Iterating Brownian motions, ad libitum

Abstract

Let be independent one-dimensional Brownian motions defined over the whole real line such that for every . We consider the th iterated Brownian motion . Although the sequences of processes do not converge in a functional sense, we prove that the finite-dimensional marginals converge. As a consequence, we deduce that the random occupation measures of converge towards a random probability measure . We then prove that almost surely has a continuous density which must be thought of as the local time process of the infinite iteration of independent Brownian motions.

Keywords and phrases. Brownian motion, Iterated Brownian motion, Harris chain, random measure, exchangeability, weak convergence, local time

AMS 2000 subject classifications. Primary 60J65,60J05; secondary 60G57,60E99

1 Introduction

Let and be independent standard one-dimensional Brownian motions starting from . The process if and if is called a two-sided Brownian motion. In this paper we study the iterations of independent (two-sided) Brownian motions. Formally, let be a sequence of independent two-sided Brownian motions and, for every and every , set

Burdzy [Bur93] studied sample path properties of the random function and coined the terminology of (second) “iterated Brownian motion” for this object. A motivation for this study is that iterated Brownian motion can be used to construct a solution to the 4-th order PDE ; see [Fun79]. This model has triggered a lot of work, see [Ber96, Bur93, BK95, BK95, ES99, KL99] and the references therein.

Another motivation is that the process is not a semimartingale (unless ). Indeed, for , a simple calculation shows that the quadratic variation of does not exist, but its quartic variation does. Similarly the –variation of is finite for . Hence, as increases, the process becomes wilder and wilder. Also, is self-similar with index , i.e.,

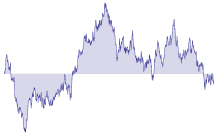

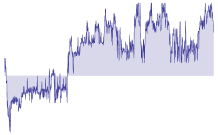

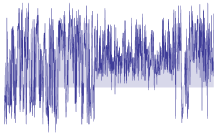

for all . See Fig. 1 for a comparison of sample paths of , . All these reasons make one suspect that convergence of the laws of the ’s in a “nice” function space (e.g., the space of continuous functions) is impossible (see Remark 1).

However, following the principle of Berman saying that wild functions must have smooth local times (see the nice survey [GH80]), we prove that the occupation measures of over converge in distribution towards a random measure which can be interpreted as the occupation measure of the infinite iteration “”. More precisely, let be the random probability measure defined by

| (1) |

for every Borel . Our main result is a limit theorem for the sequence . Restricting the integration to the unit interval is convenient and poses no loss of generality due to the self-similarity property of .

Let be the set of all positive Radon measures on . Although we focus on the real line, the interested reader should consult [Kal76] for the general theory of random measures. Endow with the topology of vague convergence, that is, the weakest topology which makes the mappings

continuous. (Here, is the set of continuous functions with compact support.) A random measure is a random element of the space , viewed as a measurable space with -algebra generated by the sets in . A sequence of random measures converges in distribution towards a random measure if for any bounded continuous mapping we have as . We write

to denote this notion. Convergence of to in distribution is equivalent to: , for any continuous (see Theorem 4.2 in [Kal76]). The latter convergence is convergence in distribution of real-valued random variables.

Theorem 1.

There exists a random measure such that . Moreover , a.s. The random probability measure almost surely admits a density with respect to the Lebesgue measure such that has compact support and is Hölder continuous with exponent for every .

We can think of as the occupation measure of the infinite iteration of i.i.d. Brownian motions. Thus the random function must be thought of as the local time of this infinite iteration. The convergence of the last theorem will be obtained by proving convergence of finite dimensional marginals of the iterated Brownian motions, namely:

Theorem 2.

For any integer , there exists a random vector such that for any pairwise distinct nonzero real numbers we have the following convergence in distribution

| (2) |

The random variables and the differences , , have all identical distribution which is that of a “signed exponential” with parameter , i.e. a distribution with density , .

