∎

22email: iankash@microsoft.com 33institutetext: E. J. Friedman 44institutetext: Internation Computer Science Institute and Department of Computer Science, University of California, Soda Hall, Berkeley, CA 94720

44email: ejf@icsi.berkeley.edu 55institutetext: J. Y. Halpern 66institutetext: Computer Science Department, Cornell University, Upson Hall, Ithaca, NY 14850

66email: halpern@cs.cornell.edu

Optimizing Scrip Systems: Crashes, Altruists, Hoarders, Sybils and Collusion††thanks: Portion of the material in this paper appeared in preliminary form in papers in the Proceedings of the 7th and 8th ACM Conferences on Electronic Commerce Friedman et al (2006); Kash et al (2007) and the Proceedings of the First Conference on Auctions, Market Mechanisms and Their Applications Kash et al (2009). Section 2 and Appendix A are reproduced from a companion paper Kash et al (2012) to make this paper self-contained. Much of the work was performed while Ian Kash and Eric Friedman were at Cornell University.

Abstract

Scrip, or artificial currency, is a useful tool for designing systems that are robust to selfish behavior by users. However, it also introduces problems for a system designer, such as how the amount of money in the system should be set. In this paper, the effect of varying the total amount of money in a scrip system on efficiency (i.e., social welfare—the total utility of all the agents in the system) is analyzed, and it is shown that by maintaining the appropriate ratio between the total amount of money and the number of agents, efficiency is maximized. This ratio can be found by increasing the money supply to just below the point that the system would experience a “monetary crash,” where money is sufficiently devalued that no agent is willing to perform a service. The implications of the presence of altruists, hoarders, sybils, and collusion on the performance of the system are examined. Approaches are discussed to identify the strategies and types of agents.

Keywords:

Game Theory P2P Networks Scrip Systems Artificial Currency1 Introduction

Money is a powerful tool for dealing with selfish behavior. For example, in peer-to-peer systems, a common problem is free riding Adar and Huberman (2000), where users take advantage of the resources offered by a system without contributing their own. One way of dealing with the problem is to have users pay for the use of others’ resources, and to pay them for contributing their own resources. The incentive to free ride then disappears. Similarly, monetary incentives are a potential solution to resource allocation problems in distributed and peer-to-peer systems: this is the business model of cloud computing services such as Amazon EC2.

In some systems, it may not be desirable to use actual money. As a result, many systems have used an artificial currency, or scrip. (See Gupta et al (2003); Ioannidis et al (2002); Miller and Drexler (1988); Reeves et al (2007); Stonebraker et al (1996); Vishnumurthy et al (2003); Brunelle et al (2006); Peterson and Sirer (2009); Aperjis et al (2008) for some examples of the use of scrip in systems.) While using scrip avoids some issues, such as processing payments, it introduces new questions a system designer must face. How much money should be printed? What should happen if the system grows rapidly or there is significant churn? What will happen if a small number of users start hoarding money or creating sybils?

The story of the Capitol Hill Baby Sitting Co-op Sweeney and Sweeney (1977), popularized by Krugman 1999, provides a cautionary tale of how system performance can suffer if these issues are not handled appropriately. The Capitol Hill Baby Sitting Co-op was a group of parents working on Capitol Hill who agreed to cooperate to provide babysitting services to each other. In order to enforce fairness, they issued a supply of scrip with each coupon worth a half hour of babysitting. At one point, the co-op had a recession. Many people wanted to save up coupons for when they wanted to spend an evening out. As a result, they went out less and looked for more opportunities to babysit. Since a couple could earn coupons only when another couple went out, no one could accumulate more, and the problem only got worse.

After a number of failed attempts to solve the problem, such as mandating a certain frequency of going out, the co-op started issuing more coupons. The results were striking. Since couples had a sufficient reserve of coupons, they were more comfortable spending them. This in turn made it much easier to earn coupons when a couple’s supply got low. Unfortunately, the amount of scrip grew to the point that most of the couples felt “rich.” They had enough scrip for the foreseeable future, so naturally they didn’t want to devote their evening to babysitting. As a result, couples who wanted to go out were unable to find another couple willing to babysit.

This anecdote shows that the amount of scrip in circulation can have a significant impact on the effectiveness of a scrip system. If there is too little money in the system, few agents will be able to afford service. At the other extreme, if there is too much money in the system, people feel rich and stop looking for work. Both of these extremes lead to inefficient outcomes. This suggests that there is an optimal amount of money, and that nontrivial deviations from the optimum towards either extreme can lead to significant degradation in the performance of the system.

In a companion paper Kash et al (2012), we gave a formal model of a scrip system and studied the behavior of scrip systems from a micro-economic, game-theoretic viewpoint. Roughly speaking, in the model agents want work done at random times. To get the work done, they must have at least $1 of scrip.111Although we refer to our unit of scrip as the dollar, these are not real dollars, nor do we view “scrip dollars” as convertible to real dollars. All the agents willing to do the work volunteer to do it, and one is chosen at random (although not necessarily uniformly at random; agents may have different likelihoods of being chosen). The agent who has the work done pays $1 to the agent chosen to do it, and gains 1 unit of utility, while the agent who does the work suffers a small utility loss. We showed that in such a scrip system, there is a nontrivial Nash equilibrium where all agents use a threshold strategy—that is, agent volunteers to work iff has below some threshold of dollars (the threshold may be different for different agents). A key part of our analysis involves a characterization of the distribution of wealth when agents all use threshold strategies.

In this paper, we use the analysis of scrip systems from Kash et al (2012) to understand how robust scrip systems are, and how to optimize their performance. We compute the money supply that maximizes social welfare, given the number of agents. As we show, the behavior mimics the behavior in the babysitting coop example. Specifically, if we start with a system with relatively little money (where “relatively little” is measured in terms of the average amount of money per agent), adding more money decreases the number of agents with no money, and thus increasing social welfare. (Since it is more likely that an agent will be able to pay for someone to work when he wants a job done.) However, this only works up to a point. Once a critical amount of money is reached, the system experiences a monetary crash: just as in the babysitting coop example, there is so much money that, in equilibrium, everyone will feel rich and no agents are willing to work. We show that, to get optimal performance, we want the total amount of money in the system to be as close as possible to the critical amount, but not to go over it. If the amount of money in the system is over the critical amount, we get the worst possible equilibrium, where no agent ever volunteers, and all agents have utility 0. This means that, for a system designers’ point of view, there is a significant tradeoff between efficiency and robustness.

The equilibrium analysis in Kash et al (2012) assumes that all agents have somewhat similar motivation: in particular, they do not get pleasure simply from performing a service, and are interested in money only to the extent that they can use it to get services performed. But in real systems, not all agents have this motivation. Some of the more common “nonstandard” agents are altruists and hoarders. Altruists are willing to satisfy all requests, even if they go unpaid (think of babysitters who love kids so much that they get pleasure from babysitting, and are willing to babysit for free); hoarders value scrip for its own sake and are willing to accumulate amounts far beyond what is actually useful. Studies of the Gnutella peer-to-peer file-sharing network have shown that one percent of agents satisfy fifty percent of the requests Adar and Huberman (2000); Hughes et al (2005). These agents are doing significantly more work for others than they will ever have done for them, so can be viewed as altruists. Anecdotal evidence also suggests that the introduction of any sort of currency seems to inspire hoarding behavior on the part of some agents, regardless of the benefit of possessing money. For example, SETI@home has found that contributors put in significant effort to make it to the top of their contributor rankings. This has included returning fake results of computations rather than performing them Zhao et al (2005).

