Equivalence of interest rate models and lattice gases

Abstract

We consider the class of short rate interest rate models for which the short rate is proportional to the exponential of a Gaussian Markov process in the terminal measure . These models include the Black, Derman, Toy and Black, Karasinski models in the terminal measure. We show that such interest rate models are equivalent with lattice gases with attractive two-body interaction . We consider in some detail the Black, Karasinski model with an Ornstein, Uhlenbeck process, and show that it is similar with a lattice gas model considered by Kac and Helfand, with attractive long-range two-body interactions . An explicit solution for the model is given as a sum over the states of the lattice gas, which is used to show that the model has a phase transition similar to that found previously in the Black, Derman, Toy model in the terminal measure.

pacs:

89.90.+n,47.11.Qr,05.70.-a,89.65.GhI Introduction

We consider in this paper the class of one-factor interest rate models with log-normally distributed short rate in the terminal measure. In these models the short rate is driven by one Gaussian Markov process . Such a process is defined by two conditions: i) for any set of times , the values have a joint normal distribution; ii) the evolution of for all depends only on . It can be shown that the most general process of this type is a time-changed Brownian motion, and includes the Ornstein-Uhlenbeck process as a particular case Doob .

This class of models includes the Black, Derman, Toy (BDT) BDT model, and the Black-Karasinski (BK) BK model, formulated in the terminal measure. The terminal measure is sometimes used in practice for these models AP , as opposed to the spot measure in which the models were originally formulated, due to the ease of calibration and simulation. Such models have been also proposed as approximations to the Libor market model LMM ; LMM1 , and as particular parametric realizations of Markov functional models 1 ; AP . A choice of measure amounts to a distributional assumption for the dynamical variables of the model. See BR for a readable introduction to the related concepts of martingales and measure for stochastic processes, and their relation to arbitrage pricing theory.

In this paper we show that these interest rate models are equivalent with lattice gases with attractive two-body interaction , placed in an external potential. The solution of the models can be expressed explicitly as an expression for the one-step zero coupon bond given by a sum over occupation numbers in the lattice gas. The expectation values required for the simulation of the model correspond to thermodynamical potentials in the lattice gas model.

We discuss in some detail the Black, Karasinski model with constant mean reversion , which is equivalent to a lattice gas with attractive two-body interaction . This is similar to a lattice gas model considered by Kac Kac , Kac, Uhlenbeck, Hemmer KUH and Kac, Helfand KacHelfand ; Helfand . This model generalizes the BDT model in the terminal measure, which corresponds to , and is equivalent with a Coulomb lattice gas with attractive two-body interactions. The latter model was studied in Ref. PhaseTransition , where it was shown that it displays discontinuous behaviour in volatility, which is similar to a phase transition in condensed matter physics EHS ; NG .

The equivalence with the lattice gas models suggests alternative simulation methods for these interest rate models, which express expectation values as sums over the states of the lattice gas. For small lattices this can be done by explicit summation over the lattice gas states, while for bigger lattices efficient numerical methods are available from statistical mechanics, such as Gibbs sampling and the Metropolis algorithm. We illustrate this approach by a numerical study of the BK model, which shows that the volatility phase transition observed in the BDT model in Ref. PhaseTransition persists also for this model.

II The interest rate model

We consider a short rate interest rate model in discrete time. The model is defined on a finite set of dates

| (1) |

For simplicity we will assume that are equally spaced, and denote with .

The fundamental dynamical quantities of the model are the zero coupon bonds . They are defined as the price at time of a payment of 1 made at time . They are stochastic quantities, and can be expressed as functions of an one-dimensional Markov process . For definiteness we consider in the following that is an Ornstein-Uhlenbeck process with zero mean reversion level

| (2) |

The mean and variance of conditional on are

| (3) | |||

| (4) |

The arguments of this paper can be easily extended to the more general case of an arbitrary Gaussian Markov process. By the Doob’s representation, the most general Gaussian Markov process can be represented as a time-modified Brownian motion Doob

| (5) |

with deterministic functions of time, and a Brownian motion.

We define the Libor rate (or simply Libor) for the period as

| (6) |

The model is defined by specifying the functional dependence of the Libor rate on the Markov driver

| (7) |

where are constants to be chosen such that the initial yield curve is correctly reproduced. This implies that the Libors are log-normally distributed in the terminal measure.

This model is similar with the Black-Karasinski model BDT ; BK , up to the difference that the latter is usually formulated in the risk-neutral measure, while in the model considered here the short rate is expressed in terms of defined in the terminal measure.

