The effect of coherence on sampling from matrices with orthonormal columns, and preconditioned least squares problems††thanks: Both authors were supported in part by NSF grant CCF-1145383. The first author also acknowledges the support from the XDATA Program of the Defense Advanced Research Projects Agency (DARPA), administered through Air Force Research Laboratory contract FA8750-12-C-0323 FA8750-12-C-0323.

Abstract

Motivated by the least squares solver Blendenpik, we investigate three strategies for uniform sampling of rows from matrices with orthonormal columns. The goal is to determine, with high probability, how many rows are required so that the sampled matrices have full rank and are well-conditioned with respect to inversion.

Extensive numerical experiments illustrate that the three sampling strategies (without replacement, with replacement, and Bernoulli sampling) behave almost identically, for small to moderate amounts of sampling. In particular, sampled matrices of full rank tend to have two-norm condition numbers of at most 10.

We derive a bound on the condition number of the sampled matrices in terms of the coherence of . This bound applies to all three different sampling strategies; it implies a, not necessarily tight, lower bound of for the number of sampled rows; and it is realistic and informative even for matrices of small dimension and the stringent requirement of a 99 percent success probability.

For uniform sampling with replacement we derive a potentially tighter condition number bound in terms of the leverage scores of . To obtain a more easily computable version of this bound, in terms of just the largest leverage scores, we first derive a general bound on the two-norm of diagonally scaled matrices.

To facilitate the numerical experiments and test the tightness of the bounds, we present algorithms to generate matrices with user-specified coherence and leverage scores. These algorithms, the three sampling strategies, and a large variety of condition number bounds are implemented in the Matlab toolbox kappa_SQ_v3.

keywords:

condition number, singular values, leverage scores, sums of random matrices, majorization, preconditioning, QR factorization,AM:

65F08, 65F10, 65F20, 65F25, 65F35, 68W20, 15A12, 15A18, 15A42, 15B10, 15B521 Introduction

Our paper was inspired by Avron, Maymounkov and Toledo’s Blendenpik algorithm and analysis [1].

Blendenpik is an iterative method for solving overdetermined least squares/regression problems with the Krylov space method LSQR [22]. In order to accelerate convergence, Blendenpik constructs a preconditioner and solves instead the preconditioned least squares problem . The solution to the original problem is recovered by solving a linear system with coefficient matrix . The innovative feature is the construction of the preconditioner by a random sampling method.

1.1 Motivation

The purpose of our paper is a thorough experimental and analytical investigation of random sampling strategies for producing efficient preconditioners. The challenge is to ensure not only that is nonsingular, but also that is well-conditioned with respect to inversion, which is required for fast convergence and numerical stability.

Here is a conceptual point of view of how Blendenpik constructs the preconditioner: First it “smoothes out” the rows of by applying a randomized unitary transform , and then it uniformly samples (i.e. selects) a small number of rows from . At last it computes a QR factorization of the smaller sampled matrix, , where the triangular factor serves as the preconditioner.

The neat and crucial observation in [1] is to realize that sampling rows from amounts, conceptually, to sampling rows from an orthonormal basis of . That is, if the columns of represent an orthonormal basis for the column space of , and if is a sampling matrix then has the same two-norm condition number as . This means, it suffices to consider sampling from matrices with orthonormal columns.

The analysis in [1] suggests that is well conditioned, if has low “coherence”. Intuitively, coherence gives information about the localization or “uniformity” of the elements of . Mathematically, coherence is the largest (squared) norm of any row of . For instance, if consists of canonical vectors, then the non-zero elements are concentrated in only a few rows, so that has high coherence. However, if is a submatrix of a Hadamard matrix, then all elements have the same magnitude, so that has low coherence.

If has low coherence, then, in the context of sampling, all rows are equally important. Hence any sampled matrix with sufficiently many rows is likely to have full rank. The purpose of the randomized transform is to produce a matrix whose orthonormal basis has low coherence.

We were intrigued by the analysis of Blendenpik because it appears to be the first to exploit the concept of coherence for numerical purposes. We also wanted to get a better understanding of the condition number bound for in [1, Theorem 3.2], which contains an unspecified constant, and of the effect of uniform sampling strategies.

1.2 Overview and main results

We survey the contents of the paper, with a focus on the main results.

From preconditioned matrices to sampled matrices with orthonormal columns (Section 2)

We start with a brief sketch of the Blendenpik least squares solver (Section 2.1), and make the important transition from preconditioned matrices to sampled matrices with orthonormal columns, made possible by the observation ([1, 24] and Lemma 1) that both have the same two-norm condition number111Here denotes the Euclidean two-norm condition number with respect to inversion of a full rank matrix . The matrix is the Moore-Penrose inverse of .,

Then we discuss the notion of coherence and its properties (Section 2.2). For a matrix with orthonormal columns, , the coherence

is the largest squared row norm222The superscript denotes transpose, and is the identity matrix with columns ..

Sampling methods (Section 3)

We discuss three randomized methods for producing sampling matrices : Sampling without replacement (Section 3.1), sampling with replacement (Section 3.2), and Bernoulli sampling (Section 3.3). We show that Bernoulli sampling can be viewed as a form of sampling without replacement (Section 3.4).

The sampling matrices from all three methods are constructed so that is an unbiased estimator of the identity matrix. The action of applying to a matrix with orthonormal columns, , amounts to randomly sampling rows from .

The numerical experiments (Section 3.5) illustrate two points: First, the three sampling methods behave almost identically, in terms of the percentage of sampled matrices that have full rank and their condition numbers, in particular for small to moderate sampling amounts. Second, those sampled matrices that have full rank tend to be very well-conditioned, with condition numbers .

As a consequence (Section 3.6), we recommend sampling with replacement for Blendenpik, because it is fast, and it is easy to implement.

Numerical experiments

Since random sampling methods can be expected to work well in the asymptotic regime of very large matrix dimensions, we restrict all numerical experiments to matrices of small dimension.

Furthermore, we consider only matrices that have many more rows than columns, . This is the situation where random sampling methods can be most efficient. In contrast, random sampling methods are not efficient for matrices that are almost square, because the number of rows in has to be at least equal to , otherwise is not possible.

Condition number bounds based on coherence (Section 4)

We derive a probabilistic bound, in terms of coherence, for the condition numbers of the sampled matrices (Theorem 7 in Section 4.1). The bound applies to all three sampling methods. From this we derive the following lower bound, not necessarily tight, on the required number of sampled rows.

-

Preview of Corollary 8 Given a failure probability , and a tolerance . To achieve the condition number bound , the number of rows from , sampled by any of three methods, should be at least

(1)

This suggests that one has to sample more rows for if has high coherence ( close to 1), if one wants a low condition number bound (small ), or if one wants a high success probability (small ).

Numerical experiments (Section 4.2) illustrate that the bounds are informative for matrices with sufficiently low coherence and sufficiently high aspect ratio . Our bounds have the following advantages (Section 4.3):

-

1.

They are tighter than those in [1, Theorem 3.2] because they are non-asymptotic, with all constants explicitly specified.

-

2.

They apply to three different sampling methods.

-

3.

They imply a lower bound, of , on the required number of sampled rows.

-

4.

They are realistic and informative – even for matrices of small dimension and the stringent requirement of a 99 percent success probability.

Condition number bounds based on leverage scores, for uniform sampling with replacement (Section 5)

The goal is to tighten the coherence-based bounds from Section 4 by making use of all the row norms of , instead of just the largest one. To this end we introduce leverage scores (Section 5.1), which are the squared row norms of ,

We use them to derive a bound for uniform sampling with replacement (Theorem 11 in Section 5.2). Then we present a more easily computable bound, in terms of just a few of the largest leverage scores (Section 5.3). It implies the following lower bound, not necessarily tight, on the number of samples.

-

Preview of Corollary 15 Given a failure probability , a tolerance , and a labeling of leverage scores in non-increasing order,

To achieve the condition number bound , the number of rows from , sampled uniformly with replacement, should be at least

(2) where and .

We show (Section 5.4) that (2) is indeed tighter than (1). This is confirmed by numerical experiments (Section 5.5). The difference becomes more drastic for matrices with widely varying non-zero leverage scores, and can be as high as ten percent. Hence (Section 5.6), when it comes to lower bounds for the number of rows sampled uniformly with replacement, we recommend (2) over (1).

Algorithms for generating matrices with prescribed coherence and leverage scores (Section 6)

The purpose is to make it easy to investigate the efficiency of the sampling methods in Section 3, and test the tightness of the bounds in Sections 4 and 5.

To this end we present algorithms for generating matrices with prescribed leverage scores and coherence (Section 6.1), and for generating particular leverage score distributions with prescribed coherence (Section 6.2). Furthermore we present two classes of structured matrices with prescribed coherence that are easy and fast to generate (Section 6.3). The basis for the algorithms is the following majorization result.

-

Preview of Theorem 25 Given integers and a vector with elements that satisfy and , there exists a matrix with orthonormal columns that has leverage scores , , and coherence .

Bound for two-norms of diagonally scaled matrices (Section B)

The bound (2) is based on a special case of the following general bound for the two-norm of diagonally scaled matrices.

-

Preview of Theorem 22 Let be a matrix with and largest squared row norm . Let be a non-negative diagonal matrix, and a labeling of diagonal elements in non-increasing order,

If , then either

or

Matlab toolbox

In order to perform the experiments in this paper, we developed a Matlab toolbox kappaSQ_v3 with a user-friendly interface [17]. The toolbox contains implementations of the three random sampling methods in Section 3, the matrix generation algorithms in Section 6, the bounds in Sections 4 and 5, and a variety of other condition number bounds. It also allows the user to input her/his own matrices.

Proofs (Sections A, B and C)

All proofs, except those for Sections 2 and 3, have been relegated to these three sections, which form the appendix.

Section A contains the proofs for Sections 4 and 5, which are based on two matrix concentration inequalities: A Chernoff bound (Section A.1), and a Bernstein bound (Section A.4).

Future work (Section 7)

We list a few issues that suggest themselves immediately as a follow up to this paper.

1.3 Literature

Existing randomized least squares methods are based on randomized projections. This means, conceptually they multiply by a random matrix , and then sample a few rows from .