Altruists and hoarders have opposite effects on a system: having altruists has the same effect as adding money; having hoarders is essentially equivalent to removing it. With enough altruists in the system, the system has a monetary crash, in the sense that standard agents stop being willing to provide service, just as when there is too much money in the system (the system still functions on a limited basis after the monetary crash because altruists still supply service). We show that, until we get to the point where the system crashes, the utility of standard agents is improved by the presence of altruists. We show that the presence of altruists makes the critical point lower than it would without them. Thus, a system designer trying to optimize the performance of the system by making the money supply as close as possible to the critical point (but under it, since being over it would result in a “crash”) needs to be careful about estimating the number of altruists.

Similarly, we show that, as the fraction of hoarders increases, standard agents begin to suffer because there is effectively less money in circulation. On the other hand, hoarders can improve the stability of a system. Since hoarders are willing to accept an infinite amount of money, they can prevent the monetary crash that would otherwise occur as money was added. In any case, our results show how the presence of both altruists and hoarders can be mitigated by appropriately controlling the money supply.

Beyond nonstandard agents, we also consider two different manipulative behaviors in which standard agents may engage: creating multiple identities, known as sybils Douceur (2002), and collusion. In scrip systems where each new user is given an initial amount of scrip, there is an obvious benefit to creating sybils. Even if this incentive is removed, sybils are still useful: they can be used to increase the likelihood that an agent will be asked to provide service, which makes it easier for him to earn money. This increases the utility of the sybilling agent, at the expense of other agents, in a manner reminiscent of the large view attack on BitTorrent Sirivianos et al (2007). From the perspective of an agent considering creating sybils, the first few sybils can provide him with a significant benefit, but the benefits of additional sybils rapidly diminish. So if a designer can make sybilling moderately costly, the number of sybils actually created by rational agents will usually be relatively small.

If a small fraction of agents have sybils, the situation is more subtle. Agents with sybils still do better than those without, but the situation is not zero-sum. In particular, even agents without sybils might be better off, due to having more opportunities to earn money. Somewhat surprisingly, sybils can actually result in everyone being better off. However, exploiting this fact is generally not desirable. The same process that leads to an improvement in social welfare can also lead to a monetary crash, where all agents stop providing service. The system designer can achieve the same effects by increasing the average amount of money or biasing the volunteer selection process. In practice, it seems better to do this than to exploit the possibility of sybils.

In our setting, having sybils is helpful because it increases the likelihood that an agent will be asked to provide service. Our analysis of sybils applies no matter how this increase in likelihood occurs. In particular, it applies to advertising. Thus, our results suggest that there are tradeoffs involved in allowing advertising. For example, many systems allow agents to announce their connection speed and other similar factors. If this biases requests towards agents with high connection speeds, even when agents with lower connection speeds are perfectly capable of satisfying a particular request, then agents with low connection speeds will have an unnecessarily worsened experience in the system. This also means that such agents will have a strong incentive to lie about their connection speed.

While collusion is considered a bad thing in most systems, in the context of scrip systems with fixed prices, it is almost entirely positive. Without collusion, if a user runs out of money he is unable to request service until he is able to earn some. However, a colluding group can pool there money so that all members can make a request whenever the group as a whole has some money. This increases welfare for the agents who collude because agents who have no money receive no service. Collusion tends to benefit the non-colluding agents as well. Since colluding agents work less often, it is easier for everyone to earn money, which ends up making everyone better off. However, as with sybils, collusion does have the potential of crashing the system if the average amount of money is too close to the critical point.

While a designer should generally encourage collusion in scrip systems, we would expect that in most systems there will be relatively little collusion, and what collusion exists will involve small numbers of agents. After all, scrip systems exist to try and resolve resource-allocation problems. If agents could collude to optimally allocate resources within the group, they would not need a scrip system in the first place. Nevertheless, our analysis of collusion indicates a way that system performance could be improved even without collusion. Many of the benefits of collusion come from agents effectively being allowed to have a negative amount of money (by borrowing from their the other agents with whom they are colluding). These benefits could also be realized if agents are allowed to borrow money, so designing a loan mechanism could be an important improvement for a scrip system. Of course, implementing such a loan mechanism in a way that prevents abuse requires a careful design.

The analysis we carry out here has a benefit beyond showing how to deal with altruists, hoarders, sybils, and collusion. In order to utilize our results effectively, a system designer needs to be able to identify characteristics of agents (with what frequency do they make requests, how likely are they to be chosen to satisfy a request, and so on) and what strategies they are following. This is particularly useful because finding an amount of money close to the point of monetary crash, but not past it, relies on an understanding of the agents in the system. Of course, such information is also of great interest to social scientists and marketers. We show how relatively simple observations of the system can be used to infer this information.

The rest of the paper is organized as follows. In Section 2, we repeat the formal model from Kash et al (2012). Then in Section 3, we summarize the results from that paper. We begin applying these results in Section 4, where we show that the analysis leads to an understanding of how to choose the amount of money in the system (or, equivalently, the cost to fulfill a request) so as to maximize efficiency, and also shows how to handle new users. In Section 5, we discuss how the model can be used to understand the effects of altruists, hoarders, sybils, and collusion and provide guidance about how system designers can handle these user behaviors. All of this guidance relies on being able to understand what strategies agents are using and what their preferences are. In Section 6, we discuss how these can be inferred by examining the system. We conclude in Section 7.

2 The Model

For the convenience of the reader we repeat Section 3 of our companion paper which describes the model Kash et al (2012).

Before specifying our model formally, we give an intuitive description of what our model captures. While our model simplifies a number of features (as does any model), we believe that it provides useful insights. We model a scrip system where, as in a P2P filesharing system, agents provide each other with service. There is a single service (such as file uploading) that agents occasionally want. In practice, at any given time, a number of agents will want service but, to simplify the formal description and analysis, we model the scrip system as proceeding in a series of rounds where, in each round, a single agent wants service (the time between rounds will be adjusted to capture the growth in parallelism as the number of agents grows).222For large numbers of agents, our model converges to one in which agents make requests in real time, and the time between an agent’s requests is exponentially distributed. In addition, the time between requests served by a single player is also exponentially distributed. In each round, after an agent requests service, other agents have to decide whether they want to volunteer to provide service. However, not all agents may be able to satisfy the request (not everyone has every file). While, in practice, the ability of agents to provide service at various times may be correlated for a number of reasons (if I don’t have the file today I probably still don’t have it tomorrow; if one agent does not have a file, it may be because it is rare, so that should increase the probability that other agents do not have it), for simplicity, we assume that the events of an agent being able to provide service in different rounds or two agents being able to provide service in the same or different rounds are independent. While our analysis relies on this assumption so that we can describe the system using a Markov chain, we expect that our results would still hold as long these correlations are sufficiently small. If there is at least one volunteer, someone is chosen from among the volunteers (at random) to satisfy the request. Our model allows some agents to be more likely to be chosen (perhaps they have more bandwidth) but does not allow an agent to specify which agent is chosen. Allowing agents this type of control would break the symmetries we use to characterize the long run behavior of the system and create new opportunities for strategic behavior by agents that are beyond the scope of this paper. The requester then gains some utility (he got the file) and the volunteer loses some utility (he had to use his bandwidth to upload the file), and the requester pays the volunteer a fee that we fix at one dollar. As is standard in the literature, we assume that agents discount future payoffs. This captures the intuition that a util now is worth more than a util tomorrow, and allows us to compute the total utility derived by an agent in an infinite game. The amount of utility gained by having a service performed and the amount lost be performing it, as well as many other parameters may depend on the agent.

