Eigenvalue distribution of large sample covariance matrices of linear processes

Abstract.

We derive the distribution of the eigenvalues of a large sample covariance matrix when the data is dependent in time. More precisely, the dependence for each variable is modelled as a linear process , where are assumed to be independent random variables with finite fourth moments. If the sample size and the number of variables both converge to infinity such that , then the empirical spectral distribution of converges to a non-random distribution which only depends on and the spectral density of . In particular, our results apply to (fractionally integrated) ARMA processes, which we illustrate by some examples.

Key words and phrases:

eigenvalue distribution, fractionally integrated ARMA process, limiting spectral distribution, linear process, random matrix theory, sample covariance matrix2000 Mathematics Subject Classification:

Primary: 15A52; Secondary: 62M101. Introduction and main result

A typical object of interest in many fields is the sample covariance matrix of a data matrix , , . The matrix can be seen as a sample of size of -dimensional data vectors. For fixed one can show, as tends to infinity, that under certain assumptions the eigenvalues of the sample covariance matrix converge to the eigenvalues of the true underlying covariance matrix [2]. However, the assumption may not be justified if one has to deal with high dimensional data sets, so that it is often more suitable to assume that the dimension is of the same order as the sample size , that is such that

| (1.1) |

For a symmetric matrix with eigenvalues , we denote by

the spectral distribution of , where denotes the Dirac measure located at . This means that is equal to the number of eigenvalues of that lie in the set . From now on we will call the sample covariance matrix. Due to Eq. 1.1, this change of normalization can be reversed by a simple transformation of the limiting spectral distribution. For notational convenience we suppress the explicit dependence of the occurring matrices on and where this does not cause ambiguity.

The distribution of Gaussian sample covariance matrices of fixed size was first computed in [20]. Several years later, it was Marchenko and Pastur [14] who considered the case where the random variables are more general i. i. d. random variables with finite second moments , and the number of variables is of the same order as the sample size . They showed that the empirical spectral distribution (ESD) of converges, as , to a non-random distribution , called limiting spectral distribution (LSD), given by

| (1.2) |

and point mass if ; in this formula, . Here and in the following, convergence of the ESD means almost sure convergence as a random element of the space of probability measures on equipped with the weak topology. In particular, the eigenvalues of the sample covariance matrix of a matrix with independent entries do not converge to the eigenvalues of the true covariance matrix, which is the identity matrix and therefore only has eigenvalue one. This leads to the failure of statistics that rely on the eigenvalues of which have been derived under the assumption of fixed , and random matrix theory is a tool to correct these statistics [4, 13]. In the case where the true covariance matrix is not the identity matrix, the LSD can in general only be given in terms of a non-linear equation for its Stieltjes transform, which is defined by

Conversely, the distribution can be obtained from its Stieltjes transform via the Stieltjes–Perron inversion formula ([3, Theorem B.8]), which states that

| (1.3) |

for all continuity points of . For a comprehensive account of random matrix theory we refer the reader to [1, 3, 15], and the references therein.

Our aim in this paper is to obtain a Marchenko–Pastur type result in the case where there is dependence within the rows of . More precisely, for , the th row of is given by a linear process of the form

Here, is an array of independent random variables that satisfies

| (1.4) |

as well as the Lindeberg-type condition that, for each ,

| (1.5) |

Clearly, Eq. 1.5 is satisfied if all are identically distributed.

The novelty of our result is that we allow for dependence within the rows, and that the equation for is given in terms of the spectral density

of the linear processes only, which is the Fourier transform of the autocovariance function

Potential applications arise whenever data is not independent in time such that the Marchenko–Pastur law is not a good approximation. This includes e. g. wireless communications [19] and mathematical finance [18, 17]. Note that a similar question is also discussed in [5]. However, they have a different proof which relies on a moment condition to be verified. Furthermore, they assume that the random variables are identically distributed so that the processes within the rows are independent copies of each other. More importantly, their results do not yield concrete formulas except in the AR(1) case and are therefore not directly applicable. In the context of free probability theory, the limiting spectral distribution of large sample covariance matrices of Gaussian ARMA processes is investigated in [7].