In the limit when the time step is taken to zero , this model becomes a continuous time short rate model, and the short rate satisfies the stochastic differential equation

| (8) |

with a function depending on and . We recognize this as the short rate evolution in the Black-Karasinski model BK .

II.1 Explicit solution of the model

According to the fundamental theorem of arbitrage pricing theory BR , the price of a financial asset expressed in units of a simpler asset (called numeraire) is a martingale. The mathematical statement of this result is expressed as

| (9) |

for any . This holds under fairly general assumptions, among which market completeness is the most important one. Speaking loosely this means that the model contains sufficiently many tradeable instruments to allow any possible payout to be reproduced as a combination thereof.

The choice of the numeraire is not unique, and any particular choice defines a measure for the stochastic process followed by the discounted asset prices . Two particular choices are most common in the context discussed here. The spot measure, or the risk-neutral measure, takes to be the money market account at time , while the terminal measure (or -forward measure) takes to be the zero coupon bond maturing at time . Once the condition (7) is imposed, different measure choices produce different observable distributional properties of the dynamical quantities of the model (rates and bonds), and thus effectively correspond to different models.

We will work in the terminal measure in the following. It is convenient to introduce the zero coupon bond prices divided by the numeraire , which will be denoted as . They are martingales in the terminal measure, and thus satisfy the condition (9), which reads explicitly

| (10) |

for all . The one-step discounted zero bond will play an important role in writing the analytical solution of this model. It satisfies a few conditions, following from the martingale condition (10). First, its expectation value is known in terms of the initial yield curve

| (11) |

It also satisfies the two conditions

| (12) | |||

| (13) |

The first condition (II.1) determines recursively the functional form of , starting with and proceeding backwards in time. This is given explicitly as a conditional expectation value

| (14) |

The second condition (13) can be used to determine also recursively, once has been determined, using the relation

| (15) |

For simplicity we denote the value of the Markov driver at time as , and its variance as .

We will state in the following the closed form of the solution of this model. The solution expresses the discounted one-step zero coupon bonds as a sum of terms containing factors. Writing the first few terms explicitly this is given by

| (16) | |||

We denoted here the weight , and the auto-covariance of the Markov process as

The general term in Eq. (II.1) containing factors of is given by a sum over all subsets of indices chosen from the indices .

In the limit of zero mean reversion , we have and , and the expression (II.1) simplifies drastically. In this limit all terms with the same number of factors have the same functional dependence of , and we recover the simple form obtained in Ref. PhaseTransition

| (18) |

where the coefficients are given by

| (19) |

where . In PhaseTransition these coefficients were determined recursively from a recursion relation, see Eq. (12) in Ref. PhaseTransition . Equation (19) gives an explicit solution of this recursion relation.

An important role is played in this model by the expectation values of the form

| (20) | |||

We enumerate in the following the applications of these expectation values with .

The expectation value of (corresponding to ) is constrained by the requirement that the initial yield curve is correctly reproduced, see (11).

| (21) | |||

The sum on the right-hand side is linear in and thus can be used to solve explicitly for this constant, provided that all with are already known. This is given in Eq. (15) in a form more convenient for practical calculation.

The expectation value appears in the calculation of the convexity-adjusted Libors Eq. (15), which can be written equivalently as

| (22) |

Finally, with determines the th moment of the Libor distribution in its natural (forward) measure according to the relation 2

| (23) | |||||

In the limit of zero mean-reversion the above expectation values are given by simple expressions PhaseTransition

| (24) |

For sufficiently small volatility , the expectation values given in Eq. (20) can be computed in an expansion of the small parameter , and keeping only the terms linear in this parameter is sufficient for most applications. In this approximation we have

| (25) |

The distribution of the Libors in their natural measure is approximatively log-normal and the ATM caplet volatility is

| (26) |

In the model with zero mean reversion , it was noted in Ref. PhaseTransition that for volatility above some critical value, the higher order terms in the expansion (20) become comparable to the linear terms of . The actual expansion parameter becomes and terms of all orders in become important. This leads to a discontinuity in the first derivative of the expectation value with respect to the volatility , which is similar to a phase transition in condensed matter physics EHS ; NG .

In the next section we express the expectation values (20) as averages over the grand canonical ensemble in an equivalent lattice gas model. This is used to show the existence of a phase transition also in this model, using a numerical simulation.

II.2 Proof

The result (II.1) can be proven using the following basic identity. For any numbers associated with the ordered sequence of times , the following expectation value with the Ornstein-Uhlenbeck process (2) is given by

| (27) | |||

where is the covariance of the process given above in Eq. (II.1). This is a slight generalization of an identity used in Ref. Kac ; KacHelfand to compute the partition function of a lattice gas with exponential interaction. It can be easily generalized to the case of a general Gaussian Markov process .

