10.1080/10556788.2013.823544 \issn1029-4937 \issnp1055-6788 \jvol29 \jnum1 \jyear2014 \jmonth

Strict linear prices in non-convex European day-ahead

electricity markets

Abstract

The European power grid can be divided into several market areas where

the price of electricity is determined in a day-ahead auction. Market

participants can provide continuous hourly bid curves and

combinatorial bids with associated quantities given the prices. The

goal of our auction is to maximize the economic surplus of all participants

subject to quantity constraints and price constraints.

The price constraints ensure that no one incurs a loss. Only traders who

submitted a combinatorial bid might miss a not-realized profit.

The resulting problem is a large scale mathematical program with equilibrium

constraints (MPEC) and binary variables that cannot be solved

efficiently by standard solvers. We present an exact algorithm and

a fast heuristic for this type of problem. Both algorithms decompose

the MPEC into a master problem (a MIQP) and pricing subproblems (LPs).

The modeling technique and the algorithms are applicable to a wide

variety of combinatorial auctions that are based on mixed integer programs.

{classcode}

90C11; 90C33; 91A46; 91B15; 91B26.

keywords:

discrete optimization; MPEC; combinatorial auctions; strict linear prices; electricity markets.1 Introduction

In this article we present the market design that is currently in use by most of the European electricity exchanges. The underlying optimization problem is a welfare maximizing combinatorial auction subject to price constraints. For each tradable commodity a single price is determined to avoid the same commodity of having different prices to different parties. Even though the main focus of the paper will be on solving the underlying problem, we also explain why the market model evolved to its current state. Furthermore we will discuss the differences to unit commitment models used in the US.

1.1 Our contribution

We provide a precise formulation of a real world optimization problem that needs to be solved anew each day: the market coupling problem between European day-ahead electricity exchanges. The market is called a non-convex market because the feasible region of the underlying optimization problem is non-convex. The non-convexity of the feasible region is caused by the presence of binary decision variables. In such a market it is difficult to find for each tradable commodity a single price while ensuring that no participant incurs a loss. The existence of such prices must be enforced by complementarity conditions yielding a Mathematical Program with Equilibrium Constraints (MPEC) and binary variables. We present a deterministic algorithm yielding a provably optimal solution and a fast heuristic that exploits the model structure. Instead of solving the large scale MPEC directly we decompose it into a Mixed Integer Quadratic Program (MIQP) and a linear pricing problem. Empirical tests suggest that the solutions determined by the heuristic are optimal in many cases. We also ensure unique prices without changing the economic surplus. Additionally, we introduce rules that allow market participants to check whether the determined prices satisfy necessary optimality conditions of the individual participant’s optimization problems.

1.2 Outline

The structure of the article is as follows. In Section 3 we give a brief introduction to the European electricity market and its features. In Section 4 we introduce the combinatorial optimization problem that is used to determine welfare maximizing solutions subject to price constraints. Analyzing this model we obtain optimality conditions which are formulated in Section 5. We then establish in Section 6 the uniqueness of prices and then we formulate a clearing heuristic and an optimal algorithm in Section 7. We conclude with computational results in Section 8 and some final remarks in Section 9.

2 Background information

In this section, we provide background information on linear prices and on the institutional differences between US electricity markets and European electricity markets.

2.1 Linear pricing schedules

The European day-ahead electricity auctions are using linear pricing schedules. We will briefly define the concept of pricing schedules, here in the multidimensional setting that is a straightforward extension of [19, p. 136].

Definition 2.1.

We consider distinct commodities. A pricing schedule is a map that returns the total amount of money to be paid by a consumer depending on his consumption vector . The schedule is called a linear pricing schedule if the map is linear, i.e., . In this case is called a linear price vector and is the price per unit for commodity . The definition is also applicable to producers if we use consumption units to model production units of commodity .

Definition 2.2.

The clearing condition of a commodity is an equation that ensures that the number of bought units of commodity is equal to the number of sold units of commodity .

Definition 2.3.

A pricing schedule is a strict linear pricing schedule if it is linear and the number of commodities is equal to the number of clearing conditions in the auction model [20]. In the electricity market, the clearing conditions are the flow conservation equations for each network node and time slot.

In linear programming the strong duality theorem provides that given a finite optimal solution to a primal linear program there exists a finite optimal solution to the dual program. The variables of the dual program are called dual variables and can be interpreted as prices [5, Chapter 12]. In convex optimization strong duality holds if a constraint qualification (e.g., Slater’s condition) is satisfied. In this case, the dual variables can also be interpreted as prices. Sometimes the dual variables are also called shadow prices to the primal program [3, Chapter 5].

Now assume that is an optimal finite solution to a convex auction model that maximizes the economic surplus. Let Slater’s condition hold and let be optimal dual variables of the clearing conditions of all commodities. Then defines a strict linear pricing schedule and defines a linear price vector. All participants are perfectly happy with the solution and the prices , as their individual optimization problems are maximized at these prices. Such a solution is called a competitive or Walrasian equilibrium (cf. [2]).

2.2 The US market

We begin with a short introduction to electricity markets in the US. In the US there exist several pool-based electricity markets, operated by independent system operators (ISO). The ISOs organize day-ahead auctions where both suppliers and consumers can submit bids. Using these bids the auction determines prices for each network node and each hour of the next day. Finally a unit commitment model computes a dispatch that minimizes total production cost while ensuring system reliability. A standard reference for unit commitment models is [11]. These models allow the participants to submit the cost structure and production capacities of each power plant. In particular it is possible to submit startup costs and minimal production capacities which are modeled by using binary variables. This detailed information allows the ISOs to ensure system reliability while minimizing the total production cost. In many unit commitment models the demand is assumed to be a price inelastic bid with a fixed given quantity.

Let us hypothetically assume a unit commitment problem can be described by a linear program (LP). Then the optimal dispatch would be determined by solving the LP and a strict linear pricing schedule is given by the dual variables of the flow conservation equations of the network nodes. As soon as binary variables are involved we have to solve a mixed integer linear program (MIP) and the determination of a reasonable strict linear pricing schedule is not as easy as in the LP case. Given an optimal solution to a MIP, in general it is impossible to find a strict linear pricing schedule where all participants neither incur a loss nor miss a not-realized profit. Definition 3.6 formally introduces the concept of a not-realized profit. O’Neill et al. [17] present a method that defines a linear pricing schedule for an optimal solution to a MIP based unit commitment model. The main idea is to treat binary actions like separate commodities. Then we can find linear prices for all commodities, including the binary actions. No participant incurs a loss and no participant misses a not-realized profit. Each binary action can be attributed to a single market participant and only this participant can carry out this binary action. For this reason the price for the individual binary action can be understood as an individual compensation payment that is paid or received by each participant. According to [17], the electricity auctions of New York Independent System Operator (\hrefhttp://www.nyiso.comNYISO) and Pennsylvania-New Jersey-Maryland Interconnection (\hrefhttp://www.pjm.comPJM) are using similar pricing methods. Another technique that defines prices for a MIP solution is called convex hull pricing ([10], [21]). This pricing schedule reduces the impact of compensation payments but still requires the use of individual compensation payments.

In Europe the common practice is to avoid compensation payments and to implement strict linear prices. This major difference renders methods that are based on compensation payments inapplicable.