Before we present the main result of this article, we explain the notation used in this article. The symbols , , and denote the sets of integers, natural, real, and complex numbers, respectively. For a matrix , we write for its transpose and for its trace. Finally, the indicator of an expression is denoted by and defined to be one if is true, and zero otherwise; for a set , we also write instead of .

Theorem 1.1.

For each , let , , be a linear stochastic process with continuously differentiable spectral density . Assume that

- i)

-

ii)

there exist positive constants and such that for all ,

-

iii)

for almost all , for at most finitely many , and

-

iv)

for almost every .

Then the empirical spectral distribution of converges, as tends to infinity, almost surely to a non-random probability distribution with bounded support. Moreover, there exist positive numbers such that the Stieltjes transform of is the unique mapping satisfying

| (1.6) |

The assumptions of the theorem are met, for instance, if is an ARMA or fractionally integrated ARMA process; see Section 3 for details.

Theorem 1.1, as it stands, does not contain the classical Marchenko–Pastur law as a special case. For if the entries of the matrix are i. i. d., the corresponding spectral density is identically equal to the variance of , and thus condition iv is not satisfied. We therefore also present a version of Theorem 1.1 that holds if the rows of the matrix have a piecewise constant spectral density.

Theorem 1.2.

For each , let , , be a linear stochastic process with spectral density of the form

| (1.7) |

for some positive real numbers and a measurable partition of the interval . If conditions i and ii of Theorem 1.1 hold, then the empirical spectral distribution of converges, as , almost surely to a non-random probability distribution with bounded support. Moreover, the Stieltjes transform of is the unique mapping that satisfies

| (1.8) |

where denotes the Lebesgue measure of the set . In particular, if the entries of are i. i. d. with unit variance, one recovers the limiting spectral distribution 1.2 of the Marchenko–Pastur law.

Remark 1.3.

In applications one often considers processes of the form with mean . If we denote by the th column of the matrix , and define the empirical mean by , then the sample covariance matrix is given by the expression instead of . However, by [3, Theorem A.44], the subtraction of the empirical mean does not change the LSD, and thus Theorems 1.1 and 1.2 remain valid if the underlying linear process has a non-zero mean.

Remark 1.4.

The proof of Theorems 1.1 and 1.2 can easily be generalized to cover non-causal linear processes, which are defined as . For this case one obtains the same result except that the autocovariance function is now given by .

Remark 1.5.

If one considers a matrix which has independent linear processes in its columns instead of its rows, one obtains the same formulas as in Theorems 1.1 and 1.2 except that is replaced by . This is due to the fact that and have the same non-trivial eigenvalues.

In Section 2 we proceed with the proofs of Theorems 1.1 and 1.2. Thereafter we present some interesting examples in Section 3.

2. Proofs

In this section we present our proofs of Theorems 1.1 and 1.2. Dealing with infinite-order moving average processes directly is dfficult, and we therefore first prove a variant of these theorems for the truncated processes . We define the matrix , , .

Theorem 2.1.

Under the assumptions of Theorem 1.1 (Theorem 1.2), the empirical spectral distribution of the sample covariance matrix of the truncated process converges, as tends to infinity, to a deterministic distribution with bounded support. Its Stieltjes transform is uniquely determined by Eq. 1.6 (Eq. 1.8).

Proof.

