Institute of Information Theory and Automation, Academy of Sciences of the Czech Republic, Pod Vodarenskou vezi 4, Prague, CZ-182 08, Czech Republic

Complex systems Time series analysis in nonlinear dynamics Econophysics

Multifractal Height Cross-Correlation Analysis: A New Method for Analyzing Long-Range Cross-Correlations

Abstract

We introduce a new method for detection of long-range cross-correlations and multifractality – multifractal height cross-correlation analysis (MF-HXA) – based on scaling of th order covariances. MF-HXA is a bivariate generalization of the height-height correlation analysis of Barabasi & Vicsek [Barabasi, A.L., Vicsek, T.: Multifractality of self-affine fractals, Physical Review A 44(4), 1991]. The method can be used to analyze long-range cross-correlations and multifractality between two simultaneously recorded series. We illustrate a power of the method on both simulated and real-world time series.

pacs:

89.75.-kpacs:

05.45.Tppacs:

89.65.GhThe research of long-range dependence and multifractality has been growing significantly in recent years with application to a wide range of disciplines [1, 2, 3, 4, 5, 6, 7, 8, 9, 10]. Recently, the examination of long-range cross-correlations has become of interest as it provides additional information about the examined processes. Carbone [11] generalized the detrending moving average (DMA) method for higher dimensions. Podobnik & Stanley [12] adjusted the detrended fluctuation analysis for two time series and introduced the detrended cross-correlation analysis (DCCA). Zhou [13] further generalized the method and introduced the multifractal detrended cross-correlation analysis (MF-DXA). Jiang & Zhou [14] then implemented moving average filtering to MF-DXA algorithm creating MF-X-DMA. In this paper, we introduce two new methods for an analysis of long-range cross-correlations – the multifractal height cross-correlation analysis (MF-HXA) and its special case of the height cross-correlation analysis (HXA).

To analyze long-range cross-correlations, we generalize the -th order height-height correlation function for two simultaneously recorded series. Let us consider two series and with time resolution and , where is a lower integer sign. For better legibility, we denote , which varies with , and we write the -order difference as and . Height-height covariance function is then defined as

| (1) |

where time interval generally ranges between . Scaling relationship between and the generalized bivariate Hurst exponent is obtained as

| (2) |

For , the method can be used for the detection of long-range cross-correlations solely and we call it the height cross-correlation analysis (HXA). Obviously, MF-HXA reduces to the height-height correlation analysis of Barabasi et al. [15] for . Note that it makes sense to analyze the scaling according to Eq. 2 only for detrended series and and only for [5]. A type of detrending can generally take various forms – polynomial, moving averages and other filtering methods – and is applied for each time resolution separately.

The bivariate Hurst exponent has similar properties and interpretation as a univariate Hurst exponent. For , the series are cross-persistent so that a positive (a negative) value of is more statistically probable to be followed by another positive (negative) value of . Conversely for , the series are cross-antipersistent so that a positive (a negative) value of is more statistically probable to be followed by a negative (a positive) value of . Note that even two pairwise uncorrelated processes can be cross-persistent111For example, let us have pairwise uncorrelated processes and following fractional Gaussian noise with and and thus . Even though the two processes are independently generated (and thus uncorrelated), they are cross-persistent. If and , then it is statistically more probable (based on persistence of the separate processes) that also and than otherwise. Therefore, if the processes moved together in period , it is statistically more likely that they will move together in period as well (and vice versa), i.e. the processes are cross-persistent..

The expected values of the bivariate Hurst exponents have been partly discussed in [12, 13, 14]. It has been shown that

| (3) |

for all for pairwise uncorrelated and correlated processes. We present some new insights into this relation. To better understand the behavior of the bivariate Hurst exponent, we use a standard multifractal formalism [16]. Consider processes and are multifractal with generalized Hurst exponents and so that

| (4) |

| (5) |

In the same way, we can write the joint scaling of two series (compare with Eq. 1) as

| (6) |

Using the definition of covariance, the left part of Eq. 6 can be rewritten as

| (7) |

From Eqs. 4 and 5, the first part of the right-hand side of Eq. 7 implies

| (8) |

which corresponds to Eq. 3. Therefore, the crucial part of long-range cross-correlations and multifractality is the scaling of covariances between and with varying . Consider now a scaling exponent and a scaling relationship

| (9) |

This leads us to three simple implications. If covariances do not scale with , then Eq. 3 holds. If the covariances scale with , the other two are as follows:

| (10) |

We show that these relationships are indeed true for artificially generated processes later in the text. Therefore, we need to distinguish between two types of long-range cross-correlations: (i) long-range cross-correlations caused by long-range dependence of the separate series, and (ii) long-range cross-correlations caused by scaling of covariances between and .

In order to test validity of the method, we present results for several artificial series. In the analysis, we apply MF-HXA with changing and fixed . In turn, we obtain the 99% jackknife confidence intervals under an assumption of a normally distributed Hurst exponent with an unknown variance. The estimated Hurst exponent is then taken as a mean of the exponents based on the various . This way, we can comment on the results with statistical power [5]. In the procedure, we apply filtering of a constant trend. We now turn to the artificial processes.

