Efficient Estimation of Nonlinear Finite Population

Parameters Using Nonparametrics

Abstract

Currently, the high-precision estimation of nonlinear parameters such as Gini indices, low-income proportions or other measures of inequality is particularly crucial. In the present paper, we propose a general class of estimators for such parameters that take into account univariate auxiliary information assumed to be known for every unit in the population. Through a nonparametric model-assisted approach, we construct a unique system of survey weights that can be used to estimate any nonlinear parameter associated with any study variable of the survey, using a plug-in principle. Based on a rigorous functional approach and a linearization principle, the asymptotic variance of the proposed estimators is derived, and variance estimators are shown to be consistent under mild assumptions. The theory is fully detailed for penalized B-spline estimators together with suggestions for practical implementation and guidelines for choosing the smoothing parameters. The validity of the method is demonstrated on data extracted from the French Labor Force Survey. Point and confidence intervals estimation for the Gini index and the low-income proportion are derived. Theoretical and empirical results highlight our interest in using a nonparametric approach versus a parametric one when estimating nonlinear parameters in the presence of auxiliary information.

Keywords auxiliary information; penalized B-splines; calibration; concentration and inequality measures; influence function; linearization; model-assisted approach; total variation distance.

1 Introduction

The estimation of nonlinear parameters in finite populations has become a crucial problem in many recent surveys. For example, in the European Statistics on Income and Living Conditions (EU-SILC) survey, several indicators for studying social inequalities and poverty are considered; these include the Gini index, the at-risk-of-poverty rate, the quintile share ratio and the low-income proportion. Thus, deriving estimators and confidence intervals for such indicators is particularly useful. In the present paper, assuming that we have a single continuous auxiliary variable available for every unit in the population, we propose a general class of estimators that take into account the auxiliary variable, and we derive their asymptotic properties for general survey designs. The class of estimators we propose is based on a nonparametric model-assisted approach. Interestingly, the estimators can be written as a weighted sum of the sampled observations, allowing a unique weight variable that can be used to estimate any complex parameter associated with any study variable of the survey. Having a unique system of weights is very important in multipurpose surveys such as the EU-SILC survey.

The estimation of nonlinear parameters is a problem that has already been addressed in several papers such as Shao (1994) for L-estimators, Binder and Kovacevic (1995) for the Gini index and Berger and Skinner (2003) for the low-income proportion. We mention also the very recent work of Opsomer and Wang (2011). Taking auxiliary information into account for estimating means or totals is a topic that has been extensively studied in the literature; it now encompasses the model-assisted and the calibration approaches, which coincide in particular cases (Särndal, 2007). In a model-assisted setting, linear models are usually used, thus leading to the well-known generalized regression estimators (GREG). Some nonparametric models have also been considered (Breidt and Opsomer, 2009). However, to the best of our knowledge, ratios, distribution functions and quantiles are the only examples of nonlinear parameters estimated using auxiliary information.

To derive our class of estimators and their asymptotic properties, we use an approach based on the influence function developed by Deville (1999). This approach utilizes a functional interpretation of the parameter of interest and a linearization principle to derive asymptotic approximations of the estimators. In general, the precision of an estimator of a nonlinear finite population parameter is obtained by resampling techniques or linearization approaches and in the present paper we focus on linearization techniques. When a sample is selected from the finite population according to a sampling design , the linearization of leads under some assumptions, to the following approximation:

| (1) |

where denotes the first-order inclusion probability for element under the design . The right term of (1) is the difference between the well-known Horvitz-Thompson estimator and the parameter it estimates, namely the total of the variable over the population . Here, referred to as the linearized variable of and the way it is derived depends on the type of linearization method used which could include the Taylor series (Särndal et al., 1992), estimating equations (Binder, 1983) or influence function (Deville, 1999) approaches. The artificial variable is used to compute the approximative variance of as

| (2) |

with the joint inclusion probability for the elements

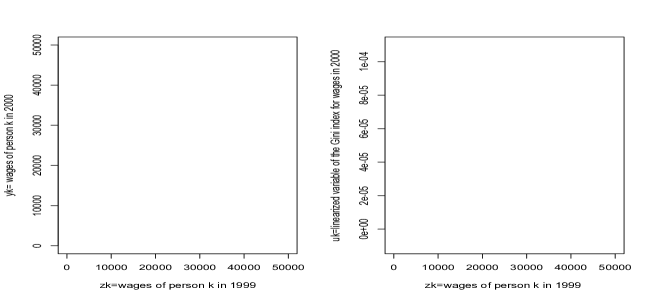

Roughly speaking, when examining (1) and (2), we can see that, if we estimate in an efficient way , we will achieve a small approximative variance and good precision for . As stated above, it is well known that auxiliary information is useful for improving on the estimation of a total in terms of efficiency and, based on a linear model, the use of a GREG estimator is the most common alternative. When estimating a total, note that the asymptotic variance of the GREG estimator depends on the residuals of the study variable on the auxiliary variable. Because linearized variables may have complicated mathematical expressions, fitting a linear model onto linearized variables may not be the most appropriate choice. This may occur even if the study and the auxiliary variables have a clear linear relationship, as illustrated in the following example. Consider a data set of size 1000 extracted from the French Labor Force Survey and consider (the wages of person in 2000) as the study variable and (the wages of person in 1999) as the auxiliary variable. We now consider the problem of estimating the Gini index. The expression of the linearized variable , for the Gini index is given in Binder and Kovacevic (1995) and recalled in equation (17). It is a complex function of the study variable , . In the left (resp. right) graphic of Figure 1, the study variable is plotted (resp. the linearized variable ) on the -axis and the auxiliary variable is plotted on the -axis. The relationship between the study variable and the auxiliary variable is almost linear; however the relationship between the linearized variable of the Gini index and the auxiliary information is no longer linear. The consequence of this is that we cannot increase the efficiency of estimating a Gini index if we take the auxiliary information into account through a GREG estimator. Therefore, nonparametric models should be preferred to estimate nonlinear parameters .

Recent work already employs nonparametric models to estimate totals (Breidt and Opsomer, 2000, Breidt et al., 2005 and Goga, 2005). The use of nonparametrics prevents model failure; however the improvement over parametric estimation for totals and means may not be significant enough to justify the supplemental difficulties of implementing nonparametric methodology. As illustrated above, the motivation for using nonparametrics becomes much stronger when estimating nonlinear parameters. Note that the use of nonparametric regression to estimate distribution functions and quantiles has also been studied, for example in Johnson et al. (2008); however, to our knowledge, this has not been performed for other nonlinear parameters.

We propose a novel methodology that allows for the efficient estimation of any parameter by combining the functional approach (Deville, 1999) with any of the previously suggested nonparametric methods. One issue with the functional approach is that several technical details are not provided in Deville (1999); thus it is difficult to derive rigorous proof of asymptotic results by following this approach. In the present paper, we propose to clarify some important points and derive rigorous proofs of our asymptotic results. Most importantly, we prove that the total variation distance between finite measures is an adequate choice for the derivation of asymptotic approximations in this context. Asymptotic results are detailed at length for penalized B-spline nonparametric estimators.