More formally, we assume that agents have a type drawn from some finite set of types. We can describe the entire population of agents using the pair , where is a vector of length and is the fraction with type . For most of the paper, we consider only what we call standard agents. These are agents who derive no pleasure from performing a service, and for whom money has no intrinsic value. Thus, for a standard agent, there is no direct connection between money (measured in dollars) and utility (measured in utils). We can characterize the type of a standard agent by a tuple , where

-

•

reflects the cost for an agent of type to satisfy a request;

-

•

is the probability that an agent of type can satisfy a request;

-

•

is the utility that an agent of type gains for having a request satisfied;

-

•

is the rate at which an agent of type discounts utility;

-

•

represents the (relative) request rate (some people want files more often than others). For example, if there are two types of agents with and then agents of the first type will make requests twice as often as agents of the second type. Since these request rates are relative, we can multiply them all by a constant to normalize them. To simplify later notation, we assume the are normalized so that ; and

-

•

represents the (relative) likelihood of an agent to be chosen when he volunteers (some uploaders may be more popular than others). In particular, this means the relative probability of two given agents being chosen is independent of which other agents volunteer.

-

•

is not part of the tuple, but is an important derived parameter that helps determine how much money an agent will have.

We occasionally omit the subscript on some of these parameters when it is clear from context or irrelevant.

Representing the population of agents in a system as captures the essential features of a scrip system we want to model: there are a large number of agents who may have different types. Note that fixing a particular tuple puts a constraint on the number of agents. For example, if there are two types, and says that half of the agents are of each type, then there cannot be 101 agents. Similar issues arise when we want to talk about the amount of money in a system. We could deal with this problem in a number of ways (for example, by having each agent determine his type at random according to the distribution ). For convenience, we simply do not consider population sizes that are incompatible with . This is the approach used in the literature on -replica economies Mas-Colell et al (1995).

Formally, we consider games specified by a tuple , where and are as defined above, is the base number of agents of each type, is number of replicas of these agents and is the average amount of money. The total number of agents is thus . We ensure that the fraction of agents of type is exactly and that the average amount of money is exactly by requiring that and . Having created a base population satisfying these constraints, we can make an arbitrary number of copies of it. More precisely, we assume that agents have type , agents have type , and so on through agent . These base agents determine the types of all other agents. Each agent has the same type as ; that is, all the agents of the form for are replicas of agent .

We also need to specify how money is initially allocated to agents. Our results are based on the long-run behavior of the system and so they turn out to hold for any initial allocation of money. For simplicity, at the start of the game we allocate each of the dollars in the system to an agent chosen uniformly at random, but all our results would hold if we chose any other initial distribution of money.

To make precise our earlier informal description, we describe as an infinite extensive-form game. A non-root node in the game tree is associated with a round number (how many requests have been made so far), a phase number, either 1, 2, 3 , or 4 (which describes how far along we are in determining the results of the current request), a vector where is the current amount of money agent has, and , and, for some nodes, some additional information whose role will be made clear below. We use to denote the type of agent .

-

•

The game starts at a special root node, denoted , where nature moves. Intuitively, at , nature allocates money uniformly at random, so it transitions to a node of the form : round zero, phase one, and allocation of money , and each possible transition is equally likely.

-

•

At a node of the form , nature selects an agent to make a request in the current round. Agent is chosen with probability . (Note that this is a probability because .) If is chosen, a transition is made to .

-

•

At a node of the form , nature selects the set of agents (not including ) able to satisfy the request. Each agent is included in with probability . If is chosen, a transition is made to .

-

•

At a node of the form , each agent in chooses whether to volunteer. If is the set of agents who choose to volunteer, a transition is made to .

-

•

At a node of the form , if , nature chooses a single agent in to satisfy the request. Each agent is chosen with probability . If is chosen, a transition is made to , where

If or , nature has no choice; a transition is made to with probability 1.

A strategy for agent describes whether or not he will volunteer at every node of the form such that . (These are the only nodes where can move.) We also need to specify what agents know when they make their decisions. To make our results as strong as possible, we allow an agent to base his strategy on the entire history of the game, which includes, for example, the current wealth of every other agent. As we show, even with this unrealistic amount of information, available, it would still be approximately optimal to adopt a simple strategy that requires little information—specifically, agents need to know only their current wealth. That means that our results would continue to hold as long as agents knew at least this information. A strategy profile consists of one strategy per agent. A strategy profile determines a probability distribution over paths in the game tree. Each path determines the value of the following random two variables:

-

•

, the amount of money agent has during round , defined as the value of at the nodes with round number and

-

•

, the utility of agent for round . If is a standard agent, then

, the total expected utility of agent if strategy profile is played, is the discounted sum of his per round utilities , but the exact form of the discounting requires some explanation. In our model, only one agent makes a request each round. As the number of agents increases, an agent has to wait a larger number of rounds to make requests, so naively discounting utility would mean his utility decreases as the number of agents increases, even if all of his requests are satisfied. This is an artifact our model breaking time into discrete rounds where a single agent makes a request. In reality, many agents make requests in parallel, and how often an agent desires service typically does not depend on the number of agents. It would be counterintuitive to have a model that says that if agents make requests at a fixed rate and they are all satisfied, then their expected utility depends on the number of other agents. As the following lemma shows, there is a unique discount rate that removes this dependency.333In preliminary versions of this work we used the discount rate of . This rate captures the intuitive idea of making the time between rounds , but results in an agent’s utility depending on the number of other agents, even if all the agent’s requests are satisfied. However, in the limit as goes to 1, agents’ normalized expected utilities (multiplied by as in Equation 1) are the same either discount rate, so our main results hold with the discount rate as well.

Lemma 1

With a discount rate of , an agent of type ’s expected discounted utility for having all his requests satisfied is independent of the number of replicas . Furthermore, this is the unique such rate such that the discount rate is when .

Proof

The agent makes a request each round with probability , so his expected discounted utility for having all his requests satisfied is

This is independent of and satisfies as desired. The choice of discount rate for the case is unique by the requirement that it be . For , the choice is unique because otherwise the agent’s expected discounted utility would not be and thus would not be independent of .

As is standard in economics, for example in the folk theorem for repeated games Fudenberg and Tirole (1991), we multiply an agent’s utility by so that his expected utility is independent of his discount rate as well. With these considerations in mind, the total expected utility of agent given the vector of strategies is

| (1) |

In modeling the game this way, we have implicitly made a number of assumptions. For example, we have assumed that all of agent ’s requests that are satisfied give agent the same utility, and that prices are fixed. We discuss the implications of these assumptions in our companion paper Kash et al (2012).

Our solution concept is the standard notion of an approximate Nash equilibrium. As usual, given a strategy profile and agent , we use to denote the strategy profile that is identical to except that agent uses .

Definition 1

A strategy for agent is an -best reply to a strategy profile for the agents other than in the game if, for all strategies ,

Definition 2

A strategy profile for the game

is an -Nash equilibrium if for all agents ,

is an -best reply to .

A Nash equilibrium is an epsilon-Nash equilibrium with .

As we show in our companion paper Kash et al (2012), has equilibria where agents use a particularly simple type of strategy, called a threshold strategy. Intuitively, an agent with “too little” money will want to work, to minimize the likelihood of running out due to making a long sequence of requests before being able to earn more money. On the other hand, a rational agent with plenty of money will think it is better to delay working, thanks to discounting. These intuitions suggest that the agent should volunteer if and only if he has less than a certain amount of money. Let be the strategy where an agent volunteers if and only if the requester has at least 1 dollar and the agent has less than dollars. Note that is the strategy where the agent never volunteers. While everyone playing is a Nash equilibrium (nobody can do better by volunteering if no one else is willing to), it is an uninteresting one.

