Comparative statistics of Garman-Klass, Parkinson, Roger-Satchell and bridge estimators

S. Lapinova, A. Saichev

National research University “Higher school of economics”, RussiaETH Zurich – Department of Management, Technology and Economics, Switzerland

Abstract

Comparative statistical properties of Parkinson, Garman-Klass, Roger-Satchell and bridge oscillation estimators are discussed. Point and interval estimations, related with mentioned estimators are considered

1 Examples of volatility estimators

Consider dependence on time of the price of some financial instrument. As a rule, at discussing of volatility, one consider its logarithm

Let point out one of the conventional volatility definition, which we are using in this paper: It is the variance

(1)

of the log-price increment

within given time interval duration .

Recall, Garman-Klass (G&K) [1], Parkinson (PARK) [2] and Roger-Satchell (R&S) [3] volatility estimators are resting on the high and low values:

(2)

Accordingly, PARK estimator is equal to

(3)

while G&K estimator given by expression

(4)

Here is the close value of the log-price increment.

Recall else R&S estimator, equal to

(5)

Besides of mentioned well-known estimators, we discuss bridge oscillation estimator. Below we call it shortly by bridge estimator. Before to define it, recall bridge stochastic process definition. It is equal to

(6)

Let introduce high and low of the bridge:

(7)

Accordingly, mentioned above bridge volatility estimator given by

(8)

The value of the factor will be calculated later.

2 Geometric Brownian motion

One of conventional models of price stochastic behavior is geometric Brownian motion (see [4, 5, 6]). In particular, it is used in theoretical justification of G&K, PARK and R&S estimators. Below we discuss statistics of mentioned volatility estimators in frame of geometric Brownian motion model. Namely, we assume that increment of the log-price is of the form

(9)

Here is the drift of the price, while is the standard Brownian motion .

Factor is the intensity of the Brownian motion.

Recall, Brownian motion posses by self-similar property

(10)

where and below sign means identity in law.

Using pointed out self-similar property, one can ensure that

(11)

Henceforth we call process by canonical Brownian motion, while factor by canonical drift.

Using relations (3), (4), (8) and (11), one find that

We have used above canonical estimators:

(12)

containing high, low and close values

(13)

of canonical Brownian motion, and high and low values

(14)

of the canonical bridge

(15)

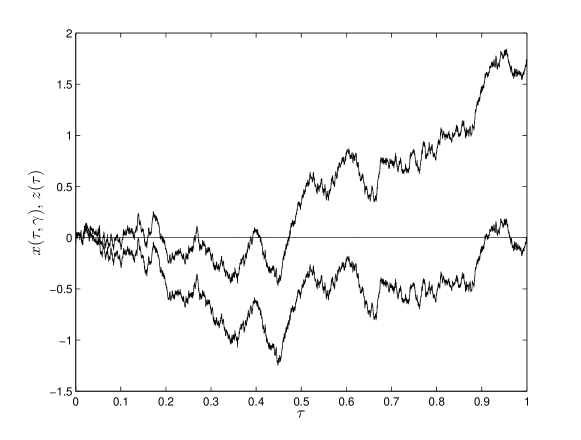

Plots of the typical paths of the canonical Brownian motion (11) for and corresponding canonical bridge (15) are given in figure 1.

Figure 1: Typical paths of canonical Brownian motion (11) for and corresponding canonical bridge (15)

It is worthwhile to note that the closer expected values of canonical estimators , , and to unity, the less biased corresponding original volatility estimators. Analogously, the smaller variances of canonical estimators the more efficient original volatility estimators , , and .

Notice additionally that canonical drift of the canonical Brownian motion (11) is, as a rule, unknown. Nevertheless, to get some idea about dependence on drift of bias and efficiency of volatility estimators, we will discuss below in details dependence of canonical estimators statistical properties on possible values of the factor .