The estimators under study combine two types of nonlinearity: nonlinearity due to the expression of a complex parameter and nonlinearity due to nonparametric estimation. We propose a two-step linearization procedure that provides an approximation of the nonparametric estimator via a Horvitz-Thompson estimator of a total using an artificial variable. Roughly speaking, this artificial variable corresponds to the residuals of the linearized variable on the fitted values under the model. Because the linearized variables depend on the parameter of interest, the residuals will also depend on this parameter. The consequence of this important and general property is that the nonparametric approach helps to get a unique system of weights that may lead to a gain in efficiency for different complex parameters.

The paper is structured as follows: the second section provides some background information on the nonparametric estimation of a finite population total in a general framework. In the third section, a class of nonparametric substitution estimators based on nonparametric regression is introduced. Variance approximations are derived using the influence function linearization approach (Deville, 1999) in a general nonparametric setting. We propose in the fourth section a penalized B-spline model-assisted estimator for the finite population totals which is in fact an extension to a survey sampling framework of the penalized B-spline estimator studied in Claeskens et al. (2009). We prove that the estimator is asymptotically design-unbiased and consistent. Next, we build the nonparametric penalized spline estimation for nonlinear parameters and we assess the validity of the two-step linearization technique. The fifth section defines a class of consistent variance estimators while section six contains a case study. The data set is extracted from the French Labor Force surveys of 1999 and 2000 as presented previously. Asymptotic and finite-sample properties of the regression B-spline estimators are illustrated for the simple random sampling without replacement and the stratified simple random sampling. This section also includes suggestions for practical implementation and guidelines for choosing the smoothing parameters. Finally, section seven concludes this study and the assumptions and the technical proofs together with some discussion are provided in the Appendix.

2 Nonparametric model-assisted estimation of finite population totals

We focus on the estimation of the total of the study variable over , taking into account the univariate auxiliary variable The values of are assumed to be known for the entire population.

Many approaches can be used to take into account auxiliary information and thus improve on the Horvitz-Thompson estimator The goal is to derive a weighted linear estimator of such that the sample weights do not depend on the study variable values but include the values for all The construction of the model-assisted (MA) class of estimators is based on a superpopulation model :

| (3) |

where the are independent random variables with mean zero and variance If was known for all the total may be estimated by the generalized difference estimator (Cassel et al., 1976),

| (4) |

Note that consists in the difference between the Horvitz-Thompson estimator and its bias under the model namely . As a consequence, is unbiased under the model, and moreover, it is unbiased under the sampling design, The variance of under the sampling design is given by

| (5) |

which shows clearly that the difference estimator is more efficient than the Horvitz-Thompson estimator if approximates well for all

In practice, we don’t know the true regression function thus we use an estimator of it. Generally, this estimator is obtained using a two-step procedure: we estimate first by under the model and next, we estimate by using the sampling design. Plugging in (4), yields the final estimator of

The linear regression function yields the generalized regression estimator (GREG) extensively studied by Särndal et al. (1992). The GREG estimator is efficient if the model fits the data well, but if the model is misspecified, the GREG estimator exhibits no improvement over the Horvitz-Thompson estimator and may even lead to a loss of efficiency. One way of guarding against model failure is to use nonparametric regression which does not require a predefined parametric mathematical expression for .

Recently, Breidt and Opsomer (2000) proposed local linear estimators and Breidt et al. (2005) and Goga (2005) used nonparametric spline regression. The unknown function is approximated by the projection of the population vector onto different basis functions, such as the basis of truncated th degree polynomials in Breidt et al. (2005) and the B-spline basis in Goga (2005). In the following, we briefly recall the definition and the main asymptotic properties of nonparametric model-assisted estimators for finite population totals (see also Breidt and Opsomer, 2009).

Let be the estimator of obtained at the population level using one of the three nonparametric methods mentioned above. Plugging into (4) results in the following nonparametric generalized difference pseudo-estimator of the finite population total:

| (6) |

Note that is called a pseudo-estimator because it is not feasible in practice since is unknown. This pseudo-estimator is still design-unbiased but it is model-biased because nonparametric estimators are biased for (Sarda and Vieu, 2000). Nevertheless, under supplementary assumptions (Breidt and Opsomer, 2000 and Goga, 2005), the bias under the model vanishes asymptotically to zero when the population and the sample sizes go to infinity. The unknown quantities are usually obtained by least squares methods (ordinary, weighted or penalized) and we may write

| (7) |

where the dimensional vector depends on the population values as well as on the projection matrix for the considered basis functions, but does not depend on The expression of depends on the chosen nonparametric method, as discussed in Breidt and Opsomer (2000), Breidt et al. (2005) and Goga (2005).

As in the parametric case, we estimate by using the sampling design,

| (8) |

where is the -dimensional design-based estimator of and is the sample restriction of Plugging into (6) yields the following nonparametric model-assisted estimator (NMA)

| (9) |

This estimator can be written as a weighted sum of the sampled observations

| (10) |

where the weights depend only on the sample and on the auxiliary information,

| (11) |

with the dimensional vector of ones, the diagonal matrix with along the diagonal and the matrix having as rows with sample restriction The estimator (10) is a nonlinear function of Horvitz-Thompson estimators, and its asymptotic variance has been obtained on a case-by-case study. Under mild hypothesis (Breidt and Opsomer, 2000, Breidt et al., 2005 and Goga, 2005), is asymptotically design-unbiased, namely and design -consistent in the sense that

| (12) |

Moreover, it can be approximated by the nonparametric generalized difference estimator

| (13) |

Furthermore, if the asymptotic distribution of is normal , we have that the asymptotic distribution of is also normal where is obtained according to formula (5) applied to residuals This means that the NMA estimators bring an improvement over parametric methods and the Horvitz-Thompson estimator when the relation between and is not linear. In this case, the residuals will be smaller than under a parametric smoother, which explains the diminution of the design variance of NMA estimators. Nevertheless, nonparametric estimators require that the auxiliary information should be known on the whole population unlike the GREG estimator that requires only the finite population total for

The efficiency of NMA estimators depends on the choice of the smoothing parameters. Opsomer and Miller (2005) and Harms and Duchesne (2010) derive the optimal bandwidth for the local polynomial regression, while Breidt et al. (2005) circumvent the issue of the number of knots by introducing a penalty coefficient. They also give a practical method for estimating this penalty.

3 Nonparametric model-assisted estimation

of nonlinear finite population parameters

3.1 Definition of the nonparametric substitution estimator

Let us consider the estimation of some nonlinear parameters by taking into account univariate auxiliary information known for all the population units.

Examples of a nonlinear parameter of interest include the ratio, the Gini coefficient and the low-income proportion. A parameter may depend on one or several variables of interest; however, the same auxiliary variable will be used to explain these variables of interest.

