Counterparty Risk Valuation:

A Marked Branching Diffusion Approach

Abstract.

The purpose of this paper is to design an algorithm for the computation of the counterparty risk which is competitive in regards of a brute force “Monte-Carlo of Monte-Carlo” method (with nested simulations). This is achieved using marked branching diffusions describing a Galton-Watson random tree. Such an algorithm leads at the same time to a computation of the (bilateral) counterparty risk when we use the default-risky or counterparty-riskless option values as mark-to-market. Our method is illustrated by various numerical examples.

Key words and phrases:

Counterparty risk valuation, BSDE, branching diffusions, super-diffusions, semi-linear PDE, Galton-Watson tree1. Introduction

The recent financial crisis has highlighted the importance of credit valuation adjustment when pricing derivative contracts. Bilateral counterparty risk is the risk that the issuer of a derivative contract or the counterparty may default prior to the expiry and fail to make future payments. This market imperfection leads naturally for Markovian models to non-linear second-order parabolic partial differential equations (PDEs). More precisely, the non-linearity in the pricing equation affects none of the differential terms and depends on the positive part of the mark-to-market value of the derivative upon default. We have a so-called semi-linear PDE. The numerical solution of this equation is a formidable task that has attracted little attention from practitioners. For multi-asset portfolios, these PDEs which suffer from the curse of dimensionality cannot be solved with finite-difference schemes. We must rely on probabilistic methods. Up to now, it seems that a brute force intensive “Monte-Carlo of Monte-Carlo” method (with nested simulations) is the only tool available for this task.

In this paper, we rely on new advanced non-linear Monte-Carlo methods for solving these semi-linear PDEs. A first approach is to use the so-called first-order backward stochastic differential equations. Unfortunately, in practise this method requires the computation of conditional expectations using regressions. Finding good quality regressors is notably difficult, especially for multi-asset portfolios. This leads us to introduce a new method based on branching diffusions describing a marked Galton-Watson random tree. A similar algorithm can also be applied to obtain stochastic representations for solutions of a large class of semi-linear parabolic PDEs in which the non-linearity can be approximated by a polynomial function.

2. Credit Valuation Adjustment

2.1. Semi-linear PDEs

For completeness, we derive the PDE arising in counterparty risk valuation of a European derivative with a payoff at maturity . In short, depending on the (modeling) choice of the mark-to-market value of the derivative upon default, we will get two types of semi-linear PDEs that can be schematically written as

| (1) |

and

| (2) | |||||

is the Itô generator of a multi-dimensional diffusion process and are arbitrary functions of and .

2.2. PDE derivation

We assume the issuer is allowed to dynamically trade underlying assets . Additionally, in order to hedge his credit risk on the counterparty name, he can trade a default risky bond, denoted . Furthermore, the values of the underlyings are not altered by the counterparty default which is modeled by a Poisson jump process. For the sake of simplicity, we consider a constant intensity. This assumption can be easily relaxed, in particular the intensity can follow an Itô diffusion. For use below, expressions with a subscript denote counterparty quantities. We consider the case of a long position in a single derivative whose value we denote . In practice netting agreements apply to the global mark-to-market value of a pool of derivative positions - would then denote the aggregate value of these derivatives. The processes satisfy under the risk-neutral measure (we assume the market model is complete)

with a -dimensional Brownian motion, a jump Poisson process with intensity and the interest rate. The no-arbitrage condition and the completeness of the market give that is a -martingale, characterized by

where denotes the Itô generator of and the derivative value after the counterparty has defaulted. At the default event, is given by111.

with the mark-to-market value of the derivative to be used in the unwinding of the position upon default and the recovery rate. There is an ambiguity in the market about the convention for the mark-to-market value to be settled at default. There are two natural conventions (see [4] for discussions about the relevance of these conventions): The mark-to-market of the derivative is evaluated at the time of default with provision for counterparty risk or without.

. Provision for counterparty risk, :

| (3) |

In the particular case when the payoff is negative, the solution is given by .

