bringhurst 11footnotetext: The European Union and the European Social Fund have provided financial support to the project under the grant agreement no. TÁMOP 4.2.1/B-09/KMR-2010-0003.

Estimation of Claim Numbers in Automobile Insurance

Abstract

The use of bonus-malus systems in compulsory liability automobile insurance is a worldwide applied method for premium pricing. If certain assumptions hold, like the conditional Poisson distribution of the policyholders claim number, then an interesting task is to evaluate the so called claims frequency of the individuals. Here we introduce 3 techniques, two is based on the bonus-malus class, and the third based on claims history. The article is devoted to choose the method, which fits to the frequency parameters the best for certain input parameters. For measuring the goodness-of-fit we will use scores, similar to better known divergence measures. The detailed method is also suitable to compare bonus-malus systems in the sense that how much information they contain about drivers.

Keywords: bonus-malus, claims frequency, Bayesian, scores

*

1 Introduction

1.1 Motivation

In compulsory liability automobile insurance a worldwide applied method is to calculate the premium of the drivers based on a so-called bonus-malus system. This might be vary for different countries, but the idea is similar: policy-holders with bad history should pay more than others without accidents in the past years. Schematically and mathematically described, there is a graph with certain vertices (they called classes), among others an initial vertex, where every new driver begins. After a year without causing any accident he or she jumps up to another class, which has a cheaper premium. Otherwise, in case of causing an accident, the insured person goes downward, to a new class with higher premium, except he or she was already in the worst one.

Also many other factors are taken into consideration when calculating ones premium, like the engine type, purpose of use, habitat, age of the person etc. Here we do not deal with these components, only concentrate on the bonus-malus system. (There are many famous books about bonus-malus systems where we can read about these factors, e.g. [3].) Namely, our aim is to estimate the expected number of accidents for certain drivers. This is usually called the claims frequency of the policyholder. First we review our necessary assumptions, among others about the distribution of claim numbers of a policyholder in one year, and the Markovian property of a random walk in such a system. Section 2 will discuss the basic problem illustrated with Belgian, Brazilian and Hungarian example. Since also a Bayesian approach will be used for estimation of , a general a priori assumption is also needed. Based on this and a gappy information about the driver, the a posteriori expected value of will be calculated.

Giving the possible closest estimation for to the actual one is a crucial task in the insurers life, since the expected value of claims, and which is the most important, the claims payments are forecasted using . Let us note that for evaluating the size of payments on the part of the insurer, the size of the certain property damages has to be approximated, not even the number of them. Here we will not care for it in this article.

1.2 Bonus-malus systems

We suppose the following assumptions, however, it is surely a simplification of the reality:

Assumptions 1.1.

-

is a constant value in time 111The case of the variable in time can be handled using double stochastic processes (Cox processes for instance), i.e. would also be a stochastic process.

-

the random walk on the graph of classes is a homogeneous Markov chain, i.e. the next step depends only on the last state, and independent of time

-

the distribution of a policyholders claim number for a year is Poisson() distributed

Notation 1.2.

For a bonus-malus system consisting of classes, let denote the worst one with the highest premium, the second worst etc., and finally the best premium class which can be achieved by a driver. On the other hand, let be the class of the policy-holder after steps (years).

Using these notations, the Markovian property can be written as . As the process is supposed to be homogeneous, it is correct to simply write instead of . These values specify an stochastic matrix with non-negative elements, namely the transition probability matrix of the random walk on states. Let us denote it by . Now to be more specific, we outline the example of the three different systems, the Belgian, Brazilian and Hungarian.

Example 1.3 (Hungarian system).

In the Hungarian bonus-malus system there are 15 premium classes, namely an initial (), 4 malus () and 10 bonus () classes222We have to be careful here not to confuse the class index of with the time index!. In our above mentioned terminology, we can think of it as . After every claim-free year the policyholder jumps one step up, unless he or she was in , when there is no better class to go. The consequence of every reported damage is 2 classes relapse, and at least 4 damages pulls the driver back to the worst state. Thus the transition probability matrix takes the form of Equation 7.1, see Appendix.

Example 1.4 (Brazilian system).

7 premium classes: . Sometimes written as 7, 6, 5, , 1 classes, e.g. in Jean Lemaire’s article [4]. Transition rules can be found in the cited article.

