In-network Sparsity-regularized Rank Minimization: Algorithms and Applications†

Abstract

Given a limited number of entries from the superposition of a low-rank matrix plus the product of a known fat compression matrix times a sparse matrix, recovery of the low-rank and sparse components is a fundamental task subsuming compressed sensing, matrix completion, and principal components pursuit. This paper develops algorithms for distributed sparsity-regularized rank minimization over networks, when the nuclear- and -norm are used as surrogates to the rank and nonzero entry counts of the sought matrices, respectively. While nuclear-norm minimization has well-documented merits when centralized processing is viable, non-separability of the singular-value sum challenges its distributed minimization. To overcome this limitation, an alternative characterization of the nuclear norm is adopted which leads to a separable, yet non-convex cost minimized via the alternating-direction method of multipliers. The novel distributed iterations entail reduced-complexity per-node tasks, and affordable message passing among single-hop neighbors. Interestingly, upon convergence the distributed (non-convex) estimator provably attains the global optimum of its centralized counterpart, regardless of initialization. Several application domains are outlined to highlight the generality and impact of the proposed framework. These include unveiling traffic anomalies in backbone networks, predicting networkwide path latencies, and mapping the RF ambiance using wireless cognitive radios. Simulations with synthetic and real network data corroborate the convergence of the novel distributed algorithm, and its centralized performance guarantees.

Index Terms:

Distributed optimization, sparsity, nuclear norm, low rank, networks, Lasso, matrix completion.Submitted:

EDICS Category: SEN-DIST, SPC-APPL, SEN-COLB.

I Introduction

Let be a low-rank matrix [], and be a sparse matrix with support size considerably smaller than . Consider also a matrix and a set of index pairs that define a sampling of the entries of . Given and a number of (possibly) noise corrupted measurements

| (1) |

the goal is to estimate low-rank and sparse , by denoising the observed entries and imputing the missing ones. Introducing the sampling operator which sets the entries of its matrix argument not in to zero and leaves the rest unchanged, the data model can be compactly written in matrix form as

| (2) |

A natural estimator accounting for the low rank of and the sparsity of will be sought to fit the data in the least-squares (LS) error sense, as well as minimize the rank of , and the number of nonzero entries of measured by its -(pseudo) norm; see e.g. [9], [21], [8], [12] for related problems subsumed by the one described here. Unfortunately, both rank and -norm minimization are in general NP-hard problems [24, 13]. Typically, the nuclear norm ( denotes the -th singular value of ) and the -norm are adopted as surrogates, since they are the closest convex approximants to and , respectively [25, 11, 32]. Accordingly, one solves

where are rank- and sparsity-controlling parameters. Being convex (P1) is appealing, and some of its special instances are known to attain good performance in theory and practice. For instance, when no data are missing (P1) can be used to unveil traffic anomalies in networks [21]. Results in [21] show that and can be exactly recovered in the absence of noise, even when is a fat (compression) operator. When equals the identity matrix, (P1) reduces to the so-termed robust principal component analysis (PCA), for which exact recovery results are available in [8] and [12]. Moreover, for the special case , (P1) offers a low-rank matrix completion alternative with well-documented merits; see e.g., [10] and [9]. Stable recovery results in the presence of noise are also available for matrix completion and robust PCA [9, 35]. Earlier efforts dealing with the recovery of sparse vectors in noise led to similar performance guarantees; see e.g., [6].

In all these works, the samples and matrix are assumed centrally available, so that they can be jointly processed to estimate and by e.g., solving (P1). Collecting all this information can be challenging though in various applications of interest, or may be even impossible in e.g., wireless sensor networks (WSNs) operating under stringent power budget constraints. In other cases such as the Internet or collaborative marketing studies, agents providing private data for e.g., fitting a low-rank preference model, may not be willing to share their training data but only the learning results. Performing the optimization in a centralized fashion raises robustness concerns as well, since the central processor represents an isolated point of failure. Scalability is yet another driving force motivating distributed solutions. Several customized iterative algorithms have been proposed to solve instances of (P1), and have been shown effective in tackling low- to medium-size problems; see e.g., [21], [10], [25]. However, most algorithms require computation of singular values per iteration and become prohibitively expensive when dealing with high-dimensional data [26]. All in all, the aforementioned reasons motivate the reduced-complexity distributed algorithm for nuclear and -norm minimization developed in this paper.

In a similar vein, stochastic gradient algorithms were recently developed for large-scale problems entailing regularization with the nuclear norm [26]. Even though iterations in [26] are highly paralellizable, they are not applicable to networks of arbitrary topology. There are also several studies on distributed estimation of sparse signals via -norm regularized regression; see e.g., [22, 17, 14]. Different from the treatment here, the data model of [22] is devoid of a low-rank component and all the observations are assumed available (but distributed across several interconnected agents). Formally, the model therein is a special case of (2) with , , and , in which case (P1) boils down to finding the least-absolute shrinkage and selection operator (Lasso) [31].

Building on the general model (2) and the centralized estimator (P1), this paper develops decentralized algorithms to estimate low-rank and sparse matrices, based on in-network processing of a small subset of noise-corrupted and spatially-distributed measurements (Section III). This is a challenging task however, since the non-separable nuclear-norm present in (P1) is not amenable to distributed minimization. To overcome this limitation, an alternative characterization of the nuclear norm is adopted in Section III-A, which leads to a separable yet non-convex cost that is minimized via the alternating-direction method of multipliers (AD-MoM) [5]. The novel distributed iterations entail reduced-complexity optimization subtasks per agent, and affordable message passing only between single-hop neighbors (Section III-C). Interestingly, the distributed (non-convex) estimator upon convergence provably attains the global optimum of its centralized counterpart (P1), regardless of initialization. To demonstrate the generality of the proposed estimator and its algorithmic framework, four networking-related application domains are outlined in Section IV, namely: i) unveiling traffic volume anomalies for large-scale networks [19, 21]; ii) robust PCA [12, 8]; iii) low-rank matrix completion for networkwide path latency prediction [20], and iv) spectrum sensing for cognitive radio (CR) networks [22, 4]. Numerical tests with synthetic and real network data drawn from these application domains corroborate the effectiveness and convergence of the novel distributed algorithms, as well as their centralized performance benchmarks (Section V).

Section VI concludes the paper, while several technical details are deferred to the Appendix.

Notation: Bold uppercase (lowercase) letters will denote matrices (column vectors), and calligraphic letters will be used for sets. Operators , , , and , will denote transposition, matrix trace, maximum singular value, Hadamard product, and Kronecker product, respectively; will be used for the cardinality of a set, and the magnitude of a scalar. The matrix vectorization operator stacks the columns of matrix on top of each other to return a supervector, and its inverse is . The diagonal matrix has the entries of on its diagonal, and the positive semidefinite matrix will be denoted by . The -norm of is for . For two matrices , denotes their trace inner product. The Frobenious norm of matrix is , is the spectral norm, is the -norm, is the -norm, and is the nuclear norm, where denotes the -th singular value of . The identity matrix will be represented by , while will stand for vector of all zeros, and . Similar notations will be adopted for vectors (matrices) of all ones.

