisc}[auto:STB—2013/10/14—10:36:11] \bauthor\bsnmBender, \bfnmC.\binitsC. and \bauthor\bsnmSteiner, \bfnmJ.\binitsJ. (\byear2013). \bhowpublishedLeast-squares Monte Carlo for BSDEs. In Numerical Methods in Finance (Carmon et al., eds.) 257–289. Springer, Berlin. \bptokimsref \endbibitem

- (5) {barticle}[mr] \bauthor\bsnmBismut, \bfnmJean-Michel\binitsJ.-M. (\byear1973). \btitleConjugate convex functions in optimal stochastic control. \bjournalJ. Math. Anal. Appl. \bvolume44 \bpages384–404. \bidissn=0022-247X, mr=0329726 \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmBouchard, \bfnmBruno\binitsB. and \bauthor\bsnmTouzi, \bfnmNizar\binitsN. (\byear2004). \btitleDiscrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. \bjournalStochastic Process. Appl. \bvolume111 \bpages175–206. \biddoi=10.1016/j.spa.2004.01.001, issn=0304-4149, mr=2056536 \bptokimsref \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmBriand, \bfnmPhilippe\binitsP., \bauthor\bsnmDelyon, \bfnmBernard\binitsB. and \bauthor\bsnmMémin, \bfnmJean\binitsJ. (\byear2001). \btitleDonsker-type theorem for BSDEs. \bjournalElectron. Commun. Probab. \bvolume6 \bpages1–14 (electronic). \biddoi=10.1214/ECP.v6-1030, issn=1083-589X, mr=1817885 \bptokimsref \endbibitem

- (8) {barticle}[mr] \bauthor\bsnmBriand, \bfnmPhilippe\binitsP., \bauthor\bsnmDelyon, \bfnmBernard\binitsB. and \bauthor\bsnmMémin, \bfnmJean\binitsJ. (\byear2002). \btitleOn the robustness of backward stochastic differential equations. \bjournalStochastic Process. Appl. \bvolume97 \bpages229–253. \biddoi=10.1016/S0304-4149(01)00131-4, issn=0304-4149, mr=1875334 \bptokimsref \endbibitem

- (9) {bmisc}[auto:STB—2013/10/14—10:36:11] \bauthor\bsnmChevance, \bfnmD.\binitsD. (\byear1997). \bhowpublishedRésolution numérique des équations différentielles stochastiques rétrogrades. Ph.D. thesis, Univ. de Provence—Aix–Marseille I, Marseille. \bptokimsref \endbibitem

- (10) {barticle}[mr] \bauthor\bsnmCoquet, \bfnmFrançois\binitsF., \bauthor\bsnmMackevičius, \bfnmVigirdas\binitsV. and \bauthor\bsnmMémin, \bfnmJean\binitsJ. (\byear1999). \btitleCorrigendum to: “Stability in of martingales and backward equations under discretization of filtration” [Stochastic Processes Appl. 75 (1998) 235–248]. \bjournalStochastic Process. Appl. \bvolume82 \bpages335–338. \biddoi=10.1016/S0304-4149(99)00020-4, issn=0304-4149, mr=1700013 \bptokimsref \endbibitem

- (11) {barticle}[mr] \bauthor\bsnmDelarue, \bfnmFrançois\binitsF. and \bauthor\bsnmMenozzi, \bfnmStéphane\binitsS. (\byear2006). \btitleA forward–backward stochastic algorithm for quasi-linear PDEs. \bjournalAnn. Appl. Probab. \bvolume16 \bpages140–184. \biddoi=10.1214/105051605000000674, issn=1050-5164, mr=2209339 \bptokimsref \endbibitem

- (12) {barticle}[mr] \bauthor\bsnmEl Karoui, \bfnmN.\binitsN., \bauthor\bsnmPeng, \bfnmS.\binitsS. and \bauthor\bsnmQuenez, \bfnmM. C.\binitsM. C. (\byear1997). \btitleBackward stochastic differential equations in finance. \bjournalMath. Finance \bvolume7 \bpages1–71. \biddoi=10.1111/1467-9965.00022, issn=0960-1627, mr=1434407 \bptokimsref \endbibitem

