Tanaka’s equation on the circle and stochastic flows

Abstract

We define a Tanaka’s equation on an oriented graph with two edges and two vertices. This graph will be embedded in the unit circle. Extending this equation to flows of kernels, we show that the laws of the flows of kernels solutions of Tanaka’s equation can be classified by pairs of probability measures on , with mean . What happens at the first vertex is governed by , and at the second by . For each vertex , we construct a sequence of stopping times along which the image of the whole circle by is reduced to . We also prove that the supports of these flows contain a finite number of points, and that except for some particular cases this number of points can be arbitrarily large.

Hatem Hajri(1)(1)(1)Université du Luxembourg, Email: Hatem.Hajri@uni.lu and Olivier Raimond(2)(2)(2)Université Paris Ouest Nanterre La Défense, Email: oraimond@u-paris10.fr

1 Introduction

Consider Tanaka’s equation

| (1) |

where is a Brownian motion on (that is and are two independent standard Brownian motions) and is a stochastic flow of mappings on . We refer to [5] for a precise definition. Roughly, and are equal in law, for any sequence of non-overlapping intervals the mappings are independent, and we have the flow property: for all , , a.s. . In [6], (1) is extended (1) to flows of kernels. A stochastic flow of kernels is the same as a stochastic flow of mappings, but the mappings are replaced by kernels, and the flow property being now that for all , , a.s. (with the usual composition of kernels). For and , is a probability measure on which describes the transport by the flow of a Dirac measure at from time to time . A simple example of flow of kernels is , where is a stochastic flow of mappings.

By applying Itô’s formula, it is easy to see that solves (1) if and only if, setting , we have for all , and ( is on and are bounded), a.s.

| (2) |

Now, if is a stochastic flow of kernels and is a Brownian motion on , we will say that ) solves Tanaka’s equation if and only if (2) holds for all , and . To give an intuitive meaning of this SDE, the transport by a solution is governed by on and by on , but with possible splitting at . We will also be interested in diffusive solutions of Tanaka’s equation, i.e. solutions that cannot be written in the form . The main result of [6] is a one-to-one correspondence between probability measures on with mean and laws of solutions to (2). Denote by , the law of the solution associated to . Then

where

and where is independent of , with law . In particular, when , then and is -measurable; this is also the unique -measurable solution of (2).

For , we recover the unique flow of mappings solving (1) which was firstly introduced in [8]. In [2], a more general Tanaka’s equation has been defined on a graph related to Walsh’s Brownian motion. In this work, we deal with another simple oriented graph with two edges and two vertices that will be embedded in the unit circle .

A function defined on is said to be derivable in if

exists. Let be the space of all functions defined on having first and second continuous derivatives and . Let be the space of all probability measures on and be a sequence of functions dense in . We equip with the following distance and its associated Borel -field:

| (3) |

In the following, denotes the argument of and in all the paper is a fixed parameter in . Define for ,

and denote by (or simply by since will not vary) the graph embedded in with two vertices and and two edges and with orientation given by (see Figure 1 below).

Definition 1.

On a probability space , let be a Brownian motion on and be a stochastic flow of kernels on . We say that solves Tanaka’s equation on denoted if for all , and , as.

| (4) |

If is a solution of and with a stochastic flow of mappings, we simply say that solves .

If is a solution of , then following Lemma 3.1 of [6], we have (see Lemma 3 (ii) below). So we will simply say that solves .

In this paper, given two probability measures on , and with mean , we construct a flow solution of . Let be such that given , the flows and are independent and has for law . The flows and provide the additional randomness when passes through or . Away from these two points, just follows on and on . We now state our first result.

Theorem 1.

-

(1)

Let and be two probability measures on satisfying

(5) There exist a stochastic flow of kernels (unique in law) and a Brownian motion on such that solves and such that if , and

then conditionally to , a.s.

and conditionally to , is independent of and has for law .