We aim to provide a general method for the estimation of using and considering the functional approach introduced by Deville (1999). The methodology consists in

considering a discrete and finite measure where is the Dirac measure at the point and is such that there is unity mass on each point with and zero mass elsewhere. Furthermore, we write as a functional of

| (14) |

The nonparametric weights are provided by (11) and is estimated by

Even if these weights are derived to estimate the total they do not depend on the study variable ; thus they can be used to estimate any nonlinear parameter of interest when it can be expressed as a function of Note that is a random measure of total mass equal to

Plugging into (14) provides the following nonparametric substitution estimator for ,

We will now illustrate the computation of using the simple case of a ratio and subsequently

the more intricate case of the Gini index and parameters defined by implicit equations.

a. The ratio R between two finite population totals. We write in a functional form as The nonparametric estimator of is easily obtained by replacing the measure with namely A similar estimation of using GREG weights was previously considered by Särndal et al. (1992).

b. The Gini index. The Gini index (Nygard and Sandström, 1985) is given by

where is the empirical distribution function. Again, the nonparametric estimator for is obtained by simply replacing with Hence,

| (15) |

where

c. Parameters defined by an implicit equation. Let be defined as the unique solution of an implicit estimating equation (Binder, 1983) that may be written in a functional form as We replace with and the nonparametric sample-based estimator of is the unique solution of the sample-based estimating equation An example of such a parameter is the odds-ratio which is extensively used in epidemiological studies. Goga and Ruiz-Gazen (2012) have studied the estimation of the odds-ratio by taking into account auxiliary information and nonparametric regression.

3.2 Asymptotic properties of the nonparametric substitution estimator under the sampling design

In this section, we investigate the asymptotic properties of the nonparametric estimator , using the asymptotic framework suggested by Isaki and Fuller (1982). Additionally, we make several assumptions (detailed in the Appendix) regarding the regularity of the functional and the first order inclusion probabilities of the sampling design.

The nonparametric estimator is doubly nonlinear, with nonlinearity due to the parameter and nonlinearity due to the nonparametric estimation. Our main goal is to approximate using a linear estimator (Horvitz-Thompson type) which will allow to compute the asymptotic variance of This approximation will be accomplished in two steps: first, we will linearize and next, we will linearize the nonparametric estimator obtained in step one.

The first linearization step is a first-order expansion of with the reminder going to zero. The parameter of interest is a statistical functional defined with respect to the measure or equivalently, with respect to the probability measure (by assumption A1). Using the first-order expansion of statistical functionals as introduced by von Mises (1947) and under the assumption of Fréchet differentiability of , the reminder depends on some distance function between and an estimator of this measure (Huber, 1981). Deville (1999) uses these facts to prove the linearization of the Horvitz-Thompson substitution estimator of ; however, no details are given about the considered distance, while Goga et al. (2009) provide only minimal details. In what follows, we provide a distance between and the true which goes to zero when the sample and the population sizes go to infinity.

We consider the total variation distance for two finite and positive measures and to be defined by

with . We first prove (lemma 1 from below), that the distance between the Horvitz-Thompson estimator of and the true goes to zero. Next, we extend the result (lemma 2 from below) to the nonparametric estimator

Let represent the Horvitz-Thompson weights, namely for all and let be the estimator of using these weights. Let and for ease of notation, . Thus, for all uniformly in and

where is the sample membership indicator.

Lemma 1.

Assume (A3) and (A5) from the Appendix. Then,

The proof is provided in the Appendix. We extend now lemma 1 to nonparametric weights given by (11). Consider again and let

where is obtained from (8) for replaced with Let also obtained from (7) for replaced with

Lemma 2.

Assume (A3) and (A5) from the Appendix. Assume in addition that:

() for all uniformly in .

() uniformly in

Then,

The proof is provided in the Appendix. In section 4, we prove that the nonparametric estimator of constructed using B-spline estimators satisfies the assumptions () and () from the above lemma. The results from Breidt and Opsomer (2000) may be used to prove the assumptions for local polynomial regression; however, this issue will not be pursued further here.

To provide the first order expansion of we must also define its first derivative. This derivative is referred to as the influence function and is defined as follows (Deville, 1999)

where is the Dirac measure at point . Note that the above definition is slightly different from the definition of the influence function given by Hampel (1974) in robust statistics, which is based on a probability distribution instead of a finite measure.

Let for all be the influence function computed at , namely

These quantities are referred to as the linearized variables of and serve as a tool for computing the approximative variance of They depend on the parameter of interest and they are usually unknown even for the sampled individuals. Deville (1999) provides many practical rules for computing for rather complicated parameters

Examples. The linearized variable of a ratio is

| (16) |

and for the Gini index, it is given by

| (17) |

where is the mean of lower than

We now provide the main result of this paper. The following theorem is the first linearization step of . This proves that under broad assumptions the nonparametric estimator is approximated by the nonparametric estimator for the population total of the linearized variable. The proof is provided in the Appendix.

Theorem 3.

(First linearization step) Assume (A1)-(A3) and (A5) from the Appendix. Additionally assume () and from lemma 2. Then, the nonparametric substitution estimator fulfills

We can put in the form of an NMA estimator. Let denote Using (11), we can write

| (18) |

where with is given by (8) and is the sample restriction of

Remark 1: A model-based interpretation of may be given. For the nonparametric model ,

the linearized variable can be fitted using the auxiliary variable

where the are independent random variables with mean zero and variance The estimator of under the model denoted by , is obtained using the same nonparametric method employed for estimating under the model This implies that is the best fit of the population vector with given by (7). Furthermore, is estimated by which leads to the pseudo-estimator of However, unlike the linear case, is not an estimate of because the sample linearized variable vector is not known and we refer to it as a pseudo-estimator. Remark also that the estimator is efficient if the nonparametric model holds.

The nonparametric pseudo-estimator given by (18) is a nonlinear function of Horvitz-Thompson estimators; however, it estimates a linear parameter of interest, namely the total of This indicates that is similar to estimators used by Breidt and Opsomer (2000), Breidt et al. (2005) and Goga (2005) although it is computed for the artificial variable The second linearization step approximates by the generalized difference estimator of given by

| (19) |

Proposition 4.

(Second linearization step) Assume that Then,

Based on theorem 3 and proposition 4, we see that the asymptotic variance of is the variance of namely

Moreover, if the asymptotic distribution of is then the asymptotic distribution of is also

In section 4, we provide the necessary assumptions for the linearized variables and the auxiliary variable

to obtain an approximation of by in a B-spline estimation context.

Remark 2. When the linearized variable is a linear combination of the study variables, the assumption from proposition 4 is reduced to assumptions on the study variables. For example, this occurs in the case of a ratio where the linearized variable is given by The error can be written as a linear combination of errors between and , respectively.

Using mild regularity assumptions on and on the sampling design, and are shown to be of order (see Fuller, 2009, for linear regression and section 4 for B-spline estimators). Thus is also of order provided that and are bounded.

Remark 3. The asymptotic variance given by theorem 3 and proposition 4 depends on the population residuals of the linearized variables under the model . For the simple case of a ratio, the relationship between and the study variables is explicit and given by . If linear models fit the data and well, then a linear model will also fit well. Nevertheless, for nonlinear parameters such as the Gini index, the relationship between and the study variable is not as simple as that for the ratio. In such situations, the use of nonparametric regression methods may provide a major improvement with respect to variance compared to parametric regression.

