60K10, 60J75

Passage times of perturbed subordinators with application to reliability

Abstract

We consider a wide class of increasing Lévy processes perturbed by an independent Brownian motion as a degradation model. Such family contains almost all classical degradation models considered in the literature. Classically failure time associated to such model is defined as the hitting time or the first-passage time of a fixed level. Since sample paths are not in general increasing, we consider also the last-passage time as the failure time following a recent work by Barker and Newby [4]. We address here the problem of determining the distribution of the first-passage time and of the last-passage time. In the last section we consider a maintenance policy for such models.

keywords:

First-passage time, last-passage time, scale function, failure time, Lévy process, gamma process, compound Poisson process, Brownian motion with drift1 Introduction and Model

For several decades, degradation data have been more and more used to understand ageing of a device, instead of only failure data. The most widely used stochastic processes for degradation models belong to the class of Lévy processes. More precisely, the three main models are the following ones: (a) Brownian motion with (positive) drift; (b) gamma processes; (c) compound Poisson processes. More generally we consider a broad class of Lévy processes corresponding to subordinators perturbed by an independent Brownian motion:

where is a subordinator, i.e. a Lévy process with non decreasing sample paths. Since jumps of are issued from and are positive, we recall that we say that is spectrally positive. This process can be characterized in terms of Lévy exponents:

Exponent is associated to the Brownian motion and to , which is in all generality a jump process. It follows that the Lévy measure of is the same as that of that we will denote by . Furthermore we will suppose that measure admits a density with respect to the Lebesgue measure, i.e. that for some density . In the following we will also need

i.e. is such that . We recall, since is a subordinator, that may write in this case in the following way

for some . We consider in this paper several approaches for modelling degradation of a device and its failure time. Failure time can traditionally be derived from a degradation model by considering the first hitting time of a critical level . The first-passage time distribution has been already derived for the particular case of two sub-models. In the case of Brownian motion with drift (corresponding to , ), it is the well-known inverse Gaussian distribution, see [15] for instance. For the pure gamma process (i.e. and is a gamma process), it has been studied by Park and Padgett [23]. Moreover they proposed an approximation for the cumulative distribution function of the hitting time based on Birnbaum-Saunders and inverse Gaussian distributions.

Recently a new approach to define the failure time was proposed by Barker and Newby [4] that consists in considering the last passage time of degradation process above . As explained in that paper, this is motivated by the fact that, even if reaches and goes beyond , resulting in a temporarily "degraded" state of the device, it can still always recover by getting back below provided this was not the last passage time through . On the other hand, if this is the last passage time then no recovery is possible afterwards and we may then consider it as a "real" failure time. Of course, this discussion about modelling failure time by the first or last passage time becomes irrelevant whenever process has non decreasing paths (which is not the case e.g. of the Brownian motion) since in that case both quantities coincide.

In this paper we then investigate these quantities for a rather wide class of so-called perturbed process. In Section 2 we provide the Laplace transform of the first passage time with penalty function involving the corresponding under and overshoot of the process. We then confront this approach to related recent existing results on such passage times distributions in the general theory of Lévy processes, that introduces the notion of so-called scale functions. The case of several sub-models is reviewed (or revisited) : in these cases the probability distribution function (pdf) and/or the cumulative distribution function (cdf) can be computed explicitly, or at least numerically. In conclusion of this section we propose an alternative degradation process that takes into account the fact that the process cannot be in theory negative and suggests that be reflected at zero. In that setting we use the aforementioned recent results in the theory of Lévy and reflected Lévy processes to obtain the joint distribution of the first passage time jointly to the overshoot distribution. In Section 3 we study the case where failure time corresponds to the last passage time above and derive its distribution in the non reflected and reflected case. Finally we consider in Section 4 a maintenance policy problem inspired by [4] and derive distribution of related quantities.

To conclude this introduction, we make precise where in the present paper previously published results are reviewed and what is actually novel. Proposition 1 in Section 2.1 is new, but its proof is similar to the one corresponding to proof of Remark 4.1 as well as Expressions (4.4) and (4.5) of Garrido and Morales [16]. Section 2.3 recalls facts (with short proofs) previously established in the literature that are useful later on. On the other hand and to the best of our knowledge, Theorems 2 and 3 in Section 3 concerning last passage times may be linked to Chiu and Yin [11], Baurdoux [5] and recent paper Kyprianou et al. [21] but are otherwise genuinely new. Similarly Section 4 deals with determining reliability quantities features unheard-of results.

