Capacitary measures for completely monotone kernels via singular control

Abstract

We give a singular control approach to the problem of minimizing an energy functional for measures with given total mass on a compact real interval, when energy is defined in terms of a completely monotone kernel. This problem occurs both in potential theory and when looking for optimal financial order execution strategies under transient price impact. In our setup, measures or order execution strategies are interpreted as singular controls, and the capacitary measure is the unique optimal control. The minimal energy, or equivalently the capacity of the underlying interval, is characterized by means of a nonstandard infinite-dimensional Riccati differential equation, which is analyzed in some detail. We then show that the capacitary measure has two Dirac components at the endpoints of the interval and a continuous Lebesgue density in between. This density can be obtained as the solution of a certain Volterra integral equation of the second kind.

Keywords: Singular control, verification argument, capacity theory, infinite-dimensional Riccati differential equation, optimal order execution, optimal trade execution, transient price impact

AMS Subject Classification: 49J15, 49K15, 31C15, 49N90, 91G80, 34G20

1 Introduction and statement of results

1.1 Background

Let be a function. The problem of minimizing the energy functional

over probability measures supported by a given compact set plays an important role in potential theory. A minimizing measure , when it exists, is called a capacitary measure, and the value is called the capacity of the set ; see, e.g., \citeasnounchoquet, \citeasnounfuglede, and \citeasnounlandkof. See also \citeasnounAikawaEssen or \citeasnounHelms for more recent books on potential theory.

In this paper, we develop a control approach to determining the capacitary distribution when is a compact interval and is a completely monotone function. In this approach, measures on will be regarded as singular controls and is the objective function. Our goal is to obtain qualitative structure theorems for the optimal control and characterize by means of certain differential and integral equations.

The intuition for this control approach, and in fact our original motivation, come from the problem of optimal order execution in mathematical finance. In this problem, one considers an economic agent who wishes to liquidate a certain asset position of shares within the time interval . This asset position can either be a long position () or a short position ). The order execution strategy chosen by the investor is described by the asset position held at time . In particular, one must have . Requiring the condition assures that the initial position has been unwound by time . The left-continuous path will be nonincreasing for a pure sell strategy and nondecreasing for a pure buy strategy. A general strategy can consist of both buy and sell trades and hence can be described as the sum of a nonincreasing and a nondecreasing strategy. That is, is a path of finite variation.

The problem the economic agent is facing is that his or her trades impact the price of the underlying asset. To model price impact, one starts by informally defining as the immediate price impact generated by the (possibly infinitesimal) trade executed at time . Next, it is an empirically well-established fact that price impact is transient and decays over time; see, e.g., \citeasnounMoroEtAl. This decay of price impact can be described informally by requiring that is the remaining impact at time of the impact generated by the trade . Here, is a nonincreasing function with , the decay kernel. Thus, is the price impact of the strategy , cumulated until time . This price impact creates liquidation costs for the economic agent, and one can derive that, under the common martingale assumption for unaffected asset prices, these costs are given by

| (1) |

plus a stochastic error term with expectation independent of the specific strategy ; see \citeasnounGSS. Indeed, let us assume that asset prices are given by where is a continuous martingale and models the price impact of the trading strategy at time . Then, we assume that the order is made at the average price and costs , which corresponds to a block shape limit order book, see \citeasnounAFS2. Accumulating these costs over , integrating by parts twice, and taking expectations yields

where we have used the fact that , due to the martingale assumption on . Further details can be found in \citeasnounGSS.

Thus, minimizing the expected costs amounts to minimizing the functional over all left-continuous strategies that are of bounded variation and satisfy and . This problem was formulated and solved in the special case of exponential decay, , by \citeasnounow. The general case was analyzed by \citeasnounASS in discrete time and by \citeasnounGSS in the continuous-time setup we have used above. We refer to \citeasnounAFS2, \citeasnounAS, \citeasnounGSS2, \citeasnounPredoiuShaikhetShreve, \citeasnounSchiedSlynko, and \citeasnounGatheralSchiedSurvey for further discussions and additional references in the context of mathematical finance.

Clearly, the cost functional coincides with the energy functional of the measure . So finding an optimal order execution strategy is basically equivalent to determining a capacitary measure for . There is one important difference, however: capacitary measures are determined as minimizers of with respect to all nonnegative measures on with total mass , while may be a signed measure with given total mass . This difference can become significant if is only required to be positive definite in the sense of Bochner (which is essentially equivalent to for all ), because then minimizers of the unconstrained problem need not exist. It was first shown by \citeasnounASS, and later extended to continuous time by \citeasnounGSS, that a unique optimal order execution strategy exists and that is a monotone function of when is convex and nonincreasing. This result has the important consequence that the constrained problem of finding a capacitary measure is equivalent to the unconstrained problem of determining an optimal order execution strategy.