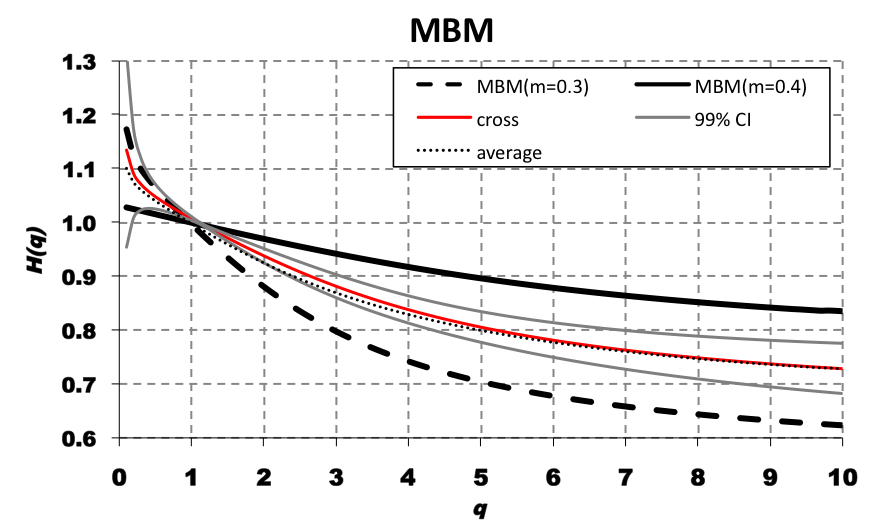

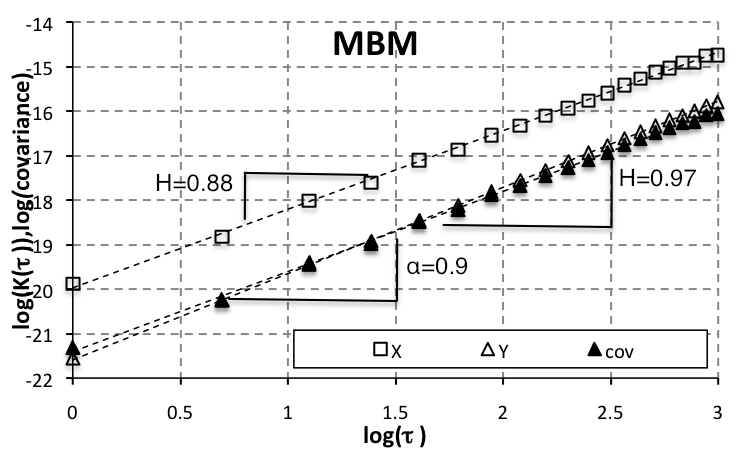

First, we start with the Mandelbrot’s binomial multifractal (MBM) measures [17, 18]. Let , and and let us work on interval [0,1]. In the first stage, the mass of 1 is divided into two subintervals [0,] and [,1], when there is the mass in the first subinterval and the mass in the second one. In the following stage, each subinterval is again halved and its mass is divided between the smaller subintervals in a ratio . After stages, we obtain a series of values. Note that the values are deterministic as there is no noise added in the simplest version of the method. For an interval , the value has a value of , where and stand for the relative frequencies of numbers 0 and 1 in a binary development of , respectively. We construct two series with and . Results are presented in Fig. 1a, showing that the bivariate Hurst exponent does not deviate significantly from the average value of and even though the analyzed series are strongly correlated.

