Stochastic finite differences and multilevel Monte Carlo for a class of SPDEs in finance

Abstract

In this article, we propose a Milstein finite difference scheme for a stochastic partial differential equation (SPDE) describing a large particle system. We show, by means of Fourier analysis, that the discretisation on an unbounded domain is convergent of first order in the timestep and second order in the spatial grid size, and that the discretisation is stable with respect to boundary data. Numerical experiments clearly indicate that the same convergence order also holds for boundary-value problems. Multilevel path simulation, previously used for SDEs, is shown to give substantial complexity gains compared to a standard discretisation of the SPDE or direct simulation of the particle system. We derive complexity bounds and illustrate the results by an application to basket credit derivatives.

1 Introduction

Various stochastic partial differential equations (SPDEs) have emerged over the last two decades in different areas of mathematical finance. A classical example is the Heath-Jarrow-Morton interest rate model [Heath et al.(1992)] of the form

| (1) |

where is the forward rate of tenor at time and its instantaneous volatility. In [Benth & Koekebakker(2008)], a similar equation has been proposed more recently to model electricity forwards. Most of the SPDEs studied share with (1) the property that the derivatives of the solution only appear in the drift term; in the case of (1) the volatility of the Brownian driver does not depend on the solution at all. Numerical methods for hyperbolic SPDEs of the type (1) have been studied, for example, in [Roth(2002)].

This article, in contrast, considers the parabolic SPDE

| (2) |

where is a standard Brownian motion, and and are real-valued parameters. It is clear that the behaviour of this equation is fundamentally different from those with additive or multiplicative noise.

The significance of (2) for the following applications is that it describes the limiting density of a large system of exchangeable particles. Specifically, if we consider the system of SDEs

| (3) |

for , with and , where are assumed i.i.d. with finite second moment, the empirical measure

has a limit for , whose density satisfies (2) in a weak sense. For a derivation of this result in the more general context of quasi-linear PDEs see [Kurtz & Xiong(1999)]. While the motivation in [Kurtz & Xiong(1999)] is to use a large particle system (3) to approximate the solution to the SPDE (2), our view point is to use (2) as an approximate model for a large particle system, and we will argue later the (computational) advantages of this approach in situations when the number of particles is large.

As a first possible application, one may consider as the log price processes of a basket of equities, which have idiosyncratic components and share a common driver (the “market”). If the size of the basket is large enough, the solution to the SPDE can be used to find the values of basket derivatives. In this paper, we study an application of a similar model to basket credit derivatives.

We mention in passing that equations of the form (2) arise also in stochastic filtering. To be precise, (2) is the Zakai equation for the distribution of a signal given observation of , see e.g. [Bain & Crisan(2009)].

It is interesting to note that the solution to the SPDE (2) without boundary conditions can be written as the solution of the PDE

| (4) |

shifted by the current value of the Brownian driver,

| (5) |

In particular, if , then

| (6) |

The intuitive interpretation of this result is that the independent Brownian motions have averaged into a deterministic diffusion in the infinite particle limit, whereas the common factor , which moves all processes in parallel, shifts the whole profile (and also adds to the diffusion, via the Itô term).

In [Bush et al.(2011)], the analysis of the large particle system is extended to cases with absorption at the boundary (),

| (7) |

It is shown that there is still a limit measure , which may now be decomposed as

where

| (8) |

is the proportion of absorbed particles (the “loss function”), and the density of satisfies (2) in with absorbing boundary condition

| (9) |

[Bush et al.(2011)] consider applications to basket credit derivatives. For the market pricing examples, they consider a simplified model, where defaults are monitored only at a discrete set of dates. Between these times, the default barrier is inactive and (2) is solved on the real line by using (4) and (5).

For the initial-boundary value problem (2), (9), however, such a semi-analytic solution strategy is no longer possible and an efficient numerical method is needed. Moreover, there is a loss of regularity at the boundary in this case, such that but not , as is documented in [Krylov(1994)].

Recent papers on the numerical solution of SPDEs deal with cases relevant to ours, yet structurally crucially different. A comprehensive analysis of finite difference and finite element discretisations of the stochastic heat equation with multiplicative white noise and non-linear driving term is given in [Gyöngy & Nualart(1997), Gyöngy(1999)] and [Walsh(2005)], respectively. [Lang(2010)] shows a Lax equivalence theorem for the SDE

in a Hilbert space, driven by a process from a class including Brownian motion, where is a suitable (e.g. elliptic differential) operator and a Lipschitz function.

In this paper, we propose a Milstein finite difference discretisation for (2) and analyse its stability and convergence in the mean-square sense by Fourier analysis. A main consideration of this paper is the computational complexity of the proposed methods, and we will demonstrate that a multilevel approach achieves a cost for the SPDE simulation no larger than that of direct Monte Carlo sampling from a known univariate distribution, for r.m.s. accuracy , and is in that sense optimal.