The case has already been noticed in the Physics literature [Tur04] in the context of infinite iteration of i.i.d. random walks. We are unfortunately unable to give an explicit formula for the distribution of when , see Section 4 for a discussion and simulations of this intriguing probability distribution. It is quite interesting to observe that the marginals and differences have all the same distribution but are, of course, dependent. In a certain sense, the infinite iteration is both self-similar at all scales and long-range dependent.

The paper is organized as follows. The first section is devoted to the proof of Theorem 2 which is the cornerstone in the proof of Theorem 1. We then turn to the study of occupation measures in Section 2. The last section presents some open questions and comments.

Acknowledgments: We are deeply indebted to Yuval Peres for insightful discussions.

2 Finite dimensional marginals

In this section, we prove Theorem 2. The convergence of one-dimensional marginal is a special case because we can explicitly give its limiting distribution, which will be of great use throughout this paper. In the general case, the convergence of finite dimensional marginals comes from ergodic property of random iterations of independent Brownian motions.

2.1 One-dimensional marginals

Let . For , we denote by a signed exponential distribution with parameter , i.e., one which has density proportional to , .

Proposition 3.

For any we have the following convergence in distribution

| (3) |

Remark 1.

Proof.

By standard properties of Gaussian variables we have the following chain of equalities in distribution

where are i.i.d. standard normal variables and is a independent fair random sign. It is then easy to see that the modulus of the right hand side of the last display actually converges almost surely as . Indeed the series of is summable and an application of the Borel-Cantelli lemma proves the claim. Thus, if we set

we have the convergence in distribution as , where is fair random sign independent of . Notice that the limit does not depend on as long as . To identify the limit distribution, we note that satisfies the following recursive distributional equation

Iterating this equation and applying the same arguments as above, it is easy to see that it admits a unique fixed point as long as almost surely. Guided by the result of [Tur04], an easy computation shows that the exponential variable of density also satisfies (E) thus completing the proof of the proposition. ∎

2.2 General case

The goal of this section is to prove Theorem 2 in the case . The convergence (2) will be achieved by applying arguments from the theory of Harris chains. The idea is to consider the random transformation which associates with any points the images of these points under a two-sided Brownian motion and to show that independent applications of this map possess an ergodic property. That is, for any initial state , the distribution of converges weakly to a unique invariant probability measure.

Let . Denote by the set of -uplets of pairwise distinct nonzero real numbers. Note that if then its image under a two-sided Brownian motion almost surely belongs to .

Proposition 4.

For any , there is a unique probability measure on such that if is distributed according to and if is an independent two-sided Brownian motion then we have the equality in distribution

| (4) |

Furthermore, for any we have the following convergence in distribution

Notice that this argument does not give an explicit expression for the stationary probability measures but characterizes them uniquely by (4). Let be a fixed integer. Fix also a -uplet . For every we set

Thus the process is a Markov chain with state space , starting from , with transition probability kernel given by

for any and , where is a two-sided Brownian motion. We denote by the expectation of this chain started from . Since we restricted ourselves to , the chain is easily seen to be irreducible with respect to the -dimensional Lebesgue measure on and aperiodic. We will show that the chain is in fact positive Harris recurrent, which will imply that it admits a unique invariant probability measure, and Proposition 4 will directly flow from it, see [MT09, Theorem 13.0.1]. The key to prove this is to consider the following sets:

Definition 1.

Fix a (large) real number. We say that the -uplet is -sparse if we have

The set of all -sparse -uplets in is denoted by .

The basic observation is that if and are two -sparse -uplets and if is a two-sided Brownian motion then the two random -uplets and are mutually absolutely continuous with Radon-Nikodým derivative bounded from below by a positive constant depending on and only. The reason is that the ratio of the two densities is a continuous function on the compact set . In other words, there exists two (dependent) Brownian motions and such that with probability at least . Put it otherwise, if we fix , then

for all and all measurable . Thus Ney’s minorization condition holds and, therefore, the set is a petite set in the sense of [MT09, Chapter 5].

Proof of Proposition 4.

In order to prove that is positive Harris recurrent, we will show that, for some , the expected return time to the petite set , by the Markov chain started from , is bounded above by a finite constant, uniformly over all .