3 Comparative efficiency of PARK and bridge estimators

Resting on, given at Appendix, analytical formulas for probability density functions (pdfs) of random variables (13) and (14), we explore in this section some atatistical properties of canonical PARK estimator and bridge one (12).

Let check, first of all, unbiasedness of canonical PARK estimator. To make it, let calculate, with help of pdf (A.7), mean square of oscillation of the canonical Brownian motion at the zero canonical drift (). After simple calculations obtain

(16)

From here and from expression (12) of canonical PARK estimator one can see that the following expression is true

Let find now the factor at expressions (8) and (12). To make it, calculate first of all the mean square of the bridge oscillation. Due to expression (A.9) for the bridge oscillation (12) pdf, one have

Accordingly, unbiased canonical bridge estimator has the form

(17)

The great advantage of the bridge estimator is its unbiasedness for any drift. This remarkable property of the pointed out estimator is the consequence of the fact that bridge (6) and its canonical counterpart don’t depend on the drift (canonical drift ) at all. On the contrary, PARK estimator becomes essentially biased at nonzero drift. In figure 2 depicted dependence on of canonical PARK estimator expected value, illustrating bias of PARK estimator at nonzero drift. Corresponding curve obtained with help of analytical expression (A.6) for canonical bridge oscillation pdf.

Figure 2: Plot of canonical PARK estimator

mean value, as function of canonical drift . It is seen that with growth of PARK estimator becomes more and more biased. Straight line is the plot of canonical bridge , mean value

Let calculate variances of canonical PARK and bridge estimators. After substitution into the rhs of expression

the sum (A.7) for the canonical Brownian motion oscillation pdf , and after summation obtain for :

Accordingly, variance of canonical PARK estimator is

(18)

As the next step, we calculate variance of canonical bridge estimator (17). Sought variance is equal to

After substitution here, following from (A.9), relation

obtain

(19)

Comparing equalities (18) and (19),

one can see that variance of bridge estimator approximately twice smaller than variance of PARK estimator.

Recall, variance of bridge estimator does not depend on drift. On the contrary, variance of PARK estimator essentially depends on the drift. One can see it in figure 3, where depicted plot of dependence, on canonical drift , of canonical PARK estimator variance.

Figure 3: Plots of dependence on of canonical PARK estimator variance. Straight line is the variance of canonical bridge estimatorFigure 4: Plot of relative bias (20) of canonical PARK estimator as function of canonical drift

Notice else that bias of some estimator is insignificant only if it is

much smaller than rms of corresponding estimator, i.e. is small the relative bias:

(20)

Plot of canonical PARK estimator relative bias, as function of canonical drift depicted in figure 4.

4 Interval estimations on the basis of PARK and bridge estimators

Given at Appendix analytical expressions (A.6), (A.7) and (A.9) for canonical Brownian motion and canonical bridge random oscillations pdfs allow us to explore in details probabilistic properties of PARK and bridge canonical estimators. Let find, at first, pdfs of mentioned canonical estimators random values. It is well known from Probabilistic Theory that pdf of canonical PARK estimator is expressed through pdf (A.6) of canonical Brownian motion oscillation by the relation

(21)

Similarly, pdf of canonical bridge estimator is equal to

(22)

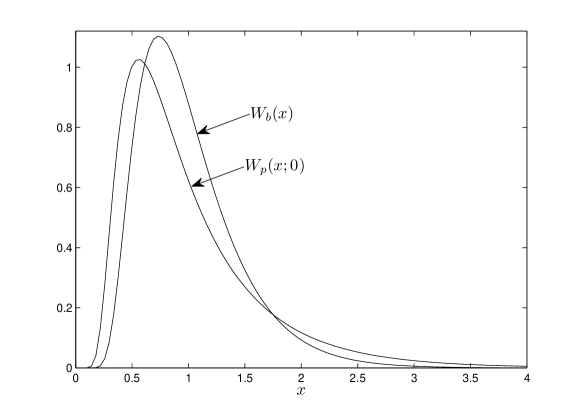

Here (A.9) is the pdf of canonical bridge oscillation. Plots of canonical PARK estimator pdf, for , and pdf of canonical bridge estimator are depicted in figure 5. In figure 6 are comparing pdfs of canonical PARK estimator, for , and pdf of canonical bridge estimator. It is seen in both figures that pdf of canonical bridge estimator is better concentrated around its expected value than canonical PARK estimator pdf.