Example 1.5 (Belgian system).

Here we look at the new Belgian system introduced in 1992, and within this we focus on business-users. The only difference between them and pleasure-users is the initial class. Transition rules can also be found in article [4]. There are 23 premium classes: , , , , , , , (sometimes written as classes).

2 The Bayesian approach

Our realistic problem is the following. When an insured person changes insurance institution, the new company not necessarily gets his or her claim history, only the class where his or her life has to keep going. The new insurer also knows the number of years the policyholder has spent in the liability insurance system. Nevertheless, based on this two information we would like to provide the best possible estimation for the certain persons . First of all we need some new notations.

Notation 2.1.

denotes the event that the investigated policyholder has spent years in the system (more precisely, from the initial class he or she has taken steps), and arrived in class .

Notation 2.2.

is the initial discrete distribution on the graph, which is a row vector of the form

. (Every driver begins in the initial state.)

As a Bayesian approach, suppose that claims frequency is also a random variable, and denote it by . In practice, the gamma mixing distribution seems to be a right choice for that, therefore only this case will be discussed now. For other cases, the calculations can be similarly, though not similarly nicely done.

Notation 2.3.

is the gamma distribution with shape and scale parameters. (Defining the scale parameter precisely, the density function is .)

For some fixed the driver causes Poisson() property damages, i.e. . It is well known that the unconditional distribution will be negative binomial with parameters in our notations. In view of this the a priori parameters can be estimated by a standard momentum or maximum likelihood method.

Remark 2.4.

It is certainly necessary to make hypothesis testing after all, because our assumptions about the mixing distribution might be wrong. In this negative-binomial-rejecting case we have two important alternatives. They are to be found among others in [1], for instance. On the one hand we can try inverse Gaussian, and on the other hand lognormal distribution for mixing.

2.1 Estimation of distribution parameters

In this subsection we give an estimation method to compute the approximate values of and parameters. Let us suppose that the insurance company has claim statistics from the past few years containing policyholders. The th insured person caused accidents by his or her fault over a time period of years, where is not necessarily an integer. According to our assumption, the distribution of is Poisson(), where is a personal time factor and is a Gamma()-distributed random variable. The unconditional distribution of as mentioned above is Negative Binomial, thus its first two moments are

| (2.1) |

| (2.2) |

Now we construct a method of moments estimation, which is not obvious how to build. For example, on the one hand, we can say that , thus . On the other hand, , thus . Generally they do not give the same results, except . Based on our simulations, we used the most accurate method, where the approximation of parameters are the result of the following equations.

| (2.3) |

| (2.4) |

Finally we have to notice the maximum likelihood method as another obvious solution for this parameter estimation. Unfortunately, the likelihood function generally has no maximum, hence this method has been rejected.

2.2 Conditional probabilities

Now we have the a priori parameters, and the information with the initial class . According to Bayes theorem, the conditional density of is

and the estimation for is the a posteriori expected value

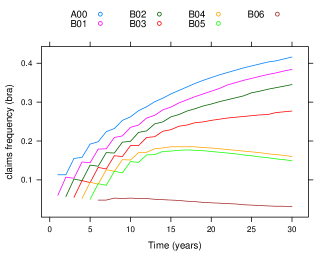

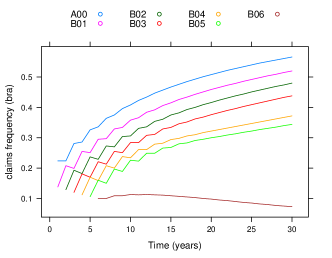

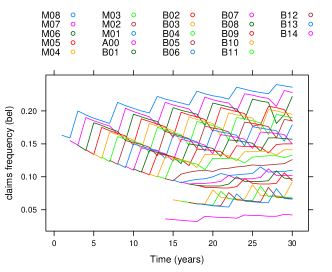

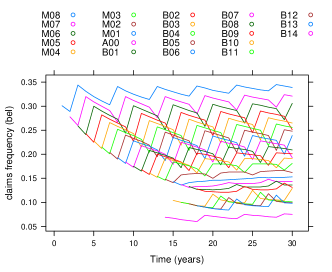

Unfortunately, presents some difficulty, because it only can be calculated pointwise as a function of , powering the transition matrix. If denotes the index of the initial class in the graph, this probability is exactly the element of the matrix, where is the index of class . Using numerical integration it can be solved relatively fast. If we have a glance at figure 2.1, we might see the claim frequency estimations for different countries and different and parameters. For example, the first figure 2.1a was made based on the Brazilian bonus-malus system with parameters and , which indicates a relatively high risk portfolio. There is a line in the chart for each bonus class, which values show the estimated frequencies in function of time. We also see that these functions stationarize in more decades, thus the information about in the system elapsed time of the individual is important.