. No provision for counterparty risk:

| (4) | |||

In the case of collateralized positions, counterparty risk applies to the variation of the mark-to-market value of the corresponding positions experienced over the time it takes to qualify a failure to pay margin as a default event - typically a few days. In the latter case, the non-linearity should be substituted with where is this delay. We will come back to this situation in the last section (see remark 5.1).

By proper discounting and replacing by for the sake of the presentation, these two PDEs can be cast into normal forms

| (5) | |||

| (6) |

with . It is interesting to note that a similar semi-linear PDE type (5) appears also in the pricing of American options.

2.3. American options

The replication price of an American option with exercise payoff satisfies a variational PDE:

This PDE can be converted into a semi-linear PDE (see [2] for details):

Stochastic representations of this equation lead to well-known early exercise premium formulas of American options. Our algorithm can also be applied to this non-linear PDE. It does not require regressions as in the well-known Longstaff-Schwartz method [10] or a “Monte-Carlo of Monte-Carlo method” as in Rogers’s dual algorithm [1, 14]. In the next section, we briefly list (non-linear) Monte-Carlo algorithms which can be used to solve PDEs (5)-(6) and highlight their weaknesses in the context of credit valuation adjustment.

3. Non-linear Monte-Carlo algorithms

3.1. A brute force algorithm

Using Feynman-Kac’s formula, the solution of PDE (5) can be represented stochastically as

| (7) |

with an Itô diffusion with generator and . By assuming that the intensity is small, we get the approximation (this is exact for PDE (6)222Precisely, we get . )

| (8) |

Then, at a next step, we discretise the Riemann integral

This last expression can be numerically tackled by using a brute force “Monte-Carlo of Monte-Carlo” method. The second MC is used to compute on each path generated by the first MC algorithm. Although straightforward, this method suffers from the curse of dimensionality and requires generating paths. Due to this complexity, the literature focuses on exposition of linear portfolios for which the second MC can be skipped by using closed-form formulas or low-dimensional parametric regressions (see for example [3] in which the authors consider the pricing of CMS spread option and CCDSs).

3.2. Backward stochastic differential equations

A first approach is to simulate a backward stochastic differential equation (in short BSDE):

| (9) | |||||

| (10) | |||||

| (11) |

where are required to be adapted processes and . BSDEs differ from (forward) SDEs in that we impose the terminal value (see Equation (11)). Under the condition , this BSDE admits a unique solution [13]. A straightforward application of Itô’s lemma gives that the solution of this BSDE is with the solution of PDE (5). This leads to a Monte-Carlo like numerical solution of (5) via an efficient discretization scheme for the above BSDE.

This BSDE can be discretized by an Euler-like scheme ( is forced to be -adapted, being the natural filtration generated by the Brownian motions):

with . This is equivalent to (we take )

This requires the computation of the conditional expectation (in practise by regression methods) which could be quite difficult and time-consuming, especially for multi-asset portfolios.

3.3. Gradient representation

A more powerful approach is synthesized by the following proposition which relies on Kunita’s stochastic flows of diffeomorphisms (see [16]). Let be the solution of the one-dimensional semi-linear PDE

| (12) |

with the terminal condition . By differentiating equation (12) with respect to (assuming smoothness of the coefficients) we get

| (13) |

with the terminal condition . The equation satisfied by the gradient is then interpreted as a (linear) Fokker-Planck PDE. We have the following representation [16]

where the Itô process is the solution to

is a standard Brownian. This representation leads to a particle algorithm [16]. Although appealing, this (forward) approach is only applicable in the one-dimension setup for which we can use a PDE solver. Can we design a similar forward algorithm applicable in higher dimensions? This leads us to branching diffusions.

