Conditional inference with a complex sampling: exact computations and Monte Carlo estimations

Abstract

In survey statistics, the usual technique

for estimating a population

total consists in summing appropriately weighted variable values for

the units in the sample. Different weighting systems exit: sampling

weights, GREG weights or calibration weights for example.

In this article, we propose to use the

inverse of conditional

inclusion probabilities as weighting system. We study examples where

an auxiliary information enables to perform an a posteriori

stratification of the population. We show that, in these cases,

exact computations of the conditional weights are possible.

When the auxiliary information consists in the knowledge of a

quantitative variable for all the units of the population, then we

show that the conditional weights can be estimated via Monte-Carlo

simulations. This method is applied to outlier and strata-Jumper

adjustments.

Keywords: Auxiliary information; Conditional inference; Finite population; Inclusion probabilities; Monte Carlo methods; Sampling weights

1 Introduction

The purpose of this article is to give a

systematic use of the auxiliary information at the

estimation phase by the means of Monte Carlo methods, in a design based approach.

In survey sampling, we often face a situation where we use information about the population (auxiliary information) available only at the estimation phase. For example, this information can be provided by an administration file available only posterior to the collection stage. Another example would be the number of respondents to a survey. It is classical to deal with the non-response mechanism by a second sampling phase (often Poisson sampling conditional to the size of the sample). The size of the respondents sample is known only after the collection.

This information can be compared to its counterpart estimated by the

means of the sample. A significant difference typically reveals an

unbalanced sample. In order to take this discrepancy into account,

it is necessary to re-evaluate our estimations. In practice, two

main technics exist: the model-assisted approach (ratio estimator,

post-stratification estimator, regression estimator) and the

calibration approach. The conditional approach we will develop in

this article has been so far mainly a theoretical concept because it

involves rather complex computations of the inclusion probabilities.

The use of Monte-Carlo methods could be a novelty that would enable

the use of conditional approach in practice.

In particular, it seems to be very helpful for the treatment of outliers and strata jumpers.

Conditional inference in survey sampling means that, at the

estimation phase, the sample selection is modelized by means of a

conditional probability. Hence, expectation and variance of the

estimators are computed according to this conditional sampling

probability. Moreover, we are thus provided with conditional

sampling weights with better properties than the original sampling

weights, in the sense

that they lead to a better balanced sample (or calibrated sample).

Conditional inference is not a new topic and several authors have

studied the conditional expectation and variance of estimators,

among them: Rao (1985), Robinson(1987), Till (1998, 1999) and

Andersson (2004). Moreover, one can see that the problematic of

conditional inference is close to inference in the context of

rejective sampling design. The difference is that in rejective

sampling, the conditioning event is controlled by the design,

whereas, in conditional

inference, the realization of the event is observed.

In section 2, the classical framework of finite population sampling and some notations are presented.

In section 3, we discuss the well-known setting of simple random

sampling where we condition on the sizes of the sub-samples on

strata (a posteriori stratification). This leads to an alternative

estimator to the classical HT estimator. While a large part of the

literature deals with the notion of correction of conditional bias,

we will directly use the concept of conditional HT estimator (Till ,

1998), which seems more natural under conditional inference. A

simulation study will be performed in order to compare the accuracy

of the conditional strategy

to the traditional one.

In section 4, the sampling design is a Poisson sampling conditional to sample size (also called conditional Poisson

sampling of size ). We use again the information about the sub-samples sizes

to condition on. We show that the conditional probability corresponds exactly

to a stratified conditional Poisson sampling and we give recursive formula

that enables the calculation of the conditional inclusion probabilities. These results are new.

In section 5, we use a new conditioning statistic. Following Till

(1998, 1999), we use the non-conditional HT estimation of the mean

of the auxiliary variable to condition on. Whereas Till uses

asymptotical arguments in order to approximate the conditional

inclusion probabilities, we prefer to perform Monte Carlo

simulations to address a non-asymptotic setting. Note that this idea

of using independent replications of the sampling scheme in order to

estimate inclusion probabilities when the

sampling design is complex has been already proposed by Fattorini (2006) and Thompson and Wu (2008).