Multilevel Monte Carlo path simulation, first introduced in [Giles(2008a)], is an efficient technique for computing expected values of path-dependent payoffs arising from the solution of SDEs. It is based on a multilevel decomposition of Brownian paths, similar to a Brownian Bridge construction. The complexity gain can be explained by the observation that the variance of high-level corrections – involving a large number of timesteps – is typically small, and consequently only a relatively small number Monte Carlo samples is required to estimate these contributions to an acceptable accuracy. Overall, for SDEs, if a r.m.s. accuracy of is required, the standard Monte Carlo method requires operations, whereas the multilevel method based on the Milstein discretisation [Giles(2008b)] requires operations.

The first extension of the multilevel approach to SPDEs was for parabolic PDEs with a multiplicative noise term [Graubner(2008)]. There have also been recent extensions to elliptic PDEs with random coefficients [Barth et al.(2010), Cliffe et al.(2011)].

Our approach, for a rather different parabolic SPDE, is similar to the previous work on SDEs and SPDEs in that the solution is decomposed into a hierarchy with increasing resolution in both time and space. Provided the variance of the multilevel corrections decreases at a sufficiently high rate as one moves to higher levels of refinement, the number of fine grid Monte Carlo simulations which is required is greatly reduced. Indeed, the total cost is only to achieve a r.m.s. accuracy of compared to an cost for the standard approach which combines a finite difference discretisation of the spatial derivative terms and a Milstein discretisation of the stochastic integrals.

The rest of the paper is structured as follows. Section 2 outlines the finite difference scheme used, and analyses its accuracy and stability in the standard Monte Carlo approach. Section 3 presents the modification to multilevel path simulation of functionals of the solution. Numerical experiments for a CDO tranche pricing application are given in section 4, providing empirical support for the postulated properties of the scheme and demonstrating the computational gains achieved. Section 5 discusses the benefits over standard Monte Carlo simulation of particle systems and outlines extensions.

2 Discretisation and convergence analysis

2.1 Milstein finite differences

Integrating (2) over the time interval gives

Making the approximation for in the first integral and

in the second, and noting the standard Itô calculus result that

where with , [Glasserman(2004), Kloeden & Platen(1992)], leads to the Milstein semi-discrete approximation

Using a spatial grid with uniform spacing , standard central difference approximations to the spatial derivatives [Richtmyer & Morton(1967)] then give the finite difference equation

| (10) | |||||

in which is an approximation to .

The spatial domain is truncated by introducing an upper boundary at and using the boundary condition . Since the initial distribution will be assumed localised, both the localisation error for a given path , and the expected error of functionals of the solution, can be made as small as needed by a large enough choice .

The system of SDEs can then be written in matrix-vector form

| (11) |

where is the vector with elements and and are the matrices corresponding to first and second central differences as explicitly given in Appendix A.

Remark 2.1

An alternative discretisation arises if the spatial derivatives are discretised first, and the Milstein scheme is applied to the resulting system of SDEs. The practical implication is that the Itô term then contains a second finite difference with twice the step size, instead of , resulting in pentadiagonal discretisation matrices instead of tridiagonal ones, specifically

| (12) |

The accuracy and stability of the two schemes are similar, hence we will not go into details.

To approximate the initial condition on the grid, we apply the initial measure to a basis of ‘hat functions’ , where

giving

For the corresponding PDE (), this is known to result in convergence provided satisfies a certain stability limit, even when the initial data are not smooth [Pooley et al.(2003), Carter & Giles(2007)]. We will see that an extension of this analysis holds for SPDEs.

2.2 Fourier stability analysis

Finite difference Fourier stability analysis ignores the boundary conditions and considers Fourier modes of the form

| (13) |

which satisfy (10) provided

where

Following the approach of mean-square stability analysis from [Higham(2000), Saito & Mitsui(1996)], we obtain

where denotes the complex conjugate of . Mean-square stability therefore requires

and enforcing this for all leads to the two conditions summarised in the following theorem.

Theorem 2.1

The Milstein finite difference scheme (11) is stable in the mean-square sense provided

| (14) | |||||

| (15) |

The analysis in Appendix A combines mean-square and matrix stability analysis to prove that in the limit the condition is also a sufficient condition for mean-square stability of the initial-boundary value problem with the boundary conditions at and .

2.3 Fourier analysis of accuracy

Fourier analysis can also be used to examine the accuracy of the finite difference approximation in the absence of boundary conditions. Considering a Fourier mode of the form the PDE (4) reveals that

and therefore

where . Fourier analysis of the discretisation gives

where , , are as defined before. Writing

we obtain, after performing lengthy expansions using MATLAB’s Symbolic Toolbox,

where, for all ,

When summing over timesteps, and are both since they have zero expectation and variance. Hence, it follows that

so the RMS error in the Fourier mode over the full simulation interval is .