3.4. Branching diffusions: an introduction

Branching diffusions have been first introduced by McKean [8] to give a probabilistic representation of the Kolmogorov-Petrovskii-Piskunov PDE and more generally of semi-linear PDEs of the type

| (14) | |||

with . Here the non-linearity is a power series in where the coefficients satisfy the restrictive condition:

| (15) |

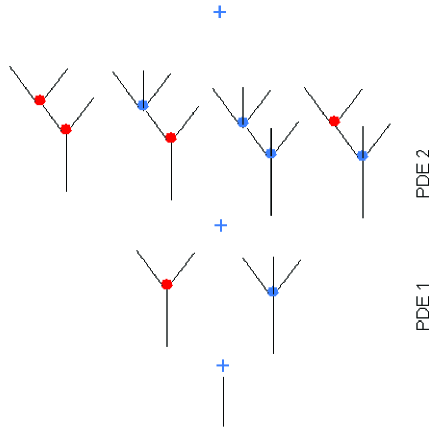

The probabilistic interpretation of such an equation goes as follows: Let a single particle start at the origin, perform an Itô diffusion on with generator , after a mean exponential time (independent of ) die and produce descendants with probability ( means that the particle dies without generating descendants). Then, the descendants perform independent Itô diffusions on (with same generator ) from their birth locations, die and produce descendants after a mean exponential times, etc. This process is called a -dimensional branching diffusion with a branching rate . can also depend spatially on or be itself stochastic (Cox process). We note the locations of the particles alive at time and the number of particles at (see Fig. 1 for examples with and descendants). We consider then the multiplicative functional defined by333 by convention.

| (16) |

where . Note that as can become infinite when (super-critical regime, see [12]), a sufficient condition on in order to have a well-behaved product is . Then solves the semi-linear PDE (14). This stochastic representation can be understood as follows: Mathematically, by conditioning on , the first-time to jump of a Poisson process with intensity , we get from (16)

where is the position of the -th particle at maturity produced by the -th particle generated at time . By using the independence and the strong Markov property, we obtain

Then, by assuming that , is uniformly bounded by in and we get from the Feynman-Kac formula that is a viscosity solution to PDE (14) (see Theorem 6.4 in [17]). By assuming that PDE (14) satisfies a comparison principle, we conclude that .

A first attempt in order to obtain a larger class of non-linearities than those defined by (15) is to consider an infinite collection of branching diffusions, the so-called super-diffusions. (15) is then extended to

| (17) |

where , and is a Radon measure on satisfying . The class of non-linearity as defined by (17) is more general than (15), in particular contains with arbitrary positive coefficients and . Unfortunately, this requires a large number of branching diffusions (as the default intensity diverges) and the non-linearity is still restrictive. This leads us to introduce a new class of branching diffusions that can be traced back to Le Jan-Sznitman [9] in the context of stochastic (Fourier) representations of solutions of the incompressible Navier-Stokes equation.

4. Marked branching diffusions

The PDE (14) should be compared with the semi-linear PDE (5) arising in the pricing of counterparty risk. It seems too restrictive and unreasonable to approximate the non-linearity by a polynomial of type (15) or even (17). A natural question is therefore to search if this construction can be generalized for an arbitrary polynomial for which the PDE is

| (18) |

with an -order polynomial in that we write for convenience . We will show below that this can be achieved by counting the branching of each monomial .

Assumption (Comp): In order to have uniqueness in the viscosity sense, we assume PDE (18) satisfies a comparison principle for sub- and super-solutions (see [7]).

For each Galton-Watson tree, we denote the number of branching of monomial type with . The descendants are drawn with an arbitrary distribution - for example we can take a uniform distribution (see an other choice in section 4.3). In Fig. 1, we have drawn the diagrams for the non-linearity up to two defaults. We then define the multiplicative functional:

Main formula:

| (19) |

We state our main result (the proof is reported in the appendix):

Theorem 4.1.

Let us assume that and (Comp) holds. The function is the unique viscosity solution of (18).

Diagrammar interpretation

From Feynman-Kac’s formula, we have

| (20) |

This integral equation can be recursively solved in terms of multiple exponential random times :

| (21) | |||||

Each term can be interpreted as a Feynman diagram (see Fig. 1) representing the trajectory of a branching diffusion with a weight depending on the branching of each monomial. For example in Fig. 1, the diagram with two red vertices corresponds to

By assuming that the series (21) is convergent, one can guess that the solution is given by our multiplicative functional (19).