2 First-passage time as failure time

We consider here the hitting time distribution of a fixed level by the perturbed process :

which we remind is a.s. finite. We study below the distribution of by determining the following quantity

| (1) |

where and is an arbitrary continuous bounded function that will be referred to as penalty function. In the following we will drop the subscript when there is no ambiguity on and then write instead of . We then determine (1) in the general case and then illustrate our results to sub-models, some of which distribution of has already been obtained.

2.1 General case

We are interested in the case where process is general. To this end, we use a well known technique that consists in approaching the jump part process in by a compound Poisson processes which, as said in the Introduction, is similar to the one used in [16] (for more details see Appendix A.1 in [16]). More precisely this process can be pointwise approximated by a sequence of compound Poisson processes such that:

-

1.

is increasing for all ,

-

2.

for all ,

-

3.

for all , has intensity and jump size with c.d.f. with

(2) (3) where . Note that defines measure such that .

Note that this approach is particularly interesting when as , i.e. when process has infinitely many jumps on any interval. Intuitively is obtained from by discarding all jumps that are of size less than . Since increases towards , we have that

| (4) |

where is the hitting time of level of the truncated process defined by for any and any . We remind that is also a.s. finite. In fact may be described as a ruin time (i.e. the first hitting time of of a stochastic process) in the following way:

and we are interested in the Laplace transform of with penalty function for all . Let be the positive solution to the following equation:

| (5) |

that we will call generalized Lundberg equation. We start by showing convergence of as .

Proposition 2.1

converges as to the unique solution to the following generalized Lundberg equation:

| (6) |

Proof.

Thanks to Expressions (2) and (3) of and c.d.f. , we may rewrite (5) in the following way

Thus is the only positive solution to equation where Let us note that increasingly converges pointwise towards

so that converges increasingly towards . Besides one can verify that admits an unique solution on , which is solution to Equation (6). Thus is less than or equal to solution and we prove that we in fact have equality which is achieved by showing that . Indeed, using inequality for all and since , we have

| (7) | |||||

We recall that the fact that is a subordinator (a non decreasing Lévy process) implies that (see e.g. (2) p.72 of [6]), hence . Remembering that is a continuous function, this implies that (7) tends to zero as , hence . ∎

The Laplace transform with penalty function of is given through the following which is a particular case of Theorem 2 of [29] adapted to our context:

Theorem 2.1

Let be a bounded continuous function and define

Then satisfies the renewal equation

| (8) |

where functions and are defined by

| (9) | |||||

| (10) |

Proof 2.2

With notations of [29], we have expressed as in (1.10) therein with , , and . Still with notations of [29], and in Theorem 2 therein, we see that function is the sum of and some function defined in Expression (2.8) of [29] that depends on . It is easy to verify that this function is the last term on the right-handside of (10).

Proposition 1

Let . Function satisfies the renewal equation

| (11) |

where functions and are defined by

| (12) | |||||

| (13) |

Hence is given by the Pollaczek-Kinchine like formula

| (14) |

Proof 2.3

As announced in the Introduction, it is also possible to use the theory of Lévy processes to propose a different approach for determining the joint distribution of the hitting time jointly to the state of , using scale functions. More precisely, we have the following proposition from e.g. Kyprianou and Palmowski [20]:

Proposition 2 (Theorem 1 (4) [20])

Let us define for all the scale function , through its Laplace transform, and by

| (15) | |||||

| (16) |

where we recall that is solution to the Lundberg equation . Then from Expression (4) p.19 of [20] one has that

| (17) |

Just to be clear on notations, we emphasize that [20] deals with spectrally negative processes. To apply it here (hence to obtain Expressions (15), (16) and (17)), we thus need to consider hitting time of of process starting from . In particular, Laplace exponent of as defined in Expression (2) of [20] by does coincide with function , and , also defined in [20], coincides with .

Remark 2.4 (scale function regularity)

Remark 2.5 (boundary value of scale function)

Still in the present case where process has unbounded variation, we have that by Lemma 8.6 p.222 of [19].

As a complement to (17), it is interesting to note that Remark 3 of [20] gives an explicit expression of the joint Laplace transform of .