4 Penalized B-spline estimators

Spline functions have many attractive properties, and they are often used in practice due to their good numerical features and ease of implementation. We suppose without loss of generality that all have been normalized and lie in For a fixed the set of spline functions of order with equidistant interiors knots is the set of piecewise polynomials of degree that are smoothly connected at the knots (Zhou et al., 1998),

For is the set of step functions with jumps at knots. For each fixed set of knots, is a linear space of functions of dimension . A basis for this linear space is provided by the B-spline functions (Schumaker, 1981, Dierckx, 1993) defined by

where if and zero, otherwise. For all each function has the knots with for (Zhou et al., 1998) which means that its support consists of a small, fixed, finite number of intervals between knots. Moreover, B-spline are positive functions with a total sum equal to unity:

| (20) |

For the same order and the same knot location, one can use the truncated power basis (Ruppert and Carroll, 2000) given by . The B-spline and the truncated power bases are equivalent in the sense that they span the same set of spline functions (Dierckx, 1993). Nevertheless, as indicated by Rupert et al. (2003), “the truncated power bases have the practical disadvantage that they are far from orthogonal”, which leads to numerical instability especially if a large number of knots are used.

4.1 Nonparametric penalized spline estimation for finite population totals

We now consider the superpopulation model given by (3). To estimate the regression function we use spline approximation and a penalized least squares criterion. We define the spline basis vector of dimension as The penalized spline estimator of is given by with as the least squares minimizer of

| (21) |

where (p) represents the -th derivate with The solution of (21) is a ridge-type estimator,

| (22) |

where is the matrix with rows and the matrix is the squared norm applied to the th derivative of . Because the derivative of a -spline function of order may be written as a linear combination of -spline functions of order , for equidistant knots (Claeskens et al., 2009) where the matrix has elements with as the -spline function of order and as the matrix corresponding to the th order difference operator.

The amount of smoothing is controlled by The case results in an unpenalized B-spline estimator the asymptotic properties of which have been extensively studied in the literature (Agarwal and Studden, 1980, Burman, 1991, and Zhou et al., 1998, among others). The case is equivalent to fitting a th degree polynomial. The theoretical properties of penalized splines with have been studied only recently by Cardot (2000), Hall and Opsomer (2005), Kauermann et al. (2009) and Claeskens et al. (2009).

The design-based estimators of are

| (23) |

where is the design-based estimator of and is the matrix given by We note that may be written as in formula (8) for

Finally, the -spline NMA estimator of is as follows:

| (24) | |||||

This indicates that may be written as a GREG estimator that uses the vectors as regressors of dimension with going to infinity and a ridge-type regression coefficient Furthermore, is a weighted sum of sampled values with weights expressed as in (11),

| (25) |

Regression splines

For we obtained the unpenalized B-spline estimator studied by Goga (2005) and called the regression splines. The B-spline property given in (20) may be written as with the dimensional vector of ones, implying that and Using these two relations in (25) (Goga, 2005), we observe that is equal to the finite population total of the prediction

where the weights are given by,

| (26) |

Note the similarity with the GREG weights obtained in the case of a linear model when the variance of errors is linearly related to the auxiliary information (Särndal, 1980). We note that for a B-spline of order the estimator becomes the well-known poststratified estimator (Särndal et al., 1992).

Based on assumptions regarding the sampling design and the variable (assumptions (A3)-(A5) from the Appendix) and assumptions regarding the distribution of and the knot number (assumptions (B1)-(B2) in the Appendix), Goga (2005) proved that the B-spline estimator for the total is asymptotically design-unbiased and consistent (equation (12)) and may be approximated by a nonparametric generalized difference estimator (equation (13)). These results are valid without supplementary assumptions regarding the smoothness of the regression function

Penalized splines using truncated polynomial basis functions

Let be the vector basis and let with be the least squares minimizer of for The solution is given by

with and the penalty matrix having zeros on the diagonal followed by one values, Note that for we obtain the same prediction as with an unpenalized B-spline estimation. This results follows from the fact that the two bases are equivalent, thus there exists a square and invertible transition matrix such that (Ruppert et al., 2003). For we have which indicates equivalency to the estimator obtained with penalized B-spline fitting given by (22) for (see Claeskens et al. (2009) for the expression of satisfying this equation).

In a design-based approach, Claeskens et al. (2005) proved that the NMA estimator is the population total of the design-based predictions They also proved that fulfils properties (12) and (13).

4.2 Asymptotic properties of the B-spline estimator of totals under the sampling design

In the following, we study the asymptotic properties of under the sampling design. We first provide a lemma concerning the convergence of The proofs are based on the results provided by Goga (2005) for the unpenalized B-spline estimator and on the fact that the inverse of the matrix is of order for the penalized B-spline estimator (lemma 1 from Claeskens et al., 2009).

Lemma 5.

-

(a)

Assume assumptions (A4)-(b) and (B1), (B2)-(a) and (B3) from the Appendix. Then,

-

(b)

Assume assumptions (A3), (A4)-(b), (A5) and (B1)-(B3) from the Appendix. Then,

where is the usual euclidian norm.

The proof is provided in the Appendix. We note that for B-spline functions of order and we obtain a poststratified estimator with a number of poststrata going to infinity. In this context, lemma 5, (b) provides a detailed theoretical justification for the poststratification example in Deville (1999, p. 196). We note also that to obtain the convergence of Claeskens et al. (2005) assume that the result from lemma 5, (b) holds. Finally, we note that GREG estimators may be viewed as a special case when the number of knots is fixed. Papers dealing with this issue usually assume that the regression coefficient satisfies the results from the above lemma (see for example Robinson and Särndal, 1983, or Isaki and Fuller, 1983). A similar result was proved by Cardot et al. (2012).

Using lemma 5, we derive the following results.

Proposition 6.

Assume assumptions (A3), (A4)-(b), (A5) and (B1)-(B3) from the Appendix. Then,

-

(a)

-

(b)

where

The proof is provided in the Appendix. Using the Markov inequality, we see from the first point of proposition 6 that is asymptotically design-unbiased for and -consistent as The second point provides an approximation of by the nonparametric generalized difference estimator

4.3 Calibration with penalized splines

The spline approach has some interesting calibration properties. Under the unpenalized B-spline framework, the weights given by (26) satisfy the calibration equation for the known population total of B-spline functions, namely

This relation is easily obtained using (20) (Goga, 2005). Because the spline space is spanned by the B-spline functions , these weights will be calibrated to the total of any polynomial of degree In particular, and Claeskens et al. (2005) prove that using the penalized splines and the truncated polynomial basis functions l provides weights that are also calibrated for the finite population totals of the polynomial basis functions

4.4 Nonparametric penalized spline estimation for nonlinear parameters

We now consider the nonlinear parameter estimated by with and the weights given by (25). As in section 3, to linearize we use a two-step procedure. The first-step linearization is given in theorem 3 provided that the assumptions and from lemma (2) are fulfilled. These assumptions are crucial because they ensure the convergence of some nonparametric estimator of to the true measure according to the distance Using classical assumptions from a B-spline framework (assumptions (B1)-(B3) from the Appendix) and mild assumptions regarding the sampling design (assumptions (A3) and (A5) from the Appendix), we prove in theorem 7 below that and are verified. The proof is basically based on lemma 5 and the fact that the distance is defined for uniformly bounded functions ensuring that the assumption (A4)-(b) is automatically fulfilled.

