A proposal for impact-adjusted valuation: Critical leverage and execution risk

Abstract

The practice of valuation by marking-to-market with current trading prices is seriously flawed. Under leverage the problem is particularly dramatic: due to the concave form of market impact, selling always initially causes the expected leverage to increase. There is a critical leverage above which it is impossible to exit a portfolio without leverage going to infinity and bankruptcy becoming likely. Standard risk-management methods give no warning of this problem, which easily occurs for aggressively leveraged positions in illiquid markets. We propose an alternative accounting procedure based on the estimated market impact of liquidation that removes the illusion of profit. This should curb the leverage cycle and contribute to an enhanced stability of financial markets.

Another issue brought to the fore by the crisis is the need to better understand the determinants of liquidity in financial markets. The notion that financial assets can always be sold at prices close to their fundamental values is built into most economic analysis…

Chairman Ben Bernanke, Implications of the Financial Crisis for Economics, Princeton, September 24th, 2010.

1 Introduction: The danger of marginal prices

Mark-to-market or “fair value” accounting is standard industry practice. It consists in assigning a value to a position held in a financial instrument based on the current market price for this instrument or similar instruments. This is justified by the theory of efficient markets, which posits that at any given time market prices faithfully reflect all known information about the value of an asset. However, mark-to-market prices are only marginal prices, reflecting the value of selling an infinitesimal number of shares.

Practitioners are typically concerned with selling more than an infinitesimal number of shares, and are intuitively aware that this practice is flawed. Selling has market impact, which depresses the price by an amount that increases with the quantity sold. The first piece will be sold near the current price, but as more is liquidated prices may drop substantially. This somewhat paradoxically implies the value of 10 % of a company is less than 10 times the value of 1 % of that company. We take advantage of what has been learned recently about market impact to propose a method for impact-adjusted valuation that results in better risk control than mark-to-market valuation. This is in line with other recent proposals that valuation should be based on liquidation prices [1, 2].

Estimating liquidation prices requires a good understanding of market impact. In recent years there is been considerable progress in both theory and practice. For large trades there is growing evidence that market impact follows a universal functional form, see e.g. [3, 4, 5]. By “large” we mean trades that exceed the liquidity currently available in the order book; such trades need to be either broken up into pieces and executed incrementally or executed in a block market. Market impact is a concave function whose slope is infinite at the origin, which means that small trades have a disproportionally large impact.

The need for a better alternative to marking to market is most evident with leverage, i.e. when assets are purchased with borrowed money. Leverage amplifies market impact. As a leveraged position is sold, a process we refer to here as deleveraging, the price tends to drop due to market impact. Counter-intuitively, due to the concave form of market impact, when a leveraged position is gradually unwound the depression in prices due to impact overwhelms the decrease in position size, and leverage initially rises rather than falls. When impact is concave, this is not unusual – the expected leverage as a sale begins always goes up, regardless of initial leverage, liquidity or position size.

As more of the position is sold, provided the initial leverage and initial position are not too large, leverage eventually comes back down and the position retains some of its value upon liquidation. However, as we show here, if the initial leverage and initial position are too large, as the position is sold the leverage diverges, and the resulting liquidation value is less than zero, i.e. the debt to the creditors exceeds the resale value of the asset. The upshot is that under mark-to-market accounting a leveraged position that appears to be worth billions of dollars may predictably be worth less than nothing by the time it is liquidated. The above scenario assumes that positions are exited in an orderly fashion; under fire sale conditions or in very illiquid markets things are even worse.

From the point of view of a regulator or a risk manager this makes it clear that an alternative to mark-to-market accounting is badly needed. Neglecting impact allows huge positions on illiquid instruments to appear profitable when it is actually not the case. We propose such an alternative based on the known functional form of market impact, and propose that valuations should be based on the expected liquidation value of assets. Under leverage this avoids the problems outlined above. Whereas mark-to-market valuation only indicates problems with excessive leverage after they have occurred, our method makes them clear before positions are entered. Thus our method gives clear indications about potential problems as they are developing, and makes such situations easier to avoid. This could be extremely useful for damping the leverage cycle and coping with pro-cyclical behaviors [6, 7, 8, 9, 10].