In this paper, we aim at describing the structure of capacitary measures/optimal order execution strategies. To this end, it is instructive to first look at two specific examples in which the optimizer is known in explicit form. \citeasnounow find that for exponential decay, , the capacitary measure has two singular components at and and a constant Lebesgue density on :

| (2) |

Numerical experiments show that it is a common pattern that capacitary measures for nonincreasing convex kernels have two singular components at and and a Lebesgue density on . However, the capacitary measure for is the purely discrete measure

where [GSS, Proposition 2.14].

So it is an interesting question for which nonincreasing, convex kernels the capacitary measure has singular components only at and and is (absolutely) continuous on . It turns out that a sufficient condition is the complete monotonicity of , i.e., belongs to and is nonnegative in for . More precisely, we have the following result, which is in fact an immediate corollary of the main results in this paper.

Corollary 1.

Suppose that is completely monotone with . Then the capacitary measure has two Dirac components at and and is has a continuous Lebesgue density on .

1.2 Statement of main results

Our main results do not only give the preceding qualitative statement on the form of but they also provide quantitative descriptions of the Dirac components of and of its Lebesgue density on . To prepare for the statement of these results, let us first assume that , which we can do without loss of generality. Then we recall that by the celebrated Hausdorff–Bernstein–Widder theorem [Widder, Theorem IV.12a], is completely monotone if and only if it is the Laplace transform of a Borel probability measure on :

In particular, every exponential polynomial,

| (3) |

with and is completely monotone. Another example is power-law decay,

which is a popular choice for the decay of price impact in the econophysics literature; see \citeasnounGatheral and the references therein. We assume henceforth that , which is equivalent to

| (4) |

A crucial role will be played by the following infinite-dimensional Riccati equation for functions ,

| (5) |

where denotes the time derivative of , and the function satisfies the initial condition

| (6) |

Remark 1.

When writing (5) in the form one sees that the functional is not a continuous map from some reasonable function space into itself, unless is concentrated on a compact interval. For instance, it involves the typically unbounded linear operator . Therefore, existence and uniqueness of solutions to (5), (6) does not follow by an immediate application of standard results such as the Cauchy–Lipschitz/Picard–Lindelöf theorem in Banach spaces [HillePhillips, Theorem 3.4.1] or more recent ones such as those in \citeasnounTeixeira and the references therein. In fact, even in the simplest case in which reduces to a Dirac measure, the existence of global solution hinges on the initial condition; it is easy to see that solutions blow up when is not chosen in a suitable manner.

We now state a result on the global existence and uniqueness of (5), (6). It states that the solution takes values in the locally convex space endowed with topology of locally uniform convergence. For integers , the space will consist of all continuous functions which, when considered as functions for some compact subset of , belong to .

Theorem 1.

When the initial value problem (5), (6) admits a unique solution in the class of functions in that satisfy an inequality of the form

| (7) |

where is a constant that may depend on and locally uniformly on . Moreover, has the following properties.

-

(a)

is strictly positive.

-

(b)

is symmetric: for all .

-

(c)

for all .

-

(d)

.

-

(e)

For every , the kernel is nonnegative definite on , i.e.,

(8) -

(f)

The functions and satisfy local Lipschitz conditions in , locally uniformly in .

In Section 1.3 we will discuss computational aspects of the initial value problem (5), (6). In particular, we will discuss its solution when is an exponential polynomial of the form (3) and we will provide closed-form solutions in the cases and .

We can now explain how to use singular control in approaching the minimization of or . To this end, using order execution strategies will be more convenient than using the formalism of the associated measures because of the natural dynamic interpretation of . Henceforth, a -admissible strategy will be a left-continuous function of bounded variation such that . Our goal is to minimize the cost functional defined in (1) over all -admissible strategies with fixed initial value . Clearly, this problem is not yet suitable for the application of control techniques since depends on the entire path of . We therefore introduce the auxiliary functions

| (9) |

These functions will play the role of state variables that are controlled by the strategy .

Lemma 1.

For any -admissible strategy , the function is uniformly bounded in and . Moreover,

| (10) |

where denotes the jump of at .

