Band Control of Mutual Proportional Reinsurance

Band Control of Mutual Proportional Reinsurance

Abstract

In this paper, we investigate the optimization of mutual proportional reinsurance — a mutual reserve system that is intended for the collective reinsurance needs of homogeneous mutual members, such as P&I Clubs in marine mutual insurance and reserve banks in the U.S. Federal Reserve. Compared to general (non-mutual) insurance models, which involve one-sided impulse control (i.e., either downside or upside impulse) of the underlying insurance reserve process that is required to be positive, a mutual insurance differs in allowing two-sided impulse control (i.e., both downside and upside impulse), coupled with the classical proportional control of reinsurance. We prove that a special band-type impulse control with and , coupled with a proportional reinsurance policy (classical control), is optimal when the objective is to minimize the total maintenance cost. That is, when the reserve position reaches a lower boundary of , the reserve should immediately be raised to level ; when the reserve reaches an upper boundary of , it should immediately be reduced to a level .

An interesting finding produced by the study reported in this paper is that there exists a situation such that if the upside fixed cost is relatively large in comparison to a finite threshold, then the optimal band control is reduced to a downside only (i.e., dividend payment only) control in the form of with . In this case, it is optimal for the mutual insurance firm to go bankrupt as soon as its reserve level reaches zero, rather than to jump restart by calling for additional contingent funds. This finding partially explains why many mutual insurance companies, that were once quite popular in the financial markets, are either disappeared or converted to non-mutual ones.

1 Introduction

Reinsurance has been long investigated as an intrinsic part of commercial insurance, of which the mainstream modeling framework is profit maximization with the one-sided impulse control of an underlying reserve process. There are two types of one-sided impulse control: downside-only impulse control (such as a dividend payment) with a fixed cost (e.g., Cadenillas et al. [8], Hojgaard and Taksar [15]) and upside-only impulse control (such as inventory ordering) with a fixed cost (e.g., Bensoussan et al. [2], Eisenberg and Schmidli [13], Sulem [19]). In this paper, we examine mutual proportional reinsurance — a mutual reserve system that is intended for the collective reinsurance needs of homogeneous mutual members, such as the P&I Clubs in marine mutual insurance (e.g., Yuan [20]) and the reserve banks in the U.S. Federal Reserve (e.g., Dawande et al. [11]). A mutual insurance differs from a general (non-mutual) insurance in two key dimensions: 1) a mutual system is not for profit and 2) a mutual reserve involves two-sided impulse control (i.e., both a dividend refund as a downside impulse to decrease the reserve with cost and a call for funds as an upside impulse to increase the reserve with cost ). It should be noted that the reserve process for a general insurance must always be positive (above zero), and the insurance firm is considered bankrupt as soon as its reserve falls to zero.

The mutual proportional reinsurance model developed in this paper is a generalization of the proportional reinsurance models (e.g., Cadenillas et al. [8], Hojgaard and Taksar [15], Eisenberg and Schmidli [13]) and is modified with the two differing characteristics noted above. More specifically, the proportional reinsurance rate can be adjusted in continuous time, and the underlying mutual reserve process is regulated by a two-sided impulse control in terms of a contingent dividend payment (i.e., a downside impulse control to decrease the mutual reserve level) and contingent call for contributions (i.e., an upside impulse control to increase the mutual reserve level). The corresponding mathematical problem for mutual proportional reinsurance becomes a two-sided impulse control system combined with a classical rate control in continuous time, a problem yet to be posed in insurance research. A problem that involves a mix of impulse control and classical control is termed a hybrid control problem in control theory, of which the diculty has been well noted (e.g., Bensoussan and Menaldi [3], Branicky and Mitter [5], Abate et al. [1]).

