Predatory trading and risk minimisation: how to (b)eat the competition

Abstract

We present a model of predatory traders interacting with each other in the presence of a central reserve (which dissipates their wealth through say, taxation), as well as inflation. This model is examined on a network for the purposes of correlating complexity of interactions with systemic risk. We suggest the use of selective networking to enhance the survival rates of arbitrarily chosen traders. Our conclusions show that networking with ’doomed’ traders is the most risk-free scenario, and that if a trader is to network with peers, it is far better to do so with those who have less intrinsic wealth than himself to ensure individual, and perhaps systemic stability.

1 Introduction

The topic of predatory trading and its links with systemic risk is of great contemporary interest: at the time of writing this paper, these links have been mentioned repeatedly in the World Economic Forum at Davos, in addition to having formed the backbone of the ’Occupy’ movements worldwide. Immense public anger has been expressed against corporate greed (with predatory trading forming a major way that this is manifested), and many intellectuals worldwide attribute this to the collapse of the world economic system. In this paper, we examine these ideas in a more technical way to see if rigorous mathematical links can be established between these two concepts.

In order to put our mathematical models in the context of current interdisciplinary literature, we quote the conclusions of two key papers. First we define predatory trading along the lines of a recent paper bp , as that which induces and/or exploits other investors’ need to ’reduce’ their positions. If one trader needs to sell, others also sell and subsequently buy back the asset, which leads to price overshooting and a reduced liquidation value for the distressed trader. In this way, a trader profits from triggering another trader’s crisis; according to the authors of bp , the crisis can spill over ’across traders and across markets’. To model this scenario, we invoke a model of predatory traders in the presence of a central reserve am_wealth , which is principally a source of wealth dissipation in the form of taxation. We assume that this dissipation acts uniformly across the traders’ wealth, irrespective of their actual magnitudes. Among our findings am_wealth is the fact that when all traders are interconnected and interacting, the entire system collapses, with one or zero survivors. This finds resonance with the ideas of another key paper haldane , where analogies with model ecosystems have led the authors to conclude that propagating complexity (via the increase of the number and strength of interactions between different units) can jeopardise systemic stability.

The original model luck_am on which am_wealth is based, was introduced as a model of complexity. It embodies predator-prey interactions, but goes beyond the best-known predator-prey model due to Lotka and Volterra by embedding interacting traders in an active medium; this is a case where the Lotka-Volterra model cannot be simply applied. As mentioned above, a central reserve bank represents such an active medium in the case of interacting traders, whose global role is to reduce the value of held wealth as a function of time am_wealth . This forms a more realistic social backdrop to the phenomenon of predatory trading, and it is this model that we study in this paper. In order to relate it to the phenomenon of systemic risk, we embed the model on complex networks watts ; albert ; these represent a compromise between the unrealistic extremes of mean field, where all traders interact with all others (too global) and lattice models, where interaction is confined to local neighbourhoods (too local). Many real world networks, in spite of their inherent differences, have been found to have the topology of complex networks rev_comnets ; soc_nets ; and the embedding of our model on such networks nirmal allows us to probe the relevance of predatory trading to systemic stability.

The plan of the paper is as follows. First, in Sec. 2, we introduce the model of interacting traders of varying wealth in the presence of a central reserve, and show that typically only the wealthiest survive. Next, in Sec. 3, we probe the effect of networks: starting with an existing lattice of interacting traders with nearest-neighbour interactions, we add non-local links between them with probability watts . Survivor ratios are then measured as a function of this ’wiring probability’ , as is increased to reflect the topologies of small world and fully random networks (). In Sec. 4, we ask the following question: can the destiny of a selected trader be changed by suitable networking? We probe this systematically by networking a given trader non-locally with others of less, equal and greater wealth and find indeed that a trader who would die in his original neighbourhood, is able to change his fate, becoming a survivor via such selective non-local networking. In Sec. 5, we provide a useful statistical measure of survival, the pairwise probability for a trader to survive against wealthier neighbours, i.e. to win against the odds. Finally, we discuss the implications of these results to systemic stability in Sec. 6.

2 Model

The present model was first used in the context of cosmology to describe the accretion of black holes in the presence of a radiation field archan . Its applications, however, are considerably more general; used in the context of economics am_wealth , it manifests an interesting rich-get-richer behaviour. Here, we review some of its principal properties luck_am .

