Confidence sets in nonparametric calibration of

exponential Lévy models

Abstract

Confidence intervals and joint confidence sets are constructed for the nonparametric calibration of exponential Lévy models based on prices of European options. To this end, we show joint asymptotic normality in the spectral calibration method for the estimators of the volatility, the drift, the jump intensity and the Lévy density at finitely many points.

Keywords: European option Jump diffusion Confidence sets Asymptotic normality Nonlinear inverse problem

MSC (2010): 60G51 62G15 91G70

JEL Classification: C14 G13

1 Introduction

The unknown future development of financial markets, as faced by participants including investors, traders and companies, can be understood to consist of model risk and “Knightian uncertainty” [12, 21]. The first describes the risk for a given calibrated model and can be evaluated by probabilistic methods, whereas the second incorporates the lack of knowledge on the underlying probability measure and is typically treated by worst case scenarios, for example, by stress testing, which amounts to taking the supremum or infimum over a range of probability measures.

In order to address such questions of robustness it is important to quantify the uncertainty in the underlying probability measure. By the choice of the model, there is a trade–off between the calibration error and the misspecification of the model. Both types of uncertainty are unavoidable but within a model the calibration error is traceable, at least with assumptions on the errors. In general, large models reduce misspecification, which motivates our choice for a rich nonparametric model. We then assess the calibration error by constructing confidence sets.

More precisely, we consider the nonparametric calibration when the risk–neutral price of a stock follows an exponential Lévy model

| (1.1) |

In this paper we restrict ourselves to Lévy processes with finite activity. Exponential Lévy models generalize the Black–Scholes model by accounting in addition to volatility and drift for jumps in the price process. They are capable of reproducing not only a volatility smile or skew but also the effect that the smile or skew is more pronounced for shorter maturities. A thorough discussion of this model is given in the monograph by Cont and Tankov [8]. They introduced in [9, 10] a nonparametric calibration method for this model based on prices of European call and put options, in which a least squares approach is penalized by relative entropy. Regularizing by a spectral cut–off, Belomestny and Reiß [2] used a different approach to the same estimation problem. Their method achieves the minimax rates of convergence, meaning that their estimators optimize the rate of convergence for the least favorable constellation in a given class of Lévy processes. We show asymptotic normality and construct confidence sets and intervals for their estimation procedure. Methods similar to theirs were also applied by Belomestny [1] to estimate the fractional order of regular Lévy processes of exponential type, by Belomestny and Schoenmakers [4] to calibrate a Libor model and by Trabs [30] to estimate self–decomposable Lévy processes.

Confidence sets measure how reliable the estimation is. This is particularly important if the calibrated model is to be used for pricing and hedging. For a recent review on pricing and hedging in exponential Lévy models see [29] and the references therein. For the influence of model uncertainty on the pricing see [7].

Nonparametric confidence intervals and sets for Lévy triplets have not been studied with the notable exception of the work by Figueroa–López [15]. The work is more general in the sense that beyond pointwise confidence intervals also confidence bands are constructed. On the other hand, the method is based on direct high–frequency observations so that the statistical problem of estimating the Lévy density is easier than in our set–up. We observe the Lévy process only indirectly since our method is based on option prices. This indirect observation scheme does not correspond to direct observations at high frequency but at low frequency, where the time between observations is fixed and does not tend to zero. An underlying deconvolution problem has to be solved and the calibration is a nonlinear inverse problem, which is mildly ill–posed for volatility zero and severely ill–posed for positive volatility.

Confidence intervals and sets in nonparametric problems are a subtle issue. Usually some smoothness assumptions on the unknown function are imposed and then the size of a confidence set, or more precisely, the rate at which the confidence set becomes smaller depends on the assumed smoothness. A confidence set adjusting to an unknown smoothness of the estimated function is called adaptive if the confidence set becomes smaller at the same rate as if the smoothness were known. In the nonparametric problem of density estimation Low [22] proved that adaptive confidence intervals do not exist. Whether in our setting adaptive confidence intervals for the volatility, the drift and the jump intensity exist is an open question. We show asymptotic normality for the parametric estimators of the volatility, the drift and the jump intensity. We also proof asymptotic normality for the pointwise estimators of the Lévy density. The joint asymptotic distribution of these estimators is derived in both the mildly and the severely ill–posed case. This is used to construct confidence intervals and joint confidence sets. The asymptotic normality results are based on undersmoothing and on a linearization of the stochastic errors.

2 The model and the estimators

2.1 The model

For an underlying , a strike price and a maturity , we denote by and the prices of European call and put options which are determined by the pricing formula. We suppose that the risk–neutral price of the stock follows the exponential Lévy model (1.1) with respect to an equivalent martingale measure and that is a finite activity Lévy process. denotes the present value of the stock and the riskless interest rate. We fix a maturity and assume that the observed option prices correspond to different strike prices and are given by the value of the pricing formula corrupted by noise as motivated by Renault [25]:

| (2.1) |

with and random variables . The minimax result in [2] is shown for general errors which are independent centered random variables with and . The noise levels can be estimated nonparametrically, for example, with the method by Fan and Yao [14]. As European put and call prices are linked by the put–call parity the observations may alternatively be given by put prices in (2.1). We transform the observations to a regression problem on the function

where denotes the log–forward moneyness. The regression model may then be written as

| (2.2) |

where .