Knowing estimators pdfs, one can produce interval estimations of possible volatility values. Consider typical interval estimation:

Let is some volatility estimator, equal to

(23)

Here is corresponding canonical estimator, while is the measured volatility. One needs to find probability

that unknown (random) volatility is not more than times exceeds known (measured) volatility estimated value .

It follows from (23) that following inequalities are equivalent:

Last means in turn that sought probability is expressed through pdf of canonical estimator by the following way:

(24)

Here is the pdf of canonical estimator .

Figure 5: Plots of canonical PARK and bridge estimators pdfs, clearly demonstrating “probabilistic preference” of bridge estimator in compare with PARK oneFigure 6: Plots of PARK and bridge canonical estimators pdfs for

Calculations, resting on relations (21), (22), (24) give probability that true volatility is less than twice of given bridge volatility estimator value . It is substantially larger than analogous probability in the case of PARK estimator:

.

Plots of probabilities (24) dependence on the level , for PARK estimator (in the case of zero drift ) and for bridge volatility estimator are given in figure 7.

Figure 7: Plots of probabilities and that true volatility is less than times exceeds values of PARK and bridge estimators

5 Comparative statistics of canonical estimators

Above, we explored in detail statistical properties of two, PARK and bridge estimators. Here we compare their statistics and statistics of another well-known volatility estimators: G&K and R&S one. Despite to previous chapters, where we have used known analytical expressions for pdfs of canonical PARK and the bridge estimators, below we use predominantly results of numerical simulations.

Namely, we produce numerical simulations of random sequences

(25)

where are iid Gaussian variables . Notice that stochastic process of discrete argument rather accurately approximates, for large , paths of canonical Brownian motion (11).

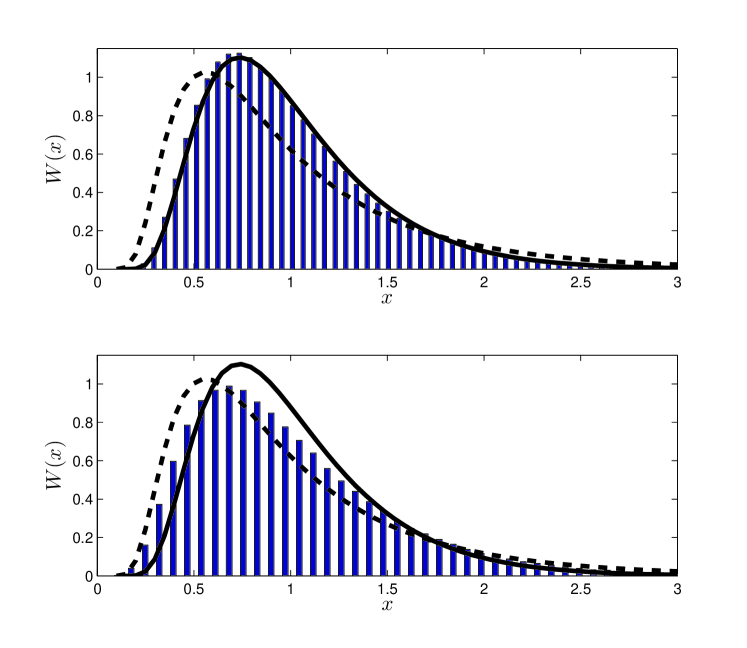

Figure 8: Upper panel: Histogram of samples of canonical bridge estimator . Solid line is the plot of canonical bridge estimator’s pdf, given by analytical expression (22), (A.9). Dashed line is the pdf of canonical PARK estimator for .

