A Nonstochastic Information Theory

for Communication and State Estimation

Abstract

In communications, unknown variables are usually modelled as random variables, and concepts such as independence, entropy and information are defined in terms of the underlying probability distributions. In contrast, control theory often treats uncertainties and disturbances as bounded unknowns having no statistical structure. The area of networked control combines both fields, raising the question of whether it is possible to construct meaningful analogues of stochastic concepts such as independence, Markovness, entropy and information without assuming a probability space. This paper introduces a framework for doing so, leading to the construction of a maximin information functional for nonstochastic variables. It is shown that the largest maximin information rate through a memoryless, error-prone channel in this framework coincides with the block-coding zero-error capacity of the channel. Maximin information is then used to derive tight conditions for uniformly estimating the state of a linear time-invariant system over such a channel, paralleling recent results of Matveev and Savkin.

Index Terms:

Nonprobabilistic information theory, zero-error capacity, erroneous channel, state estimation.I INTRODUCTION

This paper has two motivations. The first arises out of the analysis of networked control systems [2], which combine the two different disciplines of communications and control. In communications systems, unknown quantities are usually modelled as random variables (rv’s), and central concepts such as independence, Markovness, entropy and Shannon information are defined stochastically. One reason for this is that they are generally prone to electronic circuit noise, which obeys physical laws yielding well-defined distributions. In addition, communication systems are often used many times, and in everyday applications each phone call and data byte may not be important. Consequently, the system designer need only ensure good performance in an average or expected sense - e.g. small bit error rates and large signal-to-noise average power ratios.

In contrast, control is often used in safety- or mission-critical applications where performance must be guaranteed every time a plant is used, not just on average. Furthermore, in plants that contain mechanical and chemical components, the dominant disturbances may not necessarily arise from circuit noise, and may not follow a well-defined probability distribution. Consequently, control theory often treats uncertainties and disturbances as bounded unknowns or signals without statistical structure. Networked control thus raises natural questions of whether it is possible to construct useful analogues of the stochastic concepts mentioned above, without assuming a probability space.

Such questions are not new and some answers are available. For instance, if an rv has known range but unknown distribution, then its uncertainty may be quantified by the logarithm of the cardinality or Lebesgue measure of this range. This leads to the notions of Hartley entropy [3] for discrete variables and Rényi differential 0th-order entropy [4] for continuous variables. A related construction is the -entropy, which is the log-cardinality of the smallest partition of a given metric space such that each partition set has diameter no greater than [5, 6, 7]. None of these concepts require any statistical structure.

Using these notions, nonstochastic measures of information can be constructed. For instance, in [8] the difference between the marginal and worst-case conditional Rényi entropies was taken to define a nonstochastic, asymmetric information functional, and used to study feedback control over errorless digital channels. In [9], information transmission was defined symmetrically as the difference between the sum of the marginal and the joint Hartley entropies of a pair of discrete variables. Continuous variables with convex ranges admitted a similar construction, but with replaced by a projection-based, isometry-invariant functional. Although both these definitions possess many natural properties, their wider operational relevance is unclear. This contrasts with Shannon’s theory, which is intimately connected to quantities of practical significance in engineering, such as the minimum and maximum bit-rates for reliable compression and transmission [10].

The second, seemingly unrelated motivation comes from the study of zero-error capacity [11, 12] in communications. The zero-error capacity of a stochastic discrete channel is the largest block-coding rate possible across it that ensures zero probability of decoding error. This is a more stringent concept than the (ordinary) capacity [10], defined to be the highest block-coding rate such that the probability of a decoding error is arbitrarily small. The famous channel coding theorem [10] states that the capacity of a stochastic, memoryless channel coincides with the highest rate of Shannon information across it, a purely intrinsic quantity. In [13], an analogous identity for was found in terms of the Shannon entropy of the ‘largest’ rv common to the channel input and output. However, it is known that does not depend on the values of the non-zero transition probabilities in the channel and can be defined without any reference to a probabilistic framework. This strongly suggests that should be expressible as the maximum rate of a suitably defined nonstochastic information index.

This paper has four main contributions. In section II, a formal framework for modelling nonstochastic uncertain variables (uv’s) is proposed, leading to analogues of probabilistic ideas such as independence and Markov chains. In section III, the concept of maximin information is introduced to quantify how much the uncertainty in one uv can be reduced by observing another. Two characterizations of are given here, and shown to be equivalent. In section IV, the notion of an error-prone, stationary memoryless channel is defined within the uv framework, and it is proved in Theorem IV.1 that the zero-error capacity of any such channel coincides with the largest possible rate of maximin information across it. Finally, it is shown in section V how can be used to find a tight condition (Theorem V.1) that describes whether or not the state of a noiseless linear time-invariant (LTI) system can be estimated with specified exponential uniform accuracy over an erroneous channel. A tight criterion for the achievability of uniformly bounded estimation errors is also derived for when uniformly bounded additive disturbances are present (Theorem V.2); a similar result was derived in [14], using probability arguments but no information theory. In a nonstochastic setting, maximin information thus serves to delineate the limits of reliable communication and LTI state estimation over error-prone channels.

II Uncertain Variables

The key idea in the framework proposed here is to keep the probabilistic convention of regarding an unknown variable as a mapping from some underlying sample space to a set of interest. For instance, in a dynamic system each sample may be identified with a particular combination of initial states and exogenous noise signals, and gives rise to a realization denoted by lower-case . Such a mapping is called an uncertain variable (uv). As in probability theory, the dependence on is usually suppressed for conciseness, so that a statement such as means . However, unlike probability theory, the formulation presented here assumes neither a family of measurable subsets of , nor a measure on them.

Given another uv taking values in , write

| (1) | |||||

| (2) | |||||

| (3) |

Call the marginal range of , its conditional range given (or range conditional on) , and , the joint range of and . With some abuse of notation, denote the family of conditional ranges (2) as

| (4) |

with empty sets omitted. In the absence of stochastic structure, the uncertainty associated with given all possible realizations of is described by the set-family . Notice that , i.e. is an -cover. In addition,

| (5) |

i.e. the joint range is fully determined by the conditional and marginal ranges in a manner that parallels the relationship between joint, conditional and marginal probability distributions.

Using this basic framework, a nonstochastic analogue of statistical independence can be defined:

Definition II.1 (Unrelatedness)

A collection of uncertain variables is said to be (unconditionally) unrelated if

They are said to be conditionally unrelated given (or unrelated conditional on) if

Like independence, unrelatedness has an alternative characterization in terms of conditioning:

Lemma II.1

Given uncertain variables ,

-

a)

are unrelated (Definition II.1) iff the conditional range

-

b)

are unrelated conditional on iff

Proof: Trivial.