Following the method of analysis in [Carter & Giles(2007)], it can be deduced from this that the RMS and errors for are both . This is consistent with the usual accuracy of the forward-time central space discretisation of a parabolic PDE [Richtmyer & Morton(1967)], and the strong accuracy of the Milstein discretisation of an SDE, see e.g. [Kloeden & Platen(1992)].

2.4 Convergence tests

We now test the accuracy and stability of the scheme numerically.

The chosen parameters for (2) are , , , , with . These values are typical for the applications later on.

The upper boundary for the computation is , and chosen to ensure that the use of zero Dirichlet data has negligible influence on the solution.

We approximate the initial value problem without boundary conditions on (note is roughly in the centre), and also the initial-boundary value problem with zero Dirichlet conditions on .

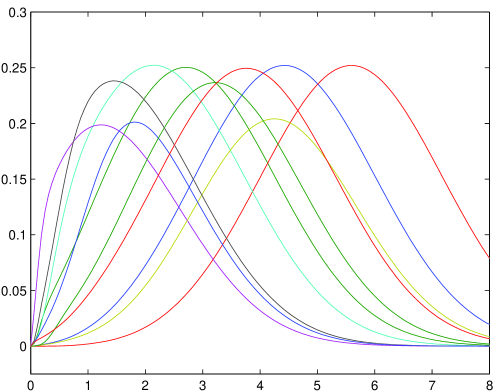

Figure 1 plots several solutions to the latter problem at , each corresponding to a different Brownian path .

It can be seen that for those realisations for which has been largely positive, the boundary at has had negligible influence and so the solution is approximately equal to the displaced Normal distribution given by (6).

For the unbounded case, we approximate the mean-square -error by

| (16) | |||||

where is the number of grid intervals, the number of timesteps, and the expectation is taken over Brownian paths , of which are samples.

To study the convergence, we introduce decreasing grid sizes and timesteps , motivated by the second order convergence in and first order convergence in as well as the stability limit for the explicit scheme, and denote the mean-square -error at level .

For the initial-boundary value problem, no analytical solution is known, but we can compute error indicators via the difference between a fine grid solution with mesh parameters and , and a coarse solution with mesh parameters and ,

| (17) | |||||

and define .

On the coarsest level, , , such that does not coincide with a grid point.

Fig. 2 shows both the computed values of and for the unbounded case, and for the bounded case.

The results confirm the theoretical convergence in the unbounded case, and support the conjecture that the convergence order is unchanged in the bounded case.

We now formalise this conjecture about the error due to the SPDE discretisation. Denote the solution to the initial boundary value problem at time for a given Brownian path and its numerical approximation with grid size and timestep .

Conjecture 2.1

The error in the solution at time satisfies the strong error estimate in the norm

Corollary 2.1

A Lipschitz payoff function has a similar strong error bound

We know Conjecture 2.1 to be true for the initial value problem on , and it conjectures that the introduction of the boundary condition at does not affect the (weak and) strong error, which is supported by the numerical results.

The conjecture assumes ; in practice, a finite value for will introduce an additional truncation error which will decay exponentially in .

Numerical tests with different parameters, not reproduced here, indicate that the error in the bounded case increases for values of close to 0, in which case more paths contribute solutions with large higher derivatives close to the zero boundary, even if the asymptotic convergence order is still . We analyse this loss of regularity further in Appendix B.

3 Multilevel Monte Carlo simulation

We now consider estimating the expectation of a scalar functional of the SPDE solution, an expected “payoff” in a computational finance context.

Defining to be the payoff arising from a single SPDE approximation, the standard Monte Carlo approach is to average the payoff from independent SPDE simulations, each one using an independent vector of Normal variables . Thus the estimator for the expected value is

The mean square error for this estimator can be expressed as the sum of two contributions, one due to the variance of the estimator and the other due to the error in its expectation,

To achieve a r.m.s. error of requires that both of these terms are . This in turn requires that , and , based on the conjecture that the weak error is . Since the computational cost is proportional to this implies an overall cost which is . The aim of the multilevel Monte Carlo simulation is to reduce this complexity to .

Consider Monte Carlo simulations with different levels of refinement, , with being the coarsest level, (i.e. the largest values for and ) and level being the finest level corresponding to that used by the standard Monte Carlo method.

Let denote an approximation to payoff using a numerical discretisation with parameters and . Because of the linearity of the expectation operator, it is clearly true that

| (18) |

This expresses the expectation on the finest level as being equal to the expectation on the coarsest level plus a sum of corrections which give the difference in expectation between simulations using different numbers of timesteps. The multilevel idea is to independently estimate each of the expectations on the right-hand side in a way which minimises the overall variance for a given computational cost.