The technical tool that we use here is the so-called drift condition, see [MT09], for a Lyapunov or “potential” function . It is required that be unbounded on . The drift of such a function is defined by

Thus, is the generator of the Markov chain. We will show that there exists a Lyapunov function such that, for some ,

| (5) |

for every . More precisely, we show that the preceding condition is satisfied for the function defined by

and for some . In the last display, we use the notation to avoid extra terms in the definition of . It is convenient to consider the terms , and comprising , separately. For any ,

Letting , we thus have

where . For the other term, we have, with a standard normal variable,

where . Putting the terms together, we find

where . Thus, for all ,

If then . If then for some or for some . In the first instance, ; in the second instance, . So, for , we have , for all . Let . Then for , we have , implying that . Thus (5) holds. Theorem 13.0.1 in [MT09] now applies, showing positive Harris recurrence. This finishes the proof of the proposition. ∎

Remark 2.

The proof actually shows that there are constants such that

when , enabling one to establish a rate of convergence towards the stationary distribution. We shall not pursue this further herein.

2.3 Properties of the ’s

We can think of as a measure on the product space (by letting it have mass outside . The probability measures are consistent. This follows from the fact that is the limit in distribution of , whereas is the limit of , for any . Therefore is the projection of on the first coordinates. By Kolmogorov’s extension theorem, there is a probability measure on such that is obtained from by projecting on the first coordinates. The family has some further properties.

2.3.1 Exchangeability

The last statement of Proposition 4 actually shows that is exchangeable, that is, invariant under permutations of finitely many coordinates. Let be a random element of with law . By the classical de Finetti/Ryll-Nardzewski/Hewitt-Savage theorem (Theorem 11.10 [Kal02]) we know that there exists a random element of (random probability measure) , such that the law of conditionally on is a product measure (the law of i.i.d. random variables). The random measure will be identified and interpreted in the next section as the occupation measure of the infinitely iterated Brownian motion.

2.3.2 Stationarity of the increments

The family of measures also possesses another property which can be described as stationarity of the increments.

Proposition 5.

Let and let be distributed according to . Then for every we have

Proof.

Let . It is easy to prove by induction on and using elementary manipulation of the Gaussian distribution that the random vector has the same distribution as the vector . Notice that the vector , thus we can apply Proposition 4 and this finishes the proof of the proposition. ∎

3 Occupation measure of the infinitely iterated Brownian motion

3.1 Existence of

Recall the definition of the random measures given by formula (1) in the Introduction, as well as the notion of convergence in distribution of random elements of . With Theorem 2 in our hands, it is now easy to prove convergence in distribution of the random measures . We first need a lemma, characterizing convergence in distribution of random elements of , tailor-made for our case. The lemma can be of independent interest.

Lemma 6.

Let be random probability measures on . The following are equivalent:

-

(i)

The sequence converges in distribution to some random probability measure.

-

(ii)

For each , and conditionally on , let be i.i.d. real-valued random variables each with (conditional) law :

for all , and Borel sets . The random vector converges in distribution, as , to some probability measure on .

Proof.

The implication (i) (ii) is an easy consequence of [Kal76, Theorem 4.2]. For the other direction, fix . We will show that the random variable converges in distribution as . Consider the random probability measure

(i.e., the empirical distribution of ). We compare to . We have

by Chebyshev’s inequality. On the other hand, converges in distribution as . Hence converges in distribution, and thus converges in distribution to some random measure . It remains to prove that almost surely has mass one. Since converges in distribution, it follows that the sequence of random variables is tight. Thus for every there exists such that for every . Conditionally on we have . Taking expectation we deduce that for every . This is sufficient to apply Theorem 4.9 in [Kal86] and deduce that is almost surely a random probability measure. ∎

Let us go back to our setting and show that the occupation measures converge to a random probability measure . Let and, conditionally on , let be i.i.d. random variables with common distribution . We show that converges (unconditionally) towards the random vector of law identified in Proposition 4. Indeed, by the definition of , for any Borel bounded function we have, by Fubini’s theorem,

The last integral converges towards as because of Theorem 2 and dominated convergence. Applying Lemma 6 we get the existence of a random probability measure such that in distribution as .