II Preliminaries and Problem Statement

Consider networked agents capable of performing some local computations, as well as exchanging messages among directly connected neighbors. An agent should be understood as an abstract entity, e.g., a sensor in a WSN, a router monitoring Internet traffic; or a sensing CR from a next-generation communications technology. The network is modeled as an undirected graph , where the set of nodes corresponds to the network agents, and the edges (links) in represent pairs of agents that can communicate. Agent communicates with its single-hop neighboring peers in , and the size of the neighborhood will be henceforth denoted by . To ensure that the data from an arbitrary agent can eventually percolate through the entire network, it is assumed that:

- (a1)

-

Graph is connected; i.e., there exists a (possibly) multi-hop path connecting any two agents.

With reference to the low-rank and sparse matrix recovery problem outlined in Section I, in the network setting envisioned here each agent acquires a few incomplete and noise-corrupted rows of matrix . Specifically, the local data available to agent is matrix , where , , and . The index pairs in are those in for which the row index matches the rows of observed by agent . Additionally, suppose that agent has available the local matrix , containing a row subset of associated with the observed rows in , i.e, . Agents collaborate to form the wanted estimator (P1) in a distributed fashion, which can be equivalently rewritten as

The objective of this paper is to develop a distributed algorithm for sparsity-regularized rank minimization via (P1), based on in-network processing of the locally available data. The described setup naturally suggests three characteristics that the algorithm should exhibit: c1) agent should obtain an estimate of and , which coincides with the corresponding solution of the centralized estimator (P1) that uses the entire data ; c2) processing per agent should be kept as simple as possible; and c3) the overhead for inter-agent communications should be affordable and confined to single-hop neighborhoods.

III Distributed Algorithm for In-Network Operation

To facilitate reducing the computational complexity and memory storage requirements of the distributed algorithm sought, it is henceforth assumed that:

- (a2)

-

An upper bound on the rank of matrix obtained via (P1) is available.

As argued next, the smaller the value of , the more efficient the algorithm becomes. A small value of is well motivated in various applications. For example, the Internet traffic analysis of backbone networks in [19] demonstrates that origin-to-destination flows have a very low intrinsic dimensionality, which renders the traffic matrix low rank; see also Section IV-A. In addition, recall that is controlled by the choice of in (P1), and the rank of the solution can be made small enough, for sufficiently large . Because , (P1)’s search space is effectively reduced and one can factorize the decision variable as , where and are and matrices, respectively. Adopting this reparametrization of in (P1), one obtains the following equivalent optimization problem

which is non-convex due to the bilinear terms , and . The number of variables is reduced from in (P1), to in (P2). The savings can be significant when is in the order of a few dozens, and both and are large. The dominant -term in the variable count of (P3) is due to , which is sparse and can be efficiently handled even when both and are large. Problem (P3) is still not amenable to distributed implementation due to: (i) the non-separable nuclear norm present in the cost function; and (ii) the global variables and coupling the per-agent summands.

III-A A separable nuclear norm regularization

To address (i), consider the following neat characterization of the nuclear norm [25, 26]

| (3) |

For an arbitrary matrix with SVD , the minimum in (3) is attained for and . The optimization (3) is over all possible bilinear factorizations of , so that the number of columns of and is also a variable. Leveraging (3), the following reformulation of (P2) provides an important first step towards obtaining a distributed estimator:

As asserted in the following lemma, adopting the separable Frobenius-norm regularization in (P3) comes with no loss of optimality, provided the upper bound is chosen large enough.

Lemma 1: Under (a2), (P3) is equivalent to (P1).

Proof:

Let denote the minimizer of (P1). Clearly, , implies that (P2) is equivalent to (P1). From (3) one can also infer that for every feasible solution , the cost in (P3) is no smaller than that of (P2). The gap between the globally minimum costs of (P2) and (P3) vanishes at , , and , where . Therefore, the cost functions of (P1) and (P3) are identical at the minimum. ∎

Lemma III-A ensures that by finding the global minimum of (P3) [which could have significantly less variables than (P1)], one can recover the optimal solution of (P1). However, since (P3) is non-convex, it may have stationary points which need not be globally optimum. Interestingly, the next proposition shows that under relatively mild assumptions on and the noise variance, every stationary point of (P3) is globally optimum for (P1). For a proof, see Appendix A.

Proposition 1: Let be a stationary point of (P3). If (no subscript in signifies spectral norm), then is the globally optimal solution of (P1).

Condition captures tacitly the role of , the number of columns of and in the postulated model. In particular, for sufficiently small the residual becomes large and consequently the condition is violated (unless is large enough, in which case a sufficiently low-rank solution to (P1) is expected). This is manifested through the fact that the extra condition in Lemma III-A is no longer needed. In addition, note that the noise variance certainly affects the value of , and thus satisfaction of the said condition.

III-B Local variables and consensus constraints

To decompose the cost function in (P3), in which summands are coupled through the global variables and [cf. (ii) at the beginning of this section], introduce auxiliary variables representing local estimates of per agent . These local estimates are utilized to form the separable constrained minimization problem

| s. to | |||

For reasons that will become clear later on, additional variables were introduced to split the norm fitting-error part of the cost of (P4), from the norm regularization on the (cf. Remark 3). These extra variables are not needed if . The set of additional constraints ensures that, in this sense, nothing changes in going from (P3) to (P4). Most importantly, (P3) and (P4) are equivalent optimization problems under (a1). The equivalence should be understood in the sense that and likewise for , where and are the optimal solutions of (P4) and (P3), respectively. Of course, the corresponding estimates of will coincide as well. Even though consensus is a fortiori imposed within neighborhoods, it extends to the whole (connected) network and local estimates agree on the global solution of (P3). To arrive at the desired distributed algorithm, it is convenient to reparametrize the consensus constraints in (P4) as

| (4) | ||||

| (5) |

where are auxiliary optimization variables that will be eventually eliminated.

III-C The alternating-direction method of multipliers

To tackle the constrained minimization problem (P4), associate Lagrange multipliers with the splitting constraints , . Likewise, associate additional dual variables and ( and ) with the first pair of consensus constraints in (4) [respectively (5)]. Next introduce the quadratically augmented Lagrangian function

| (6) |

where is a positive penalty coefficient, and the primal variables are split into three groups , , and . For notational convenience, collect all multipliers in . Note that the remaining constraints in (4) and (5), namely , have not been dualized.