By conducting this first linearization step, we see that the nonparametric B-spline estimator will be approximated by the nonparametric B-spline estimator of the total of the linearized variables given by

where with

The second-step linearization consists of providing an approximation of by a nonparametric generalized difference estimator,

where To obtain this result, we state in theorem 7, (b) a supplementary assumption regarding the linearized variable Goga and Ruiz-Gazen (2012) prove that the linearized variable of the odds-ratio satisfies this assumption.

Theorem 7.

Suppose that the sampling design satisfies assumptions (A3) and (A5). In addition, assume that (B1)-(B3) hold.

-

(a)

Assumptions and from lemma 2 are fulfilled.

As a consequence, Moreover, if the functional satisfies (A1) and (A2), then -

(b)

Suppose that the linearized variables are such that for all satisfy (A4)-(b). Then,

The proof is provided in the Appendix.

5 Variance estimation

In this section we undertake a detailed study of the variance estimation of We first give the functional form of the variance of as well as of its variance estimator and we propose a variance estimator for and assumptions under which this estimator is consistent.

The Horvitz-Thompson variance for is a quadratic form that can be written as a functional of some finite and discrete measure. We can write the variance as follows (Liu and Thompson, 1983),

| (27) |

where and is a bilinear function of and It follows from (27), that the Horvitz-Thompson variance is the finite population total of over the derived synthetic population of size This variance can be put in a functional form as follows

where Note that is a functional of degree with respect to namely A sample in this population is and has size Moreover, the first-order inclusion probabilities over the synthetic population are , which are exactly the second-order inclusion probabilities with respect to the initial sampling design The measure is estimated on by where The resulting estimator of is as follows

This is exactly the Horvitz-Thompson variance estimator, as is equal to Moreover, the functional is Fréchet differentiable, with first derivative given by

Consider now the asymptotic variance of given by

| (28) |

where is the linearized variable of and for We recognize the Horvitz-Thompson variance of the total of the population residuals We suggest estimating the variance of by using the Horvitz-Thompson variance estimator with replaced by the sample estimators

| (29) |

where is the sample estimate of The Horvitz-Thompson variance estimator with true linearized variables given by

| (30) |

The three expressions of variance above depend on the population fits residuals for all It follows that we may write as a functional of depending on parameter

Furthermore, the Horvitz-Thompson estimator and the variance estimator can be treated in a functional form as follows

Note that is the vector of sample-based fit residuals with for all Theorem 3 from Goga et al. (2009) allows us to establish under additional assumptions that the variance estimator (29) is -consistent for the asymptotic variance.

Theorem 8.

Assume that assumptions (A3) and (A5) from the Appendix hold. Also assume that holds uniformly in k and If the Horvitz-Thompson variance estimator is -consistent for then the variance estimator is also -consistent for in the sense that

The proof is given in the Appendix. Note that because the functional is Fréchet differentiable, the -consistency of the Horvitz-Thompson estimator for may also be derived with assumptions on fourth moment of and on fourth-order inclusion probabilities. The reader is referred to Breidt and Opsomer (2000) for additional details.

6 Empirical results

Let us consider a data set from the French Labor Force surveys of 1999 and 2000 as the finite populations of interest. The data consist of the monthly wages (in euros) of 19,378 wage-earners who were sampled in both years. The study variable (resp. the auxiliary variable ) is the wage of person in 2000 (resp. 1999). The objective of the simulation studies is to investigate the finite-sample performance of the regression spline estimators for two nonlinear parameters of interest and two different survey designs. We concentrate in practice on the simple approach of regression B-splines and do not consider the penalized B-splines with . The empirical study of penalized splines raises the problem of estimating the parameter which is beyond the scope of the present paper. We illustrate the efficiency of the regression B-splines estimators compared to other estimators, and we also confirm the possibility of conducting valid inference using variance estimators as detailed in the previous section.

The parameters to estimate include the mean, the Gini index and the poverty rate for the wages in 2000 using the wages in 1999 as auxiliary information. The poverty rate is the proportion of individuals whose wages are below the threshold of 60% of the median wage and correspond to the low-income proportion studied in Berger and Skinner (2003). The Gini index and the low-income proportion are the complex parameters to be estimated and we provide results for the mean as a benchmark. Note that details on the low-income proportion estimator and its associated linearized variable can be found

in Berger and Skinner (2003) and are not provided in the present paper.

In subsection 6.1, we focus on simple random sampling without replacement and in subsection 6.2, we focus on a stratified simple random sampling without replacement. We consider the following estimators for each parameter:

- the Horvitz-Thompson estimator (HT), which does not incorporate any auxiliary information,

- poststratified estimators (POST) with a different number of strata bounded at the empirical quantiles for 1999 wages,

- the GREG estimator (GREG), which takes into account the 1999 wages as auxiliary information using a simple linear model,

- B-spline estimators (BS() where denotes the spline order), which take into account the wages from 1999 as auxiliary information by using a nonparametric model with different numbers of knots () located at the quantiles of the empirical distribution for wages from 1999. The and orders are considered.

The poststratified estimator is an example of a B-spline estimator with order . The number of strata correspond to the number of interior knots plus one.

To use the regression B-spline estimators we propose in a complex survey, and derive confidence intervals, the user must be able to calculate the weights given in equation (26) and the residuals of equation (29). The weights depend on a spline basis that is easy to obtain using for instance the transreg procedure in the SAS software or the functions spline.des or bs from the splines package in the R software. Then, it is possible to use standard calibration algorithms by simply providing the () B-spline basis functions as auxiliary variables for calculating the calibrated weights that correspond to equation (26). These weights are needed to calculate the substitution estimator of the parameter of interest (e.g. the expression (15) for the Gini index). To estimate the variance, the linearized variables associated with the parameter have to be estimated. For several inequality indicators, including the Gini index and the low-income proportion, some SAS macro programs are freely available on the web site of Xavier d’Haultfœuille. Similar functions are available in the R language upon request from the authors of the present paper. Once the linearized variable is estimated, the residuals of this variable against the auxiliary variable using regression splines are calculated; this can be accomplished with the transreg procedure in the SAS software. Then, by using the residuals as if they were the study variable in standard variance estimation tools for complex surveys, the user can obtain the estimated approximative variance and derive confidence intervals.

For each simulation scheme, we draw samples according to the sampling design and compare the finite-sample properties of the HT estimator, the GREG estimator, the POST and the BS(2) and BS(3) estimators. We set knots at the quantiles of the empirical distribution of the auxiliary variable in the sample. We also compared the results with knots set at the quantiles of the empirical distribution of the auxiliary variable over the entire population. Both results are very similar; thus, we report only on the first method. For the POST, BS(2) and BS(3) estimators we tried different numbers of knots but only report the results for and . Note that in the tables, the results for and are reported in the same columns and separated by a dash. For the poststratified estimator, (resp. ) corresponds to 3 (resp. 5) strata. To summarize, in the following, we compare eight estimators (HT, GREG and POST, BS(2) and BS(3) with and ).