Proof. Clearly, , where denotes the total variation of over . To obtain (10), we integrate by parts to get

Now we write as and apply Fubini’s theorem. ∎.

The form (10) of our cost functional is now suitable for the application of control techniques. To state our main result, we let be the solution of our infinite-dimensional Riccati equation as provided by Theorem 1 and we define

| (11) |

Theorem 2.

Let be the unique optimal strategy in the class of -admissible strategies with initial value . Then

| (12) |

Moreover, has jumps at and of size

and is continuously differentiable on . The derivative is the unique continuous solution of the Volterra integral equation

| (13) |

where, for

| (14) |

the function and the kernel are given by

| (15) |

Let us recall that we know in addition from Theorem 2.20 in \citeasnounGSS that is monotone. The identity (12) immediately yields the following formula for the capacity of a compact interval.

Corollary 2.

If , the capacity of a compact interval is given by

1.3 Computational aspects

In general, the Riccati equation (5), (6) cannot be solved explicitly. A closed-form solution exists, however, when is an exponential polynomial as in (3), i.e., when has a discrete support. Let us assume that , with , , and . All the input that is needed in Theorem 2 are the values , for . By Theorem 1, is a symmetric matrix that solves the following matrix Riccati equation:

| (16) |

with , , and . According to \citeasnounLevin, the solution of this equation is given by

where and

In the special cases and , the solution of the Riccati equation (5), (6) becomes even easier and, to some extend, becomes explicit. We demonstrate this first for and then for :

Example 1.

Example 2.

In the case , we can assume that is of the form , where . Consider a solution of the matrix Riccati equation (16) with . We can simplify (16) by using the relation

| (17) |

Indeed, the equation for then becomes

This is an autonomous ODE that, for the initial condition , is solved by

| (18) |

where

We can notice that and .

Similarly,

which for the initial condition is solved by

| (19) |

where

From (17) we can now easily compute .

Next, using once again (17), we find that solves

That is,

| (20) |

We set , , and , so that . Then, we can check that is a solution of the fundamental system. By using a variation of parameters, we get that the solution of (20) satisfying is given by

with

Then, can be easily deduced from (17).

It remains to compute , which solves

We set and get after some calculations:

Thus, we finally get:

This completes this example.

Given the solution of the Riccati equation, we can approximate the continuous time strategy by a discrete one as follows ( will denote the trading size at time ).

-

•

We first set and , .

-

•

Suppose that and that and have been computed. Then, we set thanks to (59):

-

•

Set .

Alternatively, we could have approximated the minimization of the cost (1) by the following discrete problem. Let , , and consider

| (22) |

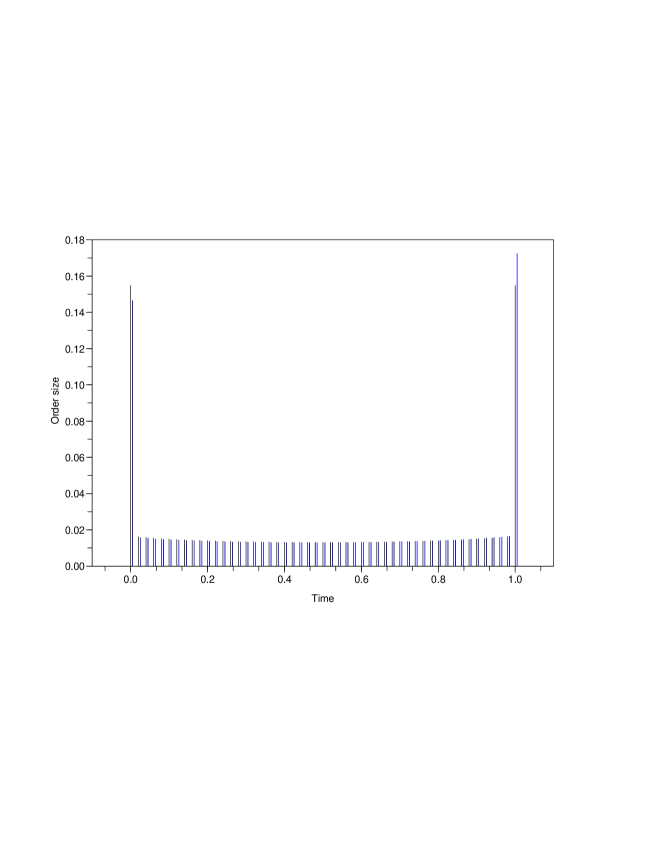

The solution of this problem is obviously given by , where for . From a financial point of view, the minimization problem (22) gives the optimal strategy when it is only possible to trade at the times , while the original problem (1) allows to trade continuously. In potential theory, it corresponds to computing the capacitary distribution of the set . It was shown in the proof of Theorem 2.20 in \citeasnounGSS that for these cap2acitary distributions converge in the weak topology of probability measures to the capacitary distribution constructed in Theorem 2. Explicit solutions of (22) for the choices and were given in \citeasnounAFS1 and \citeasnounASS (note, however, that is not completely monotone).

