Automatic Relevance Determination in Nonnegative Matrix Factorization with the -Divergence

Abstract

This paper addresses the estimation of the latent dimensionality in nonnegative matrix factorization (NMF) with the -divergence. The -divergence is a family of cost functions that includes the squared Euclidean distance, Kullback-Leibler and Itakura-Saito divergences as special cases. Learning the model order is important as it is necessary to strike the right balance between data fidelity and overfitting. We propose a Bayesian model based on automatic relevance determination in which the columns of the dictionary matrix and the rows of the activation matrix are tied together through a common scale parameter in their prior. A family of majorization-minimization algorithms is proposed for maximum a posteriori (MAP) estimation. A subset of scale parameters is driven to a small lower bound in the course of inference, with the effect of pruning the corresponding spurious components. We demonstrate the efficacy and robustness of our algorithms by performing extensive experiments on synthetic data, the swimmer dataset, a music decomposition example and a stock price prediction task.

Index Terms:

Nonnegative matrix factorization, Model order selection, Majorization-minimization, Group-sparsity.1 Introduction

Given a data matrix of dimensions with nonnegative entries, nonnegative matrix factorization (NMF) consists in finding a low-rank factorization

| (1) |

where and are nonnegative matrices of dimensions and , respectively. The common dimension is usually chosen such that , hence the overall number of parameters to describe the data (i.e., data dimension) is reduced. Early references on NMF include the work of Paatero and Tapper [1] and a seminal contribution by Lee and Seung [2]. Since then, NMF has become a widely-used technique for non-subtractive, parts-based representation of nonnegative data. There are numerous applications of NMF in diverse fields, such as audio signal processing [3], image classification [4], analysis of financial data [5], and bioinformatics [6]. The factorization (1) is usually sought after through the minimization problem

| (2) |

where means that all entries of the matrix are nonnegative (and not positive semidefiniteness). The function is a separable measure of fit, i.e.,

| (3) |

where is a scalar cost function of given ; and it equals zero when . In this paper, we will consider the to be the -divergence, a family of cost functions parametrized by a single scalar . The squared Euclidean (EUC) distance, the generalized Kullback-Leibler (KL) divergence and the Itakura-Saito (IS) divergence are special cases of the -divergence. NMF with the -divergence (or, in short, -NMF) was first considered by Cichocki et al. in [7], and more detailed treatments have been proposed in [8, 9, 10].

1.1 Main Contributions

In most applications, it is crucial that the “right” model order is selected. If is too small, the data does not fit the model well. Conversely, if too large, overfitting occurs. We seek to find an elegant solution for this dichotomy between data fidelity and overfitting. Traditional model selection techniques such as the Bayesian information criterion (BIC) [11] are not applicable in our setting as the number of parameters is and this scales linearly with the number of data points , whereas BIC assumes that the number of parameters stays constant as the number of data points increases.

To ameliorate this problem, we propose a Bayesian model for -NMF based on automatic relevance determination (ARD) [12], and in particular, we are inspired by Bayesian PCA (Principal Component Analysis) [13]. We derive computationally efficient algorithms with monotonicity guarantees to estimate the model order and to estimate the basis and the activation coefficients . The proposed algorithms are based on the use of auxiliary functions (local majorizations of the objective function). The optimization of these auxiliary functions leads directly to majorization-minimization (MM) algorithms, resulting in efficient multiplicative updates. The monotonicity of the objective function can be proven by leveraging on techniques in [9]. We show via simulations in Section 6 on synthetic data and real datasets (such as a music decomposition example) that the proposed algorithms recover the correct model order and produce better decompositions. We also describe a procedure based on the method of moments for adaptive and data-dependent selection of some of the hyperparameters.

1.2 Prior Work

To the best of our knowledge, there is fairly limited literature on model order selection in NMF. References [14] and [15] describe Markov chain Monte Carlo (MCMC) strategies for evaluation of the model evidence in EUC-NMF or KL-NMF. The evidence is calculated for each candidate value of , and the model with highest evidence is selected. References [16, 17] describe reversible jump MCMC approaches that allow to sample the model order , along with any other parameter. These sampling-based methods are computationally intensive. Another class of methods, given in references [18, 19, 20, 21], is closer to the principles that underlie this work; in these works the number of components is set to a large value and irrelevant components in and are driven to zero during inference. A detailed but qualitative comparison between our work and these methods is given in Section 5. In Section 6, we compare the empirical performance of our methods to [18] and [21].

This paper is a significant extension of the authors’ conference publication in [22]. Firstly, the cost function in [22] was restricted to be the KL-divergence. In this paper, we consider a continuum of costs parameterized by , underlying different statistical noise models. We show that this flexibility in the cost function allows for better quality of factorization and model selection on various classes of real-world signals such as audio and images. Secondly, the algorithms described herein are such that the cost function monotonically decreases to a local minimum whereas the algorithm in [22] is heuristic. Convergence is guaranteed by the MM framework.

1.3 Paper organization

In Section 2, we state our notation and introduce -NMF and the MM technique. In Section 3, we present our Bayesian model for -NMF. Section 4 details - and -ARD for model selection in -NMF. We then compare the proposed algorithms to other related works in Section 5. In Section 6, we present extensive numerical results to demonstrate the efficacy and robustness of - and -ARD. We conclude the discussion in Section 7.

2 Preliminaries

2.1 Notations

We denote by , and , the data, dictionary and activation matrices, respectively. These nonnegative matrices are of dimensions , and , respectively. The entries of these matrices are denoted by , and respectively. The column of is denoted by , and denotes the row of . Thus, and .

