Communication over Individual Channels – a general framework

Abstract

We consider the problem of communicating over a channel for which no mathematical model is specified, and the achievable rates are determined as a function of the channel input and output sequences known a-posteriori, without assuming any a-priori relation between them. In a previous paper we have shown that the empirical mutual information between the input and output sequences is achievable without specifying the channel model, by using feedback and common randomness, and a similar result for real-valued input and output alphabets. In this paper, we present a unifying framework which includes the two previous results as particular cases. We characterize the region of rate functions which are achievable, and show that asymptotically the rate function is equivalent to a conditional distribution of the channel input given the output. We present a scheme that achieves these rates with asymptotically vanishing overheads.

I Introduction

This paper revisits the “individual channel” communication model [1], which provides an alternative framework for communication over unknown channels. The communication setup is illustrated in Figure 1. An encoder sends an input sequence into the channel. The output of the channel is determined in a completely arbitrary way which is unknown to the encoder and the decoder. However, there is a perfect feedback link from the decoder to the encoder, and we also assume the existence of common randomness. Under these assumptions we would like to characterize a communication rate for the channel. Clearly, since nothing is guaranteed with respect to the output, one cannot guarantee any positive communication rate a-priori, and achieve a vanishing error probability. Therefore, instead, we define a rate as a function of the specific input and output sequences (, termed a rate function).

The motivations for this communication model are elaborated upon in our initial paper [1], and will be briefly explained here through an example. We consider the example of the binary channel , where is an arbitrary sequence. The traditional way to deal with this channel would be by using the arbitrarily varying channels (AVC) framework [2]. In this framework feedback is not considered, and the AVC capacity is the maximum reliable communication rate that can be attained irrespective of the choice, or distribution, of the state sequence (in this case ). However, in order to obtain a positive capacity, it is necessary to place a constraint on . Suppose that we limit the maximum rate of errors to , then by applying common randomness the AVC capacity becomes . This result requires placing an a-priori constraint. Furthermore, because of the worst-case nature of the AVC capacity, the communication rate will not improve if , i.e. the channel is actually better than we have assumed. Shayevitz and Feder [3] proposed to deal with this issue by using feedback, and have presented a scheme that without assuming any prior constraint on , achieves the rate .

This result, and its extensions [4] allows us to replace a-priori constraints by the empirical distribution of the noise (or state) sequence that actually occurred, thus alleviating the worst-case assumptions. The result is that the rate is defined by the sequence (i.e. the channel). Still, we need to assume a channel model relating the input and the output. Since channel models are in many cases a coarse abstraction of reality, and in some cases may be completely unknown, the next step is to ask: can we do without the model, by, so to speak “extracting” this model from the empirical data? In doing so, we define the empirical rate function by using both the input and the output. This is a fundamental change with respect to the previous models, since the input is determined by the scheme itself.

In the previous paper [1] we have shown that it is possible to attain the empirical mutual information , as well as the function , where is the empirical correlation factor. The later function is suitable for channels with real-valued inputs and outputs. These rate functions are appealing since they are direct counterparts of statistical information measures. For the case of a discrete memoryless channel, the empirical mutual information over the sequences tends in probability to the statistical mutual information over the input and output random variables. The second function tends to the mutual information between two Gaussian random variables with the same correlation factor, and thus is optimal for Gaussian channels. These results generalize achievability results for compound channels and AVCs, and enable to easily re-derive the previously mentioned results [3, 4], and even extend them [1, Section VII.B]. However many questions are left open. For example, how can these functions be modified to include memory or take into account MIMO channels, and what is the set of achievable rate functions? Is there a general way to extend the concept of “empirical mutual information”? In addition, in the previous paper we have separated the discussion on the discrete and the continuous cases, from technical reasons, and the natural question that raises to mind is whether the two results can be put into a unified theory.

The main objective of this paper is to define such a unifying theory, by first characterizing the set of achievable rate functions, presenting general communication schemes for achieving these rates with, and without feedback (where only in the first case, the communication rate is adaptive), and presenting a tighter analysis of the overheads related to universally achieving these rate functions. The new techniques used in this paper enable us to derive various rate functions and analyze the overhead (or rate loss) required for attaining them in a finite block length. We present refined proof techniques that lead to tighter bounds and re-derive, and improve over the previous results [1, 5, 6]. However note that the different proof techniques used in the previous work [1] are interesting on their own, and sometimes more intuitive. We will highlight the connections between the results in the sequel.

II Overview

Following is a high level overview of the ideas and results presented in this paper. As mentioned above we would like to refrain from stating the channel model. We define the rate of a system using a “rate function” of the input sequence and output sequence . We would like to find systems which guarantee attaining certain rate functions.

The first step is to define what “attaining” a rate function means. We refer to two kinds of systems: fixed rate systems without feedback, and adaptive-rate systems using feedback. The adaptive rate systems guarantee that the transmitted rate would be at least while keeping a small probability of error, for any input and output sequence. I.e. this guarantee holds irrespective of the channel model. In the fixed rate case, since we cannot guarantee any positive rate a-priori (the Shannon capacity of the channel in Figure 1 is ), the system only guarantees reliable communication when (the event can be considered as “outage”). Therefore the adaptive case is of more interest from a practical perspective. We allow unlimited common randomness between the encoder and the decoder, and in order to avoid circular definitions, we constrain the input distribution to a given prior . These definitions are stated formally and discussed in Section III.

In classical communication and information theory, one only considers the average error probability over the channel law and requires a certain static rate of communication, whereas here we require that the rate function would be specified per input-output pair , and that a certain error probability would be achieved. This may be seen as an over-requirement, however note that every system has, in effect, a rate function: one can always look at all the cases where the input was a specific and the output was a specific and ask what was the actual rate of error free bits that was received in this case. Thus, we can consider the “rate function” as way for characterizing communication systems which is “channel independent”. On the other hand, as we will see in Section IV-E, with a small overhead, the rate function of any system can be attained with a fixed error probability.

The first question we ask is – which rate functions are achievable (Section IV)? Theorem 1 gives a necessary and a sufficient condition for the achievability of a rate function (in the non-adaptive case), which are tight in the sense of the achieved rate for large block size . In an analogy to universal source coding, this theorem is equivalent to the Kraft inequality, stating which source encoders are feasible (in terms of the set of word lengths). Based on this result, we can characterize the “intrinsic redundancy”, which is a property of any rate function, determining the redundancy that would be needed to achieve it (Theorem 2). Then, considering more general systems, it is shown that the good-put associated with a specific choice of in any system, is in-fact an achievable rate function, and therefore can be achieved with an error probability as low as desired, per sequence, up to a small overhead in rate.

The characterization of Theorem 1 is based on the CDF of the rate function with respect to the input distribution , which is inconvenient to handle. In Section V we deal with the asymptotic behavior of rate functions, and show that asymptotically, the achievability of rate functions can be determined based on a simpler condition similar to the Chernoff bound (Theorem 4). The main result of this section is Theorem 5 which shows that the maximum rate functions are asymptotically of the form for some conditional probability . Thus, selecting rate functions is asymptotically equivalent to selecting conditional distributions . Returning again to the analogy to source coding, this claim is similar to the claim that, due to Kraft inequality, every source encoder is defined by a probability distribution on the set of possible messages [7].