There are several ways to estimate the linearized variable (see section 5). In this section, the results are almost the same, regardless of whether we use the simple HT weights, the GREG weights or the B-spline weights for estimating the linearized variable. We recommend using the simplest weights (that is, the HT weights), which is what we do in the present study.

Estimators performance of for a parameter is evaluated using the following Monte-Carlo measures:

-

•

Relative bias in percentage: .

-

•

Ratio of root mean squared errors in percentage:

-

•

Monte-Carlo Coverage probabilities for a nominal coverage probability of 95%.

6.1 Simple random sampling without replacement

The first survey design we consider is simple random sampling without replacement with three sample sizes (, and ). The number of simulations is 3,000. The eight estimators are compared and relative biases and ratios of the roots of the mean squared errors are provided in Table 1 for the different parameters and sample sizes.

Not surprisingly, for complex parameters, the largest efficiency gain is observed when the B-spline estimators are compared to the HT estimator without auxiliary information. Because the wages from 2000 are almost linearly related to the wages from 1999, considering the B-spline estimator instead of the GREG estimator does not improve the performance of the mean estimation. However, regarding the Gini index and the low-income proportion, the incorporation of auxiliary information using GREG estimators does not improve efficiency compared to the HT estimator while using a B-spline approach improves the results especially for spline functions of order . When comparing the POST estimator with the BS(2) and BS(3) estimators we notice that there is quite a large gain in efficiency when order is used instead of , while there is an efficiency loss when is used instead of , especially for sample sizes smaller than 1,000. Moreover, for and , the results do not depend heavily on the number of knots and are similar for between 2 and 4 while for the poststratified estimator, there are large variations in the results, regardless of whether we consider 3 or 5 strata. The coverage probabilities in table 2 illustrate that valid inference can be carried out using B-spline estimators as long as the spline order is not too high, especially when the sample size is not very large. No problems are detected for B-splines of order and order even when the sample size is ; however for and , the coverage probabilities for the Gini index estimation are approximately 75% which is quite far from the 95% nominal probability. This result indicates that for a moderate sample size, the variance may be underestimated when the order of the splines is larger than two. The results are not given for but we have observed that the problem worsens when we increase the order of the splines. This is not really surprising due to double linearization and nonparametric estimation.

Parameter HT GREG POST BS(2) BS(3) Mean 200 100 (0) 38 (0) 71 (0) - 63 (0) 38 (0) - 37 (0) 39 (0) - 41 (0) 500 100 (0) 40 (0) 73 (0) - 65 (0) 40 (0) - 39 (0) 38 (0) - 39 (0) 1,000 100 (0) 40 (0) 73 (0) - 66 (0) 40 (0) - 40 (0) 38 (0) - 39 (0) Gini index 200 100 (1) 96 (1) 92 (1) - 80 (1) 53 (2) - 53 (2) 70 (3) - 70 (3) 500 100 (1) 93 (0) 93 (1) - 85 (1) 50 (1) - 50 (1) 59 (1) - 56 (1) 1,000 100 (0) 92 (0) 93 (0) - 86 (0) 49 (0) - 48 (0) 55 (1) - 51 (1) Poverty rate 200 100 (2) 95 (0) 92 (0) - 80 (0) 65 (1) - 65 (1) 72 (1) - 63 (1) 500 100 (0) 95 (0) 88 (0) - 78 (0) 64 (0) - 64 (0) 68 (0) - 62 (0) 1,000 100 (1) 94 (0) 89 (0) - 78 (0) 64 (0) - 64 (0) 67 (0) - 61 (0)

Parameter HT GREG POST BSPL(2) BSPL(3) Mean 200 94 95 93 - 92 93 - 93 90 - 88 500 95 94 93 - 94 93 - 93 91 - 91 1,000 95 95 94 - 93 94 - 94 93 - 93 Gini index 200 94 93 94 - 94 89 - 87 74 - 75 500 93 93 93 - 94 91 - 90 83 - 85 1,000 95 94 95 - 94 94 - 93 88 - 90 Poverty rate 200 94 95 95 - 95 95 - 94 94 - 94 500 93 95 95 - 94 95 - 95 96 - 95 1,000 94 95 96 - 96 95 - 96 96 - 95

6.2 Stratified simple random sampling without replacement

For each simulation, we draw 5,000 samples from the French Labor Force population according to a stratified simple random sampling design without replacement. We compare the finite-sample properties of the eight estimators considered in the previous subsection. The strata are spatial divisions of the French territory in six “regions” that correspond to the major socio-economic regions of metropolitan France as defined by Eurostat. These regions are the first level of the nomenclature of territorial units for statistics classification (NUTS-1). For our example, we grouped the Northern and Eastern regions together and we grouped the Mediterranean and the Southwestern regions together. The sample size inside each stratum is 200 making the total sample size 1200. Thus, we used an unequal probability design with a sample rate inside the strata that varied from 5 to 9.3%.

As previously described, we set the knots at the quantiles of the empirical distribution of the auxiliary variable in the sample and we estimate the linearized variables using the HT weights. The simulation results are reported in Table 3 and 4 and the conclusions are similar to those obtained from the simple

random sampling design without replacement when the size of the sample is which corresponds to the sample sizes inside each stratum.

It is beneficial to use the available auxiliary information when estimating the mean but there is no need to use nonparametric estimators because

they are not more efficient than the GREG estimator. However, for complex parameters, using a GREG estimator to take auxiliary information

into account is not worthwhile in terms of variance while important gains can be made by using B-spline estimators.

The empirical coverage probabilities are all very good except for the Gini index B-spline estimator

of order three with values equal to 89-90% which confirms the problem of variance underestimation for moderate sample sizes and splines of order three.

Based on this example we do not recommend using high order values for B-spline regression, especially when the

sample sizes are smaller than 500. However, choosing instead of (which corresponds to poststratification) leads to a clear improvement

in terms of efficiency for complex parameters such as the Gini index or the low-income proportion, and we recommend this choice.

Parameter HT GREG POST BS(2) BS(3) Mean 100 (0) 40 (0) 73 (0) - 66 (0) 40 (0) - 40 (0) 40 (0) - 40 (0) Gini index 100 (0) 93 (0) 94 (0) - 88 (0) 50 (0) - 50 (0) 55 (1) - 52 (1) Poverty rate 100 (0) 93 (0) 88 (0) - 77 (0) 65 (0) - 64 (0) 68 (0) - 62 (0)

Parameter HT GREG POST BS(2) BS(3) Mean 95 95 95 - 94 94 - 94 93 - 92 Gini index 95 95 95 - 95 93 - 93 89 - 90 Poverty rate 94 95 95 - 95 95 - 95 96 - 95

7 Discussion

In this paper we considered the important problem of nonlinear parameter estimation in a finite population framework by taking into account the survey design and a unique auxiliary variable known for all the population units. Examples of nonlinear parameters are concentration and inequality measures, such as the Gini index or the low-income proportion. We proposed a general class of substitution estimators that allows us to take into account the auxiliary information via a nonparametric model-assisted approach. The asymptotic variance of this class of estimators was derived, based on broad assumptions, and variance estimators were proposed. Our main result was that the asymptotic variance depends on the extent to which the auxiliary variable explains the variation in the linearized variable . Because linearized variables of nonlinear parameter are likely to be nonlinearly related to auxiliary information, a nonparametric approach is recommended. The proposed estimators are based on weights that are flexible enough to increase the efficiency of finite population totals estimators for any study variable and to allow the consideration of parameters that are more complex than totals. Moreover, the penalized B-spline estimators were studied in detail, and the theoretical results were confirmed for regression B-spline estimators using one case study.

