An application of the method of moments to volatility estimation

using daily high, low, opening and closing prices

Cristin Buescu

Department of Mathematics, King’s College, London

Michael Taksar111This work was supported by

the Norwegian Research Council: Forskerprosjekt ES445026, “Stochastic

Dynamics of Financial Markets.” Mathematics Department, University of Missouri

Fatoumata J. Koné

Citibank, London

Abstract

We use the expectation of the range of an arithmetic Brownian

motion and the method of moments on the daily high, low, opening and closing

prices to estimate the

volatility of the stock price.

The daily price jump at the opening is

considered to be the result of the unobserved evolution of an after-hours

virtual trading day.

The annualized volatility is used to calculate Black-Scholes prices for European options,

and a trading strategy is devised to profit when these prices differ flagrantly from

the market prices.

Key words: Range-based volatility estimation, method of moments,

daily high, low, opening and closing prices, density and expectation of the

range of an arithmetic Brownian motion.

This article is a modified version of what has been studied in the Ph.D. thesis

of Koné (1996). It concerns the application of the method of moments to

range-based volatility estimation using daily high, low, opening and closing

stock prices.

Aiming to estimate volatility and not to measure it, we assume a Black-Scholes

framework with constant volatility and use daily data to achieve it (see

Rogers and Zhou (2008) for further motivation for this choice).

Incidental to this is the derivation of the density and expectation of the

range of an arithmetic Brownian motion. Subsequent to this thesis, portions of

it have been studied for different purposes (see, for instance, Sutrick et al

(1997) for the use of the density of the range of an arithmetic Brownian motion

in the do-nothing option, or Magdon-Ismail et al (2000, 2004) for the use of

the expectation of the range of an arithmetic Brownian motion in different

contexts). In particular, expressing the density of the range in the context

of Sutrick et al (1997) corrects their expression.

The literature on range-based volatility estimation includes classic work by

Garman and Klass (1980), Parkinson (1980), Rogers and Satchell (1991) and

Rogers et al (1994), whose estimators are reviewed in Yang and Zhang (2000).

Of these, the latter paper is most related to the current one because it

considers after-hours price jumps in addition to drift. However, the methods

presented here are different222see

Remarks 3.1 and 3.2,

and perhaps more practical (see the remarks of

Chan and Lien (2003) on the empirical availability of certain parameters in

Yang and Zhang (2000)).

Starting from the joint density of the running maximum and the current value of

an arithmetic Brownian motion, the density of their difference (referred to as

half-range) is obtained, and its expectation computed. This allows the

computation of the expectation of the full range (defined as maximum minus

minimum), which will then be used in the method of moments for intra-day

volatility estimation.

After-hours arrival of information results in price jumps at the opening, and

we model this as a virtual trading day which is unobservable, but which,

when succeeding the trading day, gives on average the complete statistical

representation of one day.

Black-Scholes option prices are computed using the parameter estimates, and

when they differ the most from the observed market prices a profit is made by

an appropriately devised trading strategy.

The paper is organized as follows. In Section 2 we derive the expectation and

the density function of an arithmetic Brownian motion. In Section 3 the

method of moments is used to estimate the parameters of the stock price based on

daily high, low, opening and closing data. The estimated parameters are then used in Section 4

to price European options on the stock, which are then compared to market

prices to identify instances of flagrant differences.

The effect of the mispricing is estimated by computing the

profit to be made in these opportunities. We conclude in Section 5 with

some comments on the efficiency of the method of moments in volatility

estimation.

2 The range of an arithmetic Brownian motion: expectation and density

Let be a probability space

endowed with a filtration ,

and let be a one-dimensional standard Brownian motion

adapted to . For let denote a standard arithmetic Brownian motion with

drift and volatility :

(2.1)

and let , and

denote its running maximum, minimum, and range, respectively:

(2.2)

First we derive the expectation of the range of the arithmetic Brownian

motion . This is achieved by computing the density and expectation of the

half-range from the joint density of and .

Lemma 2.1.

The joint density function of an arithmetic Brownian motion and its

running maximum can be expressed as:

(2.3)

Proof.

The proof is standard.

Using the martingale ,

Girsanov’s change of measure defines a new probability measure for

any measurable set by .

Theorem 3.2.2 of Karatzas and Shreve (1988) with and

gives that is a local

martingale.