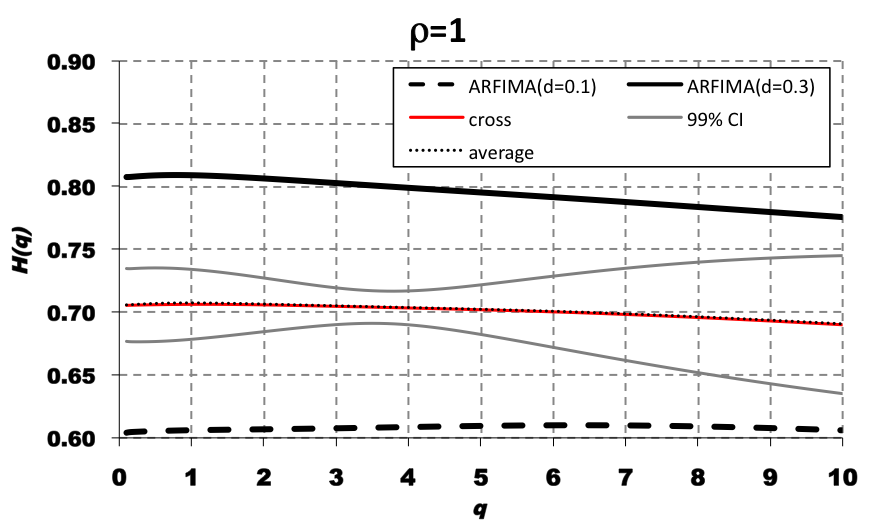

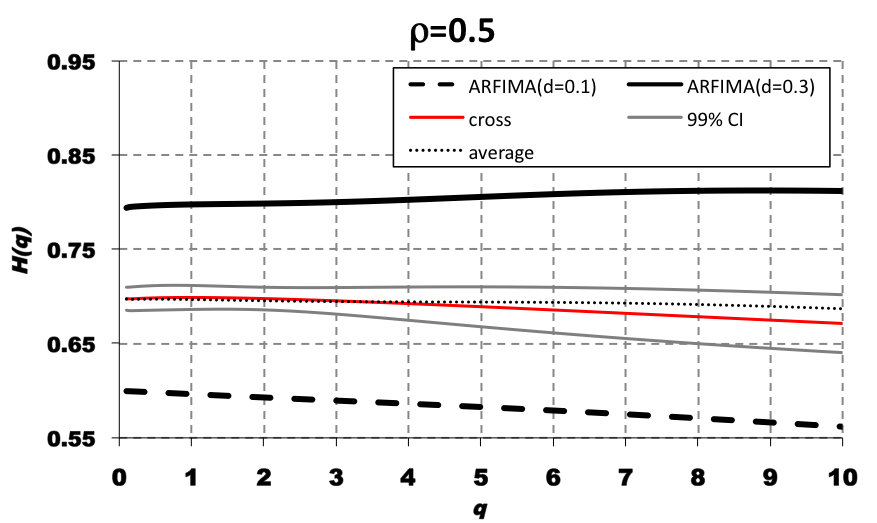

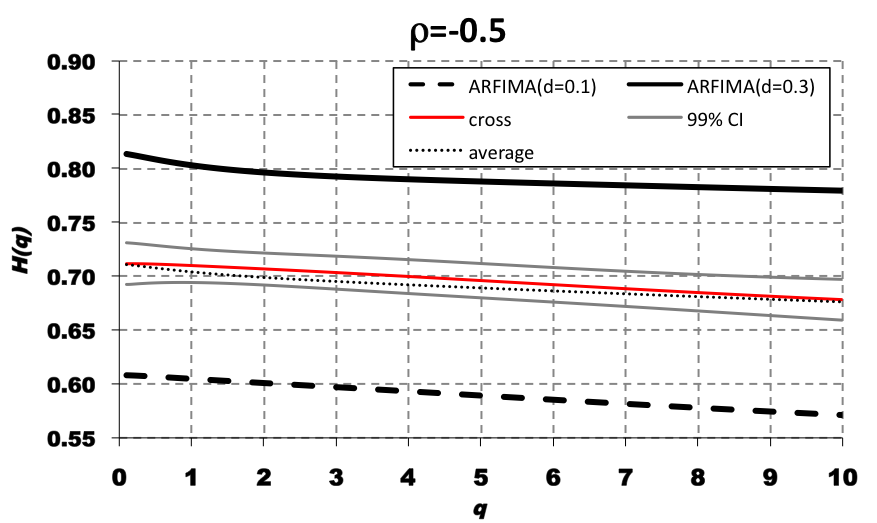

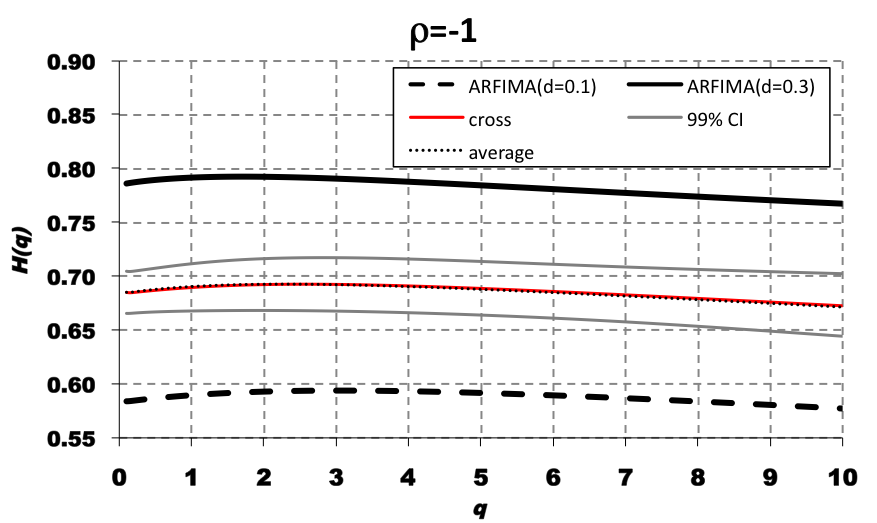

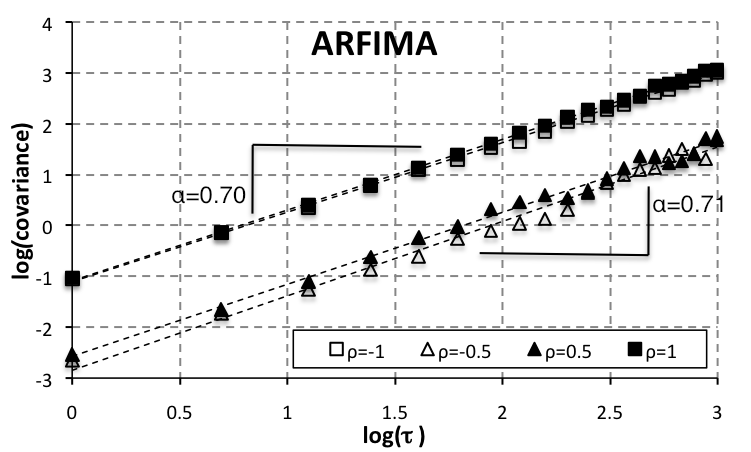

Second, we apply MF-HXA on ARFIMA processes with correlated noise terms. ARFIMA() process is defined as where is a free parameter, related to Hurst exponent as , and . We simulate long-range dependent series of length . To describe influence of the correlations on MF-HXA estimates, we generate series with correlated noise and five cases are investigated – correlation coefficients for the noise terms are set to 1, 0.5, 0, -0.5 and -1. The results are shown in Fig. 1b-f. The estimates of are not significantly different from for any or any correlation coefficient value. This result is in hand with the results shown in [14] – pairwise correlations have no effect on the estimation.

