AMauthor=Aris,color=red,markup=Higlight,icon=Star,voffset=5pt \defineavatarPMauthor=Panayotis,color=ForestGreen,markup=Highlight,icon=Help,hoffset=-1em,voffset=5pt

Power Optimization in Random Wireless Networks

Abstract

Consider a wireless network of transmitter-receiver pairs where the transmitters adjust their powers to maintain a target SINR level in the presence of interference. In this paper, we analyze the optimal power vector that achieves this target in large, random networks obtained by “erasing” a finite fraction of nodes from a regular lattice of transmitter-receiver pairs. We show that this problem is equivalent to the so-called Anderson model of electron motion in dirty metals which has been used extensively in the analysis of diffusion in random environments. A standard approximation to this model so-called coherent potential approximation (CPA) method which we apply to evaluate the first and second order intra-sample statistics of the optimal power vector in one- and two-dimensional systems. This approach is equivalent to traditional techniques from random matrix theory and free probability, but while generally accurate (and in agreement with numerical simulations), it fails to fully describe the system: in particular, results obtained in this way fail to predict when power control becomes infeasible. In this regard, we find that the infinite system is always unstable beyond a certain value of the target SINR, but any finite system only has a small probability of becoming unstable. This instability probability is proportional to the tails of the eigenvalue distribution of the system which are calculated to exponential accuracy using methodologies developed within the Anderson model and its ties with random walks in random media. Finally, using these techniques, we also calculate the tails of the system’s power distribution under power control and the rate of convergence of the Foschini–Miljanic power control algorithm in the presence of random erasures. Overall, in the paper we try to strike a balance between intuitive arguments and formal proofs.

I Introduction

The importance of transmitted power has made power control an essential component of network design ever since the early development stages of legacy wireless networks. Power control allows wireless links to achieve their required throughputs, minimizing the power used in the process and, hence, the interference induced on other links. This increases the spatial spectrum reuse, as a result, the network capacity, and prolongs the battery life of mobile users. For example, the introduction of efficient power control algorithms (both closed- and open-loop), was one of the main improvements that were brought about in third generation CDMA-based cellular networks. Likewise, substantial effort has been made to optimize the performance of future and emerging network paradigms (such as ad hoc networks) by analyzing connectivity and transport capacity under power control [1, 2, 3, 4]. As a result, several algorithms have been developed that provably allow receivers to meet signal-to-interference-and-noise ratio (SINR) requirements of the form (where the threshold value is determined by the requested rate of each link) while minimizing power subject to feasibility constraints [5, 6]. However, while the benefits of such algorithms are easy to evaluate in small networks or networks with simple geometries (e.g. with transmitters and receivers located on a grid), their behavior in large-scale random networks has not been quantified analytically.

The conditions for the feasibility of power control have been discussed extensively under general assumptions [7, 3] but without characterizing the properties of the optimal power vector in a quantitative way. In contrast, using the Laplace transform method, the authors of [8, 4] calculated the effects of fading, pathloss and random erasures on the interference to a random receiver in both regular and Poisson random networks; in addition, the authors also analyzed therein the effects of power control by inverting the pathloss and/or the fading coefficient of the direct link of a given transmitter-receiver pair. That said, interference from neighboring transmitters is modeled as an effective medium without any feedback: as a result, the impact that increasing power in a given link has on its neighbors (that also control their power in order to meet a target SINR value) is ignored.

A similar approach is taken by the authors of [9] who introduce a scheme to compensate for the fading coefficient of the direct link between transmitter and receiver (but, again, without addressing the effects on neighboring links). Such effects were partially included in the context of percolating networks in [10]; there however, the network was initially assumed to percolate with all users transmitting at maximum power, and then reducing their power while maintaining connectivity. In this way, only the links that are already connected transmit at their optimal power level, without any guarantees to others.

Interference is a serious problem in dense WiFi networks, and it is also expected to remain a major issue in the recently proposed femto-cell paradigm when such cells are deployed at a massive scale [11]. Due to their close proximity, neighboring femto-cells may create interference to one another, so when a transmitter increases its power to compensate for interference, it may precipitate a cascade of power increases which needs to be kept in check. As a result, power optimization is crucial in the above scenarios; nonetheless, little progress has been made in finding analytic performance estimates for random, interference-limited networks under power control [12].

In this paper, we present an analytical framework to quantify the optimal power characteristics of large random networks in the presence of interference by introducing a number of methods from statistical mechanics. We begin with a pure, ordered network in the form of an equally spaced square lattice of transmitters, each with a receiver located at a fixed distance in its (Voronoi) neighborhood. Randomness is then introduced in the network by removing (“erasing”) each transmitter-receiver pair with probability , leading to a network of (roughly) transceiver pairs that are placed randomly on the original lattice. This thinned network is a plausible model for a cellular network with random transmitter locations; it is also a reasonable model for a wireless network with intermittent activity where a fraction of the transmitters are inactive at any given time.

To derive an expression for the average transmitted power in a random network of this type, we employ the so-called coherent potential approximation (CPA) approach, an approximate self-consistent method which was first introduced in the study of disordered metals [13, 14]. The expressions obtained in this way turn out to be identical to those obtained using random matrix theory (RMT) [15, 16, 17] and they agree with numerical results when power control is feasible. However, they fail to account for the fact that an infinite system is always infeasible while a finite network only becomes infeasible with increasing probability for larger values of the target SINR value .

As a result, even though the problem of determining the average transmit power under power control can be reduced to the analysis of a large random matrix, traditional RMT methods are only approximately correct. The shortcomings of such methods can be traced to the fact that the interference that each receiver observes is mostly due to nearby sites, so it exhibits sizable spatial fluctuations. Consequently, the interference fluctuations at each site do not vanish in the large system limit (as posited by RMT); in fact, these fluctuations persist and, in some cases, end up dominating the behavior of the system. Instead, by modeling power control as a random walk in a random medium, we show that the problem is equivalent to the so-called Anderson impurity model which was originally introduced to describe the motion of electrons in random crystal lattices [18] and was later applied to the study of diffusion processes in disordered media [19]. Using this equivalence, we obtain analytic results for the probability that the system becomes infeasible and we are also able to estimate the tails of the distribution of power in the system under power control.

Even though we work with a specific network model, we will argue throughout the paper that this paradigm is generic for power controlled networks when interference and randomness both play a significant part. In fact, one of the main contributions of the paper is the introduction of tools and methodologies from the physics of disordered metals and the theory of random walks in random media to analyze such networks.

I-A Summary of results

We will now provide an outline of the paper, while at the same time summarizing our main contributions. In the main text of the paper, we try to use intuitive arguments –as opposed to strictly mathematics based ones, trying to bring out the important connections between the physics of disordered systems and the power control dynamics of random wireless networks. Most appendices, in contrast, are more rigorous and there we try to elucidate the details of the proofs.

Our random network model is introduced in Section II, where we also establish the connection between the erasure channel model of [15, 16], random walks in random media, and the Anderson impurity model. In Section III, we then focus on a specific one-dimensional network where only adjacent transmitters interfere with each other – the so-called Wyner model [20]. In this simple, yet insightful framework, we are then able to compute all relevant quantities exactly: in particular, we calculate

-

1.

The eigenvalue distribution of the system’s pathloss matrix, which determines its feasibility (Section III-A);

-

2.

The system’s probability of infeasibility – which, for large but finite systems, turns out to be asymptotically proportional to the tails of the system’s eigenvalue distribution (Section III-C);

-

3.

The tails of the empirical distribution of powers in the optimal power vector (Section III-D).

Accordingly, the Wyner model will serve as a reference point throughout the paper, and will motivate the results of later sections: for example, the failure of traditional RMT techniques will be established by comparing the exact density of states of the Wyner model (a distribution with a countable dense set of atoms) to that derived by RMT methods.

In Section IV, we introduce the so-called coherent potential approximation (CPA) method and we show that it is equivalent to RMT (although more general in scope). Despite its approximate nature, we demonstrate numerically that it is an extremely accurate predictor of both the average optimal power and the average variance of the power vector of the network when power control is feasible. That said, CPA exhibits a fundamental shortcoming in that it fails to predict the probability of instability of the network when operated beyond the stability region of the pure, deterministic system – an instability which stems from the infrequent appearance of small eigenvalues in the random, disordered system.

In Section V we show that power control in the network is always infeasible in the infinite system regime beyond a particular value of the SINR target, irrespective of the degree of randomness in the network. Nevertheless, for large (but finite) networks, this instability can be described by the so-called Lifshitz tails of the network’s cumulative density of eigenvalues. In Section V-B, we show that the probability that power control becomes infeasible in a finite (but large) network is proportional to the cumulative density of eigenvalues of the corresponding infinite system, thus providing an infeasibility criterion for network operation. In particular, we find that the tails of this distribution scale as (to exponential accuracy), where both and depend on the system’s dimensionality and the pathloss exponent in an explicit way (that we also calculate).

Even though the average variance of the power vector calculated in Section IV provides an indication of how large the optimal transmitting powers of the systems can become, it is also important to have an understanding of how often much higher powers occur. In Section VI, we obtain a lower bound for the tails of the empirical distribution of the optimal power vector, and we find that the cumulative power distribution scales as for (where is a power law which depends on and ); in particular, in the near-critical limit , we find that scales as for . We argue that this bound appears to be tight, but we have not been able to prove this; that said, in Appendix D we do establish a tight upper bound for -dimensional systems where only adjacent transmitters interfere.

