Shadow prices and well-posedness in the problem of optimal investment and consumption with transaction costs

Abstract.

We revisit the optimal investment and consumption model of Davis and Norman (1990) and Shreve and Soner (1994), following a shadow-price approach similar to that of Kallsen and Muhle-Karbe (2010). Making use of the completeness of the model without transaction costs, we reformulate and reduce the Hamilton-Jacobi-Bellman equation for this singular stochastic control problem to a non-standard free-boundary problem for a first-order ODE with an integral constraint. Having shown that the free boundary problem has a smooth solution, we use it to construct the solution of the original optimal investment/consumption problem in a self-contained manner and without any recourse to the dynamic programming principle. Furthermore, we provide an explicit characterization of model parameters for which the value function is finite.

1. Introduction

Ever since the seminal work of Merton (see [Mer69] and [Mer71]), the problem of dynamic optimal investment and consumption occupied a central role in mathematical finance and financial economics. Merton himself, together with many of the researchers that followed him, made the simplifying assumption of no market frictions: there are no transaction costs, borrowing and lending occur at the same interest rate, the assets can be bought and sold immediately in any quantity and at the same price (perfect liquidity), etc. Among those, transaction costs are (arguably) among the most important and (demonstrably) the most studied.

1.1. Existing work

The problem of optimal investment where transactions cost are present has received (and continues to receive) considerable attention. Following the early work of Constantinides and Magill [CM76], Davis and Norman [DN90] considered a risky asset driven by the geometric Brownian Motion for which proportional transactions costs are levied on each transaction. These authors formulated the optimal investment/consumption problem as a singular stochastic control problem, and approached it using the method of dynamic programming. Very early in the game it has been intuited, and later proved to varying degrees of rigor, that the optimal strategy has the following general form:

-

(1)

The investor should not trade at all as long as his/her holdings stay within the so-called “no-trade region” - a wedge around the Merton-proportion line.

-

(2)

Outside the “no-trade region’ , the investor should trade so as to reach the no-trading region as soon as possible, and, then, adjust the portfolio in a minimal way in order not to leave it ever after.

Such a strategy first appeared in [CM76] and was later made more precise in [DN90]. The analysis of [DN90] was subsequently complemented by that of Shreve and Soner [SS94] who removed various technical conditions, and clarified the key arguments using the technique of viscosity solutions. Still, even in [SS94], technical conditions needed to be imposed. Most notably, the analysis there assumes that the problem is well posed, i.e., that the value function is finite; no necessary and sufficient condition for this assumption, in terms of the parameters of the model, is given in [SS94]. In fact, to the best of our knowledge, the present paper provides the first such characterization.

More recently, Kallsen and Muhle Karbe [KMK10] approached the problem using the concept of a shadow price, first introduced by [JK95] and [LPS98]. Roughly speaking, the shadow-price approach amounts to comparing the problem with transaction costs to a family of similar problems, but without transaction costs, whose risky-asset prices lie between the bid and ask prices of the original model. The most unfavorable of these prices is expected to yield the same utility as the original problem where transaction costs are paid. As shown in [KMK10], this approach works quite well for the case of the logarithmic utility, which admits an explicit solution of the problem without transaction costs in a very general class of not-necessarily Markovian models. The fact that the logarithmic utility is the only member of the CRRA (power) family of utility functions with that property makes a direct extension of their techniques seem difficult to implement. Very recently, and in parallel with our work, partial results in this direction have been obtained by Herczegh and Prokaj [HP11] whose approach (and the intuition behind it) is based on the second-order nonlinear free-boundary HJB equation of [SS94], and applies only to a rather restrictive range of parameters.

1.2. Our contributions.

Our results apply to the model introduced [DN90] or [SS94], and deal with general power-utility functions and general values of the parameters. It is based on the shadow-price approach, but quite different in philosophy and execution from that of either [KMK10] or [HP11]. Our contributions can be divided into two groups:

Novel treatment and proofs of, as well as insights into the existing results. We provide a new and complete path to the solution to the optimal investment/consumption problem with transaction costs and power-type utilities. Our approach, based on the notion of the shadow price, is fully self-contained, does not rely on the dynamic programming principle and expresses all the features of the solution in terms of a solution to a single, constrained free-boundary problem for a one-dimensional first-order ODE. This way, it is able to distinguish between various parameter regimes which remained hidden under the more abstract approach of [DN90] and [SS94]. Interestingly, most of those regimes turn out to be “singular”, in the sense that our first-order ODE develops a singularity in the right-hand side. While we are able to treat them fully, those cases require a much more delicate and insightful analysis. The results of both [KMK10] and [HP11] apply only to the parameter regimes where no singularity is present.

New results. One of the advantages of our approach is that it allows us to give an explicit characterization of the set of model parameters for which the optimal investment and consumption problem with transaction costs is well posed. As already mentioned above, to the best of our knowledge, such a characterization is new, and not present in the literature.

Not only as another application, but also as an integral part of our proof, we furthermore prove that a shadow price exists whenever the problem is well-posed.

Finally, our techniques can be used to provide precise regularity information about all of the analytic ingredients, the value function being one of them. Somewhat surprisingly, we observe that in the singular case these are not always real-analytic, even when considered away from the free boundary.

1.3. The organization of the paper.

The set-up and the main results are presented in Section 2. In Section 3 we describe the intuition and some technical considerations leading to our non-standard free-boundary problem. In Section 4, we prove a verification-type result, i.e., show how to solve the singular control problem, assuming that a smooth-enough solution for the free-boundary equation is available. The proof of existence of such a smooth solution is the most involved part of the paper. In order to make our presentation easier to parse, we split this proof into two parts. Section 5 presents the main ideas of the proof, accompanied by graphical illustrations. The rigorous proofs follow in Section 6.

2. The Problem and the Main Results

2.1. The Market

We consider a model of a financial market in which the price process of the risky asset (form simplicity called the “stock”) is given by

Here, is a standard Brownian motion, and and are constants - parameters of the model. The information structure is given by the natural saturated filtration generated by . An economic agent starts with shares of the stock and units of an interestless bond and invests in the two securities dynamically. Transaction costs are not assumed away, and we model them as proportional to the size of the transaction. More precisely, they are determined by two constants and : one gets only for one share of the stock, but pays for it.

2.2. Solvency and Admissible Strategies

We assume that the agent’s initial position is strictly solvent, which means that it can be liquidated to a positive cash position. More precisely, we assume that where

| (2.1) |

The agent’s (consumption/trading) strategy is described by a triple of optional processes such that and are right-continuous and of finite variation and is nonnegative and locally integrable, a.s. The processes and have the meaning of the amount of cash held in the money market and the number of shares in the risky asset, respectively, while is the consumption rate.