A pure two-sided impulse control problem (i.e., without a classical rate control) was investigated by Constantinides [9] in the form of cash management. Constantinides and Richard [10] showed an optimal two-sided impulse control policy to exist in the form of a band control, denoted with four parameters as with . In other words, when the reserve position reaches a lower boundary , then the reserve should immediately be raised to level ; when the reserve reaches upper boundary , it should immediately be reduced to level . For our mutual proportional reinsurance problem, we specify the corresponding Hamilton-Jacobi-Bellman (HJB) equation and the associated quasi-variational inequalities (QVI), from which we analytically solve the optimal value function. We then prove that a special band-type impulse control with , combined with a proportional reinsurance policy (classical control), is optimal when the objective is to minimize the total maintenance cost. An interesting finding reported here is that there exists a situation such that if the upside fixed cost is relatively large in comparison to a finite threshold , then the optimal band control is reduced to a downside only (i.e., a dividend payment only) control in the form of with . In this case, it is optimal for the mutual insurance to go bankrupt as soon as its reserve level falls to zero, rather than to restart by calling for additional contingent funds. This finding partially explains why many mutual insurance companies, that were once quite popular in the financial markets, are either disappeared or converted to non-mutual ones.

The remainder of the paper is organized as follows. In Section 2, we formulate the mathematical model and specify the HJB equation and the QVI of the corresponding stochastic control problem. We solve the QVI for the optimal value function in Section 3. In Section 3.2, we characterize and analyze the threshold . In Section 4, we prove the verification theorem and verify the optimal control. Finally, we make concluding remarks in Section 5.

2 The Model

2.1 Feasible Control

The classical Cramer-Lundberg model of an insurance reserve (surplus) is described via a compound Poisson process:

where is the amount of the surplus available at time , quantity represents the premium rate, is the Poisson process of incoming claims and is the size of the th claim. This surplus process can be approximated by a diffusion process with drift and diffusion coefficient , where is the intensity of the Poisson process . We assume that the insurer always sets (i.e. ). Thus, with no control, the reserve process is described by

| (2.1) |

where is a standard Brownian motion.

We start with a probability space , that is endowed with information filtration and a standard Brownian motion on adapted to . Two types of controls are used in this model. The first is related to the ability to directly control its reserve by raising cash from or making refunds to members at any particular time. The second is related to the mutual insurance firm’s ability to delegate all or part of its risk to a reinsurance company, simultaneously reducing the incoming premium (all or part of which is in this case channeled to the reinsurance company). In this model, we consider a proportional reinsurance scheme. This type of scheme corresponds to the original insurer paying fraction of the original claim. The premium rate coming to the original insurer is simultaneously reduced by the same fraction. The reinsurance rate can can be chosen dynamically depending on the situation.

Mathematically, control takes a triple form:

| (2.2) |

where is a predictable process with respect to , the random variables constitute an increasing sequence of stopping times with respect to , and is a sequence of -measurable random variables, .

The meaning of these controls is as follows. The quantity represents the fraction of the claim that the mutual insurance scheme pays if the claim arrives at time . Suppose that is chosen at time . Then, in the diffusion approximation (2.1), drift and diffusion coefficient are reduced by factor (see Cadenillas et at. [7], Hojgaard and Taksar [15]).

The fact that the process is adapted to information filtration means that any decision has to be made on the basis of past rather than the future information. The stopping times represent the times when the th intervention to change the reserve level is made. If , then the decision is to raise cash by calling the members/clients. If , then the decision is to make a refund. The fact that is a stopping time and is -measurable also indicates that the decisions concerning when to make a contingent call and how much cash to raise are made on the basis of only past information. The same applies to the refund decisions.

Once control is chosen, the dynamics of the reserve process becomes:

| (2.3) |

Define the ruin time as

| (2.4) |

Control is called admissible for initial position if, for for any ,

| (2.5) |

and if

| (2.6) |

We denote the set of all admissible controls by .

The meaning of admissibility is as follows. At any time the decision to make a refund is made, the refund amount cannot exceed the available reserve. As can be seen in the following, if this condition is not satisfied, then one can always achieve a cost equal to , simply by making an infinitely large refund. The second condition of admissibility is a rather natural technical condition of integrability.

2.2 Cost Structure and Value Function

The objective in this model is to minimize the operational cost and the lost opportunity to invest the money in the market. Cost function is defined as

| (2.7) |

Here, and denote the positive and negative components of , that is, and . The costs associated with refunds are of a different nature. A contingent call always increases the total cost, whereas a refund decreases it. However fixed set-up costs and are incurred regardless of of the size of a contingent call or a refund. In addition, when the call is made and the cash is raised, there is a proportional cost associated with the amount raised. The constant represents the amount of cash that needs to be raised in order for one dollar to be added to the reserve. If the reserve is used for a refund, then a part of it may be charged as tax. The constant represents the amount actually received by the shareholders for each dollar taken from the reserve.