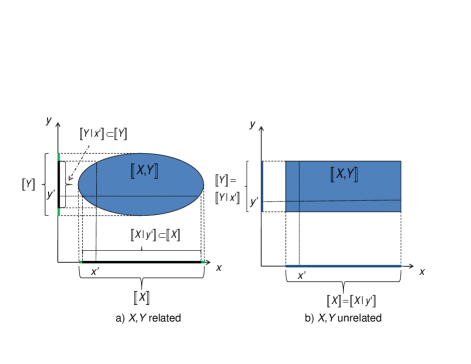

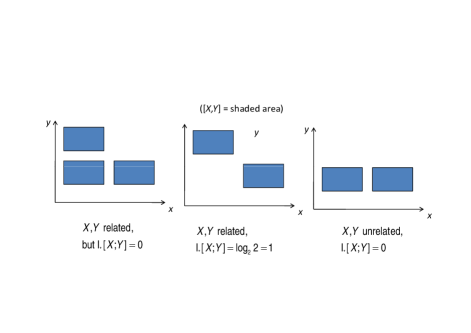

Example: Figure 1a) illustrates the case of two related uv’s and . Observe that the joint range is strictly contained in the Cartesian product of marginal ranges. In addition, for some values and , the conditional ranges and are strictly contained in the marginal ranges and , respectively.

In contrast, Figure 1b) depicts the ranges when and are unrelated. The joint range now coincides with , and and coincide with and respectively, for every and .

It is to see that for any uv’s ,

| (6) |

for all and . Equality is possible under extra hypotheses:

Lemma II.2

Let be uncertain variables s.t. are unrelated conditional on (Definition II.1). Then ,

| (7) |

Proof: See appendix A.

The second item in Lemma II.1 motivates the following definition:

Definition II.2 (Markov Uncertainty Chains)

The uncertain variables , and are said to form a Markov uncertainty chain if are unrelated conditional on (Definition II.1).

Remarks: By the symmetry of Definition II.1, is also a Markov uncertainty chain.

Before closing this section, it is noted that the framework developed above is not equivalent to treating input variables with known, bounded ranges as uniformly distributed rv’s. Such an approach is still probabilistic, and the output rv’s may have nonuniform distributions despite the uniform inputs. In contrast, in the uv model here, only the ranges are considered, and no distributions are derived at any stage.

For instance, consider an additive bounded noise channel with output , where the input and noise range on the interval . If and are taken to be mutually independent, uniform rv’s, then has a triangular distribution on , with small values of more probable than large ones. However, if and are treated as unrelated uv’s, then all that can be inferred about is that it has range , with all values in this range being equally possible.

Naturally, this lack of statistical structure does not suit all applications. However, as discussed in section I, such structure is often excess to requirements, e.g. in problems with worst-case objectives and bounded variables as in section V. A uv-based approach is arguably more natural in these settings.

III Maximin Information

The framework introduced above is now used to define a nonstochastic analogue of Shannon’s mutual information functional. Two characterizations of are developed and shown to be equivalent (Definition III.2 and Corollary III.1).

Throughout this section, are arbitrary uncertain variables (uv’s) with marginal ranges and (1), joint range (3), and conditional range family (4). Set cardinality is denoted by , with the value permitted, and all logarithms are to base 2.

III-A Previous Work

It is useful to first recall the nonprobabilistic formulations of entropy and information mentioned in section I. Though originally defined in different settings, for the sake of notational coherence they are discussed here using the uv framework of section II.

In loose terms, the entropy of a variable quantifies the prior uncertainty associated with it. For discrete-valued , this uncertainty may be captured by the (marginal) Hartley or 0-entropy

| (8) |

If has Lebesgue measure on , then the (marginal) Rényi differential 0-entropy is defined as

| (9) |

A related construction is the -entropy, which is the log-cardinality of the smallest partition of a given metric space such that each partition set has diameter no greater than [5]. None of these concepts require a probability space.

Two distinct notions of information have been proposed based on the 0-entropies above. In [8], a worst-case approach is taken to first define the (conditional) 0-entropy of given as

| (10) |

If every set in the family is -measurable on , then the (conditional) differential 0-entropy of given is

| (11) |

Noting that Shannon information can be expressed as the difference between the marginal and conditional entropies, a nonstochastic 0-information functional is then defined in [8] as

| (12) |

if is discrete-valued with , and as

| (13) |

if is continuous-valued with . In other words, the 0-information that can be gained about from is the worst-case log-ratio of the prior to posterior uncertainty set sizes.111Note that in 1965, Kolmogorov had defined as a ‘combinatorial’ conditional entropy and the log-ratio as a measure of information gain. However, these quantities have the defect of depending on the observed value , and thus are associated with a specific posterior uncertainty set . In contrast, (10)–(13) and (16) are functions of the family of all possible posterior uncertainty sets.

The definition above is inherently asymmetric, i.e. . A different and symmetric nonstochastic information index had been previously proposed in [9]. In that formulation, a conditional entropy was first defined as the difference between the joint and marginal Hartley entropies, in analogy with Shannon’s theory. The information transmission was then defined as the difference between the marginal and conditional entropies, yielding the symmetric formula

Continuous variables with convex ranges admitted a similar construction, with replaced not with but a projection-based, isometry-invariant functional.

Though these concepts are intuitively appealing and share some desirable properties with Shannon information, they have two weaknesses. Firstly, they do not treat continuous- and discrete-valued uv’s in a unified way. In particular, it is unclear how to apply the approach of [9] to mixed pairs of variables, e.g. a digital symbol encoding a continuous state, or to continuous variables with nonconvex ranges.

Secondly and more importantly, their operational relevance for problems involving communication has not been generally established. While the worst-case log-ratio approach of [8] has been used to find minimum bit rates for stabilization over an errorless digital channel, it is not obvious how to apply it if transmission errors occur.

For these reasons, an alternative approach is pursued in the remainder of this section.

III-B via the Overlap Partition

The nonstochastic information index proposed in this subsection quantifies the information that can be gained about from in terms of certain structural properties of the family of posterior uncertainty sets. These properties are described below:

Definition III.1 (Overlap Connectedness/Isolation)

-

a)

A pair of points and is called -overlap connected, denoted , if a finite sequence of conditional ranges such that , and each conditional range has nonempty intersection with its predecessor, i.e. , for each .

-

b)

A set is called -overlap connected if every pair of points in is overlap connected.

-

c)

A pair of sets is called -overlap isolated if no point in is overlap connected with any point in .