In Section 2 we review the literature on market impact and present our proposal for impacted-adjusted valuation. In Section 3 we apply this to leverage and demonstrate that over-leveraging is a critical phenomenon, with a sharp transition where the problem of liquidating the position without bankruptcy becomes serious. In Section 4 we present some alternative formulas for estimating impact, run some numbers for typical assets, and show that this is not a serious problem for really liquid assets such as stocks, but it can occur at surprisingly low leverages for assets such as credit default swaps. Section 5 concludes, discussing the broader implications for the theory of market efficiency.

2 Market impact and liquidation accounting

Accounting based on liquidation prices requires a quantitative model of market impact. Because market impact is very noisy, and because it usually requires proprietary data to study empirically, a good picture of market impact has emerged only gradually in the literature. In this section we review what is known about market impact and present our proposal for impact-adjusted valuation.

2.1 The emerging quantitative model of market impact

Understanding the nature of market impact has now been the focus of a large number of empirical studies, both from academics and practitioners (for recent reviews, see [11, 12, 3, 4, 13, 14, 5]), and a consensus is beginning to emerge. Here we are particularly concerned with the liquidation of large positions, which must either be sold in a block market or broken into pieces and executed incrementally111 Our interest in the impact of a single large trade that must be executed in pieces is in contrast to the impact of a single small trade in the orderbook, or the impact of the average order flow, both of which have different functional forms, see [12, 5].. These empirical studies now make it clear that the market impact , defined as the expected shift in price from the price observed before a buy trade () or a sell trade () to the price at which the last share is executed, is a concave function of position size normalized by the trading volume . When liquidation occurs in normal conditions, i.e. at a reasonable pace that does not attempt to remove liquidity too quickly from the order book, the expected impact due to liquidating shares is

| (1) |

where is the daily volatility, is daily share transaction volume, and a numerical constant of order unity [5]. We say more about how these parameters should be estimated when this formula is used for regulatory purposes in the next section.

Note that we are defining the expected impact in terms of prices rather than log-prices. This is possible because for cases of interest the liquidation time is short enough for prices not to move significantly away from the initial price, and the impact itself is significantly less than the price itself, so that the difference between and is small and only has a minor effect on our conclusions. This means that the domain of validity for the formula requires that the impact not be too large, roughly less than .

The quantity above is the expected impact, in the sense that it is the average outcome of liquidating shares. This is superimposed on the background price fluctuations due to the rest of the market. For typical small values of allowing orderly execution, the realized market impact is very noisy, almost invisible to the naked eye. It is not uncommon that the realized impact is in the opposite direction of the average impact. The expected impact can be regarded either as the average impact or as a median price – of prices will be above it, and below it.

We want to emphasize that here we have defined impact as the shift in prices caused by the execution of given order. Whether the long-term impact has a permanent component that remains embedded in prices long after the trade occurs, and how large such a component might be, remain controversial. Fortunately these questions do not need to be addressed for our purposes here, although they are highly relevant to understand how market prices move and how potentially destabilising feedback loops can occur (see e.g [15]).

The earliest theory of market impact due to Kyle [16] predicted that expected impact should be linear. This was further supported by the work of Huberman and Stanzl [17], who argued that providing certain assumptions are met, such as lack of correlation in order flow, impact has to be linear in order to avoid arbitrage. However, more recent empirical studies have made it clear that these assumptions are not met [18, 19, 5], and the overwhelming empirical evidence that impact is concave has driven the development of alternative theories [20, 21, 22]. For example, Farmer et al. [23] have proposed a theory based on a strategic equilibrium between liquidity demanders and liquidity providers, in which uncertainty about on the part of liquidity providers dictates the functional form of the impact. Toth et al. [5], in contrast, derive a square root impact function within a stochastic order flow model. They impose that prices are diffusive, show that this implies a locally linear “latent order book”, and provide a proof-of-principle using a simple agent-based model. Both of these theories predict roughly square root impact, though with some differences.

Both empirical studies and theory make it clear that the square-root law for expected impact under orderly execution also holds at intermediate points. That is, after a quantity is executed, the average adverse price move is given by [14, 23, 5]:

| (2) |

We should stress that the formulae above for market impact hold only under normal conditions, when execution is slow enough for the order book to replenish between successive trades (on this point, see e.g. [24, 25, 11]). If the execution schedule is so aggressive that becomes comparable to , liquidity may dry up, in which case the parameters and can no longer be considered to be fixed, but themselves react to the trade, with an expected increase of the volatility and a decrease of the liquidity. Impact in such extreme conditions is expected to be much larger than the square-root formula above. The flash crash is a good example. In these cases the expected impact becomes less concave and it can become linear or even super-linear [22]. For the above impact formula to be valid, the execution time needs to be large enough that remains much smaller than ( is a typical upper limit). The execution time should not be too long either, otherwise impact is necessarily linear in : beyond some “memory time” of the market, trades must necessarily become independent and impact must be additive, see [5].