The approach in Proposition 2 has however a cost, which is that a Laplace Transform inversion of (15) is required to obtain the scale function. However recent results have been found concerning expression of in particular cases, see Hubalek and Kyprianou [18] as well as Egami and Yamazaki [14] in the case where is a compound Poisson process with jumps following phase-type distribution. In fact the following result combines both approaches given in Propositions 1 and 2, and theoretically gives a closed form expression of scale function of any spectrally positive Lévy process:

Proposition 3

Proof 2.6

Differential equation (18) simply comes from (17) that one differentiates with

respect to (which is possible since is differentiable in light of Remark

2.4), using expression where penalty function

is identically equal to , and finally using Expression (14). Note that

differentiation of (14) is done by using the well known property of derivation of

convoluted functions , explaining why features

derivative of function .

Since by Remark 2.5 one has that , Equation (20) is then obtained by

solving the standard first order differential equation (18).

Note however that Formula (20) requires to compute the infinite series appearing in (18), which in practice may not be handy. However, since such scale functions are important in the theory of Lévy processes (in particular, these functions will be useful in Sections 2.3 and 3 for determining quantities related to first passage times of reflected processes and last passage times), any expression can be considered as welcome.

2.2 Examples

We illustrate the previous study with examples and review some famous examples related to degradation models.

Pure gamma process

Here we assume that and that is a gamma process with shape parameter and scale parameter . We recall that its Lévy exponent and Lévy measure are given by

Considering this special case into the generalized Lundberg equation, it follows that this equation has no positive solution. It appears that the presence of the perturbation in the degradation model is important for applying the result obtained by Tsai and Wilmott [29] as we did in Proposition 1. However, in this first special case, the degradation process reduces to a pure stationary gamma process and so has increasing paths. It follows that:

Consequently it is sufficient to study the distribution of for any . The hitting time distribution was already given for instance p.517 of Park and Padgett [23]:

Proposition 4 (Park and Padgett [23])

The cumulative distribution function (cdf) of is:

where is the upper incomplete Gamma function. The probability distribution function (pdf) of is, for any :

where is the di-gamma function (or logarithmic derivative of the Gamma function), is the lower incomplete Gamma function and the generalized hypergeometric function of order .

Perturbed gamma Process

Statistical inference in a perturbed gamma process has been studied in [8] using only degradation data. However sometimes both degradation data and failure time data are available (see [22] for such problem for a related model). In addition, from parameters estimation (based on degradation data for instance), one can obtain an estimation of the failure time distribution. Hence the distribution of can be of interest. In that case, is a gamma process with shape parameter and scale parameter . We recall that Lévy exponent and Lévy measure of process are then given by

| (21) |

Thus, Proposition 1 gives joint distribution of through expression of where and , being an arbitrary bounded function. Also note that from Remark 2.7 one has thanks to [27] the Central Limit Theorem

Finally, expression of the scale function is then given by (20) with and defined in (21). This will come in handy in Section 3.

Brownian motion with positive drift

We consider the case where , i.e. is a Brownian motion with drift. In such case, the distribution of the hitting time of the constant boundary is known and is called the inverse Gaussian distribution. Its pdf is given by:

Proof of this result is generally based on the symmetric principle full-filled by the Brownian motion when , or can be showed with martingale methods in the case . Alternatively the pdf can be obtained by inverting the Laplace transform of :

| (22) |

with . Note that the expression of this Laplace transform is standard and can be found e.g. in Expression (38) p. 212 of [12] (see also [1], page 19). Also note that (22) is compatible with Expression (14). Indeed in the context of Proposition 1 we have here and , thus (14) reduces to where satisfies (6), giving the exact same expression (22).

Expression of the scale function for this case is then given e.g. p.121 in [18] by

| (23) |

Note that there seems to be a small mistake in [18] of expression of (where there are some ’s instead of ’s), that we corrected here. As proved by Chhikara and Folks [10], the failure rate of an inverse Gaussian distribution is non-monotone, but it is initially increasing and then decreasing.