Given a discount rate , the cost functional associated with the control is defined as

| (2.8) |

The objective is to find the value function,

| (2.9) |

and optimal control , such that

2.3 Variational Inequalities for the Optimal Value Function

For each , define the infinitesimal generator . For any twice continuously differentiable function

| (2.10) |

Let be the inf-convolution operator, defined as

| (2.11) |

Definition 2.1.

The QVI of the control problem are

| (2.12) |

and

| (2.13) |

together with the tightness condition

| (2.14) |

3 Solution of the QVI

3.1 The HJB Equation in the Continuation Region

In this model, the application of the control that is related to calls and refunds results in a jump in the reserve process. This type of model is considered in the framework of the so-calledimpulse control. Because we also have a control whose application changes the drift and the diffusion coefficient of the controlled process, the resulting mathematical problem becomes a mixed regular-impulse control problem (e.g., Cadenillas et al. [7]). In the case of a pure impulse control, the optimal policy is of the type, where the four parameters used to construct the optimal control must be computed as a part of a solution to the problem (see Cadenillas and Zapatero [6], Constantinides and Richard [10], Harrison and Taylor [14], and Paulsen [17]). Parameters and represent the levels at which the intervention (application of impulses) must be made, whereas and stand for the positions that the controlled process must be in after the intervention is made. This is a so-called band-type policy, with and understood as the two bands that determine the nature of the optimal control. The interval is called the continuation region. When the process falls inside the continuation region, no interventions/impulses are applied. When an intervention is initiated, the time when the process reaches one of the boundaries of the continuation region corresponds to one of .

We conjecture that, in our case, the optimal intervention (impulse control) component of the problem is also of the band type. Moreover, as the following analysis implicitly shows, we can narrow our search for the optimal policy to a special band-type control , where the level associated with the contingent calls is set to zero. Therefore, only three of the four band-type policy parameters remain unknown. After finding these parameters (and determining the optimal drift/diffusion control in the continuation region), we will see that the cost function associated with this policy satisfies the QVI.

The derivation of the value function is similar to [8] and [7] . Suppose that satisfies all of the QVI conditions: (2.12), (2.13) and (2.14). First note that the function is a decreasing function of , and thus . To satisfy (2.14), for any , at least one of the two functions on the left side of the equation should be equal to zero. We conjecture that the value function has the following structure.

| (3.15) |

for . Also

| (3.16) |

for .

Assume that minimizes the function in foregoing equation. If then

| (3.17) |

provided that the right-hand side of (3.17) belongs to . (Note that if , then (3.16) cannot be satisfied and we exclude from consideration.)

Substituting (3.17) into (3.16), we get

| (3.18) |

The general solution for (3.18) is

| (3.19) |

where and are free constants to be determined later, and

| (3.20) |

It is easy to see that . From (3.17), we obtain the expression for (provided that which will be verified later):

| (3.21) |

Note that the solution of (3.18) coincides with the solution of (3.16) only in the region where

From this expression, we conjecture that there is a switching point such that when . As , by virtue of the equation (3.21), we obtain the following expression for :

| (3.22) |

For , ; and the corresponding differential equation becomes

| (3.23) |

The general solution for (3.23) is

| (3.24) |

where

| (3.25) | |||

| (3.26) |

with . Standard arguments show that

| (3.27) |

for (see e.g., Cadenillas et al. [7]). The boundary conditions for the equation are rather tricky. If and are the points at which the impulse control (intervention) is initiated then the boundary conditions at these points become

| (3.28) | |||

| (3.29) | |||

| (3.30) | |||

| (3.31) |

However, if bankruptcy is allowed and no intervention is initiated when the process reaches , then the boundary condition at 0 becomes straightforward: (see Cadenillas and Zapatero [8] and Cadenillas, et al. [7]). In our case, whether is the point that corresponds to the intervention in the form of a contingent call or whether it corresponds to bankruptcy is not given a priori; rather it is part of the solution to the problem.