I-B Notational conventions

Throughout the paper, we will use the asymptotic equality notation “ near ” to mean ; when , we will write more simply “ for large ”. To maintain the intuitive flow of the discussion, we will sometimes not distinguish between finite- and infinite–dimensional operators in the main text; whenever such a distinction is important, it will be detailed in a series of appendices at the end of the paper. Also, if is a discrete set, the real space spanned by will be denoted by and the basis vector of corresponding to will be denoted by . Finally, we will use to denote the indicator function which takes the value if its argument is true and zero otherwise.

II Model description

II-A Definitions and connection to random walks

We start by defining the basic quantities of the problem and establishing a deep connection between power control and random walks of a particle in a random medium (a connection which will be crucial for later sections).

Consider a general network with transmit-receive pairs. Let be the channel coefficient, or power gain, between transmitter and receiver , and let denote the transmit power of transmitter . We then assume that every transmitter adjusts their power to meet the target SINR criterion

| (1) |

where denotes the threshold SINR of the -th transmitter–receiver pair and is the thermal noise level at the receiver. This inequality can then be written in linear form as

| (2) |

or, more concisely, as

| (3) |

where is a vector of ones, is the network’s power vector, and the matrix is defined in components as:

| (4) |

We will then say that power control in the network is feasible [3], if there exists a finite positive vector which saturates the constraints (3); in particular, if is invertible, we will have:

| (5) |

In the seminal paper [5], it was shown that the power control dynamics

| (6) |

converge to the power vector (if it exists), which saturates the inequalities in (2) – assuming of course that their feasible set is not empty. In matrix form we can simply write

| (7) |

so the corresponding stationary solution is simply . In this way, (6) may be viewed as the evolution of a population of particles spread over a point lattice (indexed by ) with constant birth rate equal to , where is the particle transition rate from site to site and represents the rate of absorption at each site . The optimal power vector describes the stationary distribution of the process. This interpretation will allow us to view power control as a random walk process, and will be crucial in what follows.

II-B Networks without disorder

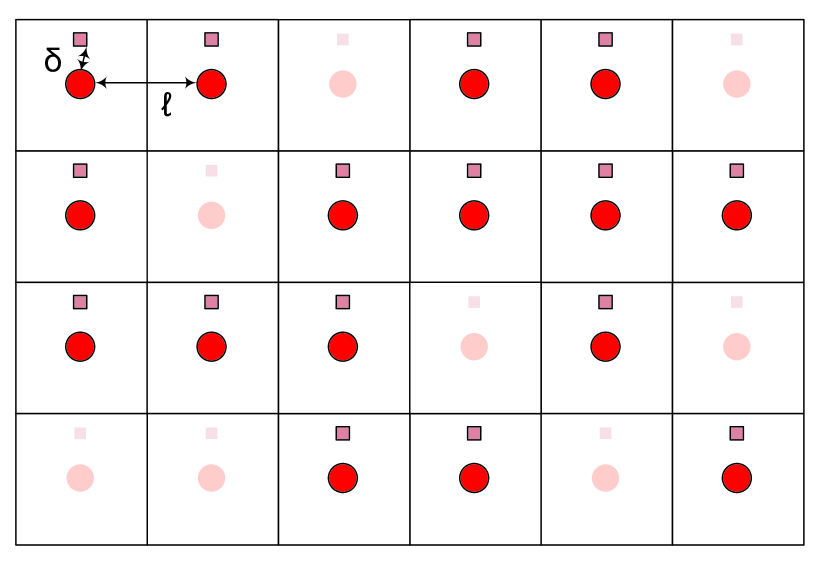

We begin with our model of an ordered network, namely a regular, deterministic network consisting of transmitters situated on the nodes of a regular -dimensional lattice (). For concreteness, in two dimensions, we will focus on square lattices with inter-neighbor distance and we will assume that each receiver is located at distance from the corresponding transmitter (see Fig. 1).

More precisely, let be a positive integer and let denote the -fold product of the cyclic group of integers modulo . The elements of will be indexed by so that denotes the position of the -th transmitter on and addition or subtraction of is taken modulo .

In this context, our model for the network’s channel coefficients (averaged for fading) will be:

| (8) |

where

-

a)

The pathloss exponent () expresses how fast the channel strength decays as a function of distance.

-

b)

denotes the distance between a transmitter and its intended receiver.

-

c)

represents the physical distance between elements of .

-

d)

The function describes the pathloss between a transmitter and a receiver located at the points in the lattice with distance apart.

This ordered network model will be crucial to our analysis, so a few remarks are in order:

Remark 1.

A simplifying assumption in (8) is the dependence on the distances between transmitters and receivers: indeed, (8) is technically correct only when each receiver is positioned vertically to the space spanned by the transmitter lattice (a line for and a plane for ) (see for example [7]). Nevertheless, (8) exhibits the correct behavior for as well as for thus, given that we will be focusing on the case where interference is relevant, the exact location of interferers far away is not important. Moreover, when the pathloss exponent has to be estimated by curve-fitting large amounts of data with sizable errors, the error induced by the perpendicularity assumption in (8) becomes negligible when compared to the estimation error for [22], so this approximation is harmless in the large system limit.

Remark 2.

It should be mentioned here that the periodicity assumption of taking addition modulo in was introduced in (8) purely for convenience: in the large system limit that we will focus on, boundary effects that would occur from embedding in instead of a -dimensional torus can be effectively ignored when because each line of the matrix is absolutely summable so the approximation error from (8) becomes negligible [21].

II-C Average power and feasibility

The first metric that we will consider for the optimal power vector is the average power per node, which can be expressed (5) as

where . Clearly, for to be well-defined, the eigenvalues of the inverse matrix must be themselves positive, so it will be important to analyze the eigenvalue structure of . To that end, note first that the eigenvalues of will be real on account of being real and symmetric.111This is actually one of the main reasons for choosing the model (8). Furthermore, given that the modular arithmetic of allows us to view as a generalized circulant matrix indexed by [23], the eigenvectors of will be Fourier modes indexed by the row vector

| (10) |

The eigenvalue corresponding to the index vector will then be the associated Fourier transform of any line of , i.e.

| (11) |

Accordingly, the minimum eigenvalue of (corresponding to the eigenvector ) will be:

| (12) |

where

| (13) |

In a network of infinite size, is finite if and only if ; the optimal power vector of the system will then be

| (14) |

leading to average power

| (15) |

Hence, for the system to be well-defined and feasible we need or, equivalently:

| (16) |

For simplicity, it will be convenient to shift the spectrum of to positive values by introducing the positive-semidefinite matrix via the equation

| (17) |

In view of (11), the eigenvalues of will then be

| (18) |

so the feasibility of the optimal power vector will be determined by the behavior of for small (i.e. by the lowest eigenvalues of ).

For , an asymptotic expansion of yields

| (19) |

with

| (20) |

On the other hand, for , the series (20) for is no longer summable; instead, using the Poisson summation formula, it can be shown that the leading order asymptotic expression for will be of the form

| (21) |

where is a computable constant. Thus, with a fair degree of hindsight, it will be convenient to introduce here the effective pathloss exponent

| (22) |

and the corresponding leading order coefficient

| (23) |

In this way, (19) and (21) may be written more simply as:

| (24) |

II-D Random networks: disorder and erasures

There are two ways of introducing randomness (disorder) in the network model of the previous section. First, the target SINR of each user (and hence, the corresponding rate) may be random at each site; second, a random fraction of the transmitters could be turned off (“erased”) at any given time. The former type of randomness can be analyzed in conjunction with the latter but, due to space limitations, we will defer this analysis for the future. In the present paper, we will only focus on erasures, which will be introduced in two different (but equivalent) ways.

II-D1 The Anderson model

The first “erasure” procedure that we will consider may be described as follows: first, the sites to be turned off are chosen at random with a fixed erasure probability . Then, the optimal transmitting power of a transmitter which is to be switched off is set to by setting for the corresponding channel strength between the -th transmitter and its intended receiver. Indeed it is not hard to see that when becomes arbitrarily large in (2), the SINR target constraint for the -th link may be met with arbitrarily small power . Formally, consider the random diagonal matrix

| (25) |

with random independent and identically distributed (i.i.d.) entries such that

| (26) | ||||

Erasures are then introduced by replacing in (17) with

| (27) |

with matrix elements , where and is a large positive parameter which turns off the sites determined by in the limit . In particular, the quantity plays the role of the excess channel gain of a given transmitter to its intended receiver: since we are interested only in optimal power solutions which assign finite positive transmitting power to each site, the limit can then be taken in the end of the calculation of the inverse matrix .

The case of spatially random can be treated in a similar fashion, by including in .

Remark.

The matrix above has deterministic off-diagonal elements and diagonal disorder and it is known in the physics literature as the Anderson model. This model was introduced by P. W. Anderson to explain localization of particles (and waves) in random media [18], and it has since been extended to study random walks in random media [24].

In this context, the optimal power vector will be given by

| (28) |

so its intra-sample average over non-erased sites can be derived by multiplying from the left by and dividing with the expected number of non-erased sites , producing

| (29) |

As a result, via spectral decomposition, may be expressed directly in terms of the eigenvalues and eigenvectors of the random matrix as

| (30) |

where denotes the -th eigenvalue of and is the corresponding eigenvector (note that is itself an eigenvector in the absence of erasures). The effect of the limit above can be appreciated by invoking Gershgorin’s circle theorem, which tells us that for large and a given realization of the randomness with ones in , the spectrum of will consist of large eigenvalues of order and and the remaining ones are in . Hence the former will not play any role in the power vector above.