The algorithms in [4, 10, 11] solve a smaller sampled problem by a direct method. Like Blendenpik [1], the algorithm in [24] computes a preconditioner from the QR factorization of a sampled submatrix, but then solves the preconditioned problem by applying the conjugate gradient method to the normal equations. The parallel solver LSRN [20] computes a preconditioner from the SVD of a sampled submatrix, and then solves the preconditioned problem with an iterative method. This solver applies to general matrices rather than just those of full column rank.

1.4 Notation

The norm denotes the Euclidean two-norm, and the two-norm condition number with respect to inversion of a real matrix with is denoted by , where is the Moore-Penrose inverse. The identity matrix is , and its columns are the canonical vectors , .

The probability of an event is denoted by , and the expected value of a random variable is denoted by .

2 The Blendenpik algorithm, and coherence

We describe the Blendenpik algorithm for solving least squares problems (Section 2.1), and present the notion of coherence (Section 2.2).

2.1 Algorithm

The Blendenpik algorithm [1, Algorithm 1] solves full column rank least squares problems with the Krylov space method LSQR [22] and a randomized preconditioner. Algorithm 1 presents a conceptual sketch of Blendenpik. The subscript “” denotes quantities associated with the sampled matrix.

The matrix is the product of a random diagonal matrix with entries, and a unitary transform, such as a Walsh Hadamard transform, or a discrete Fourier, Hartley or cosine transform [1, Section 3.2]. The transformed matrix is with and .

The sampling matrix selects rows from the transformed matrix . We discuss different types of sampling matrices in Section 3. The sampled matrix has a thin QR decomposition where is with orthonormal columns and is upper triangular.

The basis for the analysis is the thin QR decomposition , where is with orthonormal columns and is upper triangular. This QR decomposition is not computed. The next result links the condition number of the preconditioned matrix to that of the matrix , see also [1, Section 3.1] and [24, Theorem 1].

Lemma 1.

With the notation in Algorithm 1, if , then

Proof.

From and the fact that the 2-norm is invariant under premultiplication by matrices with orthonormal columns, it follows that

∎

In Sections 4 and 5 we derive bounds for the condition number of the preconditioned matrix, . Our bounds are tighter than those in [1, Theorem 3.2], because they have all constants explicitly specified, and apply to three different sampling strategies. Since Lemma 1 implies , we state the bounds for only. An important ingredient in these bounds is the coherence of .

2.2 Coherence

Coherence gives information about the localization or “uniformity” of the elements in an orthonormal basis. The more general concept of mutual coherence between two orthonormal bases was introduced in [8, §VII], in the context of signal processing and computational harmonic analysis, to describe a condition for the existence of sparse representations of signals. What we use here is a special case, and can be viewed as a measure for how close an orthonormal basis is to sharing a vector with a canonical basis.

Definition 2 (Definition 3.1 in [1], Definition 1.2 in [5]).

Let be a real matrix with orthonormal columns, , then the coherence of is

If the columns of are an orthonormal basis for the column space of a matrix , then the coherence of is .

The second part of Definition 2 emphasizes that coherence is really a property of the column space, hence basis-independent. In other words, if , where is a real orthogonal matrix, then and have the same coherence.

The range for coherence is . If is a submatrix of the Hadamard matrix, then . If a column of is a canonical vector, then . Hence an orthonormal basis has high coherence if it shares a vector with a canonical basis.

3 Sampling Methods

We present three different types of sampling methods: Sampling without replacement (Section 3.1), sampling with replacement (Section 3.2), and Bernoulli sampling (Section 3.3). We show that Bernoulli sampling can be viewed as a form of sampling without replacement (Section 3.4). The numerical experiments illustrate that there is little difference among the three methods for small to moderate amounts of sampling (Section 3.5). Hence we recommend sampling with replacement for Algorithm 1 (Section 3.6).

The sampling matrices in all three methods are scaled so that is an unbiased estimator of the identity matrix.

3.1 Sampling without replacement

The obvious sampling strategy, in Algorithm 1, picks the requested number of rows, so that the sampling matrix is just a scaled submatrix of a permutation matrix.

Uniform sampling without replacement can be implemented via random permutations333We thank an anonymous reviewer for this advice.. A permutation of the integers is a random permutation, if it is equally likely to be one of possible permutations [21, pages 41 and 48].

The following lemma presents the probability that sampling without replacement picks a particular row.

Lemma 3.

If Algorithm 1 samples out of indices, then the probability that a particular index is picked equals .

Proof.

The probability that some index, say , is not sampled in the first trial is . Now there are only indices left. So the probability that index is not sampled in the second trial is . Repeating this argument shows that with probability index is not sampled in trials.

The complementary event, the probability that index is sampled, equals . ∎

3.2 Sampling with replacement

This is the sampling strategy that appears to be analyzed in [1]. It samples exactly the requested number of rows, but with replacement, which means a row may be sampled more than once. Algorithm 2 is the same as the EXACTLY(c) algorithm [11, Algorithm 3] with uniform probabilities, which is also used in the BasicMatrixMultiplication Algorithm [9, Fig. 2].

3.3 Bernoulli sampling

The sampling strategy in Algorithm 3 is implemented in Blendenpik [1, Algorithm 1]. Following [13, Section A], we use the term Bernoulli sampling, because the strategy treats each row as an independent, identically distributed Bernoulli random variable. Each row is either sampled or not, with the same probability for each row. Algorithm 3 produces a square matrix – in contrast to Algorithms 1 and 2, which produce matrices.

The number of sampled rows, which is equal to the number of non-zero diagonal elements in , is not known a priori, but the expected number of sampled rows is . The lemma below shows that the actual number of rows picked by Bernoulli sampling is characterized by a binomial distribution [25, Section 2.2.2].

Lemma 4.

If Algorithm 3 samples from indices with probability , then the probability that it picks exactly indices equals .

Proof.

Determining the diagonal elements of the sampling matrix in Algorithm 3 can be viewed as performing independent trials, where trial is a success () with probability , and a failure () with probability . The probability of successes is given by the binomial distribution . ∎

3.4 Relating Bernoulli sampling and sampling without replacement

We show that Bernoulli sampling (Algorithm 3) is the same as first determining the number of samples with a binomial distribution (motivated by Lemma 4), and then sampling without replacement (Algorithm 1). This is described in Algorithm 4 below.

Lemma 5.

The probability that Algorithm 4 picks a particular index equals .

Proof.

Proof.

The probability that Algorithm 3 samples indices is equal to .

We show that the same is true for Algorithm 4. The choice of the sampling distribution in Algorithm 4 implies that it samples indices with probability . Since there are ways to sample out of indices, the probbility that the particular index set is picked, given that indices are being sampled is . Thus, the probability that Algorithm 4 picks indices equals

∎

3.5 Numerical experiments

We present two representative comparisons of the three sampling strategies, with two plots for each strategy: The condition numbers of full-rank sampled matrices , and the failure percentage, that is the percentage of sampled matrices that are numerically rank deficient (as determined by the Matlab command rank).

The experiments are limited to very tall and skinny matrices (with many more rows than columns, ), because that’s when the sampling strategies are most efficient. In particular, since is required for to have full column rank, sampling methods are inefficient when is not much smaller than , in which case a deterministic algorithm would be preferable.

Experimental setup

The matrices with orthonormal columns have rows and columns. The condition numbers and failure percentages are plotted against various sampling amounts , with 30 runs for each . For the failure percentages we display only those sampling amounts that give rise to rank-deficient matrices, in these particular 30 runs. For Algorithm 3 the horizontal axis represents the numerator in the probability, that is, the expected number of sampled rows. All three strategies sample from the same matrix.