The set of achievable rate functions is rather arbitrary (like the set of possible encoders, in the analogy). In Section VI we discuss the problem of selecting the rate function, using several possible constructions. Each construction has a certain justification and results in a certain form. The first construction that we term “maximum likelihood construction” (Section VI-B) is based on taking the maximum of the form over a class of models . Achieving this rate function guarantees matching (or surpassing) the rate of any system operating over any of the channels in the model class. Another way to remove the arbitrariness (Section VI-E) is to limit the scope to rate functions defined based on a predefined set of parameters (for example the empirical second order moments, or zero order joint statistics). When the parameters can take only a sub-exponential number of values, the input and output sequences can be grouped into “types” of sequences having the same values of the empirical parameters. Theorem 6 determines the optimal rate function that can be obtained in this case. We particularize the result to the memoryless case, and present the best rate function that can be defined by zero order statistics (Lemma 5). This rate function can be also stated in terms of the “maximum likelihood” construction, and on the other hand is close to the empirical mutual information, which means that the empirical mutual information is essentially optimal (in terms of using the zero order statistics). A third way to define a rate function (Section VI-F) is by taking another system as a reference and asking what is the maximum rate that can be achieved with a given decoding metric and a given prior, when the number of messages is allowed to vary – i.e. conditioned on a certain pair of input and output, how many messages can one send while still maintaining a small probability of error? In the rest of the paper we focus mainly on the “maximum likelihood’ construction.

The main strength of the “individual channel” approach is when the rate function can be obtained adaptively, without outage. Section VII focuses on rate adaptivity. In Section VII-A we present a communication scheme that attains an adaptive rate using multiple iterations of rateless coding. Theorem 7 and its corollaries characterize the performance of the proposed rate adaptive scheme. The scheme is based on a decoding metric that must satisfy some conditions and needs to be specified later, and the rate function is given as function of this metric. In what follows we substitute various metrics to obtain various rate functions. In Section VII-E we show that under a “causality” condition, the rate function (which is the asymptotical bound for all rate functions) can be adaptively achieved (Theorem 8).

Next we focus on “maximum likelihood” rate functions (Section VII-F). In Theorem 9 we show the achievability of such rate functions when the “maximum likelihood” probability can be given as a weighted sum of (which always holds when the number of -s is subexponential in ). We particularize this result for rate functions based on empirical probabilities (Theorem 10) and present bounds on the redundancy for the adaptive and non-adaptive case. In the more general case where belongs to an infinite class, we do not have a general result on adaptivity, however we show that some properties required for the application of Theorem 7 hold in general for the “maximum likelihood” construction (Lemma 7).

The rate adaptive scheme presented in Section VII-A is finite horizon, i.e. it requires prior knowledge of the block length . In Section VII-G we present an infinite horizon extension of the scheme, based on a simple “doubling trick”. The modified scheme attains the results of Theorem 7 under some assumptions. Unfortunately the results regarding rate adaptivity in Section VII are not as tight and elegant as the results in the non-adaptive case – this manifests itself in the relatively high redundancy of the scheme (which generally behaves like in the block length), as well as its complexity, and the fact we do not have a tight lower bound (necessary condition) on the redundancy.

In Section VIII we present examples for rate functions, which include as particular cases the previous results [1]. The rate functions include the empirical mutual information (Section VIII-A), an extension that uses memory in the channel (which is optimal for stationary ergodic channels, Section VIII-B), a discussion on extensions that include time variation (Section VIII-C), the modulo-additive rate function presented by Shayevitz and Feder [3] (Section VIII-D), rate functions based on compression (Section VIII-E), and a second-order rate function for the MIMO channel (Section VIII-F, Theorem 13 and Lemma 10). .

Section IX is devoted to comments and further research. In Section IX-A we compare with the results of the previous paper [1].

Before beginning the formal parts, several comments are due on the general approach taken in this paper. First, this work is theoretical in nature. No effort is made to improve the decoder complexity, or reduce the amount of common randomness required. The reason behind this is that we are mainly interested in examining this communication concept. If we see the concept is fruitful, the next step should be trying to make it the implementation practical. Also, while we do not attempt to be practical regarding the implementation, the requirements from the system do need to be related to practical targets. The second comment is that in this work we focus on transmission rate rather than on error exponents. The theoretical reason is that the discussion around error exponents is based on the fact the error probability with a fixed rate and a known, stationary ergodic channel, decreases exponentially. Here, the rate is not fixed, and the channel is not specified, so this does not necessarily hold true. The second reason is practical – from a practical perspective of requirements, there is no reason to require the system’s error probability to decrease exponentially fast (if at all, the block error rate should be allowed to increase with ). Rather, it makes sense to require a small, but fixed, error probability.

III Definitions

The definitions in this section almost identical to the ones stated in the previous paper [1], and are repeated here for completeness. The main difference is the absence of the set . We define the channel, adaptive and non-adaptive systems and achievability in the adaptive and non-adaptive sense. If the motivation for these definitions is not immediately clear, the asymptotically achievable rate functions and can be regarded as motivating examples.

III-A Notation

Uppercase letters denote random variables, and respective lowercase letters denote their sample values. Boldface letters are used to denote vectors, which are by default of length . Superscript and subscript indices are applied to vectors to define subsequences in the standard way, i.e. , . The indices are allowed to exceed the range of indices where is defined (for example be negative), in which case only the indices in the definition range will be considered (e.g. , ). The indicator function where is a set or a probabilistic event is defined as over the set (or when the event occurs) and otherwise. denotes the product of conditional probability functions e.g. . denotes a uniform distribution over the set .

denotes the set of real numbers, and denotes a Gaussian distribution with mean and variance . denotes norm. denotes the Bernoulli distribution, and denotes the binary entropy function.

A hat () denotes an estimated value. The empirical mutual information of two vectors is the mutual information between two random variables whose joint distribution equals the empirical distribution of [8, Section II]. An exact definition of empirical mutual information and other empirical information measures is delayed to sections VI-A4 and VI-A5. We denote the mutual information when .

The functions and as well as information theoretic quantities are in base 2 (bits) (and can be interpreted as other information units by changing the base of the ). We use to denote the natural logarithm.

Bachmann & Landau notations are used for orders of magnitude. Specifically, , means , or means and means .

Most of the results apply both to the case where the input is discrete, and characterized by a probability mass function, and to the case it is continuous and characterized by density function. When denoting as the probability of without specifying whether is continuous or discrete, it means that may be substituted by either the probability mass function or a density function, as applicable.

Note that proofs are given sometimes after the Theorem/Lemma is stated, and sometimes before it, as seems easier to read. In the later case the Theorem/Lemma summarizes a conclusion from a discussion.

III-B Individual channels and rate functions

Definition 1 (Channel).

A channel is defined by a pair of input and output alphabets , and is denoted

Definition 2 (Rate function).

A rate function for the channel may be any real valued function of .

Note that we do not preclude negative values, for reasons of notational convenience. Also, we have defined the set of possible outputs as length vectors mainly for the sake of concreteness; many of the results in the paper do not assume anything about the structure of , and thus in general, the output does not have to be a vector of the same length of the input.

III-C Fixed rate communication without feedback

Definition 3 (Fixed rate encoder, decoder, error probability).

A randomized block encoder and decoder pair for the channel with block length and rate without feedback is defined by a random variable distributed over the set , a mapping and a mapping . The error probability for message is defined as

| (1) |

where for such that the conditioning in (1) cannot hold, we define .

This system is illustrated in Figure 2. We treat as a random variable and as a deterministic sequence. This does not preclude applying the results to a channel whose output is a random variable and depends on , since all results are conditioned on both and . Note that the encoder rate must pertain to a discrete number of messages , but the empirical rates we refer to in the sequel may be any positive real numbers. In the sequel, is treated sometimes as a series of bits and sometimes as an index of the message.

Definition 4 (Achievability).

A rate function is achievable with a prior defined over and error probability if for any , there exist a pair of randomized encoder and decoder, with a rate of at least such that for any message : and for any where , .