In view of the above, the average optimal power will be finite and positive as long as the eigenvalues of the matrix are large enough, i.e. . More importantly, the analysis of [7, 3] (see Lemma 18.2.4 in [3]) readily yields the following stronger statement for the feasibility of power control:

Theorem 1.

Power control is feasible if and only if . Consequently, the probability of instability (or infeasibility) for the network will be:

| (31) |

where denotes the minimum eigenvalue of .

This result provides a close connection between the feasibility of the system and the lower part of the spectrum of . In fact, as an immediate corollary of Theorem 1, we obtain:

Corollary 1.

The system is always feasible for .

Despite their apparent simplicity, the results above do not provide any intuition on what happens in the network for and how feasibility breaks down for larger . In the next sections we will see that for the system becomes unstable (i.e. its powers explode) in the network configurations where the minimum eigenvalue of becomes larger than . We will also calculate the probability for this to happen.

II-D2 The erasure channel model

To make contact with previous work on the erasure channel [15, 16, 17], we will also consider a different random network model and show that it is equivalent to the large limit of (27). In particular, for every transmitter-receiver pair that is to be “switched off”, we will set the corresponding column and row elements of the channel matrix to zero by considering the matrix

| (32) |

with matrix elements , and with given by (26) as before. In this way, the multiplication with from the left and right, the “erased” sites are completely decoupled – and, hence, switched off. This has the the effect of completely decoupling the erased sites, which are thus effectively switched off.

The previous discussion (e.g. the statement of Theorem 1) obviously still applies with replaced by and with the caveat that “minimum eigenvalue” should be interpreted as the “minimum eigenvalue over the range of ” – simply note that the zero eigenvalues contributed by the erased sites should not be counted in (31). Thus, given that the lower part of the spectrum of approaches that of for large (see Proposition 5 in Appendix B), the two erasure models will be equivalent in the limit .

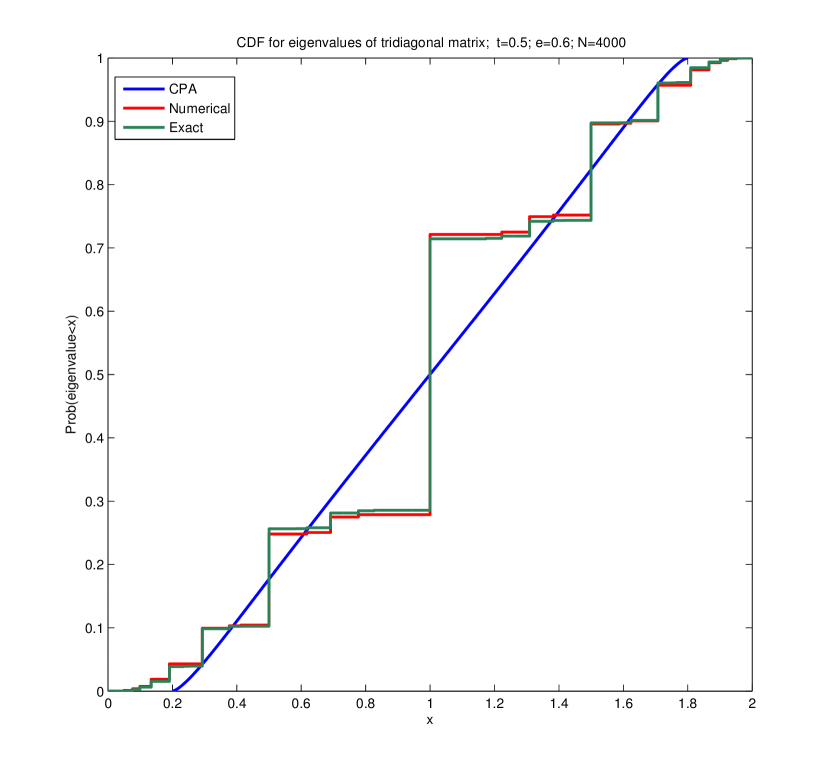

III The Wyner model: Exact results

Our goal in this section will be to analyze the so-called Wyner model [20], a simple one-dimensional random network where the asymptotic behavior of the optimal power vector can be calculated exactly. Thanks to this simple model, we will have the opportunity to introduce several metrics for the behavior of the optimal power vector that are at the core of our considerations; more importantly, the exact results obtained here will provide the intuition and necessary groundwork to understand the asymptotic behavior of more general network models that require significantly more sophisticated tools.

The Wyner model consists of a circular array of transmitters,222Again, the effects of the geometry may safely be ignored for large , so the system may be considered linear in the large limit. located a fixed distance apart so that only neighboring transmitters interfere with each others’ transmissions. Accordingly, the matrix describing the system in the sense of (17) will be a tridiagonal matrix with elements

| (33) |

where addition in and is taken modulo , and the parameter determines the interference level between users.

Comparing the above with (8), (13) and (20), it follows that the Wyner model (33) will have

| (34) |

Furthermore, since the system is one-dimensional and interference only comes from a site’s nearest neighbors, erasures will simply partition the system into independent blocks of different (random) lengths, separated by sites with zero power. In particular, in the infinite system limit, the distribution of the cluster length can be shown to be exponential, i.e.

| (35) |

Thanks to this partition, we will calculate a) the eigenvalue distribution of in the presence of erasures; b) the resulting optimal power vector; c) the system’s instability probability (i.e. the probability of the optimal power vector being infeasible); and d) the tails of the power distribution when power control is feasible.

III-A Eigenvalue distribution

As we indicated in the previous section, the feasibility of the optimal power vector for a given erasure matrix will be determined by the spectrum of . Accordingly, our aim here will be to determine the system’s integrated density of states (IDS), i.e. the number of eigenvalues not exceeding a given level divided by the size of the system; formally, we let:

| (36) |

where is the set of eigenvalues of the matrix (see Appendix B for a more detailed discussion). Clearly, each realization of partitions into disjoint tridiagonal Tœplitz blocks of varying lengths, so the eigenvalues corresponding to a block of length will be:

| (37) |

In view of the above, the probability of observing a given eigenvalue may be calculated by averaging over the possible block lengths for which this eigenvalue may occur. To that end, since the probability of observing a segment of length in the infinite system limit follows the geometric distribution (35), some algebra yields the following expression for the integrated eigenvalue density :

| (38) |

where

| (39) |

and denotes the denominator of in lowest terms.

To understand this expression, we note that the second sum in the first line of (III-A) counts the number of non-zero eigenvalues that do not exceed in a block of length . One then needs to normalize the expression with the average number of eigenvalues, or, equivalently, the average block size ; finally, the expression for results from summing over all rationals of the form that correspond to an eigenvalue occurring in blocks of different length.

The cumulative eigenvalue density (III-A) above has two interesting properties: First, the set of discontinuities of (corresponding to the atoms of the underlying eigenvalue distribution) is dense in : in particular, is discontinuous at all points of the form , , and is continuous otherwise. This is consistent with the prediction that the cumulative density of eigenvalues is discontinuous for the one-dimensional Bernoulli-distributed random potential above [25, 26].

Second, the infimum of the support of is zero for all , a behavior which is intimately connected with the infeasibility of power control in the system. However, very small eigenvalues correspond to very large (and very rare) clusters that occur with probability of the order of where

| (40) |

denotes the inverse of (37) for (i.e. is the size of the smallest cluster which supports the eigenvalue ). As a result, for small , the integrated density of eigenvalues becomes

| (41) |

The importance of this expression will become clear below, where we show that is proportional to the instability probability for large (but finite) systems.

III-B The optimal power vector

Owing to the partition of the system into erasure-free blocks, the optimal power at each point may be calculated by noting that, in any given block of length , the power control equations (2) may be rewritten more suggestively as:

| (42) |

where denotes the second-order difference operator , and we are taking boundary conditions (recall that each end of the block is erased). Depending on the value of the target SINR , we thus obtain three different solutions:

-

1.

For subcritical , we get the hyperbolic expression:

(43a) (43b) -

2.

At the critical value , we get the quadratic solution:

(44) -

3.

Finally, supercritical leads to the elliptic solution:

(45a) (45b) which is obviously equivalent to the hyperbolic solution (43) with .

Remark.

We note here that the solutions (43)–(45) of the finite difference equation (42) may be mapped to the solutions of the continuous differential equation

| (46) |

with boundary conditions . As we shall see in the next section, this last equation may be viewed as a “large ” limit of (42) where the sites are approximated by a continuum of sites and the power vector by the power distribution (see also Appendix C). This approximation will be key to the analysis of more general problems, so it is worth keeping in mind even in the exactly solvable Wyner model.

III-C Feasibility analysis and probability of instability

Obviously, for power control to be feasible, the components of the system’s optimal power vector (given by (43) and (45) for the subcritical and supercritical regime respectively) must be finite and nonnegative. Since (43) is positive for all ,333Simply note that for . the optimal power vector will always be feasible if (cf. Corollary 1). On the other hand, for , may take on negative values if : indeed, the denominator of (45) vanishes for , so the optimal power vector will start becoming infeasible beyond the critical value .