To minimize (P4) in a distributed fashion, a variation of the alternating-direction method of multipliers (AD-MoM) will be adopted here. The AD-MoM is an iterative augmented Lagrangian method especially well-suited for parallel processing [5], which has been proven successful to tackle the optimization tasks encountered e.g., with distributed estimation problems [28, 22]. The proposed solver entails an iterative procedure comprising four steps per iteration

- [S1]

-

Update dual variables:

(7) (8) (9) (10) (11) - [S2]

-

Update first group of primal variables:

(12) - [S3]

-

Update second group of primal variables:

(13) - [S4]

-

Update auxiliary primal variables:

(14)

This four-step procedure implements a block-coordinate descent method with dual variable updates. At each step while minimizing the augmented Lagrangian, the variables not being updated are treated as fixed and are substituted with their most up to date values. Different from AD-MoM, the alternating-minimization step here generally cycles over three groups of primal variables - (cf. two groups in AD-MoM [5]). In some special instances detailed in Sections IV-C and IV-D, cycling over two groups of variables only is sufficient. In [S1], is the step size of the subgradient ascent iterations (7)-(11). While it is common in AD-MoM implementations to select , a distinction between the step size and the penalty parameter is made explicit here in the interest of generality.

Reformulating the estimator (P1) to its equivalent form (P4) renders the augmented Lagrangian in (III-C) highly decomposable. The separability comes in two flavors, both with respect to the variable groups , , and , as well as across the network agents . This in turn leads to highly parallelized, simplified recursions corresponding to the aforementioned four steps. Specifically, it is shown in Appendix B that if the multipliers are initialized to zero, [S1]-[S4] constitute the distributed algorithm tabulated under Algorithm 1. For conciseness in presenting the algorithm, define the local residuals . In addition, define the soft-thresholding matrix with -th entry given by , where denotes the -th entry of .

Remark 1 (Simplification of redundant variables)

Careful inspection of Algorithm 1 reveals that the inherently redundant auxiliary variables and multipliers have been eliminated. Agent does not need to separately keep track of all its non-redundant multipliers , but only to update their respective (scaled) sums and .

Remark 2 (Computational and communication cost)

The main computational burden of the algorithm stems from solving unconstrained quadratic programs locally to update , and to carry out simple soft-thresholding operations to update . On a per iteration basis, network agents communicate their updated local estimates with their neighbors, to carry out the updates of the primal and dual variables during the next iteration. Regarding communication cost, is a matrix and its transmission does not incur significant overhead when is small. In addition, the matrix is sparse, and can be communicated efficiently. Observe that the dual variables need not be exchanged.

Remark 3 (General sparsity-promoting regularization)

Even though was adopted in (P1) to encourage sparsity in the entries of , the algorithmic framework here can accommodate more general structured sparsity-promoting penalties . To maintain the per-agent computational complexity at affordable levels, the minimum requirement on the admissible penalties is that the proximal operator

| (15) |

is given in terms of vector or (and) scalar soft-thresholding operators. In addition to the -norm (Lasso penalty), this holds for the sum of row-wise -norms (group Lasso penalty [33]), or, a linear combination of the aforementioned two – the so-termed hierarchical Lasso penalty that encourages sparsity across and within the rows of [29]. All this is possible since by introducing the cost-splitting variables , the local sparse matrix updates are for suitable (see Appendix B).

When employed to solve non-convex problems such as (P4), AD-MoM (or its variant used here) offers no convergence guarantees. However, there is ample experimental evidence in the literature which supports convergence of AD-MoM, especially when the non-convex problem at hand exhibits “favorable” structure. For instance, (P4) is bi-convex and gives rise to the strictly convex optimization subproblems (12)-(14), which admit unique closed-form solutions per iteration. This observation and the linearity of the constraints endow Algorithm 1 with good convergence properties – extensive numerical tests including those presented in Section V demonstrate that this is indeed the case. While a formal convergence proof goes beyond the scope of this paper, the following proposition proved in Appendix C asserts that upon convergence, Algorithm 1 attains consensus and global optimality.

Proposition 2: If the sequence of iterates generated by Algorithm 1 converge to , and (a1) holds, then: i) ; and ii) if , then and , where is the global optimum of (P1).

IV Applications

This section outlines a few applications that could benefit from the distributed sparsity-regularized rank minimization framework described so far. In each case, the problem statement calls for estimating low-rank and (or) sparse , given distributed data adhering to an application-dependent model subsumed by (2). Customized algorithms are thus obtained as special cases of the general iterations in Algorithm 1.

IV-A Unveiling traffic anomalies in backbone networks

In the backbone of large-scale networks, origin-to-destination (OD) traffic flows experience abrupt changes which can result in congestion, and limit the quality of service provisioning of the end users. These so-termed traffic volume anomalies could be due to external sources such as network failures, denial of service attacks, or, intruders which hijack the network services [30] [19]. Unveiling such anomalies is a crucial task towards engineering network traffic. This is a challenging task however, since the available data are usually high-dimensional noisy link-load measurements, which comprise the superposition of unobservable OD flows as explained next.

The network is modeled as in Section II, and transports a set of end-to-end flows (with ) associated with specific source-destinations pairs. For backbone networks, the number of network layer flows is typically much larger than the number of physical links . Single-path routing is considered here to send the traffic flow from a source to its intended destination. Accordingly, for a particular flow multiple links connecting the corresponding source-destination pair are chosen to carry the traffic. Sparing details that can be found in [21], the traffic carried over links and measured at time instants can be compactly expressed as

| (16) |

where the fat routing matrix is fixed and given, denotes the unknown “clean” traffic flows over the time horizon of interest, and collects the traffic volume anomalies. These data are distributed. Agent acquires a few rows of corresponding to the link-load traffic measurements from its outgoing links, and has available its local routing table which indicates the OD flows routed through . Assuming a suitable ordering of links, the per agent quantities relate to their global counterparts in (16) through and .

Common temporal patterns among the traffic flows in addition to their periodic behavior, render most rows (respectively columns) of linearly dependent, and thus typically has low rank [19]. Anomalies are expected to occur sporadically over time, and only last for short periods relative to the (possibly long) measurement interval . In addition, only a small fraction of the flows are supposed to be anomalous at any given time instant. This renders the anomaly matrix sparse across rows and columns. Given local measurements and the routing tables , the goal is to estimate in a distributed fashion, by capitalizing on the sparsity of and the low-rank property of . Since the primary goal is to recover , define which inherits the low-rank property from , and consider [cf. (16)]

| (17) |

Model (17) is a special case of (2), when all the entries of are observed, i.e., . Note that is not sparse even though is itself sparse, hence principal components pursuit is not applicable here [35]. Instead, the following estimator is adopted to unveil network anomalies [21]

which is subsumed by (P1). Accordingly, a distributed algorithm can be readily obtained by simplifying the general iterations under Algorithm 1, the subject dealt with next.

Distributed Algorithm for Unveiling Network Anomalies (DUNA). For the specific case here in which , the residuals in Algorithm 1 reduce to . Accordingly, to update the primal variables , and as per Algorithm 1, one needs to solve respective unconstrained strictly convex quadratic optimization problems. These admit closed-form solutions detailed under Algorithm 2. The DUNA updates of the local anomaly matrices are given in terms of soft-thresholding operations, exactly as in Algorithm 1.

