Optimal Constrained Investment in the Cramer-Lundberg model

Tatiana Belkina

Laboratory of Risk Theory, Central Economics and Mathematics Institute of the Russian Academy of Sciences. , Moscow, Russia

, Christian Hipp

Institute for Finance, Banking and Insurance, Karlsruhe Institute of

Technology, Karlsruhe, Germany

, Shangzhen Luo

Department of Mathematics, University of Northern Iowa, Cedar Falls, IA, USA 50614

and Michael Taksar

Department of Mathematics, University of Missouri, Columbia, MO, USA 60211

Abstract.

We consider an insurance company whose surplus is represented by

the classical Cramer-Lundberg process. The company can invest its

surplus in a risk free asset and in a risky asset, governed by

the Black-Scholes equation. There is a constraint that the

insurance company can only invest in the risky asset at a limited

leveraging level; more precisely, when purchasing, the ratio of

the investment amount in the risky asset to the surplus level is

no more than ; and when shortselling, the proportion of the

proceeds from the short-selling

to the surplus level is

no more than . The objective is to find an optimal investment policy

that minimizes the probability of ruin.

The minimal ruin probability as a function of the initial surplus is

characterized by a classical solution to

the corresponding Hamilton-Jacobi-Bellman (HJB) equation. We study

the optimal control policy and its properties. The interrelation

between the parameters of the model plays a crucial role in the

qualitative behavior of the optimal policy. E.g., for some ratios

between and , quite unusual and at first ostensibly

counterintuitive policies may appear, like short-selling a stock

with a higher rate of return to earn lower interest, or borrowing

at a higher rate to invest in a stock with lower rate of return.

This is in sharp contrast with the unrestricted case, first

studied in Hipp and Plum (2000), or with the case of no

shortselling and no borrowing studied in Azcue and Muler (2009).

This research was supported by the Russian Fund of Basic Research, Grants RFBR 10-01-00767 and RFBR 11-01-00219

This research was supported by a UNI summer fellowship

This research was supported by the Norwegian Research Council

Forskerprosjekt ES445026 “Stochastic Dynamics of Financial Markets”

Correspondence Email: luos@uni.edu, Postal Address: Department of Mathematics, University of Northern Iowa, Cedar Falls, Iowa 50614-0506, USA

1. Introduction

Ruin minimization has become a classical criterion in optimization

models and in recent years it has been extensively studied, being

of a natural interest to the policymakers and supervisory

authorities of the insurance companies. Browne [4] was one of

the first to consider the ruin minimization problem for a

diffusion model; there it was found that the optimal investment

policy is to keep a constant amount of money in the risky asset.

Taksar and Markussen in [17] studied a diffusion

approximation model in which one controls proportional

reinsurance; they obtained the minimal ruin probability function

and the optimal reinsurance policy in a closed form. In [15]

Schmidli studied the ruin optimization problem for the classical

Cramer-Lundberg process, with the control of proportional

reinsurance. In [16] a similar problem was considered with

investment and reinsurance control.

In this paper we study a ruin probability minimization problem in

which there are constraints on the investment possibilities.

Namely, the insurance company has an opportunity to invest in a

financial market that consists of a risk free asset and a risky

asset, however, it can buy the risky asset up to the limit, which

is times the current surplus and it can shortsell the risky

asset up to the limit of no more than times the current

surplus. If , then borrowing to invest is allowed and the

amount borrowed to buy the risky asset is no more than

times the current surplus. The risky asset is governed by a

geometric Brownian motion, and the surplus is modeled by the

classical compound Poisson risk process. The objective is to find

the optimal investment policy which minimizes the ruin

probability. The model was first considered in Hipp and Plum

[6], where there were no constraints on the investment

possibilities, that is the investment in the risky asset could be

at any amount (positive or negative) irrespective of the surplus

level. Further, Azcue and Muler [2], studied the same model

with no shortselling and no borrowing requirement.

It has been noticed, that in the case of no constraints on the investment

(See [4], [6], [7] and [14]),

the optimal investment strategy is highly leveraged

when the surplus levels are small. There are several papers in which

there are direct or indirect constraints imposed on the leveraging level.

In [2] bounds on the leveraging level are the result of

a no-shortselling-no-borrowing constraint.

In [13] only a limited amount of borrowing is allowed and it is at a higher rate than

the risk free lending/saving one.