The above criterion may be reformulated in terms of the length of each erasure-free block as follows: by (37), the minimum eigenvalue of a block of length such that will satisfy the inequality:

| (47) |

As a result, for , for a given realization of the erasure matrix , power control will be feasible only if the system’s largest erasure-free region (where the system’s smallest eigenvalue is encountered) satisfies the criterion (47). Hence, in view of Theorem 1, the instability probability for a finite system of size and target SINR will be:

| (48) |

where is the maximum realized cluster size and

| (49) |

denotes the minimum cluster size for which the infeasibility criterion (47) is satisfied.

The RHS of (48) may be evaluated explicitly to yield

| (50) | ||||

where each term counts the number of ways that blocks of non-erased sites can appear in a circle of length .444(50) was obtained by expressing as a sum over the possible positions of erasure-free regions, taking the -transform, averaging over the corresponding probabilities and taking the inverse -transform of the result.

Remark 1.

As , the probability of encountering arbitrarily large clusters approaches , so very large Wyner networks will be infeasible almost surely. This prediction is consistent with (50) where, with a little algebra, one can show that as . Importantly, even though this result seems to depend crucially on the specific structure of the Wyner model, we will see in Section V that this property remains true in a significantly more general class of random networks.

Remark 2.

For the instability probability to be small, has to be large and hence must be close to . In this case, (50) may be expressed to leading order as

| (51) |

with the approximation being valid for or, equivalently:

| (52) |

This shows that the instability probability in a network of size is small whenever the target SINR value lies within of the network’s critical threshold ; in other words, if is not too large, the parameter range of for which power control remains feasible can be itself fairly large.

Remark 3.

It is also important to note that the instability probability (51) is proportional to the tails of the integrated density of eigenvalues in (41). This is no coincidence: the instability probability is given by the cumulative distribution function of the minimum eigenvalue of the system, which is in turn proportional to . This important point will be made more precise in Section V-B.

III-D Power distribution in the Wyner model

Thanks to the simplicity of the Wyner network model, we may also calculate the tails of the empirical distribution of powers in the optimal power vector , or equivalently the fraction of sites with power exceeding some large value . Since all sites are statistically equivalent, this distribution may be viewed as the probability that the optimal power at the origin exceeds , i.e.:

| (53) |

Now, given that the fraction of clusters of size follows the geometric distribution (35) for large , the distribution of powers over the network may be written similarly to (III-A) as

| (54) |

The above expression is derived in a similar fashion as (III-A): We have taken into account the geometric distribution of segment lengths and have normalized over the average segment length . In addition, the second sum in the above expression corresponds to the possible positions of the site located at the origin of the lattice within a segment of length .

As we saw in the previous section, in the supercritical regime , there is a finite probability that the system will be infeasible, so it only makes sense to analyze the distribution of powers for . To that end, we will first consider the critical SINR target value with given by (44).

Obviously, if we focus on the tails of the distribution (i.e. for powers ), only the terms with sufficiently large will contribute to the sum (54): in fact, since the maximum power for a segment of size is roughly , (54) will only count the terms with . Hence, using the Euler-MacLauren formula [27] to replace sums by integrals, we get

| (55) |

where and is the number of sites in a segment of length with power greater than . This yields

| (56) |

for some constant (independent of ), so the tails of the power distribution are again determined by the rare event of observing an erasure-free region of size exceeding .

The subcritical regime can be treated in the same way, the only difference being that the power in the system will always be bounded by . When is small there is no point in discussing the tails of the distribution. However, the situation becomes quite interesting in the near-critical regime where powers are allowed. As before, introduces a characteristic length which corresponds to the minimal segment supporting power equal to at its midpoint (i.e. the point of highest power in the segment); then, by inverting (43) for , we obtain:

| (57) |

and hence:

| (58) |

This formula is quite interesting, because the exponent interpolates between for , and when .

III-E Bird’s eye view of the Wyner model

To sum up, it is worth pointing out here that the simple (but not simplistic) one-dimensional Wyner model carries all the qualitative properties of the more general models that we will encounter in the following sections.

On the one hand, power control is feasible for all when the users’ SINR target is below the critical feasibility SINR threshold of the pure, ordered Wyner network (). In this case, one obtains an explicit expression for the average power per node, simply by summing over the distribution of erasure-free segments. On the other hand, in the supercritical regime , the infinite Wyner network becomes infeasible almost surely; nonetheless, networks of finite size exhibit a finite instability probability, and this probability becomes exponentially small when . This instability is due to the occurrence of large, erasure-free regions, and the probability of this rare event is proportional to the integrated density of states evaluated at (in fact, these rare, erasure-free regions are also responsible for the occurrence of atypically large powers in the optimal power vector). In Sections V-B and VI, we will see that these mechanisms are responsible for the instability and large power characteristics of more general networks as well.

IV Average power via the coherent potential approximation

In this section, we will focus on the “bulk” characteristics of the network in the presence of randomness; in particular, we will calculate the (intra-sample) average power per node and its variance by means of the so-called coherent potential approximation (CPA) approach, an approximative methodology which has been applied extensively in the physics literature to study the movement of electrons in disordered alloys [13, 14, 28]. For simplicity, we will only show the intuition and the end results of the CPA method here; a more detailed discussion of the derivation will be given in Appendix A where we also provide further pointers to the extensive literature on the CPA method.

Importantly, even though CPA is not an exact method, it has enjoyed considerable success in calculating the energy spectrum of systems with diagonal disorder, and its predictions become increasingly accurate when the number of connections between different sites increases. It should also be mentioned that results obtained by the CPA method turn out to be identical with those predicted in [15, 16] using tools and techniques from random matrix theory and free probability theory: essentially, the self-energy that is the cornerstone of the CPA method corresponds to the -transform in RMT, so CPA may be viewed as an approximative way of applying RMT methods.

To proceed, let be the Green’s function operator (often called the resolvent in RMT) associated to the matrix of (27), namely:

| (59) |

In this notation, the intra-sample average optimal power of the system becomes

| (60) |

so we will calculate by taking the expectation of over all realizations of and then letting .

The first implicit assumption of the CPA method is that becomes deterministic in the large limit, i.e. as (a.s.). With this in mind, we will replace each random diagonal element of in with a so-called “self-energy” term capturing the effects of all other sites in the network in a self-consistent fashion (see Appendix A for a more detailed discussion of what “self-consistency” means here). In other words, CPA is essentially a “mean-field” solution to the problem where interactions across different sites are replaced by a “mean field” which measures the average effect of these interactions.

Apart from these caveats, we are now in a position to state the CPA equations (see Appendix A for details on their derivation). To begin with, the average Green’s function operator in the CPA regime will be:

| (61) |

where

| (62) |

is the resolvent (Green’s function) operator in the absence of randomness and

| (63) |

is the system’s self energy. Strictly speaking, this self energy corresponds to site , hence the CPA recipe requires only an averaging over the randomness of the given site. The implicit assumption is that all other sites have been taken into account self-consistently and have been lumped into the diagonal element of (see Appendix A), given by

| (64) |

In this way, letting in (63) readily gives

| (65) |

and hence, for , (64) leads to the following implicit expression for the self-energy :

| (66) |

The above equation can be solved numerically to yield . Then, to evaluate the average optimal power we may use (29) and the fact that is proportional to the eigenvector; doing just that, we get:

| (67) |

Importantly, this equation is identical to the one derived in [17] under the (false) conjecture that the matrices and are asymptotically free. Moreover, it is easy to see that the above result reduces to in the limit : for , the RHS of (66) vanishes only when , so (67) yields . Similarly, for , (66) gives leading to the non-interference value .

Remarkably, the CPA approach also allows us to describe the fluctuations of the optimal power vector from its average value. Indeed, for large , the (intra-sample) variance of the optimal power vector will be

| (68) |

so, by employing (28), we will have

| (69) |

By differentiating (67) with respect to , we then obtain

| (70) |

with given by (66).