The process is

a Brownian motion under the new probability measure . Equivalently,

is a Brownian

motion with drift under , and we can write:

(2.4)

An application of the reflection principle gives:

where we denote by and the standard normal density

and cumulative distribution functions, respectively.

Differentiating the formula above with respect to gives:

(2.5)

Replacing (2.5) in (2.4) and differentiating first with respect to

gives:

and differentiating then with respect to gives:

The joint density is given by the term multiplying

above.

∎

Remark 2.1.

This is one of those results that seemed to be always at hand (it can be

obtained from equation (1.8.8) of Harrison (1985)), but never derived.

Note the typo in Yang and Zhang (2000), whose expression (B1) has a plus for the

first fraction in the exponential. For this was used in Example E5

of Karatzas and Shreve (1998) in relationship to Clark’s formula to obtain

explicitly the hedging portfolio.

The density of the half-range can be obtained using a standard

two-dimensional transformation of the above joint density.

Lemma 2.2.

The density of the half-range is given by:

(2.6)

Proof.

For and

the joint density is

Taking and and using Lemma 2.1 gives:

Note that implies , thus the marginal density of is:

A change of variable gives:

therefore:

This can be rewritten as:

(2.7)

and the result follows.

∎

Proposition 2.1.

The expectation of the half-range is given by:

(2.8)

Proof.

A simple calculation yields:

A change of variable gives the result.

∎

Consider now . For each path of the Brownian motion

with drift consider a symmetric path of a Brownian motion

having drift . Then and

can be calculated using the equation (2.8) with

replaced by . Whereas the formula for the expectation of the range

follows.

Theorem 2.1.

The expectation of the range of the arithmetic Brownian motion defined in

(2.1) is given by:

(2.9)

Let us denote this

expected range function by . On closer inspection this can

be further simplified as a function of just two quantities:

(2.10)

where the function is defined by:

(2.11)

Note that as it should (the range

over a time interval of an arithmetic Brownian motion with parameters

and is the same as that over when the parameters change

to and ).

In the remainder of this section we derive the density of the range of

the arithmetic Brownian motion . This is achieved by the use of the joint

density of the minimum and the maximum of , a result with its own merit,

that we could not find published prior to Koné (1996) (Borodin and Salminen

(1996, 1.15.4) published in the same year the joint cumulative distribution

function only in terms of some definite integrals).

A version of this result is used in Sutrick et al (1997) for the same purpose,

but there it seems to have incorporated an error.

To obtain the joint density of the maximum and the minimum we start

with a lemma.

Lemma 2.3.

We can write:

(2.12)

where

(2.13)

Proof.

Using the change of measure of the proof of Lemma 2.1 and

Girsanov’s theorem we have:

Substituting (2.19)-(2) in (2.18) gives

the result.

∎

Proposition 2.2.

The joint density function of and can be represented as:

with

(2.22)

(2.23)

(2.24)

(2.25)

(2.26)

(2.28)

(2.29)

where

(2.30)

Proof.

From Lemma 2.3 we write as the difference of two terms,

which we denote and :

(2.31)

In each and we combine the exponents and then use, respectively,

a change of variable:

(2.32)

followed by an integration by parts for and replacement

of by via . The resulting eight terms are then then denoted ,

.

∎

We use the above expression to derive the density of the range. To make it

suitable for comparison with that obtained by Sutrick et al (1997) in their

Proposition 1, we change in the summations of

and .

Proposition 2.3.

The density function for the range of an arithmetic Brownian motion

can be written as:

(2.33)

where

(2.34)

and

(2.35)

with

Proof.

After replacing by in , of Proposition

2.2,

a two-dimensional transformation , gives, via Jacobian, the density

of the range and the running maximum. Its marginal density is the one we seek:

Applying a change of variable and integration by parts gives the result.

∎

Remark 2.2.

This result

corrects that of Sutrick et al (1997) where there appears to be a mistake

in the computations.

Remark 2.3.

The probabilistic starting point for both Koné (1996) and Sutrick et al

(1997) is

. The former uses a result

of Feller (1951) that can be traced to Lévy (1948):

(2.36)

while the latter uses a result of Billingsley (1968):

(2.37)

The probabilistic results

(2.36) and (2.37) are in fact equivalent, as one can be obtained from the other by

appropriately replacing the summation index with

and with .

3 The method of moments applied to volatility estimation

using daily high, low, opening and closing prices

In this section we apply Theorem 2.1 to the estimation of the drift

and volatility parameters of the stock price from

market data on high, low, opening and closing prices.