2.2 The estimation method

We call the volatility of a Lévy process , the drift and the jump intensity . We assume that the jump distribution is absolutely continuous and call its density . We denote by the corresponding exponentially weighted jump density. The aim is to estimate the Lévy triplet . In the remainder of this section we present the spectral calibration method of Belomestny and Reiß [2]. The method is based on an option pricing formula by Carr and Madan [6], which relates the Fourier transform to the characteristic function . That is why, we define

| (2.3) |

where the first equality is given by the above mentioned pricing formula and the second by the Lévy–Khintchine representation. This equation links the observations of to the Lévy triplet that we want to estimate. Let be an approximation on the true function . For example, can be obtained by linear interpolation of the data (2.2). We further define the empirical counterpart of by

where the trimmed logarithm is given by

The logarithms are taken in such a way that and are continuous functions with and is specified in [2]. Considering (2.3) as a quadratic polynomial in disturbed by motivates the following definition of the estimators for a cut–off value :

| (2.4) | ||||

| (2.5) | ||||

| (2.6) |

where the weight functions , and satisfy

| (2.7) |

The estimator for is defined by a smoothed inverse Fourier transform of the remainder

| (2.8) |

The choice of the weight functions is discussed in [28], where also possible weight functions are given. The weight functions for all can be obtained from , , and by rescaling:

Since only the symmetric part of , and the antisymmetric part of matter. The antisymmetric part of contributes a purely imaginary part to . Without loss of generality we will always assume , , to be symmetric and to be antisymmetric. We further assume that the support of , , and is contained in . We define the estimation error and likewise for the other estimators. We will also use the notation . The estimation error can be decomposed as

| (2.9) |

The first term is the approximation error and decreases in the cut–off value due to the decay of . The second is the stochastic error and increases in by the growth of . For growing sample size the term becomes smaller so that the stochastic error decays even if we let as . For the term grows polynomial in so that we can let tend polynomially to infinity, whereas for it grows exponentially in and we can let tend only logarithmically to infinity. This is the reason for the polynomial and logarithmic convergence rates for and for , respectively. For fixed sample size the cut–off value is the crucial tuning parameter in this method and allows a trade–off between the error terms. The influence of the cut–off value is analogous to the influence of the bandwidth on kernel estimators, more precisely corresponds to . The other estimation errors allow similar decompositions as in (2.9).

We shall analyze the asymptotic properties of the stochastic errors in depth. To bound the approximation errors some smoothness assumption is necessary. We assume that the Lévy triplet belongs to a smoothness class with and specified in [2, Definition 4.1]. The assumption includes a smoothness assumption of order on leading to a decay of . To profit from this decay when bounding the approximation error, we assume the weight functions to be of order , this means

| (2.10) |

2.3 Discussion of the model

In this paper we restrict to the nonparametric calibration of finite activity Lévy processes. The nonlinear penalized least–squares method by Cont and Tankov [9] and the spectral calibration method by Belomestny and Reiß [2] are mainly considered for finite activity Lévy processes. Trabs [30] extended the spectral calibration method to self–decomposable Lévy processes, which have infinite activity and Blumenthal–Getoor index zero. Extensions to higher Blumenthal–Getoor indexes are of interest but it might be difficult to distinguish statistically between volatility and small jumps. We define the measure , where denotes the Dirac measure at zero. Its structure in a neighborhood of zero is very natural since it is most useful in characterizing weak convergence of the distribution of the Lévy process in view of Theorem VII.2.9 and Remark VII.2.10 in Jacod and Shiryaev [18]. The measure determines the variance of a Lévy process and is relevant for calculating the in quadratic hedging as noted in [24]. Volatility and small jumps both contribute to the mass assigned by to a neighborhood of zero. One possibility to separate the jumps and the volatility is to assume finite jump activity. While other assumptions are possible some restriction is necessary here. Indeed, Neumann and Reiß [24] point out in their Remark 3.2 that without further restrictions the volatility cannot be estimated consistently. In Section 2.3 of [27] the spectral calibration method designed for finite intensity processes is applied to some infinite activity Lévy processes, namely to symmetric stable Lévy processes. This suggests that in the misspecified case of infinite activity has to be interpreted as the joint quantity of and the small jumps or, more precisely, as the mass assigned by to a neighborhood of zero with size proportional to . In this case should be consider only outside this neighborhood as an estimator for .

3 Asymptotic normality

3.1 The main results

The aim of this section is to establish asymptotic normality results for the estimators. We would like to state that the appropriately scaled errors of the estimators converge to normal random variables. The starting point of our error analysis is the decomposition (2.9) into the approximation error and the stochastic error. The approximation error is deterministic and only the stochastic error can be expected to converge with appropriate scaling to a normal random variable. It is common practice to resolve this problem by undersmoothing, which means that the tuning parameter is chosen such that the approximation error becomes asymptotically negligible.