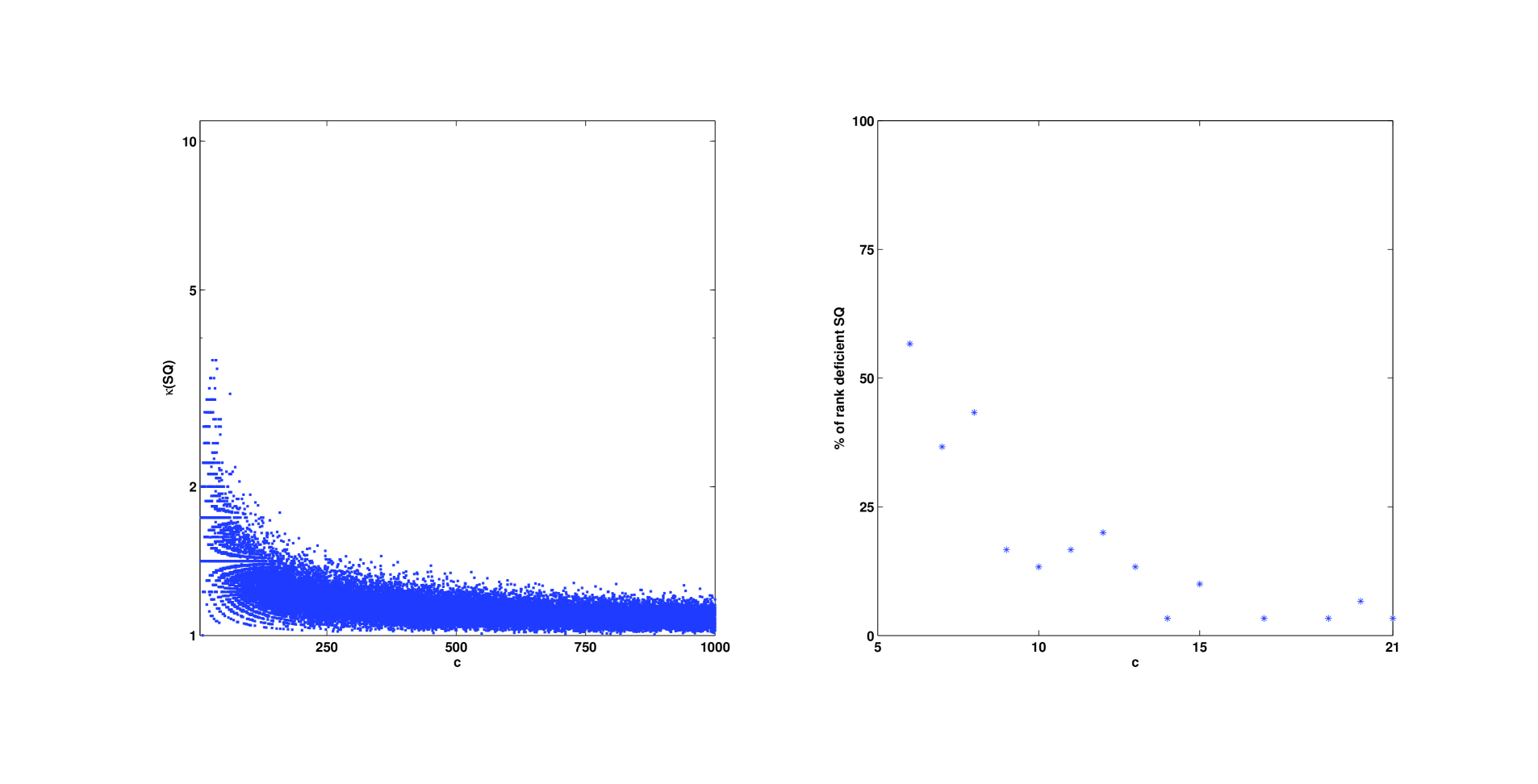

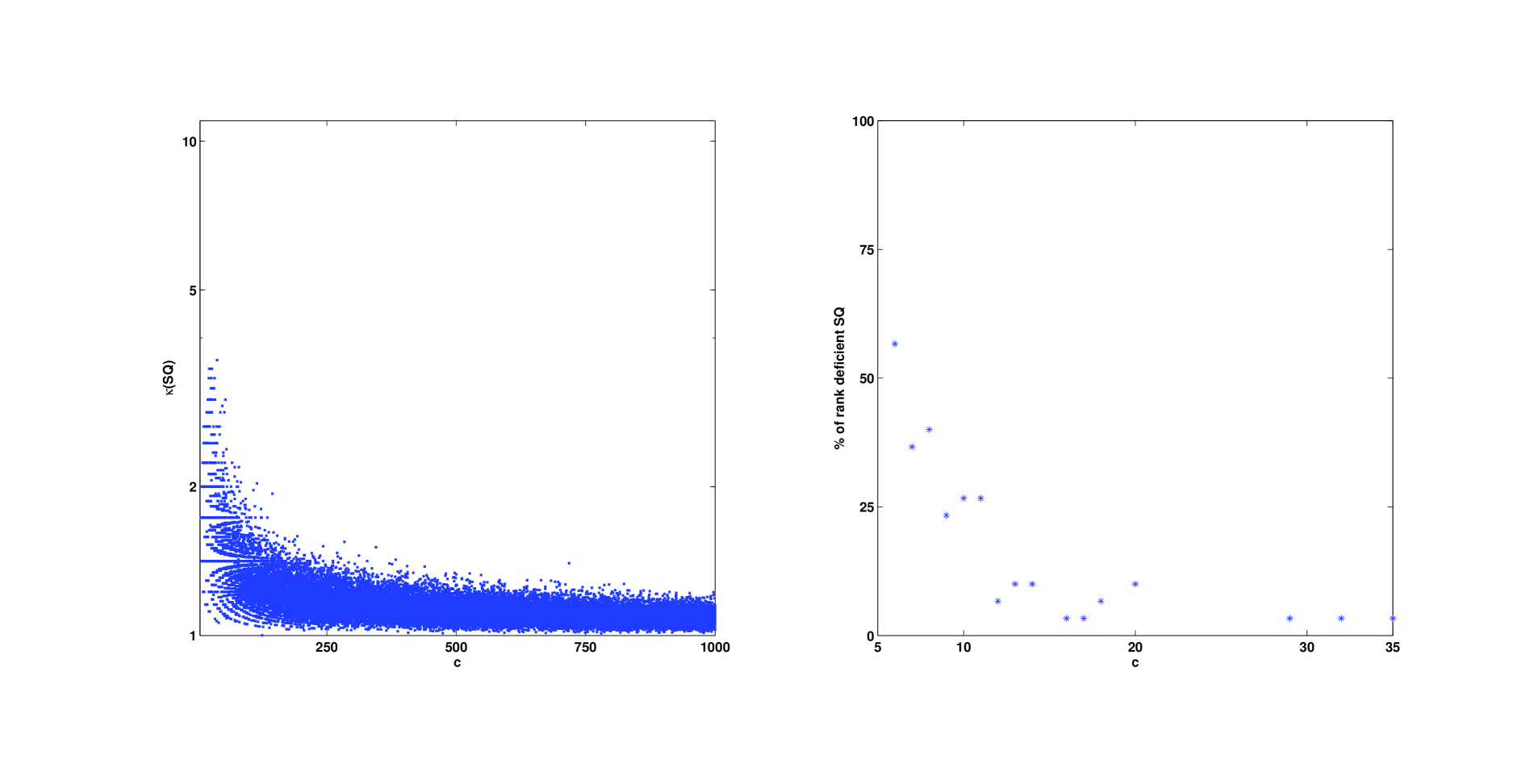

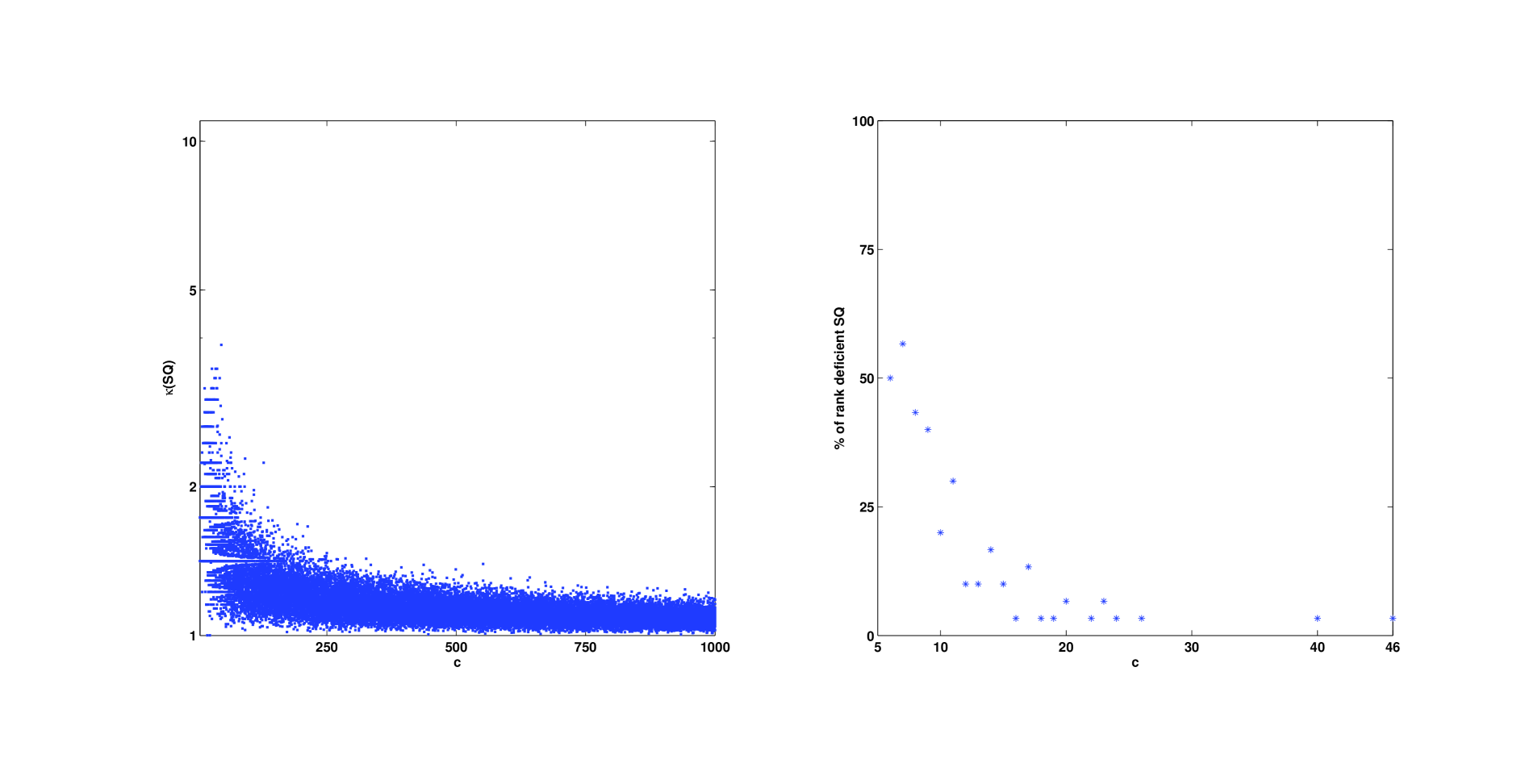

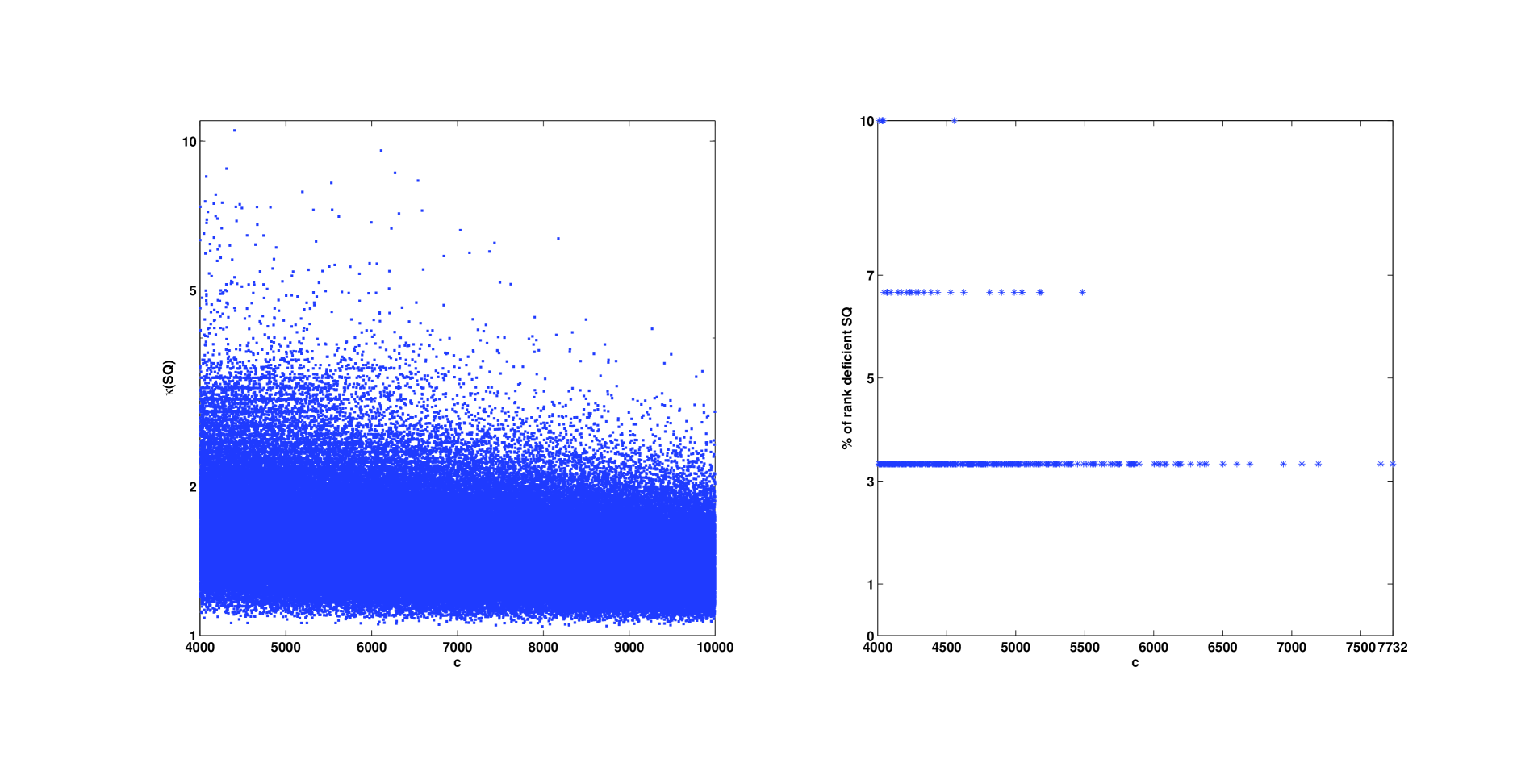

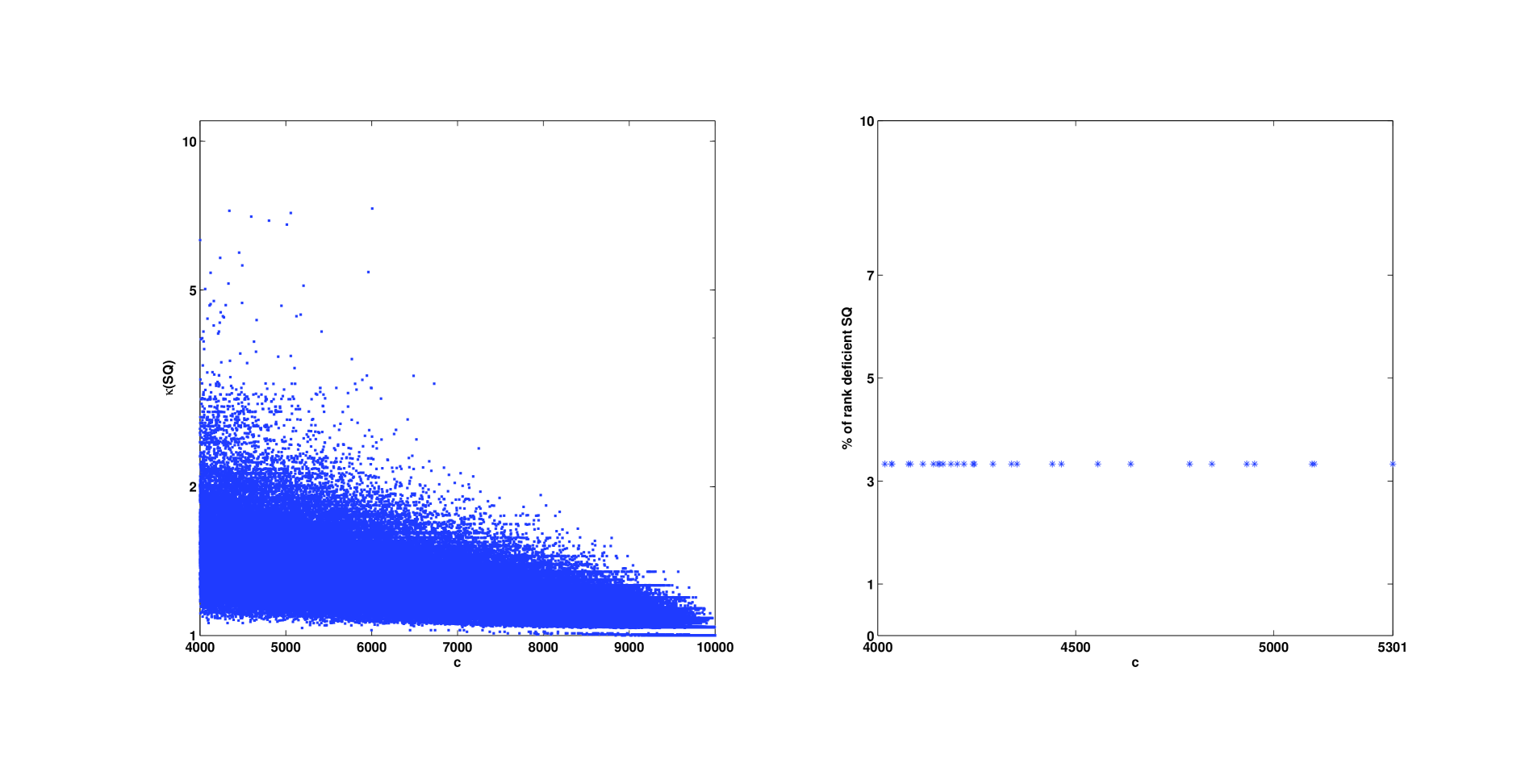

We consider two different types of matrices: Matrices with low coherence in Figure 1; and matrices with higher coherence and many zero rows in Figure 2. Our numerical experiments indicate that these coherence values are representative, in the sense that different values of coherence would not produce any other interesting effects.

(a) Algorithm 1: Sampling without replacement

(b) Algorithm 2: Sampling with replacement

(c) Algorithm 3: Bernoulli sampling

Figure 1

Shown are condition numbers and percentage of rank deficient matrices for a matrix with low coherence generated by Algorithm 2. At most 10 percent of the rows are sampled. The three strategies exhibit almost identical behavior: The sampled matrices of full rank are very well conditioned, with . Numerically rank-deficient matrices occur only for sampling amounts .

(a) Algorithm 1: Sampling without replacement

(b) Algorithm 2: Sampling with replacement

(c) Algorithm 3: Bernoulli sampling

Figure 2

Shown are condition numbers and percentage of rank deficient matrices for a matrix , generated by Algorithm 3, with coherence and many zero rows. The number of sampled rows ranges from to . The sampled matrices of full rank are very well conditioned, with . Even for , as many 10 percent of the sampled matrices can still be rank-deficient. All three algorithms have to sample more than half of the rows of in order to always produce matrices with full column rank. Specifically in these particular runs, Algorithms 1 and 3 need to sample and rows, respectively, while Algorithm 1 needs .

Note that the condition numbers of matrices from Algorithms 1 and 3 approach 1 as more and more rows are sampled. This is because no row is sampled more than once; and for all rows are sampled.

Again, the three strategies exhibit almost identical behavior: The sampled matrices of full rank are very well conditioned, with . However, due to the higher coherence, numerically rank-deficient matrices occur more frequently.

3.6 Conclusions for Section 3

The numerical experiments illustrate that the three sampling strategies behave almost identically, in particular for small to moderate sampling amounts, and that sampled matrices of full rank tend to be very well-conditioned444We have not been able to show rigorously why the condition numbers tend to be less than 10.. Furthermore, Section 3.4 shows that Bernoulli sampling can be viewed as a form of sampling without replacement, and the numerical experiments confirm the similarity in behavior.

4 Condition number bounds based on coherence