Definition 3.1.

i) A trading day is the period elapsed between the opening and

the closing bells of a calendar day.

ii) A virtual trading day is the after-hours period

beginning from the closing of one trading day and ending at the opening

of the next trading day.

iii) A one-day period consists of one trading day followed by one

virtual trading day.

We assume that the stock price has

the usual geometric Brownian motion dynamics:

(3.1)

Then the log-stock price is the arithmetic Brownian motion

defined in (2.1)

with drift coefficient

(3.2)

Note that is the one-day period drift of the stock price , while

is the similar drift of the log-price ; the volatility

parameter is the same for both and .

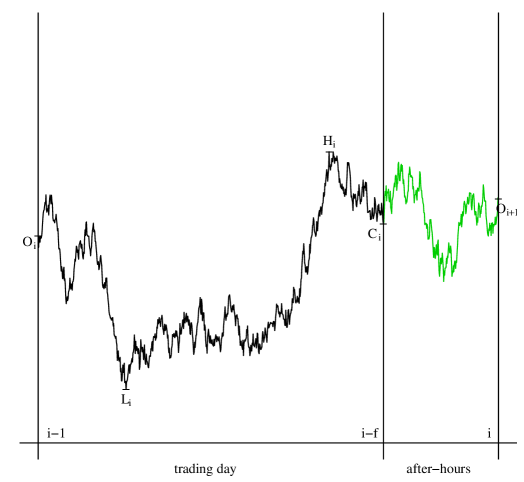

The market data used for parameter estimation is as follows: for each one-period

day we denote by the opening price and

by

and the intra-day high and low prices, respectively (i.e. the high and

low are observed only during the trading day, and not the virtual trading day

- see Figure 1).

The after-hours arrival of information in the market determines a jump between

the closing price

of one trading day and the opening price

of the next day. We model this jump by letting the same geometric

Brownian motion have an unobserved evolution during a virtual trading

day. The length of this virtual trading day is assumed to be, on average,

a fraction

of the unit length of the one-day period.

Remark 3.1.

This assumption follows

Garman and Klass (1980) and

Yang and Zhang (2000), except that they assume the after-hours trading day precedes

the actual trading day. They call it the opening jump (from to ),

and assume it is modeled

by a Poisson process.

Figure 1: A one-day period consisting of a trading day and an after-hours period

The evolution of the price during the trading period is given by:

(3.5)

and during the after-hours virtual trading period by:

(3.6)

Taking expectation in (3.5) when

and in (3.6) when gives:

(3.7)

(3.8)

Using identically distributed to , the trading day and

virtual trading day variances are obtained, respectively, as:

(3.9)

Thus, we can write heuristically:

To estimate the variance over the trading day we use the method of moments.

The range

of the arithmetic Brownian motion over the trading day

was obtained in equation (2.10):

This leads to the following equation to be solved for , the estimate of

:

(3.13)

The squared of this solution gives an estimate of

the variance (volatility squared) corresponding to the trading day part of

a one-day period.

For the after-hours part of the one-day period we have two choices:

(centered approach) used in Yang and Zhang (2000), or (non-centered)

used in Garman and Klass (1980). Using the former (i.e. the sample standard variance ),

we obtain the estimate for the variance of the entire one-day period as:

(3.14)

or, in annualized form, as:

(3.15)

Denoting by the sample variance of used in their estimator

by Yang and Zhang (2000) :

where is the estimator of Rogers and Satchell (1991) and

Rogers, Satchell and Yoon (1994) and is a constant, we note the following.

Remark 3.2.

i) The term replaces the linear combination of and

used by Yang and Zhang (2000) for the intra-day trading period, and it does not need estimating the value

of that achieves minimum variance.

ii) Our estimator is a true range-based estimator (log-range to be precise

since it uses ),

unlike that of Yang and Zhang (2000).

iii) Our estimator is independent of both the drift and the weight of

the after-hours information.

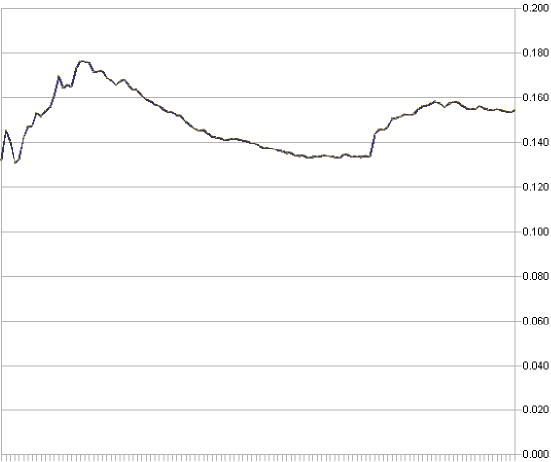

Example 3.1.