In this paper we consider general constraints on borrowing and

shortselling, which are formulated in proportions to the surplus;

they can be higher or lower than those of

no-shortselling-no-borrowing ones. Note that in many recent

papers, e.g. [2], [6], and [15], the risk free

interest rate is assumed to be zero after inflation

adjustment, and the rate of return of the risky asset is

positive. It thus excludes the case of . Here, we assume a

positive interest rate and we do not assume any relationship

between and . In [6], the condition is

implicit (there ), and the optimal policy does not involve

short-selling even though it is allowed. The same phenomenon is

observed in diffusion approximation models as well, e.g.

[13] and [14].

The generality of constraints on investment brings a whole new

dimension to the possible qualitative behavior of the optimal

policies. Some of those might look counterintuitive, at first. For

example, depending on the relationship between , and other

parameters of the model, the optimal policy might involve

shortselling not only when but also when .

Moreover, the optimal policy might consist of switching from

maximal borrowing to maximal shortselling then to maximal

borrowing again as the surplus level increases (see a detailed

analysis of the exponential claim size distribution case at the

end of this paper). This is a manifestation of a rather complex

interplay between the potential profit and risk at

different levels of surplus. In short, at some surplus levels it

is optimal for the company to leverage its risky or the risk free

asset (purchase or short-sell) at the maximum levels ( or );

and to bet on stock’s volatility to increase the chances for the

surplus level to bounce back.

Our mathematical technique is based on operator theories

applied for the solution of the corresponding HJB equation

(see [2], [6] and [15]).

We first show existence of a classical solution to the

corresponding HJB equation. To this end we first observe that the minimizer

in the HJB equation is constant, on one of the edges of the admissible values for

the proportion, as long as the wealth of the insurer is small, say.

Then we define a special operator in the space of continuous functions on compact

intervals such that the HJB equation on is equivalent to .

We prove that the operator is Lipschitz and conclude that the equation has a solution

on Finally we show that the solution, extended to is bounded and proportional to

the minimal ruin probability.

The rest of the paper is organized as follows. The optimization

problem is formulated in Section 2. In Section 3,

an operator is defined to show existence of a classical solution to the HJB equation.

A verification theorem is proved in Section 4. In

Section 5 we investigate the case with exponential claim size

distribution and present several numerical examples. The last section is

devoted to economic analysis.

2. The Optimization Problem

We assume that without investment the surplus of the insurance company is

governed by the Cramer-Lundberg process:

where is the initial surplus,

is the premium rate, is a Poisson process with intensity , the random variables ’s are positive i.i.d. representing

the size of the claims.

Suppose that at the time , the insurance company invests a

fraction of its surplus into a risky asset whose

price follows a geometric Brownian motion

Here is the stock return rate, is the volatility,

and is a standard Brownian motion independent of

and ’s. Then the fraction

of the the surplus is invested in the risk free asset whose price

is governed by

where is the risk-free interest rate. If ,

then the insurance company purchases the risky asset at a cost of

no more than its current surplus; if , the insurance

company borrows to invest in the risky asset; and if ,

the insurance company shortsells the risky asset to invest in the

risk free asset. Let stand for the

control functional. Once is chosen, the surplus process

is governed by the equation below

(2.1)

We assume all the random variables are defined on a complete probability

space . On this space we define the filtration

generated by processes and . A control policy (or just a control) is

said to be admissible if is

-predictable and it satisfies . We denote by the set of all admissible

controls.

In this paper, we make the following assumptions:

(i) the exogenous parameters , , , , , ,

are positive constants ( is not allowed); (ii) the claim

distribution function has a finite mean and it has a

continuous density with support .

The ruin time of the process under the investment strategy is defined as follows

(2.2)

and the survival probability as

(2.3)

The maximal survival probability is defined as

(2.4)

which is a non-decreasing function of . If we assume that

is twice continuously differentiable, then it solves the

following Hamilton-Jacobi-Bellman equation:

(2.5)

where

(2.6)

We note that is positive, given that

is an increasing function on .

The minimum in the HJB equation is attained at some value

and this means that

while for all other values and

This implies that for

(2.7)

We have used this formula for numerical calculations when is large enough.

3. Existence of a smooth solution to the HJB equation

For any twice continuously differentiable

function , let

(3.1)

if .

Suppose is non-decreasing and solves HJB equation (2.5) at , then

we can define a maximizer in the following form

(3.2)

and we have

So the minimum is always attained at one of the three points , , or

For consider the equation

(3.3)

From Proposition 4.2 in [2], p. 30, we obtain the existence of a function

which is twice continuously differentiable on with

(3.4)

(3.5)

(3.6)

satisfying equation (3.3).

One can show the formula for by a similar method of Proposition 4.2 in [2].