2.2 NMF with the -divergence

This paper considers NMF based on the -divergence, which we now review. The -divergence was originally introduced for in [23, 24] and later generalized to in [7], which is the definition we use here:

| (4) |

The limiting cases and correspond to the IS and KL-divergences, respectively. Another case of note is which corresponds to the squared Euclidean distance, i.e., . The parameter essentially controls the assumed statistics of the observation noise and can either be fixed or learnt from training data by cross-validation. Under certain assumptions, the -divergence can be mapped to a log-likelihood function for the Tweedie distribution [25], parametrized with respect to its mean. In particular, the values underlie the multiplicative Gamma observation noise, Poisson noise and Gaussian additive observation noise respectively. We describe this property in greater detail in Section 3.2. The -divergence offers a continuum of noise statistics that interpolates between these three specific cases. In the following, we use the notation to denote the separable cost function in (3) with the scalar cost in (4).

| Auxiliary function | |

|---|---|

2.3 Majorization-minimization (MM) for -NMF

We briefly recall some results in [9] on standard -NMF. In particular, we describe how an MM algorithm [26] that recovers a stationary point of (3) can be derived. The algorithm updates given , and given , and these two steps are essentially the same by the symmetry of and by transposition ( is equivalent to ). Let us thus focus on the optimization of given . The MM framework involves building a (nonnegative) auxiliary function that majorizes the objective everywhere, i.e.,

| (5) |

for all pairs of nonnegative matrices . The auxiliary function also matches the cost function whenever its arguments are the same, i.e., for all ,

| (6) |

If such an auxiliary function exists and the optimization of over for fixed is simple, the optimization of may be replaced by the simpler optimization of over . Indeed, any iterate such that reduces the cost since

| (7) |

The first inequality follows from (5) and the second from the optimality of . The MM update thus consists in

| (8) |

Note that if , a local minimum is attained since the inequalities in (7) are equalities. The key of the MM approach is thus to build an auxiliary function which reasonably approximates the original objective at the current iterate , and such that the function is easy to minimize (over the first variable ). In our setting, the objective function can be decomposed into the sum of a convex term and a concave term. As such, the construction proposed in [9] and [8] consists in majorizing the convex and concave terms separately, using Jensen’s inequality and a first-order Taylor approximation, respectively. Denoting and

| (9) |

the resulting auxiliary function can be expressed as in Table I, where denote constant terms that do not depend on . In the sequel, the use of the tilde over a parameter will generally denote its previous iterate. Minimization of with respect to (w.r.t) thus leads to the following simple update

| (10) |

where the exponent is defined as

| (11) |

3 The Model for Automatic relevance determination in -NMF

In this section, we describe our probabilistic model for NMF. The model involves tying the column of to the row of together through a common scale parameter . If is driven to zero (or, as we will see, a positive lower bound) during inference, then all entries in the corresponding column of and row of will also be driven to zero.

3.1 Priors

We are inspired by Bayesian PCA [13] where each element of is assigned a Gaussian prior with column-dependent variance-like parameters . These ’s are known as the relevance weights. However, our formulation has two main differences vis-à-vis Bayesian PCA. Firstly, there are no nonnegativity constraints in Bayesian PCA. Secondly, in Bayesian PCA, thanks to the simplicity of the statistical model (multivariate Gaussian observations with Gaussian parameter priors), can be easily integrated out of the likelihood, and the optimization can be done over , where is the vector of relevance weights. We have to maintain the nonnegativity of the elements in and and also in our setting the activation matrix cannot be integrated out analytically.

To ameliorate the above-mentioned problems, we propose to tie the columns of and the rows of together through common scale parameters. This construction is not over-constraining the scales of and , because of the inherent scale indeterminacy between and . Moreover, we choose nonnegative priors for and to ensure that all elements of the basis and activation matrices are nonnegative. We adopt a Bayesian approach and assign and Half-Normal or Exponential priors. When and have Half-Normal priors,

| (12) |

where for , and when . Note that if is a Gaussian (Normal) random variable, then is a Half-Normal. When and are assigned Exponential priors,

| (13) |

where for , , and otherwise. Note from (12) and (13) that the column of and the row of are tied together by a common variance-like parameter , also known as the relevance weight. When a particular is small, that particular column of and row of are not relevant and vice versa. When a row and a column are not relevant, their norms are close to zero and thus can be removed from the factorization without compromising too much on data fidelity. This removal of common rows and columns makes the model more parsimonious.

Finally, we impose inverse-Gamma priors on each relevance weight , i.e.,

| (14) |

where and are the (nonnegative) shape and scale hyperparameters respectively. We set and to be constant for all . We will state how to choose these in a principled manner in Section 4.5. Furthermore, each relevance parameter is independent of every other, i.e., .

3.2 Likelihood

The -divergence is related to the family of Tweedie distributions [25]. The relation was noted by Cichocki et al. [27] and detailed in [28]. The Tweedie distribution is a special case of the exponential dispersion model [29], itself a generalization of the more familiar natural exponential family. It is characterized by the simple polynomial relation between its mean and variance

| (15) |

where is the mean, is the shape parameter , and is referred to as the dispersion parameter. The Tweedie distribution is only defined for and . For , its probability density function (pdf) or probability mass function (pmf) can be written in the following form

| (16) |

where is referred to as the base function. For , the pdf or pmf takes the appropriate limiting form of (16). The support of varies with the value of , but the set of values that can take on is generally , except for , for which it is and the Tweedie distribution coincides with the Gaussian distribution of mean and variance . For (and ), the Tweedie distribution coincides with the Poisson distribution. For , it coincides with the Gamma distribution with shape parameter and scale parameter .111We employ the following convention for the Gamma distribution . The base function admits a closed form only for .

