Discussion of “Feature Matching in Time Series Modeling” by Y. Xia and H. Tong

doi:

10.1214/11-STS345B10.1214/10-STS345

Discussion of Feature Matching in Time Series Modeling by Y. Xia and H. Tong

and

We thank Xia and Tong for their stimulating article on time series modeling. Their emphasis on estimation rather than model specification is interesting. It brings new light to statistical applications in general and to time series analysis in particular. The use of maximum likelihood or least squares method is so common, especially with the widely available statistical software packages, that one tends to overlook its limitations and shortcomings.

There is hardly any statistical method or procedure that is truly “one-size-fits-all” in real applications. We welcome Xia and Tong’s contributions as they argue so convincingly that feature matching often fares better in time series modeling. On the other hand, we’d like to point out some issues that deserve a careful study.

1 Higher Order Properties

The conditional mean function generally provides a good description of the cyclical behavior of the underlying process, and the catch-all approach can be effectively implemented by estimating the model that matches the multi-step conditional means to the data, as eminently illustrated by the authors. Here, we want to point out the natural extension of estimating a model by matching multi-step conditional higher moments to the data. For example, in financial time series analysis, it is pertinent to model the dynamics of the conditional variances. Consider the simple case that a time series of returns, , follows a generalized autoregressive conditional heteroscedastic model of order (1, 1) or simply a model:

where , are parameters, are independent and identically distributed (i.i.d.) random variables with zero mean and unit variance, and is independent of past one-step-ahead conditional variances . Estimation of the model can be done by maximizing the Gaussian likelihood of the data, which essentially matches the conditional variances with the squared returns.

A natural generalization of the catch-all method is to estimate a model that matches the -step-ahead conditional variance to the th ahead data, for with a fixed , by minimizing some weighted measure of dissimilarity of the multi-step conditional variances to future squared returns. Various dissimilarity measures may be used. Here, we illustrate the usefulness of this idea by adopting the negative twice Gaussian log-likelihood as the dissimilarity measure, that is, estimatinga model by minimizing

where is a set of fixed weights and is the conditional variance of given information available at time . When , the new method reduces to the Gaussian likelihood method. On the other hand, under the assumption that the true model is a model and for a fixed , the estimator is expected to be consistent and asymptotically normal, with details of the investigation to be reported elsewhere. However, if the model does not contain the true model, as likely is the case in practice, the (generalized) catch-all method with may provide new information for estimating a model that better matches the observed volatility clustering pattern.

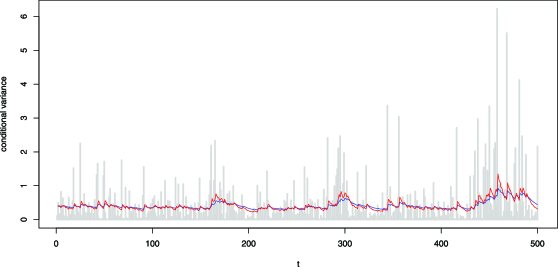

We tried this approach by fitting a model to the daily returns of a unit of the CREF stock fund over the period from August 26, 2004 to August 15, 2006; this series was analyzed by Cryer and Chan [(2008), Chapter 12], and they identified the series as a process. Gaussian likelihood estimation yields . On the other hand, the catch-all method, with and the weights , results in the estimates: and . Figure 1 contrasts the fitted values, , based on the two fitted models with the squared returns superimposed as light gray bars. The figure shows that, as compared to the model estimated by the Gaussian likelihood method, the model fitted by the catch-all method appears to track the squared returns more closely over the volatile period and transit into the ensuing quiet period at a faster rate commensurate with the data. It seems that by requiring the model to track multi-step squared returns, the method chooses a model that gives more weight to the current squared return to the future evolution of conditional variances. Indeed, as increases from 1 to , the ARCH coefficient estimate increases from 0.0439 to 0.102, whereas the coefficient decreases from 0.917 to 0.836. These systematic parametric changes signify that the true model is unlikely a model. It also matches nicely with the increasing kurtosis of the data; see Tsay [(2010), Chapter 3] for a discussion on contribution of to kurtosis of the return . This example illustrates the usefulness of the generalization of the catch-all method by matching higher moments, and also the potential usefulness of developing a test for model misspecification based on the divergence of the catch-all estimates with increasing .

2 Information Content

As statisticians, we love data. However, data have their limitation. Available data may not be informative to conduct any meaningful feature matching. When the information content pertaining to the selected feature is low, feature matching as an estimation method is likely to fail. As an example, assessment of financial risk focuses on the tail behavior of the loss over time. The relevant feature here is the upper quantiles of the loss distribution. Since big losses are rare, available data, no matter how big the sample size is, are not informative about the extreme quantiles. The uncertainty in any matching would be high.

As another example, consider the monthly time series of global temperature anomalies from 1880 to 2010. The data are available from many sources on the web, for example, the websites http://data.giss. nasa.gov/gistemp/ of the Goddard Institute for Space Studies (GISS), National Aeronautics and Space Administration (NASA) and http://www.ncdc.noaa. gov/cmb-faq/anomalies.html of the National Climatic Data Center, National Oceanic and Atmospheric Administration (NOAA). These time series are of interest because of the concerns about global warming. The key feature to match then is the underlying trend of the global temperature. To handle the time trend, two approaches are commonly used in the time series literature. The first approach is called the difference-stationarity in which the time series is differenced to obtain stationarity. The models of Box and Jenkins are examples of this approach. The second approach is called the trend-stationarity in which one imposes a linear time trend for the data. The deviation from the time trend becomes a stationary series. Even though we have 130 years of data, it remains hard for the data to distinguish a trend-sta-tionary model from a difference-stationary one. On the other hand, the long-term forecasts of a difference-stationary model differ dramatically from those of a trend-stationary model. The eventual forecasting function of an model without constant is a horizontal line with standard error approaching infinity whereas that of a trend-stationary model is a straight line going to positive or negative infinity with a finite standard error. See Tsay (2012) for further analysis of the data and model comparison.