Let be an estimator for using samples, and let for be an estimator for using samples. Each estimator is an average of independent samples, which for is

| (19) |

The key point here is that the quantity comes from two discrete approximations using the same Brownian path. The variance of this simple estimator is where is the variance of a single sample. Combining this with independent estimators for each of the other levels, the variance of the combined estimator is The corresponding computational cost is where represents the cost of a single sample on level . Treating the as continuous variables, the variance is minimised for a fixed computational cost by choosing to be proportional to , with the constant of proportionality chosen so that the overall variance is .

The total cost on level is proportional to . If the variance decays more rapidly with level than the cost increases, the dominant cost is on level . The number of samples on that level will be and the cost savings compared to standard Monte Carlo will be approximately , reflecting the different costs of samples on level compared to level . On the other hand, if the variance decays more slowly than the cost increases, the dominant cost will be on the finest level , and the cost savings compared to standard Monte Carlo will be approximately , reflecting the difference between the variance of the finest grid correction compared to the variance of the standard Monte Carlo estimator, which is similar to .

This outline analysis is made more precise in the following theorem:

Theorem 3.1

Let denote a functional of the solution of an SPDE for a given Brownian path , and let denote the corresponding level numerical approximation.

If there exist independent estimators based on Monte Carlo samples, and positive constants such that and

-

i)

-

ii)

-

iii)

-

iv)

where is the computational complexity of

then there exists a positive constant such that for any there are values and for which the multilevel estimator

has a mean-square-error with bound

with a computational complexity with bound

Proof The proof is a slight generalisation of the proof in [Giles(2008a)].

In our application, we choose and so that the ratio is held fixed to satisfy the finite difference stability condition. The computational cost increases by factor 8 in moving from level to , so .

4 Numerical experiments

In this section we study the numerical performance of the algorithms presented earlier on the example of CDO tranche pricing in a large basket limit.

4.1 CDO pricing in the structural credit model

Basket credit derivatives provide protection against the default of a certain segment (‘tranche’) of a basket of firms. A typical example is that of a collateralized debt obligation where the protection buyer receives a notional amount, minus some recovery proportion , if firms in a specified tranche of the basket default, and in return pays a regular spread until the default event occurs.

The arbitrage-free spread depends crucially on the (risk-neutral, when hedged with defaultable bonds) probability of joint defaults. For a tranche with attachment point and detachment point , the outstanding tranche notional

| (20) |

where the loss variable is the proportion of losses in the basket up to time , determines the spread and default payments related to that tranche. The risk-neutral value of the tranche spread can be derived as

| (21) |

see, e.g., [Bush et al.(2011)]. Here, is the maximum number of spread payments, the expiry, the payment dates for , the interval between payments. Spreads are quoted as an annual payment, as a ratio of the notional, but assumed to be paid quarterly. 111There is a variation for the equity tranche, and recently sometimes the mezzanine tranche, but we do not go into details here.

For an extensive survey of credit derivatives and pricing models we refer the reader to [Schönbucher(2003)], and note only that they typically fall in one of two classes: so-called reduced-form models, which model default times of firms directly as (dependent) random variables; structural models, which capture the evolution of the firms’ values, and model default events as the first passage of a lower default barrier. We will consider the latter here.

In a structural model in the spirit of the classical works of [Merton(1974)] and [Black & Cox(1976)], as extended to multiple firms e.g. in the work of [Hull et al.(2005)], a company ’s firm value, , is assumed to follow a model of the type

where is a correlation parameter, is the risk-free interest rate, the volatility, and , are standard Brownian motions.

Here, the individual firms are correlated through a common ‘market’ factor , but independent conditionally on . We make in the following the assumption that the firms are exchangeable in the sense that their dynamics is governed by the same set of parameters, specifically , . Their initial values are not necessarily identical which allows for different default probabilities for individual firms, consistent with their CDS spreads.

In this framework, the default time of the -th firm is modelled as the first hitting time of a default barrier , for simplicity constant, and the distance-to-default

| (22) |

evolves according to (3), where , . as in (7) is precisely the default time.

In the majority of applications, Monte Carlo simulation of the firm value processes is used for the estimation of tranche spreads, see e.g. [Hull et al.(2005)] or [Fouque et al.(2008), Carmona et al.(2009)]. This is largely enforced by the size of , for instance in the case of index tranches .

This, however, puts the model precisely in the realm of the large basket approximation (2). See [Bujok & Reisinger(2012)] for a numerical study of this large basket approximation. The loss functional is thereby approximated by

in terms of the numerical SPDE solution at time , which feeds into the estimator for the outstanding tranche notional (20) and subsequently the tranche spreads (21).

