Quantifying causal influences

Abstract

Many methods for causal inference generate directed acyclic graphs (DAGs) that formalize causal relations between variables. Given the joint distribution on all these variables, the DAG contains all information about how intervening on one variable changes the distribution of the other variables. However, quantifying the causal influence of one variable on another one remains a nontrivial question.

Here we propose a set of natural, intuitive postulates that a measure of causal strength should satisfy. We then introduce a communication scenario, where edges in a DAG play the role of channels that can be locally corrupted by interventions. Causal strength is then the relative entropy distance between the old and the new distribution.

Many other measures of causal strength have been proposed, including average causal effect, transfer entropy, directed information, and information flow. We explain how they fail to satisfy the postulates on simple DAGs of nodes. Finally, we investigate the behavior of our measure on time-series, supporting our claims with experiments on simulated data.

doi:

10.1214/13-AOS1145keywords:

[class=AMS]keywords:

, , and

1 Introduction

Inferring causal relations is among the most important scientific goals since causality, as opposed to mere statistical dependencies, provides the basis for reasonable human decisions. During the past decade, it has become popular to phrase causal relations in directed acyclic graphs (DAGs) Pearl00 with random variables (formalizing statistical quantities after repeated observations) as nodes and causal influences as arrows.

We briefly explain this formal setting. Here and throughout the paper, we assume causal sufficiency, that is, there are no hidden variables that influence more than one of the observed variables. Let be a causal DAG with nodes where means that influences “directly” in the sense that intervening on changes the distribution of even if all other variables are held constant (also by interventions). To simplify notation, we will mostly assume the to be discrete. denotes the probability mass function of the joint distribution . According to the Causal Markov Condition Spirtes , Pearl00 , which we take for granted in this paper, every node is conditionally independent of its nondescendants, given its parents with respect to the causal DAG . If denotes the set of parent variables of (i.e., its direct causes) in , the joint probability thus factorizes Lauritzen1996 into

| (1) |

where denotes the values of . By slightly abusing the notion of conditional probabilities, we assume that is also defined for those with . In other words, we know how the causal mechanisms act on potential combinations of values of the parents that never occur. Note that this assumption has implications because such causal conditionals cannot be learned from observational data even if the causal DAG is known.

Given this formalism, why define causal strength? After all, the DAG together with the causal conditionals contain the complete causal information: one can easily compute how the joint distribution changes when an external intervention sets some of the variables to specific values Pearl00 . However, describing causal relations in nature with a DAG always requires first deciding how detailed the description should be. Depending on the desired precision, one may want to account for some weak causal links or not. Thus, an objective measure distinguishing weak arrows from strong ones is required.

1.1 Related work

We discuss some definitions of causal strength that are either known or just come up as straightforward ideas.

Average causal effect: Following Pearl00 , denotes the distribution of when is set to the value [it will be introduced more formally in equation (6)]. Note that it only coincides with the usual conditional distribution if the statistical dependence between and is due to a direct influence of on , with no confounding common cause. If all are binary variables, causal strength can then be quantified by the Average Causal Effect Holland , Pearl00

If a real-valued variable is affected by a binary variable , one considers the shift of the mean of that is caused by switching from to . Formally, one considers the difference Northcott

This measure only accounts for the linear aspect of an interaction since it does not reflect whether changes higher order moments of the distribution of .

Analysis of Variance (ANOVA): Let be caused by . The variance of can formally be split into the average of the variances of , given with , and the variance of the expectations of , given :

| (2) |

In the common scenario of drug testing experiments, for instance, the first term in equation (2) is given by the variability of within a group of equal treatments (i.e., fixed ), while the second one describes how much the means of vary between different treatments. It is tempting to say that the latter describes the part of the total variation of that is caused by the variation of , but this is conceptually wrong for nonlinear influences and if there are statistical dependencies between and the other parents of Lewontin , Northcott .

For linear structural equations,

and additionally assuming to be independent of the other parents of , the second term is given by , which indeed describes the amount by which the variance of decreases when is set to a fixed value by intervention. In this sense,

| (3) |

is indeed the fraction of the variance of that is caused by . By rescaling all such that , we have . Then, the square of the structure coefficients itself can be seen as a simple measure for causal strength.

(Conditional) Mutual information: The information of on or vice versa is given by cover

The information of on or vice versa if is given is defined by cover

| (4) |

There are situations where these expressions (with describing some background condition) can indeed be interpreted as measuring the strength of the arrow . An essential part of this paper describes the conditions where this makes sense and how to replace the expressions with other information-theoretic ones when it does not.

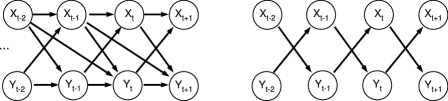

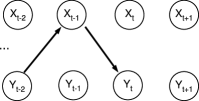

Granger causality/Transfer entropy/Directed information: Quantifyingcausal influence between time series [e.g. between and ] is special because one is interested in quantifying the effect of all on all . If we represent the causal relations by a DAG where every time instant defines a separate pair of variables, then we ask for the strength of a set of arrows. If and are considered as instances of the variables , we leave the regime of i.i.d. sampling.

Measuring the reduction of uncertainty in one variable after knowing another is also a key idea in several related methods for quantifying causal strength in time series. Granger causality in its original formulation uses reduction of variance Granger1969 . Nonlinear information-theoretic extensions in the same spirit are transfer entropy Schreiber and directed information Massey . Both are essentially based on conditional mutual information, where each variable in (4) is replaced with an appropriate set of variables.

Information flow: Since the above measures quantify dependencies rather than causality, several authors have defined causal strength by replacing the observed probability distribution with distributions that arise after interventions (computed via the causal DAG). AyKrakauer defined Information Flow via an operation, “source exclusion”, which removes the influence of a variable in a network. AyInfoFlow defined a different notion of Information Flow explicitly via Pearl’s -calculus. Both measures are close to ours in spirit and in fact the version in AyKrakauer coincides with ours when quantifying the strength of a single arrow. However, both do not satisfy our postulates.

Mediation analysis: Pearlindirect , Avin , Robins explore how to separate the influence of on into parts that can be attributed to specific paths by “blocking” other paths. Consider, for instance, the case where influences directly and indirectly via . To test its direct influence, one changes from some “reference” value to an “active” value while keeping the distribution of that either corresponds to the reference value or to the natural distribution . A natural distinction between a reference state and an active state occurs, for instance, in drug testing scenario where taking the drug means switching from reference to active. In contrast, our goal is not to study the impact of one specific switching from to . Instead, we want to construct a measure that quantifies the direct effect of the variable on , while treating all possible values of in the same way. Nevertheless, there are interesting relation between these approaches and ours that we briefly discuss at the end of Section 4.2.

2 Postulates for causal strength

Let us first discuss the properties we expect a measure of causal strength to have. The key idea is that causal strength is supposed to measure the impact of an intervention that removes the respective arrows. We present five properties that we consider reasonable. Let denote the strength of the arrows in set . By slightly overloading notation, we write instead of .