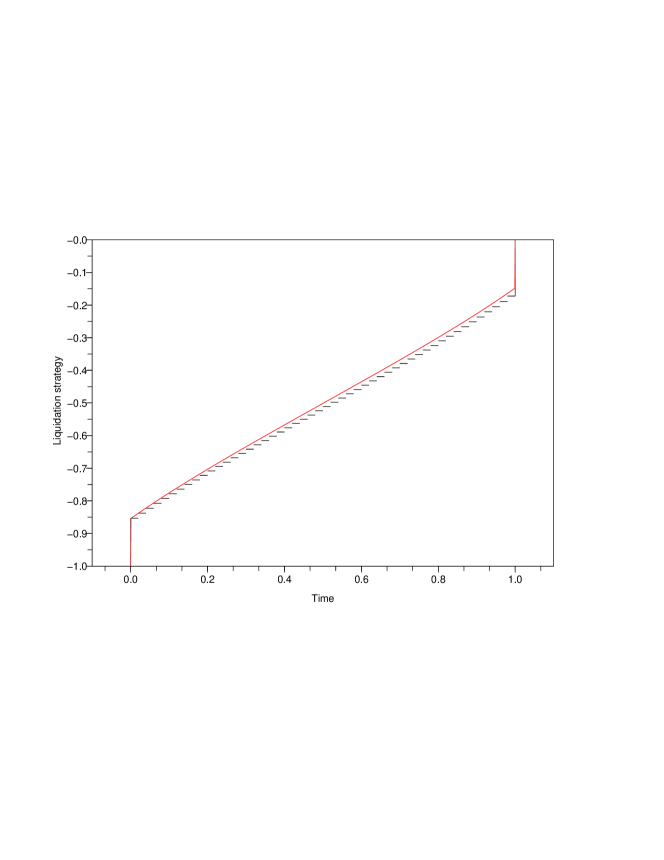

We have computed and plotted the solutions given by both methods in Figure 2 for , , and . They are already rather close together for , and they merge when . Let us discuss briefly the time complexity of the two methods. The one given by (22) gets very slow when gets large since it involves the inversion of a matrix. Instead, when has a discrete support, the matrix Riccati equation can be solved quickly and the algorithm above has a time complexity, which is much faster. However, this is no longer true when does not have discrete support. In that case, we have to approximate by a discrete measure, which means that we have to increase . Doing so, will slow down the algorithm based on the Riccati equation. A rigorous treatment of the convergence rate and time complexity of both algorithms is beyond the scope of this paper and is left for future research.

2 Proofs

2.1 Proof of Theorem 1

Let us write (5) in the form , where

| (23) |

Lemma 2.

Proof. Let be any compact interval containing . Then defined in (23) maps into itself. Moreover, is Lipschitz continuous with respect to the sup-norm on every bounded subset of . Hence, the Cauchy–Lipschitz/Picard–Lindelöf theorem in Banach spaces implies the existence of a unique local solution for some maximal time [HillePhillips, Theorem 3.4.1]. We will show below that . Then, if is another compact interval, the restriction of to must coincide with due to the uniqueness of solutions. This consistency then implies the existence and uniqueness of solutions . Moreover, the uniqueness of solutions and the fact that both (5) and (6) are symmetric in and implies that for all , which is property (b) in Theorem 1.

We now fix an interval . Before proving that , we will show that

| (24) |

This then will establishes property (c) in the statement of Theorem 1 for . Then we will use (24) to derive some estimates on that will yield and .

To prove (24), we let and . We have

| (25) |

This is a (non-homogeneous) affine ODE of the form , where the operator

is a continuous map from into the space of bounded linear operators on for each . Hence this ODE admits a unique solution in with initial condition . But (25) is solved by , which which establishes (24).