In section 6, we apply this method to practical examples: outlier and strata jumper in business survey. This new method to deal with outliers gives good results.

2 The context

Let be a finite population of size . The statistical units of

the population are indexed by a label . A

random sample without replacement is selected using a

probability (sampling design) . is the set of

the possible samples . is the indicator variable

which is equal to one when the unit is in the sample and

otherwise. The size of the sample is . Let be

the set of samples that contain . For a fixed individual , let

be the inclusion probability and let be its

sampling weight. For any variable that takes the value on the -unit ,

the sum is referred to as the total of over .

is the Horvitz-Thompson estimator of the total .

Let be an auxiliary variable that takes the value for the

individual . The are assumed to be known for all the units

of . Such auxiliary information is often used at the sampling

stage in order to improve the sampling design. For example, if the

auxiliary variable is a categorical variable then the sampling can

be stratified. If the auxiliary variable is quantitative, looking

for a balanced sampling on the total of is a natural idea. These

methods reduce the size of the initial set of admissible samples.

In the second example, .

We wish to use auxiliary information after the sample

selection, that is to take advantage of information such as the

number of units sampled in each stratum or the estimation of the

total given by the Horvitz-Thompson estimator. Let us take an

example where the sample consists in men and women, drawn

by a simple random sampling of size among a total population

of with equal inclusion probabilities . And let

us assume that we are given a posteriori the additional

information that the population has men and women. Then

it is hard to maintain anymore that the inclusion probability for

both men and women was actually . It seems more sensible to

consider that the men sampled had indeed a inclusion probability of

and a weight of . Conditional inference aims at giving some

theoretical

support to such feelings.

We use the notation for the statistic that will be used in the conditioning. is a random vector that takes values in . In fact, will often be a discrete random vector which takes values in . At each possible subset corresponds an event .

For example, if the auxiliary variable is the indicator

function of a domain, say if the unit is a man, then we

can choose the sample size in the domain (number of men in

the sample). If the auxiliary variable is a quantitative

variable, then we can choose the

Horvitz-Thompson estimator of the total .

3 A posteriori Simple Random Sampling Stratification

3.1 Classical Inference

In this section, the sampling design is a simple random sampling

without replacement(SRS) of fixed size ; ; and the inclusion

probability of each individual is . Let be the

variable of study. takes the value for the individual

. The are observed for all the units of the sample. The

Horvitz-Thompson (HT) estimator of the total

is

.

Assume now that the population is split into sub-populations called strata.

Let , be the auxiliary information to be taken into account. We split the sample into

sub-samples defined by . Let be the size of the sub-sample .

Ideally, to use the auxiliary information at the sampling stage

would be best. Here, a simple random stratified sampling (SRS

stratified) with a proportional allocation would be more

efficient than a SRS.

For such a SRS stratified, the set of admissible samples is

, and the sampling design is

. Once again, our point is

precisely to consider setting where the auxiliary information becomes available posterior to this sampling stage

3.2 Conditional Inference

The a posteriori stratification with an initial SRS was described by Rao(1985) and Till (1998). A sample of size is selected. We observe the sizes of the strata sub-samples: , . We assume that . We then consider the event:

It is clear that , so is not empty.

We consider now the conditional probability: which will be used as far inference is concerned. The conditional inclusion probabilities are denoted

Accordingly, we define the conditional sampling weights: .

Proposition 1.

-

1.

The conditional probability is the law of a stratified simple random sampling with allocation ,

-

2.

For a unit of the strata : and .

Proof.

.

, . So we have:

and we recognize the probability law of a stratified simple random sampling

with allocation .

2. follows immediately.

∎

Note that

so that the genuine HT estimator is conditionally biased in this framework.

Even if, as Till (1998) mentioned, it is possible to correct this bias simply by retrieving it from the HT estimator, it seems more coherent to use another linear estimator constructed like the HT estimator but, this time, using the conditional inclusion probabilities.

Remark that in practice should not be too small. The idea is that

for any unit , we should be able to find a sample such that

and . Thus, all the units of have a positive conditional inclusion probability.

Definition 1.

The conditional HT estimator is defined as:

The conditional Horvitz-Thompson (CHT) etimator is obviously conditionally

unbiased and, therefore, unconditionally unbiased.