To simplify the asymptotic analysis of the stochastic errors, we do not work with the regression model (2.2) but with the Gaussian white noise model. This is an idealized observation scheme, where the terms are easier to analyze. At the same time asymptotic results may be transferred to the regression model. The Gaussian white noise model is given by

| (3.1) |

where is a two–sided Brownian motion, and . In the case of equidistant design the precise connection to the regression model (2.2) is given by and , where and are the minimal and maximal design points and where we assume that the range of observations grows slower than such that as . General designs for a c.d.f. with p.d.f. can be treated by the Gaussian white noise model , where . Transferring asymptotic results from the Gaussian white noise model to the regression model is formally justified by the concept of asymptotic equivalence, which applies in particular to lower bounds and confidence statements. Brown and Low [5] show that the regression model (2.2) with Gaussian errors is asymptotically equivalent to the Gaussian white noise model (3.1). For non–Gaussian errors we refer to Grama and Nussbaum [17]. Their main assumption on the errors is slightly more than Hellinger differentiability, which is a smoothness assumption on the distributions of the errors.

The simplified approach of using the Gaussian white noise model to construct confidence sets is well suited to derive asymptotic normality and to determine the quantitative expression of the asymptotic variance. Nevertheless, it is an idealized model and the ultimate interest is in the regression model. Obtaining results directly in the regression model would probably lead to less assumptions than combining the Gaussian white noise model with an asymptotic equivalence result. Details of the application of the asymptotic equivalence result can be found at the beginning of Section 6.

The stochastic errors involve the term , which is a difference of two logarithms. In the definition of , we take and thus define the empirical version of directly without constructing in an intermediate step an empirical version of . For and it holds . That yields

where , see [2, (6.3)]. We define a linearization of the logarithm and the remainder term by

| (3.2) | ||||

| (3.3) |

To ensure continuity of the Gaussian process we assume that there is a such that . In [26] it is shown that on this assumption satisfies the Kolmogorov–Chentsov criterion [20, p. 57] and thus has a continuous version. In the sequel we are always working with this version.

The remainder term in (3.3) is small when the argument of the logarithm is close to one, that is when is small. Since we are integrating over the unit interval in (2.9) we want to be uniformly small. We shall use the notation as synonymously with the Landau notation as , meaning that there exist and such that for all .

Proposition 1.

For all holds

as .

This proposition is proved in Section 6 by metric entropy arguments. In the following theorems we control the supremum of and thus the remainder term by the conditions and for and for , respectively. Then the asymptotic distribution of the stochastic errors is governed by the linearized stochastic errors and the remainder term is asymptotically negligible. In the case the stronger condition is assumed, which is needed for the stochastic errors to converge to zero.

For the approximation error to be asymptotically negligible we need to undersmooth by choosing the cut–off value large enough such that in the case of volatility zero and by in the case of positive volatility, where is the smoothness assumed on the exponentially weighted jump measure .

In the results on asymptotic normality we will also include the estimator of the jump density at zero. This only makes sense by our smoothness assumption on since there is no way of detecting jumps of height zero. The asymptotic distribution of is not determined by the weight function but by the effective weight function

The first theorem states the joint asymptotic normality result for the mildly ill–posed case of volatility zero.

Theorem 1.

Let . Let be continuous at and let . For let be distinct and let be independent Brownian motions. If and as , then

as , where .

Remark.

The theorem is formulated in terms of the exponentially weighted jump density . By the continuous mapping theorem results on can be reformulated in terms of by multiplying with in the respective lines.

Proof.

We write , and similarly as in (2.9) for :

| (3.4) | ||||

| (3.5) | ||||

| (3.6) |

In (3.4) we can substitute using (2.9) and obtain two error terms involving and two error terms involving . By similar substitutions in (3.5) and (3.6) we see that all error terms either involve or , which we will call approximation errors and stochastic errors, respectively.

The undersmoothing is equivalent to . The approximation error of decays by (6.27) below as and thus is asymptotically negligible. The approximation errors of , of and of can be bounded similarly as done in (6.28), (6.29) and (6.30) below and are asymptotically negligible, too. Since converges with a faster rate than and converges with a faster rate than , the error vanishes asymptotically in (3.4) and in (3.5) as well as is asymptotically negligible in (3.5). For we can apply the Riemann–Lebesgue lemma to the second, the third and the fourth error term in (3.6) and we see that they are of order . For due to the symmetry of the third term vanishes asymptotically but the second and the fourth term do not. The error terms of we have to consider are in the case

and in the case

By assumption (2.10) on the order of the weight functions, , , and are continuous and bounded, especially they are Riemann–integrable and in . As the main technical step, Lemma 1 shows the convergence of the linearized stochastic errors. The remainder terms are asymptotically negligible by Lemma 6.