We seek the solution by finding a function such that

| (3.32) | |||

| (3.33) | |||

| (3.34) |

To find the free constants in the expressions for an and to paste different pieces of the solution together we apply the principle of smooth fit by making the value and the first derivatives to be continuous at the switching points and ,

| (3.35) | |||

| (3.36) | |||

| (3.37) |

where is defined by (3.22).

(It should be noted that the function , which is constructed from (3.32)-(3.34) subject to conditions (3.28)-(3.31) and (3.35)-(3.37), corresponds to the case in which the optimal policy leads to .) We begin by constructing such a function. The main technique is not to consider the function itself, but rather first to construct .

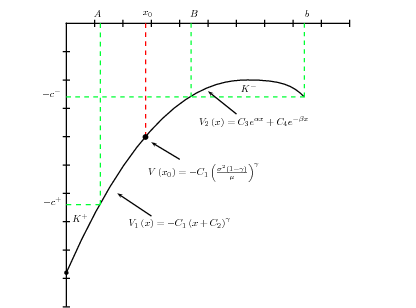

The form of is shown in Figure 1.

From and (3.17), we have . By the continuity on and at , and by (3.23), we have . From this relation and (3.24), we have

Let . Then, , and we can write

We can easily get the inequalities:

| (3.38) |

From (3.22), we get

From , and from the continuity of at , we obtain the expression for :

Let . (Obviously, since .) Now, we can write in terms of and :

What remains is to determine and . Once these constants are found, we have and , and thus . Let

where .

Note that if and , then it is easy to show that for , , and , . Therefore, is decreasing on and is concave on . In the remainder of this section, we find and and complete the construction of the function . We do this in an implicit manner by adopting an auxiliary problem in which no contingent calls are allowed and by using the optimal value function of that problem to‘ construct the function .

Let’s consider a slightly different problem in which only those controls for which on the right-hand side of (2.2) are negative allowed. This problem is similar to that considered in Cadenillas et al. [7]. Let be the optimal value function for this problem. As was shown in [7], the function satisfies the same HJB equation, except for boundary conditions (3.28) and (3.29). These conditions are replaced by .

The same arguments as those above show that we can make the conjecture that the function should be sought as a solution to (3.39)-(3.44) below.

| (3.39) | |||

| (3.40) | |||

| (3.41) | |||

| (3.42) | |||

| (3.43) | |||

| (3.44) |

where .

3.1.1 A solution to the auxiliary problem

First note that a general solution to (3.39), (3.41) is , where is the same as in (3.20) and is a free constant, and a general solution to (3.40) is , where and are the same as in (3.25),(3.26).

To solve our auxiliary problem we apply the same technique as that used in Cadenillas et al. [7]. We begin with , which is defined as follows.

| (3.45) |

In this expression, constants and are chosen in such a way that and . That is, the functions and are continuous at . (Note that is a derivative of on and is a derivative of on .) We next examine the family of functions , where . We seek such that becomes the derivative of the optimal value function .

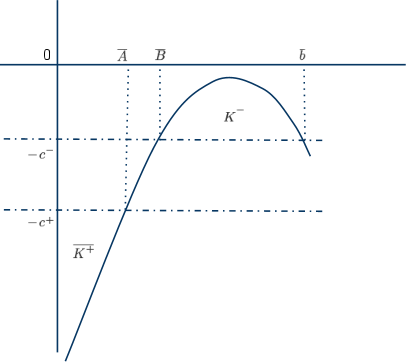

To this end, we start by finding points and such that and . Note that is a concave function, which is easily checked by differentiation. Let , the point at which the maximum of is achieved (it is easy to see that , whereas , which shows that exists; in view of the fact that , it is unique). It is obvious by virtue of the concavity of that, for any , and exist.

We now consider . Informally, is the area under the graph of and above the horizontal line . It is obvious that is a continuous function of . For , we have ; therefore . We set , as , because , whereas and . Therefore, there exists an such that . We also have and . Let

Then,

| (3.46) |

is the optimal value function of the auxiliary problem (see Figure 2). The proof here is identical to that of a similar statement in Cadenillas et al. [7] and thus we omit it.

3.2 The Optimal Value Function for the Original Problem

We employ the function obtained in the previous subsection to construct the derivative of the optimal value function . The main idea is to consider and try to find such that . The optimal value function will then be sought in the form of . To this end, we need the following proposition.