Consider an array of traders with time-dependent wealth located at the sites of a regular lattice. The time evolution of wealth of the traders is given by the coupled deterministic first order equations,

| (1) |

Here, the parameter is called the wealth accretion parameter (modelling investments, savings etc) and defines the strength of the interaction between the traders and . The first parenthesis in the R. H. S of Eqn. 1 represents the wealth gain of the th trader, which has two components: his wealth gain due to investments/savings (proportional to ) modulated by dissipation (at the rate of ) due to e.g. taxation, and his wealth gain due to predatory trading (the second term of Eqn. 1), also modulated by dissipation (at the rate of ) in the same way. Notice in the second term, that the loss of the other traders corresponds to the gain of the th trader, so that each trader ’feeds off’ the others, thus justifying the name ’predatory trading’. The last term, , represents the loss of the th trader’s wealth through inflation to the surroundings; we will see that this term ensures that those without a threshold level of wealth ’perish’, as in the case of those individuals in society who live below the poverty line. Here and in the following we will use words such as ’dying’ or ’perishing’ to connote the bankruptcy/impoverishment, of a trader and conversely, ’life’ will be associated with financial survival, i.e. solvency.

A logarithmic time is introduced in the study for convenience. We define a scaled time , where is some initial time. Similarly, for convenience, we rescale wealth to be . Using the new variables, Eqn. 1 can be rewritten as,

| (2) |

where the primes denote differentiation performed with respect to .

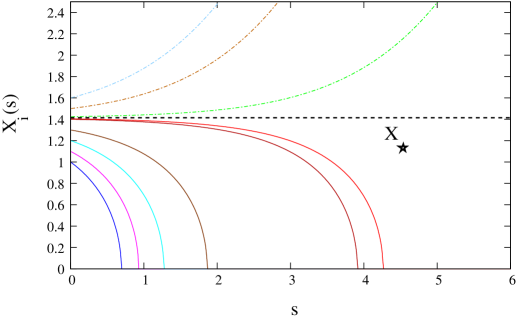

Continuing our recapitulation of the results of the model luck_am , we consider a scenario where there is a single isolated trader, whose initial (’inherited’) wealth is . Under the dynamics defined by Eqn. 2, the trader will survive financially only if (this imposes the condition luck_am ), else he will eventually go bankrupt (see Fig. 1). Next, consider a system of two traders with equal initial wealth; here, there exists a critical coupling such that for the two traders both survive, provided that their individual inherited wealth is greater than . For two unequally wealthy traders (, say), the poorer trader goes bankrupt first at time ; the richer one either survives (if his wealth at time , , exceeds the threshold ) or goes bankrupt (if ). The main inferences are twofold: the wealthier predatory trader ’consumes’ the poorer one’s wealth in due course, and then survives or not depending on whether his own wealth at that point is enough to tide him through its eventual dissipation through taxes and inflation. We thus see that this relatively simple model captures not just the mechanism of predatory trading, but also includes the flavour of more sophisticated concepts like inherited wealth, taxation and inflation.

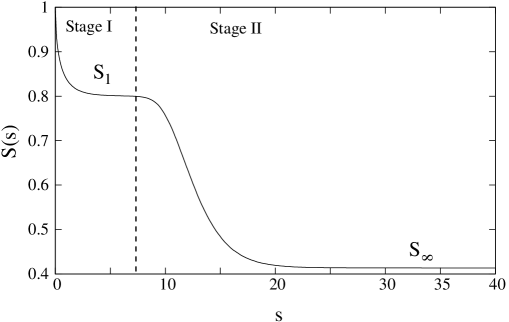

Consider the limit of an infinitely large number of traders all connected to each other; this represents a limiting mean field regime, with fully collective behaviour involving long-range interactions. For , all but the wealthiest will eventually go bankrupt. In the weak coupling regime () on the other hand, the dynamics consist of two successive stages luck_am . In Stage I, the traders behave as if they were isolated from each other (but still in the presence of the reserve); they get richer (or go bankrupt ) quickly if their individual wealth is greater (or less) than the threshold . In Stage II, slow, collective and predatory dynamics leads to a scenario where again, only the single wealthiest trader survives. This weakly interacting mean field regime shows the presence of two well-separated time scales, a characteristic feature of glassy systems book . The separation into two stages embodies an interesting physical/sociological scenario: the first stage is fast, and each trader survives or ’dies’ only on the basis of his inherited wealth, so that everyone without this threshold wealth is already eliminated before the second stage sets in. Competition and predatoriness enter only in the second stage, when the wealthier feast off their poorer competitors progressively, until there is only overlord left. This is a perfect embodiment of systemic risk, as the entire system collapses, with only one survivor remaining am_wealth .