This estimator is in fact the classical post-stratification

estimator obtained from a model-assisted approach (see S rndal et

Al.(1992) for example). However, conditional inference leads to a

different

derivation of the variance, which appears to be more reliable as we will see in next subsection.

3.3 Simulations

In this part, we will compare the punctual estimations of a total according to two strategies:

(SRS design + conditional (post-stratification) estimator) and (SRS design + HT estimator).

The population size is , the variable is a quantitative

variable drawn from a uniform distribution over the interval . The population is divided into 4 strata corresponding to the

values of (if

then belongs to the strata 1 and so on …). The auxiliary information will be the size of each strata in

the population. In this example, we get , , and .

The finite population stays fixed and we simulate with the software

R simple random samples of size . Two estimators of

the mean are computed and

compared. The first one is the HT estimator: and the second one is the

conditional estimator:

.

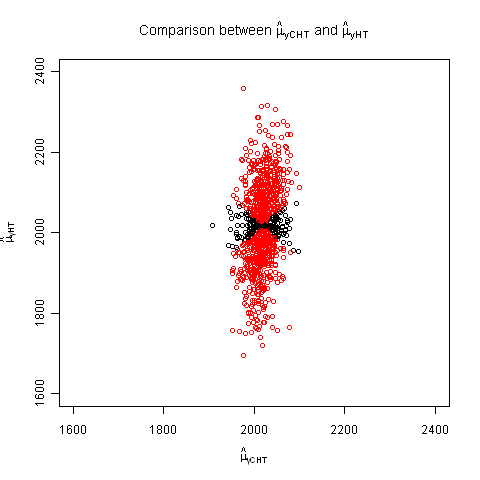

On Figure 1, we can see the values of

and for each of the

simulations. The red dots are those for which the conditional

estimation is closer to the true value than the

unconditional estimation; red dots represents 83.5% of the

simulations. Moreover, the empirical variance of the conditional

estimator

is clearly smaller than the empirical variance of the unconditional estimator.

This is completely coherent with the results obtained for the

post-stratification estimator in an model-assisted approach (see

S rndal et Al.(1992) for example). However, what is new and

fundamental in the conditional approach, is to understand that for

one fixed sample, the conditional bias and variance are much more

reliable than the unconditional bias and variance.

The theoretical study of the conditional variance estimation is a subject still to be developed.

3.4 Discussion

-

1.

The traditional sampling strategy is defined as a couple (sampling design + estimator). We propose to define here the strategy as a triplet (sampling design + conditional sampling probability + estimator).

-

2.

We have conditioned on the event: . Under a SRS, it is similar to use the HT estimators of the sizes of the strata in the conditioning, that is to use , where . Then, . We will see in Section 5 the importance of this remark.

-

3.

The CHT estimations of the sizes of the strata are equal to the true strata sizes , which means that the CHT estimations, in this setting, have the calibration property for the auxiliary information of the size of the strata. Hence, conditional inference gives a theoretical framework for the current practice of calibration on auxiliary variables.

4 A Posteriori Conditional Poisson Stratification

Rao(1985), Till (1999) and Andersson (2005) mentioned that a

posteriori stratification in a more complex setting than an an

initial SRS is not a trivial task, and that one must rely on

approximate procedures. In this section, we show that it is possible

to determine the conditional sampling design and to compute exactly

the conditional

inclusion probabilities for an a posteriori stratification with a conditional Poisson sampling of size .

4.1 Conditional Inference

Let be a Poisson sampling with inclusion probabilities

, where and

is the

complement of in . Under a Poisson sampling, the units are selected independently.

By means of rejective technics, a conditional Poisson sampling of

size can be implemented from the Poisson sampling. Then, the

sampling design is:

where .

The inclusion probabilities may be computed by means of a recursive method:

where .

This fact was proven by Chen et al.(1994) and one can also see Deville (2000), Matei and Till (2005), and Bondesson(2010). An alternative proof is given in Annex 1.

It is possible that the initial of the conditional Poisson sampling design are known

instead of the ’s. Chen et al.(1994) have shown that it is possible to inverse the functions

by the means of an algorithm which is an application

of the Newton method. One can see also Deville (2000) who gave an enhanced algorithm.