Finally, the deviance of Tweedie distribution, i.e., the log-likelihood ratio of the saturated () and general model is proportional to the -divergence. In particular,

| (17) |

where is the scalar cost function defined in (4). As such the -divergence acts as a minus log-likelihood for the Tweedie distribution, whenever the latter is defined. Because the data coefficients are conditionally independent given , the negative log-likelihood function is

| (18) |

3.3 Objective function

We now form the maximum a posteriori (MAP) objective function for the model described in Sections 3.1 and 3.2. On account of (12), (13), (14) and (18),

| (19) | |||

| (20) |

where (20) follows from Bayes’ rule and for the two statistical models,

Observe that for the regularized cost function in (20), the second term is monotonically decreasing in while the third term is monotonically increasing in . Thus, a subset of the ’s will be forced to a lower bound which we specify in Section 4.4 while the others will tend to a larger value. This serves the purpose of pruning irrelevant components out of the model. In fact, the vector of relevance parameters can be optimized analytically in (20) leading to an objective function that is a function of and only, i.e.,

| (21) |

where .

In our algorithms, instead of optimizing (21), we keep as an auxiliary variable for optimizing in (20) to ensure that the columns and the rows of are decoupled. More precisely, and are conditionally independent given . In fact, (21) shows that the -optimized objective function induces sparse regularization among groups, where the groups are pairs of columns and rows, i.e., . In this sense, our work is related to group LASSO [30] and its variants. See for example [31]. The function in (21) is a sparsity-inducing term and is related to reweighted -minimization [32]. We discuss these connections in greater detail in the supplementary material [33].

4 Inference Algorithms

In this section, we describe two algorithms for optimizing the objective function (20) for given fixed . The updates for are symmetric given . These algorithms will be based on the MM idea for -NMF and on the two prior distributions of and . In particular, we use the auxiliary function defined in Table I as an upper bound of the data fit term .

4.1 Algorithm for -ARD -NMF

We now introduce -ARD -NMF. In this algorithm, we assume that and have Half-Normal priors as in (12) and thus, the regularizer is

| (22) |

The main idea behind the algorithms is as follows: Consider the function which is the original auxiliary function times plus the regularization term. It can in fact be easily shown in [9, Sec. 6] that is an auxiliary function to the (penalized) objective function in (20). Ideally, we would take the derivative of w.r.t and set it to zero. Then the updates would proceed in a manner analogous to (10). However, the regularization term does not “fit well” with the form of the auxiliary function in the sense that cannot be solved analytically for all . Thus, our idea for -ARD is to consider the cases and separately and to find an upper bound of by some other auxiliary function so that the resulting equation can be solved in closed-form.

To derive our algorithms, we first note the following:

Lemma 1.

For every , the function is monotonically non-decreasing in . In fact, is monotonically increasing unless .

In the above lemma, by L’Hôpital’s rule. The proof of this simple result can be found in [34].

We first derive -ARD for . The idea is to upper bound the regularizer in (22) elementwise using Lemma 1, and is equivalent to the moving-term technique described by Yang and Oja in [35, 34]. Indeed, we have

| (23) |

by taking in Lemma 1. Thus, for ,

| (24) |

where is a constant w.r.t the optimization variable . We upper bound the regularizer (22) elementwise by (24). The resulting auxiliary function (modified version of ) is

| (25) |

Note that (24) holds with equality iff or equivalently, so (6) holds. Thus, is indeed an auxiliary function to . Recalling the definition of for in Table I, differentiating w.r.t and setting the result to zero yields the update

| (26) |

Note that the exponent corresponds to for the case. Also observe that the update is similar to MM for -NMF [cf. (10)] except that there is an additional term in the denominator.

For the case , our strategy is not to majorize the regularization term. Rather we majorize the the auxiliary function itself. By applying Lemma 1 with , we have that for all ,

| (27) |

which means that

| (28) |

By replacing the first term of in Table I (for ) with the upper bound above, we have the following new objective function

| (29) |

Differentiating w.r.t and setting to zero yields the simple update

| (30) |

To summarize the algorithm concisely, we define the exponent used in the updates in (26) and (30) as

| (31) |

Finally, we remark that even though the updates in (26) and (30) are easy to implement, we either majorized the regularizer or the auxiliary function . These bounds may be loose and thus may lead to slow convergence in the resulting algorithm. In fact, we can show that for , we do not have to resort to upper bounding the original function . Instead, we can choose to solve a polynomial equation to update . The cases correspond respectively to solving cubic, quadratic and linear equations in respectively. It is also true that for all rational , we can form a polynomial equation in but the order of the resulting polynomial depends on the exact value of . See the supplementary material [33].

4.2 Algorithm for -ARD -NMF

4.3 Update of

We have described how to update using either -ARD or -ARD. Since and are related in a symmetric manner, we have also effectively described how to update . We now describe a simple update rule for the ’s. This update is the same for both - and -ARD. We first find the partial derivative of w.r.t and set it to zero. This gives the update:

| (33) |

where and are defined after (20).

4.4 Stopping criterion and determination of

In this section, we describe the stopping criterion and the determination of the effective number of components . Let and be the vector of relevance weights at the current (updated) and previous iterations respectively. The algorithm is terminated whenever falls below some threshold . Note from (33) that iterates of each are bounded from below as and this bound is attained when and are zero vectors, i.e., the column of and the row of are pruned out of the model. After convergence, we set to be the number of components of such that the ratio is strictly larger than , i.e.,

| (34) |

where is some threshold. We choose this threshold to be the same as that for the tolerance level .