In order to incorporate the potential initial jump we distinguish between the initial values and the values (after which the processes are right-continuous). This is quite typical for optimal investment/consumption strategies, both in frictional and frictionless markets, when the agent initially holds stocks, in addition to bonds. In this spirit, we always assume that

A strategy is said to be self-financing if

| (2.2) |

where is the pathwise minimal (Hahn-Jordan) decomposition of into a difference of two non-decreasing adapted, right-continuous processes, with possible jumps at time zero, as we assume that

The integrals used in (2.2) above, with respect to the (pathwise Stieltjes) measures and characterized by , and , for together with , and .

A self-financing strategy is called admissible if its position is always solvent, i.e., if

| (2.3) |

The set of all admissible strategies with and is denoted by , and the set of all such that for some and - the so-called financeable consumption processes - is denoted by .

2.3. Utility functions

For , we consider the utility function of the power (CRRA) type. It is defined for by

Our task is to analyze the optimal investment and consumption problem, with the value

| (2.4) |

and stands for the (constant) impatience rate. As part of the definition of , we posit that unless .

2.4. Consistent price processes

An Itô-process is called a consistent price (process) if , for all , a.s.; the set of all consistent prices is denoted by . For each consistent price , and a solvent pair of initial holdings such that , we define the set of (frictionless) admissible strategies , as we would in the standard frictionless market where the price-process is given by . More precisely, for to belong to it is necessary and sufficient that the following three conditions hold

-

(i)

and are progressively measurable, , a.s., for all ,

-

(ii)

and , and

-

(iii)

, for all , a.s,. and

(2.5)

The set of processes that appear as the third component of an element of will be denoted by , i.e.,

The elements of can be interpreted as the consumption processes financeable from the initial holding in the frictionless market modeled by . The intuition that the presence of transaction costs can only reduce the collection of financeable consumption processes can be formalized as in the following easy proposition.

Proposition 2.1.

, for each .

Proof.

For , let be such that . By the self-financing condition (2.2), the fact that and integration by parts (simplified by the fact that is continuous), we have

| (2.6) |

Therefore, by the admissibility criterion (2.3), we have

| (2.7) |

It remains to set and , and observe that (2.7) directly implies (2.5). Thus, . ∎

It will be important in the sequel to be able to check whether an element of belongs to . It happens, essentially, when a strategy that finances it “buys” only when and “sells” only when . A precise statement is given in the following proposition.

Proposition 2.2.

Given , let be such that there exist processes and such that

-

(1)

,

-

(2)

is a right-continuous process of finite variation, and

-

(3)

the Stieltjes measure on induced by is carried by and that induced by by .

Then, .

2.5. Shadow Problems

For each consistent price process , we define an auxiliary optimal-consumption problem - called the -problem, with the value , by

| (2.8) |

where is defined as in (2.4), and the inequality on the right is implied by Proposition 2.1. In words, each consistent price affords at least as good an investment opportunity as the original frictional market.

It is in the heart of our approach to show that the duality gap, in fact, closes, i.e., that the inequality in (2.8) becomes an equality; the worst-case shadow problem performs no better than frictional one.

Definition 2.3.

A consistent price is called a shadow price if .

The central idea of the present paper is to look for a shadow price as the minimizer of the right-hand side of (2.8) viewed as a stochastic control problem. More precisely, we turn our attention to a search for an optimizer in the shadow problem:

| (2.9) |

We start by tackling the shadow problem in a formal manner and deriving an analytic object (a free-boundary problem) related to its solution. Next, we show that this free-boundary problem indeed admits a solution and use it to construct the candidate shadow price. Finally, instead of showing that our candidate is indeed an optimizer for (2.9) and that , we use the following direct consequence of Proposition 2.2.

Proposition 2.4.

Remark 2.5.

The route we take towards the existence of a shadow price may appear to be somewhat circuitous. It is chosen so as to maximize the intuitive appeal of the method and minimize (already formidable) technical difficulties.

While the remainder of the paper is devoted to the implementation of the above idea, we anticipate its final results here, for the convenience of the reader. An important by-product of our analysis is the explicit characterization of those parameter values which result in a well-posed problem (the value function is finite). To the best of our knowledge, such a characterization is not present in the literature, and the finiteness of the value function is either assumed (as in [SS94]) or deduced from rather strong conditions (as in [KMK10]).

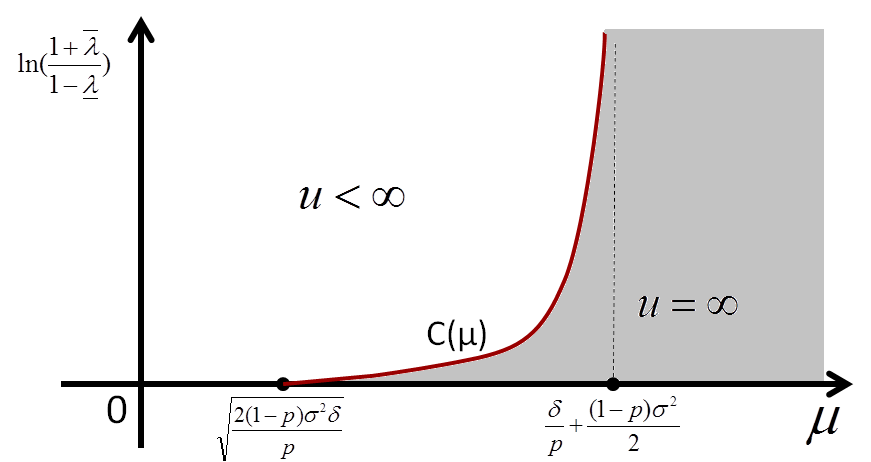

Theorem 2.6.

Given the environment parameters and the transaction costs , , the following statements are equivalent:

(1) The problem is well posed, i.e

whenever .

(2) The parameters of the model satisfy one

of the following three conditions:

- ,

- and ,

- , and

where the function is given by (6.8) in a closed form.

Remark 2.7.

For , the third condition in (2) above reduces to a well-known condition of Shreve and Soner. Indeed, the entire Section 12 in [SS94], culminating in Theorem 12.2, p. 677, is devoted to the well-posedness problem with two bonds (i.e, with ).

As demonstrated by our second main result, the shadow-price approach not only allows us to fully characterize the conditions under which a solution to the frictional optimal investment/consumption problem exists, but it also sheds light on its form and regularity.

Theorem 2.8.