2.2 How should the impact parameters be estimated?

When impact is estimated for regulatory purposes, for stability reasons it is important that the parameters should be computed over a long time horizon. For example one can take an exponential moving average of and over past values. If and are not measured over relatively long time scales impact-adjusted valuation could lead to an unstable feedback loop. Imagine, for example, an exogeneous shock (like the Japanese tsunami in March 2011) that leads to a sudden increase of volatility. If is measured over short-time scales, the expected impact also increases. This would cause a larger discount on the asset valuation, which could cause a systemic effect in which risk managers unload the asset, leading to plummeting market prices and further panic. Similarly in a temporary liquidity crisis a sudden drop of could lead to a mechanical reduction in asset values. In order to avoid these destabilising effects, the window over which and are computed should be chosen to be long, perhaps 6 months, and exclude the very recent past – e.g. the last week of trading.

2.3 Impact-adjusted accounting

The establishment of a quantitative theory for expected impact makes it possible to do impact-adjusted accounting. Rather than using the mark-to-market price, which is the marginal price of an infinitesimal liquidation, we propose using the expected price under complete liquidation. For convenience we assume liquidation in equal sized increments of shares each, where is arbitrary but small222 In general it is possible that optimal liquidation might follow a different liquidation schedule. However, our feeling is that any gains from such a schedule are likely to be small, and in any case, empirical studies show that a uniform liquidation rate is a good approximation for the average investor [14].. The expected value of a position of shares in a given asset with mark-to-market price that is liquidated in pieces of shares each is

| (3) |

Providing is large, it is a good approximation to use the continuous limit where is infinitesimal, in which case this can be written

It is sometimes also useful to use the average valuation price .

3 The critical nature of leverage

When leverage is used it becomes particularly important to take impact into account and value assets based on their expected liquidation prices. Consider an asset manager taking on liabilities to hold shares of an asset with price . For simplicity we consider the case of a single asset. The leverage is given by the ratio of the value of the asset to the total equity,

| (5) |

Holding and constant, the leverage decreases when the price of the asset increases and vice versa when it decreases. Similarly, holding and constant, selling shares reduces leverage,

| (6) |

and vice versa for buying.

3.1 Deleveraging

Now we take into account market impact and consider the case of deleveraging, i.e. exiting a leveraged position. Selling pushes current trading prices down, which under mark-to-market accounting decreases the value of the remaining unsold shares. As we show, this generally overwhelms the effect of selling the shares, increasing the leverage even as the overall position is reduced. After shares have been sold the amount of cash raised to offset the liabilites is . Using the continuous approximation

| (7) |

where is the impact of selling the entire position, which can be large if the initial position is too big and/or the liquidity is too small. The leverage after shares have been sold is

| (8) |

where is the price after selling shares. Letting be the fraction of assets that have been sold and be the initial leverage before selling begins, this can be rewritten in the form

| (9) |

It is then easy to show that:

-

•

For small , , which is larger than for , that is, whenever any leverage is used. This means, rather paradoxically, that when selling a leveraged position, the expected leverage under mark-to-market accounting always initially increases.

-

•

If the leverage eventually reaches a maximum and decreases back to one for . The crossover point where the leverage drops below its starting value can be computed by solving Eq. (8) for with , which gives

(10) It is easy to show that whenever .

-

•

If the leverage diverges during liquidation. The leverage diverges when the value of the position is equal to the liability, i.e. . This occurs when the denominator of Eq. (9) becomes zero, which yields a cubic equation for the critical value . If then the asset manager goes bankrupt before being able to take his position to zero.