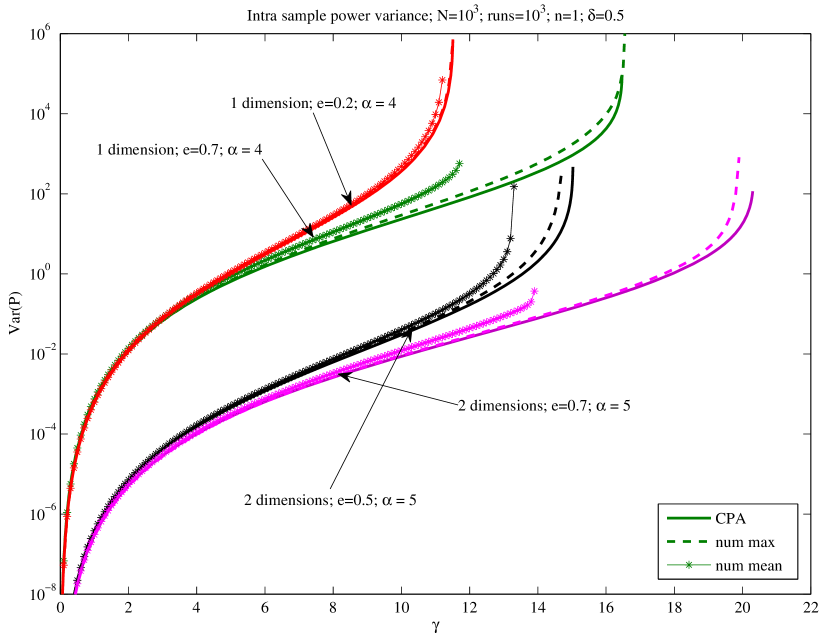

IV-A Numerical analysis and validation

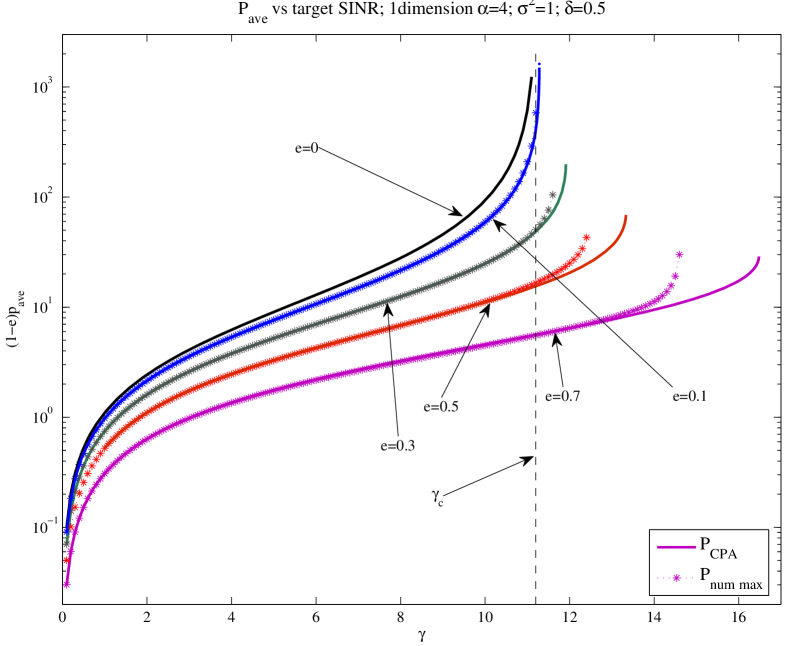

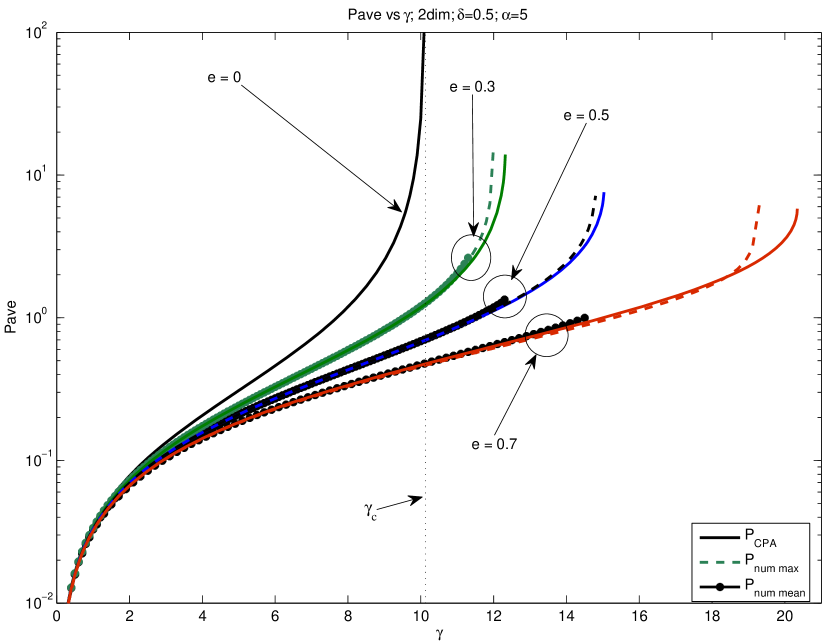

To study the accuracy of the CPA appraoch, we will analyze here the validity of (67) and (IV) for the average optimal power and its variance via numerical simulations. In Figs. 3(a) and 3(b), we plot for one and two dimensional systems respectively, as calculated from (67) and as obtained by generating instances for in (29) versus the SINR threshold . As it turns out, the analytically calculated value of is finite not only for , but also for a range of SINR target values for which the erasure-free network () is infeasible. Nonetheless, (65) and (66) show that the CPA solution cannot be extended indefinitely: it eventually reaches a value of beyond which the optimal power vector becomes infeasible.

The agreement between the CPA solutions and the Monte Carlo data is excellent over a wide range of . Nevertheless, for , the behavior of the simulated system becomes sample-dependent: in particular, for any given realization of , the graph of versus follows the CPA curve very closely until a certain random beyond which the two curves start to diverge, with the simulated network becoming infeasible soon after. We illustrate this phenomenon from two different points of view in both Fig. 3(a) and Fig. 3(b). In Fig. 3(a), and for each value of , we plotted the curve vs. that became infeasible at the largest value of from a sample of random realizations. In Fig. 3(b) we also plot the curve corresponding to the average value of over all realizations generated. This last curve terminates at the minimum value of at which some realization became infeasible. Although both curves look identical, what is striking is the significant gap in the value of where the first realization became infeasible, compared to the last. The good agreement between numerics and CPA appears also in the case of the variance (IV), which is plotted for both one- and two-dimensional networks in Fig. 4.

IV-B The breakdown of the CPA approach

Remarkably, even though the CPA expressions agree with the numerically generated data when the simulated system is feasible, there exists a significant gap between the infeasibility threshold predicted by the CPA approach and the largest value of where the simulated system breaks down. This is strongly reminiscent of our analysis of the Wyner network model in the previous section: indeed, for , the Wyner network becomes infeasible with finite probability, related to the minimum eigenvalue of becoming negative. In other words, while the bulk behavior of the system is captured remarkably well by the CPA method, tail events are not.

The aim of the following sections will be to highlight this tail behavior; for now, we will only give an intuitive explanation of why the CPA and RMT equations cannot be expected to obtain a result which remains valid for all values of .555A similar version of the CPA equations was also derived in [29, 30, 31]. Indeed, RMT typically addresses systems described by operators (or matrices) connecting all states in a random way: in the context of matrices, this means that the randomness permeates the whole matrix, so every site experiences the same, average environment. By contrast, randomness in our systems appears only in the diagonal elements of the matrix, and as it turns out, this is not “enough” to apply an approach based on a law of large numbers. In particular, since each site is connected to a finite number of sites, it experiences an independent realization of the randomness and hence the behavior at different parts of the system will exhibit significant fluctuations; as a result, it may be very misleading to replace a site’s local environment with an average “mean field” quantity.666This only makes sense in the large limit discussed in[31].

This was first exemplified by Anderson [18] who suggested that averages may often be spurious, while the distribution of rare events can be more important. The significance of tail events already appeared in the instability analysis for the Wyner model in the previous section and it will be made clearer in the following sections where we go beyond the CPA regime.

V Stability analysis

In the previous section, the numerical validation of the CPA results showed that while the CPA equations match numerical results very closely in most realizations of the network, power control becomes infeasible well before the SINR threshold predicted by the CPA method. In particular, when the simulated network is large, this instability occurs for some random, sample-dependent . In this section, we will analyze the probability of such an instability occurring: we will see that power control is always infeasible for for infinite networks (Section V-A), and we will also calculate the instability probability for finite networks (Section V-B).

V-A Feasibility and instability in infinite networks

Corollary 1 shows that the system is always feasible if , i.e. for all and for all . In contrast, we will now show that the infinite system is always infeasible if :

Theorem 2.

In the infinite system limit, power control is feasible if and infeasible if (a.s.).

Proof.

In view of Corollary 1, it suffices to consider the case . To that end, consider a finite network of edge length and a cubic region with sites per edge. Initially, we will ignore the surroundings of the smaller region, which corresponds to setting all sites outside this region to zero. Let be the minimum eigenvalue of in this smaller region. Since is a Tœplitz matrix, we will have

| (71) |

where is defined as in (13), and the RHS corresponds to the minimum eigenvalue of in the limit [21, 32]. Now, with and , there exists some such that for all . This means that for , power control in this region is infeasible, as was to be shown.

Up to this point we have neglected the effects of neighboring sites outside the region in question. However, since the power of each transmitter inside the smaller region will grow in the presence of other transmitters outside the region, it follows that power control will be infeasible in the -sized erasure-free region for , even in the presence of outside transmitting powers. As a result, if there exists an erasure-free region of size the whole system will be itself infeasible.

Now, let be the event that there are no erasures in any region of edge length . Clearly, any fixed region of size will be erasure-free with probability ; as a result, the network’s instability probability will be bounded from below by the probability of , i.e.

| (72) |

We conclude that power control in an infinite network is infeasible for any target SINR which is larger than the critical SINR threshold corresponding to an erasure-free network. ∎

Remark.

It should be pointed out that the above analysis does not deal with the case . Of course, any finite network with is feasible, because it has finite power even if it is completely devoid of erasures. Furthermore, in the case of the Wyner model (Section III-D), we saw that even though the support of the optimal power vector is unbounded for , the probability of observing an infinite power value is zero. We conjecture that this holds in general, and we will prove this assertion for some representative cases in Section VI.

V-B Instability probability in finite networks: Lifshitz tails

The instability in the supercritical regime that was established in the previous section concerns only infinite networks. In finite networks, the numerical simulations of Section IV show that this instability is probabilistic in nature: the average power is close to the one that was derived analytically using the CPA method until the system becomes infeasible at a random, sample-dependent value of . In this section we will quantify the instability probability for by building on the insights of Section III where we saw that the system becomes unstable when rare, large erasure-free regions occur. In this way, we will show that instability events are always local in origin, and we will characterize the associated instability probability by relating the size of these regions to .