We derive bounds for the condition numbers of matrices produced by the sampling strategies in section 3, in terms of coherence. These bounds are based on a specific concentration inequality and imply a, not necessarily tight, lower bound for the number of sampled rows (Section 4.1). Numerical experiments illustrate that the bounds are informative (Section 4.2). We end this section by summarizing the main features of the bounds (Section 4.3).

4.1 Bounds

We show that the three sampling strategies in Section 3 all have the same condition number bound, in terms of coherence.

Theorem 7 below is based on a matrix Chernoff concentration inequality (Section A.1). We chose this particular inequality because extensive numerical experiments with our Matlab toolbox kappaSQ_v3 [17] suggest that it tends to produce the tightest bound.

Theorem 7.

Since for , Theorem 7 implies that the sampling strategies in Section 3 are more likely to produce full-rank matrices as the number of sampled rows increases. Furthermore, for a given total number of rows , matrices with fewer columns and lower coherence are more likely to give rise to sampled matrices that have full rank.

Theorem 7 implies the following lower bound on the number of samples, but we make no claims about the tightness of this bound.

Corollary 8.

Proof.

See Section A.3. ∎

Corollary 8 implies that the sampling strategies in Section 3 should sample at least rows to produce a full rank, well-conditioned matrix. In particular, if has minimal coherence , then Corollary 8 implies that the number of sampled rows should be at least

| (3) |

that is .

To achieve with probability at least .99 requires that the number of sampled rows be at least

| (4) |

Here we chose , so that the condition number bound equals .

Remark 9.

Theorem 7 is informative only for sufficiently low coherence values.

4.2 Numerical experiments

We compare the bound for the condition numbers of the sampled matrices (Theorem 7) with the true condition numbers of matrices produced by sampling with replacement (Algorithm 2).

There are several reasons why it suffices to consider only a single sampling strategy: The three sampling methods all have the same bound (Theorem 7); Bernoulli sampling is a form of sampling without replacement (Section 3.4); and all three sampling methods exhibit very similar behavior for matrices of low coherence (Sections 3.5 and 3.6). Furthermore, this allows a clean comparison with the bounds in Section 5 which apply only to Algorithm 2.

Experimental setup

The matrices with orthonormal columns have rows and columns. The left panels in Figure 3 show the condition numbers of the full-rank sampled matrices produced by Algorithm 2 against different sampling amounts , with 30 runs for each . The right panels in Figure 3 show the percentage of rank deficient matrices against different sampling amounts . We display only those sampling amounts that give rise to rank-deficient matrices, in these particular 30 runs.