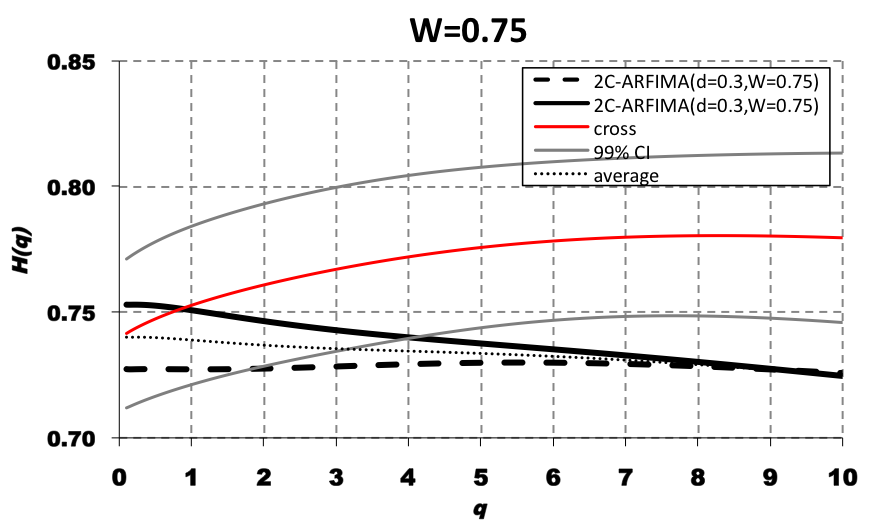

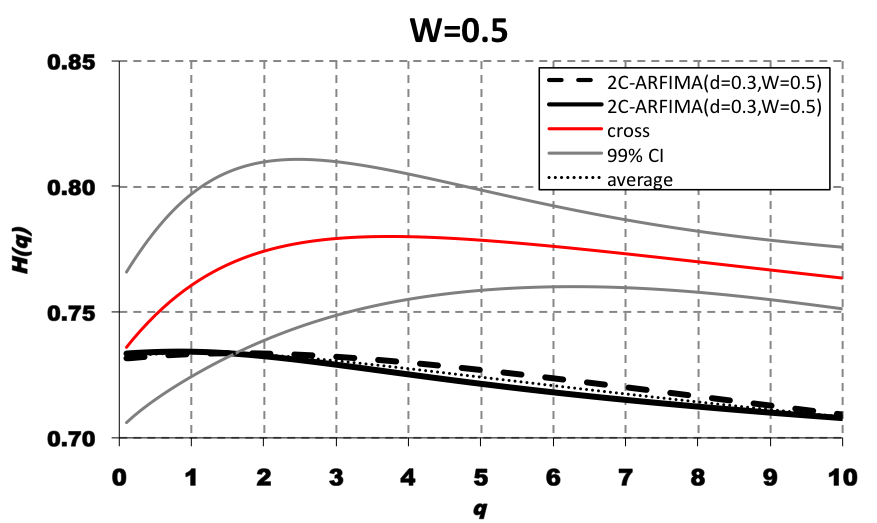

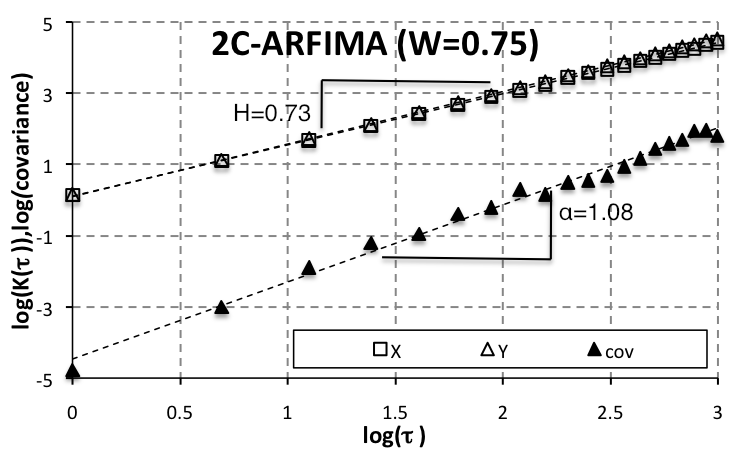

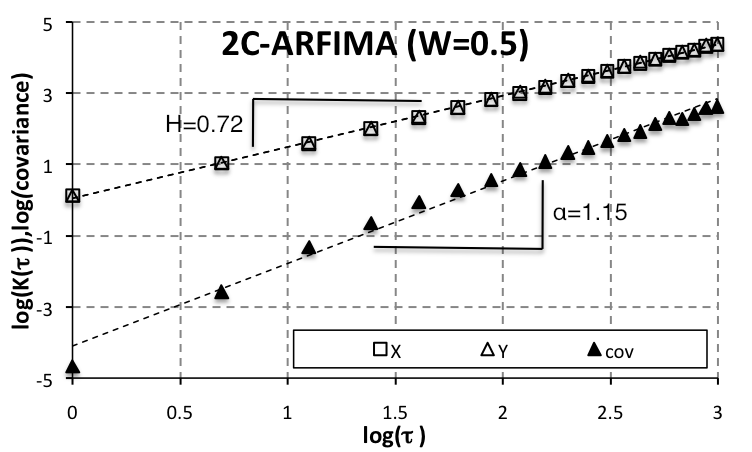

Third, we analyze the behavior of two-component ARFIMA processes [19]. For parameters and , the two-component ARFIMA(,) processes and are described by the following set of equations:

Here, is a free parameter () controlling a strength of coupling between and , and are noise terms. Note that for , we obtain two decoupled ARFIMA processes, whereas for , the two processes have long memory of the process itself as well as of the other one. In our simulations, we consider with (practically, the case has been investigated in the previous paragraph). The results are shown in Fig. 1g,h. For both and , we notice deviations of from starting already at . The deviations are statistically insignificant for lower moments (due to rather short series, ), but become statistically significant for higher moments (for when and for when ). The effect gets stronger with lower . Indeed, these are expected results as the construction of the two-component ARFIMA mixes the long memory of the separate processes together.