Given the parameters and the transaction costs , , we assume that well-posedness conditions of Theorem 2.6 hold. Then

-

(1)

There exist constants with and a function such that

-

(a)

for , and satisfies the equation

(2.10) where

(2.11) -

(b)

the following boundary/integral conditions are satisfied:

(2.12) -

(c)

The function , defined by

(2.13) admits no zeros on .

-

(a)

- (2)

- (3)

Remark 2.9.

In (2.12), if ( is a singular point described in Section 5), then the condition can be violated. For this exceptional case, Proposition 4.2 is still valid: More precisely, in the part (2) of Proposition 4.2, we need to show that . If , in (4.3), the drift is positive and the volatility is zero, thus, we conclude that .

3. A heuristic derivation of a free-boundary problem

The purpose of the present section is to provide a heuristic derivation of a free-boundary problem for a one-dimensional first-order ODE which will later be used to construct a shadow process and the solution of our main problem. With the fully rigorous verification coming later, we often do not pay attention to integrability or measurability conditions and formally push through many steps in this section.

We start by splitting the shadow problem (2.9) according to the starting value of the process :

| (3.1) |

One can significantly simplify the analysis of the above problem by noting that, since each is a strictly positive Itô-process, we can always choose processes and such that

It pays to pass to the logarithmic scale, and introduce the process , whose dynamics is given by

| (3.2) |

on the natural domain . Here, , and the function is given by (2.11) for . This way, the family of consistent price processes is parametrized by the set

where is the set of all pairs of regular-enough processes such that the process , given by (3.2) and starting at , stays in the interval , a.s.

We note that the market modeled by is complete, and that, thanks to the absence of friction, the agent with the initial holdings will achieve the same utility as the one who immediately liquidates the position, i.e., the one with the initial wealth of . Therefore, the standard duality theory suggests that

| (3.3) |

where and are related as above and

| (3.4) |

Remark 3.1.

The Legendre-Fenchel transform of admits an explicit and simple expression in the case of a power utility. Indeed, we have

where . The parameter is the negative of the conjugate exponent of , i.e., (, for ) and this relationship will be assumed to hold throughout the paper without explicit mention.

Consequently, if we combine (3.1) and (3.3), we obtain the following equality:

| (3.5) |

The expression above is particularly convenient because it separates the shadow problem into a stochastic control problem over , and a (finite-dimensional) optimization problem over and , which can be solved separately.

3.1. A dimensional reduction

Thanks to homogeneity (-homogeneity for ) of the map , a dimensional reduction is possible in the inner control problem in (3.5). Indeed, with , we have

Hence,

| (3.6) |

where

In the heuristic spirit of the present section, it will be assumed that the processes of the form and are (true) martingales so that the definition of the stochastic exponential and the simple identity

| (3.7) |

can be used to simplify the expression for even further:

| (3.8) |

Here, the measure111One should rather call a cylindrical measure, but, given the heuristic nature of the present section, we do not pursue this distinction. is (locally) given by . By Girsanov’s theorem the process

| (3.9) |

is (locally) a -Brownian motion and the dynamics of the process can be conveniently written as

The expression inside the infimum in (3.8) involves a discounted running cost. Hence, it fits in the classical framework of optimal stochastic control, and a formal HJB-equation can be written down. We note that even though the process appears in the original expression for , the simplification in (3.8) allows us to drop it from the list of state variables and, thus, reduce the dimensionality of the problem. Indeed, the formal HJB has the following form:

| (3.10) |

where the functions and are defined in (2.11).

In order to fully characterize the optimization problem, we need to impose the boundary conditions at and to enforce the requirement that stay within the interval . These amount to turning off the diffusion completely and leaving only the drift in the appropriate (inward) direction when reaches the boundary. Thanks to the form of the function and the equation (3.10), as well as the expectation that be bounded on , we are led to the boundary condition

| (3.11) |

It will be shown in the following section that, in addition to the annihilation of the diffusion coefficient, (3.11) will ensure that the drift coefficient will indeed have the proper sign of at the boundary.

3.2. Shadow price as a strategy in a game

By interpreting the problem of shadow prices as a game, one can arrive to the two-point boundary problem (3.10), (3.11) without the use of duality.

Let denote the initial wealth of the investor who is not subject to transaction costs, for a fixed and . Finding a shadow price now amounts to the following:

-

(1)

given , solving the optimal investment problem for an investor with initial wealth i.e., maximizing the expected discounted utility

over (numbers of shares of and the rate of consumption).

-

(2)

minimizing the obtained value over , and

-

(3)

finally, further minimizing over

Up to the last minimization over , the above defines a stochastic game with the value

The corresponding Isaacs equation with a two dimensional state and the initial condition scales as

Consequently, it can be reduced to a one-dimensional equation for , with , which turns out to be exactly the boundary-value problem (3.10), (3.11). Once the game is solved, we can find a shadow price by simply minimizing the value over .

We believe that a similar approach - namely of rewriting the problem of optimal investment and consumption with transaction costs as a game, through the use of consistent prices - works well in more general situations, e.g., when multiple assets are present.

3.3. An order reduction

Finally, based on the fact that the equation (2.10) is autonomous, we introduce an order-reducing change of variable. With expected to be increasing and continuous on , we define the function , with and by . This transforms the equation (2.10) into

with (free) boundary conditions and The free boundaries and are expected to be positive.

4. Proof of the main theorem: verification

We start the proof of our main Theorem 2.8 with a verification argument which establishes the implication . After that, in Lemma 4.4 and Proposition 4.5, we show (3).

Let us assume, therefore, that a triplet , as in part (1) of Theorem 2.8, is given (and fixed for the remainder of the section), and that the function is defined as in (2.13). Let and be the formal optimizers of (2.10), i.e.,

| (4.1) |

Similarly, let be the compositions of the functions , , and of (2.11) with and . Using the explicit formulas above, one readily checks that function admits a Lipschitz extension to .

While the equation (2.10) can be written in a more explicit way - which will be used extensively later - for now we choose to keep its current variational form. We do note, however, the following useful property of the function :

Proposition 4.1.

For all with , we have

| (4.2) |

Proof.

The equation (4.2) follows either by direct computation (using the explicit formulas (4.1) for and above) or the appropriate version of the Envelope Theorem (see, e.g., Theorem 3.3, p. 475 in [GK02]), which states, loosely speaking, that we “pass the derivative inside the infimum” in the equation (2.10). ∎

4.1. Construction of the state processes

The family of processes , , defined in this section, will play the role of state processes in the construction of the shadow-price process below. Thanks to the Lipschitz property of the function , for each there exists a unique solution of the following reflected (Skorokhod-type) SDE

| (4.3) |

Here, is the “instantaneous inward reflection” term for the boundary , i.e., a continuous process of finite variation whose pathwise Hahn-Jordan decomposition satisfies

The reader is referred to [Sko61] for a more detailed discussion of various possible boundary behaviors of diffusions in a bounded interval, as well as the original existence and uniqueness result [Sko61, pp. 269-274]) for (4.3).