The discounted one-step bond is given by the conditional expectation (14). Expanding out the product yields terms with factors of , up to factors. There are terms containing such factors, and they are given by a sum over all subsets of indices out of the total of indices. A generic term has the form

| (28) | |||

where the expectation value was computed using the identity (27). This reproduces the terms containing factors of in Eq. (II.1). This completes the proof of (II.1).

III The lattice gas model

The interest rate model considered in the previous section is equivalent with a one-dimensional lattice gas with attractive long-range potential

| (29) |

The particles of the lattice gas are constrained to sit at positions , with . The sites of the lattice gas are labeled as . The sites are in one-to-one correspondence with the discrete set of simulation times of the interest rate model. At each site at most one particle can be present. We define the occupation number of the site . It can take values 0 or 1, depending on whether the site is vacant or occupied.

The Hamiltonian of the lattice gas model is

| (30) |

The two-body interaction is

| (31) |

and the single-site energies are

| (32) |

For the application to the interest rate model we are interested not only in the entire lattice system, but also in the subsystem of the lattice consisting of the sites , in total sites.

Assume that the subsystem of the lattice gas is placed in a position-dependent chemical potential

| (33) |

The grand partition function of the subsystem of the lattice gas with the Hamiltonian (30) and placed in the chemical potential (33) is given by

| (34) |

The sum over the number of particles runs from 0 to , the number of lattice sites in the subsystem . For each the sum runs over all configurations of occupied sites, which are subsets of sites of the sites in the system .

The correspondence of this lattice gas model with the interest rate model is realized through the following relation between the grand partition function and the expectation value (20)

| (35) |

provided that the parameters of the lattice gas are related to those of the interest rate model as

| (36) |

This system is similar to the one-dimensional gas considered by Kac Kac and by Kac, Uhlenbeck, Hemmer KUH . A lattice version of the gas model, very similar to that considered here, was examined by Kac and Helfand in Ref. KacHelfand ; Helfand . More precisely, the latter papers consider a lattice gas, where the particles occupy a lattice with nodes and lattice spacing 1, and interact by two-body attractive potentials . This model has a phase transition in the so-called van der Waals limit, which is obtained by first going to the thermodynamical limit of large , followed by the infinite range limit . In the van der Waals limit the lattice gas model has a liquid-gas phase transition with critical temperature , and the equation of state is given by the van der Waals equation supplemented by the equal area rule KUH .

At this point it may be useful to recall a few well-known facts about phase transitions in one-dimensional systems Mattis . Although a phase transition does not exist in a one-dimensional system with short range interactions LL , it is possible for such a system to have a phase transition provided that the interaction is sufficiently long range. Sufficient conditions which have to be satisfied by the interaction in order for a phase transition to exist in a one-dimensional system were given in Dyson1 . The papers KUH provided the first instance of phase transition in a one-dimensional system, and showed explicitly that this can occur in a system with long-range interactions. The results of KUH have been extended to more general interactions and higher dimensional systems in Ref. LP .

The zero mean-reversion limit of the interest rate model is the Black, Derman, Toy model in the terminal measure PhaseTransition , and is equivalent with a lattice gas model with attractive Coulomb two-body interactions, placed into an external potential. This can be seen by writing the covariance of the Markov driver for this case as

| (37) |

The first term describes an attractive linear interaction between the pair of particles at sites , while the second term can be represented as their interactions with the repulsive external field of a static charge placed at the site .

The one-dimensional gas with Coulomb interaction between several types of charges was studied, using methods very similar to those employed here, by Edwards and Lenard EdwardsLenard . Our Coulomb lattice gas is different from a usual Coulomb gas in that all particles attract each other. The thermodynamics of a one-dimensional system with linear attractive potentials was considered in Ref. Isihara , although periodic boundary conditions were imposed such that the resulting form of the interaction is different from that considered here. A connection between stochastic processes and the (two-dimensional) Coulomb gas was realized in a different context in Ref. Dyson .

The lattice gas with non-zero mean-reversion considered here differs from that studied by Kac and Helfand KacHelfand ; Helfand in several respects, due to the peculiarities of the interest rate model.

1. The presence of the factors requires the introduction of single-site energies associated with the lattice sites. These energies are different and thus the space homogeneity of the system is lost. This space homogeneity was crucial for the analytical solution of the model in the thermodynamical limit Kac ; KUH ; KacHelfand . A similar approach is unlikely in this case for this reason.