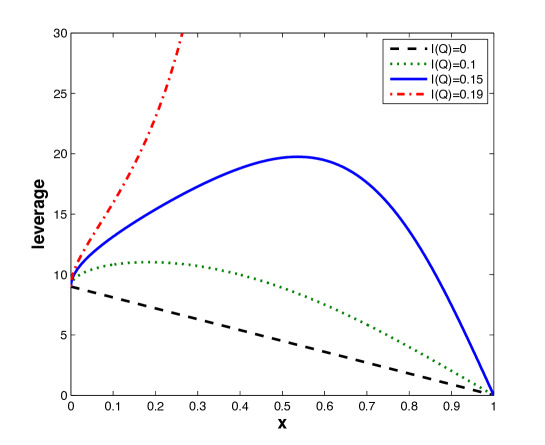

Three representative deleveraging trajectories are illustrated in Fig. 1, together with the trajectory obtained in absence of market impact. We assume a fixed starting mark-to-market leverage and show three cases corresponding to different values of the overall market impact parameter . For the two cases where the leverage is subcritical, i.e. with , the manager unwinds the position without bankruptcy. However, due to the rise in leverage during the course of liquidation, he may get in serious trouble with his prime broker along the way. For example, in the case where at its peak is more than twice its starting value.

The case where the leverage is allowed to become supercritical is a disaster. If , which for implies , the manager is trapped, and the likely outcome of attempting to deleverage is bankruptcy. (By bankruptcy we mean that the position ends up being worth less than the money borrowed to finance it, so that the manager ends up owing a debt for that position. )

3.2 Leverage under impact-adjusted prices

We now show how risk management is improved by impact-adjusted accounting. This is done by simply using the average impact-adjusted valuation price in the formula for leverage, i.e.

| (11) |

Here is the number of shares held at any given time along the way to entering position . We define the impact adjusted price for position as the liquidation price if buying were to stop and the current position were to be sold. Accordingly, when exiting a position we adopt the convention that the impact-adjusted price is based on complete liquidation of all shares, i.e. we do not allow for the possibility of pausing along the way333 The square root law for market impact is inherently related to the market’s memory [23, 5]. Once liquidation begins the market has a memory – the response of prices to each successive sale is smaller and smaller as gets bigger and bigger. An alternative definition of the impact-adjusted price while the position is being sold might be to assume a pause sufficiently long to break this memory, followed by subsequent liquidation of the remaining position . We have not adopted this because it requires an understanding of how impact decays in time, which we do not have, and in any case we do not believe this is necessary..

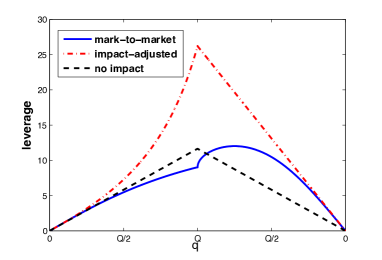

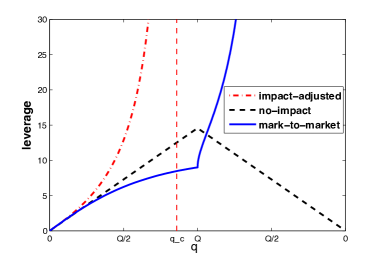

In figure 2 we show how the leverage behaves when a manager first steadily assumes a position and then steadily liquidates it. We compare three different notions of leverage:

-

•

No impact leverage is represented by the dashed black line. This is the leverage that would exist if the price remained constant (on average). It rises and falls linearly444 The reason for linearity is that when the price is constant the denominator in Eq. (5) remains constant. This is because changes in cash cancel changes in asset value. proportional to the position .

-

•

Mark-to-market leverage is represented by the solid blue line. While the position is building it rises more slowly than linearly. This is because as the position is building impact causes the price to increase, lowering leverage and partially offsetting the increasing position size. This is dangerous because it artificially overestimates profits and therefore depresses leverage. When the position is exited, in contrast, the expected leverage initially shoots up. In the subcritical case it eventually returns to zero, but in the super-critical case it diverges, indicating (too late) that the position is bankrupt.

-

•

Impact-adjusted leverage is represented by the dashed red line. It is always greater than either of the other two measures of leverage. It is particularly useful in the super-critical case – its rapid increase is a clear warning that a problem is developing, in contrast to the mark-to-market leverage. A sensible manager would thus easily avoid bankruptcy by buying less and avoiding the critical regime.