We frequently consider the situation where each agent of type uses the same threshold . In this case, a single vector suffices to indicate the threshold of each type, and we can associate with this vector the strategy where (i.e., agent of type uses threshold ).

For the rest of this paper, we focus on threshold strategies (and show why it is reasonable to do so). In particular, we show that, if all other agents use threshold strategies, it is approximately optimal for an agent to use one as well. Furthermore there exist Nash equilibria where agents do so. While there are potentially other equilibria that use different strategies, if a system designer has agents use threshold strategies by default, no agent will have an incentive to change. Since threshold strategies have such low information requirements, they are a particularly attractive choice for a system designer as well for the agents, since they are so easy to play.

When we consider the threshold strategy , for ease of exposition, we assume in our analysis that . To understand why, note that is the total amount of money in the system. If , then if the agents use a threshold , the system will quickly reach a state where each agent has dollars, so no agent will volunteer. This is equivalent to all agents using a threshold of 0, and similarly uninteresting.

3 Summary of Previous Results

In this section, we summarize the results and definitions from our companion paper Kash et al (2012) that we use in this paper. We also provide intuition for the results, some of which is taken from that paper. The first theorem shows that there exists a particular distribution of wealth such that, after a sufficient amount of time, the distribution of wealth in the system will almost always be close to that particular distribution. In order to formalize this statement, we need a number of definitions.

Let

be the set of allocations of money to agents such that the average amount of money is and no agent has more than dollars. The evolution of can be described by a Markov chain over the state space . For brevity, we refer to the Markov chain and state space as and , respectively, when the subscripts are clear from context. Let denote the set of probability distributions on such that for all types , and . We can think of as the fraction of agents that are of type and have dollars. We can associate each state with its corresponding distribution . Occasionally, we will make use of distributions on such that for all types , , without requiring that ; we denote this set of distributions . Given two distributions , let

denote the relative entropy of relative to ( if and or vice versa); this is also known as the Kullback-Leibler divergence of from Cover and Thomas (1991). For in , we make use of , the distribution in that minimizes relative entropy relative to . If happens to be in and not just this is trivially , but it is well defined in general. Given and , let (or , for brevity) denote the set of states such that . Let be the random variable that is 1 if , and 0 otherwise.

Theorem 3.1

For all games , all vectors of thresholds, and all , there exist and such that, for all , there exists a round such that, for all , we have .

Theorem 3.1 tells us that, after enough time, the distribution of money is almost always close to some , where can be characterized as a distribution that minimizes relative entropy subject to some constraints. For many of our results, a more explicit characterization will be helpful. Let . Then the value of is given by the following lemma.

Lemma 2

| (2) |

where is the unique value such that

| (3) |

We now turn from an analysis of the distribution of wealth to an analysis of best replies and equilibria. To see that threshold strategies are approximately optimal, consider a single agent of type and fix the vector of thresholds used by the other agents. If we assume that the number of agents is large, what an agent does has essentially no affect on the behavior of the system (although it will, of course, affect that agent’s payoffs). In particular, this means that the distribution of Theorem 3.1 characterizes the distribution of money in the system. This distribution, together with the vector of thresholds, determines what fraction of agents volunteers at each step. This, in turn, means that from the perspective of agent , the problem of finding an optimal response to the strategies of the other agents reduces to finding an optimal policy in a Markov decision process (MDP) . The behavior of the MDP depends on two probabilities: and . Informally, is the probability of earning a dollar during each round it is willing to volunteer, and is the probability that will be chosen to make a request during each round. Note that and depend on aspects of , , and ; if the dependence is important, we add the relevant parameters to the superscript, writing, for example, . This MDP is described formally in Appendix A.

For many of our later results and discussion, it will be important to understand how , , and affect the optimal policy for , and thus the -optimal strategies in the game. We use this understanding to show that adding money increases social welfare in Section 4, to understand how agent behaviors affect social welfare in Section 5, and to identify agent types from their behavior in Section 6. The effects of these parameters are captured by the following lemma.

Lemma 3

Consider the games (where , , , and are fixed, but may vary), and fix the vector of thresholds of the other agents. There exists a such that for all , is an optimal policy for . The threshold is the maximum value of such that

| (4) |

where is a random variable whose value is the first round in which an agent starting with dollars, using strategy , and with probabilities and of earning a dollar and of being chosen given that he volunteers, respectively, runs out of money.

While threshold strategies are optimal for the MDP, given a fixed and , the probabilities and represent the typical long-run probabilities, not the exact values in each round of the game. Nevertheless, as the following theorem shows, threshold strategies are near optimal in the actual game, not just in the MDP.

Theorem 3.2

For all games , all vectors of thresholds, and all , there exist and such that for all , types , and , an optimal threshold policy for is an -best reply to the strategy profile for every agent of type .

Given a game and a vector of thresholds, Lemma 3 gives an optimal threshold for each type . Theorem 3.2 guarantees that is an -best reply to , but does not rule out the possibility of other best replies. However, for ease of exposition, we will call the best reply to and call the best-reply function. The following lemma shows that this function is monotone (non-decreasing). Along the way, several other quantities are shown to be monotone.

Lemma 4

Consider the family of games

and the

strategies , for .

For this family of game,

is non-decreasing in and non-increasing in

; is non-decreasing in

and non-increasing in ; and the function

is non-decreasing in and non-increasing in

.

Our final theorem show that there exists a non-trivial equilibrium where all agents play threshold strategies greater than zero. In the theorem, we refer to the “greatest” vector. By this we mean that there exists a vector that is an equilibrium and, in a component-wise comparison, is greater than all other such equilibrium strategy vectors. We refer to this particular equilibrium as the greatest equilibrium.

Theorem 3.3

For all games and all , there exist and such that, if and for all , then there exists a nontrivial vector of thresholds that is an -Nash equilibrium. Moreover, there exists a greatest such vector.

The proof of Theorem 3.3 also provides an algorithm for finding equilibria that seems efficient in practice: start with the strategy profile and iterate the best-reply dynamics until an equilibrium is reached.

While multiple nontrivial equilibria may exist, in the rest of this paper, we focus on the greatest equilibrium in all our applications (although a number of our results hold for all nontrivial equilibria). This equilibrium has several desirable properties, discussed in Section 5 of our companion paper Kash et al (2012).

4 Social Welfare and Scalability

In this section, we consider a fundamental question faced by system designers: what is the optimal amount of money and how does it depend on the size of the system? We discuss how our theoretical results summarized in Section 3 show that in order to maximize social welfare, the optimal amount of money is some constant per agent. Thus, a system designer that wants to maximize social welfare should manage the average quantity of money appropriately. However, we also show that this must be done carefully. Specifically, we show that increasing the amount of money improves performance up to a certain point, after which the system experiences a monetary crash. Once the system crashes, the only equilibrium will be the trivial one where all agents play . Thus, optimizing the performance of the system involves discovering how much money the system can handle before it crashes.

In Section 2, we define the game using a tuple . Thus, our definition of a game uses the average amount of money rather than the equally reasonable total amount of money . The choice is motivated by our theoretical results. Theorem 3.1 shows that the long-term distribution of money depends on the average amount of money, but is independent of , provided that is sufficiently large. Thus, since we normalize by the number of agents in computing utility, the optimal threshold policy for the MDP developed in Appendix A is also independent of . Theorems 3.2 and 3.3 show that such policies constitute an -Nash equilibrium. Thus, modulo a technical issue regarding the rate of convergence of the Markov Chain towards its stationary distribution, to determine the optimal amount of money for a large system, it suffices to determine the optimal value of , the average amount of money per agent.