4.5 Choosing the hyperparameters

4.5.1 Choice of dispersion parameter

The dispersion parameter represents the tradeoff between the data fidelity and the regularization terms in (20). It needs to be fixed, based on prior knowledge about the noise distribution, or learned from the data using either cross-validation or MAP estimation. In the latter case, is assigned a prior and the objective can be optimized over . This is a standard feature in penalized likelihood approaches and has been widely discussed in the literature. In this work, we will not address the estimation of , but only study the influence the regularization term on the factorization given . In many cases, it is reasonable to fix based on prior knowledge. In particular, under the Gaussian noise assumption, and and . Under the Poisson noise assumption, and and . Under multiplicative Gamma noise assumption, and is a Gamma noise of mean 1, or equivalently and and . In audio applications where the power spectrogram is to be factorized, as in Section 6.3, the multiplicative exponential noise model (with ) is a generally agreed upon assumption [3] and thus .

4.5.2 Choice of hyperparameters and

We now discuss how to choose the hyperparameters and in (14) in a data-dependent and principled way. Our method is related to the method of moments. We first focus on the selection of using the sample mean of data, given . Then the selection of based on the sample variance of the data is discussed at the end of the section.

Consider the approximation in (1), which can be written element-wise as

| (35) |

The statistical models corresponding to shape parameter imply that . We extrapolate this property to derive a rule for selecting the hyperparameter for all (and for nonnegative real-valued data in general) even though there is no known statistical model governing the noise when . When is large, the law of large numbers implies that the sample mean of the elements in is close to the population mean (with high probability), i.e.,

| (36) |

We can compute for the Half-Normal and Exponential models using the moments of these distributions and those of the inverse-Gamma for . These yield

| (39) |

By equating these expressions to the empirical mean , we conclude that we can choose according to

| (42) |

In summary, and for - and -ARD respectively.

By using the empirical variance of and the relation between the mean and variance of the Tweedie distribution in (15), we may also estimate from the data. The resulting relations are more involved and these calculations are deferred to the supplementary material [33] for . However, experiments showed that the resulting learning rules for did not consistently give satisfactory results, especially when is not sufficiently large. In particular, the estimates sometimes fall out of the parameter space, which is a known feature of the method of moments. Observe that appears in the objective function (21) only through (-ARD) or (-ARD). As such, the influence of is moderated by . Hence, if we want to choose a prior on that is not too informative, then we should choose to be small compared to . Experiments in Section 6 confirm that smaller values of (relative to ) typically produce better results. As discussed in the conclusion, a more robust estimation of (as well as and ) would involve a fully Bayesian treatment of our problem, which is left for future work.

5 Connections with other works

Our work draws parallel with a few other works on model order selection in NMF. The closest work is [18] which also proposes automatic component pruning via a MAP approach. It was developed during the same period as and independently of our earlier work [22]. An extension to multi-array analysis is also proposed in [19]. In [18], Mørup & Hansen consider NMF with the Euclidean and KL costs. They constrained the columns of to have unit norm (i.e., ) and assumed that the coefficients of are assigned exponential priors . A non-informative Jeffrey’s prior is further assumed on . Put together, they consider the following optimization over :

| (43) |

where is either the squared Euclidean distance or the KL-divergence. A major difference compared to our objective function in (20) is that this method involves optimizing under the constraint , which is non-trivial. As such, to solve (43) the authors in [18] use a change of variable and derive a heuristic multiplicative algorithm based on the ratio of negative and positive parts of the new objective function, along the lines of [36]. In contrast, our approach treats and symmetrically and the updates are simple. Furthermore, the pruning approach in [18] only occurs in the rows and the corresponding columns of may take any nonnegative value (subject to the norm constraint), which makes the estimation of these columns of ill-posed (i.e., the parametrization is such that a part of the model is not observable). In contrast, in our approach and are tied together so they converge to zero jointly when reaches its lower bound.

Our work is also related to the automatic rank determination method in Projective NMF proposed by Yang et al. in [20]. Following the principle of PCA, Projective NMF seeks a nonnegative matrix such that the projection of on the subspace spanned by best fits . In other words, it is assumed that . Following ARD in Bayesian PCA as originally described by Bishop [13], Yang et al. consider the additive Gaussian noise model and propose to place half-normal priors with relevance parameters on the columns of . They describe how to adapt EM to achieve MAP estimation of and its relevance parameters.

Estimation of the model order in the Itakura-Saito NMF (multiplicative exponential noise) was addressed by Hoffman et al. [21]. They employ a nonparametric Bayesian setting in which is assigned a large value (in principle, infinite) but the model is such that only a finite subset of components is retained. In their model, the coefficients of and have Gamma priors with fixed hyperparameters and a weight parameter is placed before each component in the factor model, i.e., . The weight, akin to the relevance parameter in our setting, is assigned a Gamma prior with a sparsity-enforcing shape parameter. A difference with our model is the a priori independence of the factors and the weights. Variational inference is used in [21].

In contrast with the above-mentioned works, the work herein presents a unified framework for model selection in -NMF. The proposed algorithms have low complexity per iteration and are simple to implement, while decreasing the objective function at every iteration. We compare the performance of our algorithms to those in [18] and [21] in Sections 6.3 (music decomposition) and 6.4 (stock price prediction).

6 Experiments

In this section, we present extensive numerical experiments demonstrating the robustness and efficiency of the proposed algorithms for (i) uncovering the correct model order and (ii) learning better decompositions for modeling nonnegative data.