2.3 The European market

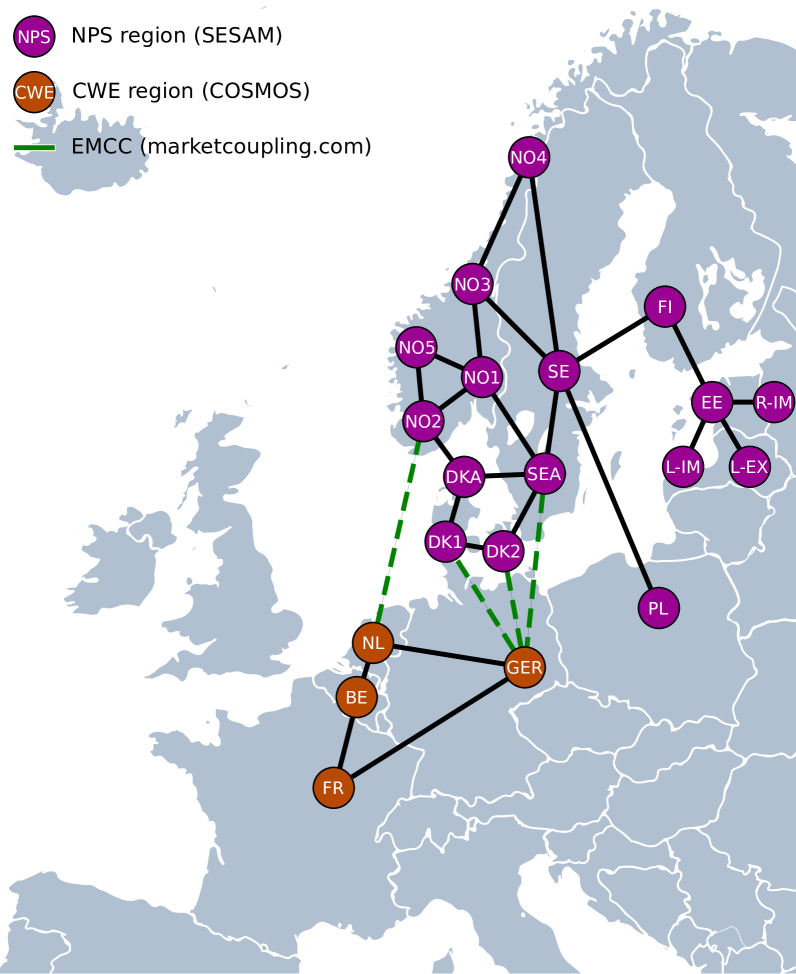

Similar to the US there exist several national and regional transmission system operators (TSO)111Nordic TSOs (NPS region): Elering, Energinet.dk, Fingrid, Litgrid, Statnett SF, Svenska Kraftnät. Central Western Europe TSOs (CWE region): Amprion, Creos Luxembourg, Elia System Operator, Rte, Tennet TSO, TransnetBW. (cf. \hrefhttps://www.entsoe.eu/the-association/members/www.entsoe.eu) in Europe. The main difference to the ISOs in the US is that the European TSOs only maintain system feasibility and reliability. They do not control the spot market for electricity, but they determine network boundary conditions within which they can guarantee the system feasibility and reliability. These boundary conditions (e.g., available transmission capacities) are submitted to independent power exchanges (PX)222Nordic PX (NPS region): Nordpool Spot AS. Central Western Europe PXs (CWE region): APX Endex, Belpex, EPEX Spot. who will run the financial spot market auctions subject to the network constraints. Some power exchanges also split their market into several bidding areas. These bidding areas are often given by national borders or network bottlenecks. For example the power exchange EPEX Spot splits its market into the bidding areas France, Germany/Austria, and Switzerland.

On top of these power exchanges, market coupling systems collect all order book data from the power exchanges and network constraints from the TSOs and compute welfare maximizing power flows between adjacent market areas and prices for the bidding areas of the power exchanges. These flows and price signals are submitted back to the exchanges and TSOs. Finally the exchanges run their own auction incorporating the cross-border flows and the price signals. For example the SESAM system couples the bidding areas of the Nordic region (NPS region) that consists of Denmark, Estonia, Finland, Lithuania, Norway, and Sweden. The COSMOS system couples the bidding areas of the Central Western European region (CWE region) that consists of Belgium, France, Germany, Luxembourg, and Netherlands. On top of these coupling systems, European Market Coupling Company (EMCC) is computing the flows between the NPS and the CWE region. SESAM is in use since 2007 and in Nov. 2009 EMCC started to couple the NPS region with Germany. In Nov. 2010 COSMOS was launched and from there on the EMCC system is coupling the NPS and the CWE region.333cf. \hrefhttp://www.nordpoolspot.com/About-us/Historywww.nordpoolspot.com/About-us/History, \hrefhttp://www.epexspot.com/en/market-couplingwww.epexspot.com/en/market-coupling, and \hrefhttp://www.marketcoupling.com/market-coupling/european-marketwww.marketcoupling.com. Figure 1 shows the interconnected NPS and CWE region in 2011. Note that these systems are distinct entities and guided by different regulations while maintaining a certain set of compatibility constraints as put forth in the European regulation of energy markets.

All European power exchanges that we consider here are already existing and are using strict linear pricing schedules. Electricity at a specific bidding area at the specific time it is being delivered is viewed as a commodity. Thus, for each bidding area and each hour of the next day an electricity price (€/MWh) is computed, such that no compensation payments are needed. This will not be subject to change in the foreseeable future. The strict linear pricing schedule is determined by a welfare maximizing optimization problem subject to quantity constraints and additional price constraints. In order to perform a correct market coupling between such power exchanges a market coupling system needs to model the underlying power exchanges exactly as they are. For this reason a European market coupling system must also implement a strict linear pricing schedule and thus cannot implement any other pricing schedule.

As of now, the TSOs in the NPS and the CWE region only submit upper and lower bounds for the flows and upper bounds for the change of flows. Therefore a market coupling system that couples these two regions only implements these basic transmission constraints. However the algorithms that we present can be easily adjusted to solve more complex transmission constrains, as long as the constraints are linear or convex. In the CWE region the introduction of so called power transmission distribution factor matrices (PTDF) is planned for 2014 [1].

3 Bidding language in European day-ahead electricity auctions

Usually the auctioneer defines a bidding language that allows the participants for expressing their bids, or in other words, their preferences. In a day-ahead electricity auction participants bid today for electricity that they want to buy or sell on the following day. They are allowed to submit their bids up to a predetermined point in time. As soon as the submission deadline has passed the submitted bids cannot be changed anymore and the auctioneer has to decide which bids to accept and which bids to reject. Then the auctioneer publishes a pricing schedule that determines the amount of money that a participant has to pay or receive if his bid was accepted.

The day-ahead electricity auctions in the CWE and NPS region have a common bidding language. The bidding language allows for submitting four different types of bids: hourly bid curves, block bids, flexible bids, and cross border trades. The number of different commodities the participants can bid for is given by the number of market areas times the number of time slots of the next day (e.g., 24 hours). For this reason an entry of a strict linear price vector reflects the price for one electrical power unit that is delivered at a specific market area throughout a specific time slot.

In order to refer to a specific area or time slot we will use the following notation: The set denotes the set of market areas and denotes the set of time slots. An entry of a strict linear price vector will be called price in area at time and is denoted by . We now define the four bid types in a formal way that suits the later exposition.

3.1 Hourly bid curve

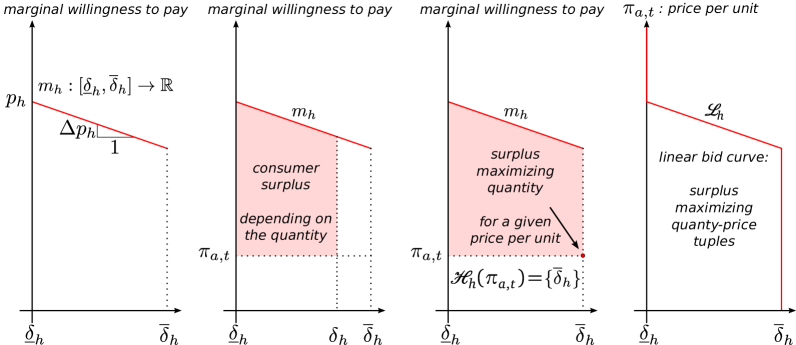

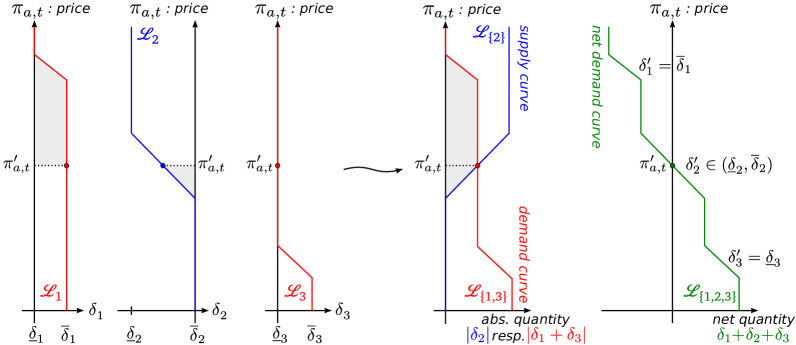

A participant can submit hourly bid curves for every area and hour to specify the optimal quantities that he is willing to buy or sell depending on a given price. At first we will study a simple linear bid curve to understand the details of bid curves, then we will see that the concept of linear bid curves can be used to express piecewise linear bid curves.

Assume that a participant submits a linear bid curve to buy electricity in area at time . He wants to buy at most units and at least units. Let his marginal willingness to pay be given by an affine non-increasing function . Figure 2 depicts his marginal willingness to pay. The function valuates the price that the consumer is willing to pay for each additional unit. If the function is constant (), then the price he is willing to pay for the first consumed unit is equal to the price he is willing to pay for the last consumed unit. His willingness to pay for the consumption of quantity units is given by . If is constant, then this term reduces to . In this case he would buy electricity if the price per unit is lower or equal to . We will now assume that the participant is interested in maximizing his consumer surplus.

Definition 3.1.

The consumer surplus of a participant is his willingness to pay for the consumption of units minus the total amount of money to be paid for units (cf. [19, p. 8]).