We remark that, in practice, it may be easier for the designer to vary the price of fulfilling a request than to control the amount of money in the system. This produces the same effect. For example, changing the cost of fulfilling a request from $1 to $2 is equivalent to halving the amount of money that each agent has. Similarly, halving the the cost of fulfilling a request is equivalent to doubling the amount of money that everyone has. With a fixed amount of money, there is an optimal product of the number of agents and the cost of fulfilling a request.

This also tells us how to deal with a dynamic pool of agents. Our system can handle newcomers relatively easily: simply allow them to join with no money. This gives existing agents no incentive to leave and rejoin as newcomers. (By way of contrast, in systems where each new agent starts off with a small amount of money, such an incentive clearly exists.) We then change the price of fulfilling a request so that the optimal ratio is maintained. This method has the nice feature that it can be implemented in a distributed fashion; if all nodes in the system have a good estimate of , then they can all adjust prices automatically. (Alternatively, the number of agents in the system can be posted in a public place.) Approaches that rely on adjusting the amount of money may require expensive system-wide computations (see Vishnumurthy et al (2003) for an example), and must be carefully tuned to avoid creating incentives for agents to manipulate the system by which this is done.

Note that, in principle, the realization that the cost of fulfilling a request can change can affect an agent’s strategy. For example, if an agent expects the cost to increase, then he may want to defer volunteering to fulfill a request. However, if the number of agents in the system is always increasing, then the cost always decreases, so there is never any advantage in waiting. There may be an advantage in delaying a request, but it is far more costly, in terms of waiting costs than in providing service, since we assume the need for a service is often subject to real waiting costs. In particular, many service requests, such as those for information or computation, cannot be delayed without losing most of their value.

Issues of implementation aside, we have now reduced the problem of determining the optimal total amount of money for a large system to that of determining the optimal average amount of money, independent of the exact number of agents. Before we can determine the optimal value of , we have to answer a more fundamental question: given an equilibrium that arose for some value of , how good is it?

Consider a single round of the game with a population of a single type and an equilibrium threshold . If a request is satisfied, social welfare increases by ; the requester gains utility and the satisfier pays a cost of . If no request is satisfied then no utility is gained. What is the probability that a request will be satisfied? This requires two events to occur. First, the agent chosen to make a request must have a dollar, which happens with probability approximately , where is the fraction of agents with no money. Second, there must be a volunteer able and willing to satisfy the request. Any agent who does not have his threshold amount of money is willing to volunteer. Thus, if is the fraction of agents at their threshold, then the probability of having a volunteer is . We believe that in most large systems this probability is quite close to 1; otherwise, either must be unrealistically small or must be very close to 1. For example, even if (i.e., an agent can satisfy 1% of requests), agents will be able to satisfy 99.99% of requests. If is close to 1, then agents will have an easier time earning money then spending money (the probability of spending a dollar is at most , while for large the probability of earning a dollar if an agent volunteers is roughly ). If an agent is playing and there are rounds played a day, this means that for he would be willing to pay today to receive over 10 years from now. For most systems, it seems unreasonable to have or this large. Thus, for the purposes of our analysis, we approximate by 1.

With this approximation, we can write the expected increase in social welfare each round as . If we have more than one type of agent, the situation is essentially the same. The equation for social welfare is more complicated because now the gain in welfare depends on the , , and of the agents chosen in that round, but the overall analysis is the same, albeit with more cases. In the general case,

| (5) |

Thus our goal is clear: find the amount of money that, in equilibrium, minimizes .

In general, as the following theorem shows, decreases as increases. More specifically, given our assumption that the system is starting at the greatest equilibrium , increasing and then following best response dynamics leads to the new greatest equilibrium . As long as is non-trivial, .

Theorems 3.1, 3.2, and 3.3 place requirements on the values of and . Intuitively, the theorems require that the s is sufficiently large to ensure that agents are patient enough that their decisions are dominated by long-run behavior rather than short-term utility, and that is sufficiently large to ensure that small changes in the distribution of money do not move it far from . In the theorems in this section, assume that these conditions are satisfied. To simplify the statements of the theorems, we use “the standard conditions hold” to mean that the game under consideration is such that and for the and needed for the results of Theorems 3.1, 3.2, and 3.3 to apply.

Theorem 4.1

Let be such that the standard conditions hold, and let be the greatest equilibrium for . Then if , the best-reply dynamics in starting at converge to some that is the greatest equilibrium of . If is a nontrivial equilibrium, then .

Proof

In the proof of Theorem 3.3, it is shown that starting at any vector greater than the greatest equilibrium and applying best-reply dynamics (iteratively replacing with the vector of best-reply strategies ) leads to the greatest equilibrium in a finite number of steps. Since is an equilibrium, . By Lemma 4, is non-increasing in . Thus, . Applying best-reply dynamics using starting at gives us an equilibrium such that . By Lemma 4, is non-decreasing in , so this is the greatest equilibrium. Suppose that is nontrivial. By Equations (2) and (5),

Again by Lemma 4, is non-decreasing in and non-increasing in . Thus, .

Theorem 4.1 tells us that, as long as the system does not crash, more money is better. The following corollary tells us that such a crash is an essential feature; a sufficient increase in the amount of money leads to a monetary crash. Moreover, once the system has crashed, adding more money does not cause the system to become “uncrashed.”

Corollary 1

Consider the family of games

such that the

standard conditions hold.

There exists a critical average amount of money such that

if , then has a nontrivial equilibrium, while if , then has no nontrivial equilibria

in threshold strategies.

(A nontrivial equilibrium may or may not exist if .)

Proof

To see that there is some for which has no nontrivial equilibrium, fix . If there is no nontrivial equilibrium in , we are done. Otherwise, suppose that the greatest equilibrium in is . Choose , and let be the greatest equilibrium in . By Theorem 4.1, . But if is a nontrivial equilibrium then, in equilibrium, each agent of type has at most dollars. But then , a contradiction.

Let be the infimum over all for which no nontrivial equilibrium exists in the game . (We know that by Theorem 3.3.) Clearly, by choice of , if , there is a nontrivial equilibrium in . Now suppose that . By the construction of , there exists with such that no nontrivial equilibrium exists in . Let the greatest equilibria with and be and , respectively. By Theorem 4.1, . Thus is also trivial.

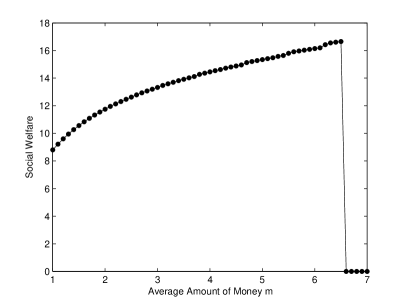

Figure 1 shows an example of the monetary crash in the game with two types of agents (with parameters ) where thirty percent are of the first type, there are 10 agents in the base economy, 100 replicas, and the average amount of money is . Formally, the game is:

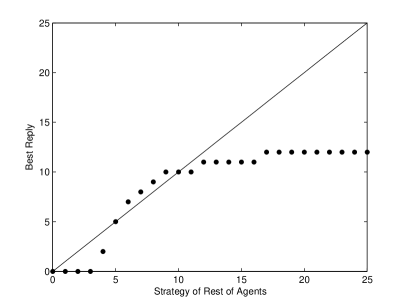

Corollary 1 tells us that this crash is a very sharp phenomenon; with some amount of money the system performs well, but with just slightly more the system stops working. This is a result of the way increasing the amount of money affects agent’s best reply functions. Figure 2, reproduced from our companion paper Kash et al (2012), gives an example of a best reply function with one type of agent. It shows, for a particular fixed value of , how the optimal strategy for an agent depends on the the strategies of the other agents. Thus, an equilibrium is a point on the line : the optimal strategy is exactly the strategy the other agents are using. In this simple case, increasing causes every point to shift downward (since strategies are discrete, there may be some minimum increase for a particular point to shift). With a large enough increase in , every point except (0,0) will be below the line and so there will be no nontrivial equilibrium. The sharpness is a result of there being a critical value at which the last point drops below the line.