Next we consider the case . Let be in and . We set

| (3.7) |

and define by the real–valued random variables and . By Lemma 3 below

| (3.12) |

as , where and are independent standard normal random variables.

The following theorem treats the stochastic errors in the case of positive volatility. Since the theorem contains no statement on the approximation errors, the condition (2.10) on the order of the weight functions may be omitted.

Theorem 2.

Let and . Assume for the cut–off value and as . Let be Riemann–integrable, in and continuous at one. Then for

as , where

Proof.

The main technical step is provided by Lemma 4, which treats the convergence of the linearized stochastic errors. The remainder terms are asymptotically negligible by Lemma 5. To see the first line we set , and in Lemma 4 and in Lemma 5. The second and third line follow analogously. In order to derive the last line we observe

and apply Lemma 4 with , , and , . The remainder term vanishes by setting in Lemma 5.

The assumption restricts to the interval . The condition is especially fulfilled if for any . For the estimation it suffices to know some upper bound of . The theorem shows that regardless whether one undersmoothes or not the stochastic errors converge with appropriate scaling to normal random variables. For the statement on asymptotic normality we have to undersmooth and further knowledge on the volatility is necessary.

In many situations the volatility is known or can be estimated easily. The volatility is preserved under a change to an equivalent measure so that it is the same for the risk–neutral and the real–world measure even if the price process is only assumed to be a semimartingale. Then one of the methods for volatility estimation from high frequency data in the presence of jumps can be used to estimate the volatility. Cont and Tankov [9] also need to fix the volatility for their calibration method of exponential Lévy models in advance since their method chooses only among measures of Lévy processes equivalent to a prior measure. They suggest using historical data or an earlier calibrated model for the choice of the prior and thus also of the volatility. In the following we will assume either that the volatility is known or that we have a sufficiently good estimator of the volatility. To control the remainder term we choose such that as . We also assume the undersmoothing condition as . A smoothness parameter is implicitly assumed so that both conditions can be satisfied simultaneously. A possible choice of is

| (3.13) |

where . Then it holds

as . Especially the term diverges for and converges to zero for so that both conditions on are fulfilled. Next we state the joint asymptotic normality result for the severely ill–posed case of positive volatility.

Theorem 3.

Let and . Let the cut–off value be chosen such that and as . Then

as , where , and is given by (3.7).

Proof.

The undersmoothing condition yields for the cut–off value and thus the approximation error of vanishes. A similar reasoning applies to the approximation errors of the other estimators. Since converges with a faster rate than and with a faster rate than the leading stochastic error terms are given in Theorem 2 and the convergence of the first three lines follows by this theorem. For all stochastic errors in (3.6) are negligible except the first one. We obtain the convergence in the last line by Theorem 2. We observe that , since is symmetric. For the relevant stochastic error terms are

We apply Lemma 4 with , and to this term. The remainder term is asymptotically negligible by Lemma 5. This shows the convergence in the next to last line.

3.2 Discussion of the results

Theorems 1 and 3 include the asymptotic distribution of , which may be used for testing the hypotheses , see Section 6.2 in [27]. If is known, we can set . Then the statements of the theorems hold with constant to zero. The estimation method can give negative values for , and . By a postprocessing step the estimated values can be corrected to be non–negative.

In Theorem 1 the noise level enters only locally into the asymptotic variance, whereas in Theorems 2 and 3 the asymptotic variance depends on the –norm of through the factor . In fact for it is possible to estimate and directly from local properties of the option function at as remarked in [2]. This local dependence on the noise level resembles some similarity to deconvolution, for instance, to the case of ordinary smooth error densities [13] or to the case of symmetric stable error densities whose characteristic function decreases slower than the characteristic function of the Cauchy distribution [31]. In both cases the density of the observations enters locally into the asymptotic variance. For the weight functions the local and global dependence is vice versa. In Theorem 1 the weight functions , , , and enter globally into the asymptotic variance while in Theorems 2 and 3 only the values of the weight functions at their endpoints appear in the asymptotic variance.

The asymptotic variance depends on the maturity. For positive volatility this dependence is through in (3.7). The martingale condition is equivalent to the equation , especially it holds that with equality if and only if that is in the Black–Scholes case. In the case of positive volatility the asymptotic variance grows exponentially as if the jump intensity is positive and it grows quadratic as .

For , , , Theorem 2 describes the asymptotic distribution of the leading stochastic error term of , , and , , i.e., the other stochastic error terms are of smaller order. Theorem 3 describes the asymptotic distribution of . Both theorems are for the case of positive volatility, where the noise in the frequency domain is exponentially heteroscedastic, so that the highest frequency, that is the cut–off frequency , dominates the stochastic error. Then this cut–off frequency can be seen in the asymptotic distribution of through the oscillating process . The variances in Theorems 2 and 3 converge by (3.12) and by the definition of . If one only considers the stochastic errors of , , and , then the covariances converge, too. But for the covariance of the stochastic errors of and of does not converge. The same holds for the covariance of the stochastic errors of and as well as and . The phenomenon that the covariances do not convergence comes from the fact that the stochastic error centers more and more at the cut–off frequency. The sequence of cut–off values has a crucial influence on the covariance. For estimators of the generalized distribution function of the Lévy density this is likely to lead to a similar dependence on the sequence of cut–off values as observed in [32] for deconvolution with supersmooth errors.