In the following two Lemmas we show that for small values

of the function is a solution to the HJB equation if , and

is a solution if

Lemma 3.1.

For , there exists

such that on function

solves

(3.7)

Proof.

We consider three cases separately and use the representation of the maximizer given in (3.2).

Firstly, for with , is a maximizer if

Secondly, for small with , since for near the relevant part for the maximum

is increasing in and so we again obtain

Thirdly for small with , it holds that

The results in lemmas 3.1 and 3.2 are intuitively appealing:

at low surplus levels,

when the stock return rate is higher than the interest rate ,

the company invests in the stock at the maximum level ;

on the other hand, when the interest rate is higher,

the company would invest in the risk-free asset at the maximum level of

(all the surplus together with shortselling proceeds at the maximum level ).

For the function with

is now extended to the range as follows.

To this end,

fix and a positive decreasing function with

(to be chosen later).

On the set of functions which are continuous on

consider the operator

(3.9)

where

and is the common density of the claims.

Lemma 3.3.

For the function is continuous on

Furthermore, the operator is Lipschitz with respect to the supremum norm on

Proof.

To prove continuity of we show that for fixed the functions

are uniformly continuous on This is true for the functions

and

The representation

shows that also is continuous on

Since the maximum of uniformly continuous functions is continuous, we have continuity of

Now we consider two continuous functions on and use the norm

Then the inequalities

together with boundedness of imply that there exists a constant

such that for all we have

∎

Using the standard Piccard-Lindelöf argument we now obtain that for all there exists

a continuously differentiable function satisfying

(3.10)

With we obtain a similar function defined on

We further show on .

Define .

Suppose , then it holds . Thus

which contradicts:

We then conclude is never and hence positive on .

Next we proceed to select an appropriate function such that an

anti-derivative of the solution of equation (3.10) solves the HJB equation.

when , by continuity of .

Now we see is twice continuously differentiable and solves HJB equation (2.5) on ;

further notice that for we have (it equals , or ).

Thus, for and provided that both and are finite.

Now we define

(3.13)

and denote

(3.14)

for any , write

(3.15)

We note it holds for .

From the previous discussions,

we see that is twice continuously differentiable and solves HJB equation (2.5) on .

And it holds on . In the sequel, we write ; and we have on . Further is bounded on . In fact, one can show

is bounded (as the verification theorem) and

is the maximal survival probability when investment control is restricted over region . We then see that decreases in .

This shows boundedness of .

Now we proceed to show that is infinite. We state two lemmas without proof.

The following lemma implies that a function that solves the HJB equation coincides with

the fixed point of operator (2.7).

For the case ,

define , where is defined in (3.19);

from Lemma 3.1 and Lemma 3.4,

we have ; now we show by contradiction.

Suppose such does not exist. Then there exists a sequence

such that .

Define ,

then .

Further one can show on

with and .

So there exits such that

Notice

There exists such that on due to boundedness of and .

Further notice

(3.20)

thus

(3.21)

which tends to . From and boundedness of ,

it must hold and then .

Since solves the HJB equation, it then holds . Contradiction!

Thus exits such that . It holds by

continuity of . Hence we can select such that ;

then we have and from Lemma 3.6,

there exists a function which is

concave and twice continuously differentiable on ,

such that on , and it solves

on .

Now define

noticing , , and

(by Lemma 3.6), and then ,

it holds

for , we then have

which is the HJB equation (the maximizer of quadratic function

in

is the vertex ). By Lemma 3.5, we conclude that

and

on .

If , by continuity of

and definition of ,

we have , which contradicts to .

If , we have since

by Lemma 3.6, and it contradicts to

This finishes the proof for the case .

The case can be shown in a similar way.

∎

By Lemma 3.7 and the previous discussions, we have the following theorem:

Theorem 3.1.

Function defined in (3.15),

with the function constructed in (3.13),

is a twice continuously differentiable solution to HJB equation (2.5) on

with the initial values

, , and .

In the following, we show some properties on the

interplay between the optimal policies and parameters.

These theorems are stated via four parameter cases.

We give the proof of Theorem 3.3 in

Appendix 2 and omit proofs the others which are similar.

the associated maximizer in the HJB equation is given by

(3.23)

where it always holds .

For , define sets:

(3.24)

Then we have:

Theorem 3.3.

If and , then

(i)

solves equation (3.22)

on , equation (3.7) on , and equation (3.8) on ;

(ii)

the associated maximizer in the HJB equation is given by

(3.25)

where it always holds .