Let the price per unit in area at time be exogenously given by the auctioneer and let it amount to currency units per quantity unit. The participant has only one decision variable: the quantity that he wants to buy. He can maximize his consumer surplus by solving the following parameterized optimization problem ( is an exogenously given parameter).

| (QP-Hourly) | ||||

Definition 3.2.

Let be an affine non-increasing function and let . The set of surplus maximizing quantities depending on the price is given by

Note that is equal to if is constant and . The two-dimensional set

is called a linear bid curve. It is called linear, because it contains exactly one linear segment that indicates a change in the quantity. Figure 2 illustrates both definitions.

In Section 4 we will study the optimality conditions that characterize the surplus maximizing quantities; for now, it suffices to be aware of the structure of linear bid curves as depicted in Figure 2.

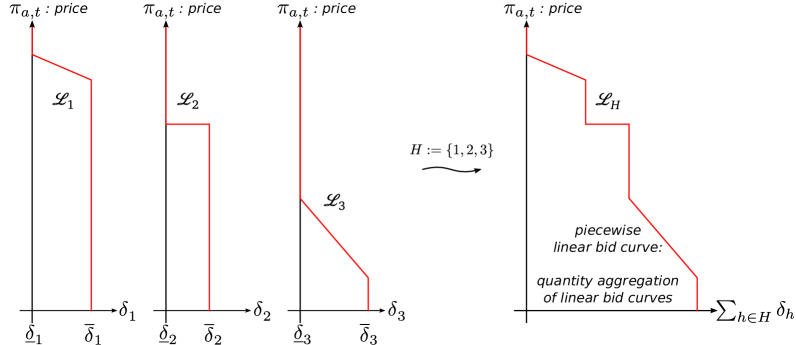

If a participant wants to submit a more complex bid curve he can simply

submit a set of linear bid curves to construct a piecewise linear bid curve

. The following definition formally introduces piecewise linear

bid curves and Figure 3 provides an example.

Definition 3.3.

Let be a finite set of linear bid curves and let be an affine non-increasing function and for all . The two dimensional set

is called a piecewise linear bid curve. Let be the set of all linear bid curves in area at time . The piecewise linear bid curve is called the aggregated bid curve of area at time .

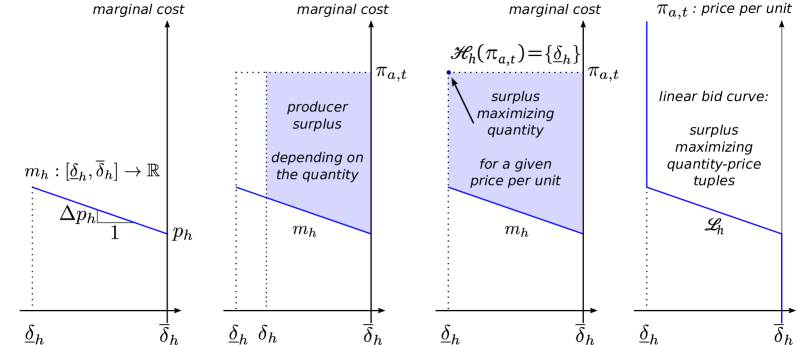

Now suppose that a participant wants to sell electricity in area at time . He is able to generate at most units and at least units. The maximal supply quantity is modeled by a negative number . This allows us for using the definitions from above, such that we do not need to distinguish between demand and supply. A positive quantity indicates demand and a negative quantity indicates supply. Like above, we assume that the marginal cost curve is an affine non-increasing function: the last supplied unit (unit ) is the most expensive one, the first supplied unit is the cheapest one. The cost for generating units is given by .

Definition 3.4.

The producer surplus of a participant is the amount of money to be received for producing units minus the cost for generating units. Figure 4 provides an example.

In Equation (1) it can be shown that the producer and consumer surplus can be expressed by the same formula. For this reason the producer can maximize his producer surplus by solving (QP-Hourly).

| (1) |

3.1.1 Notation used for hourly bid curves

As we have seen in the previous section, we do not need to model piecewise linear bid curves directly. It is sufficient to treat each underlying linear bid curve separately. For this reason we only need one set of linear bid curves for each area and time to model all piecewise linear bid curves that were submitted by the participants.

| set of all linear bid curves | |||

| set of all linear bid curves in area at time | |||

| quantity bounds of the linear bid curve | |||

| affine non-increasing marginal willingness to pay / marginal cost for | |||

| decision variable: bought quantity if positive / sold quantity if negative |

3.2 Block bids

Block bids enable traders to buy or sell electricity in an area for several (not necessarily consecutive) time slots with a single bid. A block bid can either be executed entirely or it is not executed at all. This condition is called fill-or-kill condition. Suppose that a participant wants to buy electricity in area and wants to use a block bid . Then for each hour he has to specify the quantity that he wants to buy or sell. Positive quantities indicate that he wants to buy electricity and negative quantities indicate that he wants to sell electricity. Currently it is only allowed to transmit either a pure buy bid with or a pure sell bid with for all (cf. [8]). Let be the binary variable that models whether the bid is or is not executed. Then is the total bought (or sold) quantity. Let be his constant marginal willingness to pay, i.e., for each bought electricity unit he is willing to pay currency units. His willingness to pay for the consumption of units is given by . Let the price in area and time be given, then the price-parameterized surplus maximization problem for bid looks as follows:

| (MIP-BlockBid) | ||||

The auctioneer cannot guarantee that at the end of the auction the binary variable is a surplus maximizing solution to (MIP-BlockBid), because this is simply impossible in general.

Example 3.5.

Let the set of areas and the set of hours be singletons: , . Bid is a sell block bid with quantity MWh and marginal cost €/MWh. Bid is a buy block bid with quantity MWh and marginal willingness to pay €/MWh. The two orders cannot be matched, because of the different quantities. The only feasible solution is to reject both bids, that is, . If we publish a price that is strictly smaller than €/MWh, then bid is wondering why it is rejected. If we publish a price that is strictly greater than €/MWh, then bid is wondering why it is rejected. Therefore, there exists no price where everyone is perfectly happy: there is no price such that maximizes (MIP-BlockBid)b and maximizes (MIP-BlockBid)c.

Instead of ensuring the individual surplus maximization of a block bid, the auctioneer ensures that the surplus is non-negative if the block bid is executed. In other words, a buy block bid can only be executed if the willingness to pay is greater or equal to the amount of money to be paid:

| (2) |

If the block bid is a sell block bid, then all quantities are smaller or equal to zero: . In this case is the marginal cost of production and equation (2) ensures that the sell block bid can only be executed if the money to be received for generating electricity is greater or equal to the cost for generating the electricity:

Definition 3.6.

A block bid incurs a loss if equation (2) is violated. A block bid misses a not-realized profit if it is rejected even though

| (3) |

holds. Block bids that miss a not-realized profit, are called paradoxically rejected bids (PRB), because they are rejected even though from the local point of view of the owner of the block the rejection is not a surplus maximizing solution to (MIP-BlockBid).

In Example 3.5 either block or block is paradoxically rejected, showing that paradoxically rejected blocks are inevitable.

The trader further has the possibility to link certain block bids so that the execution of some block implies the execution of some other block .

3.2.1 Notation used for block bids

| set of all block bids | |||

| set of all block bids in area | |||

| if , then can only be executed if also is executed | |||

| quantity to be bought () / sold () in hour by block bid | |||

| constant marginal willingness to pay / marginal cost of block bid | |||

| decision variable: rejected () / executed () |

3.3 Flexible bids

With flexible bids a participant can buy or sell electricity in a specific area in exactly one hour without specifying the hour in which the bid should be executed. Flexible bids must satisfy the fill-or-kill condition as well, i.e., a partial execution is not feasible. Suppose that a participant wants to buy units in area in a not specified time slot. Let his marginal willingness to pay amount to currency units per quantity unit. We need to introduce one binary variable for each time slot . If , then the flexible bid is executed in time slot . The bid may only be executed in at most one time slot: . The willingness to pay for the total consumed quantity of units is given by . Now we can write down the price-parameterized surplus maximization problem of a flexible bid.

| (MIP-FlexBid) | ||||

In general it is impossible to ensure that at the end of the auction all decision variables will be surplus maximizing for (MIP-FlexBid), but it is possible to ensures that the surplus is non-negative if the flexible bid is executed:

| (4) |

If this inequality is violated, then the flexible bid incurs a loss. At the end of the auction some flexible bids might miss a not-realized profit, i.e., from the local point of view of the owner of a flexible bid the current solution is not necessarily surplus maximizing for (MIP-FlexBid).

