Theory and Inference for a Class of Observation-Driven Models with Application to Time Series of Counts

Abstract

This paper studies theory and inference related to a class of time series models that incorporates nonlinear dynamics. It is assumed that the observations follow a one-parameter exponential family of distributions given an accompanying process that evolves as a function of lagged observations. We employ an iterated random function approach and a special coupling technique to show that, under suitable conditions on the parameter space, the conditional mean process is a geometric moment contracting Markov chain and that the observation process is absolutely regular with geometrically decaying coefficients. Moreover the asymptotic theory of the maximum likelihood estimates of the parameters is established under some mild assumptions. These models are applied to two examples; the first is the number of transactions per minute of Ericsson stock and the second is related to return times of extreme events of Goldman Sachs Group stock.

Keywords: Absolute regularity; Ergodicity; Geometric moment contraction; Iterated random functions; One-parameter exponential family; Time series of counts

1 Introduction

With a surge in the range of applications from economics, finance, environmental science, social science and epidemiology, there has been renewed interest in developing models for time series of counts. The majority of these models assume that the observations follow a Poisson distribution conditioned on an accompanying intensity process that drives the dynamics of the models, e.g., Davis et al. (2003), Fokianos et al. (2009), Neumann (2011), Streett (2000) and Doukhan et al. (2012). According to whether the evolution of the intensity process depends on the observations or solely on an external process, Cox (1981) classified the models into observation-driven and parameter-driven. This paper focuses on the theory and inference for a particular class of observation-driven models.

Many of the commonly used models, such as the Poisson integer-valued GARCH (INGARCH), are special cases of our model. For an INGARCH, the observations given the intensity process follow a Poisson distribution and is a linear combination of its lagged values and lagged . The model is capable of capturing positive temporal correlation in the observations and it is relatively easy to fit via maximum likelihood. Ferland et al. (2006) showed the second moment stationarity through a sequence of approximating processes and Fokianos et al. (2009) established the consistency and asymptotic normality of the MLE by introducing a perturbed model. However, all the above results rely heavily on the Poisson assumption and the GARCH-like dynamics of . Later Neumann (2011) relaxed the linear assumption to a general contracting evolution rule and proved the absolute regularity for this Poisson count process and Doukhan et al. (2012) showed the existence of moments under similar conditions by utilizing the concept of weak dependence.

In our study the conditional distribution of the observation given the past is assumed to follow a one-parameter exponential family. The temporal dependence in the model is defined through recursions relating the conditional mean process with its lagged values and lagged observations. Theory from iterated random functions (IRF), see e.g., Diaconis and Freedman (1999) and Wu and Shao (2004), is utilized to establish some key stability properties, such as existence of a stationary and mixing solution. This theory allows us to consider both linear and nonlinear dynamic models as well as inference questions. In particular, the asymptotic normality of the maximum likelihood estimates can be established. The nonlinear dynamic models are also investigated in a simulation study and both linear and nonlinear models are applied to two real datasets.

The organization of the paper is as follows. Section 2 formulates the model and establishes stability properties. The maximum likelihood estimates of the parameters and the relevant asymptotic theory are derived in Section 3. Examples of both linear and nonlinear dynamic models are considered in Section 4. Numerical results, including a simulation study and two data applications are given in Section 5, where the models are applied to the number of transactions per minute of Ericsson stock and to the return times of extreme events of Goldman Sachs Group (GS) stock. Some diagnostic tools for assessing and comparing model performance are also given in Section 5. Appendix A reviews some standard properties of the one-parameter exponential family and the proofs of the key results in Sections 2-4 are deferred to Appendix B.

2 Model formulation and stability properties

2.1 One-parameter exponential family

A random variable is said to follow a distribution of the one-parameter exponential family if its probability density function with respect to some -finite measure is given by

| (2.1) |

where is the natural parameter, and and are known functions. If , then it is known that and . The derivative of exists generally for the exponential family, see e.g., Lehmann and Casella (1998). Since , so is strictly increasing, which establishes a one-to-one association between the values of and . Moreover, because we assume that the support of is non-negative throughout this paper, so , which implies that is strictly increasing. Other properties of this family of distributions are presented in Appendix A.

Many familiar distributions belong to this family, including Poisson, negative binomial, Bernoulli, exponential, etc. If the shape parameter is fixed, then the gamma distribution is also a member of this family. While we restrict consideration to only the univariate case, extensions to the multi-parameter exponential family is a topic of future research.

2.2 Model formulation

Set , where is a natural parameter of (2.1) and assumed fixed for the moment. Let be observations from a model that is defined recursively in the following fashion,

| (2.2) |

for all , where is defined in (2.1), and is the conditional mean process, i.e., . Here is a non-negative bivariate function defined on when has a continuous conditional distribution or on , where , when only takes non-negative integers. Throughout, we assume that the function satisfies a contraction condition, i.e., for any , and ,

| (2.3) |

where and are non-negative constants with . Note that (2.3) implies

| (2.4) |

We point out that model (2.2) with the function satisfying (2.3) includes the Poisson INGARCH model (see Example 4.1) and the exponential autoregressive model (4.14) as special cases under some restrictions on the parameter space. The generalized linear autoregressive moving average model (GLARMA) (see Davis et al. (2003)) also belongs to this class, although the contraction condition is not necessarily satisfied. Only under very simple model specifications have the stability properties of GLARMA been established and the relevant work is still ongoing. The primary focus of this paper is on the conditional mean process , which can be easily seen as a time-homogeneous Markov chain. Note that the observation process is not a Markov chain itself.

2.3 Strict stationarity

The iterated random function approach (see e.g., Diaconis and Freedman (1999) and Wu and Shao (2004)) provides a useful tool when investigating the stability properties of Markov chains and turns out to be particularly instrumental in our research. In the definition of iterated random functions (IRF), the state space is assumed to be a complete and separable metric space. Then a sequence of iterated random functions is defined through

where take values in another measurable space and are independently distributed with identical marginal distribution, and is independent of .