-

(2)

For all flow solution of , there exists a unique pair of probability measures satisfying (5) such that .

Contrary to Tanaka’s equation, where flows are concentrated on at most two points, flows associated to have nontrivial supports. The version defined in Theorem 1 (1), and constructed in Section 2, satisfies Proposition 1 and Proposition 2 below. Proposition 1 shows the existence of some times at which the support of is only concentrated on a single point. For all , let

| (6) |

Proposition 1.

-

(1)

There exists an increasing sequence of -stopping times such that a.s. and for all and all .

-

(2)

There exists an increasing sequence of -stopping times such that a.s. and for all and all .

The next proposition shows that the support of may contain an arbitrary large number of points with positive probability (more informations can be found in Section 5).

Proposition 2.

Assume that and are both distinct from . Then there exists a sequence of events and a sequence of -stopping times such that for all ,

-

(i)

,

-

(ii)

a.s. on .

We also mention that all the sequences of stopping times discussed in the previous two propositions will be constructed independently of . They take values in where and for . Set, for ,

where and are distinct from . Then is a strong Markov chain on Proposition 1 asserts that and are recurrent for this chain. Proposition 2 asserts that for all , both and (by analogy) communicate with . So one can deduce the following immediate

Corollary 1.

For all , is a recurrent set for (i.e. a.s. for infinitely many ).

Even that the supports of the flows may be concentrated on arbitrarily many points at some times, these random sets are always finite in the following sense: a.s.

Let us describe the organization of this paper. In Section 2, we prove the first part of Theorem 1. The proof of the second part will be the subject of Section 3. In Section 4, we prove Proposition 1. Section 5 gives some informations about the support of and proves Proposition 2.

2 Construction of flows associated to

Fix two probability measures and on with mean .

2.1 Coupling flows associated with two Tanaka’s equations on .

In this section, we follow [6]. By Kolmogorov extension theorem, there exists a probability space on which one can construct a process taking values in such that (i), (ii), (iii), (iv) and (v) are satisfied, where

-

(i)

for all and is a Brownian motion on .

-

(ii)

Given , and are independent.

-

(iii)

For fixed , is independent of and

In particular

-

(iv)

Define for all

Then for all and , then

(7) -

(v)

For all and with , the law of knowing and is given by

when and is otherwise given by

on the event with .

Note that (i)-(v) uniquely define the law of

for all , This family of laws is consistent by construction.

Note in particular that, when (iv) is satisfied for and with , then (v) properly defines the law of knowing and , and we have that (iv) also holds for and with .

For , , define

and set

Recall the following

2.2 Modification of flows.

For our later needs, we will construct modifications of and of which are measurable with respect to . On a set of probability , define for all , and

Then, we have the following

Lemma 1.

(i) For all , a.s.

(ii) Consider the random sets

Then a.s. for all and in ,

Proof.

(i) By (7), a.s. for all such that , we have

Fix . With probability , is attained in and thus a.s. there exists such that

| (8) |

Taking the limit, we get a.s. From (7) and (8), we also have that a.s. and (i) is proved.

(ii) With probability , for all and in , if , then , which implies that

and thus that and that . ∎

We may now consider the following modifications of and defined for all by

Then Theorem 2 holds also for (because (i), (ii), (iii) and (iv) stated at the begining of Section 2.1 are satisfied by ).

Lemma 2.

(i) The mapping

is measurable from into .

(ii) For all , a.s.

Proof.

(i) Clearly, the mapping

is measurable. For all , we have

which shows that is measurable and a fortiori is also measurable. (ii) is a consequence of Lemma 1 (i). ∎

To simplify the notation, throughout the rest of the paper, we will denote simply by .

2.3 The construction of .

In this paragraph, we construct a stochastic flow of kernels and a stochastic flow of mappings respectively from and from . Let

| (9) |

We first define . For , set

and for and , set

where

Note that on , we have and consequently . Also, on , we have and so .