In light of Corollary 1, the system designer should try to find , the point where social welfare is maximized. In doing so, it is helpful to have an understanding of the types and strategies of agents in the systems, an issue we discuss in Section 6. In practice, the system designer may want to set the average amount of money to be somewhat less than . Since there will be a crash if , small changes in the characteristics of the population or mistakes by the designer in modeling them could lead to a crash if she chooses too close to .

The phenomenon of a monetary crash is intimately tied to our assumption of fixed prices. We saw such a crash in practice in the babysitting co-op example. If the price is allowed to float freely, we expect that, as the money supply increases, there will be inflation; the price will increase so as to avoid a crash. However, floating prices can create other monetary problems, such as speculation, booms, and busts. Floating prices also impose transaction costs on agents. In systems where prices would normally be relatively stable, these transaction costs may well outweigh the benefits of floating prices, so a system designer may opt for fixed prices, despite the risk of a crash.

We believe there may also be a happy medium between a single, permanent fixed price and prices that change freely from round to round; indeed, our advice to system designers points naturally toward it. In particular, our advice about how to optimize the amount of money relies on experimentation and observation to determine what agents are doing and what their utilities are. This information then tells the designer how much money she should provide. Since adjusting the amount of money is equivalent to adjusting prices, the designer could incorporate this process into a price setting rule. Depending on the nature of the system, this could either be done manually over time (if the information is difficult to gather and analyze) or automatically (if the information gathering and analysis can itself be automated). From this perspective, a monetary crash, though real, is not something to be feared. Instead, it is just a strong signal that the current price, while probably not too far off from a very good price, requires adjustment. Naturally, this relies on a process that proceeds slow enough that agents myopically ignore the effects of future price changes in determining their current action.

Finally, a system designer could consider interventions other than adjusting the amount of money. One obvious opportunity is the process by which volunteers are selected. Our model assumes this process is random, but it need not be. For example, the system designer could attempt to bias the process in favor of agents with smaller amounts of money. Like increasing the average amount of money, this could increase efficiency since agents would spend less time with no money, but could potentially cause a crash, since agents have less of an incentive to save for the future. Our techniques rely on the choice of agents being independent of how much money they have, do not allow us to rigorously analyze this situation. Biasing the volunteer selection rule is an idea we return to in Section 5.3, as agents who create sybils increase their probability of being chosen.

5 Dealing with Nonstandard Agents

The model in Section 2 defines the utility of standard agents, who value service and dislike using their resources to provide it to others. This seems like a natural description of the way most people use distributed systems. However, in a real system, not every user will behave they way the designer intends. A practical system needs to be robust to nonstandard behaviors. In this section, we show how our model can be used to understand the effects of four interesting types of nonstandard behavior. First, an agent might provide service even when he will receive nothing in return, behaving as an altruist. Second, rather than viewing money as a means to satisfy future requests, an agent might place an inherent value on it and start hoarding it. Third, an agent might create additional identities, known as sybils, to try and manipulate the system. Finally, agents might collude with each other.

The results of this section give a system designer insight into how to design a scrip system that takes into account (and is robust to) a number of frequently-observed behaviors.

5.1 Altruists

P2P filesharing systems often have large numbers of free riders; they work because a small number of altruistic users provide most of the files. For example, Adar and Huberman 2000 found that, in the Gnutella network, nearly 50 percent of responses are from the top 1 percent of sharing hosts. A wide variety of systems have been proposed to discourage free riding. However, according to our model, unless this system mostly eliminates the altruistic users, adding such a system will have no effect on rational users.

To make this precise, take an altruist to be someone who always volunteers to fulfill requests, regardless of whether the other agent can pay. Agent might rationally behave altruistically if, rather than suffering a loss of utility when satisfying a request, derives positive utility from satisfying it. Such a utility function is a reasonable representation of the pleasure that some people get from the sense that they provide the music that everyone is playing. For such altruistic agents, the strategy of always volunteering is dominant. While having a nonstandard utility function might be one reason that a rational agent might use this strategy, there are certainly others. For example a naive user of filesharing software with a good connection might well follow this strategy. All that matters for the following discussion is that there are some agents that use this strategy, for whatever reason. For simplicity, we assume that all such agents have the same type .

Suppose that a system has altruists. Intuitively, if is moderately large, they will manage to satisfy most of the requests in the system even if other agents do no work. Thus, there is little incentive for any other agent to volunteer, because he is already getting full advantage of participating in the system. Based on this intuition, it is a relatively straightforward calculation to determine a value of that depends only on the types, but not the number , of agents in the system, such that the dominant strategy for all standard agents is to never volunteer to satisfy any requests.

Proposition 1

For all games with , there exists a value such that, if (i.e., there are at least altruists), then never volunteering is a dominant strategy for all standard agents.

Proof

Consider the strategy for a standard agent in the presence of altruists. Even with no money, agent will get a request satisfied with probability just through the actions of the altruists. Consider a round when agent is chosen to make a request. If he has no money (because he never volunteered), his expected utility is . His maximum possible utility for the round is . Thus, a strategy where he volunteers can increase his utility for a round by at most . Thus, even if the agent gets every request satisfied, his expected utility can increase by at most

Clearly this expression goes to 0 as goes to infinity. If we take large enough that the expression is less than for all types , then the value of having every future request satisfied is less than the cost of volunteering now, so no agent will ever volunteer.

Consider the following reasonable values for our parameters: (so that each player can satisfy 1% of the requests), , (a low but non-negligible cost), /day (which corresponds to a yearly discount factor of approximately ), and an average of 1 request per day per player. Then as long as to ensure that not volunteering is a dominant strategy. While this is a large number, it is small relative to the size of a large P2P network. While the number of altruists needed to degrade the performance of the system increases somewhat with the number of agents, the point remains that a small fraction of altruists can discourage the rest of the system from providing service.

Proposition 1 shows that with enough altruists, the system eventually experiences a monetary crash, since all agents will use a threshold of zero. However, interesting behavior can still arise with smaller numbers of altruists. consider the situation where an fraction of requests are immediately satisfied at no cost without the requester needing to ask for volunteers. Intuitively, these are the requests satisfied by the altruists, although the following result also applies to any setting where agents occasionally have a (free) outside option. The following theorem shows that social welfare is increasing in .

Let be a game with a single type for which the standard conditions hold. Consider the family of games (parameterized by ) that result from if a fraction of requests can be satisfied at no cost. That is, the game is the same as , except that if an agent makes a request, with probability , it is satisfied at no cost, and with probability , an agent is chosen among the volunteers to satisfy the request, just as in , and the is charged 1 dollar to have the request satisfied.

Theorem 5.1

For the interval of values of where there is no monetary crash in , social welfare increases as increases (assuming that the greatest equilibrium is played by all agents in ).