Our proposal can be extended in several different ways. In particular, further research can extend this proposal to include multivariate auxiliary information by means of additive models, as in Breidt et al. (2005), or single index models as in Wang (2009).

Acknowledgement: we are grateful to Patrick Gabriel for his precious help for lemma 1, to Hervé Cardot for helpful discussions and to Didier Gazen for his assistance with the simulations.

Appendix: assumptions and proofs

Assumptions on functional and on sampling design.

-

(A1).

The functional is homogeneous, in that there exists a real number dependent on such that for any real We assume also that

-

(A2).

The functional is Fréchet differentiable at ; that is, there exists a functional that is linear in such that with

We note that the strong assumption of Fréchet differentiability can be weakened to compact or Hadamard differentiability. However, for Hadamard differentiability, functionals are considered with respect to the empirical distribution function and the distance should be replaced by the sup norm. Supplementary assumptions need to be supposed in order to have the consistency of the estimator of the empirical distribution function. Motoyama and Takahashi (2008) study the asymptotic behavior of Hadamard statistical functionals but only for simple random sampling without replacement.

-

(A3).

-

(A4).

-

(a)

with -probability 1.

-

(b)

with a positive constant not depending on

-

(a)

-

(A5).

, with with some positive constants and

Assumption (A3) and (A5) deal with first and second order inclusion probabilities and are rather classical in survey sampling theory (see also Robinson and Särndal, 1983 and Breidt and Opsomer, 2000). They are satisfied for many sampling designs. Assumption (A4)-(a) is a regularity condition necessary to get the consistency results. Some results need the stronger assumption (A4)-(b).

Assumptions on B-splines

-

(B1).

There exists a distribution function with strictly positive density on such that with the empirical distribution of

-

(B2).

-

(a)

;

-

(b)

with

-

(a)

-

(B3).

where with a constant that depends only on and the design density.

These assumptions are classical in nonparametric regression (Agarwal and Studden, 1980, Burman, 1991, Zhou et al., 1998); (B1) means that asymptotically, there is no sub-interval in without points and (B2) ensures that the dimension of the B-spline basis goes to infinity but not too fast when the population and the sample sizes go to infinity. Assumption (B3) concerns the penalty as used by Claeskens et al. (2009).

Proofs of results from section 3

Proof of Lemma 1. Now, let and let be the sample membership. Following the same lines as in Breidt and Opsomer (2000), we have,

uniformly in by assumption (A3),(A5) and using the fact that

Proofs of results from section 4

We state below several lemmas useful for the proofs of our main results. For a matrix we consider the norm defined by and the trace norm

We denote by and by its estimator.

Lemma 9.

Assume assumptions (B1), (B2)-(a) and (B3). Then,

-

1.

(lemma 6.3 from Agarwal and Studden, 1980).

We also have (lemma 6.3 from Zhou et al., 1998). -

2.

(lemma 1 from Claeskens et al., 2009)

Lemma 10.

(Goga, 2005) Assume (A3), (A4)-(a), (A5) and (B1), (B2)-(a). Then,

-

1.

-

2.

Proof of lemma 5. When is uniformly bounded (assumption A4,b), we have, using lemma 3 (a) (Goga, 2005) that

| (32) |

since for with we have

For (a), is bounded following Goga (2005),

| (33) | |||||

by lemma 9-(b) and relation (32). Furthermore, we have

| (34) | |||||

Under the assumption (A4)-(b), is bounded by We have that

and for with implying that

Using lemma 10-(a), we obtain that

From lemmas 9 and 10, we obtain that

Finally, we have that

Proof of proposition 6. Consider first Using the same lines as in the proof of lemma 1 and the fact that for all (Burman, 1991), we obtain that

| (35) |

Furthermore,

by (35) and lemma 5-(b). Then, the result follows by using the Markov inequality.

Now, we consider the error We write

By assumptions (A3), (A4-b) and (A5), we have that Moreover, using relation (35) and lemma 5, (a) we have which implies that

by the fact that using assumption (B2).

Proof of Theorem 7. (a) We check that assumptions () and () are fulfilled. We have with for all Following (32) and (33), we obtain that uniformly in and

| (36) |

uniformly in Now, we check the assumption (), namely uniformly in

We have

The first term from the right-side does not depend on and is of order (equation (35)). For the second term from the right-side, we can use the proof of lemma (5), more exactly the equation (34), and the fact that to obtain

Finally, we obtain that for with

Proof of Theorem 8. The proof follows the same basic steps as in Theorem 3 from Goga et al. (2009) and result 4 from Chaouch and Goga (2010). Let

with given by (30) and let also . Furthermore, the quantity can be written as

Now,

by assumptions (A3) and (A5). Using the same arguments as above, we obtain Hence, and the result then follows because

References

- [Agarwal, G. G. and Studden, W. J. (1980)] Agarwal, G. G. and Studden, W. J. (1980). Asymptotic integrated mean square error using least squares and bias minimizing splines, The Annals of Statistics, 8, 1307-1325.

- [Berger, Y. G. and Skinner, C. J. (2003)] Berger, Y. G. and Skinner, C. J. (2003). Variance estimation for a low income proportion, Applied Statistics, 52, 457-468.

- [Binder, D. A. (1983)] Binder, D. A. (1983). On the variances of asymptotically normal estimators from complex surveys International Statistical Review, 51, 279-292.

- [Binder, D. A. and Kovacevic, M. S. (1995)] Binder, D.A. and Kovacevic., M. S. (1995). Estimating some measures of income inequality from survey data: an application of the estimating equations approach. Survey Methodology, 21, 137-145.

- [Breidt, F. J. and Opsomer, J. (2000)] Breidt, F. J. and Opsomer, J. (2000). Local Polynomial Regression Estimators in Survey Sampling, The Annals of Statistics, 28, 1026-1053.

- [Breidt, F. J., Claeskens, G. and Opsomer, J. (2005)] Breidt, F. J., Claeskens G. and Opsomer, J. (2005). Model-assisted estimation for complex surveys using penalised splines, Biometrika, 92, 831-846.

- [Breidt, F. J. and Opsomer, J. (2009)] Breidt, F. J. and Opsomer, J. (2009). Nonparametric and Semiparametric Estimation in Complex Surveys, Handbooks of Statistics, vol. 29B, eds. D. Pfeffermann and C. R. Rao, 103-121.

- [Burman, P. (1991)] Burman, P. (1991). Regression function estimation from dependent observations, Journal of Multivariate Analysis, 36, 263-279.