Conceivably, the number of flows can be quite large, thus inverting the matrix to update could be complex computationally. Fortunately, the inversion needs to be carried out once, and can be performed and cached off-line. In addition, to reduce the inversion cost, the SVD of the local routing matrices can be obtained first, and the matrix inversion lemma can be subsequently employed to obtain , where and . This computational shortcut is commonly adopted in statistical learning algorithms when ridge regression estimates are sought, and the number of variables is much larger than the number of elements in the training set [15, Ch. 18]. During the operational phase of the algorithm, the main computational burden of DUNA comes from repeated inversions of (small) matrices, and parallel soft-thresholding operations. The communication overhead is identical to the one incurred by Algorithm 1 (cf. Remark 2).

Remark 4 (Incomplete link traffic measurements)

In general, one can allow for missing traffic data and the DUNA updates are still expressible in closed form.

IV-B In-network robust principal component analysis

Principal component analysis (PCA) is the workhorse of high-dimensional data analysis and dimensionality reduction, with numerous applications in statistics, networking, engineering, and the biobehavioral sciences; see, e.g., [18]. Nowadays ubiquitous e-commerce sites, complex networks such as the Web, and urban traffic surveillance systems generate massive volumes of data. As a result, extracting the most informative, yet low-dimensional structure from high-dimensional datasets is of paramount importance [15].

Data obeying postulated low-rank models include also outliers, which are samples not adhering to those nominal models. Unfortunately, similar to LS estimates PCA is very sensitive to the outliers [18]. While robust approaches to PCA are available, recently polynomial-time algorithms with remarkable performance guarantees have emerged for low-rank matrix recovery in the presence of sparse – but otherwise arbitrarily large – errors [35, 8, 12]. Robust PCA is of great interest in networking-related applications. One can think of distributed estimation using reduced-dimensionality sensor observations [27], and unveiling anomalous flows in backbone networks from Netflow data [2]; see also Section V-B.

In the network setting of Section II, each agent acquires outlier-plus-noise corrupted rows of matrix , where . Local data can thus be modeled as , where has low rank. Agents want to estimate (and the outliers ) in a distributed fashion by forming the global estimator [35]

| (18) |

which is once more a special case of (P1) when .

Distributed Robust Principal Component Analysis (DRPCA) Algorithm. Regarding the general distributed formulation in (P4), the first constraint is no longer needed since [cf. the discussion after (P4)]. As agent is interested in estimating and is separable over the rows of , the only required constraints are . These are associated with the dual variables per agent, and are updated according to Algorithm 3. All in all, each agent stores and recursively updates the primal variables , along with the matrix .

Mimicking the procedure that led to Algorithm 1, one finds that primal variable updates in DRPCA are expressible in closed form. In particular, the local outlier matrix minimizes the Lasso cost

and is given in terms of soft-thresholding operations as seen in Algorithm 3 [observe that , where is defined in (15)].

DRPCA iterations are simple with small matrices inverted per iteration to update and (see Algorithm 3). Regarding communication cost, each agent only broadcasts a matrix to its neighbors.

IV-C Distributed low-rank matrix completion

The ability to recover a low-rank matrix from a subset of its entries is the leitmotif of recent advances for localization of wireless sensors [23], Internet traffic analysis [20], [34], and preference modeling for recommender systems [3]. In the low-rank matrix completion problem, given a limited number of (possibly) noise corrupted entries of a low-rank matrix , the goal is to recover the entire matrix while denoising the observed entries, and accurately imputing the missing ones.

In the network setting envisioned here, agent has available incomplete and noise-corrupted rows of . Local data can thus be modeled as . Relying on in-network processing, agents aim at completing their own rows by forming the global estimator

| (19) |

which exploits the low-rank property of through nuclear-norm regularization. Estimator (19) was proposed in [9], and solved centrally whereby all data is available to feed an e.g., off-the-shelf semidefinite programming (SDP) solver. The general estimator in (P1) reduces to (19) upon setting and . Hence, it is possible to derive a distributed algorithm for low-rank matrix completion by specializing Algorithm 1 to the setting here.

Before dwelling into the algorithmic details, a brief parenthesis is in order to touch upon properties of local sampling operators. Operator is a linear orthogonal projector, since it projects its matrix argument onto the subspace of matrices with support contained in . Linearity of implies that , where is a symmetric and idempotent projection matrix that will prove handy later on. To characterize , introduce an masking matrix whose -th entry equals one when , and zero otherwise. Since , from standard properties of the operator it follows that .

Distributed Matrix Completion (DMC) Algorithm. Going back to the general distributed formulation in (P4), since there is no sparse component in the matrix completion problem (19), the only constraints that remain are , , . These correspond to the dual variables per agent, and are updated as shown in Algorithm 4.

In the absence of and the auxiliary variables , it suffices to cycle over two groups of primal variables to arrive at the DMC iterations. The primal variable updates can be readily obtained by capitalizing on the properties of the operator. In particular, Algorithm 1 indicates that the recursions for are given by [let ]

| (20) |

Likewise, is updated by solving the following subproblem per iteration (let )

| (21) |

Both (IV-C) and (IV-C) are unconstrained convex quadratic problems, which admit the closed-form solutions tabulated under Algorithm 4.

The per-agent computational complexity of the DMC algorithm is dominated by repeated inversions of and matrices to obtain and , respectively (see Algorithm 4). Notice that has block-diagonal structure with blocks of size . Inversion of matrices is affordable in practice since is typically small for a number of applications of interest (cf. the low-rank assumption). In addition, is the number of row vectors acquired per agent which can be controlled by the designer to accommodate a prescribed maximum computational complexity. On a per iteration basis, network agents communicate their updated local estimates only with their neighbors, in order to carry out the updates of primal and dual variables during the next iteration. In terms of communication cost, is a matrix and its transmission does not incur significant overhead for small values of . Observe that the dual variables need not be exchanged, and the overall communication cost does not depend on the network size .

IV-D Distributed sparse linear regression for spectrum cartography

In a classical linear regression setting, training data related through are given and the goal is to estimate the regression coefficient matrix based on the LS criterion111Even though vector responses and model parameters are typically considered, i.e., , the matrix notation is retained here for consistency.. However, LS often yields unsatisfactory prediction accuracy and fails to provide parsimonious estimates; see e.g., [15]. To deal with such limitations, one can adopt a regularization technique known as Lasso [31].

The general framework in this paper can accommodate distributed estimators of the regression coefficients via Lasso, when the training data are scattered across different agents, and their communication to a central processing unit is prohibited for e.g., communication cost or privacy reasons. With reference to the setup described in Section II, each agent has available the training data and wishes to find

| (22) |

in a distributed fashion. The Lasso estimator (22) is a special case of (P1) in the absence of a low-rank component; that is when , and .