We begin by recalling the relationship (31) between infeasibility and the distribution of the minimum eigenvalue of the matrix of the network, i.e.

| (73) |

where we emphasize the dependence on the size of the network by writing instead of . Of course, for finite , sites are not really erased in the network – their power is simply reduced. Thus, to obtain the instability probability for a network with bona fide erasures, we will need to take in (73) or, equivalently (see Appendix B), to apply Theorem 1 to the erasure model (32) and write:

| (74) |

where, again, we write instead of to emphasize the dependence on the size of the network.

Of course, will be positive only if , i.e. when ; in that case, we need to look at the low-end part of the spectrum of which we will study by means of its cumulative eigenvalue distribution. Formally, for finite networks, we define the cumulative densities

| (75) | ||||

where denotes the spectrum of the matrices and , defined in (27) and (32), respectively. Then, in the infinite system limit, we will have

| (76) | ||||

with as (see App. B for a detailed discussion).

Of the above quantities, the object of interest is for large (but finite) networks ; indeed, we have:

Lemma 1.

Let be the minimum eigenvalue of the matrix . Then:

| (77) |

where the expectation is taken over the realizations of the erasure matrix of (26).

Proof:

With , Markov’s inequality readily yields:

| (78) |

For the leftmost inequality, a second application of Markov’s inequality then gives

| (79) |

and our claim follows by noting that . ∎

Remark.

The above inequalities provide bounds for in terms of the averaged integrated density of states of evaluated at . At first sight, these inequalities seem quite loose: indeed, for large and fixed , the RHS of (77) may exceed , so the rightmost inequality becomes trivial. Nevertheless, we will be interested in the case where and are such that , and we will argue at the end of the section that the rightmost inequality of (77) becomes tight in this case. Hence, for large but finite , the instability probability will be proportional to with the proportionality constant depending only on .

In light of the above, we are left to calculate for large , a quantity which we will approximate with for large (see Appendix B for a justification of this approximation). This last quantity has a long history in statistical physics: in his study of the electronic properties of dirty semiconductors, Lifshitz conjectured the correct form of the density of eigenvalues close to the edge of the spectrum using a truly insightful argument based on the size of regions that are free of impurities [33]. Subsequently, a large corpus of sophisticated mathematical techniques has provided a formal footing for the method (see e.g. [34, 35, 36, 37, 38, 26] and references therein), and our instability analysis follows from applying these techniques to our random network model with erasures viewed as impurities:

Theorem 3.

Let be the integrated density of states of the Hamiltonian matrix of the random network model (32). Then

| (80) |

or, equivalently:

| (81) |

where

-

a)

is the dimensionality of the network;

-

b)

is the erasure probability;

-

c)

denotes the system’s effective pathloss exponent as given by (22);

-

d)

the leading order coefficient is given by (23);

-

e)

the quantity is defined as

(82) where is the lowest Dirichlet eigenvalue (over ) of the linear operator:

(83) i.e. the infinitesimal generator of a standard Brownian motion on for , or of a symmetric stable process of order for . In particular, for , we will have:

(84) where is the first zero of the -th order Bessel function .

The convergence of to then gives:

Corollary 2.

With notation as in Theorem 3, the integrated density of states in a random network of size satisfies

| (85) |

with probability approaching one as .

Remark.

Just as the Laplacian operator is the infinitesimal generator of a standard Brownian motion in , the operator denoted as is the infinitesimal generator of a -dimensional symmetric stable process of degree [39]. Despite its similarity with the Laplacian, it is not a local operator and can be expressed equivalently as [40] (see also Appendix C)

| (86) |

The proof of Theorem 3 is quite technical, so we defer it to Appendix B; instead, in the remainder of this section, we will provide a qualitative analysis based on Lifshitz’s original approach and the related analysis of Section III for . Lifshitz’s key insight was to realize that very low eigenvalues close to the minimum of the spectrum become exceedingly rare because they correspond to large regions without impurities (erasures) – this is so because erasures create kinks in the corresponding eigenfunctions, and these tend to increase the eigenvalue. In this way, the measure of eigenvalues below a given low eigenvalue becomes dominated by the probability of having an erasure-free region in the system such that is the minimum eigenvalue in , i.e.

| (87) |

where the dependence of on is to be determined.

At the boundary of , the corresponding eigenfunction vanishes due to the appearance of erasures, so the eigenvalues within this region can be evaluated by diagonalizing in . From (19), we know that the eigenvalues of close to the minimum one will be

| (88) |

Hence, by dimensional analysis, the value of for the minimum eigenvalue must be proportional to the inverse of the (effective) radius of , implying that scales as .777The exact meaning of will become apparent later, but for simplicity we take to be the only characteristic lengthscale of the domain .

This conclusion can be reached independently by noting that the discrete operator can be approximated for large by the Laplacian; indeed, for any , we will have:

| (89) |

where denotes the -th element of , stands for the power at transmitter located at in , and (for more details about this continuum approximation, see Appendix C). We thus obtain

| (90) |

with the proportionality constant depending on the shape of . Thus, in order to obtain the maximum of (87), we need to minimize this constant.

This can be accomplished by means of the well-known Rayleigh–Faber–Krahn inequality [41], which states that the lowest Dirichlet eigenvalue of the Laplacian over a domain with fixed volume is minimized when the domain is a -dimensional ball; equivalently, for a fixed value of , this isoperimetric principle implies that the minimal erasure-free domain (and hence the most probable one) will be a -dimensional ball. The relationship between the minimum eigenvalue and the radius of this ball can then be evaluated by solving the eigenvalue problem with Dirichlet boundary conditions . By doing just that, we obtain:

| (91) |

with given by (84) [42]. In this way, Lifshitz was able to obtain the following asymptotic expression for the cumulative density of eigenvalues (correct to exponential accuracy):

| (92) |

This result coincides with (80) for ; by contrast, it is worth recalling that the cumulative density of eigenvalues for the pure system vanishes asymptotically as – cf. (20).

Remark 1.

To illustrate the exponential sensitivity of the above result to the occurrence of even a small number of erasures in the domain , it is helpful to revisit the one-dimensional case of the Wyner model and estimate the probability of occurrence of the eigenvalue . In the absence of erasures the minimum eigenvalue of a segment of length is . The appearance of even a single erasure, for simplicity in the center of the segment, increases the eigenvalue of this region to roughly . Hence, such an event with approximately the same probability will contribute to the eigenvalue density at a much higher value, where a region of size which exponentially more probable. Hence, such events with few erasures inside the region of interest are negligible.

Remark 2.

We can use the Wyner model to also show why is dominated (to leading exponential order) by the occurrence of an erasure-free disc with minimum eigenvalue rather than its higher eigenvalues. As we saw above, one way that this eigenvalue can occur is when an erasure free region of length appears, where . This event occurs with probability of the order of . However, can also occur in a size of the erasure-free region as the second lowest eigenvalue such that . This means that , so the probability of occurring as the second lowest eigenvalue is exponentially small compared to the case where is the lowest eigenvalue.

Remark 3 (Accuracy of the IDS approximation).

An important byproduct of this analysis is that in the low eigenvalue regime, an eigenvalue appears only when an erasure-free region with volume roughly equal to occurs in the sample (recall that is such that the minimum eigenvalue of the Laplacian over is ). Also, since the eigenfunction of such an eigenvalue is localized within , it will not depend on the random disorder beyond this region. Therefore, since such erasure-free regions appear randomly and independently in the system, we may estimate the probability in (73) by assuming that there are independent regions in the system, in each of which the probability that appears is of the order of . As a result,

| (93) |

where is a power-law function of , which does not depend on . As a result, when , we conclude that

| (94) |

corroborating the tightness of the upper bound in (77).