Proof

An agent’s utility in a round where he makes a request and it is satisfied at no cost is . Since such rounds occur with probability , by assumption, our normalization guarantees that the sum of standard agents’ expected utilities in rounds where a request is satisfied at no cost is . The same analysis as in Section 4 shows that the sum of agents’ expected utilities in each of the remaining rounds is , where, as before, , the equilibrium value of in the game . Thus, expected utility as a function of is

| (6) |

To see that this expression increases as increases, we would like to take the derivative relative to and show it is positive. Unfortunately, may not even be continuous. Because strategies are integers, there will be regions where is constant, and then a jump when a critical value of is reached that causes the equilibrium to change. At a point in a region where is constant, , so the derivative of Equation (6) is . Hence, social welfare is increasing at such points.

Now consider a point where is discontinuous. Such a discontinutity occurs when the greatest equilibrium, the greatest value for which , changes. We show that, for a fixed , is non-increasing in . Since increasing can only cause the to decrease, the discontinuity must be caused by a change from an equilibrium to a new equilibrium . Fix a vector of thresholds, and let be the probability that will earn a dollar in a given round if he is willing to volunteer, given that a fraction of requests is satisfied at no cost (so that is what we earlier called ); we similarly define , his probability of being chosen to make a request. It is easy to see that and . The random variable in Equation (4) describes the first time at which an agent starting with dollars and using the threshold while earning a dollar with probability and spending a dollar with probability reaches zero dollars. As increases, and both decrease, but the ratio remains constant. Intuitively, this means that the agent “slows down” his random walk on amounts of money by a factor of . This slowdown occurs because, each time the agent would have an opportunity to volunteer or would have spent a dollar, with probability the opportunity is taken by an altruist instead, so the expected time to take a step increases by a factor of . Thus, the value of the expectation in Equation (4), and hence the right-hand side of Equation (4), decreasing as a function of . By Lemma 3, is the maximum value of such that Equation (4) is satisfied. Decreasing the right-hand side can only decrease the maximum value of , so is non-increasing as a function of .

By Lemma 4, is non-increasing in (unless the system crashes, after which it remains crashed even when a is increased further, as in Corollary 1, where the points at which social welfare is increasing form an interval). Since, as we have just shown, if there is a discontinuity at when increases, the greatest equilibrium changes at from to , we must have . In Equation (2) for , the value of the numerator is independent of , but the denominator with is greater than or equal to the denominator with . Thus is non-increasing at . By Equation (6), this means that expected utility is increasing at . Thus, in either case, social welfare is increasing in .

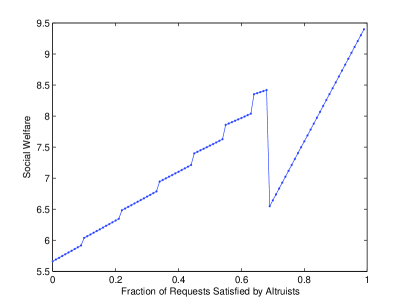

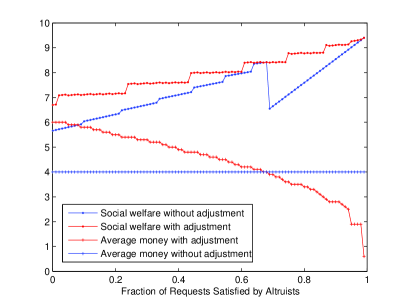

Theorem 5.1 and Proposition 1 combine to tell us that a little altruism is good for the system, but too much causes a crash. Figure 3 demonstrates this phenomenon. As we saw in Section 4, such crashes are caused when , the average amount of money, is too large. By decreasing appropriately, even relatively large values of can be exploited, as Figure 4 shows. The “social welfare without adjustment” plot is the same data from Figure 3, with the corresponding plot of the amount of money horizontal since was held fixed. By decreasing the average amount of money appropriately as the number of altruists increases, a system designer can increase social welfare while avoiding a crash of the economy (the system will still function due to the presence of altruists). Note that, in discussing social welfare, our formulation excludes the welfare of the altruists, since our focus here is on the effects of altruism on standard agents.

5.2 Hoarders

Whenever a system allows agents to accumulate something, be it work done, as in SETI@home, friends on online social networking sites, or “gold” in an online game, a certain group of users seems to make it their goal to accumulate as much of it as possible. In pursuit of this, they will engage in behavior that seems irrational. For simplicity here, we model hoarders as playing the strategy . This means that they will volunteer under all circumstances. Our analysis would not change significantly if we also required that they never made a request for work. Our first result shows that, for a fixed money supply, having more hoarders makes standard agents worse off.

Consider a game such that the standard conditions hold. Consider the family of games (parameterized by ) that result from if a fraction of agents are hoarders. That is, where an agent of type is a standard agent of type , but an agent of type is a hoarder and always uses the strategy (his probabilities are still determined by , , and ). Define by taking and for all types . Let be the smallest multiple of such that is an integer for all and . (We need to adjust because otherwise the number of agents in the base game may not be well defined.) Finally, to account for the changed , let .

Theorem 5.2

In the family of games, social welfare is non-increasing in (if the greatest equilibrium is played by all agents in ).

Proof

Let denote the greatest equilibrium in . An increase in is equivalent to taking some number of standard agents and increasing their strategy to . It follows from Lemma 4 that is non-decreasing in , and so is non-decreasing in . Again by Lemma 4, is non-increasing in . Let be the fraction of non-hoarders with zero dollars, where is the value of at the greatest equilibrium of . By Equation (2), is non-decreasing in . Thus, social welfare is non-increasing in .

Hoarders do have a beneficial aspect. As we have observed, a monetary crash occurs when a dollar becomes valueless, because there are no agents willing to take it. However, with hoarders in the system, there is always someone who will volunteer, so there cannot be a crash. Thus, for any , the greatest equilibrium will be nontrivial and, by Theorem 4.1, social welfare keeps increasing as increases. So, in contrast to altruism, where the appropriate response was to decrease , the appropriate response to hoarders is to increase . In fact, our results indicate that the optimal response to hoarders is to make infinite. This is due to our unrealistic assumption that hoarders would use the strategy regardless of the value of . There is likely an upper limit on the value of in practice, since it is unlikely that hoarders would be willing to hoard scrip if it is so easily available.

5.3 Sybils

Unless identities in a system are tied to a real world identity (for example by a credit card), it is effectively impossible to prevent a single agent from having multiple identities Douceur (2002). Nevertheless, there are a number of techniques that can make it relatively costly for an agent to do so. For example, Credence uses cryptographic puzzles to impose a cost each time a new identity wishes to join the system Walsh and Sirer (2006). Given that a designer can impose moderate costs to sybilling, how much more need she worry about the problem? In this section, we show that the gains from creating sybils when others do not diminish rapidly, so modest costs may well be sufficient to deter sybilling by typical users. However, sybilling is a self-reinforcing phenomenon. As the number of agents with sybils gets larger, the cost to being a non-sybilling agent increases, so the incentive to create sybils becomes stronger. Therefore, measures to discourage or prevent sybilling should be taken early before this reinforcing trend can start. Finally, we examine the behavior of systems where only a small fraction of agents have sybils. We show that under these circumstances a wide variety of outcomes are possible (even when all agents are of a single type), ranging from a crash (where no service is provided) to an increase in social welfare. This analysis provides insight into the tradeoffs between efficiency and stability that occur when controlling the money supply of the system’s economy.

When an agent of type creates sybils, the only parameter of his type that may change as a result is , if we redefine the likelihood of an agent being chosen to be the likelihood of the agent or any of his sybils being chosen. The other parameters, such as , remain unchanged because there is no particular reason that having multiple identities should cause the agent to, for example, desire service more often. For simplicity, we assume that each sybil is as likely to be chosen as the original agent, so creating sybils increases by . (Sybils may have other impacts on the system, such as increased search costs, but we expect these to be minor.)