Since and are measurable, it follows from Lemma 2 that

is measurable from into . Now we consider the sequence of stopping times such that and for .

Define for all ,

Then is measurable from into . By the same way, we define for

and for and

Define now for all ,

Then is measurable from into .

For every choice , is measurable and these -fields are independent for by construction. This implies the independence of the family . It is also clear that the laws of and only depend on .

2.4 The flow property for and .

To prove the flow property for both and , we start by the following

Proposition 3.

Let and be two finite -stopping times such that . Then a.s. for all , we have

and

Proof.

Define

Then (see Lemma 1 (ii)). It is also known that (see [3] page 94). We will prove the proposition on the set of probability : and we first prove the result for . From now on, we fix . Define

Then . For all , set and .

(i) Let . Then as , we have and

since . Therefore and .

(ii) Let . Then, we still have and . Recall that

and

Suppose for example , then and so (and a fortiori ) for all . From the definition,

If , then . Suppose that , then and . Since , we have

In other words, and are in so that and .

(iii) Let . Assume for example that , then since and

As , it follows that (if , then ), and so . As , we necessarily have . Thus if ,

and if ,

Since , we have and . On the other hand, since ,

But (from ), (from which entails that ). Consequently and so . The case can be done similarly.

(iv) Let . Assume for example that so that . Consider the first case: . Then and

If , then and .

If , then and .

Since , we have . Moreover , which implies (since ).

Now, if satisfies , then . If not, and are in . This implies and exactly as in (ii).

Assume now that , then satisfies (recall that ) and as before.

The result for can be proved by replacing by in and . However, the proof remains similar.

∎

Corollary 2.

Let be two finite -stopping times. Then, with probability 1, for all , we have

and

Proof.

Fix and define the family of -stopping times by and for . As is increasing, we have for all . Applying successively Proposition 3, we have a.s. for all , and all ,

and for all ,

On , we have for all whence a.s. on , for all and all ,

and

Now define the family of -stopping times by and for . Then for all , . Applying again Proposition 3, we get a.s. for all , and all ,

and for all ,

On , we have for all . Consequently a.s. on , for all , and all ,

and for all .

We have thus shown that a.s. for all and all ,

By summing over , we get that a.s. , , . The flow property for holds by the same reasoning. ∎

2.5 can be obtained by filtering .

Proposition 4.

For all , all and all continuous function , a.s.

Proof.

Fix and . Properties (ii) and (iii) of Section 2.1 imply that a.s.

Define

If is a random variable independent of , then a.s.

| (10) |

For and , let and for let . Note that and . Then since and are stochastic flows, . By Corollary 2, a.s.

and

Recall that the -fields are independent. Then, using (10), we get that a.s.

and therefore a.s.

To finish the proof, it remains to prove that as . Write

Let . Then

We have . Let , then

(see [3] page 80). By the change of variable , the right hand side converges to as which finishes the proof. ∎

2.6 The continuity.

To conclude that and are two stochastic flows, it remains to prove the following

Proposition 5.

For all , and , we have

Proof.

By Jensen’s inequality and Proposition 4, it suffices to prove the result only for and by the proof of Lemma 1.11 [5] (see also Lemma 1 [2]), this amounts to show that

| (11) |

where and are fixed from now on. For each , let and denote and simply by and .

First case : . For , we have and

If and , then , thus in the right-hand side, the second term equals . Since and , it is clear that as and similarly as . Thus (11) holds for and by the same way for .

Second case : . For all , we have

where

which converges to as . Let us prove that

For , write

Since and move parallely until one of them hits or , it comes that

Now

Obviously . Set , then a.s. on , we have by Corollary 2 and . Recall that for all and consequently for all (by the definition of ). This shows that a.s. on , we have

Finally and by interchanging the roles of and , we have . Similarly

so that (11) is satisfied for all . By the same way, it is also satisfied for all . ∎

2.7 The flows and solve .

In this paragraph we prove the following

Proposition 6.

Both and solve .