We sometimes term this kind of achievability “non-adaptive achievability” to separate it from the adaptive achievability defined below. The usage of the notation does not immediately imply the rate function is achievable (or adaptively, or asymptotically achievable, by the definitions below). We sometimes place an superscript asterisk to specify that the given function is indeed achievable. Note that the definition requires that the conditions hold for all , however this is done mainly for convenience, and if we are interested in the achievability of at a specific we can always define a new rate function whose achievability indicates that the achievability conditions are met for for the specific .

III-D Adaptive rate communication with feedback

Definition 5 (Adaptive rate encoder, decoder, error probability).

A randomized block encoder and decoder pair for the channel with block length , adaptive rate and feedback is defined as follows:

-

•

The message is expressed by the infinite sequence

-

•

The common randomness is defined as a random variable distributed over the set

-

•

The feedback alphabet is denoted

-

•

The encoder is defined by a series of mappings

-

•

The decoder is defined by the feedback function , the decoding function and the rate function .

The random variables , and denote the outcomes of the respective functions. The error probability for message is defined as

| (2) |

In all cases discussed in this paper the feedback is binary . Furthermore we sometime consider reducing the feedback rate below bit/use. In this case some of the feedback values will be fixed to , and the feedback rate is the ratio of unconstrained feedback bits.

Definition 6 (Adaptive achievability).

A rate function is adaptively achievable with a prior defined over and error probability , if there exist randomized encoder and decoder with feedback, such that and for all :

| (3) |

In other words, with probability at least , a message with a rate of at least is decoded correctly.

The model in which the decoder determines the transmission rate is lenient in the sense that it gives the flexibility to exchange rate for error probability: the decoder may estimate the error probability and decrease it by reducing the decoding rate.

III-E Approximate achievability

Definition 7 (Achievability up to a gap).

We say that is achievable (adaptively/non adaptively) up to (or with a gap of ) with a certain and , if is achievable (adaptively/non adaptively, resp.)

Note that can be translated to a loss in rate. This is clear in the adaptive case where the rate is a function of . In the non adaptive case the definition above means there is a system that transmits at rate and achieves error probability of less than whenever (which is equivalent to ).

Definition 8 (Asymptotic achievability).

A sequence of rate functions defined for is asymptotically achievable (adaptively / non adaptively) with a prior defined for vectors of increasing size, if for all there exists a sequence of functions , with , such that is achievable (adaptively / non adaptively, resp.) with the given and .

Note that relating the rate function to the achievable function through is in general weaker than requiring that their ratio would tend to 1, since does not necessarily uniformly converge. As an example, consider , and the two (equal) functions then although , . The reason to use this definition is that indeed in many cases of interest, the convergence of the rate function is non uniform. However the results are useful since has a meaning of rate, and the slow convergence occurs only at high rates.

III-F Discussion

Note that achievability is defined with respect to a fixed prior . Although the rate function depends on specific sequences, for actual communication to happen it is necessary to select input sequences, and defines the main property of this selection needed for our purpose, i.e. the input distribution.

The reason for fixing is that the achievable rates are a function of the channel input, which is determined by the scheme itself. This is an opening for possible falsity – the encoder may choose sequences for which the rate is attained more easily. For example, by setting one can attain in a void way, since the rate function will always be . We circumvent this difficulty by constraining an input distribution, and by using common randomness, requiring that the encoder emits input symbols that are random and distributed according to the defined prior. This breaks the circular dependence that might have been created, by specifying the input behavior together with the rate function.

In a high level view we can say that the individual channel framework does not contain any tools to modify the input behavior – since nothing is assumed on the effect of a change in the input, and therefore the input prior is constrained. From this reason, in the current framework we only gain rate adaptivity from feedback, and but do not improve the communication rate. In channels with memory, it is possible to improve the channel capacity using feedback, but this improvement is due to modification of the input distribution (conditioned on the output). This gain cannot be obtained in the current framework due to the constraint on the input distribution.

Note that these results hold under the theoretical assumption that one may have access to a random variable of any desired distribution, which is in some cases un-feasible to generate in an exact manner – see further discussion in our previous paper [1].

IV Fundamental limitations on rate functions

The selection of rate functions is rather arbitrary. This could be seen by the following example: suppose is achievable, and let be a permutation of the output values, then clearly is also achievable, by placing the permutation before the decoder (so that the effective channel output seen by the system is ). In general none of the rate functions generated by various values of is uniformly better than the others. In the sequel we will discuss possible reasonable ways to choose rate functions, that may eliminate some of these choices. However we start with the more basic question: what is the set of achievable rate functions?

In this section and the following ones we focus only on the non-adaptive case, and characterize the set of achievable rate functions. The role of this bound is similar to the role of Kraft’s inequality in source encoding – it does not indicate a preference to specific encoders, but merely states which encoding lengths are possible (can be implemented by uniquely decodable encoders) and which are not. The rate function takes the role of encoding lengths in Kraft’s inequality.

IV-A A characterization of the set of achievable rate functions

The following theorem presents a necessary and a sufficient conditions for a rate function to be achievable, in the fixed sense.

Theorem 1.

Consider communication over block length , with a prior and error probability . If is achievable, or adaptively achievable, then:

| (4) |

Conversely, if

| (5) |

then is achievable.

Where means the probability with respect to distributed of the event . The necessary condition refers to both achievable and adaptively achievable rate functions, whereas the sufficient condition only refers to achievable rate function (adaptive achievability is discussed in Section VII). Note that the necessary condition holds trivially for (the definition is extended to negative -s for matters of convenience, which will become clear later on). These conditions are depicted graphically in Figure 4 where the horizontal axis is the rate and the vertical axis is the probability .

Both bounds characterize the achievability of based on the probability of to exceed a threshold for a fixed value of (its CCDF). The rationale behind this characterization is as follows. Consider the system of Definition 3, and fix the output . Clearly, no information can be transmitted in this case. At each block, there is a codebook of input sequences , that would be transmitted if the input message is . The decoder does not know which of these words was chosen but only knows the codebook. However, it guarantees that in high probability it will decode the correct word, if this word has . This is possible only if in most codebooks, only one word satisfies the condition. This leads to the bound on the probability of .

Note that if a rate function satisfies the sufficient condition with strict inequality (for all or some -s and -s), then it can be modified to a larger function meeting the condition with equality, by using the inverse transform theorem, i.e. by passing the random variable through its CDF to obtain a uniform random variable and then through the desired CDF satisfying (5) with equality. A remarkable property in the necessary and sufficient conditions is that, since they are given per value of , there is no tradeoff between different (i.e. one can decide on a rate function separately for each ). Indeed, these are only bounds, and in an accurate characterization of the domain of achievable rate functions there is a tradeoff between different -s. But later on we shall see that this property, of separation between -s holds also in the asymptotical form of the bound (Theorem 5).

Following Theorem 1, it is convenient to make the following definition: define the intrinsic redundancy of a rate function with respect to a prior as:

| (6) |

This definition simply extracts the normalized coefficient before the in Theorem 1, i.e. it is the minimum value such that:

| (7) |

Theorem 1 can now be stated as follows:

-

1.

A rate function is achievable if

-

2.

A rate function is achievable only if

It is easy to see that the inequalities above together with the definition of directly imply the inequalities in Theorem 1. Note that the two bounds on converge to for fixed as .

Intuitively the intrinsic redundancy characterizes an overhead that exists in and will be expressed in a loss when trying to achieve this rate function. The more “ambitious” the rate function, the larger the redundancy. We note the following two properties of :

-

1.

When an offset is added to (or subtracted from) the rate function:

(8) -

2.

When taking the maximum of several rate functions , we have:

(9) can be regarded as the price payed for “universality”, in the sense of exceeding several rate functions.

The proof of these properties is straightforward and is deferred to Section -B.