The left panels in Figure 3 also show the condition number bound from Theorem 7. For each value of , we obtain as the solution of the nonlinear equation associated with Theorem 7 and defined as

We impose the stringent requirement of , corresponding to a 99 percent success probability. Since an explicit expression seems out of reach, we use unconstrained nonlinear optimization (a Nelder-Mead simplex direct search) to solve . This is done in Matlab with a code equivalent to

where fminsearch starts at the point 0, and terminates when . If then is plotted, otherwise nothing is plotted.

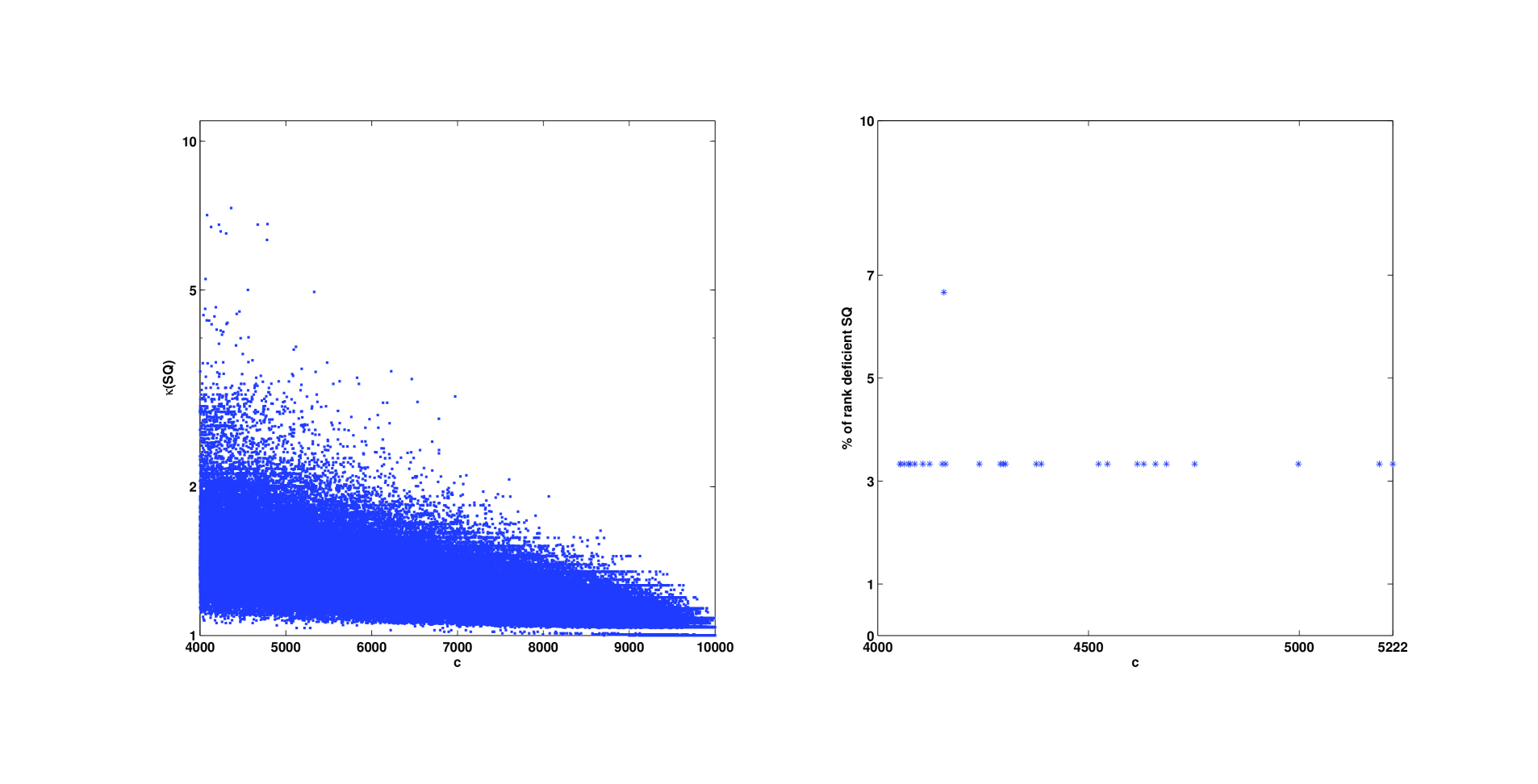

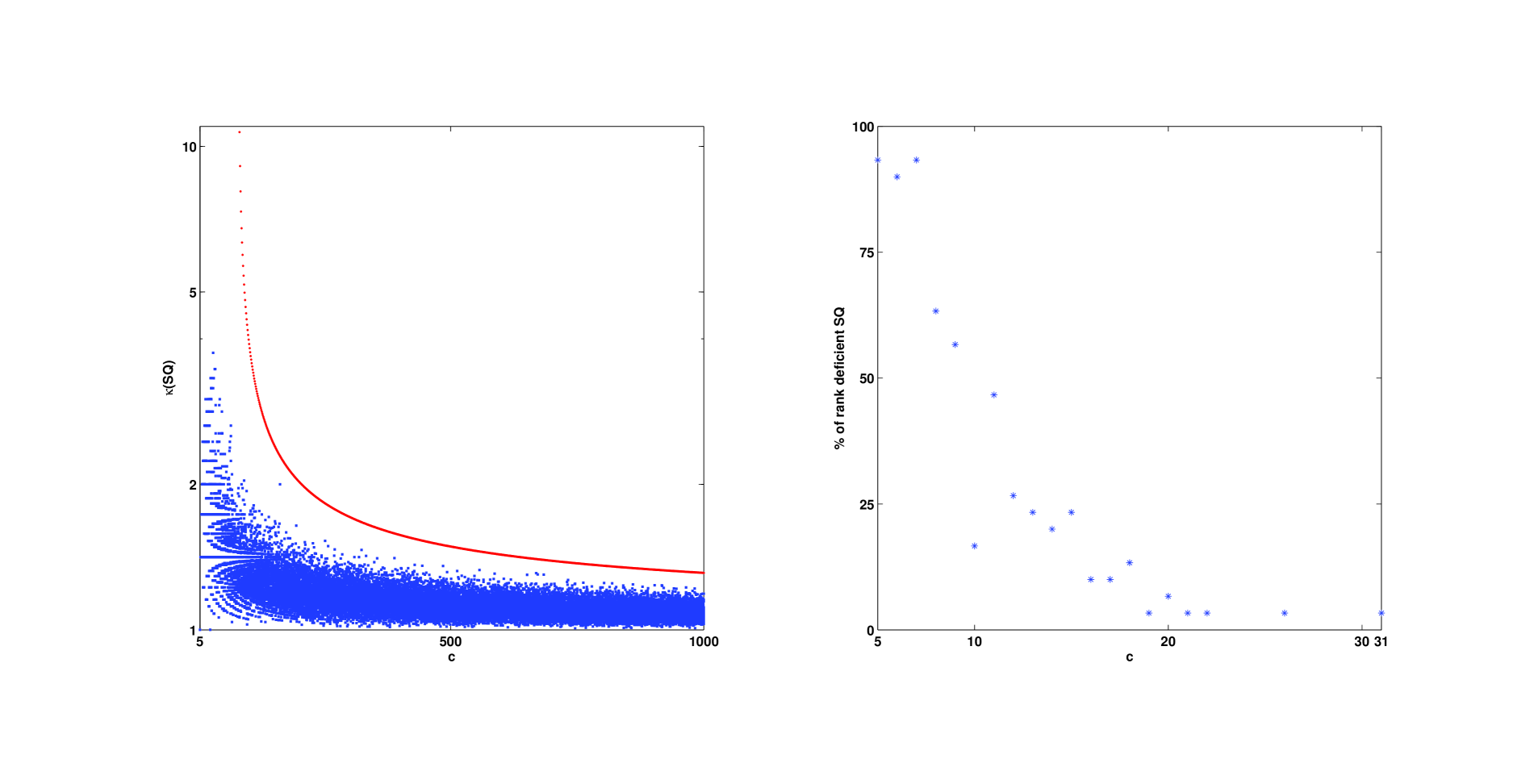

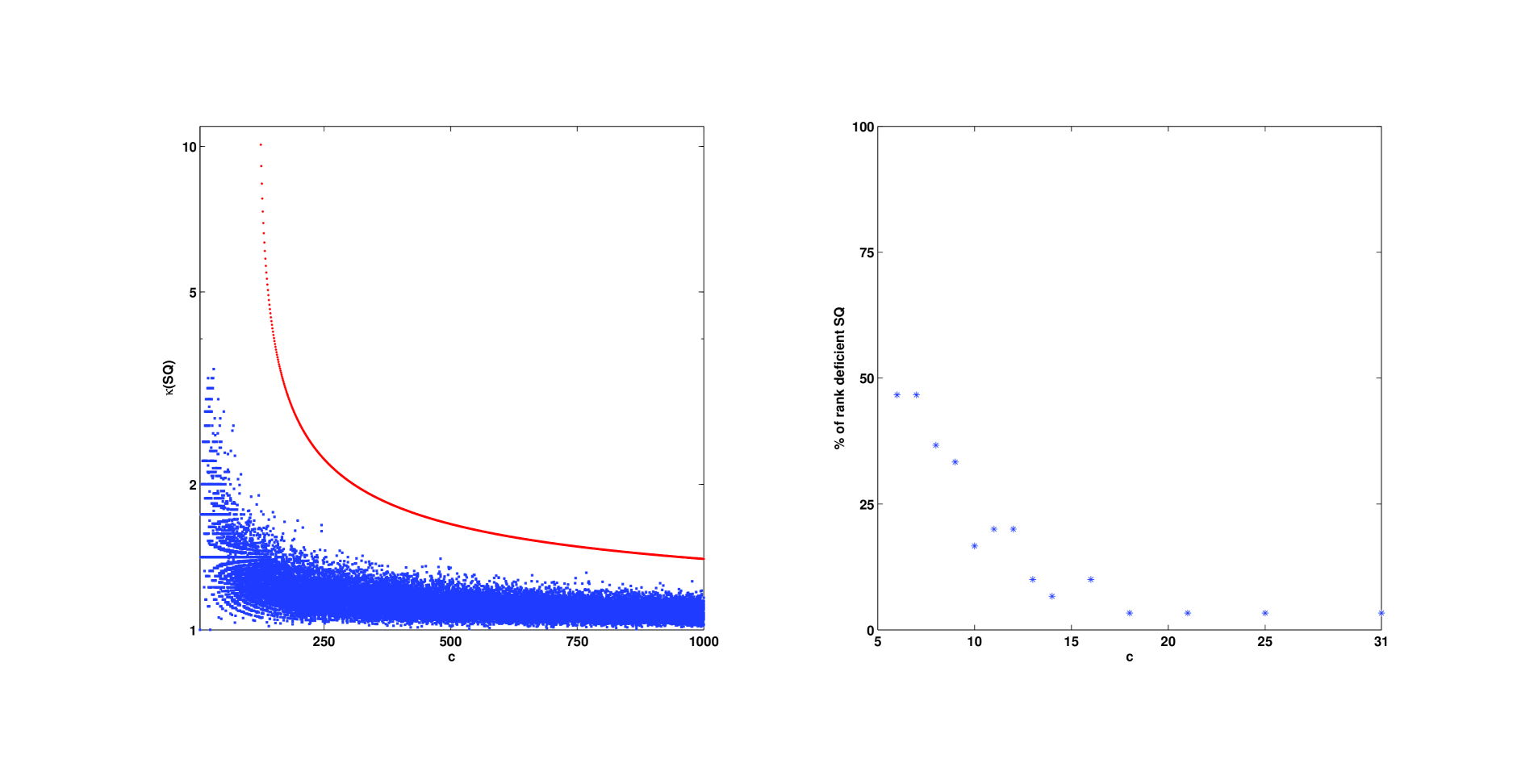

As explained in Remark 9, Theorem 7 is not informative for higher coherence values, so we consider matrices with the following properties: Minimal coherence in Figure 3(a); low coherence in Figure 3(b); slightly higher coherence with many zero rows in Figure 3(c). The matrices for Figures 3(a) and 3(b) were generated with Algorithm 2, while the matrix for Figure 3(c) was generated with Algorithm 3.

Figure 3

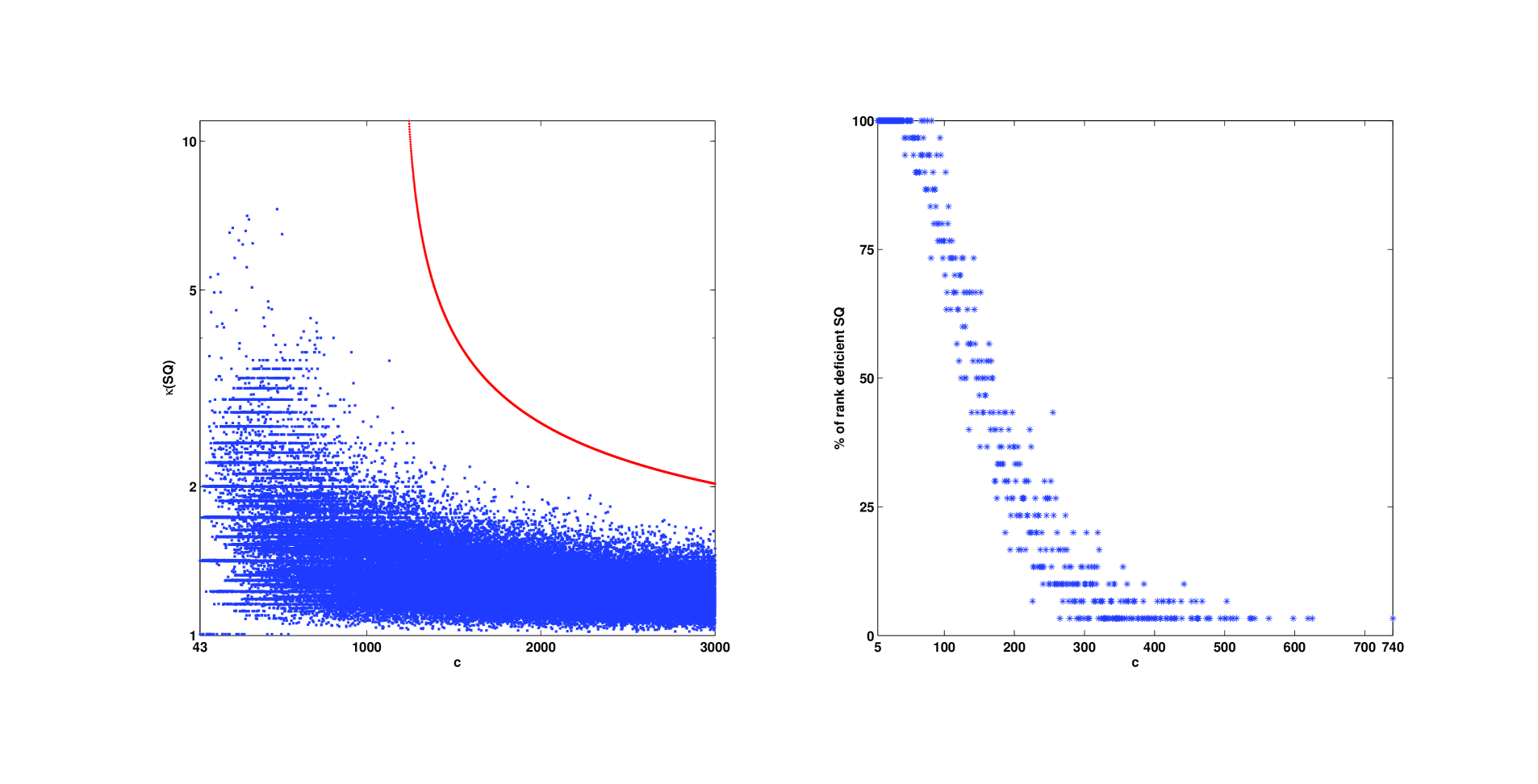

The left panels illustrate that Theorem 7, constrained to a 99 percent success probability, correctly predicts the magnitude of the condition numbers, i.e. . Hence Theorem 7 provides informative qualitative bounds for matrices with very low coherence, as well as for matrices with slightly higher coherence and many zero rows.

(a) has minimal coherence . Sampling amounts are .

(b) has low coherence . Sampling amounts are .

(c) has slightly higher coherence and many zero rows. Sampling sampling amounts are .

Table 1

This is a comparison of the numerical experiments in Figure 3 with the bounds from Theorem 7 and Corollary 8, both restricted to a 99 percent success probability.

The third column depicts the highest values of for which a rank-deficient matrix occurs, during these particular 30 runs. It should be kept in mind that these values are highly dependent on the particular sampling runs. This column is to be compared to the fourth column which contains the lowest values of where Theorem 7 starts to apply. Although there is a gap between the occurrence of the last rank deficiency and the onset of Theorem 7, the values have qualitatively the same order of magnitude.

The rightmost column in Table 1 contains the values of the lower bound (4), and is to be compared to the column with the starting values for Theorem 7. Although (4) is weaker than Theorem 7, its values are close to the starting values of Theorem 7, especially for lower coherence. Hence, the lower bound (4) captures the correct magnitude of the sampling amounts where Theorem starts to become informative.

4.3 Conclusions for Section 4

-

1.

They are non-asymptotic bounds, where all constants have explicit numerical values, hence they are tighter than the bounds in [1, Theorem 3.2].

-

2.

They apply to three different sampling methods.

-

3.

They imply a lower bound, of , on the required number of sampled rows. Although we did not give a formal proof of tightness, numerical experiments illustrate that sampling only the required number of rows implied by the bound is realistic. numerical experiments illustrate that the bound is realistic.