Lower panel: Histogram of samples of canonical G&K estimator for . Solid line is the plot of the canonical bridge estimator pdf. Dashed line is the canonical PARK estimator pdf for

Knowing iid sequences one can find corresponding iid samples of pointed out above canonical estimators. Everywhere below we take number of iid samples and discretization number equal to

Plots in figure 8 demonstrate rather convincingly accuracy of numerical simulations. In figure 9

are given two hundred samples of canonical G&K and bridge estimators, ensuring “by naked eye” that canonical bridge estimator is more efficient than G&K one.

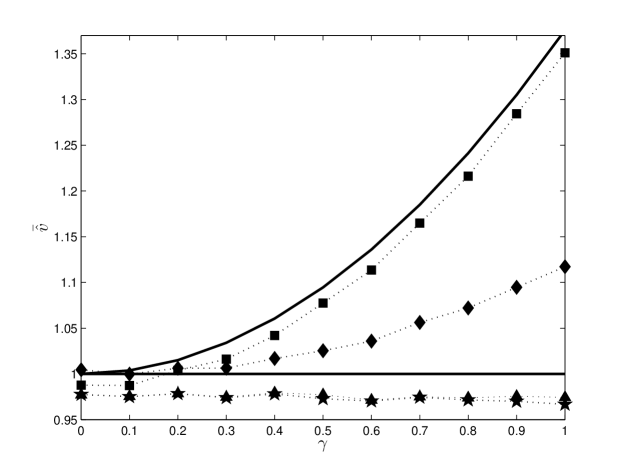

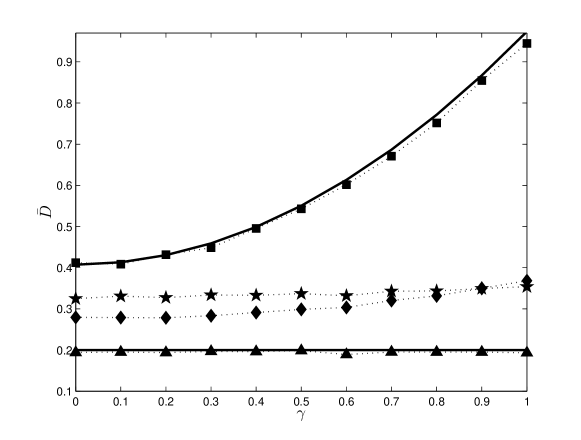

In figure 10 are given, obtained by numerical simulations, plots of canonical G&K, PARK, R&S and bridge estimators mean values, illustrating bias of G&K and PARK estimators for nonzero canonical drift , and actual absence of bias for bridge and R&S estimators.

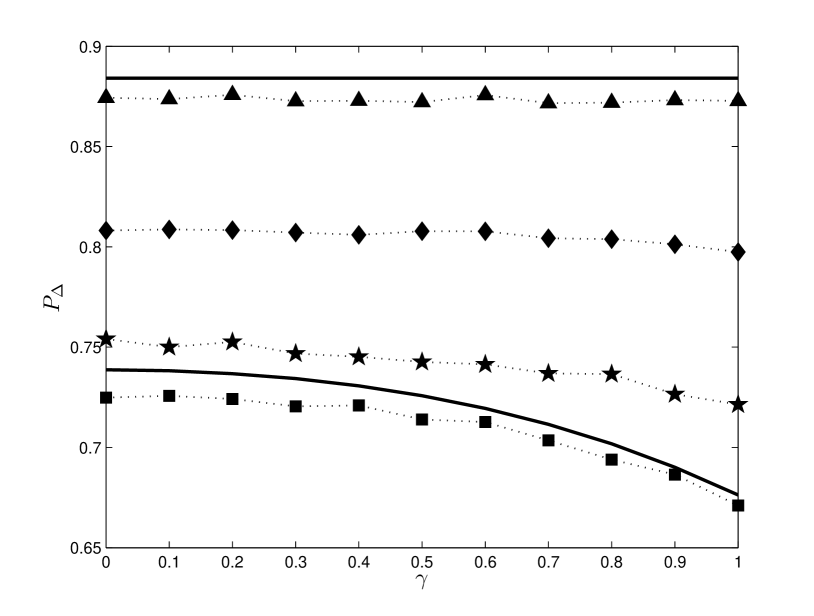

Eventually, in figure 12 are given plots of probabilities that true volatility is larger than half of corresponding estimator value and less than twice of it:

(26)

It is seen that for any mentioned probability is essentially larger for bridge estimator, than for G&K, R&S and PARK estimators.