4.2 Pricing results

All following results are for a representative set of parameter values, taken from a calibration performed in [Bush et al.(2011)] to 2007 market data, , , , . While the initial distribution used in [Bush et al.(2011)] is somewhat spread out to match individual CDS spreads of obligors, most of the mass is around and for simplicity we centre all firms there for the numerical tests, . The upper boundary is chosen as .

We consider a maturity and tranches , , , , , .

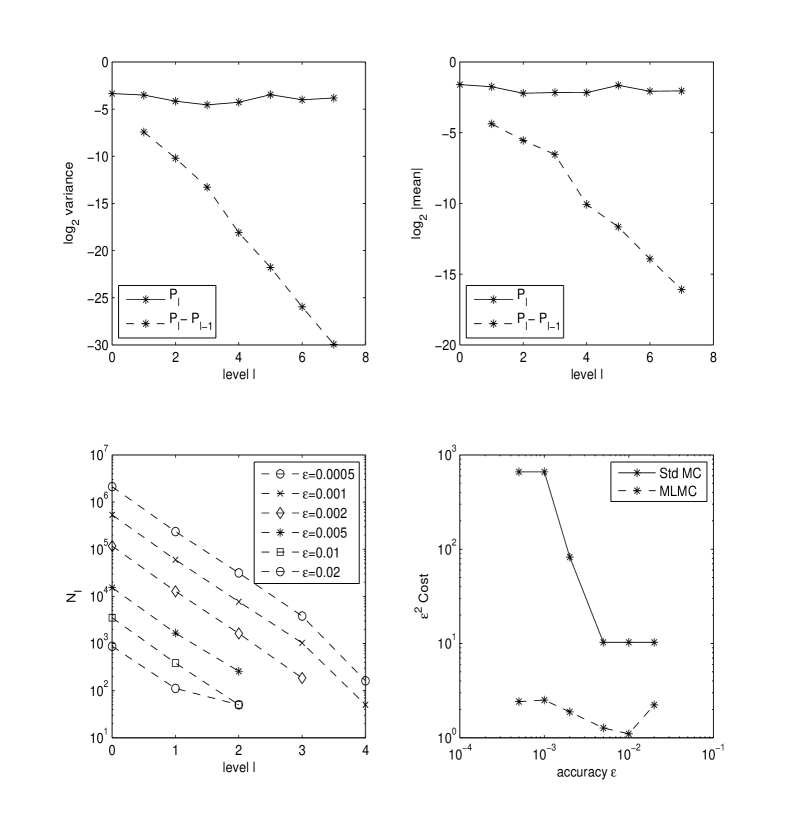

Figure 3 shows the multilevel results for the expected protection payment from the first tranche,

expressed as a fraction of the initial tranche notional.

We pick mesh sizes and for and , . This is motivated by the second and first order consistency in and respectively, and within the stability limit (15).

The top-left plot shows the convergence of the variance as well as the variance of the standard single level estimate, while the top-right plot shows the convergence of the expectation .

The bottom-left plot shows results for different multilevel calculations, each with a different user-specified accuracy requirement. For each value of the accuracy , the multilevel algorithm determines (by formula (12) from [Giles(2008a)]) the numbers of levels of refinement which are needed to ensure that the contribution to the Mean Square Error (MSE) due to the weak error on the finest grid is less than , and it determines (by formula (10) from [Giles(2008a)]) the optimal number of samples on each level so that the combined variance of the multilevel estimate is also less than , and hence the MSE is less than .

Treating a single finite difference calculation on the coarsest level as having a unit cost, the bottom-right plot compares the total cost of the standard and multilevel algorithms. Since the objective is to achieve a computational cost which is approximately proportional to , it is the cost multiplied by which is plotted versus . The results confirm that does not vary much as for the multilevel method, in line with the prediction that , whereas it grows significantly for the standard method since , where is the index of the finest level. Hence, there is a big jump in the cost of the standard method each time it is necessary to switch to a finer level to ensure the weak error is less than , whereas the jump is minimal for the multilevel method.