-

4.

Even under the stringent requirement of a 99 percent success probability, they are informative for matrices of small dimension because they correctly predict the magnitude of the condition numbers for the sampled matrices.

Note that the bounds in Theorem 7 and Corollary 8 are informative only for matrices that are tall and skinny () and have low coherence. The restriction to tall and skinny matrices is not an imposition, because it is required for the effectiveness of the sampling strategies, see Section 3.5.

In the next section we try to relax the restriction to low coherence matrices, by more thoroughly exploiting the information available from the row norms of .

5 Condition number bounds based on leverage scores, for uniform sampling with replacement

The goal is to tighten Theorem 7 by making use of all the row norms of , instead of just the largest one. To this end we introduce leverage scores (Section 5.1), which are the squared row norms of . We use them to derive a bound for uniform sampling with replacement (Section 5.2), and for more easily computable versions of the bound (Section 5.3). Analytical (Section 5.4) and experimental (Section 5.5) comparisons demonstrate that the implied lower bound on the number of sampled rows is better than the coherence-based bounds in Section 4. A review with some reflection ends this section (Section 5.6).

5.1 Leverage scores

So-called statistical leverage scores were first introduced in 1978 by Hoaglin and Welsch [15] to detect outliers when computing regression diagnostics, see also [6, 29]. Mahoney and Drineas pioneered the use of leverage scores for importance sampling strategies in randomized matrix computations [19].

Specifically, if is a real matrix with , then the hat matrix

is the orthogonal projector onto the column space of , and its diagonal elements are called leverage scores [15, Section 2]. Hence, leverage scores are basis-independent. For our purposes, though, it suffices to define them in terms of a thin QR decomposition , so that the hat matrix can be expressed as .

Definition 10.

If is a matrix with , then its leverage scores are

The diagonal matrix of leverage scores is

Note that the coherence is the largest leverage score,

5.2 Bounds

The bound in Theorem 11 below involves leverage scores and is based on a matrix Bernstein concentration inequality (Section A.4), rather than on the matrix Chernoff concentration inequality (Section A.1) for Theorem 7. Although the Bernstein inequality may not always be as tight, we did not see how to insert leverage scores into the Chernoff inequality.

Theorem 11.

Let be a real matrix with , leverage scores , , and coherence . Let be a sampling matrix produced by Algorithm 2 with . For set

If , then with probability at least we have and

Like Theorem 7, Theorem 11 implies that sampling with replacement is more likely to produce full-rank matrices as the number of sampled rows increases. Furthermore, for a given total number of rows , matrices with fewer columns and lower coherence are more likely to yield sampled matrices that have full rank. The dependence of on is discussed below.

Remark 12.

The norm has simple and tight bounds in terms of the coherence,

| (5) |

The lower bound follows from and

which implies .

