Minimax estimation for mixtures of Wishart distributions

Abstract

The space of positive definite symmetric matrices has been studied extensively as a means of understanding dependence in multivariate data along with the accompanying problems in statistical inference. Many books and papers have been written on this subject, and more recently there has been considerable interest in high-dimensional random matrices with particular emphasis on the distribution of certain eigenvalues. With the availability of modern data acquisition capabilities, smoothing or nonparametric techniques are required that go beyond those applicable only to data arising in Euclidean spaces. Accordingly, we present a Fourier method of minimax Wishart mixture density estimation on the space of positive definite symmetric matrices.

doi:

10.1214/11-AOS951keywords:

[class=AMS] .keywords:

., , and

t2Supported in part by the Natural Sciences and Engineering Research Council of Canada, Grant DG 46204.

t3Supported in part by Basic Science Research Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Education, Science and Technology (2011-0027601).

t4Supported in part by NSF Grant DMS-07-05210.

1 Introduction

The space of positive definite symmetric matrices has been studied extensively in statistics as a means of understanding dependence in multivariate data along with the accompanying problems in statistical inference. Many books and papers, for example, haff1 , haff2 , haff3 , loh , Muirhead , stein-rietz and stein , have been written on this subject, and there has been considerable interest recently in high-dimensional random matrices with particular emphasis on the distribution of certain eigenvalues johnstone08 and on graphical models lm .

In this paper we consider the problem of estimating the mixing density of a continuous mixture of Wishart distributions. We construct a nonparametric estimator of that density and obtain minimax rates of convergence for the estimator. Throughout this work, we adopt, as a guide, results developed for the classical problem of deconvolution density estimation on Euclidean spaces; see, for example, diggle , fan , Koo , mr , butsy and Zhang . Much of the difficulty with the space of positive definite symmetric matrices is due to the fact that mathematical analysis on the space is technically demanding. Helgason he2 and Terras Terras-II provide much insight and technical innovation, however, and we make extensive use of these methods.

We summarize the paper as follows. In Section 2 we discuss and set up the notation for Wishart mixtures. In Section 3 we begin by reviewing the necessary Fourier methods which allow us to construct a nonparametric estimator of the mixing density, and then we provide the estimator. The minimax property of our nonparametric estimator is stated in Section 4 along with supporting results. Section 5 presents simulation results as well as an application to finance examining real financial data. Finally, Sections 6 and 7 present the proofs.

2 Wishart mixtures

Throughout the paper, for any square matrix , we denote the trace and determinant of by and , respectively; further, we denote by the identity matrix. We will denote by the space of positive definite symmetric matrices.

For with , , the multivariate gamma function is defined as

| (1) |

where denotes the classical gamma function.

We denote by the general linear group of all nonsingular real matrices, by the group of orthogonal matrices and by the group of diagonal positive definite matrices. The group acts transitively on by the action

| (2) |

, , where denotes the transpose of . Under this group action, the isotropy group of the identity in is ; hence the homogeneous space can be identified with by the natural mapping from that sends . In distinguishing between left and right cosets, we place the quotient operation on the left and right of the group, respectively.

For , define the measure

It is well known that the measure is invariant under action (2). Relative to the dominating measure , the probability density function of the standard Wishart distribution with degrees of freedom is

| (3) |

. Consequently, for , we note that and . It then follows that, relative to the dominating measure , the density of the general Wishart distribution, with covariance parameter , is , .

Suppose next that is a random matrix and, relative to the dominating measure , has a continuous mixing density, , that is invariant under the action (2). By integration with respect to , the continuous Wishart mixture density is given by

| (4) |

. For the case in which , the standard Wishart density is essentially a chi-square density, in which case (4) is a continuous mixture of chi-square densities.

In general, (4) is a convolution operation for functions on . We denote by any matrix with , where and denote . Define , the convolution of two random matrices and which are distributed on by

and , the convolution of and by

where is the space of integrable functions raised to the th power on for . If and with densities and , respectively, are independent, then has the density since . Finally, (4) can be transformed into a scalar multiplication; see Section 3.2.