Suppose that a rate function has a given intrinsic redundancy , we may reduce it by an offset to make this rate function achievable. Denote , then will be achievable if , i.e. if . Conversely, it will not be achievable if , i.e. if . Using this argument, we can characterize the achievability of rate functions by specifying what value of (overhead) turns them into achievable. This is formalized in the following theorem:

Theorem 2.

For a rate function to be achievable up to , with prior and error probability , it is necessary that and sufficient that .

This theorem gives a meaning to the term “intrinsic redundancy” and we can see how it affects the actual redundancy. The actual redundancy is comprised of a term depending on the intrinsic redundancy and a term depending on the desired error probability. The proof is given by the discussion above. Using this theorem we can see more clearly the rate penalty for decreasing the error probability. Supposing that we know a rate function is achievable with an error probability , then we may use the theorem to bound the redundancy required to achieve it with an error probability . Furthermore, (9) implies that competing against competitors who attain the rate functions , incurs a small asymptotical price.

Up to the gap between the necessary and sufficient conditions in Theorems 1,2, these conditions are the equivalent of Kraft inequality for rate functions. If a rate function meets them, it is tight in the sense that it cannot be improved uniformly. In some sense however they are weaker than Kraft inequality, since the later applies to each uniquely decodable fixed to variable code, while our conditions apply only to communication systems which attain the error probability individually for each . In general, when comparing to information theoretic results pertaining to probabilistic channel settings, because the requirements we make are stricter (we require a rate and error probability guarantee per rather than on average), our achievability results are stronger, while our necessary conditions (converse) are weaker, since they hold for a restricted class of systems.

Theorems 1-2 also bring another observation: any rate function which is achievable (by any system), is also achievable using random coding (the system achieving the sufficient condition), up to a small overhead.

The gap between the upper and lower bounds of Theorem 1,2 is equivalent to an overhead of bits over the entire transmission. This overhead is bits for , so in the scope of working with a fixed but small (rather than ), the difference between the bounds is small. An analysis for the reasons of this gap can be found in [9]. It is shown that the necessary condition can be reduced by almost one bit at the price of complicating the decoder and the proof, and cannot be further reduced in the current form of the bound. It appears by that analysis that for most rate functions, the required redundancy is close to the one required by the sufficient condition.

IV-B Proof of Theorem 1

IV-B1 Necessary condition (converse)

In this section we prove the first part of Theorem 1. We need to show that the condition (4) holds for achievable, and adaptively achievable rate functions. We begin with the case of achievable rate functions (non adaptively).

Suppose is achievable with , . Consider and encoder and a decoder designed for rate over block size and satisfying Definition 4. There are input messages. Each input message is translated by the encoder into the random sequence , which is a random variable distributed in (implemented by the common randomness ), and is known to the decoder.

According to the requirements of Definition 4, the distribution of should be , since the definition requires the input distribution to be for any input message. However for the converse we assume a milder condition: we only assume that the scheme achieves on average, i.e. that the input distribution is when is chosen uniformly over , in other words:

| (10) |

Note that the codewords may be statistically dependent.

Denoting by the decoded message, then according to Definition 4, we have:

| (11) |

Note that the definition implies that (11) holds with respect to the transmitted message. However, since is a function of and , for a fixed it does not depend on the transmitted message, and therefore, by considering that any of the possible messages may be input to the encoder, and using Definition 4 with respect to this message, we have that (11) holds for any . Therefore the following holds for any (where probabilities are over the randomness in the codebook):

| (12) |

Therefore

| (13) |

This holds for any . In addition Definition 4 requires that such a system will exist for any , therefore (13) holds for any as well. This proves the claim for the case of achievable .

The case of adaptively achievable follows from the same argument. First, one may convert the adaptive rate system with feedback into a non-adaptive rate system with feedback: fix a rate and let the decoder output only bits, and an error if the rate is . Therefore whenever in probability the message will be decoded correctly. Now, note that (12) refers to any fixed value of . Therefore (12) holds even if the encoder knows the value of , and particularly it holds also in the presence of feedback (partial and sequential knowledge of ). Hence the results holds also for which is adaptively achievable.

IV-B2 Sufficient condition (direct)

The direct side is shown by generating the codewords i.i.d. with distribution . Thus, the condition on the input distribution is met. The decoder, after observing , chooses to be the index of the word with the maximum value of (breaking ties arbitrarily), i.e.

| (14) |

We assume a given message , and a given . Since the codewords are independent, conditioning on does not change the distribution of the other codewords. By the union bound, the probability of error is bounded by:

| (15) |

where in the last inequality we substituted . Therefore if , we will have as required.

IV-C Comments on the proof of Theorem 1

-

•

To understand the proof of the necessary condition, it is useful to think that the channel output is set to a constant. Thus, the decoder is isolated from the encoder, and is required to decide on the message based solely on its knowledge of the codebook.

-

•

The proof of the theorem teaches something about the way rate functions are achieved: conditioning on and , the different codebooks generated all include , and in addition other codeword. If is large, then in most codebooks, the other codewords will have a smaller value of , due to the constraint on its distribution. Therefore, by choosing the word with the maximum , the decoder would usually be correct. The necessary condition means that this is actually required to happen in order for to be achievable: as the decoder is “isolated” from the encoder, and still committed to (11). If there are several words with the decoder will need to toss a coin and split the distribution in some way between them, with a large probability to be in error. The analysis of the gap between the necessary and sufficient condition in [9] sheds more light on this topic.

-

•

By the current definitions, it is assumed that the input distribution does not depend on . However note that since the proofs of the necessary and sufficient conditions both consider a fixed value of , the results hold, under a suitable formulation, also for the case where the input distribution depends on .

-

•

We can adopt two point of views when considering systems satisfying Theorem 1 (the achievability of rate functions): one is as communication systems trying to convey messages over an unknown channel; another is a cynical perspective in which we do not assume the input and output are related (and thus it is impossible to convey information), but we are only trying to design systems that satisfy the promises of the theorems, and the question is viewed as a game between the encoder and decoder, and the environment choosing and the message. The first point of view gives us the motivation and application of the theorems; the second is more suitable for the design and analysis. This is similar to the case of prediction and learning with expert advice [10][11] – when designing these learning algorithms the assumption is that the information supplied by the experts is completely arbitrary, and therefore the target is not to “learn” but just to compete; but the application of the results is for learning (where we assume there is some information at least in some of the experts advice).

IV-D Examples

Example 1 (A wire).

Consider the binary input – binary output channel with the rate function , i.e. iff the output is identical to the input. This function is easily achievable, with . To attain this rate function without error , one simply transmits the message un-coded, at a rate . If the channel output happened to equal the input, the communication had succeeded. If it happened to be different, and thus no guarantee was made. needs to be uniform in order to achieve rate 1. For this rate function and any , the condition is satisfied by one sequence, and therefore . This satisfies the necessary condition in Theorem 1 with equality for , and thus the sufficient condition is not tight here.

Note that the codebook that achieves this rate function is not a random i.i.d. codebook - the codewords are fixed, or, in order to achieve the input distribution condition, should be generated by randomly permuting the possible sequences. Therefore the codewords are correlated, which is necessary in order to obtain the necessary condition. Furthermore, the regions of for which obtained for different -s are disjoint, in which case, as we have noted, the necessary condition could be tight. If we had insisted on generating the codewords independently, then this rate function could not be achieved without some loss, due to the probability of two codewords being equal, therefore in that case the maximum rate would be closer to rate determined by the sufficient condition.

Example 2 (A fixed codebook).

Similarly, consider transmission using a fixed codebook of codewords, and an arbitrary fixed decoder. We may randomly permute the messages in order to guarantee a fixed input distribution for any message. In this case when is in the codebook and otherwise. Define the rate function as if is decoded by the decoder to the message represented by , and otherwise. Then for , , and as before the necessary condition is satisfied with equality for .