Proposition 3.1.

The proof of this proposition is straightforward.

From(3.45), we can see that has a singularity at with . The concavity of on implies that is increasing on and decreasing on (recall that is constant on ). Therefore, there exists unique such that . Define

| (3.47) |

Note that decreases to at at the order of (see (3.45)); therefore, is integrable at and, as a result, .

The qualitative nature of the solution to the original problem depends on the relationship between and ; hence, we divide our analysis into two cases.

3.2.1 The case of .

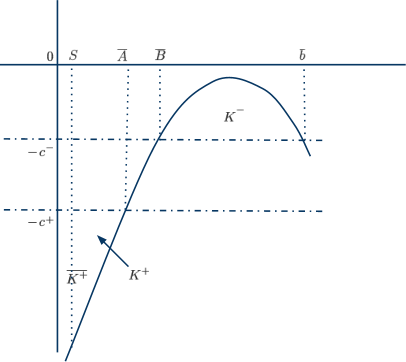

Consider the following integral

Geometrically this integral represents the area of a curvilinear triangle bounded by the lines , and the graph of the function . Obviously, is a continuous function of . Because and , there exists an (see Figure 3) such that

| (3.48) |

In what follows, we show that is the derivative of the solution to the QVI, inequalities (2.12)-(2.14).

Let

| (3.49) |

Also let

| (3.50) | |||

| (3.51) | |||

| (3.52) | |||

| (3.53) | |||

| (3.54) |

By virtue of Proposition 3.1, the function satisfies (3.18) on , as well as (3.23) on . In addition, from (3.48), we can see that

| (3.55) |

From the construction of the function , we can also see that

| (3.56) |

The proof of this theorem is divided into several propositions.

Proposition 3.2.

The function satisfies (3.16) on .

Proof.

1∘. From the construction of the function , we have on . Consequently,

| (3.57) |

on . As satisfies (3.18), it also satisfies (3.16) because these two equations are equivalent whenever (3.16) holds.

2∘. To prove that (3.16) holds for , it is sufficient to show that for each ,

| (3.58) |

because, in view of Proposition 3.1, the function satisfies (3.23) (that is, ). By subtracting (3.58) from the left hand side of (3.23), we can see that (3.58) is equivalent to

| (3.59) |

for . In view of the continuity of the first and second derivatives, and in view of the fact that (3.16) holds on , we know that (3.59) is true for . As both and on the left-hand side of (3.59) are decreasing, therefore is nonpositive for all . ∎

Note that , where

Proposition 3.3.

For each , we have

| (3.60) |

If , or if , then

| (3.61) |

Proof.

1∘. We first prove, that . Suppose that . The functional is continuously differentiable. By construction, is increasing on and decreasing on with for . Therefore, the point is the only point such that . Because , we can see that . Therefore, for ,

Also, iff

However,

This proves that for all and also shows that

| (3.62) |

Because for , we know that for any the function is an increasing function of . Therefore, the minimum in the expression for is attained for ; as a result, .

2∘. Consider for . Because for and for , we can see that has a unique minimum at . Therefore, . Thus, iff

The foregoing inequality always holds true because, by construction,

For , we note, that , and hence

| (3.63) |

∎

To complete the proof of Theorem 3.1, we need only show the following.

Proposition 3.4.

If , then (2.12) holds.

Proof.

This completes the proof of Theorem 3.1.

3.2.2 The case of

When we cannot find any such that (3.48) is satisfied. In this case, we set (that is, we have , which corresponds to ).

To prove this theorem, it is sufficient to prove Propositions 3.2-3.4. The proofs of Propositions 3.2 and 3.4 are identical to the case of , whereas that of Proposition 3.3 requires a slight modification.

Proposition 3.5.

For each ,

| (3.65) |

If , then

| (3.66) |

Proof.

The proof that for all and that for is the same as that in Proposition 3.3.

If , then is equivalent to

The foregoing inequality is always true because

by assumption.

If , then still holds, due to

the same argument as that in Proposition 3.3. ∎

Remark 3.1.

In the case of we have only for , whereas in contrast to the case when . Also, when , we have , whereas if . Equivalently, in the case that the fixed cost to call for additional funds is relatively large (i.e., , the optimal band control is reduced to with . That is, as soon as the reserve reaches zero, it becomes optimal for the mutual insurance firm to go bankrupt, rather than to be restarted by calling for additional funds.