For the next step, we let

Since is a continuous map from into and , we must have . Due to (24) we have on that

| (26) |

When defining

| (27) |

the preceding inequality can be rewritten as

Integrating these inequalities yields that for

| (28) |

with the convention for . Hence

| (29) |

Inequality (28) ensures that . Both inequalities (28) and (29) ensure the solution does not explode in finite time, which by standard arguments yields that . This proves the global existence of solutions as well as property (a) in the statement of Theorem 1. ∎

The preceding lemma works only for measures that are concentrated on a finite interval. To obtain solutions for more general measures , we need to find upper bounds that are independent of . To this end, we first derive such bounds for the function defined in (11). By Lemma 2, this function is well-defined whenever has compact support, and it follows from dominated convergence together with (28) and (29) that and that .

Lemma 3.

Under the assumptions of Lemma 2, we have

| (30) |

Proof. The lower bound in (30) is clear from . To prove the upper bound, we suppose by way of contradiction that there exist , , and such that . Then there must be a compact interval such that

is finite. Since and , the time must also be strictly positive. Moreover, there exists such that

Then is the first time at which the function reaches a new maximum, and so .

Integrating (5) with respect to and evaluating at gives

| (31) |

Since , the Cauchy–Schwarz inequality (or, alternatively, Jensen’s inequality) implies that . Moreover, the definition of and the fact that is supported on yield that . Plugging these two inequalities into (31) leads to

where is a polynomial function of degree two. It has the two roots and . Therefore for and in turn , which contradicts the fact that . ∎

Lemma 4.

Proof. The ODE (5) can be rewritten as

| (34) |

Defining as in (27) and using the upper bound in (30) thus yields that

| (35) |

Arguing as in the final step of the proof Lemma 2 now yields (32). By plugging (32) back into (34) and using once again (30), we obtain (33).∎

Lemma 5.

For all , there exist constants , depending only on , , , and such that for all and ,

| (36) |

and

| (37) |

Proof. We consider and define

By subtracting the equation (34) satisfied by from the corresponding one satisfied by , we get

| (38) |

This equation is a linear non-homogeneous ODE for and, since , solved by

Since , we get with (32) and that

| (39) |

Now, we have that

For the last inequality, we have used Fubini’s theorem and (39). Now, Gronwall’s Lemma gives:

| (40) |

Plugging this back into (39), we get the existence of a constant , which depends only on , , , and , such that

| (41) |

Finally, using (40) and (41) in (38) and recalling the locally uniform bounds (32) and (30) on and gives (37). ∎

Now drop the assumption that is supported on a compact interval and aim at proving existence and uniqueness of solutions in this general case. To this end, we take a sequence for which and define

| (42) |

so that each satisfies the assumptions of Lemma 2. By we denote the corresponding solution of (5), (6) provided by that lemma. For each , we have

| (43) |

Hence, Lemma 4 yields that for each ,

| (44) |

and

| (45) |

Similarly, Lemma 5 yields that for all , there is a constant such that for all

| (46) |

The inequalities (45), (46) and the Arzela–Ascoli theorem imply that the sequence is relatively compact in the class of continuous functions on whenever , , and hence admits a convergent subsequence in that class. By passing to a subsequence arising from a diagonalization argument if necessary, we may assume that there exists a continuous function such that locally uniformly.

The uniform bounds (44) and dominated convergence imply that

| (48) | |||||

locally uniformly in . Hence, , locally uniformly in , where is defined through (23). Since , we conclude that locally uniformly in . Moreover, we have for each that

The left-hand side of this equation converges to , whereas the right-hand side converges to . This proves that solves (5) and that .

Remark 2.

Now we turn to prove the uniqueness of solutions in the class of functions satisfying a bound of the form (7) To this end, let and be two solutions in that class and set

We will show that for all , whenever is a positive finite Borel measure of the form , where is a positive finite Borel measure with compact support. Taking, for instance, as the Lebesgue measure on will then imply that for . So this will give the uniqueness of solutions.

Let us define as

| (51) |

Lemma 6.

We have and

| (52) |

where is a positive constant that depends only on and .

Proof. For simplicity, we will drop the argument throughout the proof. We may write

Thus,

Now we integrate this inequality with respect to . The two first terms can be analyzed in the same way. First, we observe that is finite. Then we note that

| (53) |

Hence,

Thus, the two first terms can be bounded by , where is a constant that only depends on and . Using once again (53), we get that the third term can be bounded from above by , where the constant depends only on and .∎

Now we differentiate and integrate over :

We now integrate w.r.t. and get by using the Cauchy–Schwarz inequality,

By continuity of , we know that for each there is a constant such that when . Thus, we get from Lemma 6 that

which in turn gives that on by Gronwall’s Lemma. This concludes the proof of uniqueness.