Example 3 (The empirical mutual information).

Example 4 (A second order rate function).

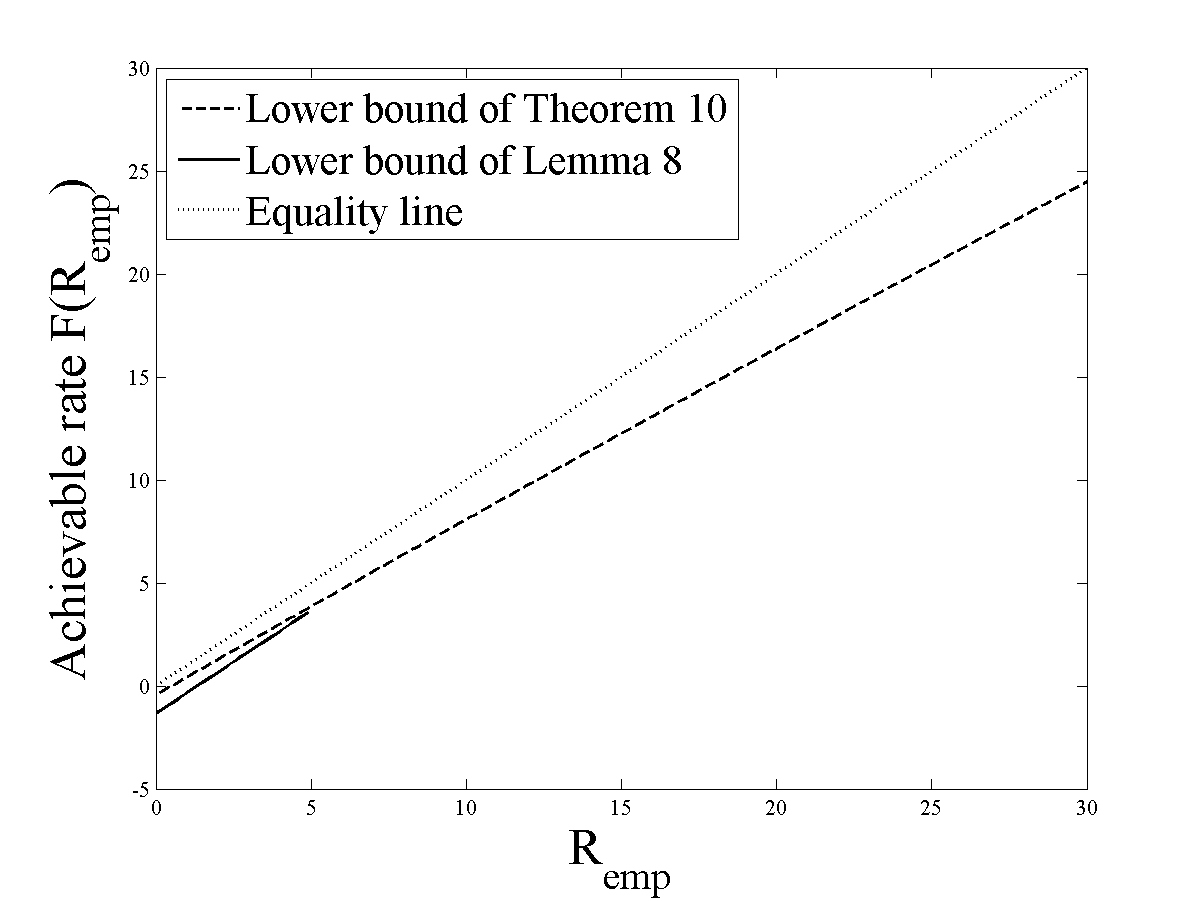

The rate function presented in the previous paper [1] has an intrinsic redundancy . This results from the factor instead of in Lemma 4 there, which causes the fact grows slower than for large values of . The implication is that this rate function cannot be attained with a fixed loss, but the loss must grow with . So for example one cannot attain , but one can attain (with ). The proof is technical and is deferred to Appendix -F5.

IV-E General systems and Good-put functions

The requirement to attain a fixed error probability for every releases the characterization of the communication system from dependence on the channel. On the other hand, it may seem as an over-requirement, since from application perspective requiring low average error probability may be sufficient. In this section it is shown that this over-requirement is not as strong as may seem: any communication system may be converted to a system guaranteeing a small error probability, with a small price in the rate.111Practically, the later system may be more complex to implement. This result holds in full generality only for the non-adaptive case, however considering the sub-set of adaptively achievable rate functions presented in Section VII, it makes sense to believe that for many systems of interest, this will hold also adaptively. Thus, the concept of attainable rate functions is not as esoteric as it would initially seem.

Let us consider a system delivering a rate with an error probability . This system may be quite general. To fix thoughts, it may be useful to consider the two examples of a practical (Turbo/LDPC) encoder and a decoder, perhaps combined within a more complex system involving channel estimation, feedback, scrambling, etc, and on the other hand, a theoretical random coding system. Each system generates a certain input distribution , which is assumed to be independent of the channel output.

In order to characterize the system with a single number, consider the rate of error-free bits delivered by the system, sometimes referred to as “good-put” (in contrast to throughput):

| (16) |

This value is a little optimistic, because it ignores the need to detect the errors. As an example, delivering one bit per second with error probability half is not the equivalent of half a bit per second. This additional gap is related to the factor in Fano’s inequality, and is asymptotically negligible. Now, assuming that and are not fixed but may change (depending, e.g. on the channel, on common randomness), the good-put is the average of the above, i.e.

| (17) |

To obtain a characterization of a system, which is independent of the channel, the above may be conditioned on the channel input and output . Define

| (18) |

In other words, is the average good-put obtained with the system when the input and output happened to be . For a deterministic block encoder/decoder, the conditional error probability is either or , and the good-put is, respectively, either or . The function is only a function of the system and not of the channel, and when a specific probabilistic channel is known, the average good put may be computed as .

Next, let us show that for any system, is an asymptotically achievable rate function (with the prior ). Initially, it is assumed that is a constant, i.e. the system delivers a constant rate, with a varying error probability . Assume the message is a uniform random variable , . The system is defined by common randomness (possibly), a transmission function and a decoding function (see Definition 3). Now, consider the system’s operation when set as a constant. Any feedback the system might have, can be ignored, as it conveys constant information. In this case, and are independent, and:

| (19) |

The error probability is

| (20) |

Now,

| (21) |

For any , the sum above is bounded by :

| (22) |

Combining (21) and (LABEL:eq:A758), yields:

| (23) |

For the function is decreasing. Substituting , yields that is decreasing with for , and therefore . For (where ), the probability above (23) can be simply upper bounded by . This yields the following simple bound:

| (24) |

For the case of , the above holds trivially. The bound above corresponds to the sufficient condition of Theorem 1, with an intrinsic redundancy of , and is therefore it is asymptotically achievable (Theorem 2). Notice that the system achieving this rate (Section IV-B2) is potentially very different than the original system. Furthermore, the bound leading from (23) to (24) is very coarse, which implies the good-put is a very pessimistic bound on the rate that can be achieved. This is because the error probability can be exponentially improved with a decrease in the rate, while in the good-put function, there is only a linear decrease (e.g. the error probability when attaining is with the original system, whereas it could have been significantly better). The extension to rate adaptive systems appears in Appendix -C . This is summarized by the following Lemma:

Theorem 3.

An interesting and insightful resulting of the combination of Theorem 3 and Theorem 5 which is proven in Section V, is that the rate of any system can be characterized by two probability functions and (where the second is the input distribution).