3 Fourier analysis on and estimation of the mixing density

In this section we review the Fourier methods needed to transform the convolution product (4) and to construct a nonparametric estimator of the mixing density .

3.1 The Helgason–Fourier transform

For , denote by the principal minor of order , . For , the power function is

| (5) |

. Let denote the Haar measure on , normalized to have total volume equal to one; then

| (6) |

, is the zonal spherical function on . It is well known that the functions are fundamental to harmonic analysis on symmetric spaces he2 , Terras-II . If are nonnegative integers then, up to a constant factor, (6) is an integral formula for the zonal polynomials which arise in many aspects of multivariate statistical analysis Muirhead , pages 231 and 232.

Let denote the space of infinitely differentiable, compactly supported, complex-valued functions on ; also, let

For and , the Helgason–Fourier transform (Terras-II , page 87) of a function is

| (7) |

where denotes complex conjugation.

3.2 The convolution property of the Helgason–Fourier transform

The following result shows that the convolution operation can be transformed into a scalar multiplication.

Proposition 3.1

Suppose and with densities and , respectively, are independent, and is -invariant. Let be the density of . Then

3.3 The inversion formula for the Helgason–Fourier transform

For with , let

denote the classical beta function. For such that for all , the Harish–Chandra -function is

| (9) |

Let , and set

| (10) | |||||

| (11) |

and

Let be the set of diagonal matrices with entries on the diagonal; then is a subgroup of and is of order . By factorizing the Haar measure on , it may be shown (Terras-II , page 88) that there exists an invariant measure on the coset space such that

The inversion formula for the Helgason–Fourier transform in (8) is that if , then he2 , Terras-II

| (12) |

. In particular, if , then

, and there also holds the Plancherel formula,

| (13) |

We refer to Terras Terras-II , page 87 ff., for full details of the inversion formula and for references to the literature.

3.4 Eigenvalues, the Laplacian and Sobolev spaces

For , we define the matrix of partial derivatives,

where denotes Kronecker’s delta. The Laplacian, , on can be written (Terras-II , page 106) in terms of the local coordinates as

The power function in (5) is an eigenfunction of (see Muirhead , page 229, Richards1 , page 283, Terras-II , page 49). Indeed, let , , and define

| (14) |

then . Since then each , , is purely imaginary; hence, , .

The operator changes the effect of invariant differential operators on functions to pointwise multiplication: if , then

, (Terras-II , page 88). For , we therefore define the fractional power, , of , as the operator such that

. Having constructed , we define the Sobolev class,

where for ,

denotes the -norm with respect to the measure . For , we also define the bounded Sobolev class,

4 Main result

In this section we will present the main result. We do so by applying the Helgason–Fourier transform to the mixture density (4) so that

| (15) |

, ; see Proposition 3.1. Having observed a random sample from the mixture density, , in (4), we estimate by its empirical Helgason–Fourier transform,

| (16) |

On substituting (16) in (15), together with the assumption that , , we obtain

, .

Analogous with classical Euclidean deconvolution, we introduce a smoothing parameter where as , and then we apply the inversion formula (12) using a spectral cut-off based on the eigenvalues of . First, we introduce the notation

where is defined in (11). We now define

| (17) |

, and take this as our nonparametric estimator of .

We now state the minimax result for the estimator (17). Let denote a generic positive constant independent of . For two sequences of real numbers and , we use the notations and to mean and , respectively, as . Moreover, means that and .

Theorem 4.1

Suppose is a density on and . Then, for the Wishart mixture (4),

| (18) |

and for any estimator of ,

| (19) |

We now provide some comments about this result. In the situation where (4) is a finite sum, so that

we have the finite mixture model. Methods for recovering the mixing coefficients can be covered by the techniques employed in chentan . We note that the continuous mixture model is a generalization of this approach.

It is noted that the condition is a density and seems to be mild. The upper bound property of (18) is established in kr2 , Theorem 3.3, with . In the latter, the moment condition

| (20) |

on the principal minors of is assumed. In our theorem, we did not impose this moment condition as condition (20) is automatically satisfied. This is pointed out and commented upon below in the proof.