In working with iterated random functions, Wu and Shao (2004) introduces the idea of geometric moment contraction (GMC), which is useful for deriving further properties of IRF. Our research is also relying heavily on GMC. Suppose there exists a stationary solution to the Markov chain , denoted by , let be independent of each other and of , and define . Then is said to be geometric moment contracting if there exist an , a and an such that, for all ,

The conditional mean process specified in (2.2) can be embedded into the framework of IRF and shown to be GMC.

In this section and the next we use to represent the function in (2.2) evaluated at the true parameter. For any , the random function is defined as

| (2.5) |

where is the cumulative distribution function of in (2.1) with , and its inverse for . Let be a sequence of independent and identically distributed (iid) uniform random variables, then the Markov chain defined in (2.2) starting from can be represented as the so-called forward process . The corresponding backward process is defined as , which has the same distribution as for any .

Proposition 1. Assume model (2.2) and that the function satisfies the contraction condition (2.3). Then

-

1.

There exists a random variable such that, for all , almost surely. The limit does not depend on and has distribution , which is the stationary distribution of .

-

2.

The Markov chain is geometric moment contracting with as its unique stationary distribution. In addition, .

-

3.

If starts from , i.e., , then is a stationary time series.

Proposition 2.3 implies that starting from any state , the limiting distribution of the Markov chain exists and the -step transition probability measure converges weakly to , as .

2.4 Ergodicity

In this section we further investigate the stability properties, including ergodicity and mixing for model (2.2). Under the conditions of Proposition 2.3, the process is strictly stationary, so we can extend it to be indexed by all the integers. The following proposition establishes ergodicity and absolute regularity when is discrete.

Proposition 2. Assume model (2.2) where the support of is a subset of , and that satisfies the contraction condition (2.3). Then

-

1.

There exists a measurable function such that almost surely.

-

2.

The count process is absolutely regular with coefficients satisfying

and hence is ergodic.

When has a continuous distribution, geometric ergodicity of can be established under stronger conditions on . The proof of the result relies on the classic Markov chain theory since is -irreducible due to the continuity of the distribution in this situation.

Proposition 3. Assume model (2.2) where the support of is , and that the function satisfies the contraction condition (2.3). Moreover if is increasing and continuous in , then

-

1.

There exists such that almost surely.

-

2.

The Markov chain is geometrically ergodic provided that , and hence is stationary and ergodic.

3 Likelihood Inference

In this section, we consider maximum likelihood estimates of the parameters and study their asymptotic behavior, including consistency and asymptotic normality. Denote the dimensional parameter vector by , i.e., , and the true parameter vector by . Then the likelihood function of model (2.2) conditioned on and based on the observations is given by

where is updated through the iterations . The log-likelihood function, up to a constant independent of , is given by

| (3.1) |

with score function

| (3.2) |

The maximum likelihood estimator is a solution to the equation . Let be the probability measure under the true parameter and unless otherwise indicated, is taken under . Recall that according to part (a) of Propositions 2.4 and 2.4. We will derive the asymptotic properties of the maximum likelihood estimator based on a set of regularity conditions:

-

(A0)

is an interior point in the compact parameter space .

-

(A1)

For any , , where is the range of . Moreover for all .

-

(A2)

For any or , the mapping is continuous.

-

(A3)

is increasing in if given has a continuous distribution.

-

(A4)

.

-

(A5)

If there exists a such that , -a.s., then .

-

(A6)

The mapping is twice continuously differentiable.

-

(A7)

, for .

Strong consistency of the estimates is derived according to the lemma below, which is adapted from Lemma 3.11 in Pfanzagl (1969).

Lemma 1. Assume that is a compact set, and that is a probability space. Let be a family of Borel measurable functions such that:

-

1.

is upper-semicontinuous for all .

-

2.

is Borel measurable for any compact set .

-

3.

for some random variable defined on .

Then

-

1.

is upper-semicontinuous.

-

2.

If is an ergodic stationary process defined on , and for all , has the same distribution as , then

for any compact set .

Pfanzagl (1969) proved the result assuming the independent structure of , but the same result proves to be true provided that the strong law of large numbers can be applied. By virtue of Lemma 3, we can derive the strong consistency of the estimates.

Theorem 1. Assume model (2.2) with the function satisfying the contraction condition (2.3), and that assumptions (A0)-(A5) hold. Then the maximum likelihood estimator is strongly consistent, that is,

The following theorem addresses the asymptotic distribution of the MLE and the idea of proof is similar to that in Davis et al. (2003). Unless otherwise indicated, and are both evaluated at , i.e., and .

Theorem 2. Assume model (2.2) with the function satisfying the contraction condition (2.3), and that assumptions (A0)-(A7) hold. Then the maximum likelihood estimator is asymptotically normal, i.e.,

where .

We remark that in practice, the population quantities in can be replaced by their estimated counterparts. Examples of such substitution will be illustrated below in specific models.

4 Examples

4.1 Linear dynamic models

The conditional mean process in these models has GARCH-like dynamics. Specifically they are described as

| (4.1) |

where , and are parameters. Observe that model (4.1) is a special case of model (2.2) by defining the function as

| (4.2) |

with and the contraction condition (2.3) corresponds to . Note that by recursion we have, for all ,

| (4.3) |

It follows that since only takes non-negative values. A direct application of Propositions 2.3, 2.4 and 2.4 gives the stability properties of model (4.1).

Proposition 4. Assume model (4.1) with . Then the process has a unique stationary distribution , and is ergodic if .

If denotes the true parameter vector, then the log-likelihood function and the score function of model (4.1) are given by (3.1) and (3.2) respectively, where is determined recursively by

| (4.4) |

The maximum likelihood estimator is a solution of the equation . Furthermore, the Hessian matrix can be found by taking derivatives of the score function, i.e.,

where

It follows from the representation with the infinite past (4.3) that assumptions (A1)-(A3) and (A6) are satisfied. In order to apply Theorem 3 when investigating the asymptotic behavior of the MLE, we need to impose the following regularity conditions:

-

(L0)

The true parameter vector lies in a compact neighborhood of , where for some .

-

(L1)

.

-

(L2)

, for .

Theorem 3. Assume model (4.1) and that assumptions (L0)-(L2) hold. Then the maximum likelihood estimator is strongly consistent and asymptotically normal, i.e.,

where , where and .