For , we define the function by and the process by . In relation to the heuristic discussion of Section 3, we note that plays the (formal) role of the inverse of the derivative . Moreover, the process has the following properties:

Proposition 4.2.

For , we have

-

(1)

, for all , a.s., and

-

(2)

and .

Proof.

Property (1) follows from the definition of the function and the assumption (c) of part of Theorem 2.8. For (2), Itô’s formula reveals the following dynamics of :

| (4.4) |

The identity (4.2) allows us to simplify the above expression to

Finally, since vanishes on the boundary, the singular term disappears and we obtain the second statement. ∎

4.2. A stochastic representation for the function

For notational convenience, we define

Proposition 4.3.

For , we have

| (4.5) |

Proof.

Using the equation (2.10), relation (4.2) and Itô’s formula, we can derive the following dynamics for the process :

where is given by (3.9) with . On the other hand, if we set and , we obtain that

Girsanov’s theorem (applicable thanks to the boundedness of ) implies that is a Brownian motion on , under the measure , defined by . Therefore,

where the boundedness of the integrands was used to do away with the stochastic integrals with respect to . The exponential identity (3.7) now implies that

| (4.6) |

For , we can use the fact that and are bounded to conclude that

These two limits can now easily be combined with (4.6) to yield (4.5).

4.3. The Shadow Market

For , we define the process and observe that, by Itô’s formula, it admits the following dynamics:

| (4.8) |

The goal of this subsection is to show that is a shadow price for the appropriate choice of the initial value . Note that is bounded away from , by the properties of .

Recall from subsection 2.5 that is the value of the optimal consumption problem in the (frictionless) financial market driven by for an agent with the initial holding in the bond, and in the stock (the -problem). The following lemma, which describes the optimal investment/consumption policy that achieves the maximum, will play a key role in the proof of the shadow property of the process . To simplify the notation, we introduce the following shortcuts:

Lemma 4.4.

For and the initial positions with , we have

| (4.9) |

Moreover, with the processes , and defined by

| (4.10) |

the optimal strategy for the -problem is given for by

| (4.11) |

Proof.

The standard complete-market duality theory (see, e.g., Theorem 9.11, p. 141 in [KS98]) implies that

where dual functional is as in (3.4). Furthermore, following the computations that lead to (3.6) in subsection 3.1, and using the representation of Proposition 4.3, we get (4.9)

Once the form of the value function has been determined, it is a routine computation derive the expressions for the optimal investment/consumption strategy. Indeed, let the processes be given by

| (4.12) |

and and as in the statement. Then, one readily checks that the triplet given by (4.11) is an optimal investment/consumption strategy.

Proposition 4.5.

Let be an admissible initial wealth, i.e., such that . For the function , given by , let the constant be defined by

Then is a shadow price.

Remark 4.6.

Proof.

The idea of the proof is to show that the triplet of Lemma 4.4 satisfies the conditions of Proposition 2.4. Since is the optimal consumption process, it will be enough to show that conditions (2) and (3) of Proposition 2.2 hold. The expression (4.11) implies that the processes and are continuous, except for a possible jump at .

Let us, first, deal with the jump at . The conditions (2) and (3) of Proposition 2.2 at translate into the following equality:

which, after (4.11) is used, becomes

| (4.13) |

If admits a solution , then clearly satisfies the equation (4.13). On the other hand, if , for all , then by continuity, either , for all or , for all . Focusing on the first possibility (with the second one being similar) we note that in this case , and so, if we pick , we get .

Next, we deal with the trajectories of the processes and for . It is a matter of a tedious but entirely straightforward computation (which can be somewhat simplified by passing to the logarithmic scale and using the identities (2.10) and (4.2)) to obtain the following dynamics:

| (4.14) |

Thanks to the fact that is a finite-variation process which decreases only when (i.e., ) and increases only when (i.e., ), the conditions (2) and (3) of Proposition 2.2 hold. ∎

5. Main ideas behind the proof of existence for the free-boundary problem

Having presented a verification argument in the previous section, we turn to the analysis of the (non-standard) free-boundary problem (2.10), (2.12). We start by remarking that that the equation (2.10) simplifies to the form

and where the second-order polynomials and are given by

The existence proof is based on a geometrically-flavored analysis of the equation (2.10), where the curves and , given by

| (5.1) |

play a prominent role. Many cases need to be considered, but we always proceed according to the following program:

-

(1)

First, we note that the boundary conditions amount to

-

(2)

Then, for a fixed we solve the ODE with initial condition and let it evolve to the right (if possible) until meeting again the curve at the -intercept . We therefore obtain a solution satisfying

If on some point along the way, only continuity is required there.

-

(3)

Finally, we vary the parameter to meet the integral condition

In order to give some intuition for the technicalities that follow, let us consider, for a moment, the ”degenerate” frictionless case . For fixed , and , the absence of transaction costs suggests a trivial solution with . In addition, the point is expected to have the highest possible -coordinate. Indeed, larger values of translate, as we saw in Lemma 4.4, to larger expected utilities. If such a point exists we call it the North pole, denote it by and its -coordinate by . In that case, furthermore, the curve decomposes into two parts (West of North) and (East of North) so that

Remark 5.1.

It turns out that:

-

(1)

The curve has a North pole, if and only if when .

-

(2)

When the North pole does exist:

-

(a)

if then and , and

-

(b)

if , we expect and

-

(a)

Before we go ahead, we note that the quantities and together with their geometric and arithmetic means play a special role. In fact, they deserve their own notation:

Another quantity that will play a role in the analysis is the Merton proportion

for an investor in a frictionless market, with the power utility. The last thing we need to do before we delve deeper into the analysis of various cases, is to introduce a suitable notation for the singular points, i.e., the points with . The explicit expressions for and above yield immediately that, in general, there are three() or two() solutions to in , two() or one() of which lie on the axis (and, therefore, do not count as singular points). The other one, denoted by is the unique singular point and will be quite important in our analysis. It has coordinates

which clearly degenerate for , ; in those cases, we set .

We are now ready to start differentiating between several (technically different) cases which are chosen, roughly, according to the following criteria: (1) whether the risk aversion is low () or high (), (2) whether the “North pole” exists, and (3) the sign of .