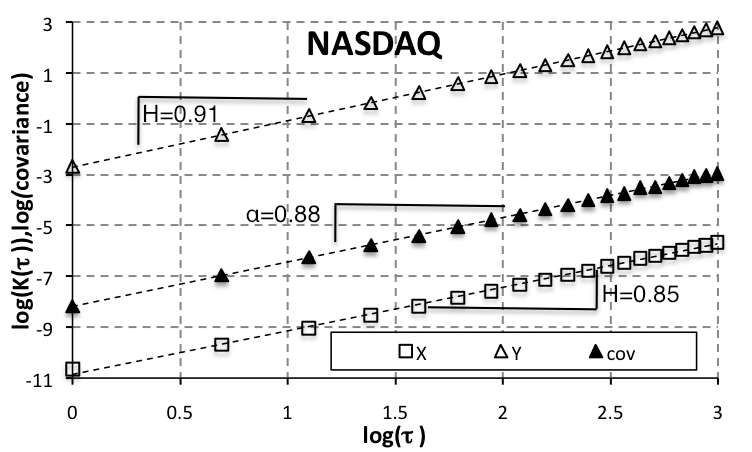

In Fig. 2, we present the results based on separation in Eq. 7, i.e. scaling of separate processes and scaling of covariances of and . For illustrational purposes, we show only the case . For MBM (Fig. 2a), the scaling of covariances is slightly lower than the average of Hurst exponents, yet remains well between them. This is reflected in the fact that the estimated is not equal to the average of estimated and but is rather close to the lower confidence interval (Fig. 1a), yet the deviation is still insignificant. In Fig. 2b, four cases of correlated ARFIMA processes are illustrated. All four processes show , which perfectly fits the expectations. We can see that the covariances are higher for highly correlated series than the less correlated series, but the scaling relation remains the same for all. The case of uncorrelated ARFIMA processes exhibits no scaling of covariances (as these vary around zero) and is thus not shown. In Figs. 2c,d, the two-component ARFIMA processes are illustrated. Here, the difference between scaling of covariances and the pair of and is remarkable for both and . The scaling of covariances is expectedly stronger for . These results perfectly support the calculations presented in Eqs. 4 – 10.

To show potential use of the method, we study different real-world financial series, which we consider the outputs of the complex systems – daily volatility and volume series of NASDAQ and S&P500 stock indices (finance.yahoo.com database), and daily returns and volatility of spot and futures prices of WTI Crude Oil (NYMEX Commodities database). Even though the real-world series are of the same length order as the simulated processes, which scale even up to and , usually does not scale for and for daily financial data [5]. Also, we apply linear filtering according to [4]. The generalized Hurst exponents are then estimated by varying between 5 and 20 for .