Proof.

First we check the result for . We will denote simply by and the mapping by to avoid any confusion. An important consequence of the modifications defined in Section 2.2 which is the key argument here is that is a Brownian motion for any finite -stopping time . To justify this, consider a finite -stopping time and for and , set

Let , then a.s. and for large enough, we have and . Lemma 1 (ii) implies that a.s. for large enough . Thus a.s.

| (12) |

Let and take a family of bounded continuous functions from into . Using the independence of increments and the stationarity of , we have

Since is a Brownian motion, the same holds for . Now the rest of the proof will be divided into three steps.

First step. Let be a finite -stopping time. Then for all , a.s. ,

We first prove this for . By Itô’s formula, for all a.s. ,

Tanaka’s formula for local time yields a.s. ,

where is the local time in of . By construction, for all . So we can deduce from the previous line that a.s. ,

Thus by unicity of the Doob-Meyer decomposition, a.s. ,

Since a.s., we get a.s. ,

Recall that for all , thus the first step holds for . The first step is similarly satisfied for and for all by distinguishing the cases and .

Second step. Let be a finite -stopping time, , . Then is independent of .

Clearly

Fix , then a.s. are in . Take a family of bounded continuous functions from into and let . By (12), we have

For large enough , we have

with . Now using the independence of increments and the stationarity of , the second step easily holds.

Third step. solves .

Denote simply by . Then a.s. for all and , is continuous on . Consequently for all , a.s. is continuous on and in particular, is measurable. Now fix and define for all ,

Then a.s. is measurable from into . Moreover is -measurable and a.s. for all by the first step. The second step yields a.s. and we may replace by directly in the stochastic integral so that, using the flow property, we get

By induction, we have a.s.

This implies that solves . The fact that solves is similar to Proposition 4.1 (ii) in [6] using Proposition 4. ∎

3 Flows solutions of

From now on is a solution of defined on a probability space . Fix and , then can be modified such that, a.s. the mapping is continuous from into . It is the version we consider henceforth for all fixed and .

Lemma 3.

(i) For all and , denote . Then a.s.

(ii) .

Proof.

(i) We follow Lemma 3.1 [6]. Define

| (13) |

Fix and let

Let such that if . By applying in , we have for ,

| (14) |

By applying in and using (14), we also have for ,

Thus that for ,

By continuity a.s.

The fact that easily follows.

(ii) Let be a sequence in such that as for all . Applying in , we get

It is easy to check that converges towards in as whence in

which proves (ii). ∎

3.1 Unicity of the Wiener solution.

Our aim in this section is to prove that admits only one Wiener solution (i.e. such that ). This solution is with . For this, we will essentially follow the general idea of [4]: the Wiener solution is unique because its Wiener chaos decomposition can be given (see (15) and (16) below). Let be semigroup of the standard Brownian motion on . Then the semigroup of the Brownian motion on writes

For all , we easily check that and . Let be the generator of .

Proposition 7.

Equation has at most one Wiener solution: If is a solution such that , then and all ,

| (15) |

where

| (16) |

no longer depends on and .

Proof.

Let be a solution of (not necessarily a Wiener flow). Our first aim is to establish the following

Lemma 4.

Fix and . Then

Proof.

Let and denote simply by . Note that the stochastic integral in the right-hand side is well defined:

and the right-hand side is smaller than . Now

For all , set and so by replacing by in , we get

Then we can write

where

Using for a bounded measurable function, we see that is less than

Since , this shows that converges to as . Note that is the sum of orthogonal terms in . Consequently

By applying Jensen’s inequality, we arrive at

where . For all , we have

Consequently

and one can deduce that tends to 0 as in . Now

Set . Then for all . By the Cauchy-Schwarz inequality

If :

Therefore , where

and

From and , we get

As , tends to obviously. On the other hand, and so

Now we easily verify that are uniformly bounded with respect to and . As a result tends to as . This establishes Lemma 4. ∎

Consequences: Let be the unique Wiener solution of . Since , we can define the stochastic flow obtained by filtering with respect to (Lemma 3-2 (ii) in [5]). Then, for all and all , a.s.