Perturbed compound Poisson process with phase-type jumps

Let us suppose that is a compound Poisson process of intensity whose jumps are phase-type distributed with representation . Let where is a column vector of which entries are equal to ’s of appropriate dimension (see e.g. Chapter VIII of Asmussen [2] for an extensive account on such distributions). In that case is given by

Egami and Yamazaki [14] give the expression of the Laplace transform by determining a closed formula for the scale functions and using results in Proposition 2. More precisely following [14], let us denote for all the complex solutions (resp. ) of Equation (resp. ), . We suppose that the ’s are distinct roots. We set

On page 4 of [14] it is stated that (this results in fact comes from Lemma 1 (1) of [3]), so that exists and is equal to . We then define

| s.t. | ||||

Then Proposition 2.1 of [14] gives expression of the Laplace transform and Proposition 3.1 of [14] yields the following interesting and useful expression of the scale function

| (24) |

Furthermore, as pointed out in [14], expressions of are more complicated but available when roots ’s have multiplicity .

2.3 Reflected processes

The previous model may not be too realistic if we consider the Brownian motion as a means of modelling small repairs, as the degradation process may then be negative. An alternative for this is to consider the reflected version of defined in the following way

The hitting time distribution of jointly to the overshoot and undershoot pdf is given by the following theorem

Theorem 5

Let us suppose that is non monotone, i.e. that . Let be defined by (15) where we recall that is solution to the Lundberg equation . Then

| (25) |

where .

Proof 2.8

We apply results from Doney [13] and we write, following notations therein, , so that Lévy measure of is and process is equal to . Following terminology of [13], is the -scale function of and is defined by (15) with instead of . Remark 4 p.14 of [13] gives expression (25) where is given by Pistorius [24] (see also Expression (15) in Theorem 1 of [13]) with and , noting that function is differentiable by Remark 2.4.

Note again that Theorem 5 is especially interesting when function admits closed form expressions, as in [18, 14]. For example in the case of a perturbed compound Poisson process with phase-type distributed jumps (and using the same notations as in Section 2.2) we have and given by (24) (of which derivative is easily available), which, plugged in (25), easily yields the Laplace transform of the corresponding hitting time jointly to the overshoot and undershoot distribution.

We now state a famous lemma that links distribution of to the cumulative distribution function of for all :

Lemma 2.1

We have for all and , .

Proof 2.9

This is a simple consequence from e.g. Lemma 3.5 p.74 of Kyprianou [19]that implies that which in turn is equal to .

3 Last-passage time as failure time

We let and be the last passage times of processes and below level defined as

which are well defined as processes and satisfy .

3.1 General case

Let us introduce the following bivariate measures and on through their double Laplace transforms

| (26) |

Expressions (26) may be found in Expressions (12) and (13) of [7], or p.154 and p.170 in Chapter 6 of [19] (note that the latter reference considers spectrally negative processes, hence roles for and are swapped therein). Furthermore, from (26) of [7] one has that has the expression

| (27) |

hence . In the same spirit, we define . (26) then reads that for all . We then have the following identity, that will be of interest later on.

Lemma 3.1

One has

| (28) |

Proof 3.1

From (15) we get the following

| (29) |

where . We recall from Remark 2.5 that . As to behaviour at of the scale function, we have, thanks to Lemma 8.4 p.222 of [19], relation , for any such that , where is a scale function defined under a different probability measure. By picking then one gets and

| (30) |

(see e.g. Second Remark p.32 of [25] for this identity as well as details on this other probability measure). At the end of Proof of Corollary 8.9 p.227 of [19], it is shown that where , hence

| (31) |

Thus in view of , (30) and (31), and since , the following integration by parts makes sense:

| (32) |

remembering that is indeed differentiable by Remark 2.4. Comparing Laplace transforms (29) and (32), we then obtain (28).

Let us also note that, according to Definition 6.4 p.142 of [19], the fact that entails that is regular for sets and (in particular, Theorem 6.5 p.142 of [19] applies here). With that in mind, and since is spectrally positive and drifts to , we may recall the following important recent result from Kyprianou et al [21].

Theorem 1 (Corollary 2 of Kyprianou, Pardo and Rivero [21])

Let us define

Then distribution of is given by the following identity for , , , :

| (33) |

where from (27).

It is clear that distribution of may be theoretically obtained from this theorem. In fact, our goal is to propose expressions of this distribution that only involves quantities that were determined in Section 2.1, e.g. scale functions, which we saw can be available in many situations, as opposed to measures and appearing in (33) which, as seen in (26), are available only through double Laplace transforms. More precisely, we have the following results.