Define sets

(3.26)

We then obtain the following two theorems for the case :

Theorem 3.4.

If and , then

(i)

solves the equation (3.22)

on set , equation (3.8) on set ;

(ii)

the associated maximizer in the HJB equation is given by

(3.27)

where .

Theorem 3.5.

If and , then

(i)

solves the equation (3.22)

on set , equation (3.7) on set , and equation (3.8) on ;

(ii)

the associated maximizer in the HJB equation is given by

(3.28)

where .

Remark 3.1.

By the verification Theorem 4.1, the function is bounded and proportional to the maximal survival function , in fact, .

Remark 3.2.

Noticing , the optimal policy always involves investment when .

Remark 3.3.

In contrast to our case, when there are no constraints on the investment as in [6], the optimal investment policy involves no shortselling of the risky asset although it is allowed.

Remark 3.4.

If , the optimal investment strategy equals , or .

4. A Verification Theorem

In this section, we prove a verification result; that is, we

show that the solution to the HJB equation is a multiple

of the maximal survival probability function.

The first lemma below shows that ruin is never caused by investment

if investment strategies are constant at low surplus levels.

Lemma 4.1.

For any non-negative integer and an admissible control policy such

that when is small if or if ,

it holds

where is defined in

(2.2), and , , ,… are

the times of claim arrivals.

Next we state an ergodicity result (Lemma 4.2) of the controlled surplus process

and non-triviality (Lemma 4.3) of the optimization.

For proofs of the lemmas we refer readers to [2] and [16].

Lemma 4.2.

For any admissible control policy , the surplus process either

diverges to infinity or drops below with probability .

Lemma 4.3.

There exists a control policy

(e.g., a suitable constant investment strategy),

such that .

Now we prove the verification theorem:

Theorem 4.1.

Suppose is a positive, increasing, and

twice continuously differentiable function on ;

and it solves the HJB equation (2.5). Then is bounded and

the maximal survival probability function is given by .

Moreover, the associated optimal investment strategy is ,

where , and is the surplus at time under

the control policy .

Proof.

For any , we extend to such that is increasing and

twice continuously differentiable on with on

and on .

For any admissible control and positive constant ,

define exit time

Write to denote the first exit time from interval

of the surplus process under the optimal control policy .

By Ito’s Lemma (See [5]), we have

(4.1)

where

Since solves the HJB equation, we have

;

further noticing that

is bounded and , are both martingales,

we take expectation on both sides of (4.1) and obtain

(4.2)

Similarly, for any admissible control , noticing

, it holds

where in the last inequality we used which holds by Lemma 4.1.

Notice as

since the claim distribution has a continuous density.

Letting and then , we obtain

from (4.5), we then have ,

which is the maximal survival probability.

The proof is completed.

∎

5. Analysis of the Case of Exponential Claims and Numerical Examples

We will analyze a specific case in which the claim size has an exponential distribution with

and the claims arrive with intensity . We give several examples.

We note that in Example 1, the parameters satisfy

(5.1)

which is equivalent to (all the parameters will be specified later).

This relation will ensure some nontrivial investment policy, which switches from

maximal long position to maximal shortselling and again to maximal long position when the

surplus increases.

Before we introduce the examples we will state an auxiliary result needed for the analysis.

Lemma 5.1.

Let be the distribution function of an exponential

random variable with parameter . Then any bounded at 0 solutions to the integro-differential equation of the second order

(5.2)

with the initial condition

(5.3)

is also a solution to the linear differential equation of the third order

The proof of this lemma was suggested to the authors by S.V. Kurochkin.

Let denote the left hand side of (5.2). Then differentiating it, we see that the left hand side of (5.4) is equal to . Therefore if is a solution to

(5.2) (that is ) then it is also a solution to (5.4).

From a general theory of the ordinary differential equations with singularities (e.g., see [8], [18] ) and a more detailed analysis in [3] follows an existence of a two parametric family of solutions to (5.4) bounded at 0 whose derivative is also bounded at 0. Moreover each such bounded solution to (5.4) satisfies (5.5) (cf. (3.6)).

Suppose is any bounded at 0 solution to (5.4), which is subject to (5.5). The condition (5.5) implies that is bounded as well.

Obviously for any , the function is a bounded solution to (5.4), satisfying (5.5).

Suppose is a bounded at function which satisfies (5.2) and (5.3). Let

. Take

Then

obviously satisfies (5.4), (5.5). Substitute into (5.2) instead of , and let denote the left hand side of (5.2). Then the left hand side of (5.4) is equal to . Thus

for some constant .