Now we turn to proving the properties (a) through (f) in Theorem 1. Property (a) (strict positivity) can be proved just as in the case of a compactly supported measure in Lemma 2. Property (b) (symmetry) is already clear. Property (c) () follows from the corresponding property of the approximating functions , the uniform bounds (44), and dominated convergence.

Property (d) states that . By dominated convergence and the bound (45), which also holds for in place of , we get that belongs to . Thus, our ODE gives , which proves property (d).

We now prove property (e). It is clearly enough to prove it when is a bounded measurable function with compact support. To this end, let . Then belongs to and

That is, for a function . Thus,

Since , we find that is nonnegative definite. Finally, with ,

This establishes property (e) in Theorem 1.

2.2 Proof of Theorem 2

The strategy in the proof of Theorem 2 is to use a verification argument and based on guessing the optimal costs for liquidating shares over with additional and arbitrary initial data . The result of our guess is formula (54) below. We explain its heuristic derivation in Appendix A.

Let be a solution of the infinite-dimensional Riccati equation (5), (6). This solution gives rise to a family of linear operators defined by

By (7), is a continuous map into both and for each . By the inequality (45), which also hold for in place of , is a continuously differentiable map into both and for each .

For , , and , we define

| (54) |

where denotes the usual inner product in . For and a -admissible strategy we define

By Lemma 1, the first two terms on the right correspond to the cost accumulated by the strategy up to time . Moreover,

due to the requirement . This gives . Our goal is thus to show the following verification lemma: with equality if and only if for a certain strategy . This will identify as the optimal strategy and as the optimal cost for liquidating shares over with additional initial data at time . In the formalism of potential theory, will then be the minimal energy of a probability measure on .

Lemma 7.

For every -admissible strategy , is absolutely continuous in and

| (55) |

for a.e. .

Proof. Recall the following integration by parts formula for left-continuous functions of locally bounded variation:

It follows that is of bounded variation and

| (56) |

as well as

| (57) |

Therefore,

We have already observed in the proof of Lemma 1 that is uniformly bounded in and by the total variation of . Hence we may integrate both sides of the preceding identity with respect to to obtain, with the symmetry of and the notation , that

By a similar reasoning we obtain

and

Using these formulas, we can now compute

Therefore, is absolutely continuous on and has the derivative

for a.e. .

To further analyze the preceding formula, we take an extra point . We let and extend and to functions on by putting

| (58) |

We furthermore define the function

and we extend the definition of via for . Finally, we set for , and one easily checks that .

With this notation, we get

where we have used the Riccati equation (5) and the notation (11) in the fourth step. This proves the assertion.∎

It follows from the above that a -admissible strategy with satisfies

for all other -admissible strategies with if vanishes for a.e. . Using (55), we write this latter condition as

| (59) |

where

Then

| (60) |

Plugging this and (56) into (59) yields that for a.e.

| (61) |

Thus, the left-continuous function coincides with an absolutely continuous function for a.e. . It follows that these two functions coincide for every . Thus, is continuous on by (56), which in turn implies via (61) that is continuously differentiable throughout .

When taking the limit in (61), we get

which gives

| (62) |

That follows from Remark 2.10 in \citeasnounGSS.

Since is continuously differentiable in , is also continuously differentiable in . Differentiating (59) with respect to yields

where we have used (56) and (60) in the second step. This gives

| (63) |

We now want to simplify (63). To this end, we use the notation and the formulas

| (64) | |||||

Then a tedious computation shows that

where is as in (14). Therefore, (63) becomes

| (65) |

Now we have . Plugging this formula back into (65) and using Fubini’s theorem yields that solves the Volterra integral equation (13). This is a Volterra integral equation of the second kind with continuous kernel and continuous function . It hence admits a unique continuous solution [Linz, Theorem 3.1]. Conversely, given such a solution , we can define a -admissible strategy via (62) and . Then satisfies (61) for as well as (63) for . Integrating (63) and reversing the steps made above in deriving (63) from (61) shows that satisfies (61) for , and so is optimal. This concludes the proof of Theorem 2.∎

Appendix A Heuristic derivation of the value function

We want to explain here how it is possible to guess the value function introduced in (54). We start our discussion by deriving a formula for the costs of a strategy that is arbitrary on and optimal on . We set

The rightmost integral can be written as

where

The first-order condition of optimality thus reads

| (66) |

where is a suitable Lagrange multiplier (compare Theorem 2.11 in \citeasnounGSS).