4 Applications

4.1 Construction of confidence intervals and confidence sets

For we define confidence intervals

| (4.5) |

where , denotes the –quantile of the standard normal distribution and

with . We fix some arbitrarily slowly decreasing function with as . We denote by the subset of Lévy triplets in that satisfy in addition

| (4.6) |

The additional conditions are used to extend the convergence in the theorems to be uniform over all Lévy triplets in , see Theorem 5.1 in [27], and to obtain honest confidence sets meaning that the level is achieved uniformly over a class of Lévy triplets.

Corollary.

If the infimum in the corollary is omitted, then the statement holds for all Lévy triplets in and is a direct consequence of Theorem 1. The same holds for the other confidence intervals and sets, where in the case of positive volatility the statements hold for the corresponding Lévy triplets in and follow from Theorem 3.

Remark.

To consider the two parameters and jointly, we define the confidence set , where denotes the –quantile of the chi–squared distribution with two degrees of freedom. Then it holds

For we define confidence intervals

| (4.11) |

where ,

and denotes the –quantile of the standard normal distribution. We assume that the weight functions are chosen such that , , , . We note that instead of estimating nonparametrically it suffices for positive volatility to estimate the –norm of . For example, in the case of equidistant design we can first estimate with the standard Nadaraya–Watson estimator for regression and then estimate the –norm of from the sum of the squared residuals, which leads to a consistent estimator as shown by Dette and Neumeyer [11].

Corollary.

For the pair a uniform confidence set may be obtained similarly as in the case . Since for the covariance of and and the covariance of and do not converge, confidence sets for and have to be constructed differently. Let us illustrate how to proceed in this case by constructing a confidence set for , . By Theorem 3 the convergence

holds for . We define

and observe that the components of are bounded for all for which the absolute value of the determinant is bounded from below by some , i.e., we have . For such

holds for . We apply the additive version of Slutsky’s lemma together with the convergence (3.12) of the appropriately scaled random variables and . In view of the definition of in (3.7) we observe that is a consistent estimator of and we apply the multiplicative version of Slutsky’s lemma, which then leads to

for such that . We define

where denotes the –quantile of the chi–squared distribution with two degrees of freedom. Then

holds for all .

4.2 A numerical example

We consider the Merton jump diffusion model [23], where the jump density is specified by

with parameters , , and where is determined by the martingale condition. We simulate data with the parameters , , , , which imply . The interest rate is taken to be . We observe prices of European options with maturity . The strike prices are obtained from sampling the data points from a centered normal distribution with variance , so that more strike prices are sampled at the money than in or out of the money. The observation error is chosen to be a centered normal distribution with variance , . Belomestny and Reiß [3] describe the implementation of the estimation method in detail.

We interpolate the corresponding European call prices linearly. The weight functions are chosen as in [28] with smoothness parameter . In the simulations the confidence intervals based on the asymptotic distribution turn out to be to conservative. Such confidence intervals would be based on the asymptotic variance of the linearized stochastic errors that is the stochastic errors, where the linearization (3.2) is used. Instead of taking the asymptotic variance of the linearized stochastic errors, we derive confidence intervals from the finite sample variance (6.14) of the linearized stochastic errors. In the finite sample variance we substitute , , , and by their respective estimators. This yields feasible confidence intervals. We estimate with the oracle choice of the cut–off values and perform 1000 Monte Carlo iterations. The coverage probabilities of confidence intervals for , and are approximately 0.98, 0.95 and 0.91, respectively. We see that the that the coverage probabilities are close to the prescribed confidence level.

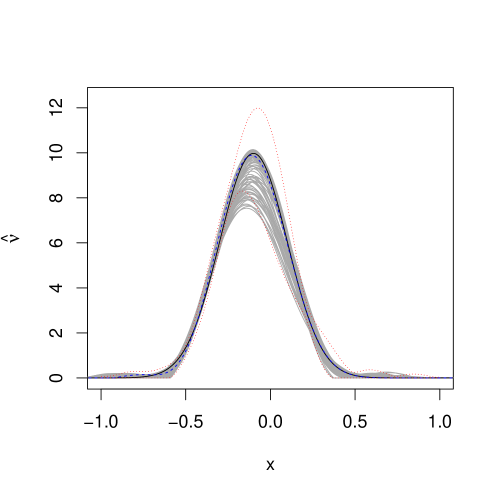

Figure 1 illustrates the true and an estimated Lévy density, and the pointwise confidence intervals based on the finite sample variance. Additional 100 estimated Lévy densities are plotted. At zero there is a negative bias since the peak is smoothed out. The precise construction of the confidence intervals and more calibration results are contained in [28].