An application domain where this problem arises is spectrum sensing in cognitive radio (CR) networks whereby sensing CRs collaborate to estimate the radio-frequency power spectrum density maps across space and frequency ; see [4, 22]. These maps enable identification of opportunistically available spectrum bands for re-use and handoff operation; as well as localization, transmit-power estimation, and tracking of primary user activities.

A cooperative approach to spectrum cartography is introduced in [4], based on a basis expansion model of . Spatially-distributed CRs collect smoothed periodogram samples of the received signal at given sampling frequencies, based on which they want to determine the unknown expansion coefficients in . The sensing scheme capitalizes on two forms of sparsity: the first one introduced by the narrow-band nature of transmit-PSDs relative to the broad swaths of usable spectrum; and the second one emerging from sparsely located active radios in the operational space. All in all, locating the active transmitters boils down to a variable selection problem, which motivates well employment of the Lasso in (22). Since data are collected by cooperating CRs at different locations, estimation of amounts to solving a distributed parameter estimation problem which demands taking into account the network topology, and devising a protocol to share the data. All these are accomplished by the algorithm outlined next.

Distributed Lasso (DLasso) Algorithm [22]. In the Lasso setting here, (P4) reduces to

| s. to | |||

which is a convex optimization problem equivalent to (22). Accordingly, the DLasso algorithm (tabulated under Algorithm 5) is readily obtained from Algorithm 1, after retaining only the update recursions for and the multipliers . A distributed protocol to select via -fold cross validation [15, Ch. 7] is also available in [22], along with numerical tests to assess its performance.

Since Lasso in (22) and its separable constrained reformulation are convex optimization problems, the general convergence results for AD-MoM iterations can be invoked to establish convergence of DLasso as well. A detailed proof of the following proposition can be found in [22, App. E].

Proposition 3: Under (a1) and for any value of the penalty coefficient , the iterates converge to the Lasso solution [cf. (22)] as , i.e.,

V Numerical Tests

This section corroborates convergence and gauges performance of the proposed algorithms, when tested on the applications of Section IV using synthetic and real network data.

Synthetic network data. A network of agents is considered as a realization of the random geometric graph model, that is, agents are randomly placed on the unit square and two agents communicate with each other if their Euclidean distance is less than a prescribed communication range of ; see Fig. 1. The network graph is bidirectional and comprises links, and OD flows. The entries of are independent and identically distributed (i.i.d.), zero-mean, Gaussian with variance ; i.e., . Low-rank matrices with rank are generated from the bilinear factorization model , where and are and matrices with i.i.d. entries drawn from Gaussian distributions and , respectively. Every entry of is randomly drawn from the set with . Unless otherwise stated, , and are used throughout. Different values of , and are examined.

Internet2 network data. Real data including OD flow traffic levels and end-to-end latencies are collected from the operation of the Internet2 network (Internet backbone network across USA) [1]. Both versions of the Internet2 network, referred as v1 and v2, are considered. OD flow traffic levels are recorded for a three-week operation of Internet2-v1 during Dec. 8–28, 2008 [19], and are used to assess performance of DUNA and DRPCA (see Sections V-A and V-B next). Internet2-v1 contains agents, links, and flows. To test the DMC algorithm, end-to-end flow latencies are collected from the operation of Internet2-v2 during Aug. 18–22, 2011 [1]. The Internet2-v2 network comprises agents, links, and flows.

Selection of tuning parameters. The sparsity- and rank-controlling parameters and are tuned to optimize performance. The optimality conditions for (P1) indicate that for and , is the unique optimal solution. This in turn confines the search space for and to the intervals and , respectively. In addition, for the case of matrix completion and robust PCA one can use the heuristic rules proposed in e.g., [9] and [8].

V-A Unveiling network anomalies

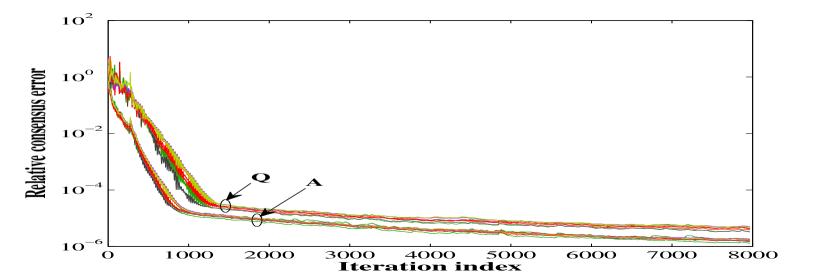

Data is generated from , where the routing matrix is obtained after determining shortest-path routes of the OD flows. For , DUNA is run until convergence is attained. These values were experimentally chosen to obtain the fastest convergence rate. The time evolution of consensus among agents is depicted in Fig. 2 (left), for representative agents in the network. The metric of interest here is the relative error per agent , which compares the corresponding local estimate with the network-wide average ; and likewise for the . Fig. 2 (left) shows that DUNA converges and agents consent on the global matrices as .

To corroborate that DUNA attains the centralized performance, the accelerated proximal gradient algorithm of [21] is employed to solve (P1) after collecting all the per-agent data in a central processing unit. For both the distributed and centralized schemes, Fig. 2 (right) depicts the evolution of the relative error for various sparsity levels, where for DUNA. It is apparent that the distributed estimator approaches the performance of its centralized counterpart, thus corroborating convergence and global optimality as per Proposition 3.

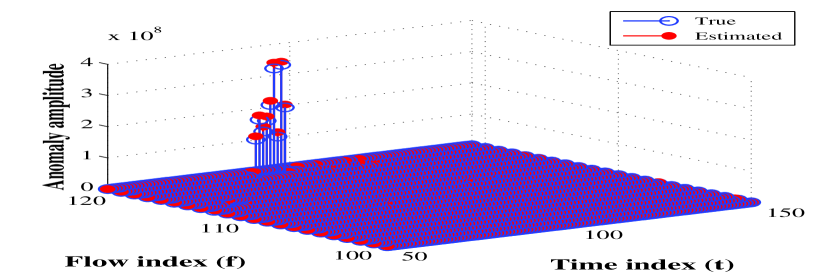

Unveiling Internet2-v1 network anomalies from SNMP measurements. Given the OD flow traffic measurements discussed at the beginning of Section V, the link loads in are obtained through multiplication with the Internet2-v1 routing matrix [1]. Even though is “constructed” here from flow measurements, link loads can be typically acquired from simple network management protocol (SNMP) traces [30]. The available OD flows are a superposition of “clean” and anomalous traffic, i.e., the sum of unknown “ground-truth” low-rank and a sparse matrices adhering to (16) when . Therefore, the proposed algorithms are applied first to obtain a reasonably precise estimate of the “ground-truth” . The estimated exhibits three dominant singular values, confirming the low-rank property of .