Consider the market data on the high, low, opening and closing prices for the IBM stock

for the period from May 26, 2010 to June 18, 2010.

For each of these days we consider the historical 3-month 333For parameter estimation Hull

(2006, p. 287) recommends using historical data of 90 to 180 days. estimates of and ,

and we solve the corresponding equation (3.13).

The solution is our estimate of the volatility corresponding to the trading day,

and we present it in annualized form (i.e. multiplied by ) in Figure 2.

We compare our estimate of the volatility corresponding to

a one-day period with the one of Yang and Zhang (2000). On June 18, 2010 they are

(see (3.15)) and (annualized

volatility corresponding to ).

Figure 2: Estimated intra-day IBM volatility - May 26 to June 18, 2010

4 European options: mispricing opportunities

We use the resulting annualized volatility to compute the Black-Scholes prices of European options on the

stock.

We then seek those instances when the computed prices differ the most from the

market prices, and devise trading strategies to take advantage of the price

difference.

We now use the volatility parameter estimated above to price European call

options

using the Black-Scholes formula:

(4.16)

with

We devise a trading strategy to take advantage of the information differential

between our estimated prices and market prices. For simplicity we trade only in

European call options, and assume that at expiry there is a payment equal to

the payoff so that no actual trading occurs in the underlying stock (naked

trading).

Having assumed a constant volatility there is no volatility smile and no

stochastic volatility444Alternative approaches like

stochastic volatility or econometric models (ARMA, GARCH etc) are not discussed

here., so we restrict our analysis to

European call options

whose strike prices are relatively close to the stock price at the beginning

of the period (preferably in the money), and whose expiry dates are up to

three months

(the parameters can be re-estimated later in view of new data).

Example 4.1.

Consider the market prices for the European call options on IBM for the period

May 26, 2010 to June 18, 2010 with expiry dates June 18 and July 16,

and strike prices (the stock price on May 26 was 125.91).

We compare these market prices with the Black-Scholes prices calculated

using (4.16). Here the inputs are the stock price, the volatility estimated in

Example 3.1, and the value of the 1-month US Treasury

bill yield for the previous day (online

Treasury data555http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/default.aspx

Since the intra-day volatility of Example 3.1 that we use in Black-Scholes formula

does not include the effect of the after-hours evolution,

we compensate by allowing our prices to differ by up to 10% from the bid-ask spread. Thus,

we trade when our estimated call price falls outside the interval (0.9bid-price, 1.1ask-price).

There are two cases.

If our price is lower, then we short-sell the option at the bid price and wait for the first day when the

estimated price is no longer lower to buy back the option at the then ask price. If it expires and the call

option is exercised then we buy the stock in the market and deliver it.

If our price is higher, then we buy the option at ask price and wait for the first day when the price is no

longer higher to sell it at the then bid price. If it reaches expiry date, then we exercise it.

This trading strategy is summarized in Algorithm 1 for between May 26, 2010 and

June 18, 2010 for European call options expiring at close June 18, 2010. The data is retrieved once a day,

except on expiration date when it is retrieved several times a day (this can be implemented as an algorithmic

trading strategy and deployed continuously without much effort, especially by those interested in technical

trading).

t

K

(bid,ask)

trade

t

(bid,ask)

trade

profit

May 26

130

0.90

(1.16,1.17)

sell

May 27

(0.96,0.99)

buy

0.17

May 28

130

0.57

(0.75,0.78)

sell

Jun 2

(0.67,0.70)

buy

0.05

Jun 7

125

1.92

(2.20,2.23)

sell

Jun 8

(1.21,1.23)

buy

0.97

Jun 7

130

0.29

(0.42,0.44)

sell

Jun 8

(0.15,0.17)

buy

0.25

Jun 8

120

3.69

(4.15,4.20)

sell

Jun 9

(4.60,4.75)

buy

(0.6)

Jun 9

125

1.09

(1.30,1.38)

sell

Jun 10

(3.05,3.15)

buy

(1.77)

Jun 17

130

1.09

(0.90,0.94)

buy

Jun 19

(1.00,1.05)

sell

0.06

Jun 18a

130

0.60

(0.48,0.51)

buy

Jun 18b

(0.63,0.69)

sell

0.12

Jun 18c

130

0.18

(0.21,0.25)

sell

Jun 18d

=130.14

exe

0.07

a

at 12:27pm

b

at 13:36pm

c

at 15:58pm

d

at 16:00pm

e

if exercised

Table 1: Trading in the call option expiring June 18, 2010

(left: open a position, right: close position)

Remark 4.1.