The proof starts from the observation that one can write , where , , , and

| (2.5) |

In particular, . In order to prove convergence of the empirical spectral distribution and to obtain a characterization of the limiting distribution, it suffices, by [16, Theorem 1], to prove that the spectral distribution of converges to a non-trivial limiting distribution. This will be done in Lemma 2.2, where the LSD of is shown to be ; the distribution is computed in Lemma 2.3 if we impose the assumptions of Theorem 1.1, respectively in Lemma 2.4 if we impose the assumptions of Theorem 1.2. Inserting this expression for into equation (1.2) of [16] shows that the ESD converges, as , almost surely to a deterministic distribution, which is determined by the requirement that its Stieltjes transform satisfies

| (2.6) |

Using the explicit formulas of computed in Lemmas 2.3 and 2.4, one obtains Eqs. 1.6 and 1.8. Uniqueness of a mapping solving Eq. 2.6 was shown in [3, p. 88]. We complete the proof by arguing that the LSD of has bounded support. For this it is enough, by [3, Theorem 6.3], to show that the spectral norm of is bounded in , which is also done in Lemma 2.2. ∎

Lemma 2.2.

Let be the matrix appearing in Eq. 2.5, and assume that there exist positive constants such that (assumption ii of Theorem 1.1). Then the spectral norm of the matrix is bounded in . If, moreover, the spectral distribution of the Toeplitz matrix converges weakly to some limiting distribution , then the spectral distribution converges weakly, as , to .

Proof.

We first introduce the notation as well as the block decomposition , . We prove the second part of the lemma first. There are several ways to show that the spectral distributions of two sequences of matrices converge to the same limit. In our case it is convenient to use [3, Corollary A.41] which states that two sequences and , either of whose empirical spectral distribution converges, have the same limiting spectral distribution if converges to zero as tends to infinity. We shall employ this result twice: first to show that the LSDs of and agree, and then to prove equality of the LSDs of and . Let ; a direct calculation shows that , and we will consider each of the two terms in turn. From the definition of it follows that the th entry of is given by . The trace of the square of the upper left block of therefore satisfies

where denotes the Riemann zeta function. As a consequence, the limit of as tends to infinity is zero. Similarly, we obtain for the trace of the square of the off-diagonal block of the bound

which shows that the limit of is zero. It follows that , as defined in Section 2, converges to zero as goes to infinity, and therefore that the LSDs of and coincide. The latter distribution is clearly given by , and we show next that the LSD of agrees with the LSD of . As before it suffices to show, by [3, Corollary A.41], that converges to zero as tends to infinity. It follows from the definitions of and that can be estimated as

Consequently, converges to zero as goes to infinity, and it follows that .

In order to show that the spectral norm of is bounded in , we use Gerschgorin’s circle theorem ([8, Theorem 2]), which states that every eigenvalue of lies in at least one of the balls with centre and radius , , where the radii are defined as . We first note that the centres satisfy

To obtain a uniform bound for the radii we first assume that . Then

Similarly we find that, for ,

is bounded, which completes the proof. ∎

In the following two lemmas, we argue that the distribution exists and we prove explicit formulas for it in the case that the assumptions of Theorem 1.1 or Theorem 1.2 are satisfied.

Lemma 2.3.

Let be a sequence of real numbers, , and . Under the assumptions of Theorem 1.1 it holds that the spectral distribution of converges weakly, as , to an absolutely continuous distribution with bounded support and density

| (2.7) |

Proof.

We first note that under assumption ii of Theorem 1.1 the autocovariance function is absolutely summable because

Szegő’s first convergence theorem ([11] and [10, Corollary 4.1]) then implies that exists, and that the cumulative distribution function of the eigenvalues of the Toeplitz matrix associated with the sequence is given by

| (2.8) |

for all such that the level sets have Lebesgue measure zero. By assumption iii of Theorem 1.1, Eq. 2.8 holds for almost all . In order to prove that the LSD is absolutely continuous with respect to the Lebesgue measure, it suffices to prove that the cumulative distribution function is differentiable almost everywhere. Clearly, for ,