As a result, solves also and by the last proposition, for all and all , a.s.

| (17) |

3.2 Proof of Theorem 1 (2).

Using the flow property and the independence of increments satisfied by , it is easily seen that the law of for all and therefore the law of is uniquely determined by the knowledge of the law of for all . In the sequel, we will show the existence of two probability measures and on with mean such that for all which will imply Part (2) of Theorem 1.

3.2.1 A stochastic flow of mappings associated to .

Let be the consistent family of Feller semigroups associated to . By Theorem 4.1 [5], a consistent family of coalescent Markovian semigroups is associated to . The Feller process associated to (resp. to ) will be called the -point motion of (resp. to ). The consistent family will be such that

-

(i)

The -point motion of up to its entrance time in is distributed as the -point motion of up to its entrance time in , where .

-

(ii)

The -point motion of is such that if then for all , .

A possible construction of such a family is the following. Fix and let be the point motion started at associated to . Let

For , define . Let be such that and where . Then define the process

Now set

For , we define and so on.

In this way, we construct a Markov process . It is the point motion of the family of semigroup . Note that such a construction does not insure that these semigroups are fellerian.

Lemma 5.

is a consistent family of coalescent Feller semigroups associated with a flow of mappings .

Proof.

For each , let be the two point motion started at associated with constructed as in Section 2.6 [5] on an extension of such that the law of given is . Define

By Theorem [5], we only need to check that: for all and

Fix and .

First case . Recall that for all where , we have

This shows that when , is supported on and so or . Moreover, by Lemma 3 (i), if , then for all where .

Let with close to such that and write

Since tends to as goes to , we have . Moreover

where . Obviously

with . On , we have and thus . As a result

Since the right-hand side converges to as , is satisfied for .

Second case . By analogy is satisfied for . Let and be close to , then and move parallely until one of them reaches or say at time . Since is Feller, the strong Markov property at time and the established result for allows to deduce for .

∎

Consequences: By the proof of Theorem 4.2 [5], there exists a joint realization on a probability space where and are two stochastic flows of kernels satisfying , and such that:

-

(i)

is a stochastic flow of kernels on ,

-

(ii)

For all , a.s. .

To simplify notations, we will denote by . Recall that (i) and (ii) are also satisfied by the pair constructed in Section 2.3. Now (ii) rewrites, for all ,

| (18) |

and using (17), we obtain, for all ,

| (19) |

with being the Wiener solution.

3.2.2 The law of .

Recall the definitions of and from (13) and set for all ,

Proposition 8.

Recall the definition of from (9). Then

-

(i)

There exist two probability measures and on with mean such that for all , conditionally to , is independent of and has for law . Moreover, for all , a.s. ,

where

-

(ii)

For all , conditionally to , and are independent.

The proof of (i) essentially follows [6] and will be deduced after establishing the lemmas 6,7,8,9 and 10 below.

For all , define and recall the definition of from (6). When , we denote simply by . We will always consider the usual augmentations of these -fields which include all -negligible sets and are right-continuous. For each each , recall that is continuous from into . Denote by the law of which is a probability measure on , then since is a Feller process (see Lemma 2.2 [5]) the following strong Markov property holds

Lemma 6.

Let and be a finite -stopping time. On , the law of knowing is given by .

Let

Thanks to (19), on the event , a.s.

By the continuity of , this shows that a.s.

| (20) |

Let such that , . Using (18), the fact that and the continuity of , we have a.s. ,

Thus a.s. and can be expressed as

| (21) |

Define the -fields:

By Lemma 4.11 in [6], we have . Let be a bounded continuous function and set

By (18), the process is constant on the excursions of out of before .

Lemma 7.

There exists an -progressive version of denoted that is constant on the excursions of out of before and satisfies a.s.