Remark 1. Under the contraction condition , can be represented as a causal ARMA(1,1) process. To see this, denote , then it follows from that is a martingale difference sequence. Therefore model (4.1) can be written as

| (4.5) |

Denote as the auto-covariance function of . If , then , for , see for example Brockwell and Davis (1991).

In practice, it can be difficult to verify assumptions (L1) and (L2), so we provide some alternative sufficient conditions for them in the following two remarks.

Remark 2. A sufficient condition for assumption (L1) is

provided that is in the range of . This can be seen by noting that .

Remark 3. If for some , this is true, for example, when is increasing and , then a sufficient condition for assumption (L2) is .

Next we consider some specific models belonging to class (4.1), most of which are geared towards modeling time series of counts.

Example 1. As a special case of the linear dynamic model (4.1) with and , the Poisson INGARCH model is given by

| (4.6) |

where are parameters. According to Proposition 4.1, it is easy to see that if , then is geometric moment contracting and has a unique stationary distribution ; moreover if , then is an ergodic stationary process. As for inference, the MLE is strongly consistent and asymptotically normal according to Theorem 4.1, i.e., , as , where . To see this, we only need to verify assumptions (L1) and (L2). Note that by Fokianos et al. (2009), we have and for , where and is a positive constant dependent on . Hence by monotone convergence theorem, we have

Hence assumption (L1) holds according to Remark 4.1. Notice that for all , so is bounded away from 0, so assumption (L2) holds according to Remark 4.1.

Moreover, the iterated random function approach can be used to study the properties of INGARCH models with higher orders. A Poisson INGARCH() model takes the form

| (4.7) |

where ; . Applying similar ideas as in the INGARCH() case, we have the following stationarity result.

Proposition 5. Consider the INGARCH model (4.7) and suppose , then is geometric moment contracting and has a unique stationary distribution.

Example 2. The negative binomial INGARCH model (NB-INGARCH) is defined as

| (4.8) |

where , are parameters and the notation represents the negative binomial distribution with probability mass function given by

When , the conditional distribution of becomes geometric distribution with probability of success , in which case (4.8) reduces to a geometric INGARCH model.

By virtue of Proposition 4.1, if , then is a geometric moment contracting Markov chain, and has a unique stationary distribution ; and when , is ergodic. As for inference, we can first estimate for fixed and calculate the profile likelihood as a function of . Then is estimated by choosing the one which maximizes the profile likelihood, and thus can be otained correspondingly. Moreover, if we assume is known and , then under assumption (L0), the maximum likelihood estimator is strongly consistent and asymptotically normal with mean and covariance matrix , where . Verification of assumptions (L1) and (L2) is sufficient to demonstrate the result. Since , so assumption (L1) holds according to Remark 4.1. Note that is increasing, so assumption (L2) holds provided according to Remark 4.1. Because , where

and , it follows from the stationarity that

Hence provided .

Example 3. We define the binomial INGARCH model as

| (4.9) |

where are parameters and since . This implies the contraction condition . In particular, when , it models time series of binary data, and is called a Bernoulli INGARCH model. If , then is geometric moment contracting and has a unique stationary distribution ; furthermore, is ergodic when .

We now consider the inference of the model. Firstly, because of the special constraint , the parameter space becomes

Since , so and . Hence assumption (L1) holds. Notice that and , so is bounded away from 0. Similar to the proof in Example 4.1, one can show that provided that . So assuming is known and , the maximum likelihood estimator is strongly consistent and asymptotically normal with mean and covariance matrix , where .

Example 4. The gamma INGARCH model, which has a continuous response, is given by

| (4.10) |

where and are the shape and scale parameters of the gamma distribution respectively and are parameters. Here the natural parameter is and the Markov chain . If , then is geometric moment contracting and has a unique stationary distribution ; furthermore, is an ergodic stationary process if .

As for the inference in this model, assume is known and . Then the maximum likelihood estimator is strongly consistent and asymptotically normal with mean and covariance matrix where . To see this, note that when , which verifies assumption (L1) according to Remark 4.1. Similar to the proof in Example 4.1, one can show that and . Hence as long as , we have . Since , assumption (L2) holds according to Remark 4.1.

4.2 Nonlinear dynamic models

It is possible to generalize (4.1) to nonlinear dynamic models. One approach is based on the idea of spline basis functions, see for example, Ruppert et al. (2003). In this framework, the model specification is given by

| (4.11) |

where , are parameters, are the so-called knots, and is the positive part of . In particular, when , (4.11) reduces to the linear model (4.1). It is easy to see that model (4.11) is a special case of model (2.2) by defining where . Note that in each of the pieces segmented by the knots, (4.11) has INGARCH-like dynamics. For example, if for some , then . This can be viewed as one of the generalizations (e.g., Samia and Chan (2010)) to the threshold autoregressive model (Tong (1990)). According to Propositions 2.3, 2.4 and 2.4, we can establish the stability properties of the model.

Proposition 6. Consider model (4.11) with parameters satisfying and for , then is geometric moment contracting and has a unique stationary distribution . Moreover if , then is ergodic.

We now consider inference for this model. Assume the knots are known for fixed. Then the parameter vector can be estimated by maximizing the conditional log-likelihood function, which is available according to (3.1). The number of knots can be selected by virtue of an information criteria, such as AIC and BIC. As for the locations of knots, there are different strategies one can adopt for choosing them. One method is to place the knots at the quantiles of the population, which can be estimated from the data. A second method is to choose the locations that maximize the log likelihood. We will employ both procedures to real datasets in the next section.

To study the asymptotic behavior of the estimates, first note that by iterating the recursion,

| (4.12) | |||||

This defines the function as in and also verifies assumptions (A1)-(A3). Hence in order to apply Theorem 4.1, we only need to impose the following regularity assumptions for the nonlinear model (4.11):

-

(NL1)

is an interior point in the parameter space , which is a compact subset of the parameter set satisfying the conditions in Proposition 4.2.

-

(NL1)

.

-

(NL2)

, for .