Similar glassy dynamics also arise when the model is solved on a periodic lattice with only nearest-neighbour interactions. The dynamical equations in Eqn. 2 take the form :

| (3) |

by keeping the terms upto first order in luck_am . Here, runs over the nearest neighbours of the site , where for a one-dimensional ring topology, , while for a two-dimensional lattice – these are the two cases we consider here. We summarize earlier results luck_am on the dynamics: In Stage I, traders evolve independently and (as before) only those whose initial wealth exceeds the threshold , survive. In Stage II, the dynamics are slow and collective, with competition and predatoriness setting in: however, an important difference with the earlier fully connected case is that there can be several survivors, provided that these are isolated from each other by defunct or bankrupt traders (i.e. no competitors remain within their effective domain). Their number asymptotes to a constant (Fig. 2), and these ’isolated overlords’ survive forever. The moral of the story is therefore that in the presence of predatory dynamics, interaction-limiting ’firewalls’ can help avoid systemic collapse: conversely, full globalisation with predatory dynamics makes systemic collapse inevitable. Apart from providing quantitative support for the conclusions of haldane , this underscores the necessity of economic firewalls for the prevention of systemic risk cl .

Following the mean field scenario, where the wealthiest trader is the only survivor, it is natural to ask if this would also hold when the range of interactions is limited. Somewhat surprisingly, this turns out not always to be the case, with nontrivial and counter-intuitive survivor patterns being found often nirmal . While one can certainly rule out the survival of a trader whose initial wealth is less than threshold (), many-body interactions can then give rise to extremely complex dynamics in Stage II for traders with . This points to the existence of ways of winning against the odds to (b)eat the competition, when interactions are limited in range; in the remainder of this paper, we use selective networking as a strategy to achieve this aim.

3 Traders in complex networks

In this section, we examine the mechanisms of selective networking: a particularly interesting example to consider is the class of small-world networks. These have the property that long- and short-range interactions can coexist; such networks also contain ‘hubs’, where certain sites are preferentially endowed with many connections. Small-world networks can be constructed by starting with regular lattices, adding links randomly with probability to their sites watts and then freezing them, so that the average degree of the sites is increased for all .

|

|

|

|

3.1 One-dimensional ring and two-dimensional square lattices

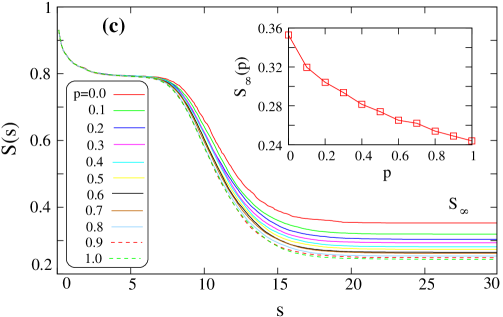

Consider a regular one-dimensional ring lattice of size . To start with, the wealth of the traders located on the lattice sites evolve according to Eqn. 3, where the interactions are with nearest neighbours only. Next, the lattice is modified by adding new links between sites chosen randomly with an associated probability . For , the network is ordered, while for , the network becomes completely random.

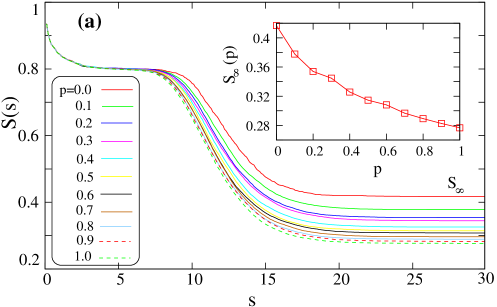

In the first scheme nirmal , we add links probabilistically starting with site and end with , only once: we call this the -cycle scheme. The survival ratios of traders as a function of reduced time for different values of wiring probability are presented in Fig. 3(a). Consider the case, which corresponds to a regular lattice; here the survival ratio shows two stages, Stage I and Stage II, in its evolution. For all values of , the existence of these well-separated Stages I and II is also observed. There is a noticeable fall in the survivor ratio as is increased, though; this is clearly visible in the asymptotic values plotted with respect to in the inset of Fig. 3(a). As increases, the number of links increases, leading to more interaction and competition between the traders, and hence a decrease in the number of survivors haldane . As expected, this behaviour interpolates between the two characteristic behaviours relevant to the regular lattice and mean field scenarios.