5 Conclusion

We have shown asymptotic normality in a nonparametric calibration method for exponential Lévy models. These results were used to derive confidence intervals and confidence sets. We have seen in a numerical example that confidence intervals based on finite sample variance perform well in terms of coverage probabilities. The confidence intervals extend the calibration method beyond a pure point estimate and enable an assessment of the calibration error. Although parametric models might be fitted better, the parametric approach is always exposed to the risk of model misspecification and the obtained confidence results should be used for a goodness–of–fit test.

The estimation method and the asymptotic normality results may be adapted to other models as long as there is an equation relating the option function to the characteristic function and the parameters of interest appear in the characteristic function. The constructed confidence intervals and sets may be used to quantify the errors in pricing, hedging and risk management.

6 Auxiliary results and remaining proofs

We will now state the conditions more precisely on which the regression model (2.2) and the Gaussian white noise model (3.1) are equivalent. As a simplification we assume that the observations in the regression model are equidistant with mesh size . We restrict the Gaussian white noise model to a sequence of growing intervals . We suppose to be an absolutely continuous function and to hold for some . The functions are both uniformly bounded as well as uniformly Lipschitz , where we used Proposition 2.1 in [2] and . These properties of are used to apply Corollary 4.2 in [5].

6.1 Proof of Proposition 1

First we define . Since it suffices to consider suprema of the absolute value over positive index sets. We assumed that there is an such that . It is shown in [26] that there exists a number such that for all with . Denote by the covering number, that is the minimum number of closed balls of radius in the metric with centers in that cover . We define and . A ball of radius in the metric covers an interval of length . Thus, it holds

The radius of the smallest ball with center in that contains is with respect to the metric . There exists such that for all . For large enough such that we have the entropy bound

| (6.1) | ||||

| here we substitute , | ||||

| (6.2) | ||||

This integral is solved by

where . For all the estimate holds. For each this yields such that for all

Thus, (6.2) can be bounded by

as . Consequently is an asymptotic upper bound of the entropy integral (6.1). We apply Dudley’s theorem [19, p. 219] to the real part of . For all this yields a continuous version of with

| (6.3) |

as . Since and are both continuous they are indistinguishable and (6.3) holds for likewise. We obtain analogously for all

as . We estimate from above for all

| (6.4) |

as . This completes the proof for the case . For we observe

By the previous considerations the growth of the first part can be bounded by

For the second part we note that as in (6.1) we have

and thus the entropy does not depend on . For the process does not contribute a logarithmic factor and it holds

as .

6.2 The linearized stochastic errors

The linearized stochastic errors are of the form , where with are Riemann–integrable function in . Next we will show that these are jointly normal distributed. Almost surely is continuous. Thus, almost surely the are Riemann–integrable and almost surely

as . Let be such that for all . For each the sums are joint, centered normal random variables. For the covariance matrix converges by the dominated convergence theorem with the dominating function , where is an integrable random variable by Proposition 1. Thus, the characteristic function converges pointwise. By Lévy’s continuity theorem this shows that the sums convergence jointly in distribution to normal random variables. So are jointly normal distributed.

For a fixed cut–off value the linearized stochastic errors are jointly normal distributed. So the natural question is whether the appropriately scaled covariance matrix converges for .

Let be Riemann–integrable functions in . It holds

where

| (6.5) |

and . We define analogously

| (6.6) |

and . We extend and by zero outside the interval .

Since we may apply Fubini’s theorem and then we apply the Itô isometry to obtain

| (6.7) |

To separate real and imaginary part we will also need

| (6.8) |

Lemma 1.

Let . For take and to be Riemann–integrable functions in . Let be continuous at the points , and let . Let be Brownian motions. If let and otherwise let the Brownian motions be distinct. Let the set consist of independent Brownian motions. Then

converge jointly in distribution to

as .

Proof.

We will first consider the case . We have seen that

| where and are defined as in (6.5) and (6.6), respectively, and , | ||||

| We notice that implies and we obtain by the Plancherel identity | ||||

| (6.9) | ||||

since the support of is . Because we are only interested in the limit we may assume . By the Riemann–Lebesgue lemma tends to zero as . The factor converges for each to as and the functions are dominated by a constant independent of . In order to apply dominated convergence it suffices that the second factor is dominated by a constant independent of and converges stochastically with respect to the Lebesgue measure on . We have

By assumption lies in and so does . A dominating constant is . It holds

| (6.10) |

is the multiple of what is called approximate identity or nascent delta function. The basic theorem on approximate identities states that converges to in as for . Thus,

as [16, p. 28] and in particular stochastically. If , then there is a neighborhood of where converges uniformly to zero. The term converges to zero almost surely and in particular stochastically. Therefore, converges to stochastically with respect to the Lebesgue measure on .

We obtain under the limit by the dominated convergence theorem

| (6.11) |

Without taking the complex conjugate in (6.9) we obtain

The same argumentation as before leads to

| (6.12) |

We combine (6.11) and (6.12) to obtain

From (6.11) and (6.12) it also follows that the covariance between real and imaginary part vanishes asymptotically.