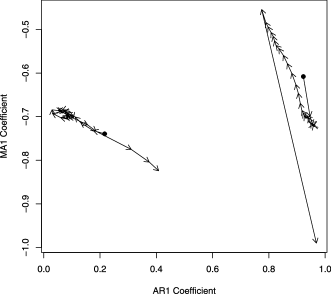

Here, we explore whether feature matching maycast new light on the preceding problem. For simplicity, we consider the annual global temperature anomalies. Model identification suggests two plausible models, namely, model and linear trend plus model. We use the plus convention for the coefficients, that is, the model specifies , where is the backshift operator such that and are i.i.d. with zero mean and variance . For simplicity, these models are fitted by conditional least squares with the residuals initialized as 0 at the first time point. We also fitted the model with the generalized catch-all method that matches the predictive distribution to the future values, in terms of the -step-ahead predictive means and variances, . The loss function is similar to that discussed in the previous section. After profiling out the innovation variance, the generalized catch-all method fits a model to the time series by minimizing

where is the vector of all parameters except the innovation variance; is the -step predictive mean, is the -step-ahead prediction variance, that is, where ’s are the coefficients in the linear representation of the model also known as the impulse response coefficients; is the harmonic mean of . When , the catch-all method reduces to Gaussian likelihood estimation. But for , the catch-all method attempts to match model prediction with “future” values, in terms of means and variances. We implemented the catch-all method for fitting the global temperature anomalies, with . Figure 2 plots the evolution of the catch-all estimates of the coefficients for the two models. It is interesting to observe that the catch-all estimates of the model quickly move away from the Gaussian likelihood estimates and fluctuate stably around an essentially model, that is, an exponential smoothing model, for a while, before they drift to more extreme values. Thus, the catch-all method suggests that for forecasting on a decadal scale, an exponential smoothing model may be appropriate for the temperature data. Similarly, the catch-all estimates of the linear trend plus noise model quickly move away from the Gaussian likelihood estimate, and fluctuate stably for a number of steps around an estimate with its coefficient comparable to that of the exponential smoothing model. As the corresponding estimates are quite close to 1, the catch-all estimates of the trend plus noise model suggest strong similarity between the two models over a forecast horizon on a decadal scale. When approaches 30, the catch-all estimates of the trend plus noise model drift off on a flight that suddenly ends into a trend plus uncorrelated noise model.

For long-term prediction, the global temperature series is of limited value. The preceding analysis highlights the conundrum that using a trend-stationary model, we simply force the data to support the trend; for difference-stationary models, we basically end up using the exponential smoothing model. This is a problem facing all estimation methods, not just feature matching.

We consider these two examples not because we question the value of feature matching in time series modeling; rather we like to point out that care must be exercised in using feature matching. In otherwords, feature matching may encounter the same problem as the traditional estimation methods. They are statistical tools. It is the statisticians who use the tools, not the tools that process the data. Which tool to use in a given application is the choice of a statistician. While we welcome the addition of feature matching to the tool kits, we like to emphasize that there are limitations in feature matching, too.

3 Feature Versus Objective

Model selection in data analysis depends critically on the objective of data analysis. Likelihood estimation seeks parameters that give the highest probability of the data under the entertained model. Feature matching searches for parameters that best describe the features of interest. The examples used in the article all have clearly defined features such as cycles and, as expected, feature matching works well. On the other hand, there are situations under which the objective of data analysis does not match well with any specific feature. For example, with the economy under pressure, unemployment is of major importance to people of all walks. It is well known that unemployment rate exhibits strong business cycles, which in sharp contrast with examples used in the article do not have a fixed (or even an approximate) period. It is then not clear which feature to match if one is interested in understanding and forecasting the U.S. unemployment rate.

Acknowledgments

K.-S. Chan thanks the U.S. National Science Foundation (NSF-0934617) and R. S. Tsay thanks the Booth School of Business, University of Chicago, for partial financial support.

References

- Cryer and Chan (2008) {bbook}[auto:STB—2011-03-03—12:04:44] \bauthor\bsnmCryer, \bfnmJ. D.\binitsJ. D. and \bauthor\bsnmChan, \bfnmK. S.\binitsK. S. (\byear2008). \btitleTime Series Analysis: With Applications in R, \bedition2nd ed. \bpublisherSpringer, \baddressNew York. \endbibitem

- Tsay (2010) {bbook}[mr] \bauthor\bsnmTsay, \bfnmRuey S.\binitsR. S. (\byear2010). \btitleAnalysis of Financial Time Series, \bedition3rd ed. \bpublisherWiley, \baddressHoboken, NJ. \endbibitem

- Tsay (2012) {bbook}[auto:STB—2011-03-03—12:04:44] \bauthor\bsnmTsay, \bfnmR. S.\binitsR. S. (\byear2012). \btitleAn Introduction to Financial Data Analysis. \bpublisherWiley, \baddressHoboken, NJ. \endbibitem