Sufficient conditions for assumptions (NL1) and (NL2) can be established similarly to those given in Remarks 4.1 and 4.1. The asymptotic properties of the MLE are summarized in the following theorem.

Theorem 4. For model (4.11), suppose that the placement of the knots is known, and that assumptions (NL0)-(NL2) hold, then the maximum likelihood estimator is strongly consistent and asymptotically normal, i.e.,

where .

We use the Poisson nonlinear dynamic model as an illustrative example of the above results and refer readers to Section 5 for implementation of the estimation procedure. The model is defined as

| (4.13) |

It follows that under the conditions of Proposition 4.2 and Theorem 4.2 that is a stationary and ergodic process, and the estimates are strongly consistent and asymptotically normal. In practice the covariance matrix of the estimates can be obtained by recursively applying

Another example of nonlinear dynamic models is the Poisson exponential autoregressive model proposed by Fokianos et al. (2009), and it is given by

| (4.14) |

where are parameters. We point out that if , then model (4.14) belongs to the class of models (2.2) and hence enjoys the stability properties stated in Propositions 2.3 and 2.4. As for the inference of the model, we refer readers to Fokianos et al. (2009) for details.

5 Numerical results

The performance of the estimation procedure for the Poisson nonlinear dynamic model is illustrated in a simulation study. The MLE is obtained by optimizing the log-likelihood function (3.1) using a Newton-Raphson method. Simulation results of the Poisson INGARCH can be found in Fokianos et al. (2009). Other models including the negative binomial linear and nonlinear dynamic models and the exponential autoregressive model (4.14) will be applied to two real datasets, and tools for checking goodness of fit will be considered.

5.1 Simulation for the nonlinear model

As specified in (4.13), a 1-knot nonlinear dynamic model is simulated according to

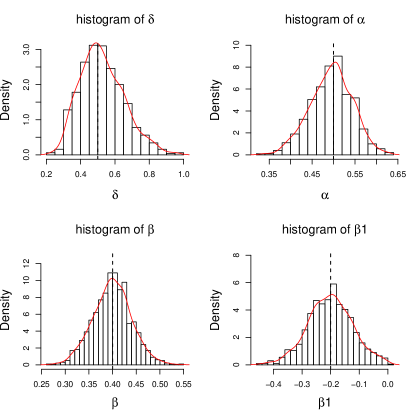

with different sample sizes. Each sample size and parameter configuration is replicated times. For each realization, the first simulated observations are discarded as burn-in in order to let the process reach its stationary regime. We first estimate the parameters assuming that the location of the knot is known, i.e., the true underlying model is (4.11) with only one knot at 5. The means and standard errors of the estimates from all 1000 runs are summarized in Table 1 and the histograms of the estimates are depicted in Figure 1. The performance of these estimates is reasonably good and consistent with the theory described in Theorem 4.2. As for estimating the parameters without knowing the location of the knots, the corresponding results of the MLE obtained by fitting a 1-knot model to all the 1000 replications are summarized in Table 2. Here the locations of the knots are determined by sample quantiles. Not surprisingly, the performance of the maximum likelihood estimates of and is not as good as in the known knot case. However, the overall model performance, as reflected in the computation of the scoring rules (described in the next section), is competitive with the known knot case. For instance when , the means of ranked probability scores (RPS) for known and unknown knot cases are and , respectively.

| True | 0.5 | 0.5 | 0.4 | -0.2 | |

|---|---|---|---|---|---|

| Estimates | 0.5596 | 0.4861 | 0.3990 | -0.2009 | 500 |

| s.e. | (0.0087) | (0.0030) | (0.0026) | (0.0051) | |

| Estimates | 0.5265 | 0.4944 | 0.3991 | -0.2016 | 1000 |

| s.e. | (0.0041) | (0.0016) | (0.0013) | (0.0025) |

| True | 0.5 | 0.5 | 0.4 | -0.2 | |

|---|---|---|---|---|---|

| Estimates | 0.5387 | 0.4852 | 0.4187 | -0.1614 | 500 |

| s.e. | (0.0089) | (0.0030) | (0.0031) | (0.0047) | |

| Estimates | 0.5002 | 0.4943 | 0.4197 | -0.1679 | 1000 |

| s.e. | (0.0042) | (0.0016) | (0.0015) | (0.0023) |

Next we turn to the problem of selecting the number of knots using an information criterion. Simulations with different sample sizes are implemented and the model selection results are summarized in Table 3. Numbers in the table stand for the proportion of times that each particular model is selected in the 1000 runs. For AIC, the 1-knot model is selected most often followed by a 2-knot model, at least in the cases when .

| Criteria | 0 knot | 1 knot | 2 knots | 3 knots | knots | |

|---|---|---|---|---|---|---|

| AIC | 500 | |||||

| BIC | 0 | |||||

| AIC | 1000 | |||||

| BIC | 0 |

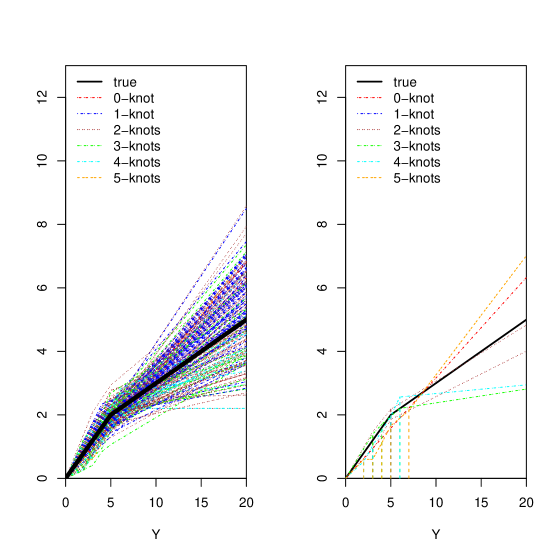

In light of the idea of interpolating the nonlinear dynamic of by a piecewise linear function, we plot in Figure 2 the fitted functions for each run of the simulations against its true form . From the graph, we can see that the piecewise linear function fitted by the 1-knot model is closest to the true curve.