5.1. Low risk aversion

In this case investor is less risk averse than the log-investor, and it is the only case when well-posedness may fail. We further separate it into several sub-cases:

- Sub-case a): . For these particular values of parameters, the problem turns out to be well posed. The reason is simple: the value function of the frictionless version is finitely-valued here. The curve is (a portion of) an ellipse, and, as such, it obviously has a ”North pole”, in agreement with Remark 5.1.

Let denote the most right-ward point (East) and by its -coordinate, so that . Taking into account Remark 5.1 and the fact that is an ellipse, we expect to find a solution of the free boundary which satisfies As described in the outline of our program above, we “evolve” the solution from the initial point to the right, as long as we can. More precisely, we consider a maximal (with respect to the domain) -solution of the initial-value problem , with the property that , i.e., such that the curve stays on the inside of . It turns out that the domain of this solution is of the form , for some , and that the following statements hold:

-

(1)

The map is continuous and strictly decreasing on , and

-

(2)

while .

It follows immediately that a unique , such that solves the free-boundary problem (2.10),(2.12) exists. The major difficulty in the analysis is the fact that, for a given , the maximal solution may encounter the singularity on its trajectory (see Figure 3. below).

An important tool here turns out the be the so-called containment curve, i.e., a function such that

-

•

cannot hit before it hits , and

-

•

must hit before it hits .

It serves a two-fold purpose here. First, it restricts the possible values the function can take and makes sure that it either does not intersect the (singular) curve at all, or that it encounters it only at the point . The shaded area in Figure 2. below depicts the region of the plane the graph is restricted to lie in, under various conditions on the problem parameters. Second, when the singular point indeed happens to lie on the graph , a well-constructed containment curve provides crucial information about the behavior of in a neighborhood of . Whether or not falls on the graph

of depends on the values of the parameters. In particular, it depends on the relative position of the points , and . The lead actor turns out to be the Merton proportion , and the following three cases need to be distinguished (see Figure 2., below):

-

(1)

: and , with the relative positions of , and , further determined by the sign of

-

(2)

: Here, and for any .

-

(3)

: In this case, . Furthermore, if and only if .

Figure 2. , .

Figure 3. below shows some of the possible shapes the graph can take, under a representative choice of parameter regimes.

Figure 3.

A rigorous treatment of the first possibility () is given in the Proposition 6.7 in Section 6. The other cases are treated in the Proposition 6.9.

- Sub-case b): . The rate of return in this sub-case is so large, that the value function of the problem with transaction costs is infinite, independently of the size of the transaction costs and . A constructive argument is presented in Proposition 6.1. From the analytic point of view, this phenomenon is related to the non-existence of the solution to the free-boundary problem; an illustration of the reason why is given by the picture to the right (Figure 4). In a nutshell, we can find an asymptotically linearly increasing curve (the notation is chosen to fit that of Section 6) such that stays above it for all . Consequently, it is prevented from reaching the other branch of the curve and satisfying the free-boundary condition.

![[Uncaptioned image]](/html/1204.0305/assets/x8.png)

Figure 4.

- Sub-case c): . This is the most interesting sub-case from the point of view of well-posedness; whether the value function is finite or not is determined by the size of the transaction costs. The curve is a hyperbola, and has no North pole. The overall approach is the same as in sub-case a): we construct a maximal solution on an interval of the form , and show that the following two statements hold:

-

(1)

The map is continuous and strictly decreasing on , and

-

(2)

while ,

where an expression for is given in (6.8) below. The reader will note two major differences when the statements here are compared to the corresponding statements in the sub-case a). The first one is that now plays the role of . The second one is that the range of the integral is not the set of positive numbers anymore. It is an interval of the form , which makes the free-boundary problem solvable only for .

In addition to the fact that we still need to deal with the possible singularity along the graph of , difficulties of a different nature appear in this sub-case. First of all, due to the unboundedness of the regions separated by a hyperbola, it is not clear whether the maximal solution started at will ever hit the curve again. Indeed, this is certainly a possibility when , as depicted in Figure 4. However, we prove by contradiction that this is not the case for . The second new difficulty has to do with fact that is finite - a fact which prevents the existence of a solution to (2.10), (2.12).

Figure 5.

5.2. High risk aversion

In this case the problem is always well posed independently of the values of and ; indeed, the utility function is bounded from above. The curve is a hyperbola for and a parabola for , and it has a North-pole for any . is a hyperbola for , and for , it is a union of two straight lines, one of which is .

Compared to the case , no major new difficulties arise here, even though one still has to deal with the existence of singularities. For this reason we only present a figure (Figure 6. below) which illustrates different sub-cases that may arise. The formal treatment is analogous to that of Section 6.

6. An existence proof for the free-boundary problem (2.10), (2.12)

After a heuristic description of the major steps in the existence proof and the associated difficulties, we now proceed to give more rigorous, formal proofs. More precisely, the goal of this section is to present a proof of the part (1) of Theorem 2.8.

As already mentioned in the previous section, the proofs in the case , are very similar (but less involved) than those in the case so we skip them and refer the reader to the first author’s PhD dissertation [Cho12] for details. We also do not provide the proof of the part (c) of Theorem 2.8, as it can be obtained easily by an explicit computation.

Out first result states that problem is not well posed for large . As a consequence, we will be focusing on the case , in the sequel.

Proposition 6.1 (, .).

If and , then , for all .

Proof.

Without loss of generality, we consider the case , and construct a portfolio as follows:

One easily checks that it is admissible and that its expected utility is given by

6.1. Maximal inner solutions of .

As explained in the previous section, the main technique we employ in all of our existence proofs is the construction of a family of solutions to the equation , followed by the choice of the one that satisfies the appropriate integral condition. We, therefore, take some time here to define the appropriate notion of a solution to a singular ODE :

Definition 6.2.

Let be a convex interval in . We say that a function is a continuous solution of the equation if

-

(1)

is continuous on ,

-

(2)

is differentiable at and , for all

We note that any function with a single-point domain is considered a continuous solution according to the above definition.

Remembering that and using the notation of the previous section we remark that the level curves are ellipses or hyperbolas, and, as such, they are not graphs in general.

We therefore introduce the upper graph and the lower graph of the level curve by

and

for all , where

Moreover, for convenience, we include the case , where the minimal and maximal solutions of (instead of ) are considered; the domain is also defined. One easily checks that

Functions and allow us to define a subclass of solutions to :

Definition 6.3.

A continuous solution is said to be a maximal inner solution if

-

(1)

, for all , and

-

(2)

cannot be extended to an interval strictly larger than , without violating either (1) or the continuous-solution property.