3.3.1 Notation used for flexible bids

| set of all flexible bids | ||||

| set of all flexible bids in area | ||||

| quantity to be bought () / sold () by flexible bid | ||||

| constant marginal willingness to pay / marginal cost of flexible bid | ||||

3.4 Cross-border trades

Trading electricity across areas is called a cross-border trade. The regulatory body stipulates that in European day-ahead electricity auctions, only transmission system operators are allowed to perform cross border trades. The cross-border trader buys electricity in low price areas and sells electricity in high price areas. Cross-border trades are only possible if there are interconnectors connecting the areas. The latter will be denoted by , where is the set of areas. An interconnector is modeled by a directed arc, whereas denotes the source and denotes the sink. The transmitted electricity on interconnector in time slot is denoted by a signed variable . We use the convention that a positive flow indicates a transfer from the source to the sink , and a negative flow indicates a transfer from to . There are upper and lower bounds on the transmission quantity. These bounds are called available transmission capacity (ATC). Also the change of flow between two consecutive hours can be limited by an upper bound , called ramp rate. Now suppose that there is a positive flow on interconnector in hour , then electricity is bought in area and sold in area . The marginal cost for buying electricity is and the price per unit to be received for selling electricity is . The surplus of a cross-border trade is called congestion rent and can be maximized by solving the following price-parameterized optimization problem.

| (LP-TSO) | ||||

The parameter is the given flow of the last hour of the previous day.

At the end of the auction the flows will be congestion rent maximizing, but we need to keep in mind that the cross-border trader is considered a price taker, i.e., the price is exogenously given by the auctioneer. We will later see that in this case the optimality conditions of cross-border trades imply that prices only diverge, if a transmission constraint is active.

3.4.1 Notation used for cross-border trades

| set of all interconnectors | ||||

| set of all interconnectors starting in | ||||

| set of all interconnectors ending in | ||||

| flow on in the last time slot of the previous day | ||||

| ramp rate; we put if we have no ramping on | ||||

| decision variable: flow on in time within bounds (ATC) |

4 Optimization problem of the auctioneer

In this section we will present the complete MPEC with binary variables that describes the auctioneers optimization problem. The aim of the auctioneer is to maximize the total economic surplus subject to the clearing condition and the constraints given by the submitted bids. We first introduce the overall model structure and then discuss the objective function as well as each constraint in detail.

| (economic surplus) | (MPEC) | ||||

| (quantity constraints) | |||||

| (C1) | |||||

| (C2) | |||||

| (C3) | |||||

| (C4) | |||||

| (price constraints) | |||||

| strict linear prices: | |||||

| non-negative surplus of block and flexible bids: | |||||

| (C5) | |||||

| (C6) | |||||

| optimality conditions of cross-border flow, (LP-TSO): | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| optimality conditions of linear bid curves, (QP-Hourly): | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

The primal variables of the model (MPEC) are and . The former are used to model the executed quantities and the latter are used to model the price constraints. In the next section we show that the primal variables and in this model are used to model the Karush-Kuhn-Tucker optimality conditions (KKT) of the price-parameterized surplus maximization problems of cross-border trades (LP-TSO) and linear bid curves (QP-Hourly). A short introduction to the KKT optimality conditions can be found in [3, Chapter 5.5.3]. Because of the KKT conditions, some of the price constraints are non-convex. The bar below or above the variables indicates that the variable is associated with a lower or upper quantity bound of a quantity constraint of (LP-TSO) or (QP-Hourly). For example the variable is associated with the upper quantity bound of (QP-Hourly). We will make this precise below. As the auctioneer needs to compute surplus maximizing quantities to the surplus maximization problems of linear bid curves and cross-border trades, the dual variables of these subproblems are primal variables in the auctioneers optimization problem. We need to explicitly add the optimality conditions (price conditions) to the model, because they are not necessarily automatically fulfilled in an optimal solution.

An important property of the model is that the determined strict linear prices are consistent with the strict linear prices that we know from convex auctions: Assume that we solve a relaxed model that only contains the quantity constraints (except for constraint (C3)) and assume that its QP-relaxation admits an integral optimal solution, with respect to the binary variables. Then we can find strict linear prices to this optimal solution that satisfy all previously mentioned price conditions. In this case, all price conditions are dispensable and could be omitted. This assertion can be verified by writing down the KKT conditions of the QP-relaxation. Van Vyve proves this assertion in Proposition 3 in [20]. The same result in a similar context is also provided in [2, Corollary 11.16].

4.1 Constraints

We now introduce the constraints mentioned above and explain them in detail.

-

(C1)

Clearing condition. This constraint ensures the identity of executed net demand and net import. The constraint is similar to the classical conservation of flow constraint typically present in network flow models. In every area and every hour the executed net demand must coincide with the net import:

-

(C2)

Ramping condition. This condition incorporates the ramping requirements on the interconnectors by limiting the change between two consecutive time slots accordingly. From one hour to the next hour the flow on interconnector may only change by units:

-

(C3)

Block bid links. To model the linking of block bids we add the following constraint. If , then block may only be executed if block is executed:

-

(C4)

Flexible bid execution at most once. A flexible bid can be executed in at most one time slot:

-

(C5)

Block price condition. In principle it is possible to obtain an equally high or even higher economic surplus by requiring altruistic behavior from some of the participants. However this is not in line with general economic principles as no participant is willing to sell at a loss. Therefore, a block bid can only be executed if it does not incur a loss:

As mentioned before the converse cannot be guaranteed: some block bids might miss a not-realized profit at the end of the auction. In other words, they might be rejected, even though the prices would allow the execution.

The block price condition is a quadratic non-convex constraint that is difficult to handle, but it is easy to linearize it if we introduce a sufficiently large constant for each . We know that is a binary variable and we assume that . Now we can rewrite the constraint as follows (cf. [5, Chapter 26-3-I(g)]):

-

(C6)

Flexible bid price condition. A flexible bid is only executed if it does not incur a loss:

where denotes the sign function. This formulation is equivalent to equation (4). Similar to block bids, also flexible bids might miss a not-realized profit, i.e., they might get rejected, even though the prices would allow the execution.

-

(C7)

Flow price condition. This condition represents the optimality condition of the cross-border traders optimization problem. The regulators force them to be price takers such that the prices are externally given by the auctioneer and the only remaining decision variable is the flow . The individual optimization problem is to maximize the congestion rent subject to the available transmission capacity and the ramp rate:

(LP-TSO) ATC ATC ramp rate ramp rate The variables in squared brackets are the dual variables to the primal constraints. By duality, essentially an optimal flow implies that a price difference between two adjacent areas implies that at least one transmission constraint is active. The KKT conditions provide a precise description of an optimal flow. From now on the KKT conditions of (LP-TSO) will be called the flow price condition.

Definition 4.1 ((Flow price condition)).

Let , , and . The flow-price tuple satisfies the flow price condition if there exist so that for all and

(5) (6) (7) (8) (9) (10) In terms of duality theory the conditions (5) and (6) correspond to dual feasibility conditions and the remaining ones are complementarity conditions. The term in square brackets is only added if .

In the following we provide three implications that help to understand the properties of an optimal flow. A derivation of these implications can be found in Appendix 10.

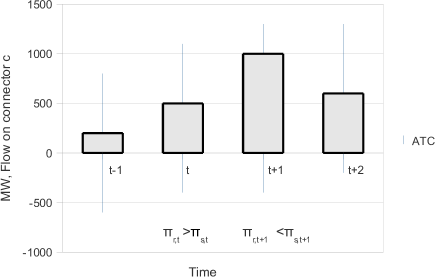

If there is no ramping on an interconnector , this condition simplifies to

(11) The economic interpretation of this simplified condition is that free transfer capacity in the forward direction implies that the price in the source area must be higher or equal to the price in the sink area. If this would not be the case, then the free capacity should be used to transfer additional electricity from the source to the sink, and therefore the market would not be in an equilibrium.

If, on the other hand, the ramping condition (C2) on an interconnector is only binding (i.e., satisfied with equality) in two consecutive hours and , and there is still available transfer capacity in that time window, then the condition simplifies to:

(12) This establishes that the price difference at one point in time can have an impact on the price difference in the following ones.

As mentioned before the flow price condition implies that prices of adjacent areas can only deviate if at least one respective transmission constraint is active (terms in square brackets are only present if ):

(13) (14) -

(C8)

Filling condition of linear bid curves. This constraint represents the optimality conditions of linear bid curves. Participants who submit linear bid curves are modeled as price takers. In the optimization problem associated with a linear bid curve the price is exogenously given and the only remaining decision variable is . The objective is to maximize the economic surplus.

(QP-Hourly) with . The variables in squared brackets correspond to the dual variables of this problem. From now on the KKT conditions of this price-parameterized optimization problem will be called filling condition.

Definition 4.2 ((Filling condition)).

Let for and . The tuple satisfies the filling condition if and only if there exist variables so that for all , ,

(15) (16) (17) (18) This condition can be reformulated to an equivalent condition:

Proposition 4.3 ((Filling condition)).

Let for and . The tuple satisfies the filling condition if and only if

(19) with .

Proof 4.4.