Assume that a posteriori, thanks to some auxiliary information, the

population is stratified in strata , . The

size of the strata is known to be equal to , and the size

of the sub-sample into is .

We consider the event .

Proposition 2.

With an initial conditional Poisson sampling of size :

-

1.

The probability conditional to the sub-samples sizes of the "a posteriori strata", , is the probability law of a stratified sampling with (independent) conditional Poisson sampling of size in each stratum,

-

2.

The conditional inclusion probability of an element of the strata is the inclusion probability of a conditional Poisson sampling of size in a population of size .

Proof.

1. For a conditional Poisson of fixe size n, a vector exists, where , such that:

where .

We remind that

Then:

where, is the law of the original Poisson sampling. Let , then:

which is the sampling design of a stratified

sampling with independent conditional Poisson sampling of size in each stratum.

2. follows immediately.

∎

Definition 2.

In the context of conditional inference on the sub-sample sizes of posteriori strata, under an initial conditional Poisson sampling of size , the conditional HT estimator of the total is:

The conditional variance can be estimated by means of one of the

approximated variance formulae

developed for the conditional Poisson sampling of size . See for example Matei and Till (2005), or Andersson(2004).

4.2 Simulations

We take the same population as in subsection 3.3.

The sampling design is now a conditional Poisson sampling of size .

The probabilities of the underlying Poisson design have been generated

randomly, in order that and .

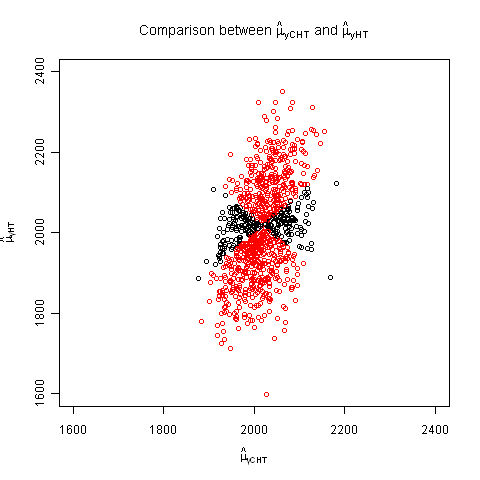

simulations were performed. Figure 2 shows that

the punctual estimation of the mean of is globally better for conditional inference.

According to of the simulations the conditional estimator is better

than the unconditional estimator (red dots).

The empirical variance as well is clearly better for the conditional estimator.

4.3 Discussion

This method allows to compute exact conditional inclusion probabilities in an "a posteriori stratification" under conditional Poisson of size . However, one can figure out that this method can be used for any unequal probabilities sampling design, had the sampling frame been randomly sorted.

5 Conditioning on the Horwitz-Thompson estimator of an auxiliary variable

In the previous sections, we used the sub-sample sizes in the strata

to condition on. The good performances of this conditional

approach result from the fact that the sizes of the sub-sample are

important characteristics of the sample that are often used at the

sampling stage. So, it was not surprising that the use of this

information at the estimation stage would enhance

the conditional estimators.

Another statistic that characterizes the representativeness of a

sample is its HT estimator of the mean (or total ) of

an auxiliary variable. This statistic is used at the sampling stage

in balanced sampling for example. So, as the sub-sample sizes into

the strata, this statistic should produce good results in a

conditional approach restraining the inference to the samples for

which the HT estimation

of are equal to the value of the selected sample .

In fact, we want the (conditional) set of the possible samples to be

large enough in order that all conditional inclusion probabilities

be different from zero. It is therefore convenient to consider the

set of samples that give HT estimations not necessarily strictly

equal to but close to .

Let , for some .

The set of possible samples in our conditional approach will be:

The conditional inclusion probability of a unit is:

If then we are in a good configuration, because we are in

a balanced sampling situation and the will certainly stay close to the .

If say, then the sample is

unbalanced, which means that in average, its units have a too large

contribution , either because they are too big (

large) or too heavy ( too large). In this case,

the samples in are also ill-balanced, because balanced

on instead of : . But conditioning on

this information will improve the estimation. Indeed, the

will be different from the . For example,

a unit with a big contribution ( large) has

more chance to be in a sample of than a unit with a

small contribution. So, we can expect that and .