[P0.]

Causal Markov condition: If , then the joint distribution satisfies the Markov condition with respect to the DAG obtained by removing the arrows in .

Mutual information: If the true causal DAG reads , then

Locality: The strength of only depends on (1) how depends on and its other parents, and (2) the joint distribution of all parents of . Formally, knowing and is sufficient to compute . For strictly positive densities, this is equivalent to knowing .

Quantitative causal Markov condition: If there is an arrow from to , then the causal influence of on is greater than or equal to the conditional mutual information between and given all the other parents of . Formally

Heredity: If the causal influence of a set of arrows is zero, then the causal influence of all its subsets (in particular, individual arrows) is also zero.

Note that we do not claim that every reasonable measure of causal strength should satisfy these postulates, but we now explain why we consider them natural and show that the postulates make sense for simple DAGs.

P0: If the purpose of our measure of causal strength is to quantify relevance of arrows, then removing a set of arrows with zero strength must make no difference. If, for instance, , removing should not yield a DAG that is ruled out by the causal Markov condition.

We should emphasize that can be nonzero even if consists of arrows each individually having zero strength.

P1: The mutual information actually measures the strength of statistical dependencies. Since all these dependencies are generated by the influence of on (and not by a common cause or influencing ), it makes sense to measure causal strength by strength of dependencies. Note that mutual information also quantifies the variability in that is due to the variability in , see also Section .4.

Mutual information versus channel capacity. Given the premise that causal strength should be an information-like quantity, a natural alternative to mutual information is the capacity of the information channel , that is, the maximum over all values of mutual information for all input distributions of when keeping the conditional .

While mutual information quantifies the observable dependencies, channel capacity quantifies the strength of the strongest dependencies that can be generated using the information channel . In this sense, quantifies the factual causal influence, while channel capacity measures the potential influence. Channel capacity also accounts for the impact of setting to values that rarely or never occur in the observations. However, this sensitivity regarding effects of rare inputs can certainly be a problem for estimating the effect from sparse data. We therefore prefer mutual information as it better assesses the extent to which frequently observed changes in influence .

P2: Locality implies that we can ignore causes of when computing , unless they are at the same time direct causes of . Likewise, other effects of are irrelevant. Moreover, it does not matter how the dependencies between the parents are generated (which parent influences which one or whether they are effects of a common cause), we only need to know their joint distribution with .

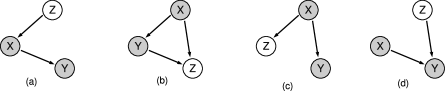

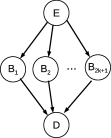

Violations of locality have paradoxical implications. Assume, for example, variable would be relevant in DAG 1(a). Then, would depend on the mechanism that generates the distribution of , while we are actually concerned with the information flowing from to instead of that flowing to from other nodes. Likewise, [see DAGs 1(b) and 1(c)] it is irrelevant whether and have further effects.

P3: To justify the name of this postulate, observe that the restriction of P0 to the single arrow case is equivalent to

To see this, we use the ordered Markov condition Pearl00 , Theorem 1.2.6, which is known to be equivalent to the Markov condition mentioned in the Introduction. It states that every node is conditionally independent of its predecessors (according to some ordering consistent with the DAG), given its parents. If denotes the predecessors of for some ordering that is consistent with and , the ordered Markov condition for holds iff

| (5) |

since the conditions for all other nodes remain the same as in . Due to the semi-graphoid axioms (weak union and contraction rule Pearl00 ), (5) is equivalent to

Since the condition on the left is guaranteed by the Markov condition on , the Markov condition on is equivalent to .

In words, the arrow is the only reason for the conditional dependence to be nonzero, hence it is natural to postulate that its strength cannot be smaller than the dependence that it generates. Section 4.3 explains why we should not postulate equality.

P4: The postulate provides a compatibility condition: if a set of arrows has zero causal influence, and so can be eliminated without affecting the causal DAG, then the same should hold for all subsets of that set. We refer to this as the heredity property by analogy with matroid theory, where heredity implies that every subset of an independent set is independent.

3 Problems of known definitions

Our definition of causal strength is presented in Section 4. This section discusses problems with alternate measures of causal strength.

3.1 ACE and ANOVA

The first two measures are ruled out by P0. Consider a relation between three binary variables , where with and being unbiased and independent. Then changing has no influence on the statistics of . Likewise, knowing does not reduce the variance of . To satisfy P0, we need modifications that account for the fact that we do observe an influence of on for each fixed value although this influence becomes invisible after marginalizing over .

3.2 Mutual information and conditional mutual information

It suffices to consider a few simple DAGs to illustrate why mutual information and conditional mutual information are not suitable measures of causal strength in general.

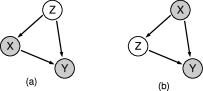

Mutual information is not suitable in Figure 2(a). It is clear that is inappropriate because we can obtain even when the arrow is missing, due to the common cause .

Conditional mutual information is not suitable for Figure 2(a). Consider the limiting case where the direct influence gets weaker until it almost disappears (). Then the behavior of the system (observationally and interventionally) is approximately described by the DAG 1(a). Using makes no sense in this scenario since, for example, may be obtained from by a simple copy operation, in which case necessarily, even when influences strongly.

3.3 Transfer entropy

Transfer entropy Schreiber is intended to measure the influence of one time-series on another one. Let be a bivariate stochastic process where influence some with , see Figure 3, left. Then transfer entropy is defined as the following conditional mutual information:

It measures the amount of information the past of provides about the present of given the past of . To quantify causal influence by conditional information relevance is also in the spirit of Granger causality, where information is usually understood in the sense of the amount of reduction of the linear prediction error.

Transfer entropy is an unsatisfactory measure of causal strength. AyInfoFlow pointed out that transfer entropy fails to quantify causal influence for the following toy model: Assume the information from is perfectly copied to and the information from to (see Figure 3, right). Then the past of is already sufficient to perfectly predict the present value of and the past of does not provide any further information. Therefore, transfer entropy vanishes although both variables heavily influence one another. If the copy operation is noisy, transfer entropy is nonzero and thus seems more reasonable, but the quantitative behavior is still wrong (as we will argue in Example 7).

Transfer entropy violates the postulates. Transfer entropy yields bits of causal influence in a situation where common sense and P1 together with P2 require that causal strength is bit (P2 reduces the DAG to one in which P1 applies). Since our postulates refer to the strength of a single arrow while transfer entropy is supposed to measure the strength of all arrows from to , we reduce the DAG such that there is only one arrow from to ; see Figure 4. Then,

The causal structure coincides with DAG 1(a) by setting , , and . With these replacements, transfer entropy yields bits instead of bit, as required by P1 and P2.