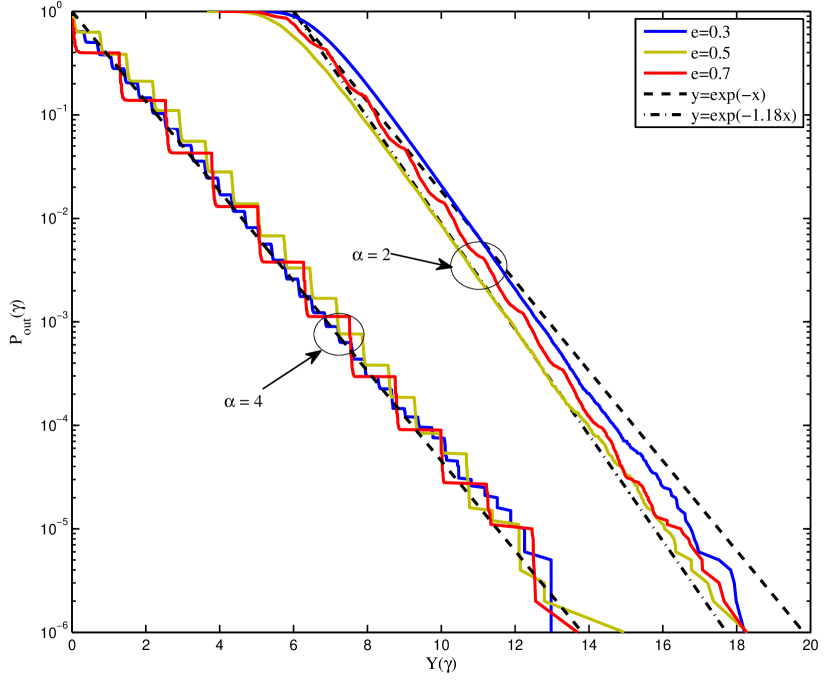

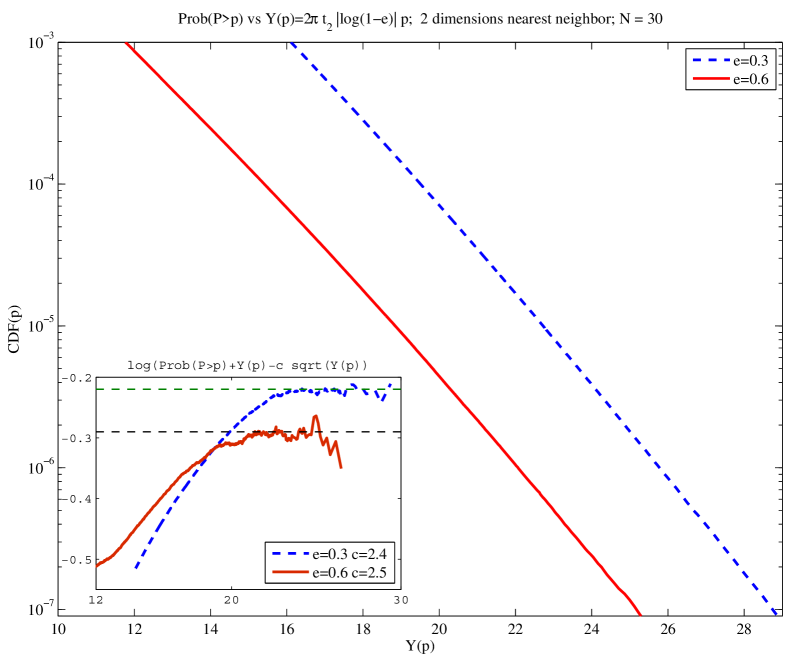

V-C Numerical validation in finite networks

We now turn to the numerical validation of our stability analysis for finite networks. As discussed above, the instability probability corresponds to the probability that the minimum eigenvalue of the system is less than (Theorem 1). To obtain a better comparison with our theoretical predictions, it will be convenient to introduce the parameter

| (95) |

which corresponds to the function of that appears in (80). Thus, for our numerical simulations to be consistent with Theorem 3, the plots of against for different values of must be concentrated around parallel lines with negative unit slope (the axis intercept is irrelevant).

Fig. 5 presents our simulations for one-dimensional networks and demonstrates remarkable agreement with Theorem 3. Just as in the case of the Wyner model (Fig. 2), the jump discontinuities that appear in the numerically calculated IDS are due to the fact that the cumulative eigenvalue density of the system is not Hölder continuous to any order in the limit [26, 25]. Finally, the plots corresponding to the long-range interaction regime also show excellent agreement with our theoretical predictions.888The exact value of for has not been calculated analytically, but is known to lie between and [43].

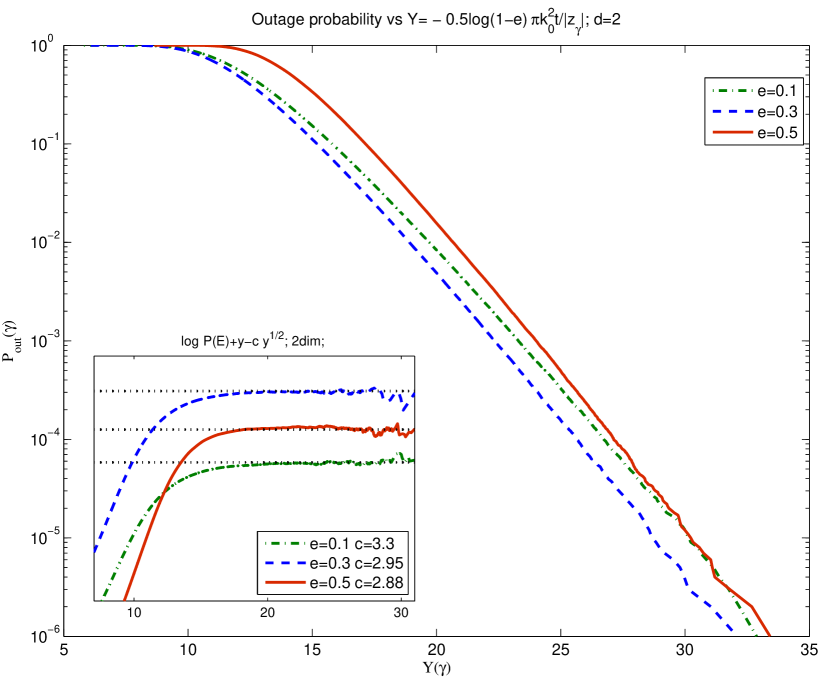

Fig. 6 presents our simulations for -dimensional networks for three different values of the erasure probability . For simplicity, we only simulated the case where only nearest neighbors interfere each other. In this case, although the plots look straight, the convergence to the theoretical exponent is not so obvious. One important reason is that the rare regions of interest are now -dimensional and hence susceptible to shape fluctuations that can be significant when the radii are not sufficiently large. In fact, based on the analysis of [44], these surface fluctuations introduce a subleading correction in the exponent of the cumulative density of eigenvalues which is of order , where is given in (91), i.e.

| (96) |

for some constant . Importantly, this last term does not appear for ; on the other hand, for , it introduces a subleading correction of order in (80) which can be significant if is not sufficiently small. In the inset of Fig. 6 we have subtracted such a term from the exponent and fitted the coefficient , obtaining asymptotic convergence to our theoretical predictions for small .

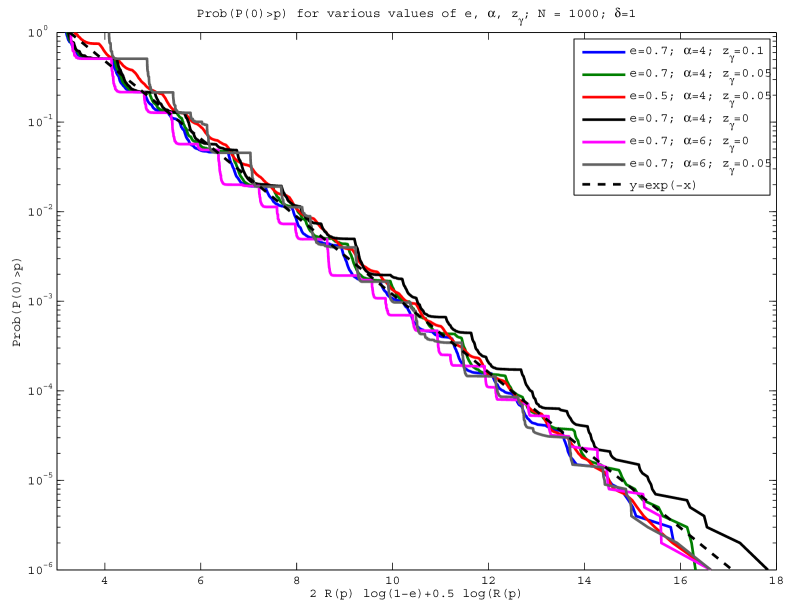

VI Tails of the power distribution

Having analyzed the instability probability for finite random networks generated by (32) in the supercritical regime , we now turn to the tails of the power distribution for . This analysis is complementary to that of Section IV where we calculated the “bulk” statistics of the optimal power vector; indeed, the importance of analyzing the tails of the power distribution lies in that they serve as an alternative outage criterion: since the available power at each transmitter is bounded, transmitters with assigned powers higher than their maximum power will effectively be in outage.

In this section, we will present a lower bound for the tails of the power distribution using the intuitive approach of the previous section, and we will argue that this lower bound becomes tight for large powers – an assertion backed by our numerical simulations and the discussion of the Wyner model in Section III. On the other hand, establishing an upper bound is significantly more difficult: using arguments from percolation theory, we obtain a tight upper bound for the power distribution when interference is only caused by nearest neighbors and the erasure probability exceeds a critical value derived from an associated bond percolation model. This approach however does not apply when the erasure probability is low, leaving a gap between the lower and upper bounds in this regime. Nevertheless, we conjecture that the scaling obtained through the lower bound is tight: in fact, as has been emphasized by Pastur for the case of the integrated density of states, the lower bounds obtained with our methodology capture the correct behavior in all known cases [26].

VI-A A lower bound for the tails of the power distribution

We will begin by presenting a lower bound for the tails of the power distribution in the short-range regime . To that end, recall that the fraction of sites with power exceeding some value in a large network may be seen as the probability that the optimal power at the origin exceeds , i.e.

| (97) |

We will thus say that a connected domain supports power at when a) ; and b) for allrealizations of the erasure matrix such that is erased while remains erasure-free (i.e. on and on ). Of course, if is sufficiently large, arbitrarily small domains containing cannot support power at : if is small enough and every site outside is erased (i.e. not transmitting), no point in will have high optimal transmitting power. Clearly then, if denotes the number of sites contained in , there exists some minimal value such that does not support power at if . Therefore, if is a domain supporting power at with minimal volume , we will have

| (98) |

so the problem boils down to determining the minimal volume which supports power at .999Interestingly, even though the lower bound (98) appears lax for arbitrary , it tightens considerably for large . Indeed, when is large, only very large domains can support power , and the minimal volume will be exponentially more probable to occur than larger erasure-free volumes; as a result, the leading contribution to from erasure-free domains will be coming from .