In the case we have to show that the covariance vanishes asymptotically. Without loss of generality we assume . We define . Then .

By the Plancherel identity and by the dominated convergence theorem

in for and especially the norms converge. From the assumption follows that . By the Cauchy–Schwarz inequality

A similar calculation shows that the integral over converges to zero and consequently

The same way follows

The are centered normal random variables and their covariance matrix converges to the covariance matrix of the claimed limit. Thus, the characteristic function converges pointwise. By Lévy’s continuity theorem this shows the convergence in distribution.

Lemma 2.

Let and . Let be Riemann–integrable and let there be a constant such that for all . Let there be such that the condition

| (6.13) |

and the corresponding condition for and hold. Then

Remark.

Obviously is the only possible definition. Thus, describes the dependence of on at one.

Proof.

We notice that (6.7) applies to the complex–valued functions and yields for and with the definitions (6.5) and (6.6) of and , respectively, and with

| (6.14) |

For all we have

| (6.15) |

For the product of two such sequences we obtain for all

| (6.16) |

Likewise

| (6.17) |

holds. We scale the integral in (6.14) appropriately:

| (6.18) | ||||

| (6.19) | ||||

| We recall that in the Gaussian white noise model we assumed to be in . Since is bounded in independently of for and since the difference between (6.17) and (6.16) is zero, only the integral over contributes to the limit. For all the limit equals | ||||

| (6.20) | ||||

which can be seen the following way. is continuous and we have for all . gets arbitrarily close to by choosing small enough. By (6.13), tends to and tends to for tending to zero. By choosing large the factor gets close to minus one for all . Thus, for small and large the term is close to for all .

Lemma 3.

Let , and . For let be continuous at one, Riemann–integrable and in . Then

converge jointly in distribution to

as , where and are independent standard normal random variables.

Proof.

The proof relies on Lemma 2. We define and . Further we set and . Then we apply Lemma 2. Condition (6.13) is satisfied since and are continuous at one and since

where for . We note that is real. By Lemma 2 the covariances converge to the covariances of the claimed limit. The convergence in distribution follows by Lévy’s continuity theorem.

Lemma 4.

Let and . Take to be Riemann–integrable, in and continuous at one. Let and denote by . Then

as .

6.3 The remainder term

In this section, we show that the contribution of the remainder term to the estimation vanishes asymptotically. We recall that the remainder term depends on the Lévy triplet.

Lemma 5.

Let . Let be Riemann–integrable and let there be a constant such that for all . If as , then for all Lévy triplets with

Proof.

By the identity , where , we have to show that for

| (6.23) |

converges in probability to zero. For holds as . We define by for and . There are and such that for all . We may assume that . If the logarithm in the definition of is replaced by the trimmed logarithm with some then remains unchanged for . Thus, the statement holds uniformly for all with .

By Proposition 1 we have . Let be given. Eventually we have

Except on a set with probability less than we have eventually

| (6.24) |

Hence (6.23) converges in probability to zero if (6.24) converges in probability to zero. The convergence

holds even in since

| (6.25) | ||||

| (6.26) | ||||

| for this converges to zero and for we further calculate, | ||||

as . Thus, (6.23) converges in probability to zero.

Lemma 6.

Let be Riemann–integrable and let there be a constant such that for all . If and as , then for all Lévy triplets with

as .

6.4 The approximation errors

The approximation error can be controlled as in [2] using the order conditions (2.10) on the weight functions. The Lévy triplet was assumed to be contained in , especially is s–times weakly differentiable and we have , .

We use and the Plancherel identity to bound the approximation error by

| (6.27) |

Analogously we obtain

| (6.28) | ||||

| (6.29) |

The last error term in (3.6) can be bounded by

| (6.30) |

References

- Belomestny [2010] Belomestny, D. (2010). Spectral estimation of the fractional order of a Lévy process. Ann. Statist. 38(1), 317–351.

- Belomestny and Reiß [2006a] Belomestny, D. and M. Reiß(2006a). Spectral calibration of exponential Lévy models. Finance and Stochastics 10(4), 449–474.

- Belomestny and Reiß [2006b] Belomestny, D. and M. Reiß(2006b). Spectral calibration of exponential Lévy Models [2]. SFB 649 Discussion Paper 2006-035, Sonderforschungsbereich 649, Humboldt–Universität zu Berlin, Germany. Available at http://sfb649.wiwi.hu-berlin.de/papers/pdf/SFB649DP2006-035.pdf.

- Belomestny and Schoenmakers [2011] Belomestny, D. and J. Schoenmakers (2011). A jump-diffusion Libor model and its robust calibration. Quant. Finance 11(4), 529–546.

- Brown and Low [1996] Brown, L. D. and M. G. Low (1996). Asymptotic equivalence of nonparametric regression and white noise. Ann. Statist. 24(6), 2384–2398.