Proof.

We closely follow Lemma 4.12 [6] and correct an error at the end of the proof there. By induction, for all integers and , define the sequence of stopping times and by the relations: and for ,

In the following will denote . For all , on , we have as. Let . Since is independent of , we have which is measurable. Set and define

Then is -progressive. For all , set , then is -progressive and for all , a.s. Indeed, fix and on the event , choose and such that , then . For all , there exists an integer such that . Thus since and belong to the same excursion interval of containing also . Now set and for all . Then is a modification of which is -progressive and constant on the excursions of out of before . Moreover a.s. ∎

We take for this -progressive version. Then is measurable.

Lemma 8.

.

Proof.

The previous lemma implies that is independent of (Lemma 4.14 [6]) and the same holds if we replace by where . For such that , define inductively and for :

Set . Then, we have the following

Lemma 9.

For all , conditionally to , are independent and have the same law (which depends on but no longer depends on ).

Proof.

We prove the result by induction on . For , this has been justified. Suppose the result holds for and let be an approximation of as in the proof of Lemma 3 (ii). For a fixed , in , we have

On , we have and therefore, in ,

| (22) |

As , a.s. Choose a family of bounded continuous functions on . For any , we will use the notation to denote the expectation under . Set , then using (22) and Lemma 6 at time , we get

Since , we have by the induction hypothesis

In conclusion

The last identity remains satisfied if we replace by a finite product

. As a result, for all bounded continuous ,

Iterating this relation, yields

In particular, for all ,

This completes the proof. ∎

Let be the law of and be the law of under . Then, we have the

Lemma 10.

The sequence converges weakly towards . For all , under , and are independent and the law of is given by .

Proof.

For each bounded continuous function

Consequently

The left-hand side no longer depends on , which completes the proof. ∎

By analogy, we define the measure such that if , then for all , under , and are independent and . Recall the definition , then for all , the law of (respectively ) knowing is given by (respectively ).

Now take and fix . Similarly to (20), we can deduce from (19) that a.s. for all ,

Note that is constructed such that for all as. and collide whenever they meet. So a.s. for all ,

By (18), the second claim of Proposition 8 (i) holds.

Proof of Proposition 8 (ii)

We first prove the following statements: For all , we have

-

(a)

Conditionally to , are independent and (resp. ) has for law (resp. ).

-

(b)

Let

Then, conditionally to , are independent and the law of (resp. ) is (resp. ).

-

(c)

Conditionally to , are independent.

-

(d)

Conditionally to , are independent.

(a) Note that and with . Now (a) holds from Proposition 8 (i) and using the independence of and .

(b) By (a), it suffices to show that on (which is a subset of ), a.s. and . The first equality is clear since is constant on the excursions of on and on , and belong to the same excursion of . Moreover, on , we have and so a.s.

Clearly and therefore for all (using the coalescence property of and the independence of increments). On , and by the flow property of , a.s.

Using (18), we get a.s. .

(c) For all , let and . Define for ,

Then by writing

and using that is -measurable, (c) easily holds from (b).

(d) By analogy with (c), conditionally to , are independent. Now (d) holds after remarking that as. .

Finally Proposition 8 (ii) holds for and thus for all using the stationarity of .

Now the proof of Proposition 8 is completed. ∎

Proposition 9.

We have .

Proof.

Like in Section 2.3, extending the probability space, we can construct a flow such that has the same law as . By Proposition 8, for all , conditionally to . For and , let and define , . Then by the independence of increments of and ,

Recall that as (see the proof of Proposition 4). Letting and using the flow property for both and , we deduce that . ∎

Remark 1.

Let be the coalescing flow constructed in Section 2, then . As before this remains to show that conditionally to , is distributed as . However the situation is more easy here and we do not need the lemmas 6,7,8,9 and 10. For example

is independent of conditionally to where is the distance to since is a Brownian motion on . Following Proposition 9, we check that . In particular solves .