3.3 Taking noisy impact into account

So far we have focused our attention on the expected impact, which can either be viewed as the average impact or as a median trajectory. In this section we show how impact-adjusted accounting can be used to compute the probability of adverse price movements. This improves on standard measures that fail to take impact into account and may dramatically underestimate the probability of bankruptcy in situations where impact is large.

To illustrate this we estimate the probability of bankruptcy for positions of varying leverage. We make the simple assumption that the noisy component of impact is independent of the order being executed, and diffuses according to the volatility as the square root of time. Under the (admittedly crude) approximation that background price movements are normally distributed we model individual realizations of price trajectories as a discrete random walk with time varying drift. For convenience we measure the time in days. The evolution of the price during execution is given by

| (12) |

where is the price at time , is the size of the position at time , and is IID gaussian noise. The term is the additional increment of impact between day and day , with is the volume traded in a given day. The total time needed to off-load the position is .

With this choice for the stochastic process we ensure that in absence of noise the price follows the deterministic trajectory predicted by the expected market impact, and that the price in absence of market impact undergoes an unbiased discrete random walk. For better risk analysis it is of course possible to use more sophisticated models of the background noise, incorporating factors such as clustered volatility, jump diffusions, or heavy tails as desired. The simple model above is sufficient to illustrate the basic idea of how such risk analysis can be done.

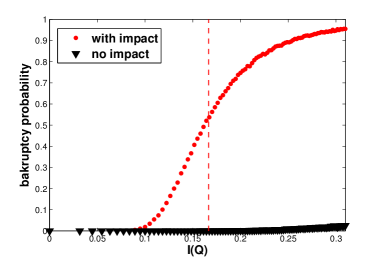

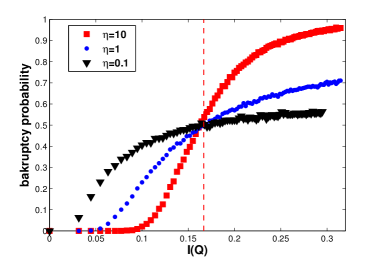

To assign probabilities for a given event, in this case bankruptcy, we simulate realizations of the noise process using Eq. (12), keeping small enough that the probability that the price becomes negative can be neglected. A typical result is shown in Fig. 3. Since the volatility of the final price scales as , whereas the average impact scales as , the sharpness of the transition is determined by their ratio . Using we can write , making it clear that is an aggressivity parameter, often called the participation rate, measuring the fraction of daily volume used for trading. In Fig. 3 we vary and while keeping constant.

The probabilities of bankruptcy are dramatically higher than they are without impact, and as expected, the transition is centered at the critical point , which is independent of the volatility. The transition is sharp for aggressive trading schedules () and is blurred as .

During liquidation it is possible for the position to temporarily become bankrupt and then recover. Whether or not a manager would be forced to default in such a situation will depend on her relationship with her creditors. Forcing bankruptcy if it occurs anywhere along the liquidation path slightly raises the probability of bankruptcy, depending on the time for execution.

4 Does leverage diverge in realistic situations?

We have shown the dangers of mark-to-market accounting for understanding leverage, but the skeptical reader may wonder whether such extreme situations actually occur in practice. In this section we plug in some typical numbers and show that for large positions in illiquid stocks such problems are not uncommon.

4.1 Impact and bid-ask spread

We have so far computed impact using the estimated volatility and volume. We now review results that connect these to the spread, which provide an alternative way to estimate the magnitude of liquidation effects, which might be more convenient in some circumstances.

It is now well established empirically that the volatility is made up of two different effects: the size of the bid-ask spread on the one hand, and the number of transactions per unit time on the other. For liquid markets the volatility on timescale can be written

| (13) |

where is a constant of order unity, that weakly depends on the market [26]. Suppose that the typical volume at the best prices is . If one assumes as before that the order is executed in increments of shares, the total number of transactions needed to liquidate shares is . Similarly the total volume in a time is . The above impact formula can therefore be rewritten as:555Note that the liquidation time drops out of the formula, which is one of the remarkable properties of the square-root impact law.

| (14) |

This expression highlights the micro-structure origin of liquidity. As is intuitively clear, it is the spread and the available volume that determine the impact cost of a trade. The quantities and should again be estimated using moving averages using market data or broker quotes for OTC/illiquid markets.