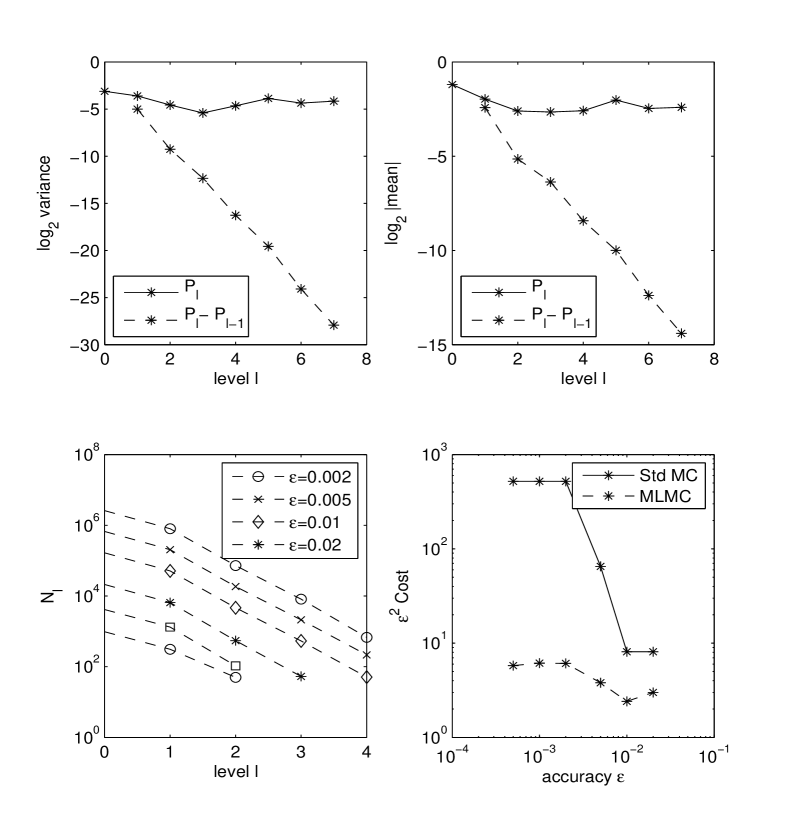

In practice, default is not monitored continuously but only at a discrete set of times, and for pricing often the simplifying assumption is made that default is only determined at the spread payment dates .

This can be incorporated as follows. In the time intervals , we solve (2) on a sufficiently large domain (e.g. ), and apply the following interface conditions at :

| (23) |

To maintain quadratic grid convergence in spite of the discontinuity introduced by (23), we choose the mesh such that a grid point coincides with the 0 boundary (e.g. by setting in the above example), and set the numerical solution after default monitoring to 0 for grid coordinates below 0 and to its previous value at 0, see e.g. [Pooley et al.(2003)].

It is seen in Fig. 4 that convergence is very similar to the previous case.

5 Conclusions

5.1 Complexity and cost

Here we discuss the computational complexity of the multilevel solution of the SPDE compared with the alternative use of the multilevel method for solving the SDEs which arise from directly simulating a large number of SDEs.

We have already explained that to achieve a r.m.s. accuracy of requires work when solving the SPDE by the standard Monte Carlo method, but the cost is using the multilevel method, provided Conjecture 2.1 is correct.

Consider now the alternative of using a finite number of particles (firms), , to estimate the tranche loss in the limit of an infinite number of particles (firms). In this case, empirical results suggest that there is an additional error (see also [Bujok & Reisinger(2012)]), and the proof of this convergence order is the subject of current research. Taking this to be the case, the optimal choice of to minimise the computational complexity to achieve an r.m.s. error of is . Using the standard Monte Carlo method, the optimal timestep is , and the optimal number of paths is , so the overall cost is . Using the multilevel method for the SDEs reduces the cost per company to , so the total cost is .

This complexity information is summarised in Table 1. There is also a practical implementation aspect to note. The computational cost per grid point in the finite difference approximation of the SPDE is minimal, requiring just three floating point multiply-add operations if equation (10) is re-cast as

with the coefficients computed once per timestep, for all .

If we let be the cost of generating all of the Gaussian random numbers for a single SPDE simulation, then the cost of the rest of the finite difference calculation with 20 points in (as used on the coarsest level of our multilevel calculations) is probably similar, giving a total cost of for each SPDE. On the other hand, each SDE needs its own Gaussian random numbers for the idiosyncratic risk, and so the cost of simulating each SDE is approximately , roughly half of the cost of the SPDEs on the coarsest level of approximation, giving a total cost of .

| Method / model | SDE | SPDE |

|---|---|---|

| Standard MC | ||

| Multilevel MC |

5.2 Further work

We have shown that stochastic finite differences combined with a multilevel simulation approach achieve optimal complexity for the computation of expected payoffs of an SPDE model. In the case of an absorbing boundary, the complexity estimate is a conjecture in so far it relies on the convergence order of the finite difference scheme, which does not follow from the Fourier analysis of the unbounded case. The matrix stability analysis in Appendix A could form part of a rigorous analysis if a Lax equivalence theorem could be proved. In the case of multiplicative white noise this is shown in [Lang(2010)]. One difficulty in the present case of an SPDE with stochastic drift is the loss of regularity towards the boundary, which may be accounted for by weighted Sobolev norms of the solution, but even then it is not clear that convergence of the functionals of interest follows.