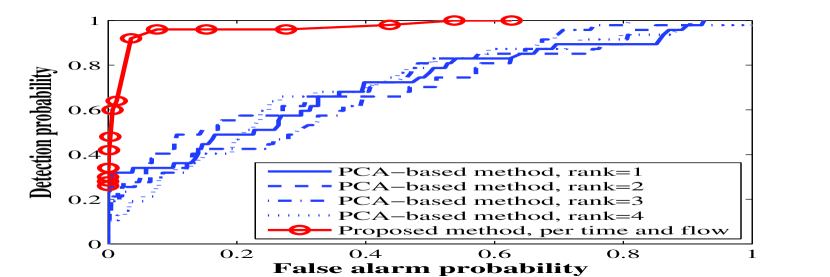

The receiver operation characteristic (ROC) curves in Fig. 3 (left) highlight the merits of DUNA when used to identify Internet2-v1 network anomalies. Even at low false alarm rates of e.g., , the anomalies are accurately detected (). In addition, DUNA consistently outperforms the landmark PCA-based method of [19], and can identify anomalous flows. Fig. 3 (right) illustrates the magnitude of the true and estimated anomalies across flows and time.

V-B Robust PCA

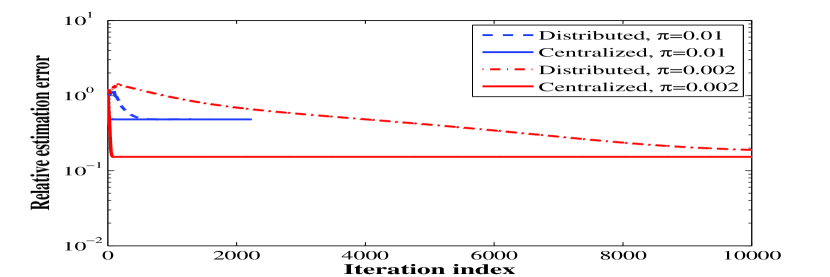

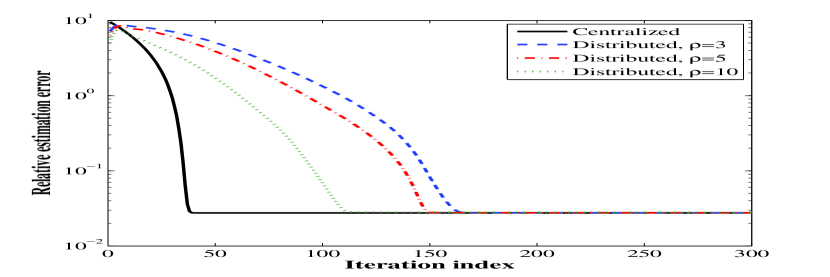

Next, the convergence and effectiveness of the proposed DRPCA algorithm is corroborated with the aid of computer simulations. An data matrix is generated as , and the centralized estimator (18) is obtained using the AD-MoM method proposed in [8]. In the network setting, each agent has available rows of . Fig. 2 (right) is replicated as Fig. 4 (left) for the robust PCA problem dealt with here, and for different values of [the assumed upper bound on rank]. It is again apparent that DRPCA converges and approaches the performance of (18) as .

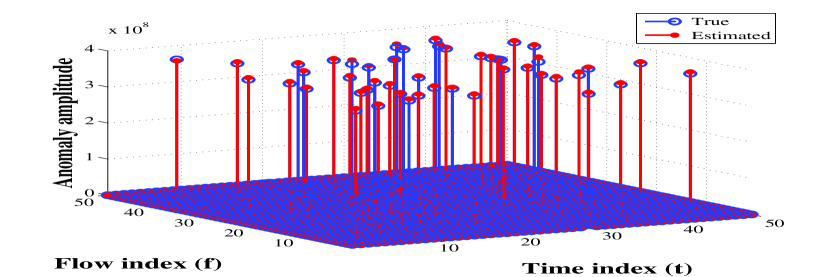

Unveiling Internet2-v1 network anomalies from Netflow measurements. Suppose a router monitors the traffic volume of OD flows to unveil anomalies using e.g., the Netflow protocol [30, 2]. Collect the time-series of all OD flows as the rows of the matrix , where and account for anomalies and noise, respectively. As elaborated in Section IV-A, the common temporal patterns across flows renders the traffic matrix low-rank. Owing to the difficulties of measuring the large number of OD flows, in practice only a few entries of are typically available [30], or, link traffic measurements are utilized as in Section V-A (recall that ). In this example, because the Internet2-v1 network data comprises only flows, it is assumed that .

To better assess performance, large spikes are injected into randomly selected entries of the ground truth-traffic matrix estimated in Section V-A. The DRPCA algorithm is run on this Internet2-v1 Netflow data to identify the anomalies. The results are depicted in Fig. 4 (right). DRPCA accurately identifies the anomalies, achieving when .

V-C Low-rank matrix completion

In addition to the synthetic data specifications outlined at the beginning of this section, the sampling set is picked uniformly at random, where each entry of the matrix is a Bernoulli random variable taking the value one with probability . Data for the matrix completion problem is thus generated as , where is an matrix with . The data available to agent is , which corresponds to a row subset of .

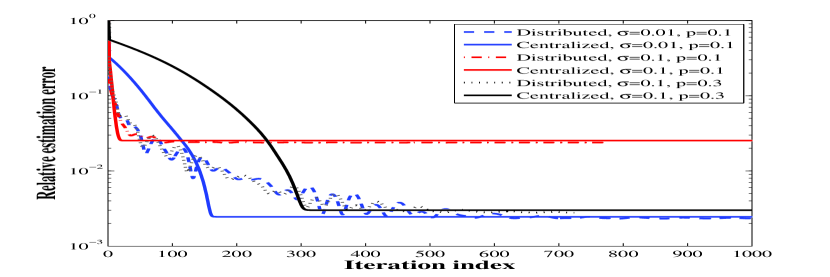

As with the previous test cases, it is shown first that the DMC algorithm converges to the (centralized) solution of (19). To this end, the centralized singular value thresholding algorithm is used to solve (19) [10], when all data is available for processing. For both the distributed and centralized schemes, Fig. 5 (left) depicts the evolution of the relative error for different values of (noise strength), and percentage of missing entries (controlled by ). Regardless of the values of and , the error trends clearly show the convergent behavior of the DMC algorithm and corroborate Proposition 3. Interestingly, for small noise levels where the estimation error approaches zero, the distributed estimator recovers almost exactly.

Internet2-v2 network latency prediction. End-to-end network latency information is critical towards enforcing quality-of-service constraints in many Internet applications. However, probing all pairwise delays becomes infeasible in large-scale networks. If one collects the end-to-end latencies of source-sink pairs in a delay matrix , strong dependencies among path delays render low-rank [20]. This is mainly because the paths with nearby end nodes often overlap and share common bottleneck links. This property of along with the distributed-processing requirements of large-scale networks, motivates well the adoption of the DMC algorithm for networkwide path latency prediction. Given the -th row of is partially available to agent , the goal is to impute the missing delays through agent collaboration.