The second definition directly shows that an optimal solution only contains quantity-price-combinations that were defined by the piecewise linear bid curves. A MIP formulation of the filling condition based on the delta-method (cf. [5, Chapter 26-3-I(f)]) can be found in Appendix 11 and a graphical illustration is given in Figure 5.

Figure 5: The tuple satisfies the filling condition. The points are in for and the point is in .

4.2 Additional market rules

For the sake of completeness we need to mention that there exist additional market rules that are not covered by the previous model. Some of these additional rules are only valid for either the CWE region or the NPS region. For example in the CWE region there is a parameter that prevents block bids with low marginal costs or high marginal willingness to pay from being rejected. In the NPS region participants can submit so called convertible block bids. A convertible block bid is basically a block bid, but if it gets rejected, it is transformed into several linear hourly bid curves and the auction starts again. Some interconnectors are facing a significant transmission loss. The factor that models this loss is called deadband. There also exist rules related to situations with extremely high or low area prices: The exchanges impose additional upper and lower bounds on the prices. If a price reaches a bound then curtailment rules come into effect: If for example an area price is at its upper bound, then demand block bids in this area have a lower priority than linear bid curves. Except for the different price intervals we will not explain these rules in detail as they are out of the scope of this paper.

Remark 4.5.

Different price intervals. The prices in the NPS region are limited to €/MW whereas the prices in the CWE region are limited to €/MW. On the on hand the area prices must be within the specific regional bounds. On the other hand all submitted price limits (marginal willingness to pay / marginal cost) must be within the specific regional price interval: Let be the feasible price interval in area , then for all block bids and flexible bids in area , and for all linear bid curves in area . Note that linear bid curves are defined for all prices in and that they are parallel to the price axis for prices in .

If a solution contains a price , then is changed to the nearest price in . By doing so, we might violate the flow price condition. In other words, there might be a price difference between two adjacent areas although none of the transport restrictions is binding. In fact, this might happen if one of the areas has a small price interval and reaches the maximal possible hourly demand or supply.

4.3 Objective function

The economic surplus is the sum of consumer surplus and producer surplus (cf. [18]). It is also called global welfare (cf. [12]) or social welfare. For example a consumer buys units at a price of per unit and he is willing to pay a price of , then his consumer surplus is given by . The producer surplus generated by hourly bid curves is determined accordingly by integrating the price per unit minus the producers marginal cost over the quantity from zero to the produced quantity.

In Section 3 we already introduced the price-parameterized surplus maximization problems of each trading product. We will now summarize the results from above.

Definition 4.6.

Definition 4.7.

The surplus of a block bid with for and is given by

Definition 4.8.

The surplus of a flexible bid with for and is given by

Another surplus arises on the interconnectors. This surplus represents the surplus of cross-border trades and is usually referred to as congestion rent.

Definition 4.9.

The congestion rent on interconnector for is given by:

Note that the congestion rent is indeed contained in the economic surplus in most market models run today. The surplus generated due to congestion rent is usually reinvested in order to reduce tariffs or build new lines444In 2007: Energinet.dk: 100% to reduce tariffs, Fingrid: 100% to build new lines, Statnett: 100% to reduction, Svenska Kraftnät: 100% to build new lines. (cf. \hrefhttp://www.nordpoolspot.com/Global/Download%20Center/TSO/How-to-calculate-the-TSO-Congestion-rent.pdfhttp://www.nordpoolspot.com). Later we will see that the flows are not uniquely determined by the maximal economic surplus, but in general ambiguities only exist, when prices of adjacent areas coincide. In these situations, there is no price difference () and thus no congestion rent, and the congestion rent cannot be influenced by changing the flow within the ambiguities. For more details on ambiguities of flows and how to choose unique flows refer to Section 6.3.

Definition 4.10.

Let be feasible for (MPEC). The economic surplus of the market is the sum of the surpluses of all market participants and is computed as follows:

| (21) | ||||

| (22) | ||||

The first line of equation (22) represents the willingness to pay or the cost of each bid, whereas the second and third represent the net amount of money to be paid or received. The next theorem shows us that the latter is equal to zero if the clearing condition (C1) is satisfied. The simplified expression of the economic surplus is equivalent to the objective of the welfare maximization problem in [16, Section II.B].

Theorem 4.11.

Let be within the given bounds and satisfy condition (C1), then the economic surplus is given by

Proof 4.12.

Observe that the objective function obtained in Theorem 4.11 is a quadratic, concave function and does not involve price variables or flow variables . While this is convenient for the actual computation, these variables still have to satisfy the stated conditions and so they implicitly influence the economic surplus.

The problem formulation (MPEC) with the objective function as stated above is in principle solvable by convex Mixed-Integer Quadratic Programming solvers like IBM CPLEX if we linearize the price conditions by using the big-M method. Solving real world instances with this technique however is very hard, because each non-convex quadratic price constraint must be modeled by using an auxiliary binary variable. For the considered instances IBM CPLEX was not able to obtain feasible solutions or improve provided warm-start solutions within 30 minutes. We also observed that MINLP solvers and general MIQP solvers like BONMIN, COUENNE, SCIP, and BARON were not able to solve a typical instance of the relaxed (QPBidCut) model to optimality within 10 minutes555Run on a compute server with two 6-Core AMD Opteron 2435 (2.6GHz) CPUs, 64GB RAM, and 64-bit Debian.. This indicates that these solvers will not be able to solve the the problem to optimality within 10 minutes if we add the non-convex complementarity conditions. This is clearly unsatisfactory as the actual market coupling auction needs to be cleared within 10 minutes. We therefore propose a heuristic and an exact algorithm for this problem.

5 Optimality conditions

In this section we define a relaxation of (MPEC) and analyze the optimality conditions of this problem. Based on this analysis we derive a heuristic and an exact algorithm that performs very well in practice. We say that is a bid selection if and . Note that a bid selection does not necessarily satisfy the block price condition.

We consider the following parameterized and relaxed version of (MPEC). We relax all price constraints and assume that a fixed bid selection is exogenously given:

| (QPRelax) | ||||

Note that (QPRelax) is a parameterized optimization problem where the binary variables are exogenously given parameters. It is a convex optimization problem with a polyhedral feasible region. Therefore, it is well defined to associate dual variables with every primal constraint. The dual variables are denoted by the Greek letters that are given in squared brackets. The next theorem will show that in this relaxation we do not need to require the filling condition (C8) or the flow price condition (C7) explicitly as these naturally follow from the KKT conditions.

Theorem 5.1 ((Natural spot price characteristics)).

Let be an exogenously given fixed bid selection, i.e., and are exogenously given parameters. A feasible solution to (QPRelax) is an optimal solution if and only if there exist prices so that satisfies the filling condition and satisfies the flow price condition. These prices are given by the optimal dual variables to the clearing condition of (QPRelax).

Proof 5.2.

Let be a fixed bid selection. The objective of the parameterized optimization problem (QPRelax) is concave and continuous differentiable and the constraints are affine linear. The Karush-Kuhn-Tucker optimality conditions provide the following: A primal feasible solution to (QPRelax) is an optimal solution if and only if there exist dual variables with

| (24) | |||||

| (25) | |||||

| (26) | |||||

| (27) | |||||

| (28) | |||||

| (29) | |||||

| (30) | |||||

| (31) | |||||

| (32) |

where the term in squared brackets is only added if . The conditions (24) to (26) are the dual feasibility conditions and conditions (27) to (32) are the complementarity conditions. Observe that equations (24), (26), and (29) to (32) imply that fulfills the flow price condition (C7). The filling condition (C8) corresponds to the equations (24), (25), and (27) to (28).

6 Uniqueness of a solution

In the following section we will discuss uniqueness aspects of the computed solution. More precisely, we will show that the economic surplus for a given bid selection is unique. The flows and the prices however are not necessarily unique as we will see. Suppose that an algorithm finds an optimal solution to (MPEC). We will see that if we fix the binary variables in (MPEC) to the optimal values, then all feasible solutions to the remaining model have the same objective value, thus the remaining model is just a feasibility problem. In practice there exist several feasible solutions to the remaining model. For this reason an auctioneer must define rules that determine a unique solution among these feasible solutions. In practice SESAM and COSMOS use slightly different rules to choose unique solutions. For the sake of exposition we propose a simple rule that chooses unique flows and prices without changing the total economic surplus. At first an algorithm chooses a bid selection, then a unique flow is chosen, and finally a unique price. As a corollary of 5.1 we obtain:

Corollary 6.1.

6.1 Unique economic surplus for a given bid selection

Let be a bid selection. Recall that the model (MPEC) requires the filling condition and the flow price condition to be satisfied. We can therefore only construct a solution to (MPEC) from a solution to (QPRelax) if there exist prices that satisfy the filling and the flow price condition. Fortunately, these are exactly the KKT optimality conditions of (QPRelax). Let be a feasible solution to (QPRelax) and suppose that there exist prices that satisfy the filling condition and the flow price condition. Corollary 6.1 provides that in this case is an optimal solution to (QPRelax). There exists exactly one optimal objective value for each parameterized (QPRelax). If we fix the bid selection in the model (MPEC) then the remaining degrees of freedom cannot influence the economic surplus anymore.