Note that the same problem occurs if causal strength between time series is quantified by directed information Massey because this measure also conditions on the entire past of .

3.4 Information flow

Note that AyInfoFlow and AyKrakauer introduce two different quantities, both called “information flow.” We consider them in turn.

After arguing that transfer entropy does not properly capture the strength of the impact of interventions, AyInfoFlow proposes to define causal strength using Pearl’s calculus Pearl00 . Given a causal directed acyclic graph , Pearl computes the joint distribution obtained if variable is forcibly set to the value as

| (6) |

Intuitively, the intervention on removes the dependence of on its parents and therefore replaces with the kronecker symbol. Likewise, one can define interventions on several nodes by replacing all conditionals with kronecker symbols.

Given three sets of nodes , and in a directed acyclic graph , information flow is defined by

To better understand this expression, we first consider the case where the set is empty. Then we obtain

which measures the mutual information between and obtained when the information channel is used with the input distribution .

Information flow, as defined in AyInfoFlow , is an unsatisfactory measure of causal strength. To quantify in DAGs 2(a) and 2(b) using information flow, we may either choose or . Both choices are inconsistent with our postulates and intuitive expectations.

Start with and DAG 2(a). Let be binary with an XOR. Let be an unbiased coin toss and obtained from by a faulty copy operation with two-sided symmetric error. One easily checks that is zero in the limit of error probability (making and independent). Nevertheless, dropping the arrow violates the Markov condition, contradicting P0. For error rate close to , we still violate P3 because is close to , while is close to zero. A similar argument applies to DAG 2(b).

Now consider . Note that it yields different results for DAGs 2(a) and 2(b) when the joint distribution is the same, contradicting P2. This is because for 2(a), while for 2(b). In other words, depends on the causal relation between the two causes and , rather than only on the relation between causes and effects.

Apart from being inconsistent with our postulate, it is unsatisfactory that tends to zero for the example above if the error rate of copying from in DAG 2(a) tends to zero (conditioned on setting to some value, the information passed from to is zero because attains a fixed value, too). In this limit, is always zero. Clearly, however, link is important for explaining the behavior of the XOR: without the link, the gate would not output “zero” for both and .

Information flow, as defined in AyKrakauer , is unsatisfactory as a measure of causal strength for sets of edges. Since this measure is close to ours, we will explain (see caption of Figure 5) the difference when introducing ours and show that P4 fails without our modification.

4 Defining the strength of causal arrows

4.1 Definition in terms of conditional probabilities

This section proposes a way to quantify the causal influence of a set of arrows that yields satisfactory answers in all the cases discussed above. Our measure is motivated by a scenario where nodes represent different parties communicating with each other via channels. Hence, we think of arrows as physical channels that propagate information between distant points in space, for example, wires that connect electronic devices. Each such wire connects the output of a device with the input of another one. For the intuitive ideas below, it is also important that the wire connecting and physically contains full information about [which may be more than the information that is required to explain the output behavior ]. We then think of the strength of arrow as the impact of corrupting it, that is, the impact of cutting the wire. To get a well-defined “post-cutting” distribution we have to say what to do with the open end corresponding to , because it needs to be fed with some input. It is natural to feed it probabilistically with inputs according to because this is the only distribution of that is locally observable [feeding it with some conditional distribution assumes that the one cutting the edge has access to other nodes—and not only the physical state of the channel]. Note that this notion of cutting edges coincides with the “source exclusion” defined in AyKrakauer if only one edge is cut. However, we define the deletion of a set of arrows by feeding all open ends with the product of the corresponding marginal distributions, while AyKrakauer keeps the dependencies between the open ends and removes the dependencies between open ends and the other variables. Our post-cutting distribution can be thought of as arising from a scenario where each channel is cut by an independent attacker, who tries to blur the attack by feeding her open end with (which is the only distribution she can see), while AyKrakauer requires communicating attackers who agree on feeding their open ends with the observed joint distribution.

Lemma 1 and Remark 1 below provide a more mathematical argument for the product distribution. Figure 5 visualizes the deletion of one edge (left) and two edges (right).

We now define the “post-cutting” distribution formally:

Definition 1 ((Removing causal arrows)).

Let be a causal DAG and be Markovian with respect to . Let be a set of arrows. Set as the set of those parents of for which and those for which . Set

| (7) |

where denotes for a given the product of marginal distributions of all variables in . Define a new joint distribution, the interventional distribution111Note that this intervention differs from the kind of interventions considered by Pearl00 , where variables are set to specific values. Here we intervene on the arrows, the “information channels,” and not on the nodes.

| (8) |

See Figure 5, left, for a simple example with cutting only one edge. Equation (8) formalizes the fact that each open end of the wires is independently fed with the corresponding marginal distribution, see also Figure 5, right. Information flow in the sense of AyKrakauer is obtained when the product distribution in (7) is replaced with the joint distribution .

The modified joint distribution can be considered as generated by the reduced DAG:

Lemma 1 ((Markovian)).

The interventional distribution is Markovian with respect to the graph obtained from by removing the edges in .

By construction, factorizes according to in the sense of (1).

Remark 1.

Markovianity is violated if the dependencies between open ends are kept. Consider, for instance, the DAG . Cutting both edges yields

which is obviously Markovian with respect to the DAG without arrows. Feeding the “open ends” with instead obtains

which induces dependencies between and , although we have claimed to have removed all links between the three variables.

Definition 2 ((Causal influence of a set of arrows)).

The causal influence of the arrows in is given by the Kullback–Leibler divergence

| (9) |

If is a single edge we write instead of .

Remark 2 ((Observing versus intervening)).

Note that could easily be confused with a different distribution obtained when the open ends are fed with conditional distributions rather than marginal distributions. As an illustrative example, consider DAG 2(a) and define as

and recall that replacing with in the right most expression yields . We call the “partially observed distribution.” It is the distribution obtained by ignoring the influence of on : is computed according to (1), but uses a DAG where is missing. The difference between “ignoring” and “cutting” the edge is important for the following reason. By a known rephrasing of mutual information as relative entropy cover we obtain

| (10) |

which, as we have already discussed, is not a satisfactory measure of causal strength. On the other hand, we have

Comparing the second expressions in (2) and (10) shows again that the difference between ignoring and cutting is due to the difference between and .

The following scenario provides a better intuition for the rightmost expression in (2).

Example 1 ((Redistributing a vaccine)).

Consider the task of quantifying the effectiveness of a vaccine. Let indicate whether a patient decides to get vaccinated or not and whether the patient becomes infected. Further assume that the vaccine’s effectiveness is strongly confounded by age because the vaccination often fails for elderly people. At the same time, elderly people request the vaccine more often because they are more afraid of infection. Ignoring other confounders, the DAG in Figure 2(a) visualizes the causal structure.