Lemma 8.

Suppose that and are functions with finite variation such that and

Then for all .

Proof. We have and hence that

which implies the assertion in view of the fact that is strictly positive definite.∎

Now suppose that we have auxiliary functions with finite variation such that and

We also define

so that

| (67) |

Therefore,

Lemma 8 hence implies that Hence, we get

From these identities we get

since the first double integral is equal to . Now we define

Then, we have

Moreover, we observe that since . This gives in particular that . Besides, we have

Thus, we obtain altogether that

This suggests the definition

so that we have

| (68) |

Thus, we have obtained the formula given by (54), and it remains to explain why should solve a Riccati equation. To do so, we consider an arbitrary strategy and consider the cost (68), which is the cost of the strategy that is equal to on and optimal on . To make the dependence on explicit, we denote this cost by . To simplify things, we will focus on the particular case (3) of a discrete measure , with , , and . With this choice, only depends on , . We introduce the following notations:

Lemma 9.

We have for all .

Proof. Note that . Hence it is clear that if . Now suppose that . Then

| (69) |

On the other hand, we have

Here we have used the facts that and . Putting everything together yields the assertion. ∎

We can now focus on infinitesimal variations, and we denote , and . We have, when ,

By simple calculations, we get , and our expression simplifies to

Let us now calculate :

To simplify computations, we define

| (70) |

as well as and . Then

With , we get and therefore

Altogether, we obtain

where is defined according to (70).

Thus, we arrive at the following quadratic form . Since we should have with for the optimal strategy, this quadratic form should be nonnegative with rank one. Indeed, since the control is of dimension one, it would not be possible to make if the rank of the quadratic form were higher than two. We are now going to write the conditions that ensures that this quadratic form is nonnegative with rank one. To do so, We introduce the new coordinates such that

In these coordinates, our quadratic form becomes

After some calculations, we get that the coefficient for , , and (for ) are respectively , , and .

Thus, the matrix for the quadratic form has coefficients

Since is of rank one, the determinant of the matrices

must vanish for and . That gives, respectively,

| (71) |

which gives precisely the Riccati equation. Thus, equation (71) holds for . In fact, the choice of is arbitrary. Had we chosen for some , we had obtained (71) for . Therefore (71) holds in fact for all .

References

- [1] \harvarditemAikawa \harvardand Essén1996AikawaEssen Aikawa, H. \harvardand Essén, M. \harvardyearleft1996\harvardyearright, Potential theory—selected topics, Vol. 1633 of Lecture Notes in Mathematics, Springer-Verlag, Berlin.

- [2] \harvarditem[Alfonsi et al.]Alfonsi, Fruth \harvardand Schied2008AFS1 Alfonsi, A., Fruth, A. \harvardand Schied, A. \harvardyearleft2008\harvardyearright, ‘Constrained portfolio liquidation in a limit order book model’, Banach Center Publications 83, 9–25.

- [3] \harvarditem[Alfonsi et al.]Alfonsi, Fruth \harvardand Schied2010AFS2 Alfonsi, A., Fruth, A. \harvardand Schied, A. \harvardyearleft2010\harvardyearright, ‘Optimal execution strategies in limit order books with general shape functions’, Quant. Finance 10, 143–157.

- [4] \harvarditemAlfonsi \harvardand Schied2010AS Alfonsi, A. \harvardand Schied, A. \harvardyearleft2010\harvardyearright, ‘Optimal trade execution and absence of price manipulations in limit order book models’, SIAM J. Financial Math. 1, 490–522.

- [5] \harvarditem[Alfonsi et al.]Alfonsi, Schied \harvardand Slynko2012ASS Alfonsi, A., Schied, A. \harvardand Slynko, A. \harvardyearleft2012\harvardyearright, ‘Order book resilience, price manipulation, and the positive portfolio problem’, SIAM J. Financial Math. 3, 511–533.

- [6] \harvarditemChoquet1954choquet Choquet, G. \harvardyearleft1954\harvardyearright, ‘Theory of capacities’, Annales de l’institut Fourier 5, 131–295.

- [7] \harvarditemFuglede1960fuglede Fuglede, B. \harvardyearleft1960\harvardyearright, ‘On the theory of potentials in locally compact spaces’, Acta mathematica 22, 139–215.