To derive the lower bound for estimating in the -norm, we shall follow the standard Euclidean approach. Thus we choose a pair of functions , , and, with denoting the Wishart density (3), we shall show that, for some constants ,

and

| (21) |

where

Precisely, let us suppose we can choose and a perturbation , and, for , let be a scaling of such that . Define

If can be chosen so that

then the lower bound rate of convergence is determined by . We shall develop such a construction and, moreover, do so in a way such that as .

Remark 4.2.

The profound influence of Charles Stein on covariance estimation originates largely from his Rietz lecture; see stein-rietz . The idea is that for certain loss functions over , the usual estimator of the covariance matrix parameter is inadmissible. Through an unbiased estimation of the risk function over covariance matrices, Stein was able to improve upon the usual estimator by pooling the observed eigenvalues of the sample covariance matrix. Subsequent to this, through a series of papers, improvements were obtained in Haff haff1 , haff2 , haff3 . Other related works include Takemura takemura , Lin and Perlman linperl and Loh loh , to name a few.

In this paper, we contribute to the case in which one observes data from a continuous mixture of Wishart distributions, not merely a sample from a single distribution. Therefore, the parameter of interest would be the mixing density of the covariance parameters. And the nonparametric estimator of the mixing density (17) is an attractive candidate because of its minimax property. Based on this procedure, one could consider the moment, or mode, of , as a possible estimator of the corresponding population parameters. Alternatively, one could take a nonparametric empirical Bayes approach as in Pensky pensky .

5 Numerical aspects and an application to finance

This section presents numerical aspects for the case with an application to finance.

5.1 Computation of estimators

Suppose and are independentwith having a Wishart distribution. Let where is upper triangular. For visualization, we display estimators of the marginal density for where with and . Let

where denotes the diagonal matrix of eigenvalues of , . Denote by the density of eigenvalues of . Then, the estimator for is given by

| (22) |

Consider the computation of when

so that . From pages 90 and 91 of Terras-II , the spherical function is given by

where Legendre function can be computed using conicalP_0(t, x) in the gsl library in R.

5.2 Simulation

Denote by the Wishart density with degrees of freedom and covariance matrix . We generate data as follows. For :

-

•

generate ;

-

•

generate ;

-

•

do a Cholesky decomposition of , and calculate .

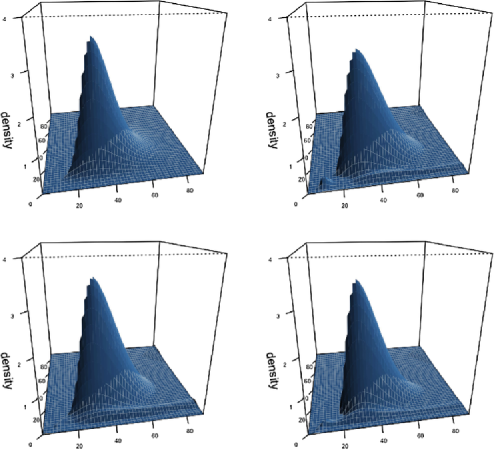

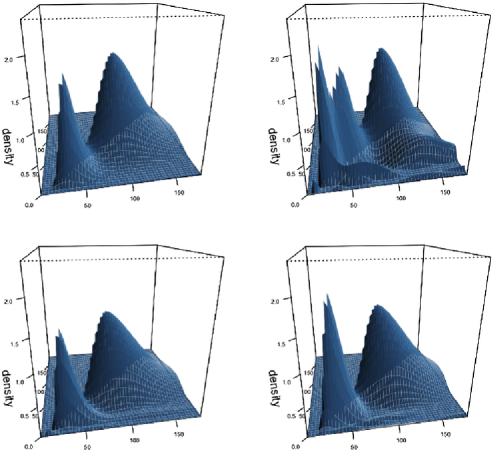

As examples, we consider a unimodal mixing density and a bimodal density . Figure 1 show the results for the unimodal case whereas Figure 2 show the results for the bimodal case. In each of these plots the

domain consists of the two eigenvalues starting with the largest. One can see that the general shapes of the estimators become closer to that of the true density as increases.