We will refer to this method as method.1 later.

3 Other methods for frequency estimation

In this section we shortly introduce 2 other (known) possible methods to evaluate policyholders’ claim frequencies. Our assumptions for the distribution of claim numbers certainly still hold.

3.1 Average claim numbers of classes

The following method is probably the simpliest, and we will refer to this as method.2. Let us suppose that statistics from the last year claim numbers are available. Take the average caused claims for every bonus classes, i.e., if last year our portfolio contained 5 policyholders each in class with claims , then the estimation for insured people’s frequencies present year in class is . Although it seems to be too simplified, in some cases it gives the best results in certain circumstances.

3.2 Claim history of individuals

At last the third method is classical, and will be referred as method.3. Here we use the insured persons claim history, i.e., suppose that he or she was insured by our company for years, and the distribution of claim numbers for each year is Poisson(). Let denote the number of aggregate claims caused by this person in his -year-long presence in the system, more precisely, in our field of vision. Then the conditional distribution of is also Poisson with parameter . Let us remark that does not have to be an integer (people often change insurer in the middle of the year in most countries). Based on this, our estimation on a certain is the conditional expected value of the Gamma distributed on condition , i.e., as well known, .

This is also a Bayesian approach as in the case of method.1, but the condition is different. Besides notice that first the and parameters have to be estimated exactly the way we have seen it before in Section 2.1.

4 Comparison using scores

The aim of this section is to make a decision which method gives the possible most accurate estimation for claims frequencies. In this context, we will use the theory of so called scores. For much more detailed information see article [2], as here we will discuss only the most important properties useful for our problem.

Scores are made for measuring the accuracy of probabilistic forecasts, i.e., measuring the goodness-of-fit of our evaluations. Let be a sample space, a -algebra of subsets of and is a family of probability measures on . Let a scoring rule be a function . We work with the expected score , where measure is our estimation and is the real one. Obviously one of the most important properties of this function is the inequality for all . In this case is proper relative to . On the other hand, we call regular relative to class , if it is real valued, except possibly it can be in case of . If these two properties hold, then the associated divergence function is .

Here we mention two main scoring rules, which will be used in sections below for comparing our evaluation methods. Remember that for an individual, the conditional distribution of the number of accidents is Poisson, so in our notations let () be , i.e., the probabilities of certain claim numbers using the estimated as condition. Similarly, () is the same probability, but for the real frequency.

4.1 Brier Score

Sometimes called quadratic score, as the associated Bregman divergence is . The score is defined as

| (4.1) |

Here we use deliberately the unknown probabilities. Although, in practice they are not know, in our simulations we are able to make decisions using them. If we want to calculate the score of our estimation subsequently, we change s to a Dirac-delta depending on the number of claims caused. In other words, if the examined policyholder had claims last year, then the corresponding score is

4.2 Logarithmic Score

The logarithmic score is defined as

| (4.2) |

(In case of caused accidents .) We mention that the associated Bregman divergence is the Kullback-Leibler divergence .

5 Simulation and results

Using R program we simulated portfolios for testing our methods the following way. This can be used for frequency evaluation in practice, if we have the appropriate inputs. First we need a portfolio containing insured people, which is used to estimate the and parameters of the negative binomial distribution. We think of it as the policyholders’ histories available in the insurers database. Taking advantage of the whole claim and bonus-malus history, we have done it exactly the way as described in Section 2.1. In the next step, we generated the history of an policyholder-containing portfolio, assuming that the distribution parameters are unchanged compare to the first portfolio. This might result some bias, but this is the best we can do based on our available data.