6.2 Uniqueness of hourly bid execution

6.3 Choosing unique flows

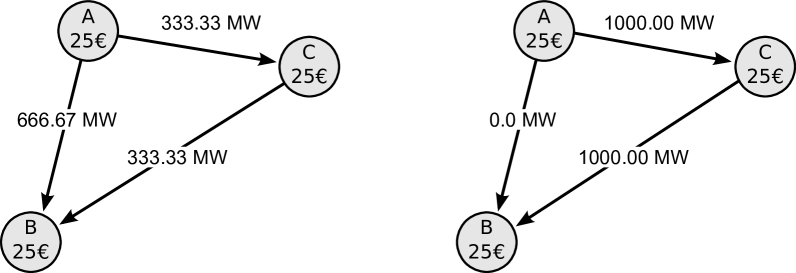

The optimality of a solution to (QPRelax) and the constraints in Section 4.1 are not sufficient to imply a unique flow. This follows from the non-uniqueness of the execution state of some linear bid curves (those with ). To obtain a unique flow, we minimize the squared flow while fixing the economic surplus. In Figure 6 an example of a non-unique flow is depicted. The left part shows the solution with minimized squared flows. In this example the prices of the adjacent areas coincide and there is no congestion rent.

The following model selects a unique flow: Let be a bid selection, be an optimal solution to (QPRelax), and let be the set of linear bid curves with non-unique execution state.

| (FixFlow) | ||||

| The economic surplus must not change (cf. Theorem 4.11): | ||||

| Clearing condition (cf. (C1)): | ||||

| Upper bounds, lower bounds, and ramp rate: | ||||

Note that the objective is strictly convex and the constraints are affine linear. So the obtained solution is unique with respect to the flow. The unique flow determines a unique net export per area and hour, therefore also the execution state of the linear bid curves in is unique.

6.4 Choosing unique prices

In this section we will explain a way of how to obtain unique prices. Let be a bid selection and an optimal solution to (QPRelax) with unique flows. Then there exist prices that satisfy the filling condition and the flow price condition. The following example will illustrate that these prices are not unique in general.

Suppose that there is only one market area , and one time slot . Let the hourly bid curve be parallel to the price axis in a price interval (i.e., no volume change). Let be an optimal solution to (QPRelax) and let be a price that satisfies the filling condition. The flow price condition is trivially satisfied as there exists no interconnector. If is in then all prices in satisfy the filling condition.

The following model takes as input a given bid selection and an optimal solution to (QPRelax), and then determines unique prices by minimizing the squared prices subject to all price conditions.

| (squared prices) | (QPPrice) | ||||

| (price constraints) | |||||

| (C5) | |||||

| (C6) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

Observe that the filling condition, the flow price condition, and the bid price constraints simplify to linear constraints, because the flow , the hourly bid execution , and the bid selection are fixed.

7 The bid cut heuristic and an exact algorithm

We will now present the proposed algorithm to solve the clearing problem. The basic idea is to relax all price constraints. For example we allow that block or flex bids incur a loss. The following model is similar to (QPRelax), but this time the bid selection is not fixed: The model can choose the best bid selection in terms of the total economic surplus. We will see that an optimal solution to this model has similar properties to those in Theorem 5.1.

| (economic surplus) | (QPBidCut) | ||||

| (quantity constraints) | |||||

| (C1) | |||||

| (C2) | |||||

| (C3) | |||||

| (C4) | |||||

Theorem 7.1.

Let be an optimum solution to (QPBidCut). Then there exist prices that satisfy the filling condition and the flow price condition. The objective value is the economic surplus in the point .

Proof 7.2.

Let be optimal for (QPBidCut). Then is a fixed bid selection and is optimal for (QPRelax). Then Theorem 5.1 yields the existence of prices that satisfy the filling condition and the flow price condition. Every feasible solution to (QPBidCut) satisfies the clearing condition (C1). Therefore, Theorem 4.11 yields that is the economic surplus.

Note that the theorem above only guarantees that the filling condition and the flow price condition can be satisfied in an optimal solution. It does not guarantee that none of the executed block bids or flexible bids incurs a loss.

Suppose now that we have an optimal solution to (QPBidCut). Then we can find prices that satisfy the filling condition and the flow price condition, but there might exist block or flexible bids that incur a loss. Thus the solution is not feasible for (MPEC). In this case an additional constraint, a so called bid cut, is added to the problem. This constraint cuts off the infeasible bid selection and a class of similar bid selections. This process is repeated until a selection is found that is feasible for (MPEC). The feasibility of a selection can be checked with a model that is similar to (QPPrice). As shown in Theorem 7.1 the flow price condition (C7) and the filling condition (C8) can be satisfied. The block and flexible bid price condition must be relaxed. Instead of choosing unique prices, we are now interested in minimizing the violation of these two conditions. Model (LPPrice) shows these modifications. We introduced a positive continuous slack variable for every executed block or flexible bid and used them to relax the according block or flexible bid price condition. Instead of minimizing the squared prices we minimize the sum of these slack variables. Now the variable models the loss of the executed block or flexible bid .

Let be an optimal solution to (QPBidCut), then the parameterized linear program (LPPrice) checks whether the solution is feasible to (MPEC): If there exists a solution with , then we have found a feasible solution to (MPEC).

| (incurred loss) | (LPPrice) | ||||

| (price constraints) | |||||

| (relaxed C5) | |||||

| (relaxed C6) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C7) | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

| (C8) | |||||

We will now introduce two families of cuts that can be used. The first one works very well in practice but is inexact as it might converge to a suboptimal solution. The second family of cuts is exact but more cuts have to be added. We will later report timings for both families in Section 8.

Definition 7.3.

Let be an optimal of (QPBidCut) and let be an optimal solution to (LPPrice). The set of bids that incur a loss at prices is given by

where is the set of executed block bids that incur a loss at prices and is the set of executed flexible bids that incur a loss at prices . The linear constraint that prohibits the execution of at least one bid of the set is given by

We refer to this class of constraints as Bid Cuts (cf. [15, Definition 5.2]).

As mentioned above, for this family of cuts, the obtained solution might be slightly suboptimal, i.e., these cuts provide us with a heuristic. Nonetheless, this cut can be applied iteratively as shown in Algorithm 1 or it can be incorporated into a branch-and-cut framework. The latter is the more effective one as it provides a very fast heuristic: The solving process of IBM CPLEX is only started once and the bid cuts are injected directly into the process by using callback functions.

If the Bid Cut is replaced with a less aggressive one that only removes exactly one invalid bid selection at a time, then the resulting algorithm will converge to the globally optimal solution. For example, the following family of cuts separates exactly one invalid bid selection.

Definition 7.4.

The most effective way to implement an exact algorithm that uses the exact bid cuts is to inject them into a branch-and-cut framework. We decided to call this algorithm Branch-And-Cut Decomposition, because we decompose the model into the upper level problem (QPBidCut) and the parameterized lower level problems (LPPrice) and use exact cuts to connect both levels.

8 Results

We will now present some computational results for the algorithms presented in Section 7. We compare the Bid Cut Heuristic and Branch-and-Cut Decomposition with the commercial algorithm EMCC Optimizer of Deutsche Börse Systems which is currently used by European Market Coupling Company (EMCC) to determine flows between the NPS and the CWE region.

For our computational tests we used 79 realistic instances that contain 10 European market areas, about 600 combinatorial bids, and about linear bid curves. All tests were performed on the same hardware666Intel Xeon Core E5440 with 8 GB memory using IBM CPLEX 12.1 as mixed integer linear/quadratic programming solver. In our tests, we did not incorporate the (FixFlow) model, as its sole purpose is the redistribution of flow without affecting the overall economic surplus. Moreover, our tests indicated that fixing the flow impacts the prices only in very pathological cases that can be disregarded in this paper. We will first give a brief introduction to an early version of the EMCC Optimizer and provide some statistics. Then we discuss the two proposed algorithms from above.