4.2 Some examples

Let us first give some orders of magnitude for stock markets. The daily volume of a typical stock is roughly of its market cap (see e.g. [27, 28]), while its volatility is of the order per day. Suppose the portfolio to be liquidated owns of the market cap of a given stock. Taking , the impact discount is

| (15) |

A hair-cut on the value of a portfolio of very liquid stocks is already quite large, and it is obviously much larger for less liquid/more volatile markets.

Let us now turn to the question of the critical leverage under mark-to-market accounting. From Section 3, the condition reads:

| (16) |

Substituting the two expressions for and rearranging gives

| (17) | |||||

| (18) |

To give a feeling for whether or not these conditions can be met, we present representative values for several different assets. For futures we assume , implying that it would take five days to trade out of the position with . For stocks we assume , which assuming the same participation rate implies a position that would take 50 trading days to unwind. Such positions might seem large, but they do occur for large funds; for instance, Warren Buffet was recently reported to have taken more than eight months to buy a share of IBM. The results are given in Table 1.

| Asset | |||||||

|---|---|---|---|---|---|---|---|

| BUND† | 0.4 % | 140 | 1.5 | 40 | 0.4% | 0.7% | 300 |

| SP500† | 1.6% | 150 | 2 | 10 | 1.6 % | 2.1 % | 100 |

| MSFT♢ | 2 % | 1.25 | 3.7 | 1 | 6.3 % | 3.2 % | 25 |

| AAPL♢ | 2.8 % | 0.5 | 1.7 | 0.1 | 8.9% | 2.9 % | 17 |

| KKR♡ | 2.5 % | 2♡ | 14 | 2.5♡ | 7.9% | 9.4 % | 16 |

| ClubMed♣ | 4.3 % | 1♣ | 45 | 11♣ | 13.5 % | 8.2 % | 11 |

| CDS♭ | – | – | 10 % | 10 | – | 20% | 7.5 |

We see that for liquid futures, such as the BUND or SP500, the critical leverage is large enough that the phenomenon we discuss here is unlikely to ever occur. As soon as we enter the world of equities, however, the situation looks quite different, whereas for OTC market the effect is certainly very real.

5 Conclusion

The above discussion underscores the need to value positions based on liquidation prices rather than mark-to-market prices. For small, unleveraged positions in liquid markets there is no problem, but as soon as any of these conditions are violated, the problem can become severe. As we have shown, standard valuations, which do nothing to take impact into account, can be wildly over-optimistic.

The solution that we have proposed accomplishes this goal by estimating liquidation prices based on recent advances in understanding market impact. The procedures that we suggest have the key virtue of being extremely easy to implement. They are based on quantities such as volatility, trading volume, or the spread, that are easy to measure. Risk estimates can be computed for the typical expected behavior or for the probability of a loss of a given magnitude – anything that can be done with standard risk measures can be easily replicated to take impact into account, with little additional effort.

The worst negative side-effects of mark-to-market valuations occur when leverage is used. As we have shown here, when liquidity is low leverage can become critical. By this we mean that as a position is being entered there is a critical value of the leverage above which it becomes very likely that liquidation will result in bankruptcy, i.e. liquidation value less than money owed to creditors. This does not require bad luck or unusual price fluctuations – it is a nearly mechanical consequence of using too much leverage.

Standard mark-to-market accounting gives no warning of this problem, in fact quite the opposite: Impact raises prices as a position is purchased, causing leverage to be underestimated. However, as a position is unwound the situation is reversed. The impact of unwinding causes leverage to rise, and if the initial leverage is critical, the leverage becomes infinite and the position is bankrupt. Under mark-to-market accounting this comes as a complete surprise. Under impact-adjusted accounting, in contrast, the warning is clear. As the critical point is approached the impact-adjusted leverage diverges, telling any sensible portfolio manager that it is time to stop buying.

The method of valuation that we propose here could potentially be used both by individual risk managers as well as by regulators. Had such procedures been in place in the past, we believe that many previous disasters could have been avoided. As demonstrated in the previous section, the values where leverage becomes critical are not unreasonable compared to those used before, such as the leverages of 50 - 100 used by LTCM in 1998, or 30-40 used by Lehman Brothers and other investment banks in 2008.