Taking into account that and are bounded, we can substitute

these expressions into the left hand side of (5.2) and see that due to condition (5.3) and

the fact that and by construction.

Therefore satisfies (5.2) , (5.3).

From [11] and [12] we know that there exists at most one solution for an integro-differential equation (5.2) with given and subject to (5.3). Thus .

∎

Lemma 5.2.

Let be a distribution function of an exponential random variable with mean . Then

the integro-differential equation (5.2) with the boundary condition

(5.3) has a one-parametric family of solutions bounded at 0. In the neighborhood each solution of this family of is represented by an asymptotic series

(5.6)

where , and

(5.7)

(5.8)

(5.9)

The asymptotic expansion means that the difference between the and the first terms in the right hand side of (5.6) is when .

The proof of this theorem can be obtained from Lemma 5.1, which reduces the integro-differential equation (5.2) to an ordinary differential equation(5.4), and a general theory of the ordinary differential equations with pole-type singularities (see [18] Ch. 4 and [10]). The particular expression for the coefficients (5.7)-(5.9) has been found in [3].

In the numerical examples, we consider exponential claim size distribution with

mean . Further, set , , and .

The other parameters are given as follows via three examples.

Example 5.1.

( and ) We choose

.

Example 5.2.

( and ) We choose

.

Example 5.3.

( and ) We choose

.

Let be the solution of the HJB equation (2.5) with .

From the previous sections, we know that is finite and the function coincides with the maximal survival probability (2.4); and the optimal feedback control function is given by (3.2). If

then the function satisfies

Numerical computations show that the optimal investment

strategy is quite surprising: there exists such that

(5.13)

In the following we show that such investment strategies typically occur

when (5.1) holds and is large.

From Lemma 3.1 we know that in the neighborhood of 0 the function satisfies

(3.1), that is (5.2) with given by (5.11); and in

this neighborhood. In view of (5.1), the coefficient in the asymptotic

expansion (5.6) of the function at 0 is positive. Thus , when and

(5.14)

If one chooses instead of its asymptotic approximation given by (5.14), then

we see that for

. If is large enough then

is small and the ratio of and the right hand side of (5.14) is close to 1 (note that for given by (5.11) the asymptotic expansion (5.6) does not depend on ) and . The choice of or in our example ensures that this is the case, as numerical

computations show. Therefore there exists

such that for , while and

for . In view of (3.2), the function satisfies (5.2) with given by (5.12) in the right neighborhood of and it satisfies (5.2) with given by (5.11) for .

This shows that for and in the right neighborhood of . Let us show that there exists such that for

, while in the right neighborhood of . That is the point is the first point of the “extreme” switching from the maximal long position to the maximal short position in the risky asset, while is the point of the second “extreme” switching from the maximal short to the maximal long position. Since the function is

convex in the neighborhood of . On the other hand, if for all then

for all and as . Contradiction!

Therefore there exists a point such that while

for . Therefore, as and there

exists such that for

and in the right neighborhood of .

Suppose that for all . Then the function satisfies (5.2)

with and given by (5.11). From the general theory of the differential equations with singularity at infinity (see [18] Chapter 4, or [8]) follows that for a solution of (5.2) we have

and

when for some positive .

(This precise formula on asymptotic approximation for

and was proved in [3], using an

approach developed in [10]. Also a similar result was obtained in [9]). Thus for being a solution to (5.2), it holds

(5.15)

Obviously the right hand side of (5.15) is positive and less than . Really

is equivalent to

which is obvious. Thus there exists

such that for and for

. That is the switching at the point is from the maximal long position to a long

position which is less than the maximal possible.

The numerical computations are depicted in the graphs.

(The authors would like to thank Yuri Gribov for providing numerical

computations for the first two examples.)