Deleting the edge corresponds to an experiment where the vaccine is randomly assigned to patients regardless of their intent and age (while keeping the total fraction of patients vaccinated constant). Then represents the conditional probability of infection, given age, when vaccines are distributed randomly. quantifies the difference to , which is the conditional probability of infection, given age and intention when patients act on their intentions. It thus measures the impact of destroying the coupling between the intention to get the vaccine and getting it via randomized redistribution.

4.2 Definition via structural equations

The definition above uses the conditional density . Estimating a conditional density from empirical data requires huge samples or strong assumptions—particularly for continuous variables. Fortunately, however, structural equations (also called functional models Pearl00 ) allow more direct estimation of causal strength without referring to the conditional distribution.

Definition 3 ((Structural equation)).

A structure equation is a model that explains the joint distribution by a deterministic dependence

where the variables are jointly independent unobserved noise variables. Note that functions that correspond to parentless variables can be chosen to be the identity, that is, .

Suppose that we are given a causal inference method that directly infers the structural equations (e.g., Hoyer , UAIidentifiability ) in the sense that it outputs -tuples with (with denoting the sample size) as well as the functions from the observed -tuples .

Definition 4 ((Removing a causal arrow in a structural equation)).

Deletion of the arrow is modeled by (i) introducing an i.i.d. copy of and (ii) subsuming the new random variable into the noise term of . The result is a new set of structural equations:

where we have omitted the superscript to simplify notation.

Remark 3.

To measure the causal influence of a set of arrows, we apply the same procedure after first introducing jointly independent i.i.d. copies of all variables at the tails of deleted arrows.

Remark 4.

The change introduced by the deletion only affects and its descendants, the virtual sample thus keeps all with . Moreover, we can ignore all variables with due to Lemma 3.

Note that must be chosen to be independent of all with , but, by virtue of the structural equations, not independent of and its descendants. The new structural equations thus generate -tuples of “virtual” observations from the input

We show below that -tuples generated this way indeed follow the distribution . We can therefore estimate causal influence via any method that estimates relative entropy using the observed samples and the virtual ones . To illustrate the above scheme, we consider the case where and are causes of and we want to delete the edge . The case where has more than parents follows easily.

Example 2 ((Two parents)).

The following table corresponds to the observed variables , as well as the unobserved noise which we assumed to be estimated together with learning the structural equations:

| (14) |

To simulate the deletion of we first generate a list of virtual observations for after generating samples from an i.i.d. copy of :

| (15) |

A simple method to simulate the i.i.d. copy is to apply some random permutation to and obtain (see suppcausalstrength , S.1). Deleting several arrows with source node requires several identical copies of , each generated by a different permutation.

We then throw away the two noise columns, that is, the original noise and the additional noise :

| (16) |

To see that this triple is indeed sampled from the desired distribution , we recall that the original structural equation simulates the conditional . After inserting we obtain the new conditional . Multiplying it with yields , by definition. Using the above samples from and samples from we can estimate

using some known schemes Perez-Cruz for estimating relative entropies from empirical data. It is important that the samples from the two distributions are disjoint, meaning that we need to split the original sample into two halves, one for and one for .

The generation of for a set of arrows works similarly: every input of a structural equation that corresponds to an arrow to be removed is fed with an independent copy of the respective variable. Although it is conceptually simple to estimate causal strength by generating the entire joint distribution , Theorem 5(a) will show how to break the problem into parts that make estimation of relative entropies from finite data more feasible.

We now revisit mediation analysis Pearl00 , Avin , Robins , which is also based on structural equations, and mention an interesting relation to our work. Although we have pointed out that intervening by “cutting edges” is complementary to the intervention on nodes considered there, distributions like can also occur in an implicit way. To explore the indirect effect in Figure 2(b), one can study the effect of on in the reduced DAG under the distribution or under the distribution obtained by setting the copy to some fixed value . Remarkably, cutting is then used to study the strength of the other path while we use it to study the strength222We are grateful to an anonymous referee for this observation. of .

4.3 Properties of causal strength

This subsection shows that our definition of causal strength satisfies postulates P0–P4. We observe at the same time some other useful properties. We start with a property that is used to show P0.

Causal strength majorizes observed dependence. Recalling that factorizes into with respect to the true causal DAG , one may ask how much error one would cause if one was not aware of all causal influences and erroneously assumed that the true DAG would be the one where some set of arrows is missing. The conditionals with respect to the reduced set of parents define a different joint distribution.

Definition 5 ((Distribution after ignoring arrows)).

Given distribution Markovian with respect to and set of arrows , let the partially observed distribution (where interactions across are hidden) for node be

Let the partially observed distribution for all the nodes be the product

| (17) |

Remark 5.

Intuitively, the observed influence of a set of arrows should be quantified by comparing the data available to an observer who can see the entire DAG with the data available to an observer who sees all the nodes of the graph, but only some of the arrows. Definition 5 formalizes “seeing only some of the arrows.”

Building on Remark 2, the definition of the observed dependence of a set of arrows takes the same general form as for causal influence. However, instead of inserting noise on the arrows, we instead simply prevent ourselves from seeing them.

Definition 6 ((Observed influence)).

Given a distribution that is Markovian with respect to and set of arrows , let the observed influence of the arrows in be

with defined in (17).

The following result, proved in Section .1, is crucial to proving P0.

Theorem 2 ((Causal influence majorizes observed dependence))

Causal influence decomposes into observed influence plus a nonnegative term quantifying the divergence between the partially observed and interventional distributions

| (18) |

The theorem shows that “snapping upstream dependencies” by using purely local data that is, by marginalizing using the distribution of the source node rather than the conditional —is essential to quantifying causal influence.

Proof of postulates for causal strength.

P0: Let be the DAG obtained by removing the arrows in from . Let be the parents of in , that is, those that are not in and introduce the set of nodes such that . By Theorem 2, implies , that is, , which implies

| (19) |

that is, .

We use again the Ordered Markov condition

| (20) |

where denote the predecessors of with respect to some ordering of nodes that is consistent with . By the contraction rule Pearl00 , (19) and (20) yields

and hence

which is the Ordered Markov condition for if we use the same ordering of nodes for .

P1: One easily checks for the 2-node DAG , because and thus

P2: Follows from the following lemma.

Lemma 3 ((Causal strength as local relative entropy)).

Causal strength can be written as the following relative entropy distance or conditional relative entropy distance:

Note that actually depends on the reduced set of parents only, but it is more convenient for the notation and the proof to keep the formal dependence on all .

Proof of Lemma 3

For all we have , because is the only conditional that is modified by the deletion.

P3: Apart from demonstrating the postulated inequality, the following result shows that we have the equality for independent causes. To keep notation simple, we have restricted our attention to the case where has only two causes and , but can also be interpreted as representing all parents of other than .