-

d)

An -overlap isolated partition (of ) is a partition of where every pair of distinct member-sets is overlap isolated.

-

e)

An -overlap partition is an overlap-isolated partition each member-set of which is overlap connected.

Remarks: For conciseness, the qualifier - will often dropped when there is no risk of confusion about the conditional range family of interest. Note that any point or set is automatically overlap connected with itself. In addition, lies in the same overlap partition set as iff .

Symmetry and transitivity guarantee that a unique overlap partition always exists:

Lemma III.1 (Unique Overlap Partition)

There is a unique -overlap partition of (Definition III.1), denoted . Every set is expressible as

| (14) |

Furthermore, every -overlap isolated partition of satisfies

| (15) |

with equality iff .

Proof: See appendix B.

Remarks: The self-referential identities in (14) are needed to prove certain key results later. The first equality says that each element of the overlap partition coincides with the set of all points that are overlap connected with it. The second states that every such is expressible as a union of elements of the set family .

Observe that from Definition III.1, overlap-isolated partitions are precisely those partitions of with the property that every conditional range lies entirely inside one member set . In other words, each possible observation unambiguously identifies exactly one partition set containing . Equivalently, these partition sets can be thought of as defining a discrete-valued function, or quantizer, on . The more sets there are in , the more distinct values this quantizer can take, and so the more refined the knowledge that can be unequivocally gained about .

By the result above, is precisely the overlap-isolated partition of maximum cardinality. This leads naturally to the definition below:

Definition III.2

The maximin information between and is defined as

| (16) |

where is the unique -overlap partition of (Lemma III.1).

Remarks: By the discussion above, represents the most refined knowledge that can be gained about from observations of . Note that this definition applies to both continuous- and discrete-valued uv’s. Also note that the self-information is identical to .

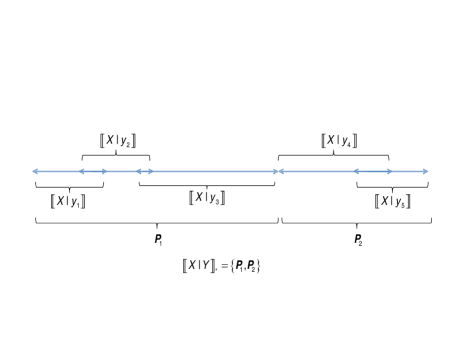

Example: Consider uv’s and with the one-dimensional conditional range family and overlap partition depicted in Figure 2. Observe that any pair of points in or in is overlap connected, and no point in is overlap connected to a point in . Also note that is the finest partition of having member sets that can always be unambiguously determined from ; a partition with larger cardinality would necessarily contain two or more neighbouring partition sets intersected by the same posterior set , and the observation would then correspond to either partition set. Thus the maximin information between and is bit.

It is easy to verify that .

Example: Let and be unrelated uv’s with and , and define the uv by if and if . The family consists of the sets and . The overlap partition has only one set, , so . However , since the largest cardinality of sets in is 2.

Finally, note that was originally defined in [1] as

where is the family of all finite subsets of ; hence the name ‘maximin’ information. This log-ratio characterization is close in spirit to (12)–(13) and can be shown to be equivalent to (16). However, since it does not have as simple an interpretation as (16) and is not needed for any of the results here, there will be no further discussion of it in what follows.

III-C via the Taxicab Partition

The definition of maximin information above is based purely on the conditional range family . As will not generally be the same, it may seem that could be asymmetric in its arguments. However, it turns out that can be reformulated symmetrically in terms of the joint range . A few additional concepts are needed in order to present this characterization.

Definition III.3 (Taxicab Connectedness/Isolation)

-

a)

A pair of points and is called taxicab connected if there is a taxicab sequence connecting them, i.e. a finite sequence of points in such that , and each point differs in at most one coordinate from its predecessor, i.e. and/or , for each .

-

b)

A set is called taxicab connected if every pair of points in is taxicab connected in .

-

c)

A pair of sets is called taxicab isolated if no point in is taxicab connected in to any point in .

-

d)

A taxicab-isolated partition (of ) is a cover of such that every pair of distinct sets in the cover is taxicab isolated.

-

e)

A taxicab partition (of ) is a taxicab-isolated partition of each member-set of which is taxicab connected.

Remarks: Note that any point or set is automatically taxicab connected with itself. In addition, taxicab connectedness/isolation in is identical to that in , with the order of elements in each pair reversed. Consequently, any taxicab-isolated partition of is in one-to-one correspondence with one of .

Taxicab-isolated partitions have the property that the particular member set that contains a given point is uniquely determined by and by alone. The argument is by contradiction: if is associated with two sets in the overlap-isolated partition, i.e. and for distinct , then and would be taxicab-connected by the sequence . In other words, the sets of a taxicab-isolated partition represent posterior knowledge that can always be agreed on by two agents who separately observe realizations of and .

Lemma III.2 (Taxicab- Overlap-Connectedness)

Thus any set is taxicab connected iff its -axis projection is overlap connected.

Proof: See appendix C.

Due to this equivalence between the two notions of connectedness, the same symbol is used. The result below makes another link:

Theorem III.1 (Unique Taxicab Partition)

In addition, every taxicab-isolated partition of satisfies

| (17) |

with equality iff .

Furthermore, a one-to-one correspondence from to the overlap partition (Lemma III.1) is obtained by projecting the sets of the former onto .

Proof: See appendix D.

The last statement of this theorem leads immediately to the following alternative characterization of maximin information:

Corollary III.1 ( via Taxicab Partition)

The maximin information (16) satisfies the identity

where is the unique taxicab partition of (Theorem III.1).

Thus .

Remarks: From the discussion following Definition III.3, the bound (17) means that represents the finest posterior knowledge that can be agreed on from individually observing and . The log-cardinality of this partition has considerable intuitive appeal as an index of information. Indeed, if and are discrete rv’s, then the elements of the taxicab partition correspond to the connected components of the bipartite graph that describes pairs with nonzero joint probability. In [13], the Shannon entropy of these connected components was called zero-error information and used to derive an intrinsic but stochastic characterization of the zero-error capacity of discrete memoryless channels. Maximin information corresponds rather to the Hartley entropy of these connected components. In section IV, it will be seen to yield an analogous nonstochastic characterization that is valid for discrete- or continuous-valued channels.