6.1 Simulations with synthetic data

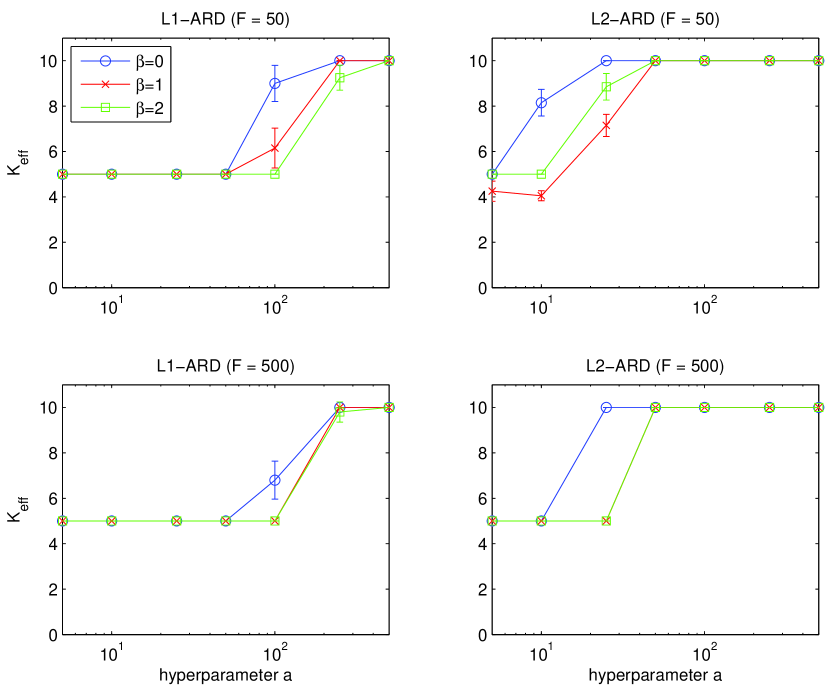

In this section, we describe experiments on synthetic data generated according to the model. In particular, we fixed a pair of hyperparameters and sampled relevance weights according to the inverse-Gamma prior in (14). Conditioned on these relevance weights, we sampled the elements of and from the Half-Normal or Exponential models depending on whether we chose to use - or -ARD. These models are defined in (12) and (13) respectively. We set and for reasons that will be made clear in the following. We define the noiseless matrix as . We then generated a noisy matrix given according to the three statistical models corresponding to IS-, KL- and EUC-NMF respectively. More precisely, the parameters of the noise models are chosen so that the signal-to-noise ratio in dB, defined as is approximately 10 dB for each . For , this corresponds to an , the shape parameter, of approximately . For , the parameterless Poisson noise model results in an integer-valued noisy matrix . Since there is no noise parameter to select Poisson noise model, we chose so that the elements of the data matrix are large enough resulting in an 10 dB. For the Gaussian observation model (), we can analytically solve for the noise variance so that the is approximately 10 dB. In addition, we set the number of columns , the initial number of components and chose two different values for , namely 50 and 500. The threshold value is set to (refer to Section 4.4). It was observed using this value of the threshold that the iterates of converged to their limiting values. We ran - and -ARD for and using computed as in Section 4.5.2. The dispersion parameter is assumed known and set as in the discussion after (18).

To make fair comparisons, the data and the initializations are the same for - and -ARD as well as for every . We averaged the inferred model order over 10 different runs. The results are displayed in Fig. 1.

Firstly, we observe that -ARD recovers the model order correctly when and . This range includes , which is the true hyperparameter we generated the data from. Thus, if we use the correct range of values of , and if the is of the order 10 dB (which is reasonable in most applications), we are able to recover the true model order from the data. On the other hand, from the top right and bottom right plots, we see that -ARD is not as robust in recovering the right latent dimensionality.

Secondly, note that the quality of estimation is relatively consistent across various ’s. The success of the proposed algorithms hinges more on the amount of noise added (i.e., the ) compared to which specific is assumed. However, as discussed in Section 3.2, the shape parameter should be chosen to reflect our belief in the underlying generative model and the noise statistics.

Thirdly, observe that when more data are available (), the estimation quality improves significantly. This is evidenced by the fact that even -ARD (bottom right plot) performs much better – it selects the right model order for all and . The estimates are also much more consistent across various initializations. Indeed the standard deviations for most sets of experiments is zero, demonstrating that there is little or no variability due to random initializations.