4 Proof of Proposition 1

In this section, we use the same notations as in Section 2. For , we denote simply by . For all define

We will further need the following

Lemma 11.

For all and , we have .

Proof.

Fix and let such that . Now define the sequence of stopping times such that and for ,

Let . Then on , and for all ,

Moreover . Since and , this proves the lemma. ∎

Let . Since , we deduce that . Obviously . Since , we have . Remark also that

This shows that on , we have and similarly on , we have .

4.1 The case .

This is the more easy case.

Lemma 12.

With probability , for all , we have

and

Proof.

This lemma is a consequence of the facts that and that . Let us just explain why implies for all . Fix . To simplify, assume . It holds that and that . Then on the event and on the event . Now, if , then (this thus implies that ). And if , then (this thus implies that ). To conclude in this case, we use the flow property . It remains to remark that . ∎

4.2 The case .

The key argument to prove Proposition 1 in this case is to find some conditions on the path of under which the image of the whole circle by at some specific time is reduced to .

We fix such that . For any -finite stopping time and define

and

Let

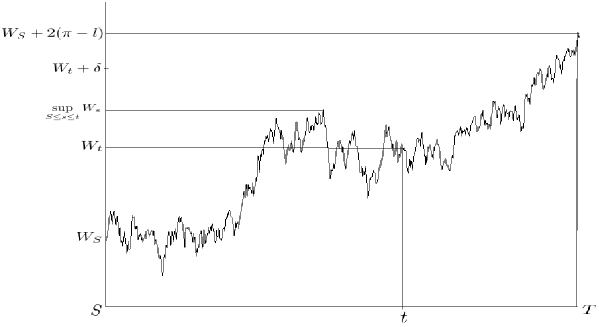

The event is the event ”for all we have ”. Setting , this event can be represented by the following figure (Figure 2).

On the event , for all and . Thus on this event, we have and a fortiori for any intermediate point such that . In other words,

Note that is independent of and that and does not depend on .

When , which is also the first time when

Then at time , we have for all . Applying the flow property, we see that on , for all . Now the rest of the proof will only require an application of the Borel-Cantelli Lemma.

We give the details in the following.

Define the sequence of -stopping times by and for (note that . Then set, for ,

Note that the events and are independent. The following proposition describes what happens on .

Proposition 10.

With probability , for all , on , we have for all ,

-

(i)

.

-

(ii)

If , then .

-

(iii)

.

-

(iv)

and .

Proof.

We take (the proof is similar for all ). Denote simply by and by .

(i) Fix . If , then .

On , we have and so (see the lines after Lemma 11). Consequently and .

Suppose , then necessarily and using that , we have

Since , we have and therefore . It is also clear that which proves the first statement.

(ii) Let with . Then arrives to before and this happens at time . Thus reaches before . Let be the greatest integer such that . Then where . Clearly . Therefore . But for all and so . As , we get . That is .

(iii) and (iv) are immediate from the flow property (Corollary 2) and (i), (ii). The result for can be proved by following the same steps with minor modifications.

∎

Since for all , is an -stopping time, the sequence is independent. We also have for all . By Lemma 11, and the Borel-Cantelli lemma yields . We deduce that with probability 1,

To deduce Proposition 1, we only need to extract from a subsequence with the preceding property satisfied for all and not just for infinitely many . This is the subject of the following

Lemma 13.

Let be the sequence of random integers defined by and for ,

Set . Then is a sequence of -stopping times such that a.s. , and for all .

Proof.

Remark that for all . For all and , we have

It remains to prove that . We will prove this by induction on . For , this is clear since and for ,

Suppose the result holds for . Then for all ,

and the desired result holds for using the induction hypothesis. ∎

We have proved Part of Proposition 1 (for both and . Part can be deduced by analogy.

5 The support of (Proof of Proposition 2)

In this section and will be denoted simply by and .