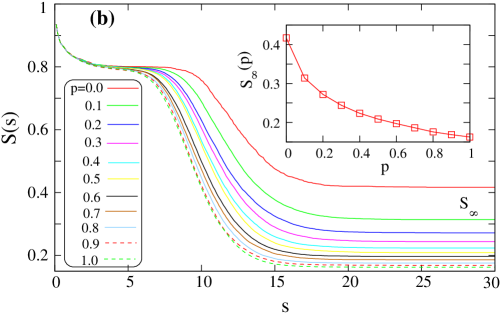

Next we implement the -cycle scheme nirmal , where the rewiring is done five times. Figure 3(b) shows the survivor ratio as a function of , where a clear decrease of for increasing . The asymptotic survival ratios for the - and -cycle schemes are shown in the insets of Fig. 3(a) and (b) respectively, with a clear decrease of as increases. In addition, the survivor ratio in the -cycle scheme is consistently smaller than in the -cycle scheme, for all .

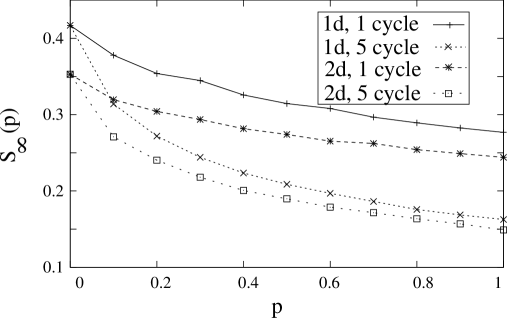

The above procedures are repeated for a two-dimensional square lattice of size nirmal , and survival ratios obtained as a function of for the - and -cycle schemes (see Figs. 3(c)-(d)). The asymptotic survivor ratios for these two cases are shown in the insets of Figs. 3(c)-(d); they follow a decreasing trend with increasing , similar to the case. Finally, we plot the asymptotic survival ratios of the - and -cycle schemes in and , in Fig. 4.

All the above simulations reinforce one of the central themes of this paper, that economic firewalls are good ways to avoid systemic collapse in a predatory scenario, since the more globalised the interactions, the greater the systemic risk haldane .

4 Networking strategies: the Lazarus effect

Since the central feature of this model is the survival of traders against the competition, it is of great interest to find a smart networking strategy which can change the fate of a trader, for example, by reviving a ’dying’ trader to life – we call this the Lazarus luke effect.

We systematically investigate the effect of adding a finite number of non-local connections to a chosen central trader. In nirmal , it was shown that the growth or decay of the wealth of a trader is solely dictated by its relative rate of change versus the cumulative rate of change of its neighbours’ wealth. The key to better survival should therefore lie in choosing to network with traders whose wealth is decaying strongly. We accordingly divide all possible non-local connections into two classes: class A comprises eventual non-survivors (), while class B comprises would-be survivors () ). In the next subsection, we look at the outcome of networking with members of class A.

4.1 Non-local connections with eventual non-survivors ()

Recall that non-survivors () die very early during Stage I. In connecting such traders to a given trader with , we can be sure that they will never be able to compete with him, much less run him out of business.