Theorem 4 ((Decomposition of causal strength))

Equation (21) follows from Theorem 2: First, we observe because both measure the relative entropy distance between and . Second, we have

The second summand in (18) reduces to

To see that the second term in equation (21) vanishes for independent , we observe because

Theorem 4 states that conditional mutual information underestimates causal strength. Assume, for instance, that and are almost always equal because has such a strong influence on that it is an almost perfect copy of it. Then because knowing leaves almost no uncertainty about . In other words, strong dependencies between the causes and makes the influence of cause almost invisible when looking at the conditional mutual information only. The second term in (21) corrects for the underestimation. When depends deterministically on , it is even the only remaining term (here, we have again assumed that the conditional distributions are defined for events that do not occur in observational data).

To provide a further interpretation of Theorem 4, we recall that can be seen as the impact of ignoring the edge ; see Remark 2. Then the impact of cutting is given by the impact of ignoring this link plus the impact that cutting has on the conditional .

P4: This postulate is part (d) of the following collection of results that relates strength of sets to its subsets.

Theorem 5 ((Relation between strength of sets and subsets))

The causal influence given in Definition 2 has the following properties:

[(a)]

Additivity regarding targets. Given set of arrows , let , then

Locality. Every only depends on the conditional and the joint distribution of all parents .

Monotonicity. Given sets of arrows targeting single node , such that the source nodes in are jointly independent and independent of the other parents of . Then we have

Heredity property. Given sets of arrows , we have

The proof is presented in Appendix .3. The intuitive meaning of these properties is as follows. Part (a) says that causal influence is additive if the arrows have different targets. Otherwise, we can still decompose the set into equivalence classes of arrows having the same target and obtain additivity regarding the decomposition. This can be helpful for practical applications because estimating each from empirical data requires less data then estimating the distance for the entire high dimensional distributions.

We will show in Section 4.4 that general additivity fails. Part (b) is an analog of P2 for multiple arrows. According to (c), the strength of a subset of arrows cannot be smaller than the strength of its superset, provided that there are no dependencies among the parent nodes. Finally, part (d) is exactly our postulate P4.

Parts (c) and (d) suggest that monotonicity may generalize to the case of dependent parents: . However, the following counterexample due to Bastian Steudel shows this is not the case.

Example 3 ((XOR—counterexample to monotonicity when parents are dependent)).

Consider the DAG(a) in Figure 2 and let the relation between be given by the structural equations

| (22) | |||||

| (23) |

Let and . Letting and we find that

For , strict concavity of the logarithm implies .

4.4 Examples and paradoxes

Failure of subadditivity: The strength of a set of arrows is not bounded from above by the sum of strength of the single arrows. It can even happen that removing one arrow from a set has no impact on the joint distribution while removing all of them has significant impact, which occurs in communication scenarios that use redundancy.

Example 4 ((Error correcting code)).

Let and be binary variables that we call “encoder” and “decoder” (see Figure 6) communicating over a channel that consists of the bits . Using the simple repetition code, all are just copies of . Then is set to the logical value that is attained by the majority of . This way, errors can be corrected, that is, removing or less of the links has no effect on the joint distribution, that is, for , hence . In words: removing or less arrows is without impact, but removing all of them is, of course. After all, the arrows jointly generate the dependence , provided that is uniformly distributed.

Clearly, the outputs of causally influence the behavior of . We therefore need to consider interventions that destroy many arrows at once if we want to capture the fact that their joint influence is nonzero.

Thus, causal influence of arrows is not subadditive: the strength of each arrow is zero, but the strength of the set of all is bit.

Failure of superadditivity: The following example reveals an opposing phenomenon, where the causal strength of a set is smaller than the sum of the single arrows.

Example 5 ((XOR with uniform input)).

Strong influence without dependence/failure of converse of P0: Revisiting Example 5 is also instructive because it demonstrates an extreme case of confounding where vanishes but causal influence is strong. Removing yields

where and . It is easy to see that

because is a uniform distribution over possible triples , whereas is a uniform distribution over a superset of triples.

The impact of cutting the edge is remarkable: both distributions, the observed one as well as the post-cutting distribution , factorize and . Cutting the edge keeps this product structure and changes the joint distributions by only changing the marginal distribution of from to .

Note that satisfies the Markov condition with respect to (i.e., the DAG obtained from the original one by dropping ) because is a constant. Since , this shows that the converse of P0 does not hold.

Strong effect of little information: The following example considers multiple arrows and shows that their joint strength may even be strong when they carry the same small amount of information.

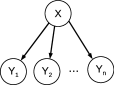

Example 6 ((Broadcasting)).

Consider a single source with many targets such that each copies , see Figure 7. Assume . If is the set of all arrows then . Thus, the single node exerts bits of causal influence on its dependents.

5 Causal influence between two time series

5.1 Definition

Since causal analysis of time series is of high practical importance, we devote a section to this case. For some fixed , we introduce the short notation for the set of all arrows that point to from some with . Then

measures the impact of deleting all these arrows. We propose to replace transfer entropy with this measure since it does not suffer from the drawbacks described in Section 3.3.

Section 4.2 describes how to estimate causal strength from finite data for one arrow and briefly mentions how this generalizes to set of arrows. To keep this section self-consistent, we briefly rephrase the description for the case of time series.

Suppose we have learned the structural equation model

| (24) |

from observed data , where the noise variables are jointly independent and independent of Assume, moreover, that we have inferred the corresponding values of the noise. If we have multiple copies of the time series, we can apply the method described in Section 4.2 in a straightforward way: Due to the locality property stated in Theorem 5(b), we only consider the variables and feed (24) with i.i.d. copies of by applying random permutations to the observations, which then yields samples from the modified distribution .

If we have only one observation for each time instance, we have to assume stationarity (with constant function ) and ergodicity and generate an artificial statistical sample by looking at sufficiently distant windows.

5.2 Comparison of causal influence with transfer entropy

We first recall the example given by AyInfoFlow showing a problem with transfer entropy (Section 3.3). Assume that the variables in Figure 3, right, are binary and the transition from to is a perfect copy and likewise the transition from to . Assume, moreover, that the two causal chains have been initialized such that, with probability , all variables are and with probability all are zero. Then the set is the singleton . Using Lemma 3, we have

Since is a perfect copy of , we have

into

One easily checks .

Note that the example is somewhat unfair, since it is impossible to distinguish the structural equations from a model without interaction between and , where is obtained from by inversion and similarly for , no matter how many observations are performed. Thus, from observing the system it is impossible to tell whether or not exerts an influence on . However, the following modification shows that transfer entropy still goes quantitatively wrong if small errors are introduced.

Example 7 ((Perturbed transfer entropy counterexample)).

Perturb Ay and Polani’s example by having copy correctly with probability . Set node ’s transitions as Markov matrix

and similarly for the transition from to .

The transfer entropy from to at time is

where denotes the conditional Shannon entropy. The equalities can be derived from d-separation in the causal DAG Figure 3, right Pearl00 . For instance, conditioning on , renders the pair independent of all the remaining past of and . We find

Hence,

which tends to zero as .