Due to assumption iv of Theorem 1.1, the set of all such that the set is non-empty is a Lebesgue null-set. Hence it is enough to consider only for which this set is empty. Let be the pre-image of , which is a finite set by assumption iii. The implicit function theorem then asserts that, for every , there exists an open interval around such that restricted to is invertible. It is no restriction to assume that these are disjoint. By choosing sufficiently small it can be ensured that the interval is contained in , and from the continuity of it follows that outside of , the values of are bounded away from , so that

In order to further simplify this expression, we denote the local inverse functions by . Observing that the Lebesgue measure of an interval is given by its length, and that the derivatives of are given by the inverse of the derivative of , it follows that

This shows that is differentiable almost everywhere with derivative . It remains to argue that the support of is bounded. The absolute summability of implies boundedness of its Fourier transform . The claim then follows from Eq. 2.8, which shows that the support of is equal to the range of . ∎

Lemma 2.4.

Let be the piecewise constant spectral density of the linear process , and denote the corresponding autocovariance function by . Under the assumptions of Theorem 1.2 it holds that the spectral distribution of converges weakly, as , to the distribution .

Proof.

Without loss of generality we may assume that . As in the proof of Lemma 2.3 one sees that exists, and that is given by

The special structure of thus implies that , where is the largest integer such that . Since must be right-continuous, this formula holds for all in the interval . It is easy to see that the function is the cumulative distribution function of the discrete measure , which completes the proof. ∎

Proof.

of Theorems 1.1 and 1.2 It is only left to show that the truncation performed in Theorem 2.1 does not alter the LSD, i. e. that the difference of and converges to zero almost surely. By [3, Corollary A.42], this means that we have to show that

| (2.9) |

converges to zero. To this end we show that has a limit, and that converges to zero, both almost surely. By the definition of and we have

We shall prove that the variances of are summable. For this purpose we need the following two estimates which are implied by the Cauchy–Schwarz inequality, the assumption that is finite, and the assumed absolute summability of the coefficients :

| (2.10a) | ||||

| (2.10b) | ||||

Therefore we can, by Fubini’s theorem, interchange expectation and summation to bound the variance of as

Considering separately the terms where and , we can write

For the expectation in the first sum not to be zero, must equal and must equal , in which case its value is unity. The expectation in the second term can always be bounded by , so that we obtain

Due to Eq. 1.1 and the assumed polynomial decay of there exists a constant such that the right hand side is bounded by , which implies that

and therefore, by the first Borel–Cantelli lemma, that converges to a constant almost surely. In order to show that this constant is zero, it suffices to shows that the expectation of converges to zero. Since , and the are independent, one sees, using Eq. 2.10a and again Fubini’s theorem, that , which converges to zero because the are square-summable.

We now consider factor of expression 2.9 and define . Then

| (2.11) |

Because of

and similarly , we have that

| (2.12) |

Equation 2.10b allows us to apply Fubini’s theorem to compute the variance of the second term in the previous display as

which is, by the same reasoning as we did for , bounded by

for some positive constant . Clearly, this is summable in . Having, by Eq. 2.10a, expected value zero, the second term of Eq. 2.12 and, therefore, also both converge to zero almost surely. Thus, we only have to look at the contribution of in expression 2.11. From Theorem 2.1 we know that converges almost surely weakly to some non-random distribution with bounded support. Hence, denoting by the eigenvalues of ,

almost surely. It follows that, in Eq. 2.9, factor is bounded, and factor converges to zero, and so the proof of Theorems 1.1 and 1.2 is complete. ∎

3. Illustrative examples

For several classes of widely employed linear processes, Theorem 1.1 can be used to obtain an explicit description of the limiting spectral distribution. In this section we consider the class of autoregressive moving average (ARMA) processes as well as fractionally integrated ARMA models. The distributions we obtain in the case of AR(1) and MA(1) processes can be interpreted as one-parameter deformations of the classical Marchenko–Pastur law.