8.1 EMCC Optimizer

The version of the EMCC Optimizer that we used in our comparison is version 2.1.2 that was used in 2009. This algorithm is based on computing a start solution with a linear program (cf. [13]) and then checking the feasibility of the bid selection. If the bid selection is not feasible, executed bids are excluded successively until the solution is feasible. Then the solution will be improved by trying to include not executed bids. For more details see [7, Chapter 4.3.2]. In some cases this search phase is very time consuming and cannot be completed within 10 minutes777The limit of 10 minutes reflected the operational requirements when the tests of this algorithm were performed (September 2009). For production it has been changed to 15 minutes.. In this case, the last feasible solution will be returned; in fact the start solution for the last phase is already feasible however might be suboptimal. In our analysis, for 22% of the instances this last phase could not be completed on time. The average time for computing the solutions amounts to 6 minutes and in at least 15% of the cases the bid selection was provably optimal. In 76% of the cases the selections could be slightly improved by our algorithms and in the remaining cases we could neither prove nor disprove the optimality of the selection. The relative distance to the best upper bound, i.e., the relative gap, averages to 2.577; a selection is considered optimal here if the relative gap is below 1 which roughly corresponds to one euro cent. On average there are 10.76 rejected combinatorial bids, so called paradoxically rejected bids (PRB) (cf. [14]) that could potentially have generated a net profit. However, in most cases these bids cannot be included without decreasing the overall economic surplus or rejecting other bids that are in the money.

Some of our ideas where used to improve later versions of the EMCC solver and, therefore, increased the daily economic surplus indirectly. For example the usage of only one aggregated hourly bid curve per area and hour instead of separate demand and supply curves decreased the computing time significantly and allowed for testing more solution candidates in less time.

8.2 Bid Cut Heuristic

The tests are based on a branch-and-cut version of the Bid Cut Heuristic. In at least 38% of the tests the absolute gap is smaller than one euro cent. The average relative gap amounts to 1.926. In 96% of the cases, the solutions found by the Bid Cut Heuristic could not be outperformed by any other algorithm of the test. On average there are only 4.65 PRBs leading to a potentially higher overall acceptance of the prices and executed quantities. The most important property of the algorithm however is its running time which averages to only 4.1 seconds. The maximum computing time was 1.1 minute and so clearing within the 10 minutes is easily possible. Moreover, due to being able to compute the solution way before the time limit is reached the auction can also be run on different machines with identical results. This would not be possible if the process would be stopped by the time limit as in this case the actual performance of the machine would potentially impact the computed prices. Note that reproduction of prices is crucial for market transparency and confidence and an algorithm that is terminated by a time limit is less suited for market clearing as the results can be influenced by side effects like CPU load that is generated by other processes.

8.3 B&C Decomposition

The Branch-and-Cut Decomposition is slower than the Bid Cut Heuristic. However using it, we can prove that the absolute gap of a solution is smaller than one euro cent. It uses the solutions of the Bid Cut Heuristic as warm start solutions. In 38% of the cases the algorithm finishes in about 9 seconds by finding the optimal solution and proving optimality. In the other cases the solver was stopped when reaching the time limit without reducing the absolute gap to one euro cent. During the computation 4% of the bid selections found by the Bid Cut Heuristic could be improved. This reduced the relative gap to 1.924 and the number of PRBs was reduced to 4.62. The improvement which is not significant indicates that the solutions obtained via Bid Cut Heuristic are very good.

Algorithm Abs. Gap Best known PRBs Relative Computing Time 10 Min Stopped at 0.01 EUR Bid Selection Gap Average (s) Min (ms) Max (s) max Time EMCC Optim. 2.1.2 15% 24% 10.76 2.577E-6 361.4 46000 600.0 22% Bid Cut Heuristic 38% 96% 4.65 1.926E-6 4.1 493 62.8 0% B&C Decomposition 38% 100% 4.62 1.924E-6 (9.3) 390.8 1114 600.0 65%

In Table 1 we summarize the results. More details about each instance can be found in Tables 2 and 3. We can see that the relative gaps of all algorithms have the same order of magnitude. The best solutions are found by the Branch-and-Bound Decomposition, but the improvement of the relative gap in comparison to the Bid Cut Heuristic is not significant. The best suited algorithm in terms of time consumption and quality of the solution is the Bid Cut Heuristic that finds very good bid selections in about 4 seconds.

9 Concluding remarks

Our proposed approach works very well in practice and we were able to derive desired properties from the formulation as an optimization problem. A possible route for improvement is to replace the bid cut by an infeasibility cut of the generalized Benders decomposition [9, 4]. The main difficulty here is to find a non-trivial cut that is strong enough to work as fast as the bid cut. Otherwise the performance of the algorithm for day-ahead market clearing might not be sufficient enough. For example the simple exact bid cut (cf. Definition 7.4) used for the Branch-and-Cut Decomposition is a valid Benders infeasibility cut, but the resulting algorithm is too slow.

A nice additional consequence of the presented model are the transparent pricing rules. In fact, for a given bid selection optimality can be checked easily: A market participant could collect all relevant information to check the flow price condition. It is clear that a solution will also satisfy the filling condition, so by applying Theorem 5.1 the participant knows that the economic surplus is maximal for the actual bid selection. This transparency is crucial for market confidence and liquidity.

We would like to mention that the flow price condition is subject to change in the future as it will include deadbands: losses during transmission via an interconnector. While this change will alter the optimality conditions of our model, our model can be adjusted to incorporate deadbands.

Acknowledgments

We would like to thank Herbert Nachbagauer and Adrian Krion for the insightful discussions, as well as the Deutsche Börse Systems team for supporting us. We also would like to thank European Market Coupling Company for their cooperation and for providing us with invaluable data and information. Furthermore we want to thank the anonymous referees for the valuable comments and discussions.

References

- Aguado et al. [2012] M. Aguado, R. Bourgeois, J. Bourmaud, et al. Flow-based market coupling in the Central Western European region — on the eve of implementation. CIGRE, C5-204, 2012. URL http://www.cigre.org.

- Blumrosen and Nisan [2007] L. Blumrosen and N. Nisan. Combinatorial Auctions. In N. Nisan, T. Roughgarden, Éva Tardos, and V. V. Vazirani, editors, Algorithmic Game Theory, chapter 11, pages 267–299. Cambridge University Press, New York, 2007. ISBN 978-0-521-87282-9.

- Boyd and Vandenberghe [2004] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, Cambridge, 2004. ISBN 0521833787.

- Chu and Xia [2004] Y. Chu and Q. Xia. Generating Benders Cuts for a General Class of Integer Programming Problems. In J.-C. Régin and M. Rueher, editors, Integration of AI and OR Techniques in Constraint Programming for Combinatorial Optimization Problems, volume 3011 of Lecture Notes in Computer Science, pages 127–141. Springer Berlin Heidelberg, 2004. ISBN 978-3-540-21836-4. 10.1007/978-3-540-24664-0_9.

- Dantzig [1963] G. Dantzig. Linear Programming and Extensions. Princeton University Press, Princeton, August 1963.

- Dattorro [2005] J. Dattorro. Convex Optimization & Euclidean Distance Geometry. Meboo Publishing, Palo Alto, 2005. ISBN 0-9764013-0-4.

- [7] EMCC GmbH. EMCC Optimizer. Internet, Nov. 2009. URL http://www.marketcoupling.com/document/1137/EMCC%20Optimizer.pdf.

- EPEX Spot SE [2013] EPEX Spot SE. EPEX Spot Exchange Rules. Internet, Jan. 2013. URL http://static.epexspot.com/document/21256/20130114_EPEX_SPOT_RR_EN.ZIP.

- Geoffrion [1972] A. M. Geoffrion. Generalized Benders decomposition. Journal of Optimization Theory and Applications, 10(4):237–260, October 1972. ISSN 0022-3239. 10.1007/BF00934810.

- Gribik et al. [2007] P. Gribik, W. Hogan, and S. Pope. Market-clearing electricity prices and energy uplift. Technical Report 31, Dec. 2007. URL http://www.hks.harvard.edu/hepg.

- Hobbs et al. [2001] B. Hobbs, M. Rothkopf, R. O’Neill, and H. po Chao, editors. The next generation of electric power unit commitment models, volume 36 of International Series in Operations Research & Management Science. Springer Netherlands, Dordrecht, 2001. ISBN 978-0-7923-7334-6. 10.1007/b108628.

- Kirschen and Strbac [2004] D. Kirschen and G. Strbac. Fundamentals of power system economics. Wiley, Chichester, 2004. ISBN 9780470845721.

- Krion [2008] A. Krion. Optimization Methods for Computation of Cross Border Flow in European Power Market Coupling. Master’s thesis, TU-Darmstadt, 2008.

- Meeus et al. [2009] L. Meeus, K. Verhaegen, and R. Belmans. Block order restrictions in combinatorial electric energy auctions. European Journal of Operational Research, 196(3):1202–1206, 2009. ISSN 0377-2217. 10.1016/j.ejor.2008.04.031.

- Müller [2009] J. C. Müller. Optimierungsmethoden für die Kopplung von Day-Ahead-Strommärkten. Master’s thesis, TU-Darmstadt, Nov. 2009.

- Niu et al. [2005] H. Niu, R. Baldick, and G. Zhu. Supply function equilibrium bidding strategies with fixed forward contracts. Power Systems, IEEE Transactions on, 20(4):1859–1867, 2005.