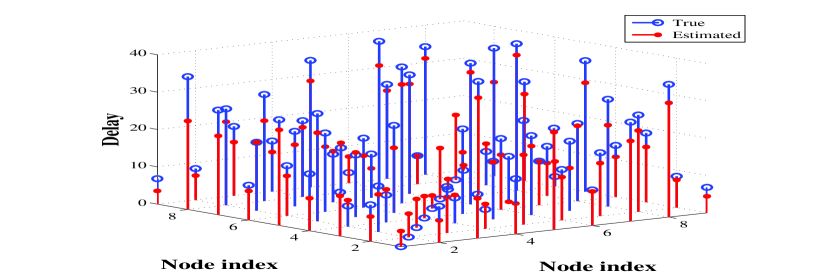

The DMC algorithm is tested here using the real path latency data collected from the operation of Internet2-v2. Spectral analysis of reveals that the first four singular values are markedly dominant, demonstrating that is low rank. A fraction of the entries in are purposely dropped to yield an incomplete delay matrix . After running the DMC algorithm till convergence, the true and predicted latencies are depicted in Fig. 5 (right) (for missing data). The relative prediction error is around .

VI Concluding Summary

A framework for distributed sparsity-regularized rank minimization is developed in this paper, that is suitable for (un)supervised inference tasks in networks. Fundamental problems such as in-network compressed sensing, matrix completion, and principal components pursuit are all captured under the same umbrella. The novel distributed algorithms can be utilized to unveil traffic volume anomalies from SNMP and Netflow traces, to predict networkwide path latencies in large-scale IP networks, and to map-out the RF ambiance using periodogram samples collected by spatially-distributed cognitive radios.

A. Proof of Proposition III-A. Recall the cost function of (P3) defined as

| (23) |

The stationary points of (P3) are obtained by setting to zero the (sub)gradients, and solving [7]

| (24) | |||

| (25) | |||

| (26) |

Clearly, every stationary point satisfies and . Using the aforementioned identities, the optimality conditions (24)-(26) can be rewritten as

| (27) | |||

| (28) |

Consider now the following convex optimization problem

| s. to | (31) |

which is equivalent to (P1). The equivalence can be readily inferred by minimizing (P5) with respect to first, and taking advantage of the following alternative characterization of the nuclear norm (see e.g., [25])

| (34) |

In what follows, the optimality conditions for the conic program (P5) are explored. To this end, the Lagrangian is first formed as

where denotes the dual variables associated with the conic constraint (31). For notational convenience, partition in four blocks , , , and , in accordance with the block structure of in (31), where and are and matrices. The optimal solution to (P5) must: (i) null the (sub)gradients

| (35) | |||

| (36) | |||

| (37) | |||

| (38) |

and satisfy (ii) the complementary slackness condition ; (iii) primal feasibility ; and (iv) dual feasibility .

Recall the stationary point of (P3), and introduce candidate primal variables , and ; and the dual variables , , , and . Then, (i) holds since after plugging the candidate primal and dual variables in (35)-(38), the subgradients vanish. Moreover, (ii) holds since

where the last two equalities follow from (28). Condition (iii) is also met since

| (45) |

To satisfy (iv), based on a Schur complement argument [16] it suffices to enforce .

B. Derivation of Algorithm 1. It is shown here that [S1]-[S4] in Section III-C give rise to the set of recursions tabulated under Algorithm 1. To this end, recall the augmented Lagrangian function in (III-C) and focus first on [S4]. From the decomposable structure of , (14) decouples into simpler strictly convex sub-problems for and , namely

| (46) | ||||

| (47) | ||||

| (48) |

Note that in formulating (47) and (48), the auxiliary variables and were eliminated using the constraints and , respectively. The unconstrained quadratic problems (47) and (48) admit the closed-form solutions

| (49) | ||||

| (50) |

Using (49) to eliminate and from (8) and (9) respectively, a simple induction argument establishes that if the initial Lagrange multipliers obey , then for all , where and . Likewise, the same holds true for and . The collection of multipliers is thus redundant, and (49)-(50) simplify to

| (51) | ||||

| (52) |

Observe that and for all , identities that will be used later on. By plugging (51) and (52) into (8) and (10) respectively, the non-redundant multiplier updates become

| (53) | ||||

| (54) |

If , then the structure of (53) reveals that for all , where and . Clearly, the same holds true for , and these identities will become handy in the sequel.

Moving on to [S3], (13) decouples into unconstrained quadratic sub-problems

The minimization (12) in [S2] also decomposes into simpler sub-problems, both across agents and across the variables and , which are decoupled in the augmented Lagrangian when all other variables are fixed. Specifically, the per agent updates of are given by

| (55) |

where the second equality was obtained after using: i) which follows from the identities and established earlier; ii) the definition ; and iii) the identity , which allows to merge the identical quadratic penalty terms and eliminate both and using (51).

Upon defining and following similar steps as the ones that led to the second equality in (VI), one arrives at

| (56) |

where the second equality follows by completing the squares. Problem (VI) is a separable instance of the Lasso (also related to the proximal operator of the -norm); hence, its solution is expressible in terms of the soft-thresholding operator as in Algorithm 1.

C. Proof of Proposition 3. Let , and likewise for all other convergent sequences in Algorithm 1. Examination of the recursion for in the limit as , reveals that . Upon vectorizing the matrix quantities involved, this system of equations implies that the supervector belongs to the nullspace of , where is the Laplacian of the network graph . Under (a1), this guarantees that . From the analysis of the limiting behavior of , the same argument leads to , which establishes the consensus results in the statement of Proposition 3. Hence, one can go ahead and define and . Before moving on, note that convergence of implies that , . These observations guarantee that the limiting solution is feasible for (P4).

To prove the optimality claim it suffices to show that upon convergence, the fixed point of the iterations comprising Algorithm 1 satisfies the Karush-Kuhn-Tucker (KKT) optimality conditions for (P4). Proposition III-A asserts that if , is indeed an optimal solution to (P1). To this end, consider the updates of the primal variables in Algorithm 1, which satisfy

| (57) | |||

| (58) | |||

| (59) |

Taking the limit from both sides of (57)–(59), and summing up over all yields

| (60) | |||

| (61) | |||

| (62) |

where . To arrive at (60), the assumption that is used, and thus which leads to .

Next, consider the auxiliary matrices , . In the limit as , the update recursion for in Algorithm 1 can be written as Proceed by defining , and observe that the input-output relationship of the soft-thresholding operator yields

| (63) |

Given (63), define the matrices and , and show that they satisfy the following properties: (i) (entrywise); (ii) if ; (iii) if ; (iv) ; and (v) . Properties (i)-(iii) follow after adding up the result in (63) for . Property (iv) is readily checked from the definitions of and . Finally, (v) follows since

where (from the identity ) is used to obtain the last equality.