3.1. Autoregressive moving average processes

Given polynomials and , an ARMA(p,q) process with autoregressive polynomial and moving average polynomial is defined as the stationary solution to the stochastic difference equation

If the zeros of lie outside the closed unit disk, it is well known that has an infinite-order moving average representation , where are the coefficients in the power series expansion of around zero. It is also known ([6]) that there exist positive constants and such that , so that assumption ii of Theorem 1.1 is satisfied. While the autocovariance function of a general ARMA process does not in general have a simple closed form, its Fourier transform is given by

| (3.1) |

Since is rational, assumptions iii and iv of Theorem 1.1 are satisfied as well. In order to compute the LSD of , it is necessary, by Lemma 2.3, to find the roots of a trigonometric polynomial of possibly high degree, which can be done numerically.

We now consider the special case of the ARMA(1,1) process , , for which one can obtain explicit results. By Eq. 3.1, the spectral density of X is given by

Equation 2.7 implies that the LSD of the autocovariance matrix has a density , which is given by

where

By Theorem 1.1, the Stieltjes transform of the limiting spectral distribution of is the unique mapping that satisfies the equation

| (3.2) | ||||

This is a quartic equation in which can be solved explicitly. An application of the Stieltjes inversion formula 1.3 then yields the limiting spectral distribution of .

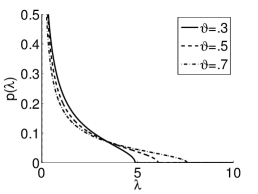

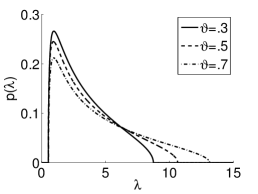

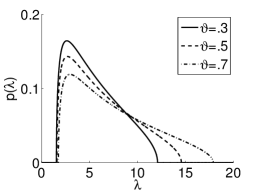

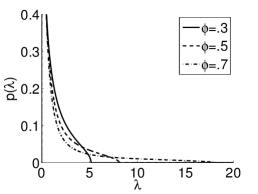

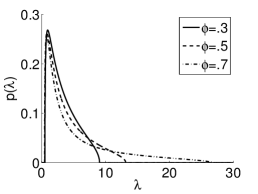

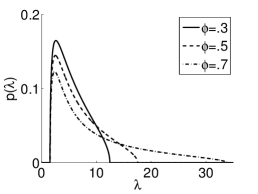

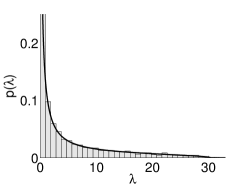

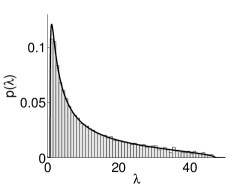

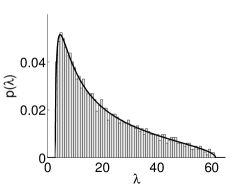

If one sets , one obtains an MA(1) process; plots of the densities obtained in this case for different values of and are displayed in Fig. 1. Similarly, the case corresponds to an AR(1) process; see Fig. 2 for a graphical representation of the densities one obtains for different values of and in this case. For the special case , , Fig. 3 compares the histogram of the eigenvalues of with the limiting spectral distribution obtained from Theorem 1.1 for different values of .

Section 3.1 for the Stieltjes transform of the limiting spectral distribution of the sample covariance matrix of an ARMA(1,1) process should be compared to [5, Eq. (2.10)], where the analogous result is obtained for an autoregressive process of order one. They use the notation and consider the spectral distribution of instead of . If one observes that this difference in the normalization amounts to a linear transformation of the corresponding Stieltjes transform, one obtains their result as a special case of Section 3.1.