- [8] \harvarditemGatheral2010Gatheral Gatheral, J. \harvardyearleft2010\harvardyearright, ‘No-dynamic-arbitrage and market impact’, Quant. Finance 10, 749–759.

- [9] \harvarditemGatheral \harvardand Schied2012GatheralSchiedSurvey Gatheral, J. \harvardand Schied, A. \harvardyearleft2012\harvardyearright, ‘Dynamical models of market impact and algorithms for order execution’, To appear in Handbook on Systemic Risk .

- [10] \harvarditem[Gatheral et al.]Gatheral, Schied \harvardand Slynko2011GSS2 Gatheral, J., Schied, A. \harvardand Slynko, A. \harvardyearleft2011\harvardyearright, Exponential resilience and decay of market impact, in F. Abergel, B. Chakrabarti, A. Chakraborti \harvardand M. Mitra, eds, ‘Econophysics of Order-driven Markets’, Springer-Verlag, pp. 225–236.

- [11] \harvarditem[Gatheral et al.]Gatheral, Schied \harvardand Slynko2012GSS Gatheral, J., Schied, A. \harvardand Slynko, A. \harvardyearleft2012\harvardyearright, ‘Transient linear price impact and Fredholm integral equations’, Math. Finance 22, 445–474.

- [12] \harvarditemHelms2009Helms Helms, L. L. \harvardyearleft2009\harvardyearright, Potential theory, Universitext, Springer-Verlag London Ltd., London.

- [13] \harvarditemHille \harvardand Phillips1957HillePhillips Hille, E. \harvardand Phillips, R. S. \harvardyearleft1957\harvardyearright, Functional analysis and semi-groups, American Mathematical Society Colloquium Publications, vol. 31, American Mathematical Society, Providence, R. I. rev. ed.

- [14] \harvarditemLandkof1972landkof Landkof, N. \harvardyearleft1972\harvardyearright, Foundations of Modern Potential Theory, Springer Verlag, Berlin Heidelberg New York.

- [15] \harvarditemLevin1959Levin Levin, J. J. \harvardyearleft1959\harvardyearright, ‘On the matrix Riccati equation’, Proc. Amer. Math. Soc. 10, 519–524.

- [16] \harvarditemLinz1985Linz Linz, P. \harvardyearleft1985\harvardyearright, Analytical and numerical methods for Volterra equations, Vol. 7 of SIAM Studies in Applied Mathematics, Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA.

- [17] \harvarditem[Moro et al.]Moro, Vicente, Moyano, Gerig, Farmer, Vaglica, Lillo \harvardand Mantegna2009MoroEtAl Moro, E., Vicente, J., Moyano, L. G., Gerig, A., Farmer, J. D., Vaglica, G., Lillo, F. \harvardand Mantegna, R. N. \harvardyearleft2009\harvardyearright, ‘Market impact and trading profile of hidden orders in stock markets’, Physical Review E 80(6), 066–102.

- [18] \harvarditemObizhaeva \harvardand Wang2013ow Obizhaeva, A. \harvardand Wang, J. \harvardyearleft2013\harvardyearright, ‘Optimal trading strategy and supply/demand dynamics’, Journal of Financial Markets 16, 1–32.

- [19] \harvarditem[Predoiu et al.]Predoiu, Shaikhet \harvardand Shreve2011PredoiuShaikhetShreve Predoiu, S., Shaikhet, G. \harvardand Shreve, S. \harvardyearleft2011\harvardyearright, ‘Optimal execution in a general one-sided limit-order book’, SIAM J. Financial Math. 2, 183–212.

- [20] \harvarditemSchied \harvardand Slynko2011SchiedSlynko Schied, A. \harvardand Slynko, A. \harvardyearleft2011\harvardyearright, Some mathematical aspects of market impact modeling, in J. Blath, P. Imkeller \harvardand S. Roelly, eds, ‘Surveys in Stochastic Processes. Proceedings of the 33rd SPA’, EMS Series of Congress Reports.

- [21] \harvarditemTeixeira2005Teixeira Teixeira, E. V. \harvardyearleft2005\harvardyearright, ‘Strong solutions for differential equations in abstract spaces’, J. Differential Equations 214(1), 65–91.

- [22] \harvarditemWidder1941Widder Widder, D. V. \harvardyearleft1941\harvardyearright, The Laplace Transform, Princeton Mathematical Series, v. 6, Princeton University Press, Princeton, N. J.

- [23]