4 Verification Theorem and the Optimal Control

Proof.

We prove this inequality when . In this case, . Let be any admissible control defined by (2.2) and process be the corresponding surplus process (2.3), with . Let be its ruin time given by (2.4). Let and . Then,

| (4.68) | |||||

By convention, . In view of (2.13), we have . Therefore, and

In view of (2.6), this implies that for any the second sum in (4.68) is bounded by the same integrable random variable independent of .

On , process is continuous, and we can apply Ito’s formula to get

| (4.70) | |||||

From this equation, using (2.6) and standard but rather tedious arguments, we can deduce that the first sum in (4) for all is also bounded by the same integrable random variable. Similar arguments show that

| (4.71) |

and

| (4.72) |

(see Cadenillas et al. [7]). Note that the second integral on the right-hand side of (4.70) is a martingale whose expectation vanishes. However, in view of (2.12), the integrand in the first integral of (4.70) is nonnegative. Therefore,

| (4.73) |

and, taking into account the dominated convergence theorem, we can see that the expectation of the first sum on the right-hand side of (4.68) is nonnegative.

Remark 4.1.

For the expectation of the stochastic integral on the right hand side of (4.70) to vanish, it is sufficient for its integrand to be bounded. In particular, it is sufficient for to be bounded. This is the case when . When , the function has a singularity at 0. We can, however, apply the same technique, first replacing by and then passing to a limit as . This will yield inequality (4.74), which is all we need for the proof of Theorem 4.1

Let , that is

| (4.76) |

From (3.46),(3.45), (3.49), and (3.53), we can see that

Consider the process defined as

| (4.77) |

, with , , and and are defined below sequentially.

If (that is, no exists, such that (3.48) holds), then

| (4.78) | |||

| (4.79) |

If (that is, there exists an , such that (3.48) holds), then

| (4.80) | |||

| (4.81) |

Remark 4.2.

Informally, if , then process is a continuous diffusion process with a drift and diffusion coefficient of, and , respectively, until the times of intervention. The times of intervention in this case are the times at which this diffusion process hits the level , which are associated with the refunds of the constant amount of . The time when is hit is the ruin time.

When , the process is a continuous diffusion process with the same drift and diffusion coefficients as above, between the times of intervention. The intervention times are the times at which this process reaches either or . At point , the control is set to displace the process to point , which corresponds to raising cash (making a call to shareholders) in the amount of . Reaching the level results in the displacement of the process to the point which, corresponds to making a refund in the amount of .

Theorem 4.2.

Proof.

In view of (4.67), it is sufficient to show that

| (4.82) |

Equality (4.76) shows that

| (4.83) |

From Propositions 3.3 and 3.5, we know that and if then . Thus, we can repeat the arguments in the proof of Theorem 3.2 and see that, for , all of the inequalities are tight. As a result, we obtain

| (4.84) |

Because we know that, when , we have and, when , the function satisfies , the first term on the left-hand side of (4.84) vanishes, and we get (4.82). ∎

5 Conclusions

The optimal policy in this model has several interesting nontrivial features. The fact that calls should be made only when there is no possibility of waiting any longer (that is when the reserve reaches zero) is supported by intuition. However, the qualitative structure of the optimal policy and its dependence on the model parameters are not as obvious.

It turns out that it is always optimal to pay dividends, no matter what the costs associated with such payments are. However, raising cash may not be optimal when the initial set-up cost is too high. Quantity , which determines the threshold for set-up cost , such that if the cost is higher than this threshold then it is optimal to allow ruin, is in itself determined via an auxiliary problem with a one-sided impulse control. Although there is no closed-form expression for the quantity , it can be determined in an algorithmic manner prior to solving the optimal control problem for the mutual insurance company.

There is one rather curious feature of the optimal solution when . As our analysis shows, in this case, and , the same as is the case when . However, from the construction of the optimal policy, we can see that the two band-type policy is optimal in this case as well. In this borderline case, we thus have two optimal policies, one for which with the lower band equal to and one for which reaching corresponds to ruin and for which . This is a rather unique feature of this particular problem that has not been observed previously.