| (a) |

|

(b) |

|

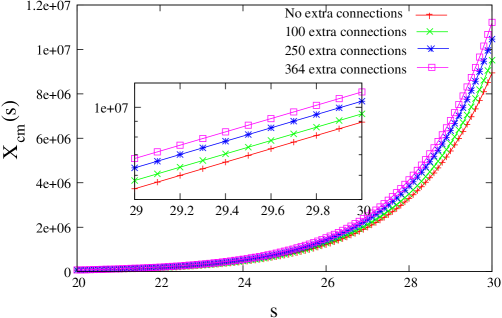

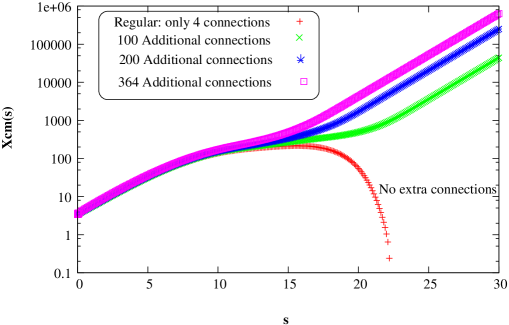

Let us consider a central trader who is an eventual survivor, as shown in Fig. 5. We now let him network with eventual non-survivors from all over the lattice, and record the growth of his wealth as a function of the number of traders in his network; the results are shown in Fig. 5 (b). When all the neighbours go out of business, their contribution in Eqn. 3 is zero, leading to the exponential solution shown in Fig. 5 (b). The wealth of the central trader increases markedly as more and more small traders are connected to him, making him an even wealthier survivor asymptotically.

| (a) |

|

|---|---|

| (b) |

|

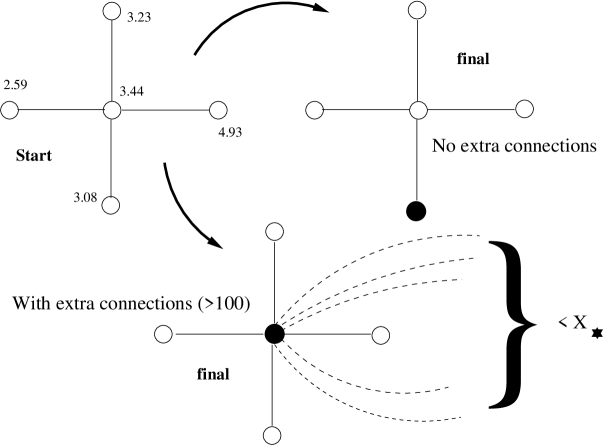

We now use this observation to return a ’dying’ trader to life. Figure 6 shows our results: the central trader would eventually have gone bankrupt in his original environment, but on adding small traders (whose wealth ) to his network, he comes back to solvency: further additions , e.g. or such traders, evidently make him an even wealthier survivor (Fig. 6 (b)). Thus, networking with eventual non-survivors is the surest way to invoke the Lazarus effect on a ’dying’ trader.

4.2 Networking with would-be survivors

Choosing to network with traders whose intrinsic wealth is greater than could turn out to be rather delicate. The financial lifespan of such traders will certainly exceed Stage I: and depending on their individual environments, they could either survive through Stage II with a positive growth rate, or die as a result of a negative growth rate. Networking with such traders is like playing Russian roulette.

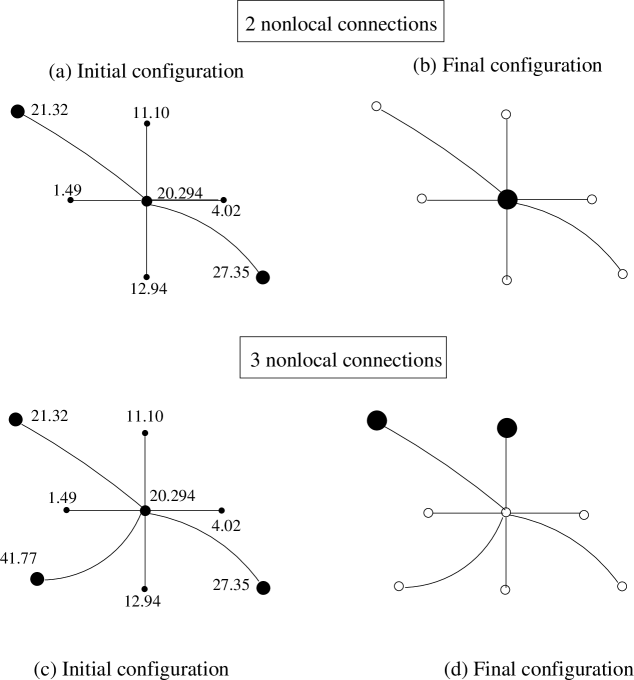

Consider first non-local connections with would-be survivors () who are poorer than our chosen trader (). Such would-be survivors will live beyond Stage I, their wealth showing at least initially a positive growth rate (Fig. 1). From a mean field perspective, we would therefore expect to see a decrease in the chances of survival of the chosen trader as it networks with more and more would-be survivors.