- Carr and Madan [1999] Carr, P. and D. Madan (1999). Option valuation using the fast Fourier transform. Journal of Computational Finance 2(4), 61–73.

- Cont [2006] Cont, R. (2006). Model uncertainty and its impact on the pricing of derivative instruments. Math. Finance 16(3), 519–547.

- Cont and Tankov [2004a] Cont, R. and P. Tankov (2004a). Financial modelling with jump processes. Chapman & Hall/CRC Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton, FL.

- Cont and Tankov [2004b] Cont, R. and P. Tankov (2004b). Non-parametric calibration of jump–diffusion option pricing models. Journal of Computational Finance 7(3), 1–50.

- Cont and Tankov [2006] Cont, R. and P. Tankov (2006). Retrieving Lévy processes from option prices: regularization of an ill-posed inverse problem. SIAM J. Control Optim. 45(1), 1–25 (electronic).

- Dette and Neumeyer [2001] Dette, H. and N. Neumeyer (2001). Nonparametric analysis of covariance. Ann. Statist. 29(5), 1361–1400.

- Ellsberg [1961] Ellsberg, D. (1961). Risk, ambiguity, and the savage axioms. The Quarterly Journal of Economics, 643–669.

- Fan [1991] Fan, J. (1991). Asymptotic normality for deconvolution kernel density estimators. Sankhyā Ser. A 53(1), 97–110.

- Fan and Yao [1998] Fan, J. and Q. Yao (1998). Efficient estimation of conditional variance functions in stochastic regression. Biometrika 85(3), 645–660.

- Figueroa-López [2011] Figueroa-López, J. (2011). Sieve-based confidence intervals and bands for Lévy densities. Bernoulli 17(2), 643–670.

- Grafakos [2004] Grafakos, L. (2004). Classical and modern Fourier analysis. Pearson Education, Inc., Upper Saddle River, NJ.

- Grama and Nussbaum [2002] Grama, I. and M. Nussbaum (2002). Asymptotic equivalence for nonparametric regression. Math. Methods Statist. 11(1), 1–36.

- Jacod and Shiryaev [2003] Jacod, J. and A. N. Shiryaev (2003). Limit theorems for stochastic processes (Second ed.), Volume 288 of Grundlehren der Mathematischen Wissenschaften. Berlin: Springer-Verlag.

- Kahane [1985] Kahane, J.-P. (1985). Some random series of functions (Second ed.), Volume 5 of Cambridge Studies in Advanced Mathematics. Cambridge: Cambridge University Press.

- Kallenberg [2002] Kallenberg, O. (2002). Foundations of modern probability (Second ed.). Probability and its Applications. New York: Springer-Verlag.

- Knight [1921] Knight, F. (1921). Risk, uncertainty and profit. New York Houghton Mifflin.

- Low [1997] Low, M. G. (1997). On nonparametric confidence intervals. Ann. Statist. 25(6), 2547–2554.

- Merton [1976] Merton, R. (1976). Option pricing when underlying stock returns are discontinuous. Journal of financial economics 3(1-2), 125–144.

- Neumann and Reiß [2009] Neumann, M. H. and M. Reiß (2009). Nonparametric estimation for Lévy processes from low-frequency observations. Bernoulli 15(1), 223–248.

- Renault [1997] Renault, E. (1997). Econometric models of option pricing errors. In D. Kreps and K. Wallis (Eds.), Advances in Economics and Econometrics: Theory and Applications, Volume 3, pp. 223–278. Cambridge: Cambridge University Press.

- Söhl [2010] Söhl, J. (2010). Polar sets for anisotropic Gaussian random fields. Statist. Probab. Lett. 80(9-10), 840–847.

- Söhl [2013] Söhl, J. (2013). Central limit theorems and confidence sets in the calibration of Lévy models and in deconvolution. Ph. D. thesis, Humboldt–Universität zu Berlin. Available at http://edoc.hu-berlin.de/docviews/abstract.php?id=40081.

- Söhl and Trabs [2013] Söhl, J. and M. Trabs (2013). Option calibration of exponential Lévy models: Confidence intervals and empirical results. Journal of Computational Finance. To appear. ArXiv:1202.5983.

- Tankov [2011] Tankov, P. (2011). Pricing and hedging in exponential Lévy models: review of recent results. In Paris-Princeton Lectures on Mathematical Finance 2010, Volume 2003 of Lecture Notes in Math., pp. 319–359. Berlin: Springer.

- Trabs [2013] Trabs, M. (2013). Calibration of selfdecomposable Lévy models. Bernoulli. To appear. ArXiv: 1111.1067.

- van Es and Uh [2004] van Es, A. J. and H.-W. Uh (2004). Asymptotic normality of nonparametric kernel type deconvolution density estimators: crossing the Cauchy boundary. J. Nonparametr. Stat. 16(1-2), 261–277.

- van Es and Uh [2005] van Es, B. and H.-W. Uh (2005). Asymptotic normality of kernel-type deconvolution estimators. Scand. J. Statist. 32(3), 467–483.