Thanks to the local Lipschitz property of the function away from , the general theory of ordinary differential equations, namely the Peano Existence Theorem (see, for example Theorem I, p. 73 in [Wal98]), states that, starting from any point with and well defined, one can construct a maximal inner solution . This solution is necessarily real-analytic away from the curve .

We will be particularly interested in maximal inner solutions started at the top portion of , i.e., at the point , for . Not assuming uniqueness, we pick one such solution, denote it by , its domain by , and the right boundary point of by . To avoid the analysis of unnecessary cases, we assume from the start that , so that is strictly increasing in the neighborhood of and the singularity is not used as the initial value (a curious reader can peak ahead to Proposition 6.9, to see how the case can be handled.)

To rule out the possible encounters of a maximal inner solution with away from the singular point , we delve a bit deeper into the geometry of the right-hand side of our ODE. We start by a technical lemma which will help us construct the containment curve . Some more explicit expressions for the upper and lower curves and are going to be needed:

| (6.1) |

where are given by

| (6.2) |

The end-points of the domains of and , i.e., those for which are given by

We can also check that are solutions of and that are the solutions to . Finally, we note for future reference that holds, and that, for , the -coordinates of the north and east points () are given by and

Lemma 6.4.

For and , there exists constant such that

-

(1)

and .

-

(2)

for .

Proof.

(1) A direct calculation shows that, for , we have , as well as

By continuity, we can find such that

We can check that , which, in turn, implies

that . Since

and , we conclude that

(2) The result follows from and

.

∎

With the constant as in Lemma 6.4 above fixed, we define the containment curve and a containment region by

The significance of these objects is made clearer in the following proposition. The reader is invited to consult Figure 2 for an illustration.

Proposition 6.5.

For and , the following statements hold:

-

(1)

If , then , , and . For , .

-

(2)

is simply connected. It is bounded if and only if .

-

(3)

.

-

(4)

.

-

(5)

for .

-

(6)

. For such that , we have .

Proof.

(1) It is easily checked that, when all sets are seen as subsets of , that

Hence, it will be enough to show that following two claims hold:

Claim 1: For , we have . Since is a straight line on and is concave on , the easy-to-check facts that

imply that , on . Similarly, on .

Claim 2: , with equality if and only if . Several sub-cases are considered:

-

i)

: Then, and . Since is strictly concave and , the map is strictly increasing on . Thus, .

-

ii)

, : implies that .

-

iii)

, : .

-

iv)

, : implies .

(2) For the simple connectedness of , it is enough to show that is an interval. Given that , for all , it is enough to show that is an interval. With , similarly as in the proof of Claim 1, we observe that for , Therefore, . Since is strictly concave and is constant after , we have , to the right of the right-most point at which equals .

Since is strictly concave and is constant after , boundedness of is equivalent to the boundedness of the domain , of and . The set is, in turn, bounded, if and only if .

(3) The statement follows from definitions of and , and the fact that is the unique singular point.

(4) We only need to observe that from (1).

(5) The result follows from (3),(4) and the definition of .

(6) -smoothness of follows easily from the construction. With as in (2) above, we have

For , by Lemma 6.4, we have

For , , but the condition implies that

With the result of Proposition 6.5 in hand, we can say more about the shape of the function and its domain . In particular, we show that the graph stays at a positive distance from any point of , except, maybe, . Remember that if .

Proposition 6.6.

For such that , we have

-

(1)

.

-

(2)

.

-

(3)

is a closed interval of the form , for some . If and , then .

Proof.

(1) Suppose that it is not true. Then, there exists such that and . Since for close enough, we have . Combine this with , we deduce that and . So, and . Using this, we can calculate , which contradict to the fact that for close enough.

(2) Noting that , we assume that there exists a point with . With denoting the infimum of all such points, we observe immediately that and . If, additionally, , we can use the continuity of to conclude that and . By using (1), we can exclude the case , otherwise, should be , which contradicts to the choice of . Then, since , we reach a contradiction with part (6) of Lemma 6.5:

In the case , we have and, by the definition of the point and the domain , there exists , such that . Consequently, we have for some , and we observe that , because is a decreasing function of near . Now we reach a contradiction as in the case :

where can be showed by part (6) of Lemma 6.5.

(3) We first observe that the initial value lies on the graph of the function which is strictly increasing in the neighborhood of . Therefore, any extension of to the left of would cross and exit the set . So, left end-point of the domain should be .

To deal with the right end-point of , we note that noe of the following must occur: 1) explodes, 2) cossed, or 3) is hit. The first possibility is easily ruled out by the observation that no explosion can happen without crossing the curve , first. The second possibility is severely limited by (2) above; indeed, with part (1) of Proposition 6.5, . It is clear now that, in the right end-point limit , the function hits , provided . For and , clearly exists, and, so, . Furthermore, since . In case and , we also conclude that , by observing that for and . ∎

6.2. The sub-case

We focus on the case in this subsection. The curve is now an ellipse and it admits a north pole with the -coordinate . By part (1) of Proposition 6.5 and (2) of Proposition 6.6, we have the following dichotomy, valid for all .

-

(1)

For , , and

-

(2)

For , if and only if .

We start with the first possibility which avoids the singularity altogether.

Proposition 6.7 (, , ).

Proof.

By part (2) of Proposition 6.5, is bounded and in . is a consequence of part (3) of Proposition 6.6. Since , smoothness of follows from the general theory (Peano’s theorem). Moreover, the existence of the initial value , with the desired properties, is a direct consequence of the listed properties of , by way of the intermediate value theorem. We, therefore, focus on (6.3) in the remainder of the proof, which is broken into several claims. The proof of each claim is placed directly after the corresponding statement.

Claim 1: If , then . This follows from part (1) of Proposition 6.6.

Claim 2: The map is continuous. For this, we use the implicit-function theorem and the continuity of with respect to the initial data (see, e.g., Theorem VI., p 145 in [Wal98]). To be able to use the implicit-function theorem, it will be enough to observe that, is not tangent to (or ) at , which is a consequence of and Claim 1. above.

Claim 3: The map is continuous. It suffices to use the dominated convergence theorem. Its conditions are met, since (by Proposition 6.5, part (5)).

Claim 4: . The joint continuity of at and the fact that , imply that there exists such that

We define and remind the reader that for each , so that . Hence, we can pick such that , for .

For any given , if it so happens that for , then Proposition 6.5, part (4), implies that on . Therefore,

which is contradiction. We conclude that intersects on , for each .

Using the fact that on , we conclude that on . By Proposition 6.5, part (4) and the fact that for small , we have that on . Therefore,

Claim 5: . We start with the inequality , which implies that . Thus, by Proposition 6.5, part (5), we have

Before we move on to the case , we need a few facts about a specific, singular, ODE.