Since we are interested in large powers for , we will focus on large domains . In Section V-B we related the volume of an erasure-free domain to the minimum eigenvalue of the Dirichlet Laplacian over the domain; here, we need to relate it instead to the maximum power that can be supported therein. In Appendix D-A we will provide details to the proof of the following proposition:

Proposition 1.

Let and . Then, for large :

| (99) |

where is the volume of the unit -dimensional ball and is given by

| for , | (100a) | ||||

| for , | (100b) | ||||

where is the -th order modified Bessel function of the first kind and . In particular, for , we will have:

| (101) |

where

| for , | (102a) | ||||

| for . | (102b) | ||||

VI-B An upper bound for nearest neighbor interactions

We now provide an upper bound for the tails of the empirical power distribution summarized in Proposition 2. Technically, it only applies to the random network model where interference arises only from nearest neighbor interactions. In the one dimensional case, this corresponds to the Wyner model discussed in Section III for which, as mentioned above, the lower bound is indeed tight. In the two dimensional case, we can also obtain a matching upper bound for the tails of the power distribution by using a site percolation argument (see Appendix D):

Proposition 2.

By combining (101) and (103) for the case , we then obtain the following growth estimate for the tails of :

Corollary 3.

VII Long-term behavior of the power control dynamics

So far, our analysis has focused on the statistical properties of the optimal power vector in (5), as well as the conditions under which this vector (and power control in general) is feasible. In Section II-A we also discussed the Foschini–Miljanic power control algorithm (6) which provably converges to – assuming that is itself feasible – i.e. that . Two related obvious questions which arise are the following:

-

(a)

If the system is feasible (i.e. ), what is the rate of convergence of the power control dynamics (6) in the presence of random erasures?

-

(b)

On the other hand, if , how long does it take for the powers in the network to start becoming very large?

To answer these questions, we will first analyze the solution of the Foschini–Miljanic power control dynamics with for finite : in the limit , this solution will converge to the actual vector with erasures at the sites with in (26). Beginning with the subcritical case , let ; then:

| (105) |

Without loss of generality, we may focus on the origin ; thus, projecting to the -th element of , we obtain:

| (106) |

In the limit , the LHS of this expression converges to which is the quantity we are interested in. Since , if the initial powers of the sites are bounded, the elements of will also be bounded for all ; hence, since , we will also have for some , leading to

| (107) |

Taking the average of the above expression and the limit we get

| (108) |

where is the average number of distinct sites visited by a random walk generated by up to time – cf. (142). As a result, our analysis in Appendix B gives

Proposition 3 (Asymptotic behavior for subcritical ).

We demonstrate the tightness of the above inequality in a couple of cases. First, assume that all initial powers are greater than (which itself is an upper bound for the elements of ), so all elements in are positive. Denoting with the minimum of all elements of , we will have

| (110) |

Corollary 4.

If , the inequality in (109) becomes an equality, i.e.

| (111) |

The same can be shown when has zero elements and hence for finite . In the limit , the minimum of this vector will be zero; that said, the operation of will project out such terms, so this issue does not make a difference. Therefore, in this limit, the inequality (110) will hold for , where is the maximum eigenvalue of . We therefore expect that the equality in (111) should be tight in general.

As a result of the above discussion we see that the timescale at which the system converges to its optimal vector is for . It interesting to compare this timescale with the corresponding one at which an infeasible system with becomes unstable, that is the powers of the system become very large. For concreteness, we will focus on the case where where we can make precise quantitative statements. To that end, it will be more convenient to express the solution of (7) in the form

| (112) |

where and correspond to the two terms in the top line. Taking the average over realizations and evaluating the element at in the infinite size and limits, will be bounded by , where and are the minimum/maximum values of the elements in , respectively. The resulting integrand in the second term above can then be expressed as . For large times , so the integral may be approximated by

| (113) |

where is the solution of the equation .

This result can also be obtained by an asymptotic evaluation of the integral of the asymptotic expression of the integrand. To do this, one only needs to bound the small time behavior of the integrand (where its approximate expression is not valid) and to control in a similar way the leading correction to the asymptotic expression of . Doing just that, we obtain:

Proposition 4 (Asymptotic behavior for supercritical ).

Remark.

The above result shows that the characteristic time over which an infinite infeasible system becomes unstable is given by . This time for small can be much larger than .

VIII Conclusions

In this paper we studied the optimal power vector that achieves an SINR target criterion in the presence of both randomness and interference. In particular, we derived the statistics of the optimal power vector and the long-term behavior of the Foschini–Miljanic power control algorithm [5] in the presence of random erasures. This was made possible by mapping the problem of power minimization in the presence of nonlinear SINR constraints to the so-called Anderson impurity model which can be analyzed by studying random walks in a lattice with randomly placed traps.

Drawing tools and ideas from statistical physics, we calculated the average power and the variance of the optimal power vector by means of the coherent potential approximation (CPA) approach, a method originally introduced in the study of disordered metals. Despite the method’s approximative nature, our results are fairly accurate over a wide range of parameters for the erasure density in the network and the users’ target SINR value ; on the other hand, the CPA method fails to predict the infeasibility of power control in the system when the users’ target SINR exceeds a certain critical value. To calculate the probability of the system becoming unstable, we then employed a different set of mathematical tools in order to calculate the low eigenvalue density of the random system. Remarkably, the same tools also allowed us to estimate the tails of the power distribution under power control, thus obtaining a complementary outage criterion for networks with power-limited transmitters. In all cases, our predictions for the system’s instability probability and its large power tail behavior were confirmed by numerical simulations. Finally, we calculated the average long-term behavior of the Foschini–Miljanic power control algorithm in the presence of random erasures, and we showed that its rate of convergence exhibits nontrivial time-dependencies.

Summing up, we have found that approximate methods (like CPA) provide good quantitative results for quantities related to bulk properties of the system (such as the intra-sample average of the optimal power vector or its variance). Nevertheless, rare events (such as instability or the occurrence of atypically large powers in the optimal power vector) are conditional on the appearance of large regions with no inactive transmitters. These regions are then responsible for the breakdown of the whole system, so our analysis focused on estimating the probability of observing such erasure-free regions.

We believe that the results (and insights) obtained in this paper regarding tail events may be applied to significantly more general network models. For example, the probability that a finite-sized network can become infeasible may be approximated by the probability of occurrence of large regions of a given critical size with closely packed users. Due to the size of the paper however, we decided not to present applications of these methods to specific situations, but to defer them instead to a future paper.

Appendix A Derivation of the CPA equations

In this appendix we will motivate the derivation of the CPA equations applied in Section IV; the interested reader can find more information on the method in [13, 14] and references therein.

Specifically, our aim will be to calculate the average resolvent operator (61). Unfortunately, methods from random matrix theory cannot be applied here directly because the random matrix is diagonal (nevertheless, the end results will end up being related). As such, the main idea behind CPA is to replace the random matrix in the resolvent operator with a constant diagonal matrix so that the difference is “small” if we pick in the right way.101010This assumption is correct for full random matrices, but only approximately so for diagonal random matrices .

We thus start by defining the matrix

| (116) |

where is the resolvent operator in the absence of disorder:

| (117) |

The matrix can then be expressed as

| (118) |

where the so-called scattering matrix is defined as

| (119) |

Up to this point everything is exact, and by expressing (119) recursively and averaging over (in ) we can obtain . This could be plugged into (A) to obtain , but this is an impossible task in general. On the other hand, if we assume that is small, we may expect that the second term in the last equation will also be small on average. The CPA approach amounts to averaging over the randomness of a single random site and demanding that the corresponding diagonal element of vanishes on average. Hence, it is an approximation which “hides” the effects of all other sites into and then reduces to a self-consistent single site problem. This somewhat obscure assumption leads to

| (120) |

where

| (121) |

is the (shifted) unperturbed resolvent operator evaluated at the -th site (the second equality follows from the fact that the eigenvectors of are Fourier modes).

Appendix B Derivation of the integrated density of states

Our aim in this appendix will be twofold: First and foremost, we seek to derive the low-energy asymptotic expressions (80) for the IDS of the disordered Hamiltonian matrix in the large lattice limit . This will provide an approximation for the integrated density of eigenvalues for a large finite system, which will then be used to approximate the instability probability in Section V-B. In so doing however, we will also provide the necessary tools that are required in Section VII to estimate the long-term behavior of the Foschini–Miljanic power control dynamics (6).

In a nutshell, our approach will be as follows:

- 1.

-

2.

In Section B-2, we will derive the IDS of in the large system limit by exchanging the limits and : specifically, by working in the infinite system where and are viewed as infinite-dimensional operators (instead of as matrices of order ), we will harvest the integrated density of states of from the density of by taking the limit .

-

3.

To calculate , we will take the Laplace transform of and express it as a Feynman–Kac path integral over a random walk in with transition probabilities determined by (Section B-3).

- 4.

- 5.

-

6.

Finally, in Section B-6, we obtain the small behavior of by inverting the Laplace transform for large .

In what follows, we will make this roadmap precise by encoding each step in a series of lemmas.