6.2 Simulations with the swimmer dataset

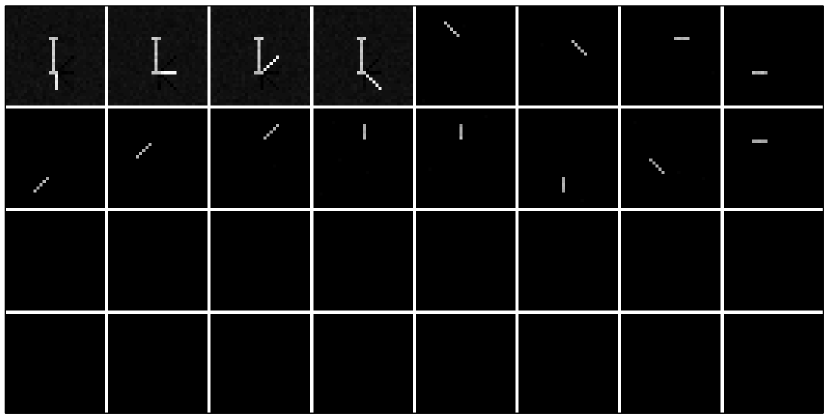

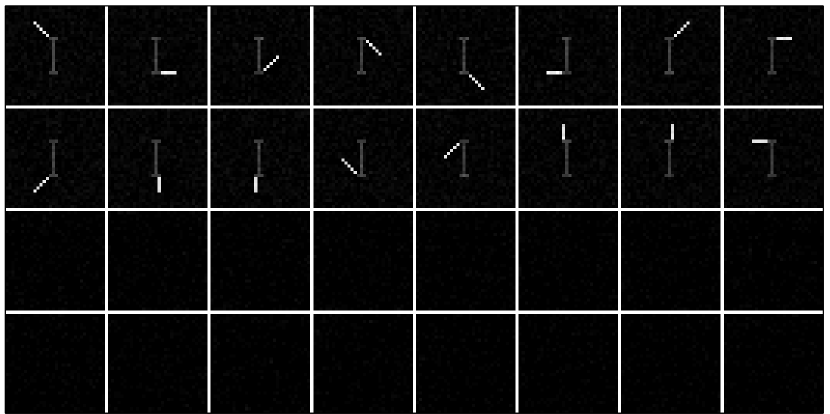

In this section we report experiments on the swimmer dataset introduced in [37]. This is a synthetic dataset of images each of size . Each image represents a swimmer composed of an invariant torso and four limbs, where each limb can take one of four positions. We set background pixel values to 1 and body pixel values to 10, and generated noisy data with Poisson noise. Sample images of the resulting noisy data are shown in Fig. 2. The “ground truth” number of components for this dataset is , which corresponds to all the different limb positions. The torso and background form an invariant component that can be associated with any of the four limbs, or equally split among limbs. The data images are vectorized and arranged in the columns of .

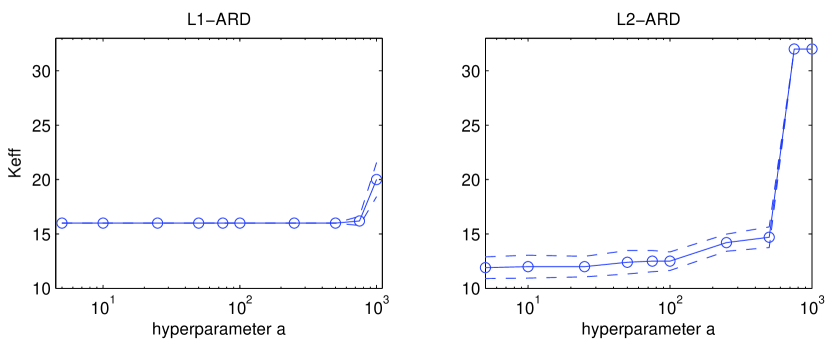

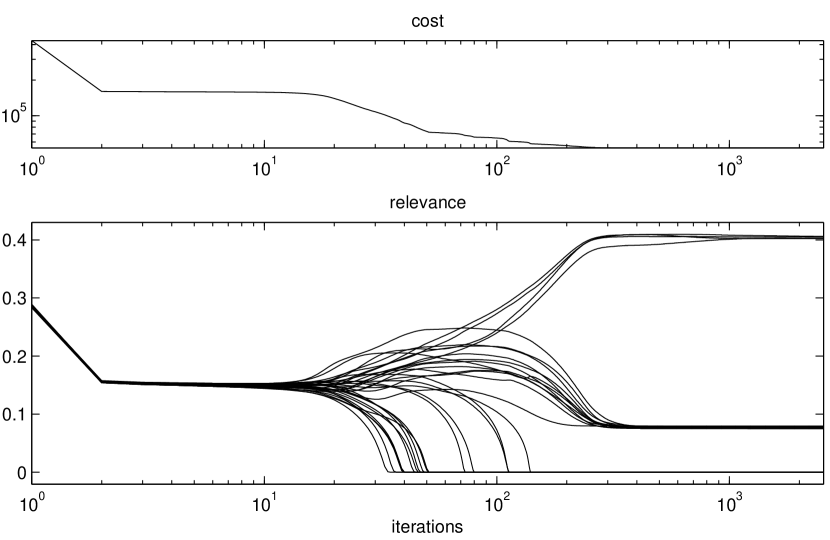

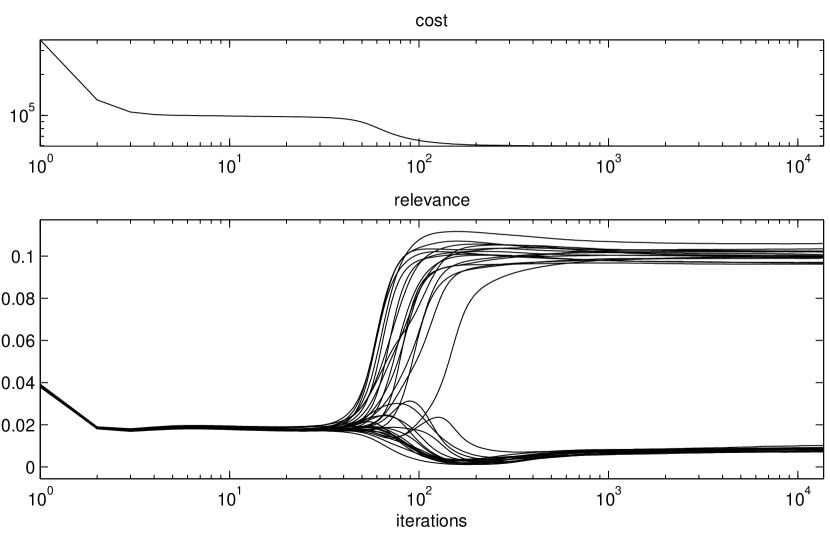

We applied - and -ARD with (KL-divergence, matching the Poisson noise assumption, and thus ), and . We tried several values for the hyperparameter , namely , and set according to (42). For every value of we ran the algorithms from 10 common positive random initializations. The regularization paths returned by the two algorithms are displayed in Fig. 3. -ARD consistently estimates the correct number of components () up to . Fig. 4 displays the learnt basis, objective function and relevance parameters along iterations in one run of -ARD when . It can be seen that the ground truth is perfectly recovered.