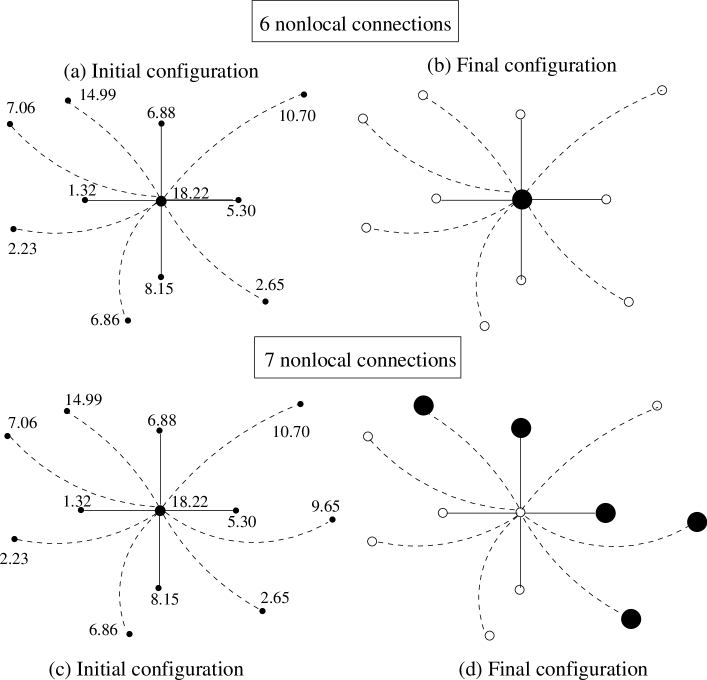

Figure 7 shows a sample scenario, where the central trader is connected non-locally with would-be survivors who are poorer than himself. In Fig. 7 (a) the central trader networks with 6 would-be survivors and is able to survive asymptotically (Fig. 7 (b) ). On the other hand, adding one more would-be survivor (Fig. 7 (c)) to the existing network of the central trader, causes him to go out of business at long times (Fig. 7 (d)). As the central trader is made bankrupt by the arrival of the new connection, the fates of some of his other links are also changed (cf. Figs. 7 (b) and (d)).

To understand the dynamics, we present the rates of growth for another sample scenario in Fig. 8. An increase in the number of non-local connections with would-be survivors, leads to a fall in the absolute value of as well as its rate of growth . Beyond a certain number of networked contacts, the wealth of the central trader begins to decay, and eventually vanishes. This crossover from life to death happens when the cumulative rate of the wealth growth of the neighbours is larger than that of the central trader . Unfortunately, however, the intricate many-body nature of this problem precludes a prediction of when such crossovers might occur in general.

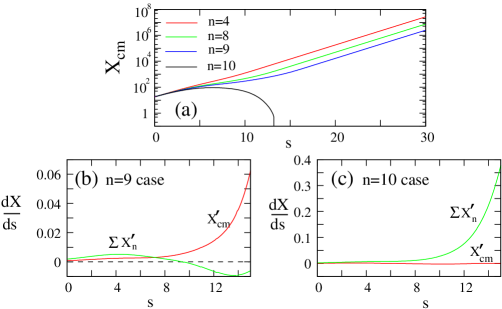

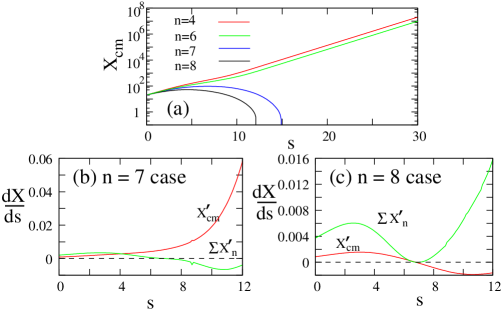

Finally, in the case where a given trader networks with would-be survivors who are richer than himself ( and ), one would expect a speedier ’death’. One such sample scenario is depicted in Fig. 9 and the corresponding rates of evolution of the traders’ wealth in Fig. 10. We notice that in his original configuration with four neighbours ()), the central trader is a survivor. As we increase the number of networked connections, the growth rate of his wealth gets stunted; there is a substantial fall for 2 extra links ( in Fig. 10). Adding one more link () does the final damage; the central trader goes bankrupt. The rates shown in Fig. 10 (b) and (c) for and connections vividly capture the competition for survival, leading to solvency in one case and bankruptcy in the other.