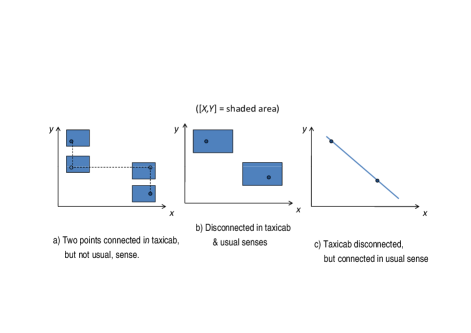

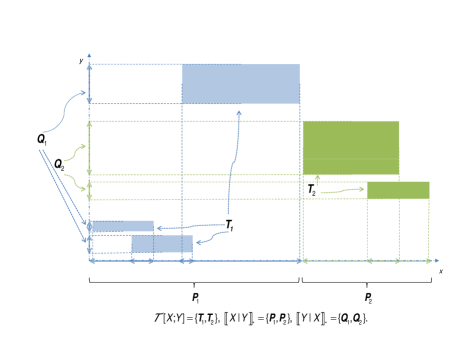

Example: The shaded regions in Figure 4 depict the joint range of uv’s having the conditional range family of Figure 2. The taxicab partition consists of the sets and ; it can be seen that every pair of points in each set is taxicab connected, and no point in one set is taxicab-connected with a point in the other. Projecting and onto yields and , the sets comprising the overlap partition . Similarly, consists of the projections and of and onto .

If two agents observe and separately, then they will always be able to agree on the index of the unique taxicab partition set that contains , since it is also the index of the overlap partition sets and that contain and respectively. The amount of information they share is then bit.

III-D Properties of Maximin Information

Two important properties of maximin information are now established. These properties are also exhibited by Shannon information and will be needed to prove Theorem V.1.

Lemma III.3 (More Data Can’t Hurt)

The maximin information (16) satisfies

| (18) |

Proof: By Definition III.1, every set is overlap connected in . As , is also overlap connected in . Pick a set that intersects . As is overlap connected in , it also . Thus , since by (14) must include all points . Consequently, there is only one for each .

Furthermore, since covers , every set of must intersect and thus include some of its set(s). Thus the map is a surjection from , implying that .

Lemma III.4 (Data Processing)

Proof: By Lemma III.3,

By Definition II.2, for every and , so . Substituting this into the RHS of the equation above and applying (16) again completes the proof.

Remark: By the symmetry of Markov uncertainty chains and maximin information, .

III-E Discussion

Maximin information is a more conservative index than Shannon information . For instance, Corollary III.1 implies that unrelated uv’s must share 0 maximin information, but the converse does not hold, unlike the analogous case with Shannon information. This is because is the largest cardinality of -partitions such that the unique partition set containing any realization can be determined by observing either or alone. Even if and are related, there may be no way to split the joint range into two or more sets that are each unambiguously identifiable in this way.

Example: Let . As = , and are related. However, every pair of points in is taxicab-connected, so has only one set, , and . See also Figure 5 for other examples.

This conservatism might suggest that could be derived from Shannon information via a variational principle, i.e. as

However, such an approach would be too conservative, since the infimum can be zero even when the maximin information is strictly positive. A formal proof of this is not given due to space constraints, but a sketch of the argument follows. Let be a (suitably well-behaved) joint probability density function (pdf) that is strictly positive on the Lebesgue measurable support of Figure 3(b) and that has finite Shannon information. Pick a point in the interior of the support and for any and sufficiently small , let be rv’s with joint pdf , where is a uniform pdf on a square of dimension centred at . Observe that if , the joint pdf becomes a unit delta function centred at , which automatically yields zero mutual information. As must vary continuously with , it follows that as . The nonnegativity of Shannon information then implies that the infimum above must be zero, but the maximin information remains 1.

IV Channels and Capacity

In this section, a connection is made between maximin information and the problem of transmission over an erroneous, discrete-time channel.

IV-A Stationary Memoryless Uncertain Channels

Let be the space of all -valued, discrete-time functions . An uncertain (discrete-time) signal is a mapping from the sample space to some function space of interest. Confining this mapping to any time yields an uncertain variable (uv), denoted . The signal segment is denoted . As with uv’s, the dependence on will not usually be indicated: thus the statements and mean that and respectively. Also note that here is a subset of the function space .

A nonstochastic parallel of the standard notion of a stationary memoryless channel in communications can be defined as follows:

Definition IV.1

Given an input function space and a set-valued transition function , a stationary memoryless uncertain channel maps any uncertain input signal with range to an uncertain output signal so that

| (20) | |||||

The set-valued reverse transition function of the channel is

| (21) |

Remarks: The set-valued map here plays the role of a time-invariant transition probability matrix or kernel in communications theory. The input function class is included to handle possible constraints such as limited time-averaged transmission power or input run-lengths, though in the rest of this paper is taken as .

The definition above implicitly assumes no feedback from the receiver back to the transmitter. If such feedback is present then by arguments similar to Massey’s [15], a more general definition must be used - see [16].

The following lemma shows that the conditional range of the input sequence given an output sequence is defined by the reverse transition function and the unconditional input range.

Lemma IV.1

Proof: See appendix E.

The largest information rate across a channel is formally defined as follows:

Definition IV.2

The peak maximin information rate of a stationary memoryless uncertain channel (Definition IV.1) is

| (23) |

where is the input function space and is the uncertain output signal yielded by the uncertain input signal .

It can be shown that the term under the supremum over time on the RHS is super-additive. A standard result called Fekete’s lemma then states that the supremum over time on the RHS of (23) is achieved in the limit as . This leads immediately to the following identity:

Lemma IV.2

IV-B Zero-Error Capacity

It is next shown how relates to the concept of zero-error capacity [11, 12], which Shannon introduced after its more famous sibling the (ordinary) capacity [10]. As described in section I, the zero-error capacity of a stochastic channel is defined as the largest average block-coding bit-rate at which input “messages” can be transmitted while ensuring that the probability of a decoding error is exactly zero (not just arbitrarily small, as with the usual capacity). It is well known that does not depend on the probabilistic nature of the channel, in the sense that the specific values of the nonzero transition probabilities play no role. This suggests that ought to be defineable using the nonstochastic framework of this paper.

To see this, observe that a length- zero-error block code may be represented as a finite set , where each codeword corresponds to a distinct “message”. The average coding rate is thus bits/sample, under the constraint that any received output sequence corresponds to at most one possible . In other words , a set of codewords is valid iff for each possible channel output sequence , . Thus the zero-error capacity may be defined operationally as

| (25) |

where the limit again follows from superadditivity and

| (26) | |||||

with the family of all finite subsets of and , the reverse block transition function (22).