In contrast to -ARD, Fig. 3 shows that the value of returned by -ARD is more variable across runs and values of . Manual inspection reveals that some runs return the correct decomposition when (and those are the runs with lowest end value of the objective function, indicating the presence of apparent local minima), but far less consistently than -ARD. Then it might appear like the decomposition strongly overfits the noise for . However, visual inspection of learnt dictionaries with these values show that the solutions still make sense. As such, Fig. 5 displays the dictionary learnt by -ARD with . The figure shows that the hierarchy of the decomposition is preserved, despite that the last 16 components capture some residual noise, as a closer inspection would reveal. Thus, despite that pruning is not fully achieved in the 16 extra components, the relevance parameters still give a valid interpretation of what are the most significant components. Fig. 5 shows the evolution of relevance parameters along iterations and it can be seen that the 16 “spurious” components approach the lower bound in the early iterations before they start to fit noise. Note that -ARD returns a solution where the torso is equally shared by the four limbs. This is because the penalization favors this particular solution over the one returned by -ARD, which favors sparsity of the individual dictionary elements.

With , the average number of iterations for convergence is approximately for -ARD for all . The average number of iterations for -ARD is of the same order for , and increases to more than iterations for , because all components are active for these ’s.

6.3 Music decomposition

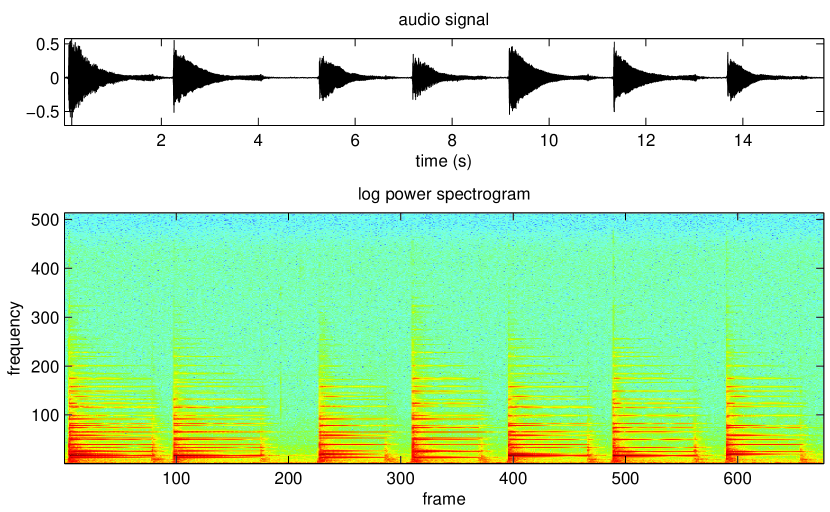

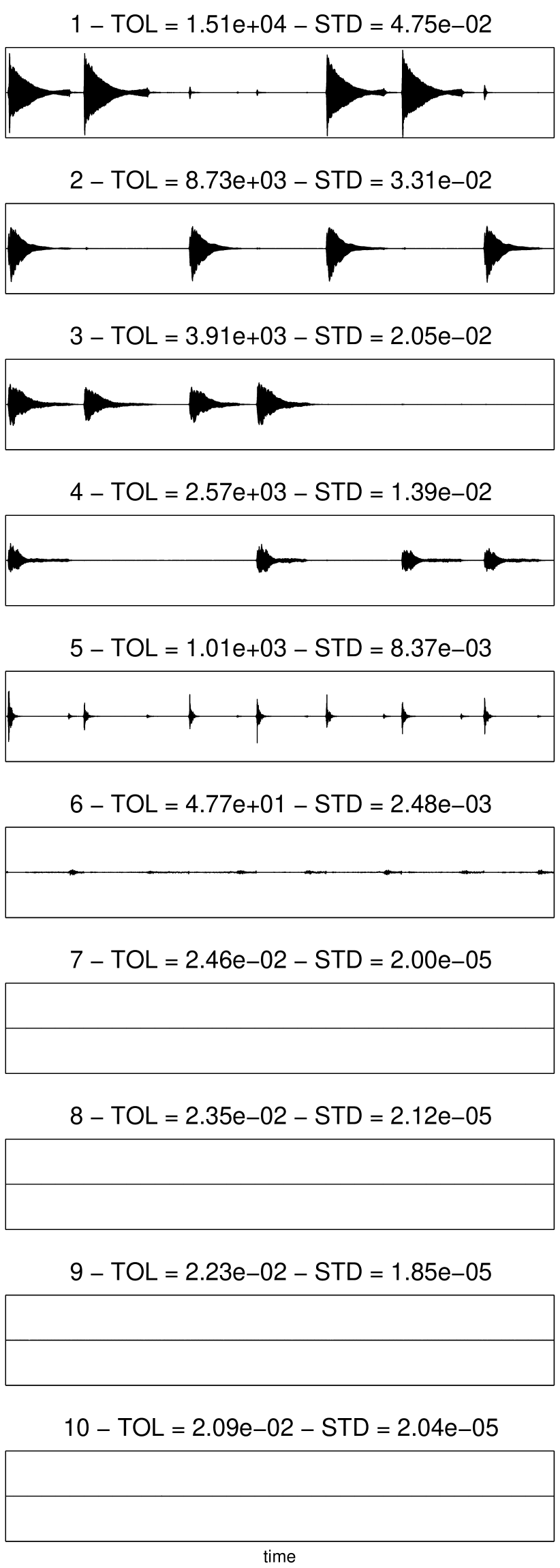

We now consider a music signal decomposition example and illustrate the benefits of ARD in NMF with the IS divergence (). Févotte et al. [3] showed that IS-NMF of the power spectrogram underlies a generative statistical model of superimposed Gaussian components, which is relevant to the representation of audio signals. As explained in Sections 3.2 and 4.5, this model is also equivalent to assuming that the power spectrogram is observed