- (13) {barticle}[mr] \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE. and \bauthor\bsnmLabart, \bfnmCéline\binitsC. (\byear2007). \btitleError expansion for the discretization of backward stochastic differential equations. \bjournalStochastic Process. Appl. \bvolume117 \bpages803–829. \biddoi=10.1016/j.spa.2006.10.007, issn=0304-4149, mr=2330720 \bptokimsref \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE. and \bauthor\bsnmLabart, \bfnmCéline\binitsC. (\byear2010). \btitleSolving BSDE with adaptive control variate. \bjournalSIAM J. Numer. Anal. \bvolume48 \bpages257–277. \biddoi=10.1137/090755060, issn=0036-1429, mr=2608369 \bptokimsref \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE., \bauthor\bsnmLemor, \bfnmJean-Philippe\binitsJ.-P. and \bauthor\bsnmWarin, \bfnmXavier\binitsX. (\byear2005). \btitleA regression-based Monte Carlo method to solve backward stochastic differential equations. \bjournalAnn. Appl. Probab. \bvolume15 \bpages2172–2202. \biddoi=10.1214/105051605000000412, issn=1050-5164, mr=2152657 \bptokimsref \endbibitem

- (16) {barticle}[mr] \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE. and \bauthor\bsnmMakhlouf, \bfnmAzmi\binitsA. (\byear2010). \btitle-time regularity of BSDEs with irregular terminal functions. \bjournalStochastic Process. Appl. \bvolume120 \bpages1105–1132. \biddoi=10.1016/j.spa.2010.03.003, issn=0304-4149, mr=2639740 \bptokimsref \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmLemor, \bfnmJean-Philippe\binitsJ.-P., \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE. and \bauthor\bsnmWarin, \bfnmXavier\binitsX. (\byear2006). \btitleRate of convergence of an empirical regression method for solving generalized backward stochastic differential equations. \bjournalBernoulli \bvolume12 \bpages889–916. \biddoi=10.3150/bj/1161614951, issn=1350-7265, mr=2265667 \bptokimsref \endbibitem

- (18) {bbook}[mr] \bauthor\bsnmMa, \bfnmJin\binitsJ. and \bauthor\bsnmYong, \bfnmJiongmin\binitsJ. (\byear1999). \btitleForward–backward Stochastic Differential Equations and Their Applications. \bseriesLecture Notes in Math. \bvolume1702. \bpublisherSpringer, \blocationBerlin. \bidmr=1704232 \bptokimsref \endbibitem

- (19) {bbook}[mr] \bauthor\bsnmNualart, \bfnmDavid\binitsD. (\byear2006). \btitleThe Malliavin Calculus and Related Topics, \bedition2nd ed. \bpublisherSpringer, \blocationBerlin. \bidmr=2200233 \bptokimsref \endbibitem

- (20) {bincollection}[mr] \bauthor\bsnmPardoux, \bfnmÉ.\binitsÉ. and \bauthor\bsnmPeng, \bfnmS.\binitsS. (\byear1992). \btitleBackward stochastic differential equations and quasilinear parabolic partial differential equations. In \bbooktitleStochastic Partial Differential Equations and Their Applications (Charlotte, NC, 1991). \bseriesLecture Notes in Control and Inform. Sci. \bvolume176 \bpages200–217. \bpublisherSpringer, \blocationBerlin. \biddoi=10.1007/BFb0007334, mr=1176785 \bptokimsref \endbibitem

- (21) {barticle}[mr] \bauthor\bsnmPardoux, \bfnmÉ.\binitsÉ. and \bauthor\bsnmPeng, \bfnmS. G.\binitsS. G. (\byear1990). \btitleAdapted solution of a backward stochastic differential equation. \bjournalSystems Control Lett. \bvolume14 \bpages55–61. \biddoi=10.1016/0167-6911(90)90082-6, issn=0167-6911, mr=1037747 \bptokimsref \endbibitem

- (22) {barticle}[mr] \bauthor\bsnmRichou, \bfnmAdrien\binitsA. (\byear2011). \btitleNumerical simulation of BSDEs with drivers of quadratic growth. \bjournalAnn. Appl. Probab. \bvolume21 \bpages1933–1964. \biddoi=10.1214/10-AAP744, issn=1050-5164, mr=2884055 \bptokimsref \endbibitem

- (23) {barticle}[mr] \bauthor\bsnmZhang, \bfnmJianfeng\binitsJ. (\byear2004). \btitleA numerical scheme for BSDEs. \bjournalAnn. Appl. Probab. \bvolume14 \bpages459–488. \biddoi=10.1214/aoap/1075828058, issn=1050-5164, mr=2023027 \bptokimsref \endbibitem