The main result of this section shows that admits an intrinsic characterization in terms of maximin information theory:

Theorem IV.1 ( via Maximin Information)

Proof: As is a partition of ,

| (27) | |||||

| (28) | |||||

It is next shown that , a uv for which (27) is an equality. For any (26), let be a surjection from .222As in the mutual-information characterization of Shannon capacity, it is implicit that the underlying sample space is infinite, so that such a surjection always exists for each . Then no point in is overlap connected (Definition III.1) with any other, since at least one of the conditional ranges overlap-connecting them would then have 2 or more distinct points; this is impossible by (22) and (26). Thus the overlap partition (Lemma III.1) of is a family of singletons, comprising the individual points of .

If has a set of maximum cardinality, then choosing forces the LHS of (27) to coincide with the RHS. Otherwise, the RHS of (27) will be infinite and may be chosen to have arbitrarily large cardinality, again yielding equality in (27), by (16). This achieves equality in (28).

Remarks: This result shows that the largest average bit-rate that can be transmitted across a stationary memoryless uncertain channel with errorless decoding coincides with the largest average maximin information rate across it. This parallels Shannon’s channel coding theorem for stochastic memoryless channels and arguably makes more relevant for problems involving communication than other nonstochastic information indices.

It must be noted that ensuring exactly zero decoding errors is a stringent requirement and is impossible over many common channels, such as the the binary symmetric, binary erasure and additive white Gaussian noise channels, which have . However, a number of channels are known to possess nonzero , such as the pentagon and additive bounded noise channels. Zero-error capacity is also an object of study in graph theory, where it is related to the clique number. See [12] for a comprehensive survey of the literature on .

V State Estimation of Linear Systems over Erroneous Channels

In this section, maximin information is used to study the problem of estimating the states of a linear time-invariant (LTI) plant via a stationary memoryless uncertain channel (Definition IV.1), without channel feedback. First, some related prior work is discussed.

V-A Prior Work

In the case where the channel is an errorless digital bit-pipe, the state estimation problem is formally equivalent to feedback stabilization with control inputs known to both encoder and decoder. The central result in this scenario is the so-called “data rate theorem”, which states that the estimation error or plant state can be stabilized or taken to zero iff the sum of the log-magnitudes of the unstable eigenvalues of the system is less than the channel bit-rate. This condition holds in both deterministic and probabilistic settings, and under different notions of convergence or stability, e.g. uniform, th moment or almost surely (a.s.) [17, 18, 19, 20, 21, 22, 23]. See also [24] for recent work on quantized estimation of stochastic LTI systems.

However, if transmission errors occur, then the stabilizability and estimation conditions become highly dependent on the setting and objective, leading to a variety of different criteria. For instance, given a stochastic discrete memoryless channel (DMC) and a noiseless LTI system with random initial state, a.s. convergence of the state or estimation error to zero is possible if and (almost) only if the ordinary channel capacity ; this was proved for digital packet-drop channels with acknowledgements in [25], and for general DMC’s with or without channel feedback in [26]. The same result also holds for asymptotic stabilizability via an additive white Gaussian noise channel [27], with no channel feedback. See also [28] for bounds on mean-square-error convergence rates for state estimation over stochastic DMC’s, without channel feedback.

Suppose next that additive stochastic noise perturbs the plant and the objective is to bound the th moment of the states or estimation errors. Assuming channel feedback, bounded noise and scalar states, the achievability of this goal is determined by the anytime capacity of the channel [29]. Other related articles are [30, 31, 32] - the first two consider moment stabilization over errorless channels with randomly varying bit-rates known to both transmitter and receiver, and the last studies mean-square stabilization via DMC’s with no channel feedback. See also the recent papers [33, 34] for explicit constructions of error-correcting codes for control.

For the purposes of this section, the most relevant prior work is [14] (see also [35]), in which the channel is modelled as a stochastic DMC, and the plant is LTI with random initial state but is perturbed by additive nonstochastic bounded disturbances. It was shown that if channel feedback is absent, then a.s. uniformly bounded estimation errors are possible iff , the zero-error capacity [11] of the channel. However, under perfect channel feedback the necessary and sufficient condition becomes , the zero-error feedback capacity defined in [11]; the same criterion applies if the goal is to stabilize the plant states in the a.s. uniformly bounded sense, with or without channel feedback. As and are (often strictly) less than , both these conditions are more restrictive than for plants with stochastic or no process noise, even if the disturbance bound is arbitrarily small. In rough terms, the reason for the increased strictness is that nonstochastic disturbances do not enjoy a law of large numbers that averages them out in the long run. As a result it becomes crucial for no decoding errors to occur in the channel, not just for their average probability to be arbitrarily small. This important result was proved using probability theory, a law of large numbers and volume-partitioning arguments, but no information theory.

The scenarios considered in this section are similar to [14], with the chief difference being that that neither the initial state nor the erroneous channel are modelled stochastically here. As a consequence, probability and the law of large numbers cannot be employed in the analysis. Instead, maximin information is applied to yield necessary conditions that are then be shown to be tight (Thms. V.1 and V.2). Only state estimation without channel feedback is considered here, since the maximin-information theoretic analysis of systems with feedback is significantly different - see [16] for some preliminary results.

In what follows, denotes either the maximum norm on a finite-dimensional real vector space or the matrix norm it induces, and denotes the corresponding -ball centered at .

V-B Disturbance-Free LTI Systems

Consider an undisturbed linear time-invariant (LTI) system

| (29) | |||||

| (30) |

where the initial state is an uncertain variable (uv). The output signal is causally encoded via an operator as

| (31) |

Each symbol is then transmitted over a stationary memoryless uncertain channel with set-valued transition function and input function space (Definition IV.1), yielding a received symbol . Note that the encoder is told nothing about the values of these received symbols, i.e. there is no channel feedback. These symbols are used to produce a causal prediction of by means of another operator as

| (32) |

Let denote the prediction error.

The pair is called a coder-estimator. Such a pair is said to yield -exponential uniformly bounded errors if for any uv with range ,

| (33) |

where are specified parameters. If the stronger property

| (34) |

holds, then -exponential uniform convergence is said to be achieved.

Impose the following assumptions:

- DF1:

- DF2:

- DF3:

Remarks: Condition DF1 can be relaxed to requiring the observability of on the invariant subspace corresponding to eigenvalues greater than or equal to in magnitude. Assumption DF2 basically states that the channel outputs can depend on the initial state only via the channel inputs. Condition DF3 entails negligible loss of generality, since if were to exceed the largest plant eigenvalue magnitude , then the trivial estimator would achieve (34) and communication would not be needed.333The case introduces technicalities that can be handled by modifying to the arguments below; for the sake of conciseness it is not explicitly treated here.