As expected, we observe that fewer connections (here, ) are needed, compared to the earlier case with smaller would-be survivors (), to eliminate the chosen trader. In closing, we should of course emphasise that the values mentioned here are illustrative.

5 Survivor distributions and rare events

We have seen that the safest strategy for the Lazarus effect is to network with eventual non-survivors, i.e. those who will never get past Stage I. It is also relatively safe to network with would-be survivors, provided they are poorer than oneself. (This would explain why multinationals are not afraid to enter an arena where smaller-size retailers predominate, for example). However, in this section we consider rare events, where the wealthiest trader in a given neighbourhood dies marginally, and a poorer one survives against the odds.

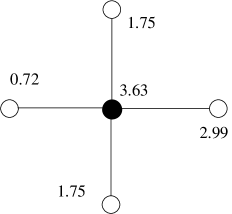

We look first at the four immediate neighbours of a given trader, and consider their pairwise interactions with him. Clearly, had such a pair been isolated, the larger trader would have won luck_am . However, many-body interactions in the lattice mean that this is not always true. We therefore ask the question: what is the proportion of cases where the poorer trader wins?

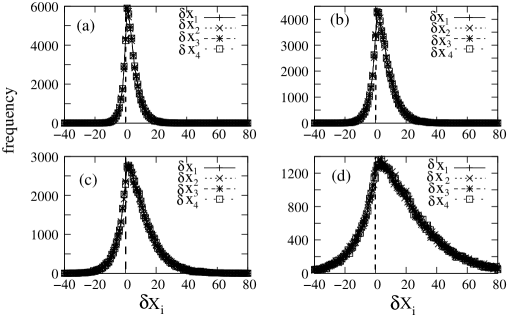

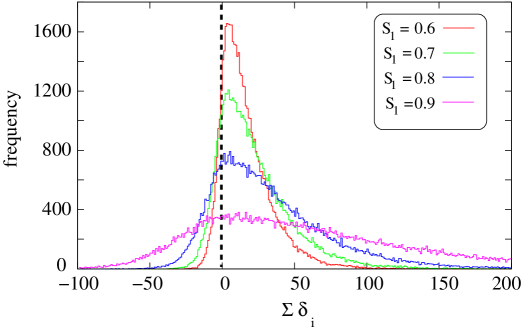

Each survivor has four neighbours; we first calculate the probability distribution of the initial wealth differences in a pairwise fashion between a survivor and each of his neighbours. The initial wealth differences are given by () corresponding to the four neighbours - right, left, bottom and top - of a survivor. The distribution of for all the survivors is shown in Fig. 11. Here, a negative means that the survivor is poorer than his neighbour, and conversely for positive . All four distributions corresponding to four neighbouring pairs overlap due to isotropy; the resulting distributions are universal functions of wealth differences, depending only on .

We also obtain the cumulative wealth difference between survivors and all of their four neighbours viz. (see Fig. 12). The distributions of are plotted in Fig. 12 for different values of . For a positive cumulative wealth difference we know that the survivor is richer than his neighbours, matching our intuition based on the mean-field regime. The negative side of the distribution is more interesting, comprising traders who are poorer than their four neighbours combined, and who have won against the odds.

Notice that both the survivor-neighbour pair distribution (Fig. 11), and the survivor- all neighbours cumulative distribution (Fig. 12) get broader with increasing . This is because increasing luck_am increases the number of potential survivors beyond Stage 1. In each case, the fraction of area under the negative side of the survivor pair-distribution gives an estimate of survivors against the odds – an example of some of the rare events alluded to at the beginning of this section.