After that, we estimated the claim frequency parameters of policyholders separately based on the three estimation methods described above, and compared them to the real parameters using scores. Our aim is to make a decision among the methods, and decide, which would give the best fit results in certain cases. In other words, for certain input parameters, which method gives good-fit estimations in expected value, where the higher score value means the better goodness-of-fit. Before discussing results, we better stop for a few remarks.

As we are interested in the expected values of scores for certain inputs, we will apply a Monte-Carlo-type technique. This means that we generate the above mentioned two portfolios times independently, but in each first ones preserving the and distribution inputs. After that, based on the approximated and , we estimate the parameters of the second portfolios. Each method gives one score number for each simulation, which is the average of scores calculated for individuals. (Of course aggregate scores would be equally appropriate, since it differs only in an multiplier from the average.) At last we take the mean of mean scores, and the higher score resulting method is the better.

Remark 5.1.

For reference we will write and plot the score results also for comparing the real frequencies to the real frequencies, since these scores are not equal to 0, as in the divergence case. In function of year steps, these scores should be constant, contrary to the charts below, where small differences can be observed. The reason is that in the Monte-Carlo simulations we generated also the parameters over and over.

Remark 5.2.

In our simulations input parameters are

-

1.

the number of policyholders in the first portfolio, which is used to estimate the and parameters.

-

2.

the number of policyholders in the second portfolio. This contains individuals, whose parameters have to be evaluated. In practice, there might be an overlap between these two files.

-

3.

Real and distribution parameters.

-

4.

Number of year steps. This means the time elapsed in years, since the certain individual is insured by our company. Note that it implies the knowledge of claims history and bonus classification, thus it is a very important feature, as it affects the goodness-of-fit of our estimation methods.

-

5.

Number of years elapsed before entering our company. This affects method.1 and method.2, because the Markov chain on the bonus classes converges slowly to the stationary distribution.

-

6.

Transition rules of the examined country.

-

7.

Number of simulated portfolios. As we approximate the scores via Monte-Carlo-type technique, it has to be large enough.