And, in consequence, the

conditional weight will be lower

than and higher than , which will "balance" the samples of .

Discussion:

-

•

we can use different ways in order to define the subset . One way is to use the distribution function of , denoted and to define as a symmetric interval:

where for example.

Hence,

and .

As the cdf is unknown in general, one has to replace it by an estimated cdf of , denoted , computed by means of simulations.

6 Generalization: Conditional Inference Based on Monte Carlo simulations.

In this section, we consider a general initial sample design

with the inclusion probabilities . We condition on the event

For example,

we can use the

unconditional HT estimator of and an interval that contains , the HT estimation of with the

selected sample . In other words, we will take into account the

information

that the HT estimator of the total of the auxiliary variable lies in some region .

The mathematical expression of is

straightforward:

But effective computation of the

’s may be not trivial if the distribution of

is complex. Till (1998) used an asymptotical

approach to solve this problem when ;

he has used normal approximations for the conditional and unconditional laws of .

In the previous sections, we have given examples where we were able

to compute the ’s (and actually the

’s) exactly. In this section, we give a general

Monte Carlo method to compute the .

6.1 Monte Carlo

We will use Monte Carlo simulations to estimate and . We repeat independently times the sample selection with the sampling design , thus obtaining a set of samples . For each simulation , we compute and . Then we compute statistics:

We obtain a consistent estimator of , as :

| (1) |

6.2 Point and variance estimations in conditional inference

Definition 3.

The Monte Carlo estimator of the total is the conditional Horvitz-Thompson estimator of after replacing the conditional inclusion probabilities by their Monte Carlo approximations:

The Monte Carlo estimator of the variance of is:

where

Fattorini(2006) established that is asymptotically unbiased as ,

and that its mean squared error converges to the variance of .

Thompson and Wu (2008) studied the rate of convergence of the estimators and of the estimator following Chebychev’s inequality. Using normal approximation instead of the Chebychev’s inequality gives more precise confidence intervals. We have thus a new confidence interval for :

where is the distribution function of the normal law .

As for the relative bias, standard computation leads to:

| (2) | |||||

where . We used the inequality which is verified for large .

The number of simulations is set so that

reaches a pre-established

value. Because of our conditional framework, is

a stochastic variable which follows a negative binomial distribution

and we have .

For instance, if , with , we expect simulations.

7 Conditional Inference Based on Monte Carlo Method in Order to Adjust for Outlier and Strata Jumper

We will apply the above ideas to two examples close to situations that can be found in establishments surveys: outlier and strata jumper.

We consider an establishments survey, performed in year "n+1", and addressing year "n". The auxiliary information which is the turnover of the year "n" is not known at the sampling stage but is known at the estimation stage (this information may come from, say, the fiscal administration).

7.1 Outlier

In this section, the auxiliary variable is simulated following a gaussian law, more precisely excepted for unit for which we assume that . The unit is an outlier. The variable of interest is simulated by the linear model

where , is independent from . The outcomes are and

.

We assume that the sampling design of the establishments survey is a

SRS of size out of the population of size and

that the selected sample contains the unit . For this

example, we have repeated the sample selection until the unit

has been selected in .

We obtain , which is over the true value and

(recall that the true value of is ).

We set and as in section 5 and we use Monte

Carlo simulations in order to compute the conditional inclusion

probabilities

. Each simulation is a selection of a sample following

a SRS of size from the fixed population . Recall that the value of

will eventually be known for any unit .

Actually, we use two sets of simulations. The first set is performed in order to estimate the cdf of the statistic which will be used to condition on. This estimated cdf will enable us to construct the interval . More precisely, we choose the interval by the means of the estimated cdf of and so that .

is then the set of the possible samples in our conditional approach:

Note that . typically contains samples that over-estimate the mean of .

The second set of Monte Carlo simulations consists in

sample selections with a SRS of size performed in order to

estimate the conditional inclusion probabilities

. () simulated samples

fall in , and among them, samples contain the

outlier, which correspond to the estimated conditional inclusion

probability of the outlier: . It

means that almost all the samples of contain the outlier

that is mainly responsible for the over-estimation because of its

large value of the variable !