In the next section, we focus on convergence issues and deduce a sufficient condition to ensure that if is bounded.

4.1. Convergence issues

The number of particles , produced by the branching , is

| (22) |

The probability of such a configuration satisfies the recurrence equation

| (23) | |||||

Indeed, if we have a tree with a branching at time , a particle among the particles must die and produce descendants (with probability ). The remaining particles must survive until maturity (with probability ).

We prove in the appendix that the Laplace transform of , , satisfies the equation

| (24) | |||

| (25) |

In the particular case of one branching type , we have

By assuming that , the expectation in (19) can then be bounded by

| (26) |

from which we deduce a sufficient condition for convergence:

Proposition 4.2.

Let us assume that . Set .

-

(1)

Case : We have (as defined by (19)) if there exists such that

In the particular case of one branching type , the sufficient condition for convergence reads as

-

(2)

Case : for all .

Note that our blow-up criteria does not depend on the probabilities as expected.

4.2. PDE (6)

We assume that the function can be well approximated by a polynomial (see section 5) and we consider the PDE

From Feynman-Kac’s formula, we have

with a Poisson default time with intensity . As compared to the previous section, we have the term instead of . This term can be computed using the previous algorithm by imposing that the particle can default only once. This corresponds to the first three diagrams in Fig. (1). As is valued in , our formula (19) is convergent here for all polynomial non-linearities.

4.3. Optimal probabilities

Is there a better choice than an uniform distribution for improving the convergence?

4.4. Numerical Experiments

Before applying our algorithm to the problem of credit valuation adjustment, we check it on polynomials which do not belong to the classes defined by (15) and (17).

4.4.1. Experiment 1

We have implemented our algorithm for the two PDE types

and

with . is the Itô generator of a geometric Brownian motion with a volatility and the Poisson intensity is . In financial terms, this corresponds to a CDS spread around basis points. The maturity is years. From (27), we note that our optimal probability distributions for PDE1 and PDE2 coincide with the uniform distribution. Moreover Proposition (4.2) gives that the solution does not blow up.

The numerical method has been checked against a one-dimensional PDE solver with a fully implicit scheme (see Table. 1) for which we find (PDE1) and (PDE2). Note that this algorithm converges as expected and the error is properly indicated by the Monte-Carlo standard deviation estimator (see column Stdev).

| N | Fair(PDE2) | Stdev(PDE2) | Fair(PDE1) | Stdev(PDE1) |

|---|---|---|---|---|

4.4.2. Experiment 2

Same test with (see Table. 2) and same comments as above.

| N | Fair(PDE2) | Stdev(PDE2) | Fair(PDE1) | Stdev(PDE1) |

|---|---|---|---|---|

4.4.3. Experiment 3: Blow-up explosion

It is well-known that the semi-linear PDE in

blows up in finite time if for any bounded positive payoff (see [15]). We deduce that the PDE with the non-linearity blows up in finite time () in one dimension. Using Proposition (4.2), our sufficient condition reads as

We have verified this explosion when the maturity is greater than year (in our case , ) using our algorithm (and a PDE solver as a benchmark). Note that for , the algorithm starts to blow up (see Stdev = ). A different stochastic representation can be obtained by setting . We get

and this can be interpreted as a binary tree with a weight . Our stochastic representation gives then

| (28) |

where is the time where the -th branching appears. This representation (28) appears in [11] and was used to reproduce Sugitani’s blow-up criteria [15].

| Maturity(Year) | BBM alg.(Stdev) | PDE |

|---|---|---|

5. Credit valuation adjustment algorithm

In the previous section, we have assumed that the payoff was bounded: . Then, the solution can then be written as where satisfies

| (29) |

Therefore, by re-scaling, we can consider that the payoff satisfies the condition . The condition can be easily relaxed as observed in ([6], see Remark 3.7). Let be a payoff with -exponential growth for some . We scale the solution by an arbitrary smooth positive function given by

If we write the linear operator as , then satisfies a PDE444 is written in . A similar expression can be obtained in a multi-dimensional setup. with the same non-linearity :

with .