References

- [1] [Online]. Available: http://internet2.edu/observatory/archive/data-collections.html

- [2] A. Abdelkefi, Y. Jiang, W. Wang, A. Aslebo, and O. Kvittem, “Robust traffic anomaly detection with principal component pursuit,” in Proc. of ACM CoNEXT Student Wkshp., Philadelphia, USA, Nov. 2010.

- [3] G. Adomavicius and A. Tuzhilin, “Toward the next generation of recommender systems: A survey of the state-of-the-art and possible extensions,” IEEE Trans. Knowledge and Data Engineering, vol. 17, no. 6, pp. 734–749, Jun. 2005.

- [4] J. A. Bazerque and G. B. Giannakis, “Distributed spectrum sensing for cognitive radio networks by exploiting sparsity,” IEEE Trans. Signal Process., vol. 58, pp. 1847–1862, Mar. 2010.

- [5] D. P. Bertsekas and J. N. Tsitsiklis, Parallel and Distributed Computation: Numerical Methods. Athena-Scientific, 1999.

- [6] P. J. Bickel, Y. Ritov, and A. Tsybakov, “Simultaneous analysis of Lasso and Dantzig selector,” Ann. Statist., vol. 37, pp. 1705–1732, Apr. 2009.

- [7] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge University Press, 2004.

- [8] E. J. Candes, X. Li, Y. Ma, and J. Wright, “Robust principal component analysis?” Journal of the ACM, vol. 58, no. 1, pp. 1–37, May 2011.

- [9] E. J. Candes and Y. Plan, “Matrix completion with noise,” Proceedings of the IEEE, vol. 98, pp. 925–936, Jun. 2010.

- [10] E. J. Candes and B. Recht, “Exact matrix completion via convex optimization,” Found. Comput. Math., vol. 9, no. 6, pp. 717–722, Dec. 2009.

- [11] E. J. Candes and T. Tao, “Decoding by linear programming,” IEEE Trans. Info. Theory, vol. 51, no. 12, pp. 4203–4215, Dec. 2005.

- [12] V. Chandrasekaran, S. Sanghavi, P. R. Parrilo, and A. S. Willsky, “Rank-sparsity incoherence for matrix decomposition,” SIAM J. Optim., vol. 21, no. 2, pp. 572–596, 2011.

- [13] A. Chistov and D. Grigorev, “Complexity of quantifier elimination in the theory of algebraically closed fields,” in Math. Found. of Computer Science, ser. Lecture Notes in Computer Science. Springer Berlin / Heidelberg, 1984, vol. 176, pp. 17–31.

- [14] S. Chouvardas, K. Slavakis, Y. Kopsinis, and S. Theodoridis, “A sparsity-aware adaptive algorithm for distributed learning,” IEEE Trans. Signal Process., 2011, see also arXiv:1112.5716v1 [cs.IT].

- [15] T. Hastie, R. Tibshirani, and J. Friedman, The Elements of Statistical Learning, 2nd ed. Springer, 2009.

- [16] R. A. Horn and C. R. Johnson, Matrix Analysis. Cambridge University Press, 1985.

- [17] D. Jakovetic, J. Xavier, and J. Moura, “Cooperative convex optimization in networked systems: Augmented Lagrangian algorithms with directed gossip communication,” IEEE Trans. Signal Process., vol. 59, pp. 3889 –3902, Aug. 2011.

- [18] I. T. Jolliffe, Principal Component Analysis. New York: Springer, 2002.

- [19] A. Lakhina, M. Crovella, and C. Diot, “Diagnosing network-wide traffic anomalies,” in Proc. of ACM SIGCOMM, Portland, USA, Aug. 2004.

- [20] Y. Liao, W. Du, P. Geurts, and G. Leduc, “DMFSGD: A decentralized matrix factorization algorithm for network distance prediction,” IEEE/ACM Trans. Network., 2011, see also arXiv:1201.1174v1 [cs.NI].

- [21] M. Mardani, G. Mateos, and G. B. Giannakis, “Unveiling network anomalies across flows and time via sparsity and low rank,” IEEE Trans. Info. Theory, Feb. 2012 (submitted).

- [22] G. Mateos, J. A. Bazerque, and G. B. Giannakis, “Distributed sparse linear regression,” IEEE Trans. Signal Process., vol. 58, pp. 5262–5276, Oct. 2010.

- [23] A. Montanari and S. Oh, “On positioning via distributed matrix completion,” in Sensor Array and Multichannel Signal Processing Workshop, Jerusalem, Oct. 2010, pp. 197–200.

- [24] B. K. Natarajan, “Sparse approximate solutions to linear systems,” SIAM J. Comput., vol. 24, pp. 227–234, 1995.

- [25] B. Recht, M. Fazel, and P. A. Parrilo, “Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization,” SIAM Rev., vol. 52, no. 3, pp. 471–501, 2010.

- [26] B. Recht and C. Re, “Parallel stochastic gradient algorithms for large-scale matrix completion,” 2011 (submitted).

- [27] I. D. Schizas, G. B. Giannakis, and Z. Q. Luo, “Distributed estimation using reduced-dimensionality sensor observations,” IEEE Trans. Signal Process., vol. 55, pp. 4284–4299, Aug. 2007.

- [28] I. D. Schizas, A. Ribeiro, and G. B. Giannakis, “Consensus in ad hoc WSNs with noisy links - part I: Distributed estimation of deterministic signals,” IEEE Trans. Signal Process., vol. 56, pp. 350–364, Jan. 2008.

- [29] P. Sprechmann, I. Ramirez, G. Sapiro, and Y. Eldar, “C-HiLasso: A collaborative hierarchical sparse modeling framework,” IEEE Trans. Signal Process., vol. 59, no. 9, pp. 4183–4198, Sep. 2011.

- [30] M. Thottan and C. Ji, “Anomaly detection in IP networks,” IEEE Trans. Signal Process., vol. 51, pp. 2191–2204, 2003.

- [31] R. Tibshirani, “Regression shrinkage and selection via the Lasso,” J. Royal. Statist. Soc B, vol. 58, pp. 267–288, 1996.

- [32] J. Tropp, “Just relax: Convex programming methods for identifying sparse signals,” IEEE Trans. Info. Theory, vol. 51, pp. 1030–1051, Mar. 2006.

- [33] M. Yuan and Y. Lin, “Model selection and estimation in regression with grouped variables,” J. Royal. Statist. Soc B, vol. 68, pp. 49–67, 2006.

- [34] Y. Zhang, M. Roughan, W. Willinger, and L. Qiu, “Spatio-temporal compressive sensing and internet traffic matrices,” in Proc. of ACM SIGCOM Conf. on Data Commun., New York, USA, Oct. 2009.

- [35] Z. Zhou, X. Li, J. Wright, E. Candes, and Y. Ma, “Stable principal component pursuit,” in Proc. of Intl. Symp. on Info. Theory, Austin, USA, Jun. 2010, pp. 1518–1522.