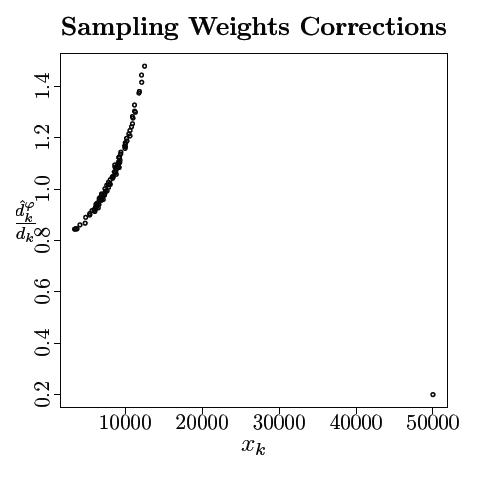

The weight of the unit has changed a lot, it has decreased from

to . The

conditional sampling weights of the other units of are more

comparable to

their initial weights (see Figure 7.1).

The conditional MC estimator

leads to a much better estimation of : .

![[Uncaptioned image]](/html/1201.1490/assets/outlier3.jpg)

Figure 7.1 gives an

idea of the conditional inclusion probabilities for all the units of

. Moreover, this graph shows that the correction of the sampling

weights is not a monotonic function

of , which is in big contrast with calibration techniques which

only uses monotonic functions for weight correction purposes.

A last remark concerns the distribution of the statistics

. Figure 3 shows

an unconditional distribution with 2 modes and far from gaussian.

This shows that in presence of outlier,

we can not use the method of Till (1999), which assumes a normal distribution for .

7.2 Strata Jumper

In this section, the population is divided into 2 sub-populations: the small firms and the large firms. Let us say that the size is appreciated thanks to the turnover of the firm. Official statistics have to be disseminated for this 2 different sub-populations. Hence, the survey statistician has to split the population into 2 strata corresponding to the sub-populations. This may not be an easy job because the size of firms can evolve from one year to another.

Here we assume that, at the time when the sample is selected, the

statistician does not know yet the auxiliary information of the

turnover of the firm for the year "n", more precisely the

strata the firm belongs to for the year "n". Let us assume

that he only knows this information for the previous

year,"n-1". This information is denoted by . In practice,

small firms are very numerous and the sampling rate for this strata is chosen low.

On the contrary, large firms are less numerous and their sampling rate is high.

When a unit is selected among the small firms but eventually happens

to be a large unit of year "n", we call it a strata jumper.

At the estimation stage, when the information becomes available,

this unit will obviously be transferred to strata 2 . This will

bring a problem, not due to its -value (which may well be typical

in strata 2) but to its sampling weight, computed according to

strata 1 (the small firms), and which will appear to

be very large in comparison to the other units in strata 2 at the estimation stage.

In our simulations, the population is split in 2 strata, by

means of the auxiliary variable : , of size

,

is the strata of presumed small firms and , of size , the strata of presumed large firms.

The auxiliary variable , which is the turnover of the year

"n" known after collection, is simulated under a gaussian law

for the units of the strata

and for one selected unit of the strata . Let us

say that this unit, the strata jumper, is unit .

Our simulation gives . The variable of interest is

simulated by the linear model , where

, and independent.

We do not simulate the value of and for the other units of

the strata because we will focus on the estimation of the

mean of for the sub-population of large firms of year

: . We

find

and is .

The sampling design of the establishments survey is a stratified SRS

of size in and in . We assume

that the selected sample contains the unit . In practice,

we repeat

the sample selection until the unit (the strata jumper) has been selected.

As previously, and are defined as in Section 5.

We use Monte Carlo simulations in order to compute

the conditional inclusion probabilities . A simulation is

a selection of a sample with stratified SRS of size in and in .

We choose the statistic in order to condition on. simulations are performed in order to estimate the cdf of and the conditional inclusion probabilities.

Our simulations give ,

which is far from the true value

and (recall that the true value of is ).