The main result of this subsection is given below:

Theorem V.1

Consider the linear time-invariant system (29)–(30), with plant matrix , uncertain initial state and outputs that are coded and estimated (31)–(32) without channel feedback, via a stationary memoryless uncertain channel (Definition IV.1) with zero-error capacity (25). Let be the eigenvalues of and suppose that Assumptions DF1–DF3 hold.

If there exists a coder-estimator that yields -exponential uniformly bounded estimation errors (33) with respect to a nonempty -ball of initial states, then

| (35) |

V-B1 Proof of Necessity

The necessity of (35) is established first. Without loss of generality, let the state coordinates be chosen so that is in real Jordan canonical form (see e.g. [36], Theorem 3.4.5), i.e. it consists of square blocks on its diagonal, with the th block having either identical real eigenvalues or identical complex eigenvalues and conjugates for each . Let the blocks be ordered by descending eigenvalue magnitude. For any , let comprise those components of governed by the th real Jordan block , and let consist of the corresponding components of and , respectively.

Let denote the number of eigenvalues with magnitude , including repeats. Pick arbitrary and

| (36) |

and then divide the interval on the th axis into

| (37) |

equal subintervals of length , for each . Denote the midpoints of the subintervals so formed by , , and inside each subinterval construct an interval centred at but of shorter length . Define a hypercuboid family

| (38) |

and observe that any two hypercuboids are separated by a distance of along the th axis for each . Set the initial state range .

As ,

| (41) | |||||

where diam denotes set diameter under the maximum norm; (V-B1) holds since translating a set in a normed space does not change its diameter; denotes Euclidean norm; and denotes smallest singular value.

Now, an asymptotic identity of Yamamoto states that , where denotes smallest-magnitude eigenvalue (see e.g. [37], Thm 3.3.21). As there are only finitely many blocks , s.t.

| (42) |

In addition, for any region in a normed vector space,

| (43) | |||||

By (33), there then exists such that

| (44) | |||||

For some , the hypercuboid family (38) is an -overlap isolated partition (Definition III.1) of . To see this, suppose in contradiction that that is overlap connected in with another hypercuboid in . Then there would exist a set containing a point and a point in some . Thus , implying

| (45) | |||||

However, by construction any two hypercuboids are disjoint and separated by a distance of at least along the th axis for each . Thus if is the real Jordan block corresponding to some eigenvalue , , then

since all the eigenvalues of have equal magnitudes. The RHS of this would exceed the RHS of (45) when is sufficiently large that , yielding a contradiction.

As is an -overlap isolated partition of for sufficiently large ,

| (46) | |||||

| (47) |

where (46) follows from (36) and the inequality , for every . However, since is a Markov uncertainty-chain (Definition II.2),

Substituting this into the LHS of (47), taking logarithms, dividing by and then letting yields

As may be arbitrarily small, this establishes the necessity of (35).

V-B2 Proof of Sufficiency

The sufficiency of (35) is straightforward to establish. Define new state and measurement vectors and , for every . In these new coordinates, the system equations (29)–(30) become

| (48) | |||||

| (49) |

By (35) and (25), s.t. , a finite set with and

| (50) |

Down-sample (48)–(49) by to obtain the LTI system

| (51) | |||||

| (52) |

Now, distinct codewords can be transmitted over the channel and decoded without error once every samples. Furthermore sum of the unstable eigenvalue log-magnitudes of . By the “data rate theorem” (see e.g. [17]), there then exists a coder-estimator for the LTI down-sampled system (51)–(52) that estimates the states of (51) with errors tending uniformly to 0. For every , write for some and , and define an estimator

Then

as , and hence , tend to .

V-C LTI Systems with Disturbances

The results and techniques of the previous subsection can be readily adapted to analyze systems with disturbances. Suppose that, instead of (29)–(30), the plant state and output equations are

| (53) | |||||

| (54) |

where the uncertain signals and represent additive process and measurement noise. The objective is uniform boundedness, i.e. (33) with . Make the following assumptions:

- D1:

-

The plant dynamics (53) are strictly unstable, i.e. the matrix has spectral radius strictly larger than 1.

- D2:

-

The uncertain noise signals and are uniformly bounded, i.e. s.t. all possible signal realizations and have -norms .

- D3:

-

The zero sequence is a possible process and measurement noise realization, i.e. .

- D4:

-

The initial state , and are mutually unrelated (Definition II.1).

- D5:

The following result holds:

Theorem V.2

Consider a linear time-invariant plant (53)–(54), with plant matrix , uncertain initial state , and bounded uncertain signals and additively corrupting the dynamics and outputs respectively. Suppose the plant outputs are coded and estimated (31)–(32) without feedback via a stationary memoryless uncertain channel (Definition IV.1) having zero-error capacity (25), and assume conditions DF1 and D1–D5.

If there exists a coder-estimator (31)–(32) yielding uniformly bounded estimation errors with respect to a nonempty -ball of initial states, then

| (55) |

where are the eigenvalues of .

Conversely, if (55) holds as a strict inequality, then a coder-estimator can be constructed to yield uniform boundedness for any given -ball of initial states.

Proof: Necessity is straightforward. If a coder-estimator achieves uniform boundedness, then this uniform bound is not exceeded if the uncertain disturbances are realized as the zero signal, which by hypothesis is an element of both and . By unrelatedness , so the initial state range is unchanged. Furthermore, condition D5 implies , i.e. condition DF2. As uniform boundedness is just -exponential uniform boundedness with (33), Theorem V.1 applies immediately to yield (55).

The sufficiency of (55) is established next. By (55) and (25), s.t. , a finite set with and

| (56) |

Down-sample (53)–(54) by to obtain the LTI system

| (57) | |||||

| (58) |

where the accumulated noise term can be shown to be uniformly bounded over for each . Now, distinct codewords can be transmitted over the channel and decoded without error once every samples. Furthermore sum of the unstable eigenvalue log-magnitudes of . By the “data rate theorem” for LTI systems with bounded disturbances controlled or estimated over errorless channels, (see e.g. [17, 21, 19]), there then exists a coder-estimator for the LTI down-sampled system (53)–(54) that estimates its states with errors uniformly bounded over .

For every , write for some and , and define an estimator

Then

As the RHS is uniformly bounded over , the proof is complete.

V-D Discussion

Like the results of Matveev and Savkin [14] on LTI state estimation via an erroneous channel without feedback, Thms. V.1 and V.2 involve the zero-error capacity of the channel. In their formulation, the process and measurement noise are treated as bounded unknown deterministic signals, but the channel and initial state are modelled probabilistically. The estimation objective is to achieve estimation errors that, with probability (w.p.) 1, are uniformly bounded over all admissible disturbances, and the necessity part of their result was proved with the aid of a law of large numbers.