5.2 Two data applications

1. Number of transactions of Ericsson stock

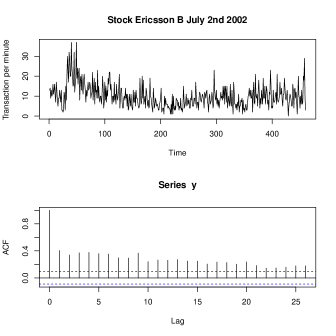

As an illustrative example, both linear and nonlinear dynamic models are employed to fit the number of transactions per minute for the stock Ericsson B during July 2nd, 2002 which consists of 460 observations. Figure 3 plots the data and the autocorrelation function. The positive dependence displayed in the data suggests the application of the models in our study.

By computing the MLE of the parameters, the fitted Poisson INGARCH model is given by

and the fitted NB-INGARCH model is

where . The standard deviations in the parentheses are calculated according to the remark after Theorem 3.

As for the Poisson nonlinear dynamic model, AIC and BIC are used to help select the number of knots among 0 to 5; the values are reported in Table 4.

| 0-knot | 1-knot | 2-knot | 3-knot | 4-knot | 5-knot | |

|---|---|---|---|---|---|---|

| LogL | -1433.19 | -1431.21 | -1431.08 | -1430.58 | -1431.12 | |

| AIC | 2874.38 | 2874.17 | 2875.17 | 2875.30 | 2880.25 | |

| BIC | 2893.07 | 2898.95 | 2904.08 | 2908.35 | 2917.43 |

The fitted 1-knot Poisson model, which has the smallest AIC, is given by

Note that the AIC values of the 2-knot and 3-knot models are both close to that of the 1-knot model, and therefore are used as a basis for comparison with the minimum AIC model. These models are given by and , respectively.

As can be seen from the model checking below, the negative binomial INGARCH model seems to outperform the Poisson-based models. This could be explained by the over-dispersion exhibited by the data, since the mean and variance are 9.91 and 32.84, respectively. To this end, we fit the nonlinear negative binomial models and select the number of knots by minimizing the AIC. It turns out that the AIC value of a 1-knot model is the second smallest among all the candidates, with 2674.69 compared to the smallest value 2674.04, which is attained by the negative binomial INGARCH model fitted above. The fitted 1-knot negative binomial nonlinear model is given by , where follows

Here the locations of knots for the nonlinear dynamic model are all estimated by the corresponding sample quantiles. We also tried estimating the knots by maximizing the likelihood, and in this application, the results by both methods are nearly identical. The exponential autoregressive model (4.14) is also applied to this dataset by Fokianos et al. (2009) and is given by

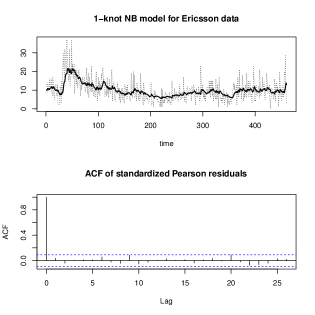

To assess the adequacy of the fit by all of the above models, we will consider an array of graphical and quantitative diagnostic tools for time series, some of which are specifically designed for time series of counts. Readers can refer to Davis et al. (2003) and Jung and Tremayne (2011) for a comprehensive treatment of the tools. In our study, we first consider the standardized Pearson residuals which can be obtained by replacing the population quantities by their estimated counterparts. If the model is correctly specified, then the residuals should be a white noise sequence with constant variance. It turns out that all the models considered above give very similar fitted conditional mean processes and the standardized Pearson residuals appear to be white. Figure 4 displays the fitted result for the 1-knot negative binomial model.

Another tool for model checking is through the probability integral transform (PIT). When the underlying distribution is continuous, it is well known that the PIT follows standard uniform distribution. However, if the underlying distribution is discrete, some adjustments are required and the so-called randomized PIT is therefore introduced by perturbing the step function characteristic of the CDF of discrete random variables (see Brockwell (2007)). More recently, Czado et al. (2009) proposed a non-randomized version of PIT as an alternative adjustment. Since it usually gives the same conclusion for model checking, we do not provide the non-randomized version here. For any , the randomized PIT is defined by

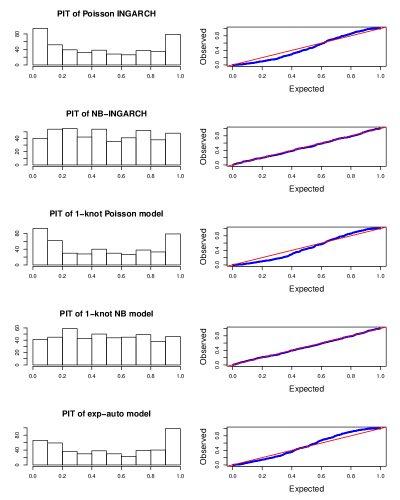

where is a sequence of iid uniform random variables, is the predictive cumulative distribution. In our situation, is simply the CDF of a Poisson or a negative binomial distribution. If the model is correct, then is an iid sequence of uniform random variables. Jung and Tremayne (2011) reviewed several ways to depict this and we adopt their method in our study. To test if the PIT follows uniform distribution, the histograms of PIT from different models are plotted and a Kolmogorov-Smirnov test is carried out. The results are summarized in Figure 5, and the -values are reported in Table 5. It can be seen that both of the two negative binomial-based models pass the PIT test, while none of the Poisson-based models does. This observation could be explained, as mentioned above, by the over-dispersion phenomenon of the data.