3.2 Support of

Proposition 7.

Almost surely, the random probability measure has a bounded support.

In order to prove the last proposition we use a very general fact:

Lemma 8.

Let be a sequence of random probability measures converging in distribution towards a random probability measure . Suppose that the support of is contained in and that the sequences of random variables and are tight. Then has a compact support, almost surely.

Proof.

Let us argue by contradiction and suppose that has probability at least of having an unbounded support. By the assumption made on and there exists such that and for every . For the chosen above, there exists such that we have with probability at least . Now choose . Suppose that, conditionally on , the random variables are i.i.d. with common law . We then have

| (6) | |||||

On the other hand, if are i.i.d., conditionally on , we have

| (7) |

Since for fixed we have in distribution as , comparing (6) and (7) leads to a contradiction. ∎

We further establish a result on the limit of the oscillation of on an interval, as . Recall, that the oscillation of a function on an interval is defined by , and let, for ,

Lemma 9.

Let be the oscillation of a Brownian motion on a unit interval and let be i.i.d. copies of . Then, for all ,

Proof.

Let

Then , and

Thus iterating this equation, we get in the spirit of the proof of Proposition 3 the following equality in distribution

An argument similar to the one used in the proof of Proposition 3 shows that the right-hand side of the last display actually converges almost surely as , to the infinite product . Hence converges in distribution to the same random variable. ∎

Remark 3.

Roughly speaking, the oscillation of the infinitely iterated Brownian motion is the same, in distribution, over any interval of any length.

3.3 Density of

This section is devoted to the analysis of the properties of the density of . We will proceed in two steps. First, using standard technique of Fourier analysis for occupation densities (see e.g. [Ber69]), we will prove that almost surely has a density which is in . At the same time, we obtain some estimates about this Fourier transform. We will then use a very general result of Pitt [Pit78] on local times to prove that this density is in fact continuous and even Hölder continuous with exponent for every .

3.3.1 Harmonic analysis of

For , let

be the Fourier transform of the random probability measure .

Proposition 10.

For any we have

| (8) |

Proof.

By the definition of the Fourier transform , we have

By the convergences already established we have

where are two independent random variables uniformly distributed over and also independent of the sequence of Brownian motions . By stationarity of the increments (see the proof of Proposition 5), for any , we have in distribution, and thus,

Applying Proposition 3 and the dominated convergence theorem we get that

∎

In particular, applying Fubini’s theorem we deduce from (8) that

and thus that almost surely. By standard results on Fourier transforms, this implies that, almost surely, has density with respect to the Lebesgue measure which is in . Notice that the estimates (8) in fact give us a bit more than that, namely, for every we have

Applying the standard Sobolev inequality, we deduce that for every we have

where is a universal constant; see Theorem 1.38 in [BCD11]. Since can be arbitrarily close to and since is itself a density (thus a.s.) we get that for any almost surely.

3.3.2 Continuity of the density

The idea to prove continuity of the density is to apply once again a Brownian motion “on top of ” and to use the general theory developed in [Pit78]. Formally, if has density (which is in every ) we define the random measure by

where is an independent two-sided Brownian motion. Clearly, we have

(equality in distribution). So it suffices to show that has a continuous density. This follows from the lemma:

Lemma 11.

Let be the density of a probability measure supported on a compact interval such that for every . Let also be a two-sided Brownian motion and consider the occupation measure of with respect to the measure defined as follows

for any Borel positive function . Then the random measure almost surely has a density which is locally Hölder continuous of exponent for any .

Proof.

Let and choose such that where is defined by . Applying Hölder’s inequality we get that

We can thus apply Theorem 4 of [Pit78] and get that a continuous density over which satisfies a local Hölder condition , for any . ∎

4 Comments

Occupation over other measures.

In this work we considered the occupations measures of over the time interval but the proofs apply in the more general setting of occupation measures of over any probability measure on which is not atomic. More precisely if is a probability measure on which has no atom, we define the occupation of over by

for any Borel . Then the random probability measures converge towards in distribution as well.

Explicit finite dimensional marginals.