However, one should worry about other potentially destabilizing feedback loops that our impact-adjusted valuation could trigger. For example, in a crisis situation, spreads and volatilities increase while the liquidity of the market decreases, leading to a stronger discount on the asset valuation. But as was the case during the 2008 crisis, the write-down of the value of some books lead to further fire-sales, fueling more panic. So it is important to estimate the parameters entering the impact formula (volatility, spread and available volumes) using a slow moving average to avoid any over-reaction to temporary liquidity draughts.

A key point underlying our discussion here is that market impact occurs for both informed and uninformed trades. Empirical studies make it clear that temporary market impact occurs even if trades are made for reasons, such as hedging or liquidity, that have nothing to do with underlying fundamentals. This should not be surprising: Typically the counterparty has no way of knowing whether the opposite side of the trade is “informed” or “uninformed”666 To be clear, there are two kinds of impact. The first is due to correctly anticipating price movements. On the timescales for completing a trade this is typically small. The second is due to influencing prices. Our point is that if my counterparty is anonymous I have no way of knowing how informed she is, and therefore must react in a generic manner.

The failure of mark-to-market accounting can thus be viewed as a failure of the theory of efficient markets, or at the very least the need to take a liberal view of what it means. The fact that prices can change substantially due to random events that have nothing to do with fundamentals reflects a failure of prices to provide accurate valuations. Alternatively, one can take a generous view of what the word “accurate” means, as Fisher Black did when he famously said, “we might define an efficient market as one in which price is within a factor of 2 of value By this definition I think almost all markets are efficient almost all of the time. ‘Almost all’ means at least ” [29].

The failure of marginal prices as a useful means of valuation is part of an emerging view of markets as dynamic, endogenously driven and self-referential [30, 15], as suggested long ago by Keynes [31] and more recently by Soros [32]. For example, recent studies suggest that exogenous news play a minor role in explaining major price jumps [33], while self-referential feedback effects are strong [34]. Market prices are molded and shaped by trading, just as trading is molded and shaped by prices, with intricate and sometimes destabilising feedback. Because the liquidity of markets is so low, the impact of trades is essential to understand why prices move [11].

Acknowledgments

This work was supported by the National Science Foundation under grant 0965673, by the European Union Seventh Framework Programme FP7/2007-2013 under grant agreement CRISIS-ICT-2011-288501, and by the Sloan Foundation. JPB acknowledges important discussions with X. Brokmann, J. Kockelkoren and B. Toth.

References

- [1] C. Acerbi and G. Scandolo, “Liquidity risk theory and coherent measures of risk,” Quantitative Finance, vol. 08, pp. 681–692, 2008.

- [2] F. Caccioli, S. Still, M. Marsili, and I. Kondor, “Optimal liquidation strategies regularize portfolio selection,” the European Journal of Finance, 2011.

- [3] N. Torre, BARRA Market Impact Model Handbook. Berkeley: BARRA Inc., 1997.

- [4] R. Almgren, C. Thum, H. L. Hauptmann, and H. Li, “Direct estimation of equity market impact,” Risk, vol. 18, p. 5752, 2005.

- [5] B. Toth, Y. Lemperiere, C. Deremble, J. de Lataillade, J. Kockelkoren, and J.-P. Bouchaud, “Anomalous price impact and the critical nature of liquidity in financial markets,” Physical Review X, vol. 1, no. 2, p. 021006, 2011.

- [6] J. Geanakoplos, “Liquidity, default, and crashes: Endogenous contracts in general equilibrium,” in Advances in Economics and Econometrics: Theory and Applications, Eighth World Congress (M. Dewatripont, L. P. Hansen, and S. J. Turnovsky, eds.), vol. 2, pp. 170–205, Cambridge: Cambridge University Press, 2003.

- [7] T. Adrian and H. Shin, “Liquidity and leverage,” Tech. Rep. 328, Federal Reserve Bank of New York, May 2009.

- [8] M. K. Brunnermeier and L. H. Pedersen, “Market liquidity and funding liquidity,” Review Of Financial Studies, vol. 22, no. 6, pp. 2201–2238, 2009.

- [9] S. Thurner, G. Geanakoplos, and J. D. Farmer, “Leverage causes fat tailes and clustered volatility,” Quantitative Finance, vol. 12, no. 5, pp. 695–707, 2012.

- [10] J. Geanakoplos, “Solving the present crisis and managing the leverage cycle,” FRBNY Economic Policy Review, pp. 101–131, 2010.