The main aims of this section have been to demonstrate firstly, that statistical assumptions are not necessary to capture the essence of this problem (modulo zero-probability events); and secondly, that even with no probabilistic structure to exploit, information-theoretic techniques can be successfully applied, based on . Although the channel and initial state here are modelled nonstochastically and, furthermore, the estimation errors are to be bounded uniformly over all samples , not just w.p.1, the achievability criterion (55) of subsection V-C essentially recovers the earlier result.444The only difference is that the necessary condition here is not a strict inequality as in the earlier result, because the proof technique here relies on nulling the disturbances. A lengthier analysis that explicitly considers process noise effects would elicit a strict inequality; due to space constraints this is omitted.

In addition, unlike [14] and Theorem V.2, Theorem V.1 assumes no disturbances and concerns performance as measured by a specific convergence rate, not just bounded errors. The criterion (35) agrees with [14] when , but is more (less) stringent when . It applies when, for instance, the states of a possibly stable noiseless LTI plant are to be remotely estimated with errors decaying at or faster than a specified speed .

VI Conclusion

In this paper a formal framework for modelling nonstochastic variables was proposed, leading to analogues of probabilistic ideas such as independence and Markov chains. Using this framework, the concept of maximin information was introduced, and it was proved that the zero-error capacity of a stationary memoryless uncertain channel coincides with the highest rate of maximin information across it. Finally, maximin information was applied to the problem of reconstructing the states of a linear time-invariant (LTI) system via such a channel. Tight criteria involving were found for the achievability of uniformly bounded and uniformly exponentially converging estimation errors, without any statistical assumptions.

An open question is whether maximin information can be used in the presence of feedback. Two challenges present themselves. Firstly, the equivalence between the problems of state estimation and control in the errorless case is lost if channel errors occur, because the encoder does not necessarily know what the decoder received. Secondly, from [14, 35] it is known that for both the problems of LTI state estimation with channel feedback and LTI control, the relevant channel figure-of-merit for achieving a.s. bounded estimation errors or states respectively is its zero-error feedback capacity , which can be strictly larger than [11].

These issues suggest that nontrivial modifications of the techniques presented here may be required to study feedback systems. Preliminary results concerning this problem are presented in the conference paper [16].

Acknowledgements

The author acknowledges the helpful suggestions of the anonymous reviewers.

References

- [1] G. N. Nair, “A non-stochastic information theory for communication and state estimation over erroneous channels,” in Proc. 9th IEEE Int. Conf. Contr. Automation, Santiago, Chile, 2011, pp. 159–64.

- [2] P. Antsaklis and J. Baillieul, Eds., Special Issue on Networked Control Systems, in IEEE Trans. Automat. Contr. IEEE, Sep. 2004, vol. 49.

- [3] R. V. L. Hartley, “Transmission of information,” Bell Syst. Tech. Jour., vol. 7, no. 3, pp. 535–63, 1928.

- [4] A. Renyi, “On measures of entropy and information,” in Proc. 4th Berkeley Symp. Maths., Stats. and Prob., Berkeley, USA, 1960, pp. 547–61.

- [5] A. N. Kolmogorov and V. M. Tikhomirov, “-Entropy and -capacity,” Uspekhi Mat., vol. 14, pp. 3–86, 1959, Eng. translation Amer. Math. Soc. Trans., ser. 2, vol. 17, pp. 277–364.

- [6] D. Jagerman, “-Entropy and approximation of band-limited functions,” SIAM J. App. Maths, vol. 17, no. 2, pp. 362–77, 1969.

- [7] D. Donoho, “Counting bits with Kolmogorov and Shannon,” Stanford Uni., USA, Tech. Rep. 2000-38, 2000.

- [8] H. Shingin and Y. Ohta, “Disturbance rejection with information constraints: Performance limitations of a scalar system for bounded and Gaussian disturbances,” Automatica, vol. 48, no. 6, pp. 1111–1116, 2012.

- [9] G. J. Klir, Uncertainty and Information Foundations of Generalized Information Theory. Wiley, 2006, ch. 2.

- [10] C. E. Shannon, “A mathematical theory of communication,” Bell Syst. Tech. Jour., vol. 27, pp. 379–423, 623–56, 1948, reprinted in ‘Claude Elwood Shannon Collected Papers’, IEEE Press, 1993.

- [11] ——, “The zero-error capacity of a noisy channel,” IRE Trans. Info. Theory, vol. 2, pp. 8–19, 1956.

- [12] J. Korner and A. Orlitsky, “Zero-error information theory,” IEEE Trans. Info. Theory, vol. 44, pp. 2207–29, 1998.

- [13] S. Wolf and J. Wullschleger, “Zero-error information and applications in cryptography,” in Proc. IEEE Info. Theory Workshop, San Antonio, USA, 2004, pp. 1–6.

- [14] A. S. Matveev and A. V. Savkin, “Shannon zero error capacity in the problems of state estimation and stabilization via noisy communication channels,” Int. Jour. Contr., vol. 80, pp. 241–55, 2007.

- [15] J. L. Massey, “Causality, feedback and directed information,” in Proc. Int. Symp. Inf. Theory App., Nov. 1990, pp. 1–6, full preprint downloaded from http://csc.ucdavis.edu/r̃gjames/static/pdfs/.

- [16] G. N. Nair, “A nonstochastic information theory for feedback,” in Proc. IEEE Conf. Decision and Control, Maui, USA, 2012, pp. 1343–48.

- [17] W. S. Wong and R. W. Brockett, “Systems with finite communication bandwidth constraints I,” IEEE Trans. Autom. Contr., vol. 42, pp. 1294–9, 1997.

- [18] ——, “Systems with finite communication bandwidth constraints II: stabilization with limited information feedback,” IEEE Trans. Autom. Contr., vol. 44, pp. 1049–53, 1999.

- [19] J. Hespanha, A. Ortega, and L. Vasudevan, “Towards the control of linear systems with minimum bit-rate,” in Proc. 15th Int. Symp. Math. The. Netw. Sys. (MTNS), U. Notre Dame, USA, Aug 2002.

- [20] J. Baillieul, “Feedback designs in information-based control,” in Stochastic Theory and Control. Proceedings of a Workshop held in Lawrence, Kansas, B. Pasik-Duncan, Ed. Springer, 2002, pp. 35–57.

- [21] S. Tatikonda and S. Mitter, “Control under communication constraints,” IEEE Trans. Autom. Contr., vol. 49, no. 7, pp. 1056–68, July 2004.