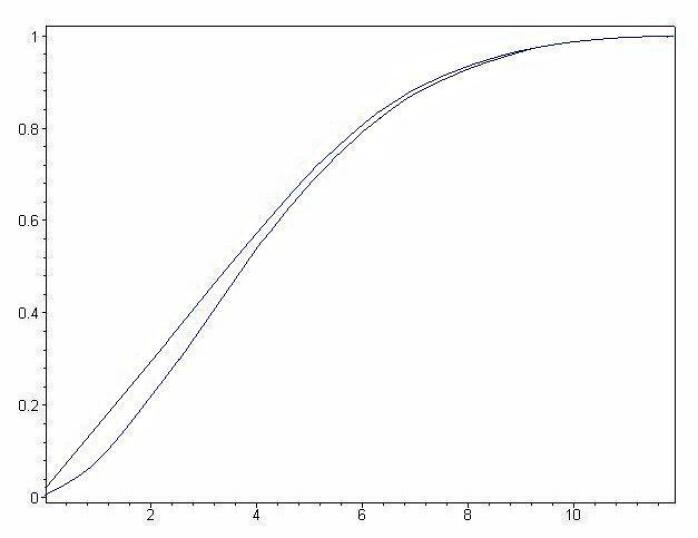

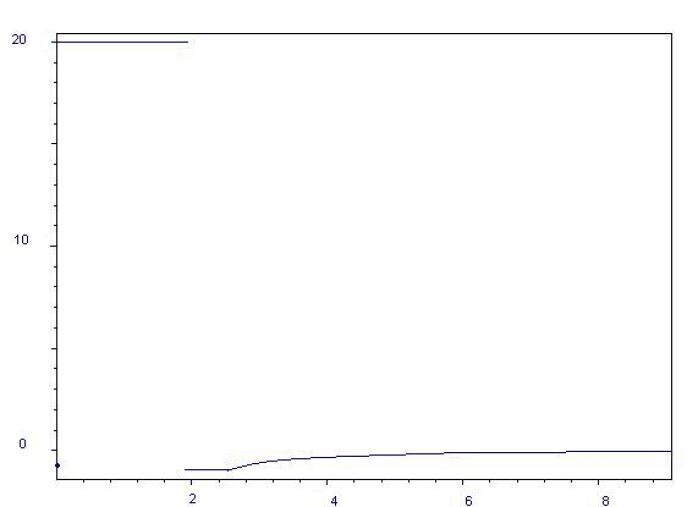

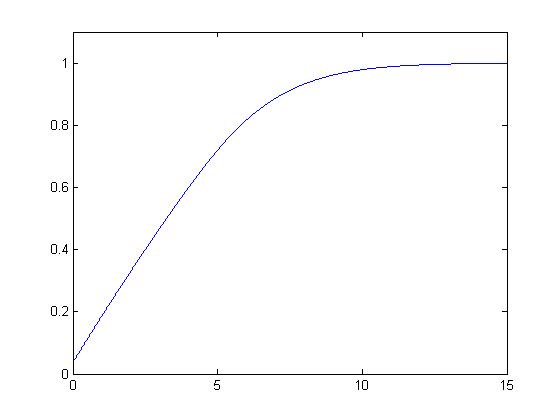

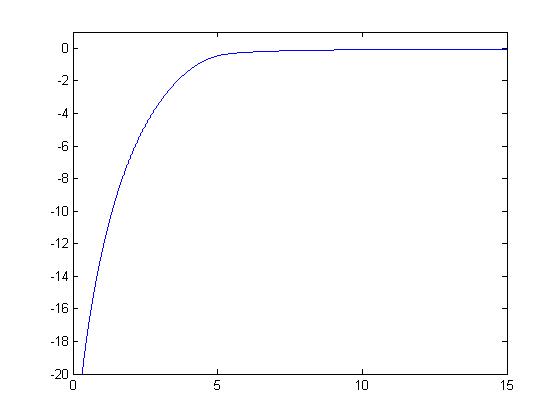

Figure 1. Example 1 - Maximal survival probability

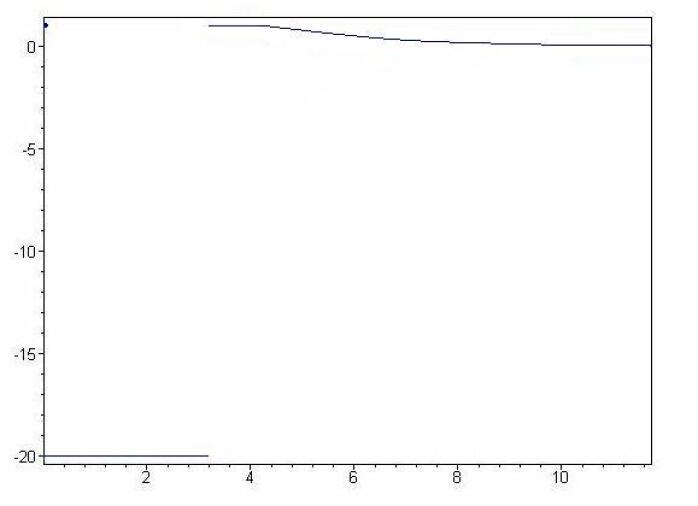

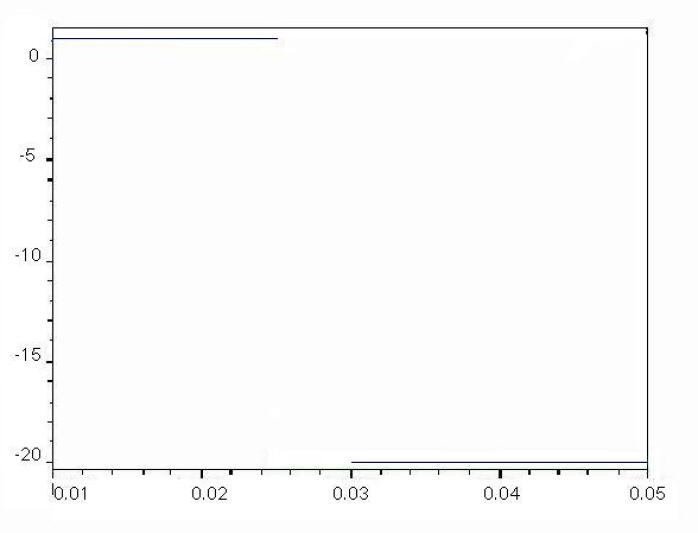

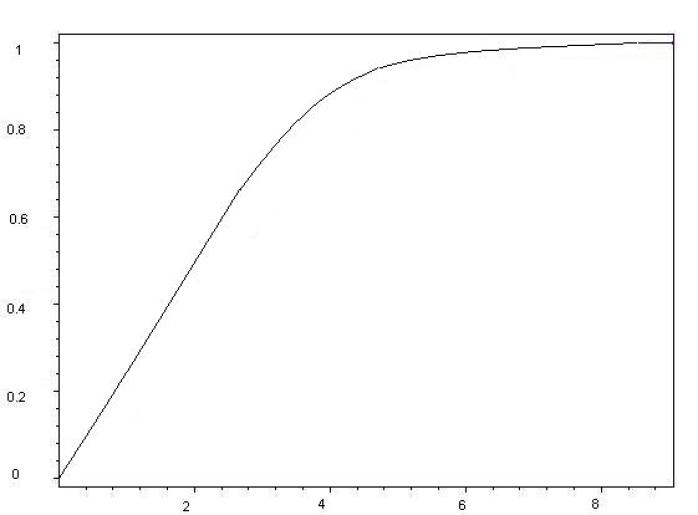

(The lower curve is for the no-borrowing-no-shortselling case)Figure 2. Example 1 - Optimal investment proportionFigure 3. Example 1 - Optimal investment proportion near zero surplusFigure 4. Example 2 - Maximal survival probabilityFigure 5. Example 2 - Optimal investment proportionFigure 6. Example 3 - Maximal Survival ProbabilityFigure 7. Example 3 - Optimal investment proportion

6. Economic Interpretation

As we can see from Lemma 3.1 and Lemma 3.2 in the neighborhood of 0, when the surplus level is low, the optimal policy is always to take position which brings the highest rate of return. If then it is optimal to borrow and to take the maximal long position, if

then the optimal policy requires to shortsell the risky asset and put into the risk-free asset the maximal allowable amount. In case and the optimal policy would require no

shortselling, maintaining at low levels maximal long position and then purchasing risky asset at the level less than the maximum possible so as to reduce the volatility of the portfolio. Like wise when and , only shortselling is needed, at first at the maximal possible level and then at the level lower than the maximal.

The nature of the optimal policy becomes less obvious, when the surplus level increases in the case when , while . Depending on the available actions (that is, depending on and ) we might have qualitatively completely different optimal policies. In this case, the nature of the optimal policy is the result of a rather nontrivial interplay between the rate of return and the volatility. As we saw in the example analyzed in Section 6, when the condition (5.1) is

satisfied and is much larger than , then at certain surplus levels we have to switch from the maximal long position, which was used at low surplus levels to the maximal short position, now “gambling” on the effect of a largest possible volatility which must increase the surplus level with higher probability than otherwise would be the case. At first glance this policy might appear counterintuitive, if one takes into account that for such a policy the rate of return is the lowest possible. When the surplus level increases even more, it becomes again optimal to stick to the highest possible rate of return; and with high surplus levels, it is optimal to have lower than the maximal possible rate of return, simultaneously having lower volatility. It is worth mentioning, that when is not much larger than a similar analysis show that the effect of switching to the short position is not observed, and no shortselling is optimal at any surplus levels; i.e., the set defined in (3.24) could be empty then.