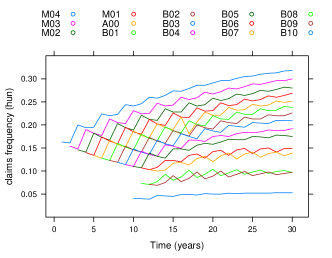

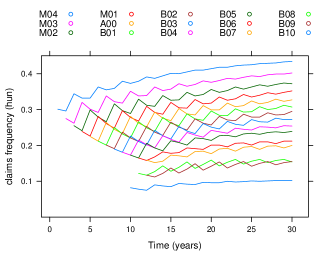

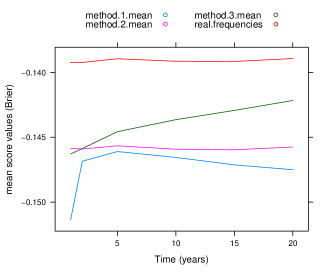

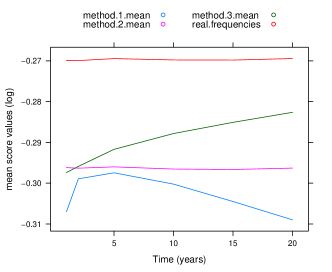

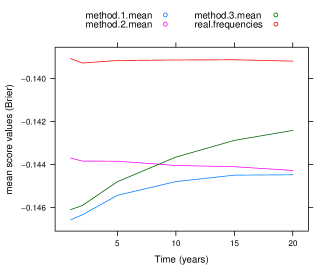

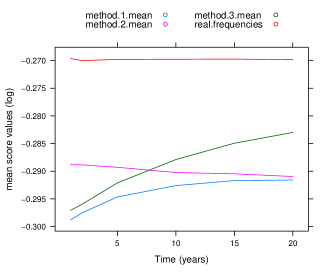

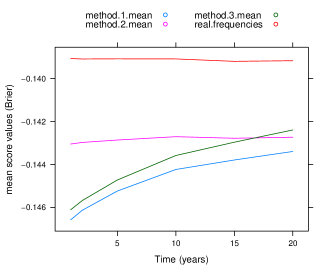

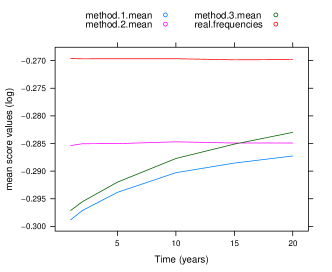

Figure 5.1 shows an example. We simulated 50 times a 80 thousand-people-containing portfolio, estimated and parameters, then estimated the parameters of 20 thousand policyholders. After that we set the results of the three methods against the real frequencies using scores. For every simulation and country we got 2 scores, the Brier score and Log score. The points of the charts are the average scores for this 50 simulations for certain year steps. Certain year steps mean that we generated the so called second portfolios (the current we are analysing) as we had information about policyholders and years back, respectively. Intermediate points are approximated linearly. Note that standard deviation of the sample of Brier scores in the Hungarian example are under , and under in case of Log scores.

Remark 5.3.

In practice, there are different lengths of claim histories available for different policyholders. In function of this length, we can decide that the parameters of a group of insured people will be evaluated using method.2, and the rest using method.3, for example.

Remark 5.4.

Here (5.1) we let the random walks of policyholders on the systems run for 15 years, thus our observations start at that point, i.e., year steps start at that time.

The example clearly shows the differentiation capability of systems containing more bonus-malus classes. In other words, the more classes the system has, the more years needed for method.3 to get the start of method.2. Here the Bayesian type method.1 is the worst in every case, but we shall not forget that in certain circumstances it can be useful. For example, if the claim history is largely deficient.

On the tested parameters the two types of scores gave almost the same results (difference is not significant), what we have been expecting. Same means that if method.x is the best according to Brier scores, then it is the best according to Log scores, too.

6 Conclusions

In this article we introduced the principle of bonus-malus systems, and the necessary assumptions about the distribution of claim numbers of policyholders, inter alia that the number of claims caused in a year by an insured person is conditionally Poisson distributed. The goal was to evaluate these frequency parameters, which is the expected number if claims caused, and we did not deal with the size of them. Since the unconditional distribution is negative binomial, we can simply evaluate the shape and scale parameters based on the insurers claim history from past years. Though the current portfolio might have some different parameters, this file is the best we can use.

We introduced 3 methods for frequency estimation, where one was never used by actuaries to our knowledge, and the other two are known. The main aim of this article was to decide which method is the most appropriate in certain circumstances, i.e., for given parameters. Our decision is made based on scores, which are devoted to measure the bias of two distributions. If method.x gives frequency parameters, and the real ones are , then method.x is the best choice among the other methods, if the average score is greater than in the other cases. The discussion implies a Monte-Carlo-type algorithm, which can be used in practice to make decisions.

At last, but not least, our method includes a technique, which is suitable to compare bonus-malus systems in the following sense. In function of years, the longer the method.2 is better than others, the more informative is the system, as we expect more accurate evaluation of claims frequencies using the past years average claim numbers in different classes, than using other methods. For parameters chosen in example 5.1, in the Brazilian system, method.3 based on claims history becomes the most appropriate in the second year, while in the Hungarian system it needs 7-8, and in the Belgian 16-17 years.

7 Appendix

7.1 shows the transition probability matrix of the Hungarian bonus-malus system.

| (7.1) |

References

- [1] Fishman, George S. (1996) Monte Carlo: Concepts, Algorithms, and Applications. Springer-Verlag, New York.

- [2] Gneiting, T. and Raftery, A. E. (MAR 2007) Strictly Proper Scoring Rules, Prediction, and Estimation. Journal of the American Statistical Association, Volume 102, Issue 477, pp. 359-378.

- [3] Lemaire, J. (1996) Automobile Insurance. Kluwer-Nijhoff Publishing, 2nd Printing, Boston.

- [4] Lemaire, J. (1998) Bonus-Malus Systems: The European and Asian Approach to Merit-Rating. North American Actuarial Journal, 2:1, pp. 26-47.

Name: Miklós Arató

Address: Room D-3-311, Pázmány Péter sétány 1/C, 1117 Budapest, Hungary

E-mail: aratonm@ludens.elte.hu

Name: László Martinek

Address: Room D-3-309, Pázmány Péter sétány 1/C, 1117 Budapest, Hungary

E-mail: martinek@cs.elte.hu