Increasing benefits an agent by increasing his value of and thus , his probability of earning a dollar (see Equation (8) in Appendix A). When , the agent has more opportunities to spend money than to earn money, so he will regularly have requests go unsatisfied due to a lack of money. In this case, the fraction of requests he has satisfied is roughly , so increasing by creating sybils results in a roughly linear increase in utility. As Theorem 5.3 shows, when is close to , the increase in satisfied requests is no longer linear, so the benefit of increasing begins to diminish. Finally, when , most of the agent’s requests are being satisfied, so the benefit from increasing is very small. Figure 5 illustrates an agent’s utility as varies for .444 Except where otherwise noted, the remaining figures in this section assume that , and that there is a single type of rational agent with , , , , , and . These values are chosen solely for illustration, and are representative of a broad range of parameter values. The figures are based on calculations of the equilibrium behavior. We formalize the relationship between , , and the agent’s utility in the following theorem, whose proof is deferred to Appendix B.

Theorem 5.3

Fix a game and vector of thresholds . Let . In the limit as the number of rounds goes to infinity, the fraction of the agent’s requests that have an agent willing and able to satisfy them that get satisfied is if and if .

Theorem 5.3 gives insight into the equilibrium behavior with sybils. Clearly, if sybils have no cost, then creating as many as possible is a dominant strategy. However, in practice, we expect there is some modest overhead involved in creating and maintaining a sybil, and that a designer can take steps to increase this cost without unduly burdening agents. With such a cost, adding a sybil might be valuable if is much less than , and a net loss otherwise. This makes sybils a self-reinforcing phenomenon. When a large number of agents create sybils, agents with no sybils have their significantly decreased. This makes them much worse off and makes sybils much more attractive to them. Figure 6 shows an example of this effect. This self-reinforcing quality means that it is important to take steps to discourage the use of sybils before they become a problem. Luckily, Theorem 5.3 also suggests that a modest cost to create sybils will often be enough to prevent agents from creating them because with a well chosen value of , few agents should have low values of .

We have interpreted Figures 5 and 6 as being about changes in due to sybils, but the results hold regardless of what caused differences in . For example, agents may choose a volunteer based on characteristics such as connection speed or latency. If these characteristics are difficult to verify and do impact decisions, our results show that agents have a strong incentive to lie about them. This also suggests that the decision about what sort of information the system should enable agents to share involves tradeoffs. If advertising legitimately allows agents to find better service or more services they may be interested in, then advertising can increase social welfare. But if these characteristics impact decisions but have little impact on the actual service, then allowing agents to advertise them can lead to a situation like that in Figure 6, where some agents have a significantly worse experience.

We have seen that when a large fraction of agents have sybils, those agents without sybils tend to be starved of opportunities to work (i.e. they have a low value of ). However, as Figure 6 shows, when a small fraction of agents have sybils this effect (and its corresponding cost) is small. Surprisingly, if there are few agents with sybils, an increase in the number of sybils these agents have can actually result in a decrease of their effect on the other agents. Because agents with sybils are more likely to be chosen to satisfy any particular request, they are able to use lower thresholds and reach those thresholds faster than they would without sybils, so fewer are competing to satisfy any given request. Furthermore, since agents with sybils can almost always pay to make a request, they can provide more opportunities for other agents to satisfy requests and earn money. Social welfare is essentially proportional to the number of satisfied requests (and is exactly proportional to it if everyone shares the same values of and ), so a small number of agents with a large number of sybils can improve social welfare, as Figure 7 shows. Note that, although social welfare increases, some agents may be worse off. For example, for the choice of parameters in this example, social welfare increases when twenty percent of agents create at least two sybils, but agents without sybils are worse off unless the twenty percent of agents with sybils create at least eight sybils. As the number of agents with sybils increases, they start competing with each other for opportunities to earn money and so adopt higher thresholds, and this benefit disappears. This is what causes the discontinuity in Figure 6 when approximately a third of the agents have sybils.

This observation about the discontinuity also suggests another way to mitigate the negative effects of sybils: increase the amount of money in the system. This effect can be seen in Figure 8, where for social welfare is very low with sybils but by it is higher than it would be without sybils.

Unfortunately, increasing the average amount of money has its own problems. Recall from Section 4 that, if the average amount of money per agent is too high, the system will crash. It turns out than just a small number of agents creating sybils can have the same effect, as Figure 8 shows. With no sybils, the point at which social welfare stops increasing and the system crashes is between and (we only calculated social welfare for values of that are multiples of 0.25, so we do not know the exact point of the crash). If one-fifth of the agents each create a single sybil, the system crashes if , a point where, without sybils, the social welfare was near optimal. Thus, if the system designer tries to induce optimal behavior without taking sybils into account, the system will crash. Moreover, because of the possibility of a crash, raising to tolerate more sybils is effective only if was already set conservatively.

This discussions shows that the presence of sybils can have a significant impact on the tradeoff between efficiency and stability. Setting the money supply high can increase social welfare, but at the price of making the system less stable. Moreover, as the following theorem shows, whatever efficiencies can be achieved with sybils can be achieved without them, at least if there is only one type of agent. In the theorem, we consider a system where all agents have the same type . Suppose that some subset of the agents have created sybils, and all the agents in the subset have created the same number of sybils. We can model this by simply taking the agents in the subsets to have a new type , which is identical to except that the value of increases. Thus, we state our results in terms of systems with two types of agents, and .

Theorem 5.4

Suppose that and are two types that agree except for the value of , and that . If is an -Nash equilibrium for with social welfare , then there exist , , and such that is an -Nash equilibrium for with social welfare greater than .

The analogous result for systems with more than one type of agent is not true. Figure 6 shows a game with a single type of agent, some of whom have created two sybils. However, we can reinterpret it as a game with two types of agents, one of whom has a larger value of . With this reinterpretation, Figure 6 shows that social welfare is higher when all the agents are of the type with the higher value of than when only 40% are. Moreover, if only 40% of the agents have type , social welfare would increase if the remaining agents created two sybils each (resulting in all agents having the higher value of ). Note that this situation, where there are two types of agents, of which one has a higher value of , is exactly the situation considered by Theorem 5.4. Thus, the theorem shows that for any equilibrium with two such types of agents, there is a better equilibrium where one of those types creates sybils so as to effectively create only one type of agent.

While situations like this show that it is theoretically possible for sybils to increase social welfare beyond what is possible to achieve by simply adjusting the average amount of money, this outcome seems unlikely in practice. It relies on agents creating just the right number of sybils. For situations where such a precise use of sybils would lead to a significant increase in social welfare, a designer could instead improve social welfare by biasing the algorithm agents use for selecting which volunteer will satisfy the request.

Thus far, we have assumed that when agents create sybils the amount of money in the system does not change. However, the presence of sybils increases the number of apparent agents in the system. Since social welfare depends on the average amount of money per agent, if the system designer mistakes these sybils for an influx of new users and increases the money supply accordingly, she will actually end up increasing the average amount of money in the system, and may cause a crash. This emphasizes the need for continual monitoring of the system rather that just using simple heuristics to set the average amount of money, an issue we discuss more in Section 6.

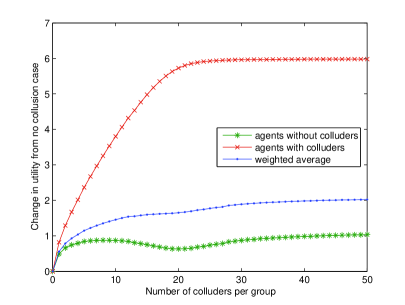

5.4 Collusion