If, furthermore, this achievable rate function satisfies the structure defined in Section VII, then it is also asymptotically adaptively achievable. I.e. there exists a system attaining the same rates, but with an error probability as small as desired, per any pair of sequences.

V An asymptotical characterization of achievable rate functions

In Theorem 1 we have shown that achievable rate function have a CCDF upper bounded by a decaying exponential function. Therefore it stands to reason that the Chernoff bound for the probability may be rather tight. From this observation we derive asymptotical necessary and sufficient conditions which are easier to calculate. The main result of this section is that asymptotically achievable rate functions are bounded by the form for some conditional probability assignment . As a result this form can be used as a prototype for rate functions.

V-A The Chernoff and Markov inequalities

The Chernoff and Markov inequalities are useful tools in the following analysis. The Markov inequality simply states that for any non-negative random variable ,

| (25) |

The proof is simple, by applying the expected value operator to both sides of . From this simple bound, many useful bounds can be derived, for example the Chebyshev inequality is obtained by substituting . The Chernoff upper bound for is obtained by substituting for some constant , and then optimizing over . The main strength of Chernoff bound results from the fact that when is a sum of independent random variables , then breaks into a product of terms associated with each individual element, which is in most cases simpler to calculate. Since information theoretic values are associated with log-probabilities, the Markov and Chernoff bounds are virtually the same in our context (the Chernoff bound when applied to the log-probabilities is equivalent to the Markov inequality applied to the probabilities).

V-B Application of the Chernoff bound

Consider a sequence of rate functions for . We would like to find out whether is asymptotically attainable. Although may be asymptotically attainable, the intrinsic redundancy associated with it may not tend to zero. In other words, it may be possible to attain (with ), but is not necessarily of the form with . Therefore it is useful to consider more general functions . As an example for such a case see the rate function for the continuous MIMO channel presented in Section VIII-F, which is achieved up to .

We consider the rate function . Using the Chernoff/Markov inequality to bound the probabilities in Theorem 1, we have:

| (26) |

where

| (27) |

In many cases, for a suitable choice of , such as , calculating is simpler than calculating the probability . From this bound we have that the intrinsic redundancy (6) of satisfies

| (28) |

by Theorem 2, this implies that is achievable up to . If for any sequence , we have (in other words, increases subexponentially with ), this implies that is achievable where and therefore is asymptotically achievable. On the other hand, as we show below, this condition is also necessary. This manifests the claim that the use of the Chernoff bound is asymptotically tight.

V-C Asymptotic tightness of the Chernoff bound

Theorem 4.

A sequence of rate functions is asymptotically achievable with a sequence of priors , iff there exists a sequence of functions , such that for all :

| (29) |

where is defined in (27).

Note that comparing with the conditions of Theorem 1, which are conditions on the CCDF of and must be satisfied per , the condition above is a simpler condition on an expected value, which doesn’t explicitly refer to the rate .

Let us begin with the following lemma which is the heart of the reverse part.

Lemma 1.

Any achievable rate function (with ) satisfies for :

| (30) |

Proof: Suppose that achievable, by Theorem 1 this implies

| (31) |

Intuitively it is clear that this constraint on the CCDF of implies the exponential factor in (30) is canceled out by the exponential decay of the distribution. For a fixed , define the random variable and substitute . Then the above can be written as a condition on the CDF of , :

| (32) |

Next, this condition on the CDF is translated to a conclusion on the expected value. Since by definition we can write the bound as , i.e. is bounded by the CDF of a uniform random variable . This implies that we can bound , as formulated in the following Lemma:

Lemma 2 (CDF inequality).

Let be a random variable and let the probability function of be bounded by , where is a probability function and is monotonically increasing for all such that , then there exists a random variable such that .

Proof: Since is monotonically increasing it is invertible for values in the region . Let . Then by the well known inverse transform theorem is uniform and therefore by applying we obtain that is distributed according to . Since is monotonically increasing, so is its inverse. Thus by applying to both sides of the inequality we obtain .

Returning to the proof of Lemma 1, let be a random variable that satisfies , then

| (33) |

The condition is required for the integral to exist. Notice that it is possible to prove the result by using integration in parts, however the current proof technique avoids any continuity/integrability assumptions.

Proof of Theorem 4:

Direct part: if (29) holds for some sequence , then there exists an upper bounding sequence such that , therefore by Theorem 2 and (28), we have that is achievable up to

| (34) |

Therefore defining , we have that , and is achievable, and therefore by definition is asymptotically achievable.

Reverse part: Suppose that is asymptotically achievable. Then by definition for any , there exists a sequence of functions such that is achievable. By Lemma 1 this implies (for ):

| (35) |

Defining , then by definition (27) the LHS equals . Choosing we have that , while

| (36) |

and therefore

| (37) |

which satisfies (29).

V-D Conditional probabilities and rate functions

We now apply Theorem 4 to obtain a more intuitive form for the asymptotical rate functions. We assume that the conditions of Theorem 4 hold. For the sake of discussion, let us for the moment replace the limits with equalities, i.e. assume that (i.e. ) and . Then by definition (27) we have:

| (38) |

Denote the summand:

| (39) |

then (38) implies for every . Therefore is a legitimate conditional distribution on . By inverting the relation (39), is written as:

| (40) |

The considerations above remain the same for continuous input, by replacing the sum with an integral. Note that this rate function is not defined for with , however by the definitions of achievability, the values of for such have no consequence, and therefore we may leave them “undefined”. This form (40) provides a general way to obtain rate functions which are achievable up to a small factor. Specifically, since rate functions of the form (40) have by definition , they have (28), and are therefore, achievable up to (Theorem 2). This observation is formalized below.

Lemma 3.

For any conditional distribution , the rate function defined in (40) has and is achievable (with a prior and error probability ) up to .

On the other hand, it is also possible to give a lower bound on the redundancy of this rate function (the reverse of Lemma 3) by using the proof technique from Theorem 4. The following Lemma is proven in Appendix -E:

Lemma 4.

If the rate function defined in (40) satisfies , then this function is achievable (with a prior and error probability ) up to , only if

The fact the bound is negative is not surprising, since this rate function has a non-positive intrinsic redundancy. Using both Lemmas we can bound the redundancy up to an order of . .

The main result of this section states that all rate functions are asymptotically bounded by the form of (40) (for some ). I.e. this is a general way to construct all asymptotically achievable rate functions.

Theorem 5.

A sequence of rate functions is asymptotically achievable (with a sequence of priors ), iff there exist a sequence of functions and a sequence of conditional distributions such that

| (41) |

Proof: Direct part: if (41) holds, then is upper bounded by the rate function (40), which is asymptotically achievable by Lemma 3, and therefore by definition is asymptotically achievable.

Reverse part: suppose is asymptotically achievable, then by Theorem 4, for some and a bounding sequence :

| (42) |

Define

| (43) |

by definition of (27), the denominator is the sum over of the numerator therefore is a conditional distribution. Extracting from (43) and substituting in (42) we have:

| (44) |

Defining we have that

| (45) |

Therefore satisfies the conditions of the theorem.

V-E Manipulating rate functions

Following the results of this and the previous section we can consider various manipulations of rate functions.

-

•

In Section 4 we have seen that when taking the maximum over rate functions, the increase in the intrinsic redundancy is at most .

-

•

Theorem 1 states the achievability conditions separately per . Therefore if we have two rate functions that satisfy the sufficient condition, and we mix them by arbitrarily choosing for each one of the rate functions, the resulting rate function is achievable.

-

•

Suppose that we have sequences of rate functions of the form

(46) By definition this rate function has a non-positive intrinsic redundancy. Then the following rate function:

(47) satisfies (as visible from the first expression in (47)), and has intrinsic redundancy at most (as visible from the second expression in (47)).