Theorem 2

We have for all and ,

| (34) | |||||

| (35) |

where is density of r.v. and defined in (15) with . Besides, for all , and for , , the Laplace transform of jointly to density of the under and overshoot is given by

| (36) |

Let us compare results given in Theorem 2 with existing ones in the literature concerning last passage times of Lévy processes. References [11] and [5] give distributions of respectively last exit times and last exit times before an exponentially distributed time, in terms of their Laplace transform, for a similar class of Lévy processes; however Theorem 2 is more adapted here as it directly gives its cdf jointly to the density of the overshoot, thus avoiding an inverse Laplace transform. As said before, the slight advantage of Formula (36) over (33) is that it only involves the scale function.

Proof 3.2

Let us start by showing (34) and (35). Let . By definition of we note that for all event is equal to . Hence using the Markov property:

where is the probability that process

starting from will never hit and is given e.g. through Formula (4) p.19 of [20] by

and where is the density of r.v. and in

(15). By integrating from to one gets (34). Equation

(35) stems from the basic equality .

We now turn to (36), and use Theorem 1 to this end. Since by

Fubini theorem we have

and in view of (33), one just needs to compute the following integral:

| (37) |

which we strive to do now. The first integral in the righthandside of (37) verifies,

| (38) | |||||

Relation (30) yields that which, from (31), tends to as . This justifies the following integration by parts:

| (39) |

which, inserted in (38), yields the following simplification

| (40) |

The second integral in the righthandside of (37) verifies

| (41) | |||||

3.2 Examples

We consider here some examples from those studied previously and for which last-passage time is relevant.

Brownian motion with positive drift

In the case where , and , we have

which, plugged in (34) and (35), yields expression of the cdf as well as its cdf jointly to density of . Note that by deriving this expression of the cdf one obtains after some calculation the following density for

which agrees with the already known density of the last passage time of a Brownian motion with drift, see e.g. Expression (1.12) p.2 of [26].

Perturbed gamma process

In the case where is a gamma process with shape parameter and scale parameter , densities of and are given by and . We also recall that function defined in Proposition 3 has expression given in (18) with characteristics of the gamma perturbed process being given by (21). Hence a bit of calculation yields

where , , is the gamma function and , , is the parabolic cylinder function (see (9.241.2) p.1064 of [17]). These expressions, plugged in (35) and (36), yield expression of the cdf of jointly to density of as well as the Laplace transform of jointly to density of the over and undershoot.

Perturbed compound Poisson process with phase-type distributed jumps

In the case where is a compound Poisson process with phase-type distributed jumps of parameters as in Section 2.2, we have, using same notations as in that section that density of shocks is equal to (see Theorem 1.5(b) p.218 of [2])and

where . These expressions, plugged in (35)and (36), yield expression of the cdf of jointly to density of as well as the Laplace transform of jointly to density of the over and undershoot.

3.3 Reflected processes

As for the previous section dealing with first-passage time, we consider the last-passage time for the reflected version of perturbed increasing Lévy process.

Theorem 3

The Laplace transform of is given by

where we recall that with .

Proof 3.3

We start similarly as in the proof of Theorem 2 and let an independent r.v. following an . Event is equal to . Since reflected process behaves like the non reflected process on event for , we have, for all , and using the Markov property,

| (42) |

where is the probability that process starting from will never hit and has expression , as observed in Proof of Theorem 2. Since on , we have by Fubini theorem (and since is a differentiable function by Remark 2.4),

From Lemma 2.1, we have that which is equal to , as follows an distribution. This yields the result.

Again we emphasize that is available in practice either through series (14) in Proposition 1, or through (17) in Proposition 2. Also note that proof of Theorem 3 implicitly yields the following side result.

Proposition 4

Let be an independent distributed r.v. Then for all we have

| (43) |

Proof 3.4

As in showing (35), we use the fact that as well as (42) to derive that . To obtain (43) we just need to prove that r.v. admits a density given by . Indeed Lemma 2.1 yields that , thus what remains to prove is that is differentiable with respect to . This can be seen thanks to the convenient expression (17) that yields that differentiability property since function is a differentiable function by Remark 2.4 (and is obviously differentiable by (16)).

4 A maintenance policy

We now as an application consider the maintenance strategy described in Barker and Newby [4]. Degradation of a certain component is modelled according to a process . We suppose that, without maintenance, is a perturbed process with same parameters as and that failure occurs at the last passage time of level of the

degradation process.