- [Cardot, H. (2002)] Cardot, H. (2002). Local roughness penalties for regression splines, Computational Statistics, 17, 89-102.

- [Cardot, H., Goga, C. and Lardin, P. (2012)] Cardot, H., Goga, C. and Lardin, P. (2012). Uniform convergence and asymptotic confidence bands for model-assisted estimators of the mean of sampled functional data, submitted.

- [Cassel, C. M., Särndal, C. E. and Wretman, J. H. (1976)] Cassel, C. M., Särndal, C. E. and Wretman, J. H. (1976). Some results on generalized difference estimation and generalized regression estimation for finite populations, Biometrika, 63, 615-620.

- [Chaouch, M. and Goga, C. (2010)] Chaouch, M. and Goga, C. (2010). Design-based estimation for geometric quantiles with application to outlier detection, Computational Statistics and Data analysis, 54, 2214-2229.

- [Claeskens, G., Krivobokova, T. and Opsomer, J., (2009)] Claeskens, G., Krivobokova, T. and Opsomer, J. (2009). Asymptotic properties of penalized spline estimators, Biometrika, 96, 529-544.

- [Deville, J. C. (1999)] Deville, J. C. (1999). Variance estimation for complex statistics and estimators: linearization and residual techniques, Survey Methodology, 25, 193-203.

- [ Dierckx, P. (1993)] Dierckx, P. (1993). Curves and Surface Fitting with Splines, Clarendon Press, Oxford, United Kingdom.

- [Fuller, W. A. (2009)] Fuller, W. A. (2009). Sampling Statistics, Wiley.

- [Goga, C. (2005)] Goga, C. (2005). Réduction de la variance dans les sondages en présence d’information auxiliaire : une approche non paramétrique par splines de régression, The Canadian Journal of Statistics, 33, 1-18.

- [Goga, C., Deville, J. C. and Ruiz-Gazen, A. (2009)] Goga, C., Deville, J. C. and Ruiz-Gazen, A. (2009). Use of functionals in linearization and composite estimation with application to two-sample survey data, Biometrika, 96, 691-709.

- [Goga, C. and Ruiz-Gazen, A. (2012)] Goga, C. and Ruiz-Gazen, A. (2012). Estimating the odds-ratio using auxiliary information. in revision.

- [Hall, P. and Opsomer, J. (2005)] Hall, P. and Opsomer, J. (2005). Theory for penalized spline regression. Biometrika, 92, 105-118.

- [Hampel, F.R., (1974)] Hampel, F.R. (1974). The influence curve and its role in robust statistics, Journal of American Statistical Association, 69, 383-393.

- [Harms, T. and Duchesne, P. (2010)] Harms, T. and Duchesne, P. (2010). On kernel nonparametric regression designed for complex survey data, Metrika, 72,111-138

- [Huber, P.J. (1981)] Huber, P.J. (1981). Robust Statistics Wiley.

- [Isaki, C. T. and Fuller, W.A. (1983)] Isaki, C. T. and Fuller, W.A. (1983). Survey design under the regression superpopulation model. Journal of American Statistical Association, 77, 89-96.

- [Jonhson, A. A., Breidt, F. J. and Opsomer, J. (2008)] Jonhson, A. A., Breidt, F. J. and Opsomer, J. (2008). Estimating distribution function from survey data using nonparametric regression, Journal of Statistical Theory and Practice, 2, 419-431.

- [Kauermann, G., Krivobokova, T. and Fahrmeir, L. (2009)] Kauermann, G., Krivobokova, T. and Fahrmeir, L. (2009). Some asymptotic results on generalized penalized spline smoothing, J. R. Statist. Soc. B (2009), 71, 487 503.

- [Liu, T. P. and Thompson, M. E. (1983)] Liu, T. P. and Thompson, M. E. (1983). Properties of estimators of quadratic finite populations functions: the batch approach. The Annals of Statistics, 11, 275-285.

- [Motoyama, H. and Takahashi, H. (2008)] Motoyama, H. and Takahashi, H. (2008). Smoothed versions of statistical functionals from a finite population. J. Japan Statist. Soc., 38, 475-504.

- [Nygard, F. and Sandström, A. (1985)] Nygard, F. and Sandström, A. (1985). The estimation of the Gini and the entropy inequality parameters in finite populations. Journal of Official Statistics, 4, 399-412.

- [Opsomer, J and Wang, J.C. (2011)] Opsomer, J and Wang, J.C. (2011). On the asymptotic normality and variance estimation of nondifferentiable survey estimators. Biometrika, 98, 91-106.

- [Opsomer, J., Miller, C. P. (2005)] Opsomer, J., Miller, C. P. (2005). Selecting the amount of smoothing in nonparametric regression estimation for complex surveys, Journal of Nonparametric Statistic, 17, 593 611.

- [Robinson, P. and Särndal, C.E. (1983)] Robinson, P. and Särndal, C.E. (1983). Asymptotic properties of the generalized regression estimator in probability sampling. Sankhya: The Indian Journal of Statistics, 45, 240-248.

- [Ruppert, D. and Carroll, R. J. (2000)] Ruppert, D. and Carroll, R. J. (2000). Spatially-adaptative penalties for spline fitting. Australian and New Zealand Journal of Statistics, 42, 205-223.

- [Ruppert, D., Wand, M.P. and Carroll, R.J. (2003)] Ruppert, D., Wand, M. P. and Carroll, R. (2003). Semiparametric regression, Cambridge Series in Statistical and Probabilistic Mathematics.

- [Sarda, P. and Vieu, P. (2000)] Sarda, P. and Vieu, P. (2000). Kernel Regression, Smoothing and Regression: Approaches, Computation, and Application, eds. Michael G. Schimek, Wiley & Sons, Inc.

- [Särndal C. E. (1980)] Särndal C. E. (1980). On the -inverse weighting best linear unbiased weighting in probability sampling, Biometrika, 67, 639-650.

- [Särndal C. E. , Swensson B. and Wretman J. (1992)] Särndal C. E. , Swensson B. and Wretman J. (1992). Model Assisted Survey Sampling Springer, Berlin.

- [Särndal C. E. (2007)] Särndal C. E. (2007). The calibration approach in survey theory and practice, Survey methodology, 33, 99-119.

- [Schumaker, L. L. (1981)] Schumaker, L. L. (1981). Spline Functions: Basic Theory, Wiley, New York.

- [Shao, J. (1994)] Shao, J. (1994). -statistics in complex survey problems, The Annals of Statistics, 22(2), 946-967.

- [von-Mises, R. (1947)] von-Mises, R. (1947). On the asymptotic distribution of differentiable statistical functions. Annals of Mathematical Statistics, 18, 309-348.

- [Wang, L. (2009)] Wang, L. (2009). Single-index model-assisted estimation in survey sampling, Journal of Nonparametric Statistics, 21, 487-504.

- [Zhou, S., Shen, X. and Wolfe, D. A. (1998)] Zhou, S., Shen, X. and Wolfe, D. A. (1998). Local asymptotics for regression splines and confidence regions. The Annals of Statistics, 26, 1760-1782.