The consistent family distributions introduced in Proposition 4 are the limiting distributions of the finite-dimensional marginals of the ’s. They are characterized by (4). Although they arise naturally in the study of iteration of Brownian motions, to the best of our knowledge, they have not been investigated so far for and in particular no explicit formulae are known for the density of , .

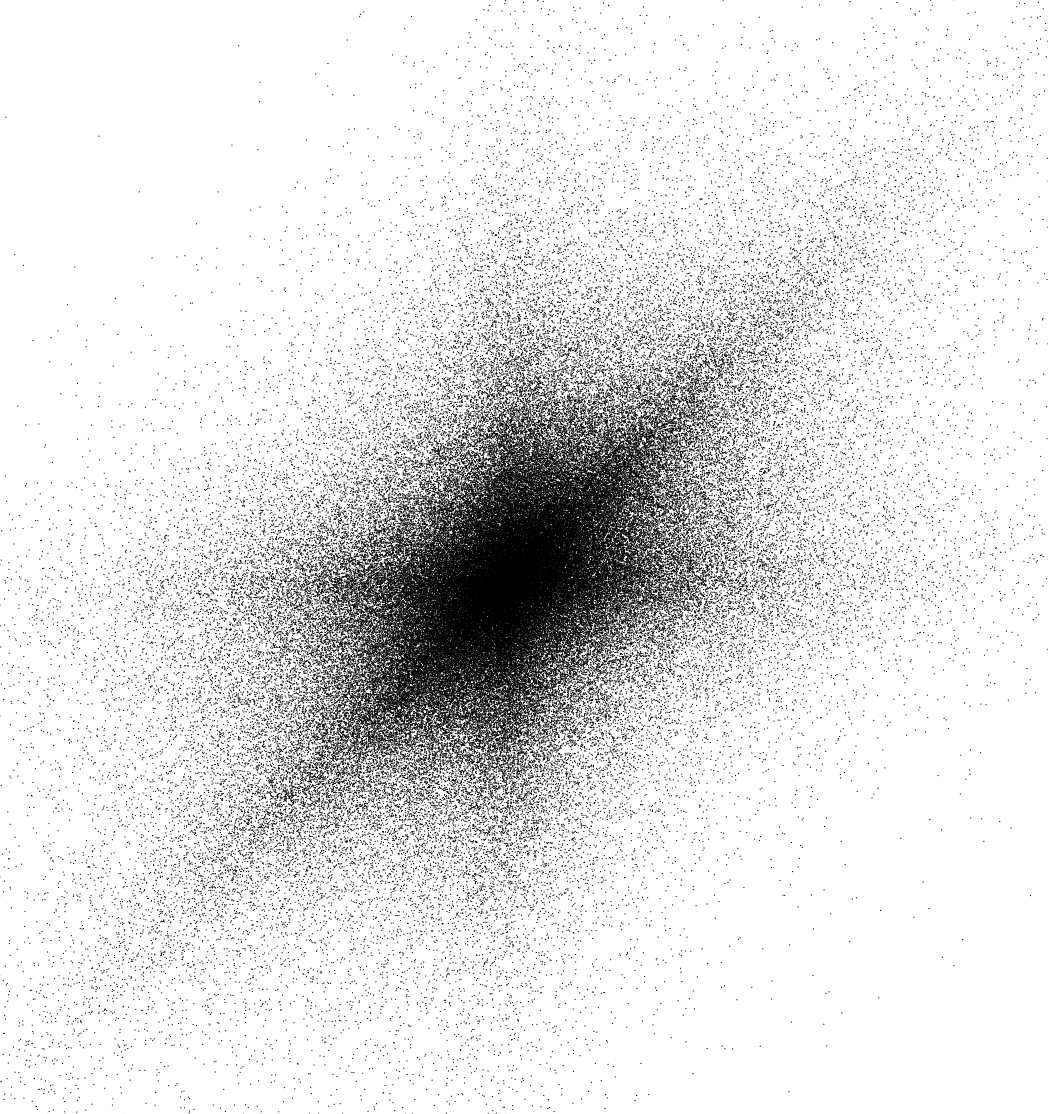

In Fig. 3 many independent points have been sampled according to . A clear shape “sea star” emerges and we conjecture that the level-lines of the density of would be dilatation of this unique shape. However we do not have any candidate for this density.