To measure the power of predictions by models, various scoring rules have been proposed in literature, see e.g., Czado et al. (2009) and Jung and Tremayne (2011). Most of them are computed as the average of quantities related to predictions and take the form where is the CDF of the prediction distribution and denotes some scoring rule. In this paper we calculate three scoring rules: logarithmic score (LS), quadratic score (QS) and ranked probability score (RPS), as a basis for evaluating the relative performance of our fitted models. For definition of these scores, see Jung and Tremayne (2011). Table 5 summarizes these scores for all of the fitted models. As seen from the table, most of the diagnostic tools favor the one-knot negative binomial model for the Ericsson data.

| Model | log likelihood | -value of PIT | LS | QS | RPS |

|---|---|---|---|---|---|

| Poisson INGARCH | -1433.19 | 3.1167 | -0.0576 | 2.6883 | |

| NB INGARCH | -1332.02 | 0.7386 | 2.8958 | -0.0671 | 2.6063 |

| 1-knot Poisson model | -1431.21 | 3.1123 | -0.0573 | 2.6848 | |

| 2-knot Poisson model | -1431.08 | 3.1121 | -0.0575 | 2.6843 | |

| 3-knot Poisson model | -1430.58 | 3.1110 | -0.0580 | 2.6779 | |

| 1-knot NB model | 0.8494 | ||||

| Exp-auto model | -1448.69 | 3.1504 | 2.6924 |

2. Return times of extreme events of Goldman Sachs Group (GS) stock

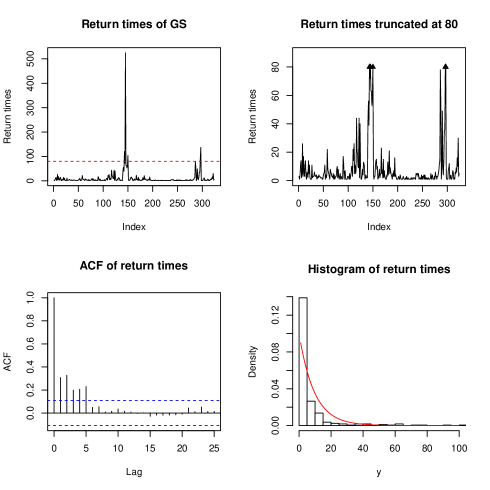

As a second example, we construct a time series based on daily log-returns of Goldman Sachs Group (GS) stock from May 4th, 1999 to March 16th, 2012. We first calculate the hitting times, , for which the log-returns of GS stock falls outside the and quantiles of the data. The discrete time series of interest will be the return (or inter-arrival) times . If the data are in fact iid, or do not exhibit clustering of large values, then the ’s should be independent and geometrically distributed with probability of success (Chang (2010)). Figure 6 plots the return times of the stock, and the ACF and histogram of the return times. Note that in order to ameliorate the visual effect of some extremely large observations, the time series is also plotted in the top right panel of Figure 6 on a reduced vertical scale, in which it is truncated at 80 and the five observations that are affected are depicted by solid triangles.

To explore this time series, three models: the geometric INGARCH (negative binomial INGARCH (4.8) with ), and the 1-knot and 2-knot geometric-based models are fitted to the data. The number of knots for the nonlinear dynamic models is chosen by minimizing the AIC, and the locations of knots are estimated by maximizing the likelihood based on a grid search. In addition, the following constraint is imposed: there should be at least 30 observations in each of the regimes segmented by the knots in order to guarantee that there are sufficient observations to obtain quality estimates of the parameters. The sample quantile method for estimating knot locations did not perform as well.

Since it follows from the definition of return times that for any , we use a version of the geometric distribution that counts the total number of trials, instead of only the failures. In particular, the fitted 1-knot geometric-based model is given by , where

and the fitted 2-knot geometric-based model is

where . Notice that in both models, is very close to unity, i.e., the estimated parameters are close to the boundary of the parameter space. This is similar to the integrated GARCH (IGARCH) model in which . In our application, the mean of the time series of return times is about 10, while the variance is 1101. A simple simulation according to the fitted model yields the mean and median very close to those of the data, but the variance of the simulated data is extraordinarily large, which resembles the feature of the observed data. This is because, although the fitted models are still stationary, the parameters no longer satisfy the conditions specified in Theorem 4.2 that ensure a finite variance.

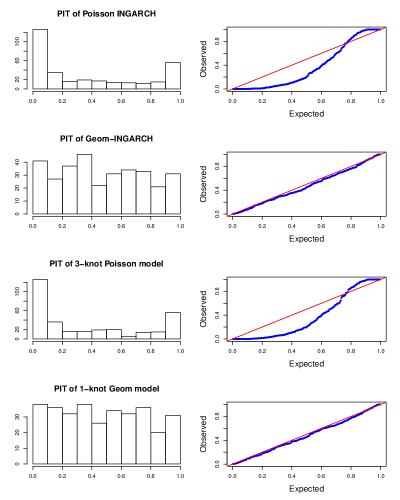

It turns out that the geometric-based models fitted above are capable of capturing the high volatility part of the data. Their standardized Pearson residuals are also calculated and appear to be white. Results of the PIT test are depicted in Figure 7, and the prediction scores and the -values of the PIT test are summarized in Table 6. Two Poisson-based models are also included for comparison, and as expected, they do not perform as well as the geometric-based models.

| Model | log likelihood | -value of PIT | LS | QS | RPS |

|---|---|---|---|---|---|

| Poisson INGARCH | -2681.06 | 8.2842 | -0.0675 | 4.1373 | |

| Geom INGARCH | -857.73 | 0.2581 | 2.6477 | -0.1436 | 3.4100 |

| 3-knot Poisson model | -2670.33 | 8.2510 | -0.0693 | 4.1400 | |

| 1-knot Geom model | -857.58 | 0.3988 | 2.6472 | 3.4041 | |

| 2-knot Geom model | 0.2006 | -0.1435 |

Acknowledgement

This research is supported in part by NSF grant DMS-1107031.

Appendix A. Properties of the exponential family

An important property of the one-parameter exponential family that is heavily used in this paper is the stochastic monotonicity. A random variable is said to be stochastically smaller than a random variable (written as Y) if for all , where and are the cumulative distribution functions of and respectively. We refer readers to Yu (2009) for the related theory.

Proposition 7. Suppose two random variables and follow distributions belonging to the one-parameter exponential family (2.1) with the same and , but with natural parameters and respectively. If , then is stochastically smaller than .

Proof.

Denote the probability density functions of and as and defined in (2.1), respectively. Then the log ratio of the two densities is

which is apparently a concave function in . So it follows from Definition 2 in Yu (2009) that is log concave relative to , i.e., . Moreover, since is increasing in , so for continuous , and for discrete . Hence according to Theorem 1 in Yu (2009), is stochastically smaller than , i.e., . ∎

Denote as the cumulative distribution function of in (2.1) with , and its inverse for . The result below provides a useful tool for the coupling technique employed to establish mixing conditions for the observation process.