These results have analogs in universal source coding. In source coding, given encoders with encoding lengths (for the source sequence ), by defining the universal distribution , one obtains the encoding lengths , which satisfy , i.e. there is a regret of at most compared to the encoders. This fact, that stems from the logarithmic relation between probabilities and encoding lengths is the basis for universal encoding (since the normalized penalty vanishes as ). Similarly in our case, the logarithmic loss in the number of competitors will be the basis for universally competing with multiple models.

V-F Discussion

The definition of asymptotical achievability: As we have noted, the definition of asymptotical achievability is rather loose, by allowing any that translates the rate function to a strictly achievable one. This is done mainly for the sake of the adaptive case, in which, as we shall see, takes various forms, usually non linear. However for the non adaptive case, the definition could have been narrowed by considering only of the linear form with , . All results in this section would be true also under this restricted form of .

VI Constructions for rate functions

In the last two sections we have defined the conditions for achievability of rate functions, but haven’t dealt with the selection of the rate function out of all achievable functions. In this section, we deal with the problem of selecting the rate function. We define constructions for rate functions which have meaningful structure. This is similar to choosing, from all encoders which comply with Kraft inequality, those that compete well with all encoders based on a family of models. We propose two main constructions:

-

1.

ML construction: Rate functions that guarantee achieving the mutual information rate over a family of potential channel distributions.

-

2.

Rate functions that are defined via a certain parameterization or classification of sequences.

These constructions supply reasoning for choosing a specific rate function, give a uniform way to construct several rate functions that seem to be of interest, and will allow us later to prove general claims referring to the construction (rather than specific to a certain rate function).

VI-A Empirical distributions and information measures

We begin with some definitions that will be useful in the sequel. The definitions below are applicable to probability distributions or probability density functions, unless stated otherwise.

VI-A1 Empirical distribution

Given sequences (or equivalently vectors or ordered tuples) , where and are discrete alphabet sets, we define the empirical distribution:

| (48) |

and the conditional empirical distribution

| (49) |

For example yields the empirical distribution of each value in the sequence given the two previous values. The empirical distribution of a sequence denoted is just the zero order empirical distribution.

VI-A2 Empirical probability

Given a probability law , the probability of the sequence is . The empirical probability of the discrete sequence , is the probability of the sequence under the i.i.d. empirical distribution of itself, and denoted . I.e.:

| (50) |

Note that the empirical probability is, in general, not a legitimate probability distribution (but a super-distribution, i.e. it has ), as we shall see below.

Similarly, we define the conditional empirical probability, as the probability of the sequence under the conditional empirical distribution of itself (induced by another sequence). To keep the definitions general we denote the conditioning sequence by (here and in the sequel). This conditioning sequence may include or possibly delayed or modified versions of and . For the purpose of this section it does not matter whether is derived from since all sequences are fixed. The conditional empirical probability means that for each set of symbols in for which a certain symbol in appears, i.e. , we separately measure the empirical probability.

| (51) |

VI-A3 Maximum likelihood probability

In structuring universal schemes, we many times base a universal model on a wide class of probabilistic models [7] (attempting to beat each model in the class). The definition of maximum likelihood probability generalizes the definition of empirical probability above, and provides a useful tool for constructing rate functions.

Denote by a class of distributions over the sequence , with the index (the class not necessarily finite or countable). The maximum likelihood estimate of from is

| (52) |

The maximum likelihood distribution defined by is the distribution defined by the parameter . The maximum likelihood probability of the sequence , is the maximum probability given to by any member in , or can be alternatively written as the probability of under the maximum likelihood distribution:

| (53) |

By definition satisfies . Except in degenerate cases, is not a probability distribution, but a (strict) super-probability. Specifically, if we have two different distributions , then at least at one point (or equivalently ) therefore the sum , since the summand is at least and larger than at at least one point.

The definition extends trivially to the conditional case. Using a class of conditional distributions with respect to the generic sequence , every fixed value of induces a set of probabilities on . We define

| (54) |

Note that the class of conditional distributions may be derived from a class of joint distributions , but this is not necessary.

For discrete sequences, taking to be the class of i.i.d. distributions (defined by the probability for each value of )

| (55) |

we have that the maximum likelihood distribution is the empirical distribution of , i.e.

| (56) |

This is shown below:

| (57) |

Therefore . As a result, the empirical probability of , , equals the maximum likelihood probability of under the i.i.d. model class. Therefore the maximum likelihood probability is a generalization of empirical probability, which is not limited to discrete sequences, and can be applied to continuous sequences, and include time structure.

Another consequence of the fact that for the class of memoryless models is that for any i.i.d. distribution , and every sequence: (since ).

The same result holds for the conditional case, i.e. defining the class as the class of conditionally memoryless models , we have that . To see that, note that the distribution can be written as a product of the distribution of sub-vectors of which have constant (i.e. all indices for which ). Each of these sub-vectors has an independent set of parameters , and maximizing the probability over implies maximizing the probability of each sub-vector separately. As we have seen above, this maximization yields the empirical probability of over the sub-vector. Therefore the maximum is obtained for .

VI-A4 Maximum likelihood, empirical and quazi-empirical entropies

Given a probability distribution , the self information of the element is defined as

| (58) |

and the entropy is the expected value of the self information:

| (59) |

We define the quazi-empirical entropy of a sequence with respect to a model as above expression, where the expected value is replaced by the empirical expectation:

| (60) |

The last expression implies that the quazi-empirical entropy is the normalized self information of the sequence , with the i.i.d. probability .

For discrete sequences, the empirical entropy of a sequence is defined as the entropy of the random variable with the distribution [8, Section II]. The empirical entropy of a sequence is obtained from (59) by replacing the distribution with the empirical distribution :

| (61) |

Equivalently using (50) we may relate to the empirical probability:

| (62) |

This supplies an intuitively appealing way to understand as the normalized self information of the sequence, under its estimated i.i.d. probability . Equivalently we may write the empirical entropy as the quazi-empirical entropy using the empirical distribution . From the relation between the empirical probability and the maximum likelihood probability , we have that

| (63) |

I.e. in extracting the i.i.d. model extracted from (rather than using an arbitrary ) we minimize its quazi-empirical entropy.

As an extension, given a class of models , we may define the maximum likelihood entropy of a sequence as the normalized self information of the sequence under the maximum-likelihood distribution.

| (64) |

As before, all relations extend trivially to the conditional case (conditioned on the generic sequence ), by simply considering each sub-vector of related to a specific value in . I.e.

| (65) |

| (66) |

While the standard chain rule holds for empirical entropies (being entropies of dummy random variables), it does not, in general, hold for entropies defined by maximum likelihood probabilities. Since, in general, we have:

| (67) |

Then

| (68) |

However, equality holds in (67), (68) when the parameters can be separated into a set of parameters controlling and a set controlling . This occurs for example in the discrete memoryless case (where is the empirical entropy), since the single letter distribution can be separated into and , and therefore we have equality in this case.

VI-A5 Empirical mutual information

Similarly to the empirical entropy, the empirical mutual information of two vectors is defined as the mutual information between two random variables with the joint distribution , i.e. whose joint distribution equals the empirical distribution of [8, Section II]. This way of defining the empirical mutual information and empirical entropy as mutual information/entropy of alternative random variables, can be extended to conditional forms. In general, all expressions such as , , , , are interpreted as their respective probabilistic counterparts , , , , where are random variables distributed according to the empirical distribution of the vectors . Equivalently can be defined as a random selection of an element of the vectors i.e. . It is clear from this equivalence that known properties of these values, such as relations between mutual information and entropy, non-negativity, chain rules, etc, are directly translated to relations on their empirical counterparts.