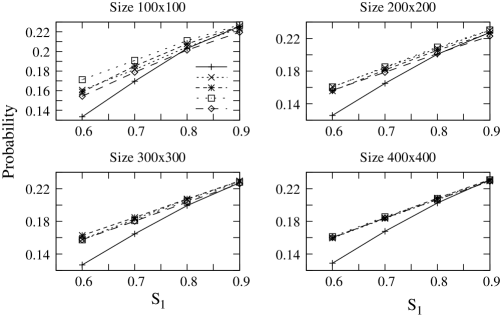

Figure 13 shows this fraction, both in terms of individual survivor-pair distributions and cumulative distributions, as a function of the of the initial wealth distribution, for different system sizes. There are more survivors, hence more survivors against the odds, leading to an increase in the fraction plotted on the y-axis of Fig. 13 for both distributions. For the largest system size, there is full isotropy in the pairwise distributions; the probability of finding a survivor against the odds is now seen to be a regular and universal function of in both pairwise and cumulative cases, relying only on wealth differences rather than on wealth. Finally, the cumulative distribution gives a more stringent survival criterion than the pairwise one, as is to be expected from the global nature of the dynamics.

A major conclusion to be drawn from Fig. 13 is the following: there are traders who are eliminated against the odds (traders who are wealthier than the eventual survivor). These should be easier to revive (as they have failed marginally) by selective networking than those who have failed because they are indeed worse off. This question is of real economic relevance, and its mathematical resolution seems to us to be an important open problem.

6 Discussion

We have used the model of luck_am to investigate two related issues in this paper on predatory trading am_wealth : first, that of systemic risk in the presence of increasing interactions, and next, the use of selective networking to prevent financial collapse. As long-range connections are introduced with probability to individual traders nirmal , we find that the qualitative features of the networked system remain the same as that of the regular case. The presence of two well-separated dynamical stages is retained, and the glassy dynamics and metastable states of luck_am persist. However, the number of survivors decreases as expected with increasing , quantitatively validating the thesis if haldane ; and systemic risk is far greater as the complexity of interactions is increased. This view finds resonance with the present economic scenario, where it appears that some measure of insulation via economic firewalls, is needed to prevent individual, and hence eventually systemic, collapse.

Another central result of this paper is the use of smart networking strategies to modify the fate of an arbitrary trader. We find that it is safest to network with eventual non-survivors; their decay and eventual death lead to the transformation of the destiny of a given site, from bankruptcy to solvency, or from solvency to greater solvency. Networking with peers, or with those who are born richer, in general leads to the weakening of one’s own finances, and an almost inevitable bankruptcy, given a predatory scenario.

However, the above is not immutable: the probability distributions in the last section of the paper indicate an interesting universality of survival ‘against the odds’. It would be interesting to find a predictive way of financial networking that would enable such a phenomenon to occur both at the individual, and at the societal, level.

Acknowledgements.

AM gratefully acknowledges the input of J M Luck, A S Majumdar and N N Thyagu to this manuscript.References

- (1) Brunnermeier M K and Pedersen L H (2005) Predatory Trading. Journal of Finance LX:1825-1864

- (2) Mehta A, Majumdar A S and Luck J M (2005) How the rich get richer. Pp. 199-204 in ‘Econophysics of Wealth Distributions’ edited by Chatterjee A et al, Springer-Verlag Italia

- (3) Luck J M and Mehta A (2005) A deterministic model of competitive cluster growth : glassy dynamics, metastability and pattern formation. Eur. Phys. J. B 44:79-92

- (4) Haldane A G and May R M (2011) Systemic risk in banking ecosystems. Nature 469:351-355

- (5) Watts D J and Strogatz S H (1998) Collective dynamics of small-world networks. Nature 393 440-442.

- (6) Barabasi A L and Albert R (1999) Emergence of scaling in random networks. Science 286: 509-512 .

- (7) Albert R and Barabasi A L (2002) Statistical mechanics of complex networks. Rev. Mod. Phys. 74: 47 - 97 ; Newman M, Barabasi A L, and Watts D J (2006) The structure and dynamics of networks. Princeton Univ. Press, New Jersey.

- (8) Amaral L A N et al (2000) Classes of small-world networks. Proc. Natl. Acad. Sci. 97: 11149 - 11152

- (9) Thyagu N N and Mehta A (2011) Competitive cluster growth on networks: complex dynamics and survival strategies. Physica A 390:1458-1473

- (10) Majumdar A S (2003) Domination of black hole accretion in brane cosmology Phys. Rev. Lett. 90:031303

- (11) Mezard M, Parisi G and Virasoro M (1987) Spin Glass Theory and Beyond. World Scientific, Singapore.

- (12) Lagarde C, at the World Economic Forum, Davos 2012.

- (13) Luke 16:19-31.