5.3 Application to stochastic volatility

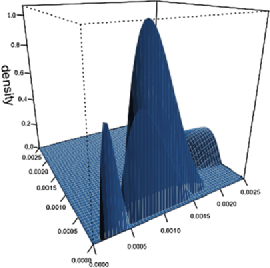

Stochastic volatility using the Wishart distribution is of much interest in finance; see, for example, amu and gs . In particular, this entails a situation precisely of the form (4). Let us apply this to the situation where we are interested in estimating the mixing density.

Although our methods can be applied to a portfolio of many assets, let us restrict ourselves to two assets since this would be the smallest multivariate example. Indeed, let and denote the daily closing stock prices of Samsung Electronics (005930.KS) and LG-display (034220.KS), respectively, traded on the Korea Stock Exchange (KSC) for 2010, where the data can be easily accessed on public financial websites. We will assume as usual that follows a bi-variate normal distribution for . We transform the daily data to weekly data and compute the weekly covariance matrix for . In case a week has a holiday, we repeat the last previous observation. Under the usual assumptions this would constitute observations from a mixture model (4) with a standard Wishart distribution with four degrees of freedom.

Figure 3 plots the mixing density estimator corresponding to the two eigenvalues. One can see that there are two peaks, suggesting a possible bimodal stochastic volatility mixing density in the eigenvalues.

6 Proof of upper bound

The strategy here is, first, to decompose the integrated mean-squared error into its variance and bias components,

and, last, to estimate each component separately using estimates based on the Plancherel formula and the inversion formula for the Helgason–Fourier transform.

6.1 The integrated bias

Lemma 6.1

Suppose that and . Then

We have for

Applying the Plancherel formula, we obtain

Consequently,

where we use the fact that

Therefore

where the equality follows from the Plancherel formula. By assumption, , the latter integral is bounded above by , so we obtain

and the proof is complete.

6.2 The integrated variance

To obtain bounds for the integrated variance, several preliminary calculations are needed. In particular, we begin with the variance calculation of the empirical Helgason–Fourier transform, which has similarities to the usual empirical characteristic function.

Lemma 6.2

For and ,

By (16),

Observe also that

since . Applying this result to (6.2) and taking expectations, we obtain

where the last equality follows from the fact that are independent and identically distributed as , and because .

Following Terras Terras-II , pages 34 and 35, let

denote the positive Weyl chamber in . For , let and set

and define the normalizing constant by . Denote .

Lemma 6.3

As ,

By the Plancherel formula,

as .

Choose . Observe that

| (27) |

Since is a continuous function of on a compact set , is uniformly bounded on such on . Since is a density so that is also a density, we have

Hence, it follows from continuity and the compactness of

which has been used in the above calculation.

In addition, we use the fact that, as ,

a result which follows from Proposition 7.2 of Helgason he2 , page 450.

7 Proof of lower bound

We need to provide some detailed calculations, and the essence of the proof is contained for the case ; hence we will keep this assumption for the remainder of this paper. The generalization to may be obtained by using higher order hyperbolic spherical coordinates. In this section, we assume that is a -invariant function defined on .

7.1 Convolution and Helagson–Fourier transform in polar coordinate

For , let with , so that . Let

with for , and write

By a change of variables,

| (28) |

where

and

Denote . The next lemma is straightforward so we shall omit the proof.

Lemma 7.1

For , and , the matrix equation

has a solution and . Further, has minimum and maximum values and , respectively, and and can be defined uniquely.

In general, if both and are -invariant functions on , then is also -invariant and . Hence, is -invariant and due to -invariance of and . From this and Lemma 7.1, we can define

for , , . Denoting by the distribution function corresponding to the standard Wishart density with respect to the measure , we have that for ,

| (29) |

The Laplacian for -invariant functions in polar coordinate is given by , where

and the spherical function is given by

| (30) |

with , the Legendre function; see Terras Terras-II . It can be seen that

so that with .

7.2 -divergence

Choose as the perturbation function as in Fan fan . Then, one can construct satisfying the following conditions: {longlist}[(P5)]

is -invariant and separable with for .

for .

.

and , where and .

.

Let be a density on such that is sufficiently smooth and satisfies , , where is a normalizing constant. Define the function

where for .