The single-site energies are constrained by the condition (22) such that the initial yield curve is correctly reproduced. According to this relation, depends on the properties of the subsystem of the lattice gas, and must be determined by a recursive procedure starting with the smallest subsystem and adding one lattice site at a time.

2. The two-body interaction in the lattice gas (29) contains a second exponential term , which is not present in Refs. KacHelfand ; Helfand . This is due to the fact that the expectation values (27) are conditional on , while KacHelfand ; Helfand integrate over . While the new term does not have the typical form of a two-body interaction, its inclusion does not present any problem of principle. Also, this term becomes vanishingly small if the subsystem is chosen such that , and the simple exponential Kac interaction is recovered in this limit.

The equivalence of these interest rate models with lattice gases suggests an alternative way of calibrating and simulating such models. The expectation values are usually AP ; 1 computed by evaluating the nested integrations over the values of the Markov driver at the simulation times, using numerical approaches such as finite difference or Monte Carlo methods. The results (II.1) and (20) suggest that the expectation values can be also computed as averages over the grand canonical ensemble in the lattice gas. For small lattices, this can be done by explicit summation over all possible occupation numbers ( configurations for a lattice with sites), while for larger lattices alternative methods familiar from statistical mechanics can be used, such as Gibbs sampling and the Metropolis-Hastings algorithm Metropolis ; Hastings .

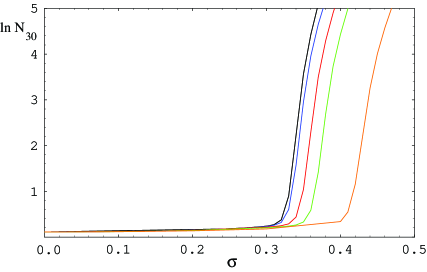

As an illustration of this approach, we show in Fig. 1 the results of a simulation of the BK model in the terminal measure performed by summing over the occupation numbers of the lattice gas. These plots show the multiplicative convexity adjustment for as function of for several values of the mean-reversion parameter . The simulation assumed quarterly time steps , for a total simulation time years. The forward yield curve is flat with . The curve is obtained using the recurrence method of PhaseTransition , and the remaining curves were obtained by computing using (20) by explicit summation over the states of the subsystem of the lattice gas.

These results show that the transition observed in Ref. PhaseTransition persists also in the model considered here. The mean-reversion allows one to control the range of the two-body interaction in the lattice gas. In the limit the lattice model particles attract each other with Coulomb potentials, while for the potential becomes exponential and is given in Eq. (29). In the limit the results of PhaseTransition are recovered: the convexity adjustment factor increases suddenly above the critical volatility . As the mean reversion is increased from zero, the transition persists, and the critical volatility increases from its value. The limit is well-behaved, as expected for a finite size lattice.

The study of the limit of this model presented in Ref. PhaseTransition showed that the phase transition is not visible under usual simulation methods used in practice for such interest rates models, such as finite difference or Monte Carlo methods. This is due to the fact that these methods effectively truncate the range of values of the Markovian driver to a few () multiples of . Such a truncation omits the contributions to the expectation values which are responsible for the phase transition. The alternative method proposed here offers a possible way to study the properties of these models, free of these limitations.

IV Conclusions

We presented in this paper the exact solution of a class of interest rates models with log-normally distributed short rates in the terminal measure. The solution is formulated naturally in terms of a lattice gas with sites corresponding to the simulation times of the model . At each site only one particle can be present, and the particles interact by attractive two-body potentials which are determined by the stochastic process followed by the short rate.

The analogy with the lattice gas models simplifies very much the simulation of these models, as many of the important expectation values in the interest rate model can be written in closed form as averages over the grand canonical ensemble in the corresponding lattice gas. The numerical evaluation of these averages is straightforward for small lattices (few simulation times in the interest rate model), while for larger lattices the number of configurations ( for a lattice with sites) becomes too large for direct evaluation, and approximation methods familiar from statistical mechanics may have to be used Metropolis ; Hastings .

We used the exact lattice gas solution to study numerically the Black, Karasinski model in the terminal measure with constant mean-reversion and volatility. This showed the appearance of a phase transition in the convexity adjustments of single-period interest rates, similar to that noted in the Black, Derman, Toy model in the terminal measure in Ref. PhaseTransition . This adds further support to the suggestion made in Ref. PhaseTransition that the presence of such a transition is generic for all interest rate models with log-normally distributed rates in the terminal measure. Although the present numerical study considered only the version of the model with constant parameters, the method can be extended without any major difficulty also to the more general case of time-dependent model parameters. This is in contrast to the method of the recursion relations used in PhaseTransition to solve the limit of the model with uniform volatility, which does not appear to be easily extended beyond this case due to the unmanageable complexity of the resulting expressions.