The bounds (5) are attained for extreme values of the coherence:

-

•

In case of minimal coherence for all , we have . Thus , and the upper bound is attained.

-

•

In case of maximal coherence , we have . Thus , and both, lower and upper bounds are attained.

5.3 Computable bounds

We present easily computable bounds for , based on coherence and several of the largest leverage scores.

To this end, we use a labeling of the leverage scores in non-increasing order,

Corollary 13.

Proof.

See Section B.2. ∎

The number of large leverage scores appearing in Corollary 13 depends on the coherence: Few leverage scores for high coherence, but more for low coherence. Henceforth we will use the approximation from Corollary 13 instead of the true value , for two reasons: First, numerical experiments show that the approximation tends to be very accurate. Second, the approximation is convenient, because it requires only a leverage score distribution rather than a full-fledged matrix .

Remark 14.

Corollary 13 is tight for the extreme cases of minimal and maximal coherence.

Inserting this approximation for into the expression for in Theorem 11 yields a, not necessarily tight, lower bound on the number of samples.

Corollary 15.

Under the assumptions of Theorem 11,

where , samples are sufficient to achieve with probability at least .

In particular, if has minimal coherence , then Corollary 15 implies that the number of sampled rows should be at least

This is the same as the coherence-based lower bound (3).

To achieve with probability at least .99 requires that the number of sampled rows be at least

| (6) |

5.4 Analytical comparison of the bounds in Sections 4.1 and 5.2

An analytical comparison between Theorems 7 and 11 is not obvious, because they are based on different concentration inequalities. Instead we compare the implied lower bounds for the number of sampled rows, and show that the leverage-score based bound in Corollary 15 is at least as tight as the coherence-based bound in Corollary 8.

Corollary 16.

Proof.

See Section B.3. ∎

5.5 Experimental comparison of the bounds in Sections 4.1 and 5.2

We present numerical experiments to compare the lower bounds for the number of sampled rows in Corollaries 8 and 15, for different values of coherence. This gives quantitative insight into the comparison in Corollary 16, and illustrates the reduction in the number of sampled rows from Corollary 15, as compared to Corollary 8.

Experimental setup

Table 2

This table shows the lower bounds on the number of sampled rows, for a leverage score distribution generated with Algorithm 2 that consists of one large leverage score, equal to the coherence, and all remaining leverage scores being non-zero and identical. The bounds, as well as the approximation to , are displayed for eight different values of coherence, ranging from minimal coherence to .

Table 2 illustrates that with increasing coherence, the number of sampled rows implied by Corollary 15 is only about 20 percent of that from Corollary 8. This is because increases much more slowly than . For instance, when .

| 1 | 5 | 10 | 15 | 20 | 25 | 50 | 100 | |

|---|---|---|---|---|---|---|---|---|

| Cor. 8 | 108 | 540 | 1,079 | 1,618 | 2,157 | 2,697 | 5,393 | 10,786 |

| Cor. 15 | 96 | 191 | 310 | 432 | 556 | 682 | 1,3343 | 2,777 |

| 1.00 | 1.01 | 1.04 | 1.10 | 1.19 | 1.30 | 2.22 | 9.95 |

Table 3

This table shows the lower bounds on the number of sampled rows. The corresponding leverage score distribution is generated with Algorithm 3 and consists of as many zeros as possible. All non-zero leverage scores, expect possibly one, are equal to the coherence , so that . The bounds are displayed for eight different values of coherence, ranging from minimal coherence to .

The bounds for Corollary 8 are the same as in Table 2, because the coherence values are the same. Since , the difference between Corollaries 8 and 15 is not as drastic as in Table 2, yet it increases with increasing coherence. For , Corollary 15 remain informative, while Corollary 8 does not.

| 1 | 5 | 10 | 15 | 20 | 25 | 50 | 100 | |

|---|---|---|---|---|---|---|---|---|

| Cor. 8 | 108 | 540 | 1,079 | 1,618 | 2,157 | 2,697 | 5,393 | 10,787 |

| Cor. 15 | 96 | 477 | 954 | 1,431 | 1,908 | 2,385 | 4,770 | 9,539 |

5.6 Conclusions for Section 5

The goal of this section was to derive condition number bounds that are based on leverage scores rather than just coherence, when rows are sampled uniformly with replacement (Algorithm 2). Corollary 16 and the numerical experiments illustrate that the lower bound on the number of sampled rows implied by Corollary 15 is smaller than that from Corollary 8.

Although the coherence based bound in Theorem 7 is derived from a stronger concentration inequality than the one for Theorem 11, this difference disappears in the weakening necessary to obtain lower bounds for the amount of sampling. Even in cases when the leverage score measure is the same as the coherence, Corollary 15 still retains a small advantage, which can increase with increasing coherence. Hence Corollary 15 tends to remain informative for larger values of coherence, even when Corollary 8 fails.

The difference in implied sampling amounts becomes more drastic in the presence widely varying non-zero leverage scores, and can be as high as ten percent. This is because the coherence-based bound in Corollary 8 cannot take advantage of the distribution of the leverage scores.

Hence, when it comes to lower bounds for the number of rows sampled uniformly with replacement, we recommend Corollary 15.

6 Algorithms for generating matrices with prescribed coherence and leverage scores

In order to investigate the efficiency of the sampling methods in Section 3, and test the tightness of the bounds in Sections 4 and 5, we need to generate matrices with orthonormal columns that have prescribed leverage scores and coherence. The algorithms are implemented in the Matlab package kappa_SQ_v3 [17].

We present algorithms for generating matrices with prescribed leverage scores and coherence (Section 6.1), and for generating particular leverage score distributions with prescribed coherence (Section 6.2). Such distributions can then, in turn, serve as inputs for the algorithm in Section 6.1. Furthermore we present two classes of structured matrices with prescribed coherence that are easy and fast to generate (Section 6.3).

6.1 Matrices with prescribed leverage scores

We present an algorithm that generates matrices with orthonormal columns that have prescribed leverage scores. In Section C we prove an existence result to show that this is always possible.

Algorithm 1 is a transposed version of [7, Algorithm 3]. It repeatedly applies Givens rotations that rotate two rows and , and are computed from numerically stable expressions [7, section 3.1]. At most such rotations are necessary. Since each rotation affects only two rows, Algorithm 1 requires arithmetic operations.

6.2 Leverage score distributions with prescribed coherence

We present algorithms that generate leverage score distributions for prescribed coherence. The resulting distributions then serve as inputs for Algorithm 1. These particular leverage score distribution help to distinguish the effect of coherence, which is the largest leverage score, from that of the remaining leverage scores.

One large leverage score

Given a prescribed coherence , Algorithm 2 generates a distribution consisting of one large leverage score equal to and the remaining leverage scores being identical and non-zero.

In the special case of minimal coherence , Algorithm 2 generates identical leverages equal to , which is the only possible leverage score distribution in this case.

Many zero leverage scores

Given a prescribed coherence, Algorithm 3 generates a distribution with as many zero leverage scores as possible. This serves as an “adversarial” distribution for the sampling algorithms in Section 3.

Given a prescribed coherence , Algorithm 3 first determines the smallest number of rows that can realize this coherence, sets leverage scores equal to , assigns another leverage score to to take up the possibly non-zero slack, and sets the remaining leverage scores to zero.

6.3 Structured matrices with prescribed coherence

We present two classes of structured matrices with orthonormal columns that have prescribed coherence. Although the structure puts constraints on the matrix dimensions, the generation of these matrices is faster than running Algorithm 1. Note that the matrices produced by Algorithm 1 also have structure, but it is not easily characterized.

Stacks of diagonal matrices

Given matrix dimensions and , where is an integer, and prescribed coherence . The matrix below has orthonormal columns and coherence , and consists of stacks of diagonal matrices,

Matrices with Hadamard structure

Given matrix dimensions and , where and is also a power of two, and prescribed coherence . The matrix

has orthonormal columns and coherence , and is defined recursively as follows. For

define square matrices of dimension and square matrices of dimension as follows,

Note that only the final matrix has orthonormal columns and coherence while, in general, the intermediate matrices and do not. We omit the messy induction proof, because it does not provide much insight.

7 Future work

We have investigated three strategies for uniform sampling of rows from matrices with orthonormal columns: Without replacement, with replacement, and Bernoulli sampling. We derived bounds on the condition numbers of the sampled matrices, in terms of coherence and leverage scores. Numerical experiments confirm that the bounds are realistic, even for high success probabilities and matrices with small dimensions.

The following work still needs to be done.

-

•

Conversion of the kappa_SQ_v3 MATLAB toolbox from a research code to a robust, flexible, and user-friendly GUI that facilitates reproducible research in the randomized algorithms community.

- •

- •

-

•

Determination of a statistically significant number of runs for each sampling amount , for two purposes:

-

1.

To assert, within a specific confidence interval, bounds on the condition numbers of the actually sampled matrices.

- 2.

-

1.

Acknowledgements

We are very grateful to John Holodnak, Petros Drineas and two anonymous reviewers for reading our paper so carefully and for providing many helpful suggestions.

Appendix A Proofs for Sections 4 and 5.2

For the coherence-based bounds in Section 4 we first present a matrix concentration inequality (Section A.1), and then the proofs of Theorem 7 (Section A.2) and Corollary 8 (Section A.3).

For the bound based on leverage scores in Section 5.2, we first present a matrix concentration inequality (Section A.4), and then the proof of Theorem 11 (Section A.5).

A.1 Matrix Chernoff Concentration inequality

Denote the eigenvalues of a Hermitian matrix by , and the smallest and largest eigenvalues by and , respectively.

Theorem 17 (Corollary 5.2 in [28]).

Let be a finite number of independent random Hermitian positive semidefinite matrices with . Define

and . Then for any

and for any

A.2 Proof of Theorem 7

We present a separate proof for each sampling method.

Algorithm 1: Sampling without replacement

The proof follows directly from [27, Lemma 3.4].

Algorithm 2: Sampling with replacement

Algorithm 3: Bernoulli sampling

The proof is similar to the one above, and a special case of [12, Theorem 6.1].