For a function and , define

so that

Proposition 7.2

Suppose (P1)–(P5) hold. For a pair of densities

the -divergence between and satisfies

provided that .

The fact that is a lower bound follows from Proposition 7.2 whose proof follows from a sequence of lemmas below.

7.3 Perturbing function

Denote and for . Note that for .

Lemma 7.3

Suppose (P1) holds. Then .

By (32) and the change of variable , we obtain

The desired result follows from the Plancherel formula (13) and change of variable .

Lemma 7.4

Suppose (P1), (P2) and (P3) hold. Then there exists a positive constant such that .

Suppose . Observe that

and that for ,

Now, the Plancherel formula (13) and change of variable gives

A suitable choice of gives the desired result.

Lemma 7.5

Under (P1) and (P2), .

For ,

The desired result follows from the inequality , the Plancherel formula (13) and change of variable .

7.4 Tail behavior

Lemma 7.6

For and ,

Change of variable gives the desired result.

If has the distribution function , then has the distribution function with density . By (29) and a change of variables,

| (33) |

Lemma 7.7

We have is -invariant, and as and

Lemma 7.8

Define

Then, there exist and a constant such that when and ,

for all provided that and .

Denote

and for ,

Consider . Suppose . If and , then

Let and . Note that

Since then we have

and by Lemma 7.6 with , and

Hence, if , then as . Suppose . If and , then

Observe that

Since , then we have

and by Lemma 7.6, with , and ,

Hence, for ,

as .

Consider . Let and . Suppose . On , on . Note that If follows from these and Lemma 7.6 that

and if ,

7.5 Proof of Proposition 7.2

From (P5), one can choose sufficiently small such that is a density. By (28) and (33),

Let

and for ,

By (33), Lemmas 7.5, 7.7 and the Plancherel formula (13), we obtain

Lemma 7.1 and (P4) imply

| (34) |

Let . It follows from (34), Lemmas 7.7 and 7.8 that

Now letting and combining the above bounds, we obtain

Choosing , we have the desired result.

References

- (1) {barticle}[mr] \bauthor\bsnmAsai, \bfnmManabu\binitsM., \bauthor\bsnmMcAleer, \bfnmMichael\binitsM. and \bauthor\bsnmYu, \bfnmJun\binitsJ. (\byear2006). \btitleMultivariate stochastic volatility: A review. \bjournalEconometric Rev. \bvolume25 \bpages145–175. \biddoi=10.1080/07474930600713564, issn=0747-4938, mr=2256285 \bptokimsref \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmButucea, \bfnmC.\binitsC. and \bauthor\bsnmTsybakov, \bfnmA. B.\binitsA. B. (\byear2008). \btitleSharp optimality in density deconvolution with dominating bias, I, II. \bjournalTheory Probab. Appl. \bvolume52 \bpages24–39, 237–249. \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmChen, \bfnmJiahua\binitsJ. and \bauthor\bsnmTan, \bfnmXianming\binitsX. (\byear2009). \btitleInference for multivariate normal mixtures. \bjournalJ. Multivariate Anal. \bvolume100 \bpages1367–1383. \biddoi=10.1016/j.jmva.2008.12.005, issn=0047-259X, mr=2514135 \bptokimsref \endbibitem

- (4) {barticle}[mr] \bauthor\bsnmDiggle, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1993). \btitleA Fourier approach to nonparametric deconvolution of a density estimate. \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume55 \bpages523–531. \bidissn=0035-9246, mr=1224414 \bptokimsref \endbibitem

- (5) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear1991). \btitleOn the optimal rates of convergence for nonparametric deconvolution problems. \bjournalAnn. Statist. \bvolume19 \bpages1257–1272. \biddoi=10.1214/aos/1176348248, issn=0090-5364, mr=1126324 \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmGourieroux, \bfnmChristian\binitsC. and \bauthor\bsnmSufana, \bfnmRazvan\binitsR. (\byear2010). \btitleDerivative pricing with Wishart multivariate stochastic volatility. \bjournalJ. Bus. Econom. Statist. \bvolume28 \bpages438–451. \biddoi=10.1198/jbes.2009.08105, issn=0735-0015, mr=2723611 \bptokimsref \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmHaff, \bfnmL. R.\binitsL. R. (\byear1979). \btitleEstimation of the inverse covariance matrix: Random mixtures of the inverse Wishart matrix and the identity. \bjournalAnn. Statist. \bvolume7 \bpages1264–1276. \bidissn=0090-5364, mr=0550149 \bptokimsref \endbibitem