- [22] G. N. Nair and R. J. Evans, “Stabilizability of stochastic linear systems with finite feedback data rates,” SIAM J. Contr. Optim., vol. 43, no. 2, pp. 413–36, July 2004.

- [23] ——, “Exponential stabilisability of finite-dimensional linear systems with limited data rates,” Automatica, vol. 39, pp. 585–93, Apr. 2003.

- [24] K. You and L. Xie, “Quantized Kalman filtering of linear stochastic systems,” in Kalman Filtering. Nova Publishers, 2011, pp. 269–88.

- [25] S. Tatikonda and S. Mitter, “Control over noisy channels,” IEEE Trans. Autom. Contr., vol. 49, no. 7, pp. 1196–201, July 2004.

- [26] A. S. Matveev and A. V. Savkin, “An analogue of Shannon information theory for detection and stabilization via noisy discrete communication channels,” SIAM J. Contr. Optim., vol. 46, no. 4, pp. 1323–67, 2007.

- [27] J. H. Braslavsky, R. H. Middleton, and J. S. Freudenberg, “Feedback stabilization over signal-to-noise ratio constrained channels,” IEEE Trans. Autom. Contr., vol. 52, no. 8, pp. 1391–403, 2007.

- [28] G. Como, F. Fagnani, and S. Zampieri, “Anytime reliable transmission of real-valued information through digital noisy channels,” SIAM J. Contr. Optim., vol. 48, no. 6, pp. 3903–24, 2010.

- [29] A. Sahai and S. Mitter, “The necessity and sufficiency of anytime capacity for stabilization of a linear system over a noisy communication link part 1: scalar systems,” IEEE Trans. Info. Theory, vol. 52, no. 8, pp. 3369–95, 2006.

- [30] N. C. Martins, M. A. Dahleh, and N. Elia, “Feedback stabilization of uncertain systems in the presence of a direct link,” IEEE Trans. Autom. Contr., vol. 51, no. 3, pp. 438–47, 2006.

- [31] P. Minero, M. Franceschetti, S. Dey, and G. N. Nair, “Data rate theorem for stabilization over time-varying feedback channels,” IEEE Trans. Autom. Contr., vol. 54, no. 2, pp. 243–55, 2009.

- [32] S. Yuksel and T. Basar, “Control over noisy forward and reverse channels,” IEEE Trans. Autom. Contr., vol. 56, no. 5, pp. 1014–29, 2011.

- [33] R. Ostrovsky, Y. Rabani, and L. J. Schulman, “Error-correcting codes for automatic control,” IEEE Trans. Info. Theory, vol. 55, no. 7, pp. 2931–41, 2009.

- [34] R. T. Sukhavasi and B. Hassibi, “Error correcting codes for distributed control,” preprint, available at http://arxiv.org, no. 1112.4236v2, 25 Feb. 2012.

- [35] A. S. Matveev and A. V. Savkin, Estimation and Control over Communication Networks. Birkhauser, 2008.

- [36] R. A. Horn and C. R. Johnson, Matrix Analysis. Cambridge University Press, 1985.

- [37] ——, Topics in Matrix Analysis. Cambridge University Press, 1991.

Appendix A Proof of Lemma II.2

Appendix B Proof of Lemma III.1 (Unique Overlap Partition)

The first step is to establish the existence of an overlap partition. For any , let be the set of all points in with which is overlap connected. Obviously is an -cover. Any two points in are overlap connected, since they are both overlap connected with . Furthermore, if any two sets and have some point in common, then they must coincide, since and imply that . Moreover, if and are distinct, hence disjoint, then they are overlap isolated; otherwise some point would be overlap connected with both and and thus lie in , which is impossible. Thus the family is an overlap partition.

To prove that it is unique, let be any overlap partition. Then every set in must be contained in , for each . However, must also be included in . Otherwise there would be a point outside that is overlap connected with ; this would have to lie in some set , impossible since must be overlap isolated from . Thus for each , and so .

To establish (14), for any let . As each element of consists of all the points it is overlap connected with, it follows that , for each . Furthermore and are overlap isolated and thus have null intersection, for every . Thus

To prove (15), observe that every set intersects exactly one set , i.e. . Otherwise, would also overlap some other set in the partition ; since is overlap-connected, this would imply that there is a point in and one in that are overlap-connected, which is impossible since is an overlap-isolated partition. Furthermore, since is a cover of , every set in must intersect some set in it. Thus is a surjection from and so .

To prove the equality condition, observe that ,

If , then is a bijection from , and so the union above can only run over one set . Consequently , i.e. the bijection from is an identity.

Appendix C Proof of Lemma III.2

With regard to the first statement, note that if are taxicab connected, then there is a taxicab sequence

of points in . This yields a sequence of conditional ranges s.t. for each , with and . Thus .

To prove the reverse implication, suppose that and pick any and . Then a sequence of conditional ranges s.t. , for each , where and . For every pick an . Then the taxicab sequence

comprises points in . Thus are taxicab connected in .

To prove the forward implication of the 2nd statement, note that if any is taxicab connected with any , then are overlap connected. Similarly, if every are overlap connected then for each and , is taxicab connected with . The statement then follows by noting that .

The 3rd statement ensues similarly. If every is taxicab disconnected from any , then every is overlap disconnected from any .

Similarly, if every is overlap disconnected from any , then and , is taxicab disconnected from . The proof is completed by noting that and .

Appendix D Proof of Theorem III.1 (Unique Taxicab Partition)

For any set in the unique overlap partition , define and the cover of .

By Lemma III.2, the sets of are individually taxicab connected and mutually taxicab isolated, so is a taxicab partition.

To establish uniqueness, note that if is any taxicab partition, then by the same token its projection is an overlap partition, which by uniqueness must coincide with . Thus ,

i.e. every set in is inside a single set in . As and are partitions of , it follows then that must coincide exactly with an element of .

To prove (17), first observe that every set intersects exactly one set , i.e. . Otherwise, would also intersect some other set in the partition ; since is taxicab-connected, this would imply that there is a point in and one in that are taxicab-connected, which is impossible since is a taxicab-isolated partition. Furthermore, since is a cover, every set in must intersect some set in it. Thus is a surjection from and so .

Appendix E Proof of Lemma IV.1

Pick any . As for each , it follows that . Moreover , thus establishing that the LHS of (22) is contained in the RHS.

It is now shown that the RHS is contained in the LHS, proving equality. If the RHS is empty then so is the LHS, by the preceding argument, yielding the desired equality. If the RHS is not empty, pick an arbitrary element in it, i.e. and , for each . By (21), for each , or equivalently . Thus s.t. and . This implies that . Thus the RHS of (22) is contained in the LHS, completing the proof.