A.3 Proof of Corollary 8

First we simplify the bound in Theorem 7 based on the inequality for . This implies for Theorem 7 that

Solving for gives

If we can show that , then the above lower bound for definitely holds if

To show for , apply the definition so that . Expand into the power series . For this yields , where

since each summand is positive for . Thus for we obtain

A.4 Matrix Bernstein concentration inequality

The matrix concentration inequality below is the basis for Theorem 11. It is a version specialized to square matrices of [23, Theorem 4]. In numerical experiments we found it to be tighter than [11, Theorem 4] and the Frobenius norm bound [9, Theorem 2].

Theorem 18 (Theorem 4 in [23]).

Let be independent random matrices with , . Let and . Then for any

A.5 Proof of Theorem 11

The proof is similar to that of [2, Lemma 3]. Represent the outcome of uniform sampling with replacement in Algorithm 2 by , where are matrices, , with expected value

Thus, the zero mean versions are . To apply Theorem [23, Theorem 4] to the we need to verify that they fulfill the required conditions. First, by construction, , . Second, since and are symmetric positive semidefinite,

where the last inequality follows from the definition of , and . Hence we set . Third, since is symmetric,

From follows

| (7) |

Since , we obtain

Substituting this into (7) yields

Positive semi-definiteness gives

We set . Applying [23, Theorem 4] to

shows that with probability at least .

Appendix B Two-norm bound for scaled matrices, and proofs for Sections 5.3 and 5.4

We derive a bound for the two-norm of diagonally scaled matrices (Section B.1), which leads immediately to the proofs of Corollary 13 (Section B.2), and Corollary 16 (Section B.3).

B.1 Bound

We present two majorization bounds for Hadamard products of vectors (Lemmas 21 and 20), and use them to derive a bound for the two-norm of diagonally scaled matrices (Theorem 22).

Definition 19 (Definition 4.3.41 in [16]).

Let and be vectors with real elements. The elements, labelled in algebraically decreasing order, are and . The vector weakly majorizes the vector , if

The vector majorizes the vector , if weakly majorizes and also .

The first lemma follows from a stronger majorization inequality for functions that are monotone and lattice superadditive.

Lemma 20 (Theorem II.4.2 in [3]).

If and are vectors with non-negative elements, then

The second lemma is a variant of a well-known majorization result for Hadamard products of vectors [16, Lemma 4.3.51]. Since the version below is slightly different, we include a proof from first principles.

Lemma 21.

Let , and be vectors with non-negative elements. If weakly majorizes , then

Proof.

The following arguments hold for . Start out with the upper bound, and separate the last summand,

| (8) |

Re-writing the right sum and applying , , gives

Insert this into (8) and gather common terms,

where the second inequality follows from the majorization . ∎

Now we are ready to bound the two norm of a row scaled matrix , where is of full column rank, and is a non-negative diagonal matrix. The obvious bound is

| (9) |

However, the bound in Theorem 22 below, which incorporates the largest row norm of and several of the largest (in magnitude) diagonal elements of , turns out to be tighter.

Theorem 22.

Let be a real matrix with , smallest singular value , and largest squared row norm . If , then

Proof.

Let be a vector with and . Furthermore let , , be the elements of , so that .

Apply Lemma 20

Since and , , we can apply Lemma 20 with and , to obtain

Verify assumptions of Lemma 21

In order to apply Lemma 21 with

we need show that the assumptions are satisfied, meaning all vector elements are non-negative and the majorization condition holds. Clearly for and . This leaves . From follows that . The definition of implies , so that

Thus, all vector elements are non-negative.

To show the majorization condition, start with the Cauchy-Schwartz inequality,

This yields, regardless of whether or not,

Moreover, for ,

This gives the weak majorization condition , .

Apply Lemma 21

Since the assumptions of Lemma 21 are satisfied, we can conclude that . At last, substitute into this majorization relation the expressions for and . If , then

otherwise

∎

Corollary 23.

Let be a real matrix with , and coherence . If , then

Proof.

B.2 Proof of Corollary 13

Apply Corollary 23 with , , , and to prove the first inequality,

As for the second inequality, implies

If, in addition, is an integer, then and .

B.3 Proof of Corollary 16

Appendix C Existence of matrices with prescribed coherence and leverage scores

This section is the basis for Algorithm 1. We review a well-known majorization result (Theorem 24). We use it to show (Theorem 25) that, given prescribed matrix dimensions and leverage scores, there always exists a matrix with orthonormal columns that has the required dimensions and (squared) row norms equal to the leverage scores.

Our approach is again based on majorization, see Definition 19, and in particular on the fact that the eigenvalues of a real symmetric matrix majorize its diagonal elements.

Theorem 24 (Theorem 4.3.48 in [16]).

Let and be vectors with real elements and , respectively, . If majorizes , then there exists a real symmetric matrix with eigenvalues and diagonal elements , .

With the help of Theorem 24 we show that there exists a matrix with orthonormal columns that has prescribed leverage scores and coherence.

Theorem 25.

Given integers and with ; and a vector with elements that satisfy and . Then there exists a matrix with orthonormal columns that has leverage scores , , and coherence .

Proof.

Let be a vector with elements that satisfy for , and for . We are going to construct a matrix by applying Theorem 24 to and . To this end, we first need to show that majorizes .

Majorization

We distinguish the cases and .

- Case :

-

From follows

- Case :

-

From and follows

Hence

which means that weakly majorizes . Since also , we can conclude that majorizes .

Construction of

Theorem 24 implies that there exists a real symmetric matrix with eigenvalues and diagonal elements , . Since has eigenvalues equal to one, and all other eigenvalues equal to zero, it has an eigenvalue decomposition

where is a real orthogonal matrix, and has orthonormal columns. Therefore has leverage scores and coherence . ∎

References

- [1] H. Avron, P. Maymounkov, and S. Toledo, Blendenpik: Supercharging Lapack’s least-squares solver, SIAM J. Sci. Comput., 32 (2010), pp. 1217–1236.

- [2] L. Balzano, B. Recht, and R. Nowak, High-Dimensional Matched Subspace Detection When Data are Missing, 2011. arXiv:1002.0852v2.

- [3] R. Bhatia, Matrix Analysis, vol. 169, Springer, 1997.

- [4] C. Boutsidis and P. Drineas, Random projections for the nonnegative least-squares problem, Linear Algebra Appl., 431 (2009), pp. 760–771.

- [5] E. J. Candès and B. Recht, Exact Matrix Completion via Convex Optimization, Found. Comput. Math., 9 (2009), pp. 717–772.

- [6] S. Chatterjee and A. S. Hadi, Influential Observations, High Leverage Points, and Outliers in Linear Regression, Statist. Sci., 1 (1986), pp. 379–393.

- [7] I. S. Dhillon, R. W. Heath, M. A. Sustik, and J. A. Tropp, Generalized finite algorithms for constructing Hermitian matrices with prescribed diagonal and spectrum, SIAM J. Matrix Anal. Appl., 27 (2005), pp. 61–71.

- [8] D. L. Donoho and X. Huo, Uncertainty principles and ideal atomic decomposition, IEEE Trans. Inform. Theory, 47 (2001), pp. 2845–2862.

- [9] P. Drineas, R. Kannan, and M. W. Mahoney, Fast Monte Carlo Algorithms for Matrices. I. Approximating Matrix Multiplication, SIAM J. Comput., 36 (2006), pp. 132–157.

- [10] P. Drineas, M. W. Mahoney, and S. Muthukrishnan, Sampling algorithms for regression and applications, in Proc. 17th Ann. ACM-SIAM Symp. on Discrete Algorithms, New York, 2006, ACM, pp. 1127–1136.

- [11] P. Drineas, M. W. Mahoney, S. Muthukrishnan, and T. Sarlós, Faster Least Squares Approximation, Numer. Math., 117 (2011), pp. 219–249.

- [12] A. Gittens and J. A. Tropp, Tail Bounds for All Eigenvalues of a Sum of Random Matrices, 2011. arXiv:1104.4513.

- [13] D. Gross and V. Nesme, Note on Sampling without Replacement from a Finite Collection of Matrices, 2010. arXiv:1001.2738.

- [14] N. Halko, P. G. Martinsson, and J. A. Tropp, Finding Structure with Randomness: Probabilistic Algorithms for Constructing Approximate Matrix Decompositions, SIAM Rev., 53 (2011), pp. 217–288.

- [15] D. C. Hoaglin and R. E. Welsch, The Hat Matrix in Regression and ANOVA, Amer. Statist., 32 (1978), pp. 17–22.

- [16] R. A. Horn and C. R. Johnson, Matrix Analysis, Cambridge University Press, Cambridge, second ed., 2013.

- [17] I. Ipsen and T. Wentworth, kappaSQ_v3, 2013. http://www4.ncsu.edu/~ipsen/papers.html.

- [18] D. V. Lindley, The Bayesian approach, Scand. J. Statist., 5 (1978), pp. 1–26. With discussion.

- [19] M. W. Mahoney, Randomized Algorithms for Matrices and Data, Now Publishers Inc., 2011.

- [20] X. Meng, M. A. Saunders, and M. W. Mahoney, LSRN: A Parallel Iterative Solver for Strongly Over- or Under-determined Systems, 2011. arXiv:1109.5981v1.

- [21] M. Mitzenmacher and E. Upfal, Probability and Computing: Randomized Algorithms and Probabilistic Analysis, Cambridge University Press, New York, 2006.

- [22] C. C. Paige and M. A. Saunders, LSQR: An algorithm for sparse linear equations and sparse least squares, ACM Trans. Math. Software, 8 (1982), pp. 43–71.

- [23] B. Recht, A simpler Approach to Matrix Completion, J. Machine Learning, 12 (2011), pp. 3413–3430.

- [24] V. Rokhlin and M. Tygert, A fast randomized algorithm for overdetermined linear least-squares regression, Proc. Natl. Acad. Sci. USA, 105 (2008), pp. 13212–13217.

- [25] S. Ross, Introduction to Probability Models, Academic Press, Amsterdam, ninth ed., 2007.

- [26] A. Talwalkar and A. Rostamizadeh, Matrix Coherence and the Nyström Method, 2010. arXiv:1004.2008v1.

- [27] J. A. Tropp, Improved Analysis of the Subsampled Hadamard Transform, Adv. Adapt. Data Anal., 3 (2011), pp. 115–126.

- [28] , User-friendly tail bounds for sums of random matrices, Found. Comput. Math., (2011), pp. 1–46.

- [29] P. F. Velleman and R. E. Welsch, Efficient Computing of Regression Diagnostics, Amer. Statist., 35 (1981), pp. 234–242.