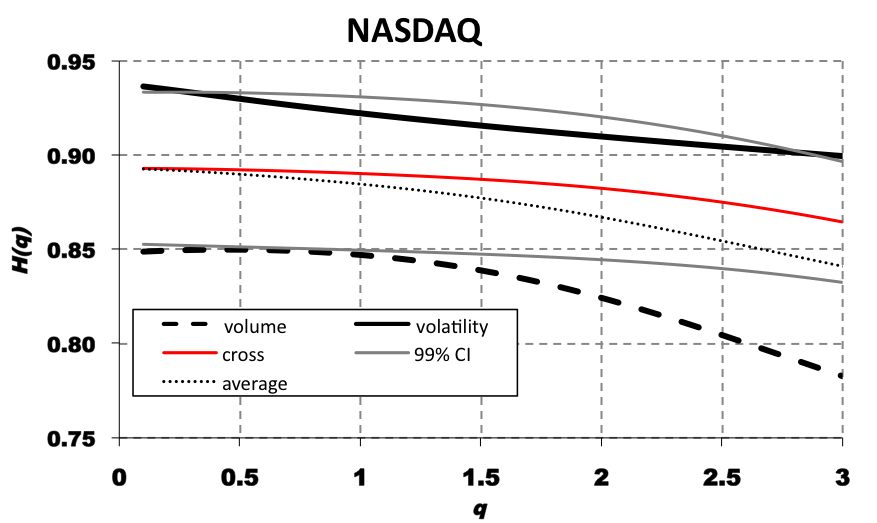

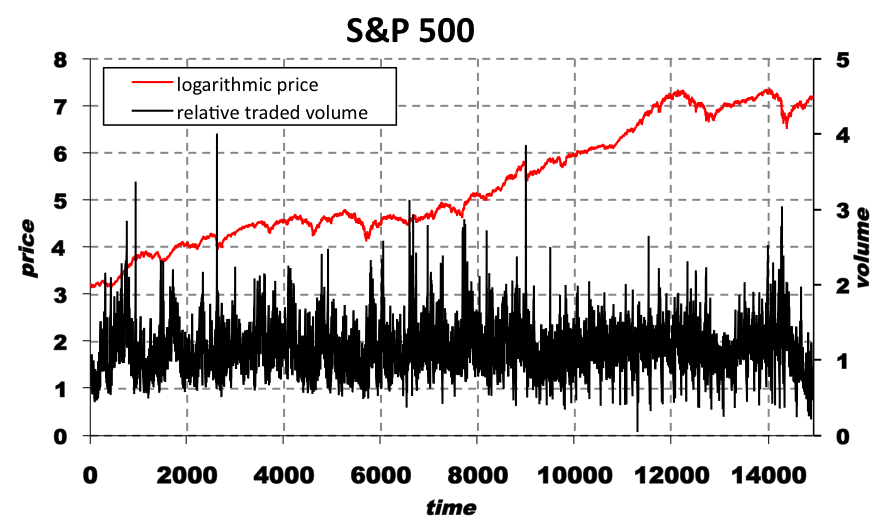

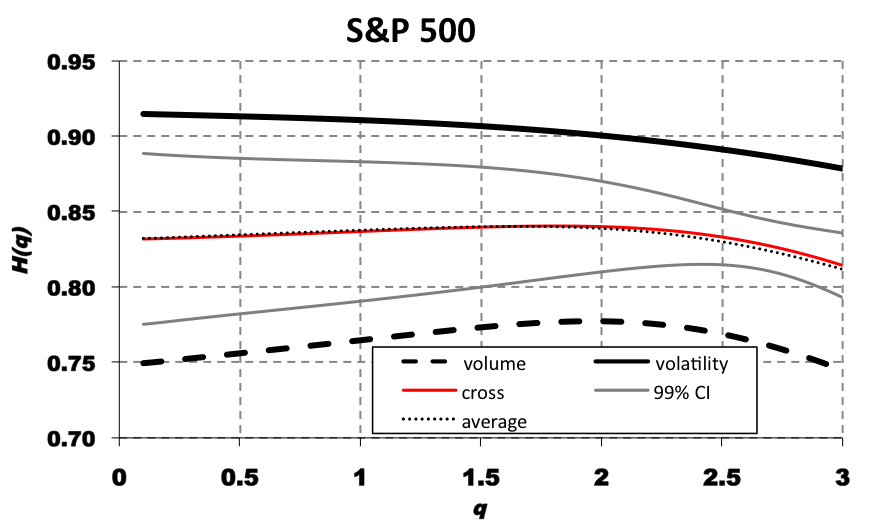

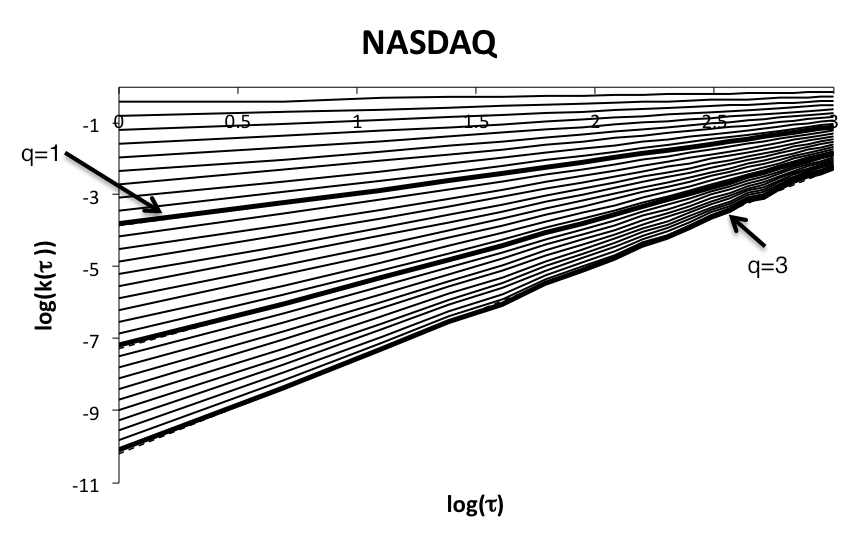

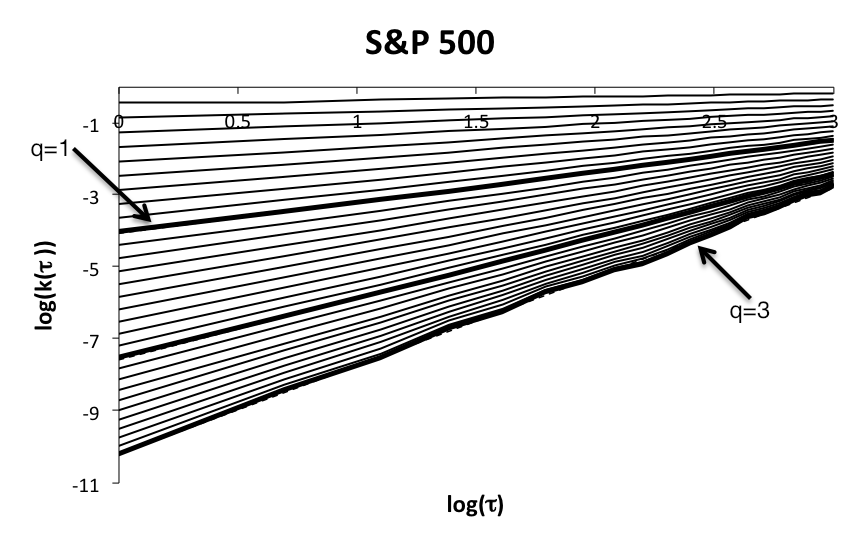

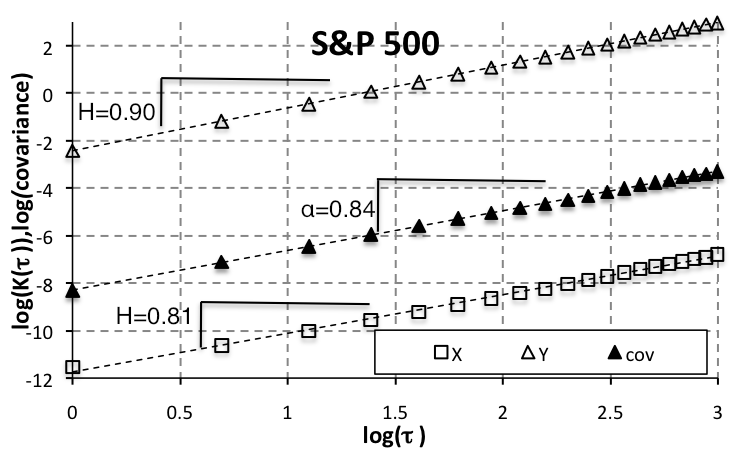

For the stock indices, we analyze the series of volume and volatility for the longest available datasets – from 11.10.1984 to 26.4.2011 for NASDAQ (6,693 observations) and from 3.1.1950 to 26.4.2011 for S&P500 (15,428 observations). We take absolute returns, defined as where is a stock index closing price, as a measure of volatility. Volume series are transformed as a relative deviation from a moving average of traded volume in approximately past two trading years (500 observations) to control for an exponential increase of the traded volume in past decades (Fig. 3a,c). The estimated generalized Hurst exponents are shown in Fig. 3b,d. For both stock indices, the trading volume and volatility are strongly persistent as well as cross-persistent. Nevertheless, the bivariate Hurst exponent does not differ significantly from the average of and , i.e. the cross-persistence of the series is mainly due to the persistence of the separate processes and the fact that the processes are correlated (Fig. 4e,f). The scaling of is very stable up to and for all examined s (Fig. 4a,b). The results are in hand with [12] who found weaker persistence of the process of traded volume. However, the definitions of traded volume differ from our study.