Causal influence, on the other hand, is given by the mutual information because all edges other than are irrelevant (see Postulate P2). Thus,

which tends to for . Hence, causal influence detects the causal interactions between and based on empirical data, whereas transfer entropy does not. Thanks to the perturbation, the joint distribution tells us the kind of causal relations by which it is generated. For large enough samples, the strong discrepancy between transfer entropy and our causal strength thus becomes apparent.

6 Causal strength for linear structural equations

For linear structural equations, we can provide a more explicit expression of causal strength under the assumption of multivariate Gaussianity. Let random variables be ordered such that there are only arrows from to for . Then we have structural equations

where all are jointly independent noise variables. In vector and matrix notation we have

| (25) |

where is lower triangular with zeros in the diagonal.

To compute the strength of , we assume for reasons of convenience that all variables have zero mean. Then can be computed from the covariance matrices alone.

The covariance matrix of reads

where denotes the covariance matrix of the noise (which is diagonal by assumption) and the transpose of the inverse of a matrix.

To compute the covariance matrix of , we first split into , where contains only those entries that correspond to the edges in the set and only those corresponding to the complement of . Using this notation, the modified structural equations read

| (26) |

where and each has the same distribution as and satisfies joint independence of all . It is convenient to define the modified noise

with covariance matrix

| (27) |

where contains only the diagonal entries of (recall that all are independent). The modified variables are now given by the equation

which formally looks like (25), although the components of are dependent while the in (25) are independent. Thus, we obtain the modified covariance matrix of by

The causal strength now reads

with given by (27).

Example 8 ((Linear structural equations with independent parents)).

It is instructive to look at the following simple case:

For the set with some calculations show

For the single arrow , we thus obtain

If is the only parent, that is, , we have

with as in equation (3) introduced in the context of ANOVA. Note that the relation between our measure and is less simple for because would then still measure the fraction of the variance of explained by , while is related to the fraction of the conditional variance of , given its other parents, explained by . This is because our causal strength reduces to a conditional mutual information for independent parents; see the last sentence of Theorem 4.

7 Experiments

Code for all experiments can be downloaded athttp://webdav.tuebingen.mpg.de/causality/.

7.1 DAGs without time structure

We here restrict attention to linear structural equations, but interesting generalizations are given by additive noise models Hoyer , UAIidentifiability , Jonastpami and post-nonlinear models ZhangUAI .

The first step in estimating the causal strength consists in inferring the structure matrix in (25) from the given matrix of observations with and (the th row corresponds to the observed values of ). We did this step by ridge regression. We decompose into the sum as in Section 6.

Then we divide the columns of into two parts and of sample size . While is kept as it is, is used to generate new samples according to the modified structural equations: First, we note that the values of the noise variables corresponding to the observations are given by the residuals

Then we generate a matrix by applying independent random permutations to the columns of , which simulates samples of the random variables in (26). Samples from the modified structural equation are now given by

To estimate the relative entropy distance between and (with samples and ), we use the method described in Perez-Cruz : Let be the euclidean distance from the th column in to the th nearest neighbor among the other columns of and be the distance to the th nearest neighbor among all columns of , then the estimator reads

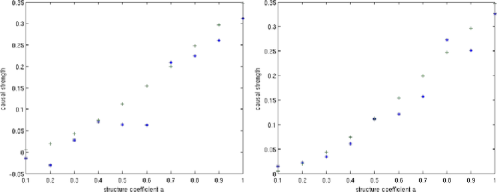

Figure 8 shows the difference between estimated and computed causal strength for the simplest DAG with increasing structure coefficient. For some edges, we obtain significant bias. However, since the bias depends on the distributions Perez-Cruz , it would be challenging to correct for it.

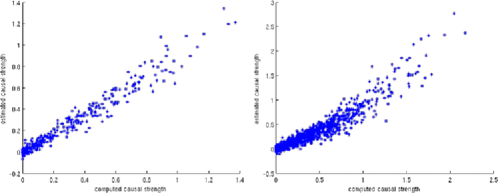

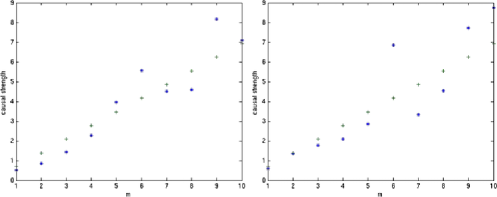

To provide a more general impression on the estimation error, we have considered a complete DAG on and nodes and randomly generated structure coefficients. In each of runs, the structure matrix is generated by independently drawing each entry from a standard normal distribution. For each of the arrows and each we computed and estimated , which yields the -value and the -value, respectively, of one of the points in the scatter plots in Figure 9. Remarkably, we do not see a significant degradation for nodes (right) compared to (left).

7.2 Time series

The fact that transfer entropy fails to capture causal strength has been one of our motivations for defining a different measure. We revisit the critical example in Section 5.2, where the dynamical evolution on two bits was given by noisy copy operations from to and to . This way, we obtained causal strength bit when the copy operations is getting perfect. Our software for estimating causal strength only covers the case of linear structural equations, with the additional assumption of Gaussianity for the subroutines that compute the causal strength from the covariance matrices for comparison with the estimated value.

A natural linear version of Example 7 is an autoregressive (AR-) model of order given by

where are independent noise terms. We consider the stationary regime where and have unit variance and has variance . For the influence from on , and similarly from to gets deterministic. We thus obtain infinite causal strength (note that two deterministically coupled random variables with probability density have infinite mutual information). It is easy to see that transfer entropy does not diverge, because the conditional variance of is if only the past of is given and if the past of is given in addition. Reducing the variance by the factor corresponds to the constant information gain of , regardless of how small is.

Figure 10 shows the computed and estimated values of causal strength for decreasing , that is, the deterministic limit. Note that, in this limit, the estimated relative entropy can deviate strongly from the true one because the true one diverges since lives on a higher dimensional manifold than . This probably explains the large errors for , which correspond to quite low noise level already.

8 Conclusions

We have defined the strength of an arrow or a set of arrows in a causal Bayesian network by quantifying the impact of an operation that we called “destruction of edges”. We have stated a few postulates that we consider natural for a measure of causal strength and shown that they are satisfied by our measure. We do not claim that our list is complete, nor do we claim that measures violating our postulates are inappropriate. How to quantify causal influence may strongly depend on the purpose of the respective measure.

For a brief discussion of an alternative measure of causal strength and some of the difficulties that arising when quantifying the total influence of one set of nodes on another, see the supplementary material suppcausalstrength .

The goal of this paper is to encourage discussions on how to define causal strength within a framework that is general enough to include dependencies between variables of arbitrary domains, including nonlinear interactions, and multi-dimensional and discrete variables at the same time.