A natural question arises: what if ruin is explicitly disallowed, and we must find an optimal policy from among those for which . As can be seen from our analysis, we find a solution to this problem for the case of . However, when this inequality does not hold, then of the stochastic control technique and the HJB equation used in this paper do not work. Another approach should be developed, as can be seen indirectly in the work of Eisenberg [12] and Eisenberg and Schmidli [13], where a similar (although not identical) problem is considered for the case of a surplus process modeled via the classical Cramer-Lundberg model. This constitutes an interesting and challenging problem for future study, the nature of whose solution is not obvious at this time.

References

- [1] Abate, A., A. D. Ames, S. Sastry. 2005. Stochastic approximations for hybrid systems, Proceedings of the 24th American Control Conference, Portland, OR, 1557-1562.

- [2] Bensoussan, A., R.H. Liu, S.P. Sethi. 2006. Optimality of an (s, S) policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach, SIAM Journal on Control and Optimization. 44(5), 1650-1676.

- [3] Bensoussan, A., J. L. Menaldi. 2000. Stochastic hybrid control, Journal of Mathematical Analysis and Applications, 249, 261-288.

- [4] Branicky, M.S., V.S. Borkar, S.K. Mitter. 1998. A unified framework for hybrid control: model and optimal control theory, IEEE Transactions on Automatic Control, 43(1), 31-45.

- [5] Branicky, M.S., S.K. Mitter. 1995. Algorithms for optimal hybrid control, Proceedings of the 34th IEEE Conference on Decision and Control.

- [6] Cadenillas, A., F. Zapatero. 1999. Optimal central bank intervention in the foreign exchange market, Journal of Economic Theory, 87(1), 218-242.

- [7] Cadenillas, A., T. Choulli, M. Taksar, L. Zhang. 2006. Classical and impulse stochastic control for the optimization of the dividend and risk policies of an insurance firm, Mathematical Finance. 16(1), 181-202.

- [8] Cadenillas, A., F. Zapatero. 2000. Classical and impulse stochastic control of the exchange rate using interest rate and reserves, Mathematical Finance, 10, 141-156.

- [9] Constantinides, G. M. 1976. Stochastic cash management with fixed and proportional transaction costs, Management Science, 22, 1320-1331.

- [10] Constantinides, G.M., S.F. Richard. 1978. Existence of optimal simple policies for discounted-cost inventory and cash management in continuous time, Operations Research, 26(4), 620-636.

- [11] Dawande, M., M. Mehrotra, V. Mookerjee, C. Srikandarajah. 2010. An analysis of coordination mechanism for the U.S. cash supply chain. Management Science, 56(3), 553 - 570.

- [12] Eisenberg, J. 2011. Optimal control of capital injections by reinsurance and investments, working paper.

- [13] Eisenberg, J., H. Schmidli. 2010. Minimizing expected discounted capital injections by reinsurance in a classical risk model, Scandinavian Actuarial Journal, forthcoming (first published on March 19, 2010).

- [14] Harrison, J.M., T.M. Sellke, A.J. Taylor. 1983. Impulse control of Brownian motion, Mathematics of Operations Research, 8(3), 454-466.

- [15] Hojgaard, B., M. Taksar. 2004. Optimal dynamic portfolio selection for a corporation with controllable risk and dividend distribution policy, Quantitative Finance, 4(3), 256-265.

- [16] L{\o}kka, A,. M. Zervos. 2008. Optimal dividend and issuance of equity policies in the presence of proportional costs, Insurance: Mathematics and Economics, 42(3), 954-961.

- [17] Paulsen, J. 2008. Optimal dividend payments and reinvestments of diffusion processes with both fixed and proportional costs, SIAM Journal on Control and Optimization, 47(5), 2201-2226.

- [18] Schmidli, H. 2001. Optimal proportional reinsurance policies in a dynamic setting, Scandinavian Actuarial Journal, Taylor & Francis, 1, 55-68.

- [19] Sulem, A. 1986. A solvable one-dimensional model of a diffusion inventory system, Mathematics of Operations Research, 11, 125-133.

- [20] Yuan, J. 2008. Computational optimization of mutual insurance systems: a quasi-variational inequality approach, Doctoral Dissertation, Hong Kong Polytechnic University.