3.2. Fractionally integrated ARMA processes

In many practical situations, data exhibit long-range dependence, which can be modelled by long-memory processes. Denote by the backshift operator and define, for , the (fractional) difference operator by

A process is called a fractionally integrated ARMA(p,d,q) processes with and if is an ARMA(p,q) process. These processes have a polynomially decaying autocorrelation function and therefore exhibit long-range-dependence, cf. [6, Theorem 13.2.2] and [9, 12]. We assume that , and that the zeros of the autoregressive polynomial of lie outside the closed unit disk. Then it follows that has an infinite-order moving average representation , where the have, in contrast to our previous examples, not an exponential decay, but satisfy , for some . Therefore, if , one can apply Theorem 1.1 to obtain the LSD of the sample covariance matrix, using that the spectral density of is given by

Acknowledgements

Both authors gratefully acknowledge financial support from Technische Universität München - Institute for Advanced Study funded by the German Excellence Initiative, and from the International Graduate School of Science and Engineering.

References

- [1] G. W. Anderson, A. Guionnet, and O. Zeitouni. An introduction to random matrices, volume 118 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 2010.

- [2] T. W. Anderson. An introduction to multivariate statistical analysis. Wiley Series in Probability and Statistics. Wiley-Interscience, Hoboken, third edition, 2003.

- [3] Z. Bai and J. W. Silverstein. Spectral analysis of large dimensional random matrices. Springer Series in Statistics. Springer, New York, second edition, 2010.

- [4] Z. D. Bai, D. Jiang, J.-F. Yao, and S. Zheng. Corrections to LRT on large-dimensional covariance matrix by RMT. Ann. Stat., 37(6B):3822–3840, 2009.

- [5] Z. D. Bai and W. Zhou. Large sample covariance matrices without independence structures in columns. Stat. Sinica, 18(2):425–442, 2008.

- [6] P. J. Brockwell and R. A. Davis. Time series: theory and methods. Springer Series in Statistics. Springer-Verlag, New York, second edition, 1991.

- [7] Z. Burda, A. Jarosz, M. A. Nowak, and M. Snarska. A random matrix approach to VARMA processes. New Journal of Physics, 12:075036, 2010.

- [8] S. Gerschgorin. Über die Abgrenzung der Eigenwerte einer Matrix. Bulletin de l’Académie des Sciences de l’URSS. Classe des sciences mathématiques et naturelles, 6:749–754, 1931.

- [9] C. W. J. Granger and R. Joyeux. An introduction to long-memory time series models and fractional differencing. J. Time Ser. Anal., 1(1):15–29, 1980.

- [10] R. M. Gray. Toeplitz and circulant matrices: A review. Now Publishers, Boston, 2006.

- [11] U. Grenander and G. Szegő. Toeplitz forms and their applications. Chelsea Publishing, New York, second edition, 1984.

- [12] J. R. M. Hosking. Fractional differencing. Biometrika, 68(1):165–176, 1981.

- [13] Iain M. Johnstone. On the distribution of the largest eigenvalue in principal components analysis. Ann. Statist., 29(2):295–327, 2001.

- [14] V. A. Marchenko and L. A. Pastur. Distribution of eigenvalues in certain sets of random matrices. Mat. Sb. (N.S.), 72(114)(4):507–536, 1967.

- [15] M. L. Mehta. Random matrices. Pure and Applied Mathematics. Elsevier/Academic Press, Amsterdam, third edition, 2004.

- [16] G. Pan. Strong convergence of the empirical distribution of eigenvalues of sample covariance matrices with a perturbation matrix. J. Multivar. Anal., 101(6):1330–1338, 2010.

- [17] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, T. Guhr, and H. E. Stanley. Random matrix approach to cross correlations in financial data. Physical Review E, 65(6):66126, 2002.

- [18] M. Potters, J.-P. Bouchaud, and L. Laloux. Financial applications of random matrix theory: old laces and new pieces. Acta Phys. Polon. B, 36(9):2767–2784, 2005.

- [19] A. M. Tulino and S. Verdu. Random Matrix Theory and Wireless Communications. Now Publishers, Boston, 2004.

- [20] J. Wishart. The generalised product moment distribution in samples from a normal multivariate population. Biometrika, 20A(1/2):32–52, 1928.