A similar phenomenon can be observed when and . For certain values of the parameters, the optimal policy at low surplus levels would involve shortselling the risky asset so as to have the maximal rate of return for the resulting portfolio, while at higher surplus level we might observe a switch to the policy with the highest volatility, that is to the one with maximal long position in the risky asset even though that is the policy with the lowest return rate.

It is worth mentioning that none of those effects can be observed when we have either unconstrained case as in [6] or the no-borrowing-no-shortselling case of [2]. In [6] the ability to have unlimited large leverage enables one to adhere only to the policies without shortselling,

while in [2], the no-shortselling constraint does not allow to achieve sufficiently large volatility, of the portfolio, so as to reach higher levels with higher probability while having a lower rate of return.

References

[1]

[2] Azcue, P. and Muler, M.:

Optimal Investment Strategy to Minimize the Ruin Probability of an Insurance Company under Borrowing Constraints,

Insurance Math. Econom.44(1) 26–34, (2009)

[3] Belkina, T.A., Konyukhova N.B., Kurkina, A. O.: Optimal control of investments in dynamical insurance models: II. Cramer-Lundberg model with exponential claim size distribution (in Russian), Survey of the Industrial and Applied Mathematics 17, 3–24 (2010).

[4] Browne, S.:

Optimal investment policies for a firm with a random risk process: exponential utility and minimizing the probability of ruin,

Math. Ope. Res20(4), 937–958 (1995)

[5] Cont, R. and Tankov, P.:

Financial modelling with jumps processes,

Chapman & Hall/CRC, Boca Raton, (2004)

[6] Hipp, C. and Plum, M.:

Optimal investment for insurers,

Insurance Math. Econom.27, 215–228 (2000)

[7] Hipp, C. and Plum, M.:

Optimal investment for investors with state dependent income, and for insurers. Finance and Stochastics (3) 7, 299–321 (2003)

[9] Frolova, A., Kabanov, Y., and Pergamenshchikov S.: In the insurance

business risky investments are dangerous, Finance and Stochastics,

6, 227-235 (2002).

[10] Konyukhova, N.B.: Singular Cauchy problems

for systems of ordinary differential equations, U.S.S.R.

Comput. Maths. Math. Phys. , 23, 72–82 (1983).

[11] Konyukhova, N.B.: Singular Cauchy problems for some systems of nonlinear functional differential equations.

Differential Equations, 31, 1286-1293 (1995).

[12] Konyukhova, N.B.: Singular problems for systems of nonlinear functional differential equations. Int. Scientific Journal Spectral and Evolution Problems, 20, 199–214 (2010)

[13] Luo, S.:

Ruin minimization for insurers with borrowing constraints,

North American Actuarial Journal, 12 (2), 143 – 174 (2008)

[14] Promislow, S.D. and Young, V.:

Minimizing the probability of ruin when claims follow Brownian motion with drift,

North American Actuarial Journal9(3), 109–128 (2005)

[15] Schmidli, H.:

Optimal proportional reinsurance policies in a dynamic setting,

Scan. Actuarial J.1, 55–68 (2001)

[16] Schmidli, H.:

On minimizing the ruin probability by investment and reinsurance,

The Annals of Applied Probability12(3), 890–907 (2002)

[17] Taksar, M. and Markussen, C.:

Optimal dynamic reinsurance policies for large insurance portfolios,

Finance and Stochastics7 97–121 (2003)

[18] Wasow, W: Asymptotic Expansion for Ordinary Differential Equations. Dover, New York, 1987.

For and , there exists function

satisfying the following: on ; ;

and for

(6.4)

Appendix 2.

Now we prove Theorem 3.3.

For any , define . From Lemma 3.4,

we have . It holds by continuity.

Select such that .

Then it holds .

From Lemma 3.6, there exists a function

concave and twice continuously differentiable on that solves

on .

Now define

noticing and

for , we have

i.e., solves the HJB equation. By Lemma 3.5, we conclude

and

on . Since is the supremum, if , then we have

which contradicts . Thus it holds and we conclude that

equals in a neighborhood of and solves (3.22) with maximizer .

For any ,

we choose such that for all on ;

from Lemma 6.1, there exists such that

for and it solves on .

Hence we have and on .

Now define

it follows and

.

Thus solves HJB equation (3.7) on .

By Lemma 3.5, we conclude

and

on ; since is the supremum, if ,

then or .

This contradicts .

Hence we have . Thus is equal to and solves

(3.7) with maximizer on that contains .

Similarly one can show for any , in a neighborhood of ,

is equal to and solves (3.8) with maximizer .