5.1 The case .

When and are both different from , a precise description of can be given as follows. Recall the definitions of the sequences and from Section 4.1 and set . Then for all ,

and for all ,

In fact, for all ,

with being the unique reflecting Brownian motion on (see [1]) solution of

and

If , then is a Wiener flow such that for all .

5.2 The case .

From the definition of , is carried by at most two points for all , and . Using the flow property and the fact that a.s., it is therefore clear that a.s.

We assume in this section that and are both distinct from (for the other case, see Remark 2 below).

Fix a decreasing positive sequence such that . Now define

and for ,

We are going to prove the following

Proposition 11.

Let and for all . Then for all ,

-

(i)

,

-

(ii)

a.s. on .

Moreover a.s. for all

-

(ii1)

On ,

with for all ,

(Note that .)

-

(ii2)

On , we have

with for all ,

(Note that .)

To prove this proposition, let us first establish the following

Lemma 14.

Fix and define

where . Then

Proof.

Recall the definition of from the begining of Section 4. Consider the event

Using the Markov property at time , we have . Note that can be expressed as

On , we have and so . Moreover, on

In other words which proves the inclusion and allows to deduce the lemma. ∎

Proof of Proposition 11

(i) The sequence is independent and therefore we only need to check that for all . But this is immediate from Lemma 14 for even. By replacing with , it is also immediate for odd.

(ii) We denote the properties (ii1) and (ii2) respectively by and . Let prove all the by induction. First and are clearly satisfied since and on . Suppose that all the hold for all where . On , for all since for all , we have

Moreover, on , we have

Thus for all , we have

so that holds. Similarly, on , cannot reach before since for all ,

Moreover, on ,

Thus, on , for all and easily holds.

Remark 2.

When , by considering

and then , we similarly show that may be sufficiently large with positive probability.

Acknowledgement

The first author is grateful to Yves Le Jan who suggested to him this problem as a part of his Ph.D.

References

- [1] R. F. Bass and E. P. Hsu. Pathwise uniqueness for reflecting brownian motion in euclidian domains. Probab. Theory and Rel. Fields 117, pp. 183-200., 117(3):183–200, 2000. \hrefhttp://www.ams.org/mathscinet-getitem?mr=1771660MR1771660.

- [2] Hatem Hajri. Stochastic flows related to Walsh Brownian motion. Electronic journal of probability 16, 1563-1599, 2011. \hrefhttp://www.ams.org/mathscinet-getitem?mr=2835247MR2835247.

- [3] Ioannis Karatzas and Steven E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991. \hrefhttp://www.ams.org/mathscinet-getitem?mr=1725357MR1725357.

- [4] Yves Le Jan and Olivier Raimond. Integration of Brownian vector fields. Ann. Probab., 30(2):826–873, 2002. \hrefhttp://www.ams.org/mathscinet-getitem?mr=1905858MR1905858.

- [5] Yves Le Jan and Olivier Raimond. Flows, coalescence and noise. Ann. Probab., 32(2):1247–1315, 2004. \hrefhttp://www.ams.org/mathscinet-getitem?mr=2060298MR2060298.

- [6] Yves Le Jan and Olivier Raimond. Flows associated to Tanaka’s SDE. ALEA Lat. Am. J. Probab. Math. Stat., 1:21–34, 2006. \hrefhttp://www.ams.org/mathscinet-getitem?mr=2235172MR2235172.

- [7] L. C. G. Rogers and David Williams. Diffusions, Markov processes, and martingales. Vol. 2. Cambridge Mathematical Library. Cambridge University Press, Cambridge, 2000. \hrefhttp://www.ams.org/mathscinet-getitem?mr=1780932MR1780932.

- [8] S. Watanabe. The stochastic flow and the noise associated to Tanaka’s stochastic differential equation. Ukraïn. Mat. Zh., 52(9):1176–1193, 2000. \hrefhttp://www.ams.org/mathscinet-getitem?mr=1816931MR1816931.