Appendix: Further properties of causal strength and proofs

.1 Proof of Theorem 2

Expand as

Note that the second term can be written as

| (30) | |||

| (31) | |||

| (32) | |||

| (33) |

Causal influence is thus observed influence plus a correction term that quantifies the divergence between the partially observed and interventional distributions. The correction term is nonnegative since it is a weighted sum of conditional Kullback–Leibler divergences.

.2 Decomposition into conditional relative entropies

The following result generalizes Lemma 3 to the case where contains more than one edge. It shows that the relative entropy expression defining causal strength decomposes into a sum of conditional relative entropies, each of it referring to the conditional distribution of one of the target nodes, given its parents:

Lemma 6 ((Causal influence decomposes into a sum of expectations)).

The causal influence of set of arrows can be rewritten

where denotes the target nodes of arrows in .

The result is used in the proof of Theorem 5 below.

Proof of Theorem 5 Using the chain rule for relative entropy cover , we get

where we have used that for all . Then the statement follows from the definition of . Note that a similar statement for (i.e., swapping the roles of and ) would not hold because then the weighting factor in (.2) needed to be replaced with the factor , which is sensitive even to deleting edges not targeting .

.3 Proof of Theorem 5

Parts (a) and (b) follow from Lemma 6 since is the th summand in (.2), which obviously depends on and only.

To prove part (c), we will show that the restrictions of to the variables form a so-called Pythagorean triple in the sense of Amari , that is,

This is sufficient because the left-hand side and the first term on the right-hand side of equation (.3) coincide with and , respectively, due to part (b). Note, however, that

because we have such a locality statement only for terms of the form . We therefore consistently restrict attention to and find

where we have used that the sources in are jointly independent and independent of the other parents of . By definition of , the second summand reads

which proves (.3).

By Lemma 6, it is only necessary to prove part (d) in the case where both and consist of arrows targeting a single node. To keep the exposition simple, we consider the particular case of a DAG containing three nodes where and . The more general case follows similarly. Observe that if and only if

| (37) |

for all such that . Multiplying both sides with and summing over all yields

because the right-hand side does not depend on . Using (37) again, we obtain

for all with . Hence , and thus .

.4 Causal influence measures controllability

Causal influence is intimately related to control. Suppose an experimenter wishes to understand interactions between components of a complex system. For the causal DAG in Figure 1(d), she is able to observe nodes and , and manipulate node . To what extent can she control node ? The notion of control has been formalized information-theoretically in touchette04 :

Definition 7 ((Perfect control)).

Node is perfectly controllable by node at if, given , {longlist}[(ii)]

states of are a deterministic function of states of ; and

manipulating gives rise to all states of .

Perfect control can be elegantly characterized:

Theorem 7 ((Information-theoretic characterization of perfect controllability))

A node with inputs and is perfectly controllable by alone for iff there exists a Markov transition matrix such that

| (C1) | |||||

| (C2) |

Here, denotes the conditional Shannon entropy of , given that has been observed and has been set to .

The theorem restates the criteria in the definition. For a proof, see touchette04 .

It is instructive to compare Theorem 7 to our measure of causal influence. The theorem highlights two fundamental properties of perfect control. First, (C1), perfect control requires there is no variation in ’s behavior—aside from that due to the manipulation via —given that is observed. Second, (C2), perfect control requires that all potential outputs of can be induced by manipulating node . This suggests a measure of the degree of control should reflect (i) the variability in ’s behavior that cannot be eliminated by imposing values and (ii) the size of the repertoire of behaviors that can be induced on the target by manipulating a source.

For the DAG under consideration, Theorem 4 states that

The first term, , quantifies size of the repertoire of outputs of averaged over manipulations of . It corresponds to requirement (C2) in the characterization of perfect control: that for all . Specifically, the causal influence, interpreted as a measure of the degree of controllability, increases with the size of the (weighted) repertoire of outputs that can be induced by manipulations.

The second term, [which coincides with here], quantifies the variability in ’s behavior that cannot be eliminated by controlling . It corresponds to requirement (C1) in the characterization of perfect control: that remaining variability should be zero. Causal influence increases as the variability tends toward zero provided that the first term remains constant.

Acknowledgement

We are grateful to Gábor Lugosi for a helpful hint for the proof of Lemma 1 in Supplement S.1 and to Philipp Geiger for several corrections.

[id=suppA]

\stitleSupplement to “Quantifying causal influences”

\slink[doi,text=10.1214/13-AOS1145SUPP]10.1214/13-AOS1145SUPP \sdatatype.pdf

\sfilenameaos1145_supp.pdf

\sdescriptionThree supplementary sections:(1) Generating an i.i.d.

copy via random permutations; (2) Another option to define causal

strength; and (3) The problem of defining total influence.

References

- (1) {bbook}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmAmari, \bfnmS.\binitsS. and \bauthor\bsnmNagaoka, \bfnmH.\binitsH. (\byear1993). \btitleMethods of Information Geometry. \bpublisherOxford Univ. Press, \blocationNew York. \bptokimsref \endbibitem

- (2) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmAvin, \bfnmC.\binitsC., \bauthor\bsnmShpitser, \bfnmI.\binitsI. and \bauthor\bsnmPearl, \bfnmJ.\binitsJ. (\byear2005). \bhowpublishedIdentifiability of path-specific effects. In Proceedings of the International Joint Conference in Artificial Intelligence, Edinburgh, Scotland 357–363. Professional Book Center, Denver. \bptokimsref \endbibitem

- (3) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmAy, \bfnmN.\binitsN. and \bauthor\bsnmKrakauer, \bfnmD.\binitsD. (\byear2007). \btitleGeometric robustness and biological networks. \bjournalTheory in Biosciences \bvolume125 \bpages93–121. \bptokimsref \endbibitem

- (4) {barticle}[mr] \bauthor\bsnmAy, \bfnmNihat\binitsN. and \bauthor\bsnmPolani, \bfnmDaniel\binitsD. (\byear2008). \btitleInformation flows in causal networks. \bjournalAdv. Complex Syst. \bvolume11 \bpages17–41. \biddoi=10.1142/S0219525908001465, issn=0219-5259, mr=2400125 \bptokimsref \endbibitem

- (5) {bbook}[mr] \bauthor\bsnmCover, \bfnmThomas M.\binitsT. M. and \bauthor\bsnmThomas, \bfnmJoy A.\binitsJ. A. (\byear1991). \btitleElements of Information Theory. \bpublisherWiley, \blocationNew York. \biddoi=10.1002/0471200611, mr=1122806 \bptokimsref \endbibitem

- (6) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmGranger, \bfnmC. W. J.\binitsC. W. J. (\byear1969). \btitleInvestigating causal relations by econometric models and cross-spectral methods. \bjournalEconometrica \bvolume37 \bpages424–38. \bptokimsref \endbibitem

- (7) {bincollection}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmHolland, \bfnmP. W.\binitsP. W. (\byear1988). \btitleCausal inference, path analysis, and recursive structural equations models. In \bbooktitleSociological Methodology (\beditor\bfnmC.\binitsC. \bsnmClogg, ed.) \bpages449–484. \bpublisherAmerican Sociological Association, \blocationWashington, DC. \bptokimsref \endbibitem