We choose the interval by the means of the estimated cdf of and so that .

is then the set of the possible samples in our

conditional approach:

All samples in over-estimate the mean of .

Among the simulations, simulated samples ()

belongs to . of them contains the strata jumper,

which gives the estimated conditional inclusion probability of the

strata jumper . It is not a surprise

that the strata jumper is in one sample of over two.

Indeed, its initial sampling

weight is high in comparison to the weights

of the other selected units

of the strata , and its contribution contributes to over-estimate the mean of .

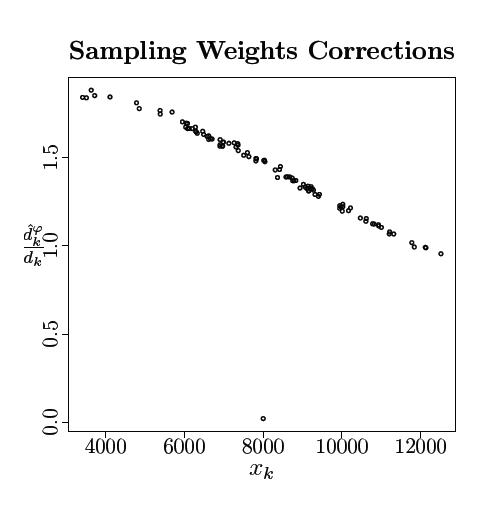

The conditional inclusion probabilities for the other units of are comparable to

their initial (see Figure 4).

The conditional MC estimator

leads to a better estimation of : .

Figure 4 shows that sampling weights correction is here

a non-monotonic function of the variable . We point out that the usual calibration

method would not be able to perform this kind of weights correction

because the calibration function used to correct the weights should be monotonic.

Similarly to the outlier setting, the

unconditional distribution of the statistics has 2 modes and is far from gaussian.

8 Conclusion

At the estimation stage, a new auxiliary information can reveal that

the selected sample is imbalanced. We have shown that a conditional inference

approach can take into account this information and leads to a more precise

estimator than the unconditional Horvitz-Thompson estimator in the sense that

the conditional estimator is unbiased (conditionally and unconditionally)

and that the conditional variance is more rigorous in order to estimate the precision a posteriori.

In practise, we recommend to use Monte Carlo simulations in order to estimate the conditional

inclusion probabilities.

This technic seems particularly adapted to the treatment of outliers

and strata-jumpers.

Appendix A Annex 1: Inclusion Probability with Conditional Poisson Sampling

References

- [1] Anderson, P.G. (2004). A conditional perspective of weighted variance estimation of the optimal regression estimator. Journal of statistical planning and inference.

- [2] Chen, X.-H., Dempster, A., and Liu, J. (1994). Weighted finite poplation sampling to maximize entropy. Biometrika, 81, 457-469.

- [3] Deville, J.C. (2000). Note sur l’algorithme de Chen, Dempster et Liu. Technical report, France CREST-ENSAI. [In French]

- [4] Fattorini L. (2006). Applying the Horvitz-Thompson criteion in complexe designs: A computer-intensive perspective for estimating inclusion probabilities. Biometrika, 93, 269-278.

- [5] Matei, A. and Till , Y. (2005). Evaluation of variance approximations and estimators in unequal probability sampling with maximum entropy. Journal of Official Statistics, 21, 543-570.

- [6] Rao, J.N.K. (1985). Conditional inference in survey sampling. Survey Methodology, 11, 15-31.

- [7] Robinson, J. (1987). Conditioning ratio estimates under simple random sampling. Journal of the American Statistical Association, 82, 826-831.

- [8] S rndal C.-E., Swenson B. and Wretman J. (1992). Model Assisted Survey Sampling. Springer-Verlag, 264-269.

- [9] Thompson M., E. and Wu C. (2008). Simulation-based Randomized Systematic PPS Sampling Under Substitution of Units. Survey Methodology, 34, 3-10.

- [10] Till , Y. (1998). Estimation in surveys using conditional inclusion probabilities: Simple random sampling. International Statistical Review, 66, 303-322.

- [11] Till , Y. (1999). Estimation in surveys using conditional inclusion probabilities: comlex design. Survey Methodology, 25, 57-66.