Funaki’s PDE.

Following Funaki [Fun79], we can show that solves the PDE , where , with initial data , , where is a function satisfying growth conditions [Fun79]. The solution is given by . Although it is probably not possible to give a PDE meaning to the exchangeable collection of random variables , we remark that the limit to the signed exponential translates into .

Ray-Knight theorem.

In the spirit of the famous Ray-Knight theorems, do we have another way to describe the density of as a diffusion process?

Reflected Brownian motion.

Fractional Brownian motion.

Fractional Brownian motion generalizes Brownian motion in that it is a Gaussian -self-similar process with stationary increments, where . Again, it is likely that Proposition 4 go through, but the limit is even harder to describe. Of course, this raises the following interesting question: what kind of processes can be iterated ad libitum and result into some kind of limit?

References

- [BCD11] Hajer Bahouri and Jean-Yves Chemin and Raphaël Danchin. Fourier analysis and nonlinear partial differential equations Springer, 2011.

- [Ber69] Simeon M. Berman. Harmonic analysis of local times and sample functions of Gaussian processes. Trans. Amer. Math. Soc., 143:269–281, 1969.

- [Ber96] Jean Bertoin. Iterated Brownian motion and stable subordinator. Statist. Probab. Lett., 27(2):111–114, 1996.

- [BK95] Krzysztof Burdzy and Davar Khoshnevisan. The level sets of iterated Brownian motion. In Séminaire de Probabilités, XXIX, volume 1613 of Lecture Notes in Math., pages 231–236. Springer, Berlin, 1995.

- [Bur93] Krzysztof Burdzy. Some path properties of iterated Brownian motion. In Seminar on Stochastic Processes, 1992 (Seattle, WA, 1992), volume 33 of Progr. Probab., pages 67–87. Birkhäuser Boston, Boston, MA, 1993.

- [ES99] Nathalie Eisenbaum and Zhan Shi. Uniform oscillations of the local time of iterated Brownian motion. Bernoulli, 5(1):49–65, 1999.

- [Fun79] Tadahisha Funaki. Probabilistic construction of the solution of some higher order parabolic differential equation[s]. Proc. Japan Acad., 55, Ser. A, 176–179, 1979.

- [GH80] Donald Geman and Joseph Horowitz. Occupation densities. Ann. Probab., 8(1):1–67, 1980.

- [Kal76] Olav Kallenberg. Random measures. Akademie-Verlag, Berlin, 1976.

- [Kal86] Olav Kallenberg. Random measures. Akademie-Verlag, Berlin, fourth edition, 1986.

- [Kal02] Olav Kallenberg. Foundations of Modern Probability. Springer-Verlag, New York, 2002.

- [KL99] Davar Khoshnevisan and Thomas M. Lewis. Iterated Brownian motion and its intrinsic skeletal structure. In Seminar on Stochastic Analysis, Random Fields and Applications (Ascona, 1996), volume 45 of Progr. Probab., pages 201–210. Birkhäuser, Basel, 1999.

- [MT09] Sean Meyn and Richard L. Tweedie. Markov chains and stochastic stability. Cambridge University Press, Cambridge, second edition, 2009. With a prologue by Peter W. Glynn.

- [Pit78] Loren D. Pitt. Local times for Gaussian vector fields. Indiana Univ. Math. J., 27(2):309–330, 1978.

- [Tur04] Loïc Turban. Iterated random walk. Europhys. Lett., 65(5):627–632, 2004.

| Nicolas Curien | Takis Konstantopoulos | |

| Département de Mathématiques et Applications | Department of Mathematics | |

| École Normale Supérieure, 45 rue d’Ulm | Uppsala University P.O. Box 480 | |

| 75230 Paris cedex 05, France | 751 06 Uppsala, Sweden | |

| nicolas.curien@ens.fr | takis@math.uu.se |