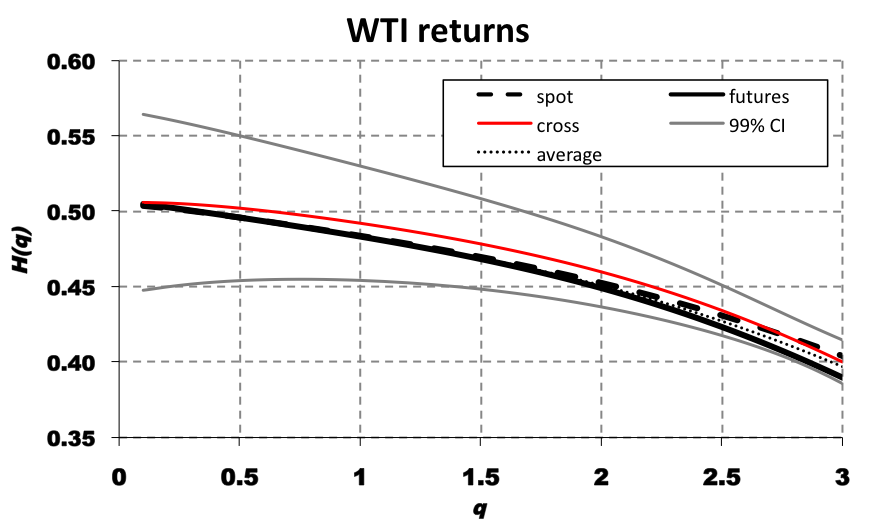

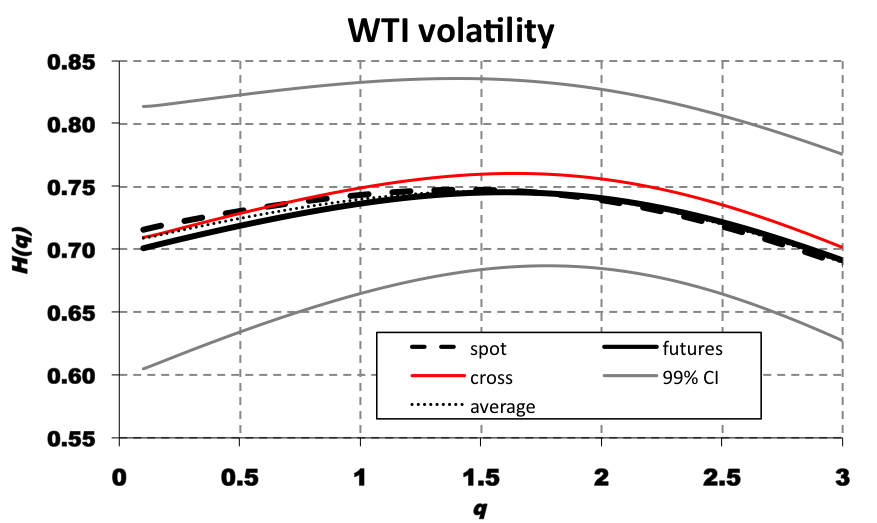

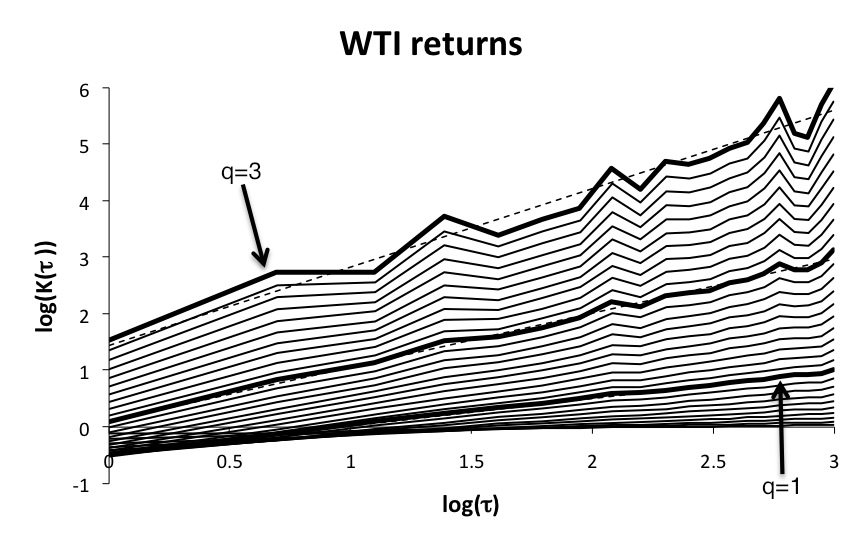

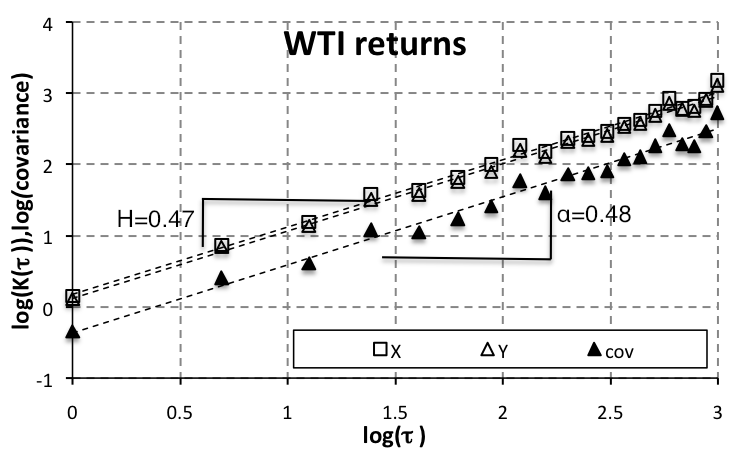

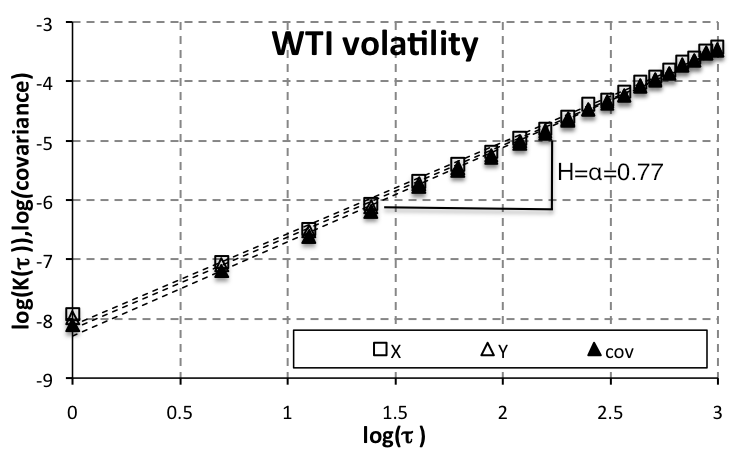

For the WTI spot and futures prices, we cover a period from 2.1.1986 to 26.4.2011 (6,348 observations) and analyze the logarithmic returns and the volatility again in the form of absolute returns. The results are shown in Fig. 3e,f. For both returns and volatility, the estimates of the generalized Hurst exponents practically overlap for all . On one hand, the returns show no signs of long-range correlations or cross-correlations. On the other hand, the volatility of separate processes show strong persistence as well as cross-persistence. Moreover, the generalized Hurst exponents vary only slightly with and are not even monotonically declining as expected for multifractal processes, suggesting that the processes of volatility are monofractal. Yet again, the cross-persistence of the series is mainly due to the persistence of the separate processes and high correlation between the processes (Fig. 4g,h) as does not significantly deviate from . The scaling of shows different behavior for returns and volatilities. As for volatility, the scaling is very stable up to and . On contrary, the scaling for returns becomes less stable with growing (Fig. 3c,d).

In conclusion, we introduce the new method for an analysis of long-range cross-correlations and multifractality – the multifractal height cross-correlation analysis. The scaling of covariances of the absolute values of the series gives additional information about dynamics of two simultaneously recorded series and can cause divergence of the bivariate Hurst exponent from the average of the separate univariate Hurst exponents. A utility of the method has been shown on several artificial series as well as the real-world time series. We argue that even though majority of the analyzed series are cross-persistent, such cross-persistence is mainly caused by persistence of the separate processes and the fact that the series are correlated. The scaling of covariances of the absolute values of the examined processes is with good agreement with this result. A larger study comparing bias and efficiency of MF-HXA compared to the other methods analyzing long-range cross-correlations (MF-X-DFA and MF-X-DMA) shall follow.