- [11] J.-P. Bouchaud, J. D. Farmer, and F. Lillo, “How markets slowly digest changes in supply and demand,” in Handbook of Financial Markets: Dynamics and Evolution (T. Hens and K. Schenk-Hoppe, eds.), pp. 57–156, Elsevier, 2009.

- [12] J.-P. Bouchaud, Price Impact. John Wiley & Sons, Ltd, 2010.

- [13] R. Engle, R. Ferstenberg, and J. Russel, “Measuring and modeling execution cost and risk,” Tech. Rep. 08-09, University of Chicago, 2008.

- [14] E. Moro, L. G. Moyano, J. Vicente, A. Gerig, J. D. Farmer, G. Vaglica, F. Lillo, and R. Mantegna, “Market impact and trading protocols of hidden orders in stock markets,” Physical Review E., vol. 80, no. 6, p. 066102, 2009.

- [15] J.-P. Bouchaud, The Endogenous Dynamics of Markets: Price Impact, Feedback Loops and Instabilities. A. Berd (Risk Books, Incisive Media, London, 2011), 2010.

- [16] A. S. Kyle, “Continuous auctions and insider trading,” Econometrica, vol. 53, pp. 1315–1335, 1985.

- [17] G. Huberman and W. Stanzl, “Price manipulation and quasi-arbitrage,” Econometrica, vol. 72, no. 4, pp. 1247–1275, 2004.

- [18] J.-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart, “Fluctuations and response in financial markets: The subtle nature of “random” price changes,” Quantitative Finance, vol. 4, no. 2, pp. 176–190, 2004.

- [19] F. Lillo and J. D. Farmer, “The long memory of the efficient market,” Studies in Nonlinear Dynamics & Econometrics, vol. 8, no. 3, p. 1 33, 2004.

- [20] R. C. Grinold and R. N. Kahn, Active Portfolio Management. New York: The McGraw-Hill Companies, Inc., 1995.

- [21] X. Gabaix, P. Gopikrishnan, V. Plerou, and H. Stanley, “Institutional investors and stock market volatility,” Quarterly Journal of Economics, vol. 121, pp. 461–504, 2006.

- [22] J. Gatheral, “No-dynamic-arbitrage and market impact,” Quantitative Finance, vol. 10, p. 749, 2010.

- [23] J. D. Farmer, A. Gerig, F. Lillo, and H. Waelbroeck, “How efficiency shapes market impact,” tech. rep., 2011. http://arxiv.org/abs/1102.5457.

- [24] P. Weber and B. Rosenow, “Order book approach to price impact,” Quantitative Finance, vol. 5, pp. 357–364, 2005.

- [25] J.-P. Bouchaud, J. Kockelkoren, and M. Potters, “Random walks, liquidity molasses and critical response in financial markets,” Quantitative Finance, vol. 6, no. 2, pp. 115–123, 2006.

- [26] M. Wyart, J.-P. Bouchaud, J. Kockelkoren, M. Potters, and M. Vettorazzo, “Relation between bid-ask spread, impact and volatility in double auction markets,” Quantitative Finance, vol. 8, p. 41, 2008.

- [27] A. W. Lo and J. Wang, “Trading volume: Definitions, data analysis, and implications of portfolio theory,” Review of Financial Studies, vol. 13, pp. 257–300, 2000.

- [28] Z. Eisler and J. Kertesz, “Size matters: some stylized facts of the stock market revisited,” The European Physical Journal B, vol. 51, p. 145, 2006.

- [29] F. Black, “Noise,” Journal of Finance, vol. 41, no. 3, pp. 529–543, 1986.

- [30] D. Sornette, Endogenous versus exogenous origins of crises. S. Albeverio, V. Jentsch and H. Kantz, eds. (Springer, Heidelberg), 2005.

- [31] J. M. Keynes, The General Theory of Employment, Interest and Money. London: Macmillan, 1936.

- [32] G. Soros, The new Paradigm for financial markets: The Crash of 2008 and What it Means. PublicAffairs, 2009.

- [33] A. Joulin, A. Lefevre, D. Grunberg, and J.-P. Bouchaud, “Stock price jumps: news and volume play a minor role,” Wilmott Magazine, vol. September-October 46, p. 1, 2008.

- [34] V. Filimonov and D. Sornette, “Quantifying reflexivity in financial markets: towards a prediction of flash crashes,” tech. rep., 2012.