Proposition 8. Suppose that is a uniform random variable, and define two random variables and as

where and . Then .

Proof.

It follows from the construction of and that they follow the one-parameter exponential family (2.1) with natural parameters and respectively, and , . If , then is stochastically smaller than by virtue of Proposition Appendix A. Properties of the exponential family. It follows that for , i.e., . This implies . Similarly if , then . Hence we have . ∎

Appendix B. Proofs

B.1. Proof of Proposition 2.3

It suffices to verify the two conditions formulated in Wu and Shao (2004). For any in the state space , . Next for a fixed , there exists a unique such that due to the strict monotonicity of . For any , there exists a unique such that . Hence by the contraction condition (2.3), we have

| (5.1) | |||||

It follows from and Proposition Appendix A. Properties of the exponential family that for any , . Therefore

Similarly for , we have . So for any , we have . Now suppose , then

By induction, is geometric moment contracting and as a result, is its unique stationary distribution.

To show that , notice that by taking conditional expectation on both sides of (2.4), we have . Inductively one can show that for any ,

Since for any , as , in particular, , so by Theorem 3.4 in Billingsley (1999) we have

To prove (c), let be a sequence of independent uniform random variables and independent of , then . Since is a stationary sequence if , so must also be a stationary process.

B.2. Proof of Proposition 2.4

Define a sequence of functions in a way such that , and for , . Then it follows from (2.2) that for all ,

By virtue of the contraction condition (2.3), we have . By induction, it follows that for any ,

Since , it follows that , as . Hence there exists a measurable function such that almost surely, which proves (a).

To prove (b), denote for . Then the coefficients of absolute regularity of the stationary count process are defined as

where according to . Because the distribution of given is the same as that of given for , the coefficients of absolute regularity become

| (5.2) | |||||

Let be the -field in generated by the cylinder sets, then we can rewrite the coefficients of absolute regularity as

| (5.3) |

We will provide an upper bound for (5.3) by coupling two chains and defined on a common probability space. Assume that both chains start from the stationary distribution, that is, , and that is independent of . Let as be an iid sequence of uniform random variables, and construct the chains as follows:

Since and are independent, so for any ,

Hence we have

| (5.4) | |||||

Therefore the coefficients of absolute regularity are bounded by

| (5.5) |

Observe that the construction of the two chains agrees with the definition of geometric moment contraction (Definition 1 in Wu and Shao (2004)), so it follows from Proposition 2.3 that for all . Then

Hence according to (5.5), the coefficients of absolute regularity satisfy . Recall the well-known fact that -mixing implies strong mixing (e.g., Doukhan (1994)), so is stationary and strongly mixing at geometric rate, in fact, it is ergodic. In particular, is an ergodic stationary process. It follows from that is also ergodic.

B.3. Proof of Proposition 2.4

The proof utilizes the classic Markov chain theory, see for example Meyn and Tweedie (2009). (a) follows from the same argument as in the proof of Proposition 2.4. As for (b), for any fixed , define as Lebesgue measure on , where , and let be a set with . To prove the irreducible, we need to show that for any , there exists , such that . If , then , which implies that . Because of the assumptions on the function , and the fact that the distribution of given has positive probability everywhere, so . On the other hand, if , it is easy to see that . If , then by the same argument above, we have . However, if , then . Hence we have . By induction, there exists such that , where for . Since , and the function is increasing in both coordinates, so . Hence is irreducible.

We now show that is aperiodic, i.e., a irreducible Markov chain is said to be aperiodic if there exists a small set with such that for any , and . Note that in the setting of the proposition, any compact set is a small set. So we take for some positive large enough. For any , from the proof of irreducibility, it is easy to see that . Similarly we have .

To check the drift condition, let . There exists , such that . For , we have

Hence the drift condition holds by taking the small set , which establishes the geometric ergodicity of . It is well known that a geometrically ergodic Markov chain starting from its stationary distribution is strongly mixing with geometrically decaying rate, hence is an ergodic stationary time series (e.g., Meyn and Tweedie (2009)). Denote as a sequence of iid uniform random variables, then it follows from that is stationary and ergodic.

B.4. Proof of Theorem 3

We first show the identifiability and then establish the consistency result using Lemma 3. Throughout the proof, we assume that the process is in its stationary regime. Note that by assumption (A1), , which implies . So it follows from assumptions (A2) and (A4) that for any ,

This implies . Denote , then according to the extended mean ergodic theorem (see Billingsley (1995) pp. 284 and 495). In order to prove the identifiability, we need to show that is the unique maximizer of , that is, for any , . First it follows from assumption (A5) that for any and all , , where . Let , then we have

On the set , there exists between and such that by the mean value theorem. It follows from that is strictly convex and must be strictly between and . So there exists lying strictly between and such that . Therefore

Since is strictly increasing, so in either of the two cases: and . Hence , for any , which establishes the identifiability. To show the consistency, first note that by assumption (A4), we have

The function in Lemma 3 can be defined as

where . Hence it follows from assumption (A2) and Lemma 3 that is upper-semicontinuous and for any compact subset , . Take as a local base of and let be a neighborhood of , then Lemma 3 can be applied to . Because u.s.c function attains its maximum on compact sets and for any , we have

| (5.6) |

Notice that for any , . Let such that (5.6) holds and . For such , suppose infinitely often, say, along a sequence denoted by , then

| (5.7) | |||||

However, according to (5.6), we have

which contradicts (5.7). Hence there exists a null-set such that for all , for all large enough. It follows by taking any set that converges to almost surely.

B.5. Proof of Theorem 3

We define a linearized form of as , and the corresponding linearized log-likelihood function of as

Let , then define

| (5.8) | |||||

Let , then , so is a martingale difference sequence. Note that

which converges almost surely to by the mean ergodic theorem and assumption (A7). Moreover, for any ,

Then it follows from the central limit theorem for martingale difference sequences that

where is evaluated at . The other term in (5.8) by Taylor expansion is

which is of the order of . Hence , where . It then follows that .