The equivalence of the interest rates models considered with interacting lattice gases shows that the former have a rich dynamics which has not been fully explored. Physical intuition about the lattice gas equivalent should give further insight into the dynamics of the interest rate models. In particular, one natural question is whether a phase transition similar to that studied in Ref. KUH is present also in the lattice gas considered here, and if it is observed also for a finite size lattice. The analog of the van der Waals limit for this case corresponds to simultaneously scaling the volatility as as the mean reversion is taken to zero . It would be interesting to see if the behaviour of the system in this limit has implications also for the practically relevant case of non-zero volatility.

Finally, it would be interesting to investigate whether the exact solution presented here can be extended also to other interest rate models, with more general distributional properties. Hopefully the lattice gas analogy will remain useful also for more general interest rate models.

References

- (1) J. L. Doob, Heuristic approach to the Kolmogorov-Smirnov theorems, Ann. Math. Stat. 20, 393 (1949).

- (2) F. Black, E. Derman and W. Toy, A one-factor model of interest rates and its application to Treasury bond options, Fin. Anal. J. 46(1), 33 (1990).

- (3) F. Black and W. Karasinski, Bond and option pricing when short rates are lognormal, Fin. Anal. J. 47(4), 52 (1991).

- (4) L. Andersen and V. Piterbarg, Interest rate modeling, Atlantic Financial Press, 2010.

- (5) A. Daniluk and D. Gatarek, A fully lognormal Libor market model, Risk, 2005

- (6) O. Kurbanmuradov, K. Sabelfeld and J. Schoenmakers, Lognormal approximations to Libor market models, J. Comp. Finance 6(1), 69, 2002.

- (7) J. B. Hunt and J. E. Kennedy, Financial derivatives in theory and practice, Wiley Series in Probability and Statistics, 2005.

- (8) M. Baxter and A. Rennie, Financial calculus: An introduction to derivative pricing, Cambridge University Press, 1996.

- (9) M. Kac, On the partition function of a one-dimensional gas, Phys. Fluids 2, 8 (1959).

- (10) M. Kac, G. E. Uhlenbeck, P. C. Hemmer, On the van der Waals Theory of the Vapor-Liquid Equilibrium. I. Discussion of a One-Dimensional Model, J. Math. Phys. 4, 216 (1963); ibid. 4, 229; ibid. 5, 60.

- (11) M. Kac and E. Helfand, Study of several lattice systems with long-range forces, J. Math. Phys. 4, 1078 (1963).

- (12) E. Helfand, Approach to a phase transition in a one-dimensional system, J. Math. Phys. 5, 127 (1964).

- (13) D. Pirjol, Phase transition in a log-normal Markov functional model, J. Math. Phys. 52, 013301 (2011), arXiv:1007.0691.

- (14) E. H. Stanley, Introduction to phase transitions and critical phenomena, Oxford University Press, 1987.

- (15) N. Goldenfeld, Lectures on phase transitions and the renormalization group, Frontiers in Physics, Addison-Wesley, 1992.

- (16) D. Pirjol, Nonanalytical behaviour in a log-normal Markov functional model, arXiv:1104.0322.

- (17) D. C. Mattis, The many-body problem: an encyclopedia of exactly solved models in one dimension, World Scientific, New York 1992.

- (18) L. Landau and E. M. Lifschitz, Statistical physics 1, Pergamon, Oxford, 1980.

- (19) F. Dyson, Existence of a phase transition in a one-dimensional Ising ferromagnet, Comm. Math. Phys. 12, 91 (1969); ibid. 21, 269 (1971).

- (20) J. L. Lebowitz and O. Penrose, Rigorous Treatment of the van der Waals-Maxwell Theory of the Liquid-Vapor Transition, J. Math. Phys. 7, 98 (1966).

- (21) S. F. Edwards and A. Lenard, Exact statistical mechanics of a one-dimensional system with Coulomb forces. II. The method of functional integration, J. Math. Phys. 3, 778 (1962).

- (22) A. Isihara, Consideration of a phase transition in a one-dimensional gas, Physica 64, 497 (1973).

- (23) F. Dyson, A Brownian motion model for the eigenvalues of a random matrix, J. Math. Phys. 3, 1191 (1962).

- (24) N. Metropolis et al., Equations of state calculations by fast computing machines, J. Chem. Phys. 21, 1087 (1953).

- (25) W. K. Hastings, Monte Carlo sampling methods using Markov chains and their applications, Biometrika 57, 97 (1970).