Lemma 6.8.

Given , consider the ODE

| (6.4) |

where are continuous functions, with . Then, the following statements hold:

Proof.

Elementary transformations can be used to show that for any solution of (6.4) defined on , there exist constants and such that

We first note that . So, to satisfy the condition , the only possibility is . Then, the L’Hospital’s rule implies that

and we immediately conclude (1) and (2).

As far as (3) is concerned, since , for any , the limiting behavior is independent of . Moreover, another use of the L’Hospital’s rule implies that , as , for each .

It remains to show (4), and, for this, we start by computing the derivative at of . Like above, we use the L’Hospital rule and the explicit expression for :

Similarly, , and, so . To establish that , we first use the L’Hospital rule to compute , so that, using the equation (6.4) for , we can immediately deduce that . ∎

Proposition 6.9 (, , ).

Remark 6.10.

(1) The parameter regime treated in Proposition 6.9 above leads to a truly singular behavior in the ODE (2.10). Indeed, the maximal continuous solution passes through the singular point , at which the right-hand side is not well-defined. It turns out that the continuity of the solution, coupled with the particular form (2.10) of the equation, forces higher regularity (we push the proof up to ) on the solution. The related equation (6.4) of Lemma 6.8 provides a very good model for the situation. Therein, uniqueness fails on one side of the equation (and general existence on the other), but the equation itself forces a smooth passage of any solution through the origin. It follows immediately, that, even though high regularity can be achieved at the singularity, the solution will never be real analytic there, except, maybe, for one particular value of . This is a general feature of singular ODE with a rational right-hand sides. Consider, for example, the simplest case which admits as a solution the textbook example of a function which is not real analytic.

(2) For large-enough , the value of such that solves (2.10), (2.12), will fall below , and an interesting phenomenon will occur. Namely, the right free boundary will stop depending on or . Indeed, the passage through the singularity simply “erases” the memory of the initial condition in . In financial terms, the right boundary of the no-trade region will be stop depending on the transaction costs, while the left boundary will continue to open up as the transaction costs increase.

Proof.

We will only prove (1) here; (2) can be proved by the same methods used in the proof of c) below.

For both (1) and (2), follows easily.

a) By Proposition 6.5, part (1), . So, if , the statement

can be proved by using the argument from the proof of

Proposition 6.7, mutatis mutandis.

b) The existence of the limit from the statement is established in a matter similar to that used to prove the continuity of the map in Claim 2. in the proof of Proposition 6.7. The existence of the limit follows from a standard argument involving a weak formulation and the dominated convergence theorem. Finally, by part (2) of Proposition 6.6 and , we conclude that is defined and continuous on , with .

c) As in the proof of Proposition 6.7, does not hit either or on . Hence, we must have ; moreover since the curves and coalesce at , the limit exists and equals to . In particular, we have and .

For , part b) above guarantees that a continuous solution with a domain of the form , with , exists. Therefore, by maximality, a maximal inner solution , with exists (in other words, , for all ).

Our next task is to upgrade the regularity of from to , where, clearly, we can focus on a neighborhood of the point : we need to show that that exist and are continuous at . The argument is divided in several claims, whose proofs follow the respective statements.

Claim 1: does not admit a local minimum on . Suppose, to the contrary, that it does. Then, there exists and a point such that

For , parts (3) and (4) of Proposition 6.5 imply that

| (6.6) |

We focus on the case , with the other one - when - being similar. By (6.6), we have ; moreover, since , we get , on . This leads to the following contradiction:

Claim 2: and decreases around . We observe that for , , and , and conclude that is differentiable at and . By the Claim 1., exist. So, using the mean value theorem, we obtain and conclude that .

Given an in a small-enough neighborhood of , the concavity of implies that

The mean value theorem can now be used to conclude that there exist , arbitrarily close to , with such that

Finally, if we combine the obtained results with those of Claim 1., we can conclude that decreases near .

Claim 3: The second derivative of exists at and

| (6.7) |

The proof is based on an explicit computation where the easy-to-check fact that our ODE admits the form

is used. We begin with the equality

By L’Hospital’s rule, as , the right-hand side above converges to

which, in turn, evaluates to the half of the right-hand side of (6.7).

Having computed a second-order quotient of differences for at , we could use the concavity of at (established in Claim 2. above) to conclude that is twice differentiable there. We opt to use a short, self-contained argument, instead, where denotes the right-hand side of (6.7). For small enough , we have

If we fix and choose , we obtain

from which the claim follows immediately.

Claim 4: For convenience, we change variables as follows

With respect to the new coordinate system, we have , and ; we need to show that . This follows, however, directly from Lemma 6.8, as we obtain the ODE (6.4) if we differentiate the equality , and pass to the new coordinates. The coefficient functions and admit a rather messy but explicit form which can be used to establish their continuity. Indeed, it turns out that and can be represented as continuous transformations of functions of , and , which are, themselves, continuous. Similarly, the condition imposed in Lemma 6.8 is satisfied because one can use the aforementioned explicit expression to conclude that ∎

6.3. The sub-case .

This sub-case is, perhaps the most challenging of all, as it combines the existence of a singularity with a possible failure of the well-posedness of the value function.

For let be the (ordered) solutions of the quadratic equation , where , and are as in (6.2). The analysis in the sequel centers around the constants and , given by

| (6.8) |

Lemma 6.11.

Assume that and . Then

-

(1)

is the smallest solution to . Moreover is nonnegative and if and only if .

-

(2)

is bounded if and unbounded otherwise.

-

(3)

For , .

-

(4)

For , we have

-

(5)

There exists a constant such that for and we have

-

(6)

is well-defined and nonnegative. Moreover, if and only if .

Proof.

(1) It follows by direct computation.

(2) It is easily checked that the leading coefficient of (seen as a polynomial in ) is positive. Therefore, for . Since is linear in and its values at are positive, for . Thus, the expression inside the square root in (6.1) is positive for and , which, in turn, implies that for , is unbounded.

Similarly, since for small enough , we conclude that the domain of is bounded. Part (4) of Proposition 6.5, implies that is a bounded set for any sufficiently small . We conclude that is bounded for .

(3) From the definition of we get

We already checked that for . Also, for , since . Thus, for . Furthermore,

| (6.9) |

We can now conclude that the left-hand side of (6.9) is positive on , since the function is concave and its values at are positive. It follows immediately that for .

(4) This can be shown by the direct computation.