- (8) {barticle}[mr] \bauthor\bsnmHaff, \bfnmL. R.\binitsL. R. (\byear1980). \btitleEmpirical Bayes estimation of the multivariate normal covariance matrix. \bjournalAnn. Statist. \bvolume8 \bpages586–597. \bidissn=0090-5364, mr=0568722 \bptokimsref \endbibitem

- (9) {barticle}[mr] \bauthor\bsnmHaff, \bfnmL. R.\binitsL. R. (\byear1991). \btitleThe variational form of certain Bayes estimators. \bjournalAnn. Statist. \bvolume19 \bpages1163–1190. \biddoi=10.1214/aos/1176348244, issn=0090-5364, mr=1126320 \bptokimsref \endbibitem

- (10) {bbook}[mr] \bauthor\bsnmHelgason, \bfnmSigurdur\binitsS. (\byear1978). \btitleDifferential Geometry, Lie Groups, and Symmetric Spaces. \bseriesPure and Applied Mathematics \bvolume80. \bpublisherAcademic Press, \baddressNew York. \bidmr=0514561 \bptokimsref \endbibitem

- (11) {barticle}[mr] \bauthor\bsnmJohnstone, \bfnmIain M.\binitsI. M. (\byear2008). \btitleMultivariate analysis and Jacobi ensembles: Largest eigenvalue, Tracy–Widom limits and rates of convergence. \bjournalAnn. Statist. \bvolume36 \bpages2638–2716. \biddoi=10.1214/08-AOS605, issn=0090-5364, mr=2485010 \bptokimsref \endbibitem

- (12) {bmisc}[auto:STB—2011/12/28—12:52:23] \bauthor\bsnmKim, \bfnmK. R.\binitsK. R., \bauthor\bsnmKim, \bfnmP. T.\binitsP. T., \bauthor\bsnmKoo, \bfnmJ. Y.\binitsJ. Y., \bauthor\bsnmOh, \bfnmJ.\binitsJ. and \bauthor\bsnmZhu, \bfnmH.\binitsH. (\byear2011). \bhowpublishedAn analysis of diffusion tensor image data based on mixture of Wisharts. Preprint, Korea Univ. \bptokimsref \endbibitem

- (13) {bincollection}[auto:STB—2011/12/28—12:52:23] \bauthor\bsnmKim, \bfnmP. T.\binitsP. T. and \bauthor\bsnmRichards, \bfnmD. St. P.\binitsD. S. P. (\byear2010). \btitleDeconvolution density estimation on spaces of positive definite symmetric matrices. In \bbooktitleFestschrift for T. P. Hettmansperger (\beditorD. Hunter et al., eds.) \bpages147–168. \bpublisherWorld Scientific, \baddressSingapore. \bptokimsref \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmKoo, \bfnmJa-Yong\binitsJ.-Y. (\byear1993). \btitleOptimal rates of convergence for nonparametric statistical inverse problems. \bjournalAnn. Statist. \bvolume21 \bpages590–599. \biddoi=10.1214/aos/1176349138, issn=0090-5364, mr=1232506 \bptokimsref \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmLetac, \bfnmGérard\binitsG. and \bauthor\bsnmMassam, \bfnmHélène\binitsH. (\byear2007). \btitleWishart distributions for decomposable graphs. \bjournalAnn. Statist. \bvolume35 \bpages1278–1323. \biddoi=10.1214/009053606000001235, issn=0090-5364, mr=2341706 \bptokimsref \endbibitem