Let us then consider the following maintenance rule. The component is inspected at times such that inter inspection time verifies , where is some non increasing function. Let be some "maintenance function". On inspection at time , one of the following actions is undertaken:

-

•

either the system did not fail in interval , in which case preventive maintenance occurs and degradation process evolves like with initial condition up until time , where is degradation state at instant ; in other words one has ,

-

•

or the system failed in interval in which case it is repaired and degradation process starts anew, i.e. evolves like with initial condition .

We will suppose in this section that function is differentiable from to and bijective. Note that these two assumptions are not too stringent and can be relaxed, in which case expressions of distributions computed in this section would only be more complicated.

We then define r.v. as the first inspection after which system is reset, i.e.

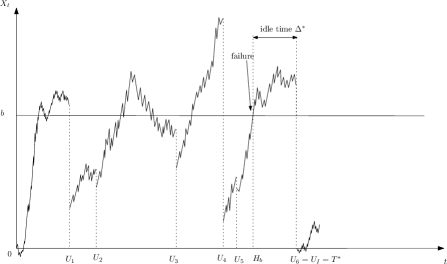

This means that is a regeneration time for the degradation process. Process then behaves like independent copies of in intervals with possibly different initial states. Figure 1 shows a sample path of , with failure in interval and thus starting anew at time with . Note that process thus constructed is càdlàg and such that, given its state at any instant , is independent from , i.e. from its history before . This can be written as

We also introduce the idle time which is the unavailability period of time during which component is down until next scheduled inspection:

where is the failure time of the component and then necessarily lies in . We are interested in quantities involving (possibly joined) distributions of , , as well as the state of the degradation process at inspection times. For this purpose we introduce the following quantities:

-

•

the distribution of the degradation process on inspection after maintenance jointly to the fact that there was no failure before inspection, given that degradation process starts at ,

-

•

, the probability that failure occurred before next inspection, given that degradation process starts at ,

-

•

, , the survival function of the idle time given that degradation process starts at .

These three quantities are easily obtained:

Proposition 1

We have the following expressions

Proof 4.1

We recall that we supposed that is a one to one differentiable function out of practicality. Expression for simply comes from (35) with and a simple change of variable and remarking that last hitting time of level of process with is the same in distribution as that of level of process with . Expression for is obtained from (34) with and because of process starting from . Finally expression for comes from the fact that

and using (34) with and to obtain expression of .

We may now state main results of this section that concern quantities of interest introduced at the beginning of the section.

Theorem 2

Distribution of jointly to the state of the degradation process just after inspection and preventive maintenance is given by

| (44) |

Distribution of the idle time jointly to and the state of the degradation process just after inspection and preventive maintenance is given by

| (45) |

Proof 4.2

The first probability is obtained by writing it in the form where

Since evolution of process in given is independent from , , we may write that probability in the following form

and conclude by the fact that by the stationary increment property we have and in order to obtain (44). (45) is derived by similar arguments.

Note that Theorem 2 yields other interesting quantities. For example the expected time before reparation jointly to the number of inspections/maintenances is obtained thanks to (44) by

Remark 4.3 (Case of the reflected process)

It is possible to adapt the previous setting to the reflected process and constructed a reflected degradation process with inspection and maintenance by considering exponentially distributed inter-inspection times of which conditional distribution given is , instead of deterministic times, where is the same function as in the non reflected caseand again featuring a maintenance function . Results from Theorem 3 as well as equality (43) would yield similar expressions for , for exponentially distributed horizonand an equivalent of Theorem 2 for such an inspection strategy could be obtained.

References

- [1] M.S. Abdel-Hameed. Degradation processes: an overview. Advances in degradation modelling. Applications to reliability, survival analysis and finance, M.S. Nikulin N. Limnios N. Balakrishan W. Kahle C. Huber-Carol (Eds). Chapter 2: 17–25. Birkhaüser, 2010.

- [2] S. Asmussen. Ruin probabilities. Advanced series on statistical sciences and applied probability, World Scientific, 2000.

- [3] S. Asmussen, F. Avram and M. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Processes and their Applications, 109(1): 79–111, 2004.

- [4] C.T. Barker and M.J. Newby. Optimal non-periodic inspection for a multivariate degradation model. Reliability Engineering and System Safety, 94: 33–43, 2009.