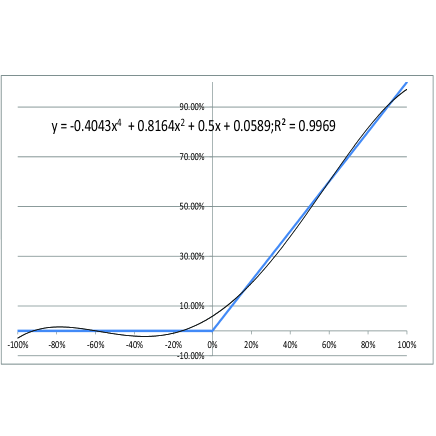

What remains to be done in order to use (19) is to approximate by a polynomial :

| (30) |

In our numerical experiments, we take (see Fig. 2)

| (31) |

Proposition 4.2 gives that the solution does not blow up if (Take with ). Moreover, as a numerical check of (26), we have computed using a PDE solver the solution of (30) with , , and years. The solution coincides with our upper bound in (26) and should satisfy

| (32) |

We found (PDE solver) and the reader can check that this value satisfies the above identity (32) as expected.

5.1. Algorithm: Final recipe

The algorithm for solving PDEs (5)-(6) can be described by the following steps:

-

(1)

Choose a polynomial approximation of on the domain .

-

(2)

Simulate the assets and the Poisson default time with intensity (resp. ) for PDE2 (resp. PDE1). Note that the intensity can be stochastic (Cox process), usually calibrated to default probabilities implied from CDS market quotes.

-

(3)

At each default time, produce descendants with probability (given by (27)). For PDE type , descendants, produced after the first default, become immortal.

-

(4)

Evaluate for each particle alive the payoff

where denotes the number of branching type . We should highlight that the algorithm for is always convergent for all whatever condition on the payoff as the multiplicative functional involves at most particles.

Remark 5.1.

In the case of collateralized positions, the non-linearity should be substituted with where is a delay. Using our polynomial approximation, we get . By expanding this function, we get monomials of the form . Our algorithm can then be easily extended to handle this case. At each default time , we produce descendants starting at and descendants starting at .

A natural question is to characterize the error of the algorithm as a function of the approximation error of by . Using the parabolicity of the semi-linear PDE, we can characterize the bias of our algorithm (the proof is reported in the appendix):

Proposition 5.2.

A similar result can be found for PDE (6). In the case of American options, our algorithm gives robust lower and upper bounds.

5.2. Complexity

By approximating with an infinite high-order polynomial - say - our algorithm converges towards the brute force “Monte-Carlo of Monte-Carlo” method with a complexity . By comparison, with our choice (31), the complexity is at most for PDE type (6). Moreover, this method allows to solve exactly PDE type (5), which can not be tackled without relying on an approximation within the “Monte-Carlo of Monte-Carlo” method.

5.3. Numerical examples

We have implemented our algorithm for the two PDE types

and

with Poisson intensities , and a recovery rate (see Tab. 4, 5, 6, 7). In financial term, this corresponds to CDS spreads around and basis points. The method has been checked using a PDE solver with the polynomial approximation (31) (see Column “PDE with poly.”). In order to justify the validity of (31), we have included the PDE price with the true non-linearity (see Column “PDE”). As it can be observed, prices, produced by our algorithm, converge to the PDE solver with the polynomial approximation and are close to the exact CVA values. We would like to highlight that replacing the Black-Scholes generator by a multi-dimensional operator can be easily handled in our framework by simulating the branching particles with a diffusion process associated to . This is out-of-reach with finite-difference scheme methods and not such an easy step for the BSDE approach.

| Maturity(Year) | PDE with poly. | BBM alg. | PDE |

|---|---|---|---|

| Maturity(Year) | PDE with poly. | BBM alg.(Stdev) | PDE |

|---|---|---|---|

| Maturity(Year) | PDE with poly. | BBM alg. | PDE |

|---|---|---|---|

| Maturity(Year) | PDE with poly. | BBM alg.(Stdev) | PDE |

|---|---|---|---|

6. Conclusion

Credit valuation adjustment is now an important quantitative issue which needs to receive special attention. The brute force “Monte-Carlo of Monte-Carlo” or the BSDE approach is not, as it looks like, a decent solution for multi-asset portfolios. We have shown the efficiency of our algorithm based on marked branching diffusions on various numerical examples. This method can also be used for semi-linear PDEs with polynomial non-linearities and extended to fully non-linear PDEs by including in the branching process Malliavin weights for derivatives. We left this investigation for future research.