This strategy results in an overall loss of 0.68 (see Table 1). This is due mostly

to one large loss induced by a large sudden move in the stock price

on June 10 (127.3 versus 123.9 the day before). That is because we use yesterday’s

intra-day volatility to trade in today’s world.

Over a time horizon longer than a month the strategy can absorb

such shocks in the stock prices, provided they are sparse. Alternatively, one can

implement an additional stopping rule when the change in the stock price exceeds a pre-determined margin.

A similar behaviour is exhibited when applying the same trading strategy to

the European call option expiring at close July 16, 2010, but as the expiry date

is longer than a couple of months the limitations of the assumptions of the model become apparent.

5 Conclusions

We have used the method of moments to estimate the volatility of the stock price

and used this to identify arbitrage opportunities in the market of European

options. As a by-product we have derived the density and expectation of the

range of an arithmetic Brownian motion.

In comparison to the estimate of Yang and Zhang (2000), our volatility estimate takes

advantage of the actual range of the Brownian motion and perhaps does not

overestimate as much. It is most useful for short expiration dates and for strike prices

that are not far out. We believe it is an efficient alternative that

can be easily computed and has a practical implementation. These traits recommend it

to the attention of practioners in the field.

REFERENCES

Billingsley, P. (1968):

Convergence of probability measures. John Wiley, New York.

Chan, L. and D. Lien (2003):

Using high, low, open, and closing prices to estimate the effects of cash

settlements on futures prices.

International Review of Financial Analysis 12, 35–47.

Fama, E.F. (1965):

The behaviour of stock market prices.

Journal of Business 38, 34–105.

Feller, W. (1951):

The asymptotic distribution of the range of sums of independent random

variables.

Annals of Mathematical Statistics 22, 427–432.

Garman, M. and M. Klass (1980):

On the estimation of security price volatilities from historical data.

Journal of Business 53(1), 67–78.

Harrison, J.M. (1985):

Brownian motion and stochastic flow systems.

Wiley, New York.

Hull, J.C. (2006):

Options, futures and other derivatives. 6th ed,

Prentice Hall, New Jersey.

Karatzas, I. and S. E. Shreve (1998):

Brownian motion and stochastic calculus.

Springer, New York.

Koné, F. J. (1996):

Estimation of the volatility of stocks using the high, low and

closing prices.

Ph.D. thesis, State University of New York at Stony Brook.

Lévy, P. (1948):

Processus stochastique et mouvement brownien. Gauthier-Villars, Paris.

Magdon-Ismail, M. and A. Atiya (2000):

Volatility estimation using high, low and close data - a maximum likelihood

approach.

Computational Finance, June CF2000 Proceedings.

Magdon-Ismail, M., A. Atiya, A. Pratap and Y. Abu-Mustafa (2004):

On the maximum drawdown of a Brownian motion.

Journal of Applied Probability, 41(1), 147–161.

Parkinson, M. (1980):

The extreme value method for estimating the variance of the rate of return.

Journal of Business 53(1), 61–65.

Rogers, L.C.G. and S. Satchell (1991):

Estimating variance from high, low and closing prices.

Annals of Applied Probability 1(4), 504–512.

Rogers, L.C.G., S. Satchell and Y. Yoon (1994):

Estimating the volatility of stock prices: a comparison of methods that use

high and low prices.

Applied Financial Economics 4, 241–247.

Rogers, L.C.G. and F. Zhou (2008):

Estimating correlation from high, low, opening and closing prices.

The Annals of Applied Probabilty 18(2), 813–823.

Sutrick K., J. Teall, A. Tucker and J. Wei (1997):

The range of Brownian motion processes: density functions and derivative

pricing applications.

The Journal of Financial Engineering 6(1), 31–46.

Yang D. and Q. Zhang (2000):

Drift-independent volatility estimation based on high,

low, open, and close prices.

Journal of Business 73, 477–491.