- [5] E. Baurdoux. Last exit before an exponential time for spectrally negative Lévy processes. Journal of Applied Probability, 46: 542–558, 2009.

- [6] J. Bertoin. Lévy processes. Cambridge University Press, 2007.

- [7] E. Biffis and M. Morales. On a generalization of the Gerber-Shiu function to path-dependent penalties. Insurance, Mathematics and Economics, 46(1): 92–97, 2010.

- [8] L. Bordes, C. Paroissin and A. Salami. Parametric inference in a perturbed gamma degradation process. Preprint, http://hal.archives-ouvertes.fr/hal-00535812/fr/, 2010.

- [9] T. Chan, A.E. Kyprianou and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probability Theory and Related Fields, 2010.

- [10] R.S. Chhikara and J.L. Folks. The inverse Gaussian distribution as a lifetime model. Technometrics, 19(4): 461–468, 1977.

- [11] S.N. Chiu and C. Yin. Passage times for a spectrally negative Lévy process with applications to risk theory. Bernoulli, 11(3): 511–522, 2005.

- [12] D.R. Cox and H.D. Miller. The theory of stochastic processes. Chapman and Hall/CRC, 1965.

- [13] R.A. Doney. Some excursion calculations for spectrally one-sided Lévy processes. Séminaire de Probabilités XXXVIII, M. Emery, M. Ledoux and M. Yor (Eds), pp.5–15. Springer, 2005.

- [14] M. Egami and K. Yamazaki. On scale functions of spectrally negative Lévy processes with phase-type jumps. arXiv:1005.0064v3, 2010.

- [15] J.L. Folks and R.S. Chhikara. The inverse Gaussian distribution and its statistical application - A review. Journal of the Royal Statistical Society (B), 40: 263–275, 1978.

- [16] J. Garrido and M. Morales. On the expected discounted penalty function for Lévy risk processes. North American Actuarial Journal, 10(4): 196–218, 2006.

- [17] I.S. Gradshteyn and I.M. Ryzhik. Tables of integrals, seriesand products. Academic Press, 1980.

- [18] F. Hubalek and A.E. Kyprianou. Old and New Examples of Scale Functions for Spectrally Negative Lévy Processes. Progress in Probability, 63: 119–145, 2010.

- [19] A.E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Springer, 2006.

- [20] A.E. Kyprianou and Z. Palmowski. A martingale review of some fluctuation theory for spectrally negative Lévy processes. Séminaire de Probabilités XXXVIII, M. Emery, M. Ledoux and M. Yor (Eds), pp. 16–29. Springer, 2005.

- [21] A.E. Kyprianou, J.C. Pardo and V. Rivero. Exact and asymptotic -tuple laws at first and last passage. Annals in Applied Probability, 20(2):522–564, 2010.

- [22] A. Lehmann. Joint modelling of degradation and failure time data. Journal of Statistical Planning and Inference, 5(1): 1693–1706, 2009.

- [23] C. Park W.J. Padgett. Accelerated degradation models for failure based on geometric Brownian motion and gamma processes. Lifetime Data Analysis, 11:511–527, 2005.

- [24] M.R. Pistorius. On exit and ergodicity of the spectrally negative Lévy process reflected at its infinmum. Journal of Theoretical Probability, 17(1): 183–220, 2004.

- [25] M.R. Pistorius. A potential-theoretical review of some exit problems of spectrally negative Lévy processes. Séminaire de Probabilités XXXVIII, M. Emery, M. Ledoux and M. Yor (Eds), pp. 30–41. Springer, 2005.

- [26] C. Profeta, B. Roynette and M. Yor. Option prices as probabilities. Springer-Finance, 2010.

- [27] B. Roynette, P. Vallois and A. Volpi. Asymptotic behavior of the hitting time, overshoot and undershoot for some Lévy processes. ESAIM Probability and Statistics, 12: 58–97, 2008.

- [28] M. Shaked and J.G. Shanthikumar. On the first-passage times of pure jump processes. Journal of Applied Probability, 25(3): 501–509, 1988.

- [29] C.C.L. Tsai and G.E. Willmot. A generalized defective renewal equation for the surplus process perturbed by diffusion. Insurance, Mathematics and Economics, 30: 51–66, 2002.