- (16) {bincollection}[mr] \bauthor\bsnmLin, \bfnmShang P.\binitsS. P. and \bauthor\bsnmPerlman, \bfnmMichael D.\binitsM. D. (\byear1985). \btitleA Monte Carlo comparison of four estimators of a covariance matrix. In \bbooktitleMultivariate Analysis VI (Pittsburgh, PA, 1983) (\beditorP. R. Krishnaiah, ed.) \bpages411–429. \bpublisherNorth-Holland, \baddressAmsterdam. \bidmr=0822310 \bptokimsref \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmLoh, \bfnmWei-Liem\binitsW.-L. (\byear1991). \btitleEstimating covariance matrices. \bjournalAnn. Statist. \bvolume19 \bpages283–296. \biddoi=10.1214/aos/1176347982, issn=0090-5364, mr=1091851 \bptokimsref \endbibitem

- (18) {barticle}[mr] \bauthor\bsnmMair, \bfnmBernard A.\binitsB. A. and \bauthor\bsnmRuymgaart, \bfnmFrits H.\binitsF. H. (\byear1996). \btitleStatistical inverse estimation in Hilbert scales. \bjournalSIAM J. Appl. Math. \bvolume56 \bpages1424–1444. \biddoi=10.1137/S0036139994264476, issn=0036-1399, mr=1409127 \bptokimsref \endbibitem

- (19) {bbook}[mr] \bauthor\bsnmMuirhead, \bfnmRobb J.\binitsR. J. (\byear1982). \btitleAspects of Multivariate Statistical Theory. \bpublisherWiley, \baddressNew York. \bidmr=0652932 \bptokimsref \endbibitem

- (20) {barticle}[mr] \bauthor\bsnmPensky, \bfnmMarianna\binitsM. (\byear1999). \btitleNonparametric empirical Bayes estimation of the matrix parameter of the Wishart distribution. \bjournalJ. Multivariate Anal. \bvolume69 \bpages242–260. \biddoi=10.1006/jmva.1998.1803, issn=0047-259X, mr=1703374 \bptnotecheck year\bptokimsref \endbibitem

- (21) {barticle}[mr] \bauthor\bsnmRichards, \bfnmDonald St. P.\binitsD. S. P. (\byear1985). \btitleApplications of invariant differential operators to multivariate distribution theory. \bjournalSIAM J. Appl. Math. \bvolume45 \bpages280–288. \biddoi=10.1137/0145015, issn=0036-1399, mr=0781108 \bptokimsref \endbibitem

- (22) {bmisc}[auto:STB—2011/12/28—12:52:23] \bauthor\bsnmStein, \bfnmC.\binitsC. (\byear1975). \bhowpublishedEstimation of a covariance matrix. Rietz lecture, 1975 Annual Meeting of the IMS, Atlanta, GA. \bptokimsref \endbibitem

- (23) {bmisc}[mr] \bauthor\bsnmSteĭn, \bfnmČ.\binitsČ. (\byear1977). \bhowpublishedLectures on the theory of estimation of many parameters. In Studies in the Statistical Theory of Estimation, Part I (I. A. Ibragimov and M. S. Nikulin, eds.). Zap. Naučn. Sem. Leningrad. Otdel. Mat. Inst. Steklov. (LOMI) 74 4–65, 146, 148 (in Russian). Steklov Mathematical Institute, Moscow. [English transl.: J. Soviet Math. 34 (1986) 1373–1403.] \bptokimsref \endbibitem

- (24) {barticle}[mr] \bauthor\bsnmTakemura, \bfnmAkimichi\binitsA. (\byear1984). \btitleAn orthogonally invariant minimax estimator of the covariance matrix of a multivariate normal population. \bjournalTsukuba J. Math. \bvolume8 \bpages367–376. \bidissn=0387-4982, mr=0767967 \bptokimsref \endbibitem

- (25) {bbook}[mr] \bauthor\bsnmTerras, \bfnmAudrey\binitsA. (\byear1988). \btitleHarmonic Analysis on Symmetric Spaces and Applications. II. \bpublisherSpringer, \baddressBerlin. \bidmr=0955271 \bptokimsref \endbibitem

- (26) {barticle}[mr] \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. (\byear1990). \btitleFourier methods for estimating mixing densities and distributions. \bjournalAnn. Statist. \bvolume18 \bpages806–831. \biddoi=10.1214/aos/1176347627, issn=0090-5364, mr=1056338 \bptokimsref \endbibitem