Acknowledgements. The author wishes to thank the members of the Global Markets Quantitative Research Group at Société Générale for their comments. He is also grateful to Jean-François Delmas and Denis Talay for useful discussions.

Appendix

Proof of Theorem 4.1.

Proof of formula 24.

We set for convenience. We get the relation

which is equivalent to

The Laplace transform of , , satisfies the first-order PDE

The solution is given by

where the coefficients are solutions of the ODEs

The solution is given by with

This gives

where satisfies

Finally, we use that . ∎

Proof of Proposition 5.2.

The function satisfies the linear PDE

Note that the term is lower bounded. Feynman-Kac’s formula gives

from which we conclude the proof as by assumption. ∎

References

- [1] Andersen, L., Broadie, M. : A Primal-Dual Simulation Algorithm for Pricing Multi-Dimensional American Options, Management Science, 2004, Vol. 50, No. 9, pp. 1222-1234.

- [2] Benth, F.E., Karlsen, K.H., Reikvam, K. : A semilinear Black and Scholes partial differential equation for valuing American options, Finance and Stochastics, Vol. 7 (2003), issue 3.

- [3] Brigo, D. Pallavicini, A. : Counterparty risk and CCDSs under correlation, Risk magazine, Feb. (2008).

- [4] Brigo, D., Morini, M. : Close-out convention tensions, Risk magazine, Dec. (2011).

- [5] Dynkin, E.B. : Diffusions, superdiffusions and partial differential equations, American Mathematical Society (2002).

- [6] Fahim, A., Touzi, N., Warin, X. : A probabilistic numerical method for fully nonlinear parabolic PDEs, Ann. Appl. Probab. Volume 21, Number 4 (2011), 1322-1364.

- [7] Soner, H. M., Fleming, W. H. : Controlled Markov Processes and Viscosity Solutions, Springer-Verlag, 1993.

- [8] McKean, H. P. : Application of Brownian motion to the equation of Kolmogorov-Petrovskii-Piskunov, Communications on Pure and Applied Mathematics, Vol. 28, Issue 3, pp 323-331, May 1975.

- [9] Le Jan, Y., Sznitman, A-S : Stochastic cascades and 3-dimensional Navier Stokes equations, Prob. Theory Relat. Fields, 109, 343-366, (1997).

- [10] Longstall, F.A., Schwartz, E.S. : Valuing American options by simulation: a simple least-squares approach, Journal of derivatives 5, 25-44, 1997.

- [11] López-Mimbela, J.A., Wakolbinger, A. : Length of Galton-Watson trees and blow-up of semilinear systems, J. Appl. Probab. Volume 35, Number 4 (1998), 802-811.

- [12] Méléard, S. : Modèles aléatoires en Ecologie et Evolution, Lecture notes (in French), Ecole Polytechnique (2009).

- [13] Pardoux, E., Peng, S. : Adapted Solution of a Backward Stochastic Differential Equation, Systems Control Lett., 14, 55-61 (1990).

- [14] Rogers, L.C. : Monte-Carlo valuation of American options, Mathematical Finance 12, 2002, 271-286.

- [15] Sugitani, S. : On non-existence of global solutions for some nonlinear integral equations, Osaka J. Math., 12 (1975), 45-51.

- [16] Talay, D. : Probabilistic Numerical Methods for Partial Differential Equations: Elements of Analysis, In Graham, C. (ed.) et al., Probabilistic Models for Nonlinear Partial Differential Equations. Springer. Lect. Notes Math. 1627:148–196, 1996.

- [17] Touzi, N. : Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE, Lecture Notes, 2010.