- (8) {bincollection}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmHoyer, \bfnmP.\binitsP., \bauthor\bsnmJanzing, \bfnmD.\binitsD., \bauthor\bsnmMooij, \bfnmJ.\binitsJ., \bauthor\bsnmPeters, \bfnmJ.\binitsJ. and \bauthor\bsnmSchölkopf, \bfnmB.\binitsB. (\byear2009). \btitleNonlinear causal discovery with additive noise models. In \bbooktitleAdvances in Neural Information Processing Systems 21: 22nd Annual Conference on Neural Information Processing Systems 2008 (\beditor\bfnmD.\binitsD. \bsnmKoller, \beditor\bfnmD.\binitsD. \bsnmSchuurmans, \beditor\bfnmY.\binitsY. \bsnmBengio and \beditor\bfnmL.\binitsL. \bsnmBottou, eds.) \bpages689–696. \bpublisherCurran Associates, \blocationRed Hook, NY. \bptokimsref \endbibitem

- (9) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmJanzing, \bfnmD.\binitsD., \bauthor\bsnmBalduzzi, \bfnmD.\binitsD., \bauthor\bsnmGrosse-Wentrup, \bfnmM.\binitsM. and \bauthor\bsnmSchölkopf, \bfnmB.\binitsB. (\byear2013). \bhowpublishedSupplement to “Quantifying causal influences.” DOI:10.1214/ 13-AOS1145SUPP. \bptokimsref \endbibitem

- (10) {bbook}[mr] \bauthor\bsnmLauritzen, \bfnmSteffen L.\binitsS. L. (\byear1996). \btitleGraphical Models. \bseriesOxford Statistical Science Series \bvolume17. \bpublisherOxford Univ. Press, \blocationNew York. \bidmr=1419991 \bptokimsref \endbibitem

- (11) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmLewontin, \bfnmR. C.\binitsR. C. (\byear1974). \btitleAnnotation: The analysis of variance and the analysis of causes. \bjournalAmerican Journal Human Genetics \bvolume26 \bpages400–411. \bptokimsref \endbibitem

- (12) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmMassey, \bfnmJ.\binitsJ. (\byear1990). \bhowpublishedCausality, feedback and directed information. In Proc. 1990 Intl. Symp. on Info. Th. and Its Applications. Waikiki, Hawaii. \bptokimsref \endbibitem

- (13) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmNorthcott, \bfnmR.\binitsR. (\byear2008). \btitleCan ANOVA measure causal strength? \bjournalThe Quaterly Review of Biology \bvolume83 \bpages47–55. \bptokimsref \endbibitem

- (14) {bbook}[mr] \bauthor\bsnmPearl, \bfnmJudea\binitsJ. (\byear2000). \btitleCausality: Models, Reasoning, and Inference. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=1744773 \bptokimsref \endbibitem

- (15) {bincollection}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmPearl, \bfnmJ.\binitsJ. (\byear2001). \btitleDirect and indirect effects. In \bbooktitleProceedings of the 17th Conference on Uncertainty in Artificial Intelligence (UAI2001) \bpages411–420. \bpublisherMorgan Kaufmann, \blocationSan Francisco, CA. \bptokimsref \endbibitem

- (16) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmPérez-Cruz, \bfnmF.\binitsF. (\byear2009). \bhowpublishedEstimation of information theoretic measures for continuous random variables. In Advances in Neural Information Processing Systems 21: 22nd Annual Conference on Neural Information Processing Systems 2008 (D. Koller, D. Schuurmans, Y. Bengio and L. Bottou, eds.) 1257–1264. Curran Associates, Red Hook, NY. \bptokimsref \endbibitem

- (17) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmPeters, \bfnmJ.\binitsJ., \bauthor\bsnmJanzing, \bfnmD.\binitsD. and \bauthor\bsnmSchölkopf, \bfnmB.\binitsB. (\byear2011). \btitleCausal inference on discrete data using additive noise models. \bjournalIEEE Transac. Patt. Analysis and Machine Int. \bvolume33 \bpages2436–2450. \bptokimsref \endbibitem

- (18) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmPeters, \bfnmJ.\binitsJ., \bauthor\bsnmMooij, \bfnmJ.\binitsJ., \bauthor\bsnmJanzing, \bfnmD.\binitsD. and \bauthor\bsnmSchölkopf, \bfnmB.\binitsB. (\byear2001). \bhowpublishedIdentifiability of causal graphs using functional models. In Proceedings of the 27th Conference on Uncertainty in Artificial Intelligence (UAI 2011) 589–598. AUAI Press, Corvallis, OR. Available at http://uai.sis.pitt.edu/papers/11/p589-peters.pdf. \bptokimsref \endbibitem

- (19) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmRobins, \bfnmJ. M.\binitsJ. M. and \bauthor\bsnmGreenland, \bfnmS.\binitsS. (\byear1992). \btitleIdentifiability and exchangeability for direct and indirect effects. \bjournalEpidemiology \bvolume3 \bpages143–155. \bptokimsref \endbibitem

- (20) {barticle}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmSchreiber, \bfnmT.\binitsT. (\byear2000). \btitleMeasuring information transfer. \bjournalPhys. Rev. Lett. \bvolume85 \bpages461–464. \bptokimsref \endbibitem

- (21) {bbook}[mr] \bauthor\bsnmSpirtes, \bfnmPeter\binitsP., \bauthor\bsnmGlymour, \bfnmClark\binitsC. and \bauthor\bsnmScheines, \bfnmRichard\binitsR. (\byear1993). \btitleCausation, Prediction, and Search. \bseriesLecture Notes in Statistics \bvolume81. \bpublisherSpringer, \blocationNew York. \biddoi=10.1007/978-1-4612-2748-9, mr=1227558 \bptokimsref \endbibitem

- (22) {barticle}[mr] \bauthor\bsnmTouchette, \bfnmHugo\binitsH. and \bauthor\bsnmLloyd, \bfnmSeth\binitsS. (\byear2004). \btitleInformation-theoretic approach to the study of control systems. \bjournalPhys. A \bvolume331 \bpages140–172. \biddoi=10.1016/j.physa.2003.09.007, issn=0378-4371, mr=2046360 \bptokimsref \endbibitem

- (23) {bmisc}[auto:STB—2013/09/19—12:14:10] \bauthor\bsnmZhang, \bfnmK.\binitsK. and \bauthor\bsnmHyvärinen, \bfnmA.\binitsA. (\byear2009). \bhowpublishedOn the identifiability of the post-nonlinear causal model. In Proceedings of the 25th Conference on Uncertainty in Artificial Intelligence, Montreal, Canada 647–655. AUAI Press, Arlington, VA. \bptokimsref \endbibitem