There are several possible extensions of the present basic model as discussed in [Bujok & Reisinger(2012)], ranging from stochastic volatility and jump-diffusion to contagion models. The methods developed in this paper should be of use there also, building for example on multilevel versions of jump-adapted discretisations for jump-diffusion SDEs [Bruti-Liberati & Platen(2010), Xia & Giles(2012)].

References

- [Bain & Crisan(2009)] Bain, A. & Crisan, D. Fundamentals of Stochastic Filtering, Springer, 2009.

- [Barth et al.(2010)] Barth, A., Schwab, C., & Zollinger, N. Multi-level Monte Carlo finite element method for elliptic PDEs with stochastic coefficients, Num. Math., 119(1):123-161, 2010.

- [Benth & Koekebakker(2008)] Benth, F.E. & Koekebakker, S. Stochastic modeling of financial electricity contracts, Energy Economics, 30(3):1116–1157, 2008.

- [Black & Cox(1976)] Black, F. and Cox, J. Valuing corporate securities: some effects of bond indenture provision, J. Finance, 31:351–367, 1976.

- [Bruti-Liberati & Platen(2010)] Bruti-Liberati, N. & Platen, E. Numerical Solution of Stochastic Differential Equations with Jumps in Finance, Springer, 2010.

- [Buckwar & Sickenberger(2011)] Buckwar, E. & Sickenberger, T. A comparative linear mean-square stability analysis of Maruyama- and Milstein-type methods, Math. Comp. Sim., 81:1110–1127, 2011.

- [Bujok & Reisinger(2012)] Bujok, K. & Reisinger, C. Numerical Valuation of Basket Credit Derivatives in Structural Jump-Diffusion Models, J. Comp. Fin., to appear.

- [Bush et al.(2011)] Bush, N., Hambly, B., Haworth, H., Jin, L., & Reisinger, C. Stochastic evolution equations in portfolio credit modelling, SIAM Fin. Math., 2(1):627–664, 2011.

- [Carmona et al.(2009)] Carmona, R., Fouque, J.-P., & Vestal, D, Interacting particle systems for the computation of rare credit portfolio losses, Fin. Stoch., 13(4):613–633, 2009.

- [Carter & Giles(2007)] Carter, R. & Giles, M.B. Sharp error estimates for discretisations of the 1D convection/diffusion equation with Dirac initial data, IMA J. Num. Anal., 27(2):406–425, 2007.

- [Cliffe et al.(2011)] Cliffe, K.A., Giles, M.B., Scheichl, R., & Teckentrup, A.L. Multilevel Monte Carlo methods and applications to elliptic PDEs with random coefficients, Computing and Visualization in Science, 14(1):3–15, 2011.

- [Fouque et al.(2008)] Fouque, J., Wignall B., & Zhou, X. Modeling correlated defaults: first passage model under stochastic volatility. J. Comp. Fin., 11(3): 43–78, 2008.

- [Giles(2008a)] Giles, M.B. Multi-level Monte Carlo path simulation, Operations Research, 56(3):981–986, 2008.

- [Giles(2008b)] Giles, M.B. Improved multilevel Monte Carlo convergence using the Milstein scheme, pp. 343–358 in Monte Carlo and Quasi-Monte Carlo Methods 2006, editors Keller, A., Heinrich, S., & Niederreiter, H., Springer-Verlag, 2008.

- [Glasserman(2004)] Glasserman, P. Monte Carlo Methods in Financial Engineering, Springer, 2004.

- [Graubner(2008)] Graubner, S. Multi-level Monte Carlo Methoden für stochastische partielle Differentialgleichungen. Diplomarbeit, TU Darmstadt, 2008.

- [Gyöngy(1999)] Gyöngy, I. Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise II, Potential Anal., 11:1–37, 1999.

- [Gyöngy & Nualart(1997)] Gyöngy, I. & Nualart, D. Implicit schemes for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise, Potential Anal., 7:725–757, 1997.

- [Heath et al.(1992)] Heath, D., Jarrow, R., & Morton, A. Bond pricing and the term structure of interest rates: A new methodology for contingent claims valuation, Econometrica, 60(1):77–105, 1992.

- [Higham(2000)] Higham, D.J. Mean-square and asymptotic stability of the stochastic theta method, SIAM J. Num. Anal., 38(3):753–769, 2000.

- [Hull et al.(2005)] Hull, J., Predescu, M., & White, A. The valuation of correlation-dependent credit derivatives using a structural model, J. Credit Risk, 6(3):99–132, 2005.

- [Kloeden & Platen(1992)] Kloeden, P.E. & Platen, E. Numerical Solution of Stochastic Differential Equations, Springer, 1992.

- [Krylov(1994)] Krylov, N.V. A -theory of the Dirichlet problem for SPDEs in general smooth domains, Probab. Theory Relat. Fields, 98:389–421, 1994.