in multiplicative exponential noise, i.e., setting . We investigate the decomposition of the short piano sequence used in [3], a monophonic 15 seconds-long signal recorded in real conditions. The sequence is composed of 4 piano notes, played all at once in the first measure and then played by pairs in all possible combinations in the subsequent measures. The STFT of the temporal data was computed using a sinebell analysis window of length (46 ms) with 50 % overlap between two adjacent frames, leading to frames and frequency bins. The musical score, temporal signal and log-power spectrogram are shown in Fig. 6. In [3] it was shown that IS-NMF of the power spectrogram can correctly separate the spectra of the different notes and other constituents of the signal (sound of hammer on the strings, sound of sustain pedal etc.).

We set (3 times the “ground truth” number of components) and ran -ARD with , and computed according to (42). We ran the algorithm from 10 random initializations and selected the solution returned with the lowest final cost. For comparison, we ran standard nonpenalized Itakura-Saito NMF using the multiplicative algorithm described in [3], equivalent to -ARD with and . We ran IS-NMF 10 times with the same random initializations we used for ARD IS-NMF, and selected the solution with minimum fit. Additionally, we ran the methods by Mørup & Hansen (with KL-divergence) [18] and Hoffman et al. [21]. We used Matlab implementations either publicly available [21] or provided to us by the authors [18]. The best among ten runs of these methods was selected.

Given an approximate factorization of the data spectrogram returned by any of the four algorithms we proceeded to reconstruct time-domain components by Wiener filtering, following [3]. The STFT estimate of component is reconstructed by

| (44) |

and the STFT is inverted to produce the temporal component .222With the approach of Hoffman et al. [21], the columns of have to be multiplied by their corresponding weight parameter prior to reconstruction. By linearity of the reconstruction and inversion, the decomposition is conservative, i.e.,

(a) IS-NMF

(b) ARD IS-NMF

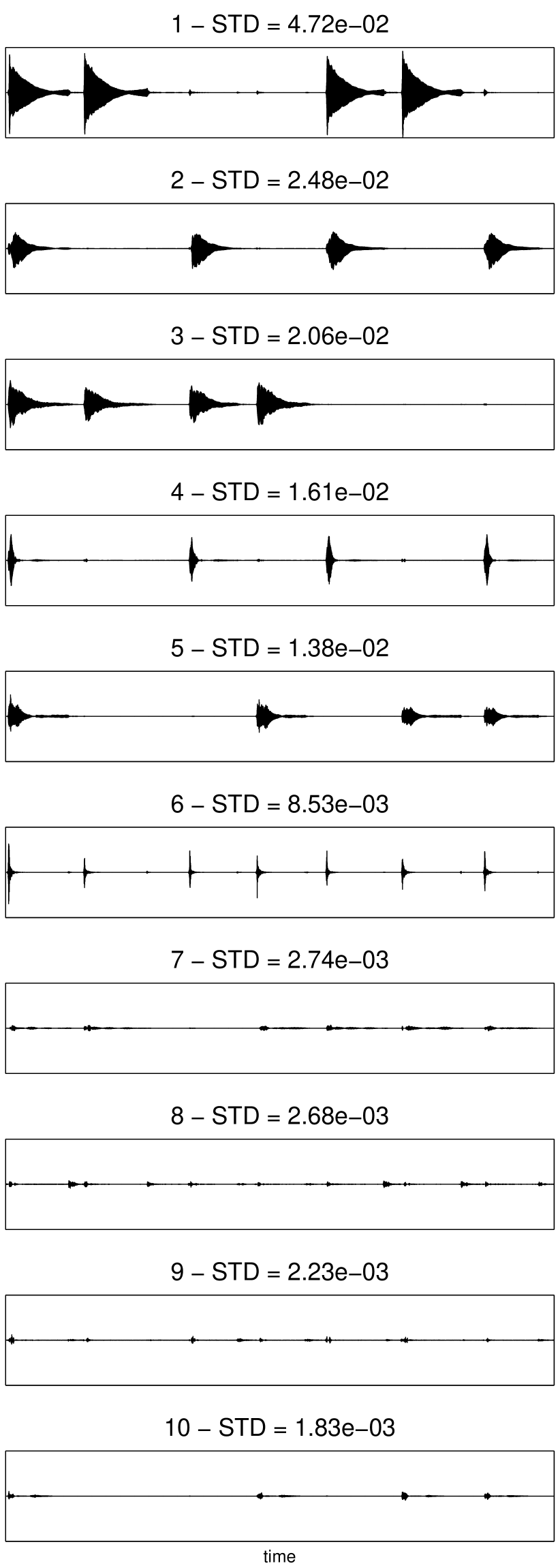