(5) A straightforward (but somewhat tedious) calculation yields that , as , uniformly in . So, by (3), we can choose such that for some and all , . Also, we can check that there exists a constant such that for and we have

whence the first inequality in the statement of (5) follows. The second one is obtained in a similar manner.

(6) We first observe that and for . Then, the statement follows from the integrability of on and the fact that , which is, in turn, implied by (4) and (5) above. ∎

Remark 6.12.

In our current parameter range (, ), the level curve is a hyperbola and the curve is an ellipse for large-enough values of . In fact, is the smallest value of such that is a hyperbola (and, therefore, unbounded).

For , the Merton proportion cannot take the value , so we only consider the cases and in the following proposition:

Proposition 6.13 (, ).

Assuming that and , we have the following statements:

-

(1)

If , then , for each .

-

(2)

If then if and only if .

In both cases, . Moreover, for , we have

| (6.10) |

where is given by (6.8).

Proof.

The parts of statements (1) and (2) involving singularities are proved similarly to parallel statements in Proposition 6.9. We show that for , with the case being quite similar. Proceeding by contradiction, we suppose that , for some . Then, just like in the proof of Proposition 6.9, we can show that does not admit a local minimum on . Thus, there exists such that . From Proposition 6.11, part (2), we learn that , whereas from part (3) we conclude that there exists such that . Since for large enough , we can use part (4) of Proposition 6.11, to obtain a contradiction

with the fact that the inequality implies that , for large .

It remains to prove (6.10). The main idea is to intersect the solution with the (unbounded) level curve . If the two points of intersection are denoted by (the intersection is on ) and (intersection on ), with (see Figure 8), then the integral in (6.10) is split into three integrals on the intervals , and . The first and the last integrals are then computed using the change of variable , while the limit of the middle integral is shown to be zero.

![[Uncaptioned image]](/html/1204.0305/assets/x13.png)

Figure 8. and

We start this program by observing that the region is unbounded (see Proposition 6.11 (2)), and, hence, so is the region . Also, we observe that for . We conclude from there that intersects the region

Therefore, .

Since doesn’t admit a local minimum on , is uniquely defined and strictly increases on and strictly decreases on . Consequently, there exists a pair with and such that

Let be the inverse function of on , so that

where the last equality can be obtained by differentiating the middle one. A change of variables yields

| (6.11) |

where the existence of the limit and its value are obtained using parts (4) and (5) of Proposition 6.11, together with the fact that . In particular, part (5) of Proposition 6.11 allows us to apply the dominated convergence theorem. Similarly, we have

| (6.12) |

It remains to show that as . By Proposition 6.11 (parts (3) and (4)), there exist and such that , for . Moreover, part (2) of the same proposition guarantees the existence of a constant such that

Then, for and , and, so, for , we have

where the first equality follows by direct computation, the second one by the fact that and , and the final inequality from the choice of . Hence,

The remaining task in the proof of Theorem 2.6 is to show that the problem is not well posed, whenever .

Proposition 6.14.

Assume that and . If , where is defined in (6.8), then , i.e., the problem is not well posed.

Proof.

Without loss of generality, we assume that ; indeed, it is enough to scale (the initial value of) the stock price by , otherwise.

For , the function in Proposition 6.13 corresponds to the value function under the transaction costs and such that , where . More precisely, Lemma 4.4 in Section 4 above yields that

| (6.13) |

where is the optimal utility for the initial position , under the transaction costs and . The strict increase of and the decrease of , imply that is strictly decreasing, wherever it is defined. It now easily follows that

which, together with (6.10) and the representation (6.13), yields that . Since, clearly, is decreasing in , this amounts to saying that

Remark 6.15.

The map is strictly decreasing in general, not just under the parameters restricted by the hypothesis of Proposition 6.14. The same argument, as the one given in the proof of Proposition 6.14, applies. In particular, this fact can be used to show that the free-boundary problem (2.10), (2.12) has a unique solution for all values of the transaction costs, as long as .

It is, perhaps, interesting to note that the authors are unable to come up with a purely analytic argument for the monotonicity of . The crucial step in the proof of Proposition 6.14 above is to relate the value of to the original control problem, and then argue by using the natural monotonicity properties of the control problem itself, rather than the analytic description (2.10) only.

References

- [Cho12] Jinhyuk Choi, A shadow-price approach to the problem of optimal investment/consumption with proportional transaction costs and utilities of power type, Ph.D. thesis, The University of Texas at Austin, 2012.

- [CM76] G. M. Constantinides and M. J. P. Magill, Portfolio selection with transactions costs, Journal of Economic Theory 13 (1976), 245–263.

- [DN90] M. H. A. Davis and A. R. Norman, Portfolio selection with transaction costs, Math. Oper. Res. 15 (1990), no. 4, 676–713.

- [GK02] Victor Ginsburgh and Michiel Keyzer, The structure of applied general equilibrium models, The MIT Press, 2 2002.

- [HP11] A. Herczegh and V. Prokaj, Shadow price in the power utility case, preprint, http://arxiv.org/abs/1112.4385, 2011.

- [JK95] Elyes Jouini and Hédi Kallal, Martingales and arbitrage in securities markets with transaction costs, J. Econom. Theory 66 (1995), no. 1, 178–197.

- [KMK10] J. Kallsen and J. Muhle-Karbe, On using shadow prices in portfolio optimization with transaction costs, Ann. Appl. Probab. 20 (2010), no. 4, 1341–1358.

- [KS98] Ioannis Karatzas and Steven E. Shreve, Methods of mathematical finance, Applications of Mathematics (New York), vol. 39, Springer-Verlag, New York, 1998.

- [LPS98] Damien Lamberton, Huyên Pham, and Martin Schweizer, Local risk-minimization under transaction costs, Math. Oper. Res. 23 (1998), no. 3, 585–612.

- [Mer69] R. C. Merton, Lifetime portfolio selection under uncertainty: the continuous-time case, Rev. Econom. Statist. (1969), 247–257.

- [Mer71] by same author, Optimum consumption and portfolio rules in a continuous-time model, J. Economic Theory (1971), 373–413.

- [Sko61] A. V. Skorohod, Stochastic equations for diffusion processes with a boundary, Teor. Verojatnost. i Primenen. 6 (1961), 287–298.

- [SS94] S. E. Shreve and H. M. Soner, Optimal investment and consumption with transaction costs, Ann. Appl. Probab. 4 (1994), no. 3, 609–692.

- [Wal98] Wolfgang Walter, Ordinary differential equations, Graduate Texts in Mathematics, vol. 182, Springer-Verlag, New York, 1998, Translated from the sixth German (1996) edition by Russell Thompson, Readings in Mathematics.