In particular, we can write the empirical mutual information as:

| (69) |

Writing the entropies as the self information under the empirical distribution we have:

| (70) |

Note the similarity to the form (40).

VI-B Maximum likelihood based rate functions

VI-B1 Rationale

In Section V-D we observed that attainable rate functions are asymptotically limited by the form

| (71) |

Let us assume that there is a probabilistic model relating to , and is the true conditional probability resulting from this model. In this case the value is termed the information spectrum or information density [12, (1.5)], and we have that the mutual information between the input and output vectors is

| (72) |

As noted by Han and Verdú [12], for general models (not necessarily i.i.d. or ergodic), the mutual information is not necessarily an achievable rate, and their characterization of channel capacity in this case relies on the “ in probability” of , which means the maximum value such that the probability that tends to as . In other words, achieving a rate requires that in high probability .

Setting the rate function as the normalized information density of a specific probabilistic model, i.e. , is advantageous, especially when this rate function is attained adaptively, since this means that on average, the communication rate would be . For general models, and with the suitable prior , this value may be is larger than the Han-Verdú capacity (which a lower bound in probability of rather than its mean). This occurs due to the use of feedback for rate adaptation. As an example, suppose a non-ergodic binary channel may be in one of two states, which are determined by a single random drawing with equal probabilities – either the output equals the input for , or it is independent of the input. Clearly, no positive rate can be guaranteed on this channel, but if one allows the rate to vary, we may achieve a rate of [bit/use], the time, and thus a rate of [bit/use] on average.

If we attain the normalized information density adaptively, then not only we attain the mutual information on average, but we also attain a rate of at least the liminf in probability of with high probability (the later value becomes the channel capacity if the input distribution is optimized). Another rationale for choosing as the rate function, is that we know from Theorem 5 that asymptotically the rate function is bounded by for some conditional distribution . If one assumes that the channel model truly induces the conditional probability , then the average rate would be which is maximized when . I.e. when the channel induces , any choice other than in the numerator will degrade the achieved rate, while choosing attains the mutual information. So far, we have justified why it makes sense to choose the rate function if the channel is assumed to be known.

However, the main motivation for the individual channel framework is to avoid the probabilistic model. One possible approach is to guarantee a rate close to the information density, for a class of models. Let be a class of models for joint probability of the vectors . We denote by , the marginal and the conditional distribution resulting from . Then a possible rate function is the maximum normalized information density over all models in the family.

| (73) |

Clearly, attaining this rate function guarantees attaining the above properties (the mutual information rate on average and the liminf in high probability) for all channels in the family. The family of distributions may be constrained to have but this is not necessary, and it is sometimes more convenient to avoid this constraint. However we assume that there exist such that and therefore (73) includes maximization over information densities (and possibly other values which are not legitimate information densities, but are still achievable rate functions). In this case the achieving the maximization in the numerator would not necessary yield the “correct” marginal .

To summarize, we have seen that attaining the ML-based rate function (73) is advantageous. In the sequel we analyze the intrinsic redundancy associated with this rate function, and show how it can be achieved adaptively in many cases of interest. However we must note that there is a gap between the justification for this rate function, and what attaining it actually yields. In justifying this rate function we have analyzed the behavior in the case that the relation between and is governed by a probability law from a given class, however the system attaining of (73) will not only guarantee this behavior but guarantees a certain rate and error probability for each pair of sequences (which is more than required to obtain the target of achieving the mutual information rate for all channels in the class, using feedback). Therefore we should not treat this system as the best system attaining the mutual information rate, but rather as a system attaining the of (73) per each pair of sequences, where this on one hand guarantees a certain behavior when are governed by a probability law from the class, but also guarantees some computable rate when a different probability law is applied. This may be compared against a system which attempts to learn by measuring the channel, and may also attain the mutual information rate, but does not give any guarantee on what occurs when another probability law is applied.

VI-B2 Intrinsic redundancy

For finite classes, it is easy to bound the intrinsic redundancy of (73). Since the intrinsic redundancy of is non-positive (see Section V-D), according to Property 2 of the intrinsic redundancy (Section 4), the intrinsic redundancy of is at most . Therefore we may allow the size of the class to increase with , and as long as this increase is sub-exponential, the intrinsic redundancy would tend to with , and therefore of (73) would be asymptotically achievable. However, as we shall see, (73) may be asymptotically achievable even for infinite parametric classes as long as suitable smoothness conditions hold.

The size of the model class yields a coarse estimate for the intrinsic redundancy of (73). A finer analysis is by relating the intrinsic redundancy to the regret of a universal distribution representing the model class . In universal source coding of a family of sources with distributions , one seeks a single distribution , which approximates all distributions in the class, up to a certain loss , termed the “regret”, which represents the difference in encoding lengths when is used, compared to when is used [7]. The minimax regret is the minimum value of the worst case regret over all models and sequences .

It is easy to show [7] that the distribution which achieves the minimax regret is

| (74) |

This distribution is simply a normalization of the super-probability (which we would like to approximate by a probability), and is termed “Normalized Maximum Likelihood” (NML). The regret is determined by the size of the normalization factor

| (75) |

where

| (76) |

The fact is minimax optimal is evident by observing, that is required to be the closet probability that approximates the superprobability (in a logarithmic minimax regret sense), and a normalization by a constant factor, which yields a constant regret is best, since decreasing the factor at any point would necessarily require increasing it at other points, thus increasing the maximum regret. The resulting regret was analyzed by Barron, Rissanen, Yu and others and is known up to negligible terms in many cases of interest. For continuous parametric families, where is a vector of size it was shown by Rissanen [13, Theorem 1] that under certain conditions, there exists having the following regret, determined up to a vanishing factor:

| (77) |

where is the limit of the normalized Fisher information matrix. Since this value does not grow with the main factor in the regret is , which is the penalty associated with the “richness” of the class. Rissanen’s conditions are sometimes limiting. As an example, they do not hold for the class of memoryless sources where is the vector of letter probabilities, at the boundary of , i.e. when one of the element of is or , since the Fisher information is infinite at these points. One solution is to apply the result only to the interior of and account for the boundaries separately. However specifically for the class of memoryless sources, there are explicit expressions for the regret, with the same behavior as determined by (77). See Section VII-F2 in the following for a more detailed discussion of the memoryless and conditional cases. A conclusion from (77) is that the minimax redundancy of the NML, which is optimal, satisfies

| (78) |

Returning to our problem we begin with a general analysis of the intrinsic redundancy of assuming that the conditions for (77) hold. For each separately, we form a distribution on which has a bounded regret with respect to the maximum likelihood probability (one option is the NML). By (77) we have that

| (79) |

where here the asymptotical Fisher information matrix may, in general depend on . Now writing

| (80) |

Since is a probability distribution, the first term has a non-positive intrinsic redundancy (Lemma 3), and therefore by the additivity of intrinsic redundancy, has intrinsic redundancy of .

Note that although the intrinsic redundancy obtained here has a similar form to the minimax regret in universal source coding, the number of parameters will be in most cases larger due to the conditioning on . As an example, to model all i.i.d. sources over alphabet one needs parameters to define the letter distribution ( letter distributions, and a constraint on the sum). To model all memoryless distributions , one needs parameters for each value of therefore parameters.

VI-B3 Universality over a set of probabilistic non-ergodic channels

.

VI-C Variations on the maximum likelihood construction

VI-C1 The doubly maximum likelihood construction

In the maximum-likelihood construction proposed above (73) the rate function depends on the prior . It is sometimes convenient to avoid the specific dependence on by replacing it with the maximum-likelihood probability of the sequence .

Since we assumed there exists such that , we have , therefore we have:

| (81) |