6 Acknowledgements

We are grateful for scientific and financial help of Higher school of economics (Russia, Nizhny Novgorod) and Nizhny Novgorod State University (Russia).

Figure 9: Plots of two hundreds samples of canonical estimators. Up to down are samples of G&K, R&S, bridge and PARK estimators. It is seen even by “naked eye” that bridge estimator estimates volatility more accurately than another mentioned estimatorsFigure 10: Mean values of canonical PARK (), G&K (), R&S () and bridge () estimators.

Solid lines are theoretical expectations, borrowing from figure 2Figure 11: Estimations of variance of PARK (), R&S (), G&K () and bridge () canonical estimators. Solid lines are plots of theoretical variances, borroved from the figure 3. It is seen that for any bridge estimator’s variance significantly smaller than variances of another mentioned estimators Figure 12: Estimations of probability (26) at different values, for PARK

(), R&S (), G&K () and bridge () estimators. Solid lines are results of theoretical calculations, resting on formula (26)

References

[1]

Garman, M., and M. J. Klass. 1980. On the Estimation of Security Price Volatilities From Historical Data. Journal of Business 53: 67-78.

[2]

PARK, M. 1980. The extreme value method for estimating the variance of the rate of return. The Journal of Business 53: 61-65.

[3]

Rogers L. C. G., S. E. Satchell. 1991. Estimating variance from high, low and closing prices. The annals of Applied Probability 1: 504-512

[4]

Jeanblanc, M., M. Yor, M. Chesney. 2009. Mathematical Methods for Financial Markets. London: Springer Verlag.

[5]

Cont, R., P. Tankov. 2004. Financial Modelling With Jump Processes. London: CRC Press.

[6]

Saichev A., Ya. Malevergne, D. Sornette. 2010. Theory of Zipf’s Law and Beyond. Heidelberg: Springer Verlag.

[7]

Borodin, A. N., P. Salminen. 2002. Handbook of Brownian Motion – Facts and Formulae (Second Edition). Basel: Birkhäuser Verlag.

[8]

Saichev, A., D. Sornette. 2011. Time-Bridge Estimators of Integrated Variance.

arXiv:1108.2611v1 [q-fin.ST] 12 Aug 2011.

Appendix A Probabilistic properties of high, low and close values

Here are given pdfs of random variables (13) and variables (14), which one need for canonical estimators (12) statistical analysis.

Let begin with random variable . Obviously, its pdf is

It is easy to show, additionally, that joint pdf of high value (13) of canonical Brownian motion and the close value is equal to

Let write here explicit expression for joint pdf of random variables (13).

Using formulas, given at the monograph [7] and in the article [8], one might show that pointed out joint pdf given by:

(A.3)

Here is the unit step function, equal to unity for and zero otherwise. Besides, above there is function

(A.4)

We need, at exploring statistical properties of canonical G&K estimator, in joint pdf of canonical Brownian motion (11) oscillation and the close value . As it follows from (A.3), (A.4), mentioned pdf is equal to

(A.5)

After integration above joint pdf over all values obtain pdf of oscillation :

(A.6)

Here have used auxiliary function

In particular case of zero drift (), one get from (A.6) following expression

(A.7)

All statistical properties of high and low values (14) of canonical bridge (15) are defined by their two-fold joint pdf , given by relation

(A.8)

Following from here pdf of canonical bridge oscillation given by equality