- [Kurtz & Xiong(1999)] Kurtz, T.G. & Xiong, J. Particle representations for a class of nonlinear SPDEs, Stoch. Proc. Appl., 83:103–126, 1999.

- [Lang(2010)] Lang, A. A Lax equivalence theorem for stochastic differential equations, J. Comp. Appl. Math., 234(12):3387–3396, 2010.

- [Merton(1974)] Merton, R., On the pricing of corporate debt: The risk structure of interest rates, J. Fin., 29:449–470, 1974.

- [Pooley et al.(2003)] Pooley, D.M., Vetzal, K.R., & Forsyth, P.A. Remedies for non-smooth payoffs in option pricing, J. Comp. Fin., 6:25–40, 2003.

- [Richtmyer & Morton(1967)] Richtmyer, R.D. & Morton, K.W. Difference Methods for Initial-Value Problems, Wiley-Interscience, 1967.

- [Roth(2002)] Roth, C. Difference methods for stochastic partial differential equations, Z. Angew. Math. Mech., 82(11–12):821–830, 2002.

- [Roth(2006)] Roth, C. A combination of finite difference and Wong-Zakai methods for hyperbolic stochastic partial differential equations, Stoch. Anal. Appl., 24(1):221–240, 2006.

- [Saito & Mitsui(1996)] Saito, Y. & Mitsui, T. Stability analysis of numerical schemes for stochastic differential equations, SIAM J. Num. Anal., 33(6):2254–2267, 1996.

- [Schönbucher(2003)] Schönbucher, P.J. Credit Derivatives Pricing Models, Wiley, 2003.

- [Walsh(2005)] Walsh, J.B. Finite element methods for parabolic stochastic PDEs, Potential Anal., 23:1–43, 2005.

- [Xia & Giles(2012)] Xia, Y. & Giles, M.B. Multilevel path simulation for jump-diffusion SDEs, in Monte Carlo and Quasi-Monte Carlo Methods 2010, editors Wozniakowski, H. & Plaskota, L., Springer-Verlag, 2012.

- [Zhou(2001)] Zhou, C., An analysis of default correlations and multiple defaults, The Review of Financial Studies, 14:555–576, 2001.

Appendix A Mean-square matrix stability analysis

If is the vector with elements then the finite difference equation can be expressed as

where is the identity matrix and and are the matrices corresponding to central first and second differences, which for are

From the recurrence relation we get

Noting that is anti-symmetric and is symmetric, and that

where corresponds to a central second difference with twice the usual span,

(with the end values of being chosen to correspond to and ), and and are each entirely zero apart from one corner element,

then after some lengthy algebra we get

where

and

It can be verified that the eigenvector of has elements for , and the associated eigenvalue is

where are the same functions as defined in the mean-square Fourier analysis. In addition, in the limit , , and therefore in this limit the Fourier stability condition

is also a sufficient condition for mean-square matrix stability.

Appendix B Regularity considerations

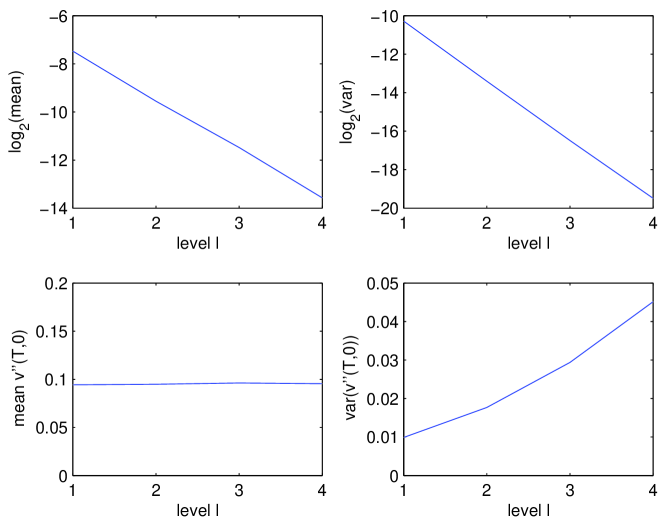

Figure 5 shows the convergence behaviour as the computational grid is refined. Level 0 has ; is reduced by factor 2 and by factor in moving to finer levels.

The top-left plot shows the convergence of , with notation as in Sections 3 and 4.2; the top-right plot shows the convergence of .

The bottom two plots show the behaviour of , which is estimated on each grid level using the standard second difference

The left plot indicates that the mean of this quantity is well behaved, but the right plot indicates a singular behaviour of its variance, with the value increasing rapidly with increased grid resolution.

This is in accordance with the result shown in [Krylov(1994)], that for the unique solution to the SPDE, is square integrable, but has a singularity at 0.