- O’Neill et al. [2005] R. O’Neill, P. Sotkiewicz, B. Hobbs, M. Rothkopf, and W. Stewart. Efficient market-clearing prices in markets with nonconvexities. European Journal of Operational Research, 164(1):269–285, 2005.

- Pindyck and Rubinfeld [2005] R. S. Pindyck and D. L. Rubinfeld. Microeconomics. Pearson Prentice Hall, Upper Saddle River, NJ, 6. ed., internat. ed. edition, 2005. ISBN 0131912070.

- Tirole [1988] J. Tirole. The Theory of Industrial Organization. MIT Press, Cambridge, 1988. ISBN 0262200716.

- Van Vyve [2011] M. Van Vyve. Linear prices for non-convex electricity markets: models and algorithms. CORE Discussion Papers 2011050, Université catholique de Louvain, Center for Operations Research and Econometrics (CORE), 2011. URL http://EconPapers.repec.org/RePEc:cor:louvco:2011050.

- Wang et al. [2011] G. Wang, U. Shanbhag, T. Zheng, E. Litvinov, and S. Meyn. An extreme-point global optimization technique for convex hull pricing. In Power and Energy Society General Meeting, 2011 IEEE, pages 1–8, San Diego, 2011. 10.1109/PES.2011.6039395.

10 Simplifications of the flow price condition

Proof 10.1 (Proof of eq. (11).).

Suppose that there is no ramping on any interconnector. Then we have for all so that with (9) and (10) it follows that for all and . Equation (6) before simplifies to

| (33) |

We also know that implies and that implies . Together with (33) we therefore conclude

Using this equation we can interpret the term as the shadow price of available transmission capacity: an additional unit of transmission capacity increases the economic surplus by euro (on a sufficiently small interval).

Proof 10.2 (Proof of eq. (12).).

Suppose that there is ramping on the interconnector and that the ramping condition (C2) is only binding in the two consecutive time slots and . Suppose further that there is still available transfer capacity in that time window. In other words we have and . Together with equation (7) and (8) it follows that . We assume that the ramping condition is active only between hour and , and that it is active in forward direction (see Figure 7). This yields that and for all with we have . Thus and vanish, except for . From equation (6) and (5) we get

These statements together provide , , and . We can now interpret the variables as the shadow prices for ramping, in short the ramping prices. Here the economic surplus could by increased by euro if the ramp rate would be increased by one unit (again on a sufficiently small interval).

11 MIP formulation of the filling condition

The filling condition can be easily formulated using binary auxiliary variables. For each linear bid curve we introduce a binary variable . Without loss of generality we assume that the linear bid curves are sorted at first by areas and hours, and then by descending prices, that is,

Recall that . The filling condition can now be formulated like this:

Note that the presented algorithms do not rely on the inclusion of this condition. In fact, including it does not impede the solving process. The slowdown arises due to the inclusion of the filling condition combined with the price conditions of combinatorial bids. This is due to having also to formulate the flow price condition by using a complicated MIP formulation and this condition cannot be solved fast enough by standard solvers.

12 Presolving

Before starting the optimization process, we can compute upper and lower bounds for the prices. For every area and hour we can determine the intersection of the hourly net curve with the price axis. This price would be the clearing price if no block bid would be executed and no power would be imported or exported. Now we assume that we have to import as much additional power as possible and that all supply block bids are executed. The additional power must be bought by hourly bids, thus the price decreases along the hourly net curve until all additional power is consumed by hourly bids. This price represents a lower bound for the specific area and hour. Upper bounds can be determined similarly.

Formula (34) is directly derived from the clearing constraint (C1) and shows the upper and lower quantity bounds of the hourly net curves. The price bounds can be derived from these quantity bounds.

| (34) |

With the help of these bounds the execution state of the blocks and hourly bids that always realize a profit or incur a loss is given. The bounds can also be used to cut off infeasible classes of bid selections in the branch-and-cut tree. We implemented theses techniques, but unfortunately the solving process could not be enhanced significantly.

#

Comb.

Linear

Solver 2.1.2

Bid Cut Heuristic

BnC Decomposition

Bids

Bid Curves

Comp. Time

Rel. Gap

PRBs

Comp. Time

Rel. Gap

PRBs

Comp. Time

Rel. Gap

PRBs

1

742

34536

299000

0

4

2632

0

4

6621

0

4

2

727

34726

* 821000

4.00E-10

8

3101

0

7

600565

0

7

3

792

35227

208000

3.19E-09

5

2017

3.19E-09

5

600562

3.19E-9

5

4

750

34733

476000

4.77E-08

10

2621

4.61E-08

7

600334

4.61E-8

7

5

685

32613

190000

4.64E-08

10

1881

0

6

4929

0

6

6

630

30065

350000

0

3

1086

0

3

3992

0

3

7

775

34516

* 883000

1.34E-08

8

2615

1.31E-08

7

600251

1.31E-8

7

8

772

33545

243000

2.22E-07

8

2260

1.70E-07

6

600339

1.70E-7

6

9

542

34876

578000

2.30E-07

5

2528

0

1

12653

0

1

10

595

31226

576000

1.99E-08

6

2199

0

5

53924

0

5

11

585

31888

116000

2.51E-06

17

10102

9.49E-07

5

600247

8.85E-7

5

12

598

33262

396000

4.51E-07

8

1968

0

3

9831

0

3

13

435

29590

112000

2.74E-06

9

9970

1.14E-06

7

600213

1.14E-6

7

14

558

31959

460000

3.63E-06

18

4531

1.84E-06

5

600232

1.84E-6

5

15

593

35384

399000

0

2

2143

0

2

7845

0

2

16

583

36302

248000

3.29E-06

9

2868

2.83E-06

2

600339

2.83E-6

2

17

585

37046

602000

3.78E-07

11

5676

1.88E-07

5

600272

1.88E-7

5

18

155

18195

111000

0

1

493

0

1

1114

0

1

19

149

18287

61000

0

1

543

0

1

1135

0

1

20

453

30471

141000

2.29E-07

9

1235

2.20E-07

2

600178

2.20E-7

2

21

201

30027

123000

3.21E-06

12

1871

0

3

6824

0

3

22

675

30027

149000

1.73E-06

12

1824

1.50E-06

5

600225

1.50E-6

5

23

701

31559

135000

5.85E-06

27

34961

5.92E-07

12

600210

5.92E-7

12

24

728

29902

440000

3.43E-06

4

1334

3.43E-06

4

600183

3.43E-6

4

25

651

30196

268000

3.24E-06

11

2366

3.11E-06

7

600216

3.11E-6

7

26

642

28589

162000

5.18E-06

4

2090

5.16E-06

3

600237

5.16E-6

3

27

622

31692

342000

3.40E-06

21

2720

3.25E-06

7

600177

3.25E-6

7

28

604

31535

268000

1.08E-07

4

1551

2.59E-08

3

600204

2.59E-8

3

29

707

33882

611000

5.34E-06

7

3430

5.33E-06

6

600201

5.33E-6

6

30

665

33821

249000

1.04E-08

2

1656

1.04E-08

2

600285

1.04E-8

2

31

684

33975

609000

2.39E-05

68

62814

5.04E-06

12

600231

5.04E-6

12

32

599

27453

181000

8.31E-06

6

2597

8.32E-06

6

600243

8.31E-6

6

33

420

27247

176000

9.49E-06

3

1227

9.49E-06

3

600222

9.49E-6

3

34

163

24801

46000

0

0

802

0

0

2620

0

0

35

142

26142

99000

2.40E-08

1

1020

0

1

3090

0

1

36

618

31584

362000

1.57E-07

12

2189

2.23E-07

7

600226

1.23E-7

7

37

249

27231

94000

0

1

1003

0

1

4403

0

1

38

609

29589

152000

3.78E-07

27

2279

4.41E-09

11

600224

4.41E-9

11

39

297

30596

102000

7.50E-07

7

1342

0

1

5729

0

1

40

318

30068

247000

0

2

1681

0

2

6123

0

2

*) Computing time was extended in this test so that the

inclusion phase could be finished.

#

Comb.

Linear

Solver 2.1.2

Bid Cut Heuristic

BnC Decomposition

Bids

Bid Curves

Comp. Time

Rel. Gap

PRBs

Comp. Time

Rel. Gap

PRBs

Comp. Time

Rel. Gap

PRBs

41

253

27288

158000

6.43E-08

5

1062

0

2

4626

0

2

42

604

29969

358000

7.12E-05

2

1459

7.12E-05

2

600261

7.12E-5

2

43

644

32188

361000

1.96E-07

9

1658

2.89E-08

4

600246

2.89E-8

4

44

683

32477

232000

0

2

1387

0

2

4125

0

2

45

695

33131

608000

1.64E-06

7

6630

1.62E-06

4

600293

1.62E-6

4

46

576