For the rest of the proof, we show that the difference between and is negligible as grows large. By writing , the difference becomes

| (5.9) | |||||

By Taylor expansion, the first term in (5.9) is , where lies between and , and . Since

and under the smoothness assumption, so the first term in (5.9) converges to 0 uniformly on for any . We now apply Taylor expansion to each component in the second term of (5.9),

where , and both lie between and . Therefore the second term in (5.9) becomes

which converges to 0 on a compact set of under smoothness assumptions. So (5.9) converges to 0 as , which implies that and have the same asymptotic distribution, i.e.,

Note that , where is the conditional maximum likelihood estimator. Hence

B.6. Proof of Theorem 4.1

According to Theorems 3 and 3, it is sufficient to establish the identifiability of the model, that is, we need to verify assumption (A5). Suppose for some , , -a.s, then . It follows from (4.3) that

If , then which contradicts the fact that . So must be the same as . Similarly one can show that and , which implies . Hence the model is identifiable.

B.7. Proof of Remark 4.1

The most difficult case is the derivative with respect to and we only give its proof, since the arguments for and are similar. First note that

where . Then on account of stationarity, one can show that

where . Hence if .

B.8. Proof of Proposition 4.1

The proof considers two separate cases: and , since they require different methods to construct the state space.

-

1.

: without loss of generality we consider . Denote , then is a Markov chain. Note that . can be constructed by iteratively imposing the random function , ,

For any in the state space , define metric as , where and are to be decided. Let , then for any we have

where the last equation holds because . Therefore it is sufficient to find an and strictly positive such that

This can be obtained if the equation yields a root . It can be shown that under the root . Note that the choice of is not unique.

-

2.

: without loss of generality we consider the INGARCH(2,2) model. Define a Markov chain , then the chain can be obtained by defining the iterated random functions as , where and . Note that we cannot define in the same way as in the first case, since otherwise it contradicts the independence assumption of sequence. Define the metric on as , where and . Take , then for any , we have

Similarly to the first case, one needs to solve the inequality

for an and a strictly positive triple . This can be achieved if , which implies the quadratic equation has a root . The result hence follows by a simple induction.

B.9. Proof of Theorem 4.2

References

- Billingsley (1995) Billingsley, P. (1995) Probability and Measure (3rd edition). New York: Wiley.

- Billingsley (1999) Billingsley, P. (1999) Convergence of probability measures. (2nd edition). New York: Wiley.

- Brockwell (2007) Brockwell, A. E. (2007) Universal residuals: A multivariate transformation. Statistics and Probability Letters, 77(14), 1473–1478.

- Brockwell and Davis (1991) Brockwell, P. and Davis, R. (1991) Time Series: Theory and Methods, 2nd Edition. Springer.

- Chang (2010) Chang, L. (2010) Conditional Modeling and Conditional Inference. Ph.D. thesis, Brown University.

- Cox (1981) Cox, D. R. (1981) Statistical analysis of time series: Some recent developments. Scandinavian Journal of Statistics, 8, 93–115.

- Czado et al. (2009) Czado, C., Gneiting, T. and Held, L. (2009) Predictive model assessment for count data. Biometrics, 65, 1254–1261.

- Davis et al. (2003) Davis, R., Dunsmuir, W. and Streett, S. (2003) Observation-driven models for Poisson counts. Biometrika, 90, 777–790.

- Diaconis and Freedman (1999) Diaconis, P. and Freedman, D. (1999) Iterated random functions. SIAM Review, 41, 45–76.

- Doukhan (1994) Doukhan, P. (1994) Mixing: Properties and Examples. Lecture notes in Statistics 85. Springer-Verlag.

- Doukhan et al. (2012) Doukhan, P., Fokianosb, K. and Tj stheim, D. (2012) On weak dependence conditions for Poisson autoregressions. Statistics and Probability Letters, 82(5), 942–948.

- Ferland et al. (2006) Ferland, R., Latour, A. and Oraichi, D. (2006) Integer-valued GARCH process. Journal of Time Series Analysis, 27(6), 923–942.

- Fokianos et al. (2009) Fokianos, K., Rahbek, A. and Tjøstheim, D. (2009) Poisson autoregression. Journal of the American Statistical Association, 104(488), 1430–1439.

- Jung and Tremayne (2011) Jung, R. and Tremayne, A. (2011) Useful models for time series of counts or simply wrong ones? AStA Advances in Statistical Analysis, 95, 59–91.

- Lehmann and Casella (1998) Lehmann, E. and Casella, G. (1998) Theory of Point Estimation (2nd edition). Springer-Verlag.

- Meyn and Tweedie (2009) Meyn, S. and Tweedie, R. (2009) Markov Chains and Stochastic Stability (2nd edition). Cambridge University Press.

- Neumann (2011) Neumann, M. (2011) Absolute regularity and ergodicity of Poisson count processes. Bernoulli, 17, 1268–1284.

- Pfanzagl (1969) Pfanzagl, J. (1969) On the measurability and consistency of minimum contrast estimates. Metrica, 14, 249–272.

- Ruppert et al. (2003) Ruppert, D., Wand, M. and Carroll, R. (2003) Semiparametric regression (Cambridge Series in Statistical and Probabilistic Mathematics). Cambridge University Press.

- Samia and Chan (2010) Samia, N. and Chan, K. (2010) Maximum likelihood estimation of a generalized threshold stochastic regressio model. Biometrika, 98 (2), 433–448.

- Streett (2000) Streett, S. (2000) Some observation driven models for time series of counts. Ph.D. thesis, Colorado State University, Department of Statistics.

- Tong (1990) Tong, H. (1990) Non-Linear Time Series. A Dynamical System Approach. New York: Oxford University Press.

- Wu and Shao (2004) Wu, W. and Shao, X. (2004) Limit theorems for iterated random functions. Journal of Applied Probability, 41, 425–436.

- Yu (2009) Yu, Y. (2009) Stochastic ordering of exponential family distributions and their mixtures. Journal of Applied Probability, 46, 244–254.