Acknowledgements.

The support from the Czech Science Foundation under Grants 402/09/H045 and 402/09/0965 and from the Grant Agency of the Charles University (GAUK) under project 118310 are gratefully acknowledged. The author would also like to thank J. Barunik and L. Vacha for helpful comments and discussions.References

- [1] \NameShiogai Y., Stefanovska A. McClintock P. \REVIEWPhysics Reports 488201051.

- [2] \NameLiao F., Garrison D. Jan Y.-K. \REVIEWMicrovascular Research 80(1)201044.

- [3] \NameZuo R., Cheng Q. Xia Q. \REVIEWJournal of Geochemical Exploration 102200937.

- [4] \NameDi Matteo T., Aste T. Dacorogna M. \REVIEWJournal of Banking and Finance 292005827.

- [5] \NameDi Matteo T. \REVIEWQuantitative Finance 7200721.

- [6] \NameChen C.-C., Lee Y.-T. Chang Y.-F. \REVIEWPhysica A 38720084643.

- [7] \NameRehman S. \REVIEWChaos, Solitons and Fractals 392009499.

- [8] \NameHayakawa M., Hattori K., Nickolaenko A. Rabinowicz L. \REVIEWPhysics and Chemistry of the Earth 292004379.

- [9] \NameBarunik J. Kristoufek L. \REVIEWPhysica A 389(18)20103844.

- [10] \NameKristoufek L. \REVIEWChaos, Solitons and Fractals 43201068.

- [11] \NameCarbone A. \REVIEWPhysical Review E 762007056703.

- [12] \NamePodobnik B. Stanley H. \REVIEWPhysical Review Letters 1002008084102.

- [13] \NameZhou W.-X. \REVIEWPhysical Review E 772008066211.

- [14] \NameJiang Z.-Q. Zhou W.-X. \REVIEWPhysical Review E 2011Forthcoming.

- [15] \NameBarabasi A.-L., Szepfalusy P. Vicsek T. \REVIEWPhysica A 178199117.

- [16] \NameCalvet L. Fisher A. \BookMultifractal volatility: theory, forecasting, and pricing (Academic Press) 2008.

- [17] \NameMeneveau C. Sreenivasan K. \REVIEWPhysical Review Letters 5919871424.

- [18] \NameMandelbrot B., Fisher A. Calvet L. \REVIEWCowles Foundation Discussion Paper 11641997.

- [19] \NamePodobnik B., Horvatic D., Lam Ng A., Stanley H. Ivanov P. \REVIEWPhysica A 38720083954.

| (a) | (b) | (c) | (d) |

|

|

|

|

| (e) | (f) | (g) | (h) |

|

|

|

|

| (a) | (b) | (c) | (d) |

|---|---|---|---|

|

|

|

|

| (a) | (b) | (c) |

|

|

|

| (d) | (e) | (f) |

|

|

|

| (a) | (b) | (c) | (d) |

|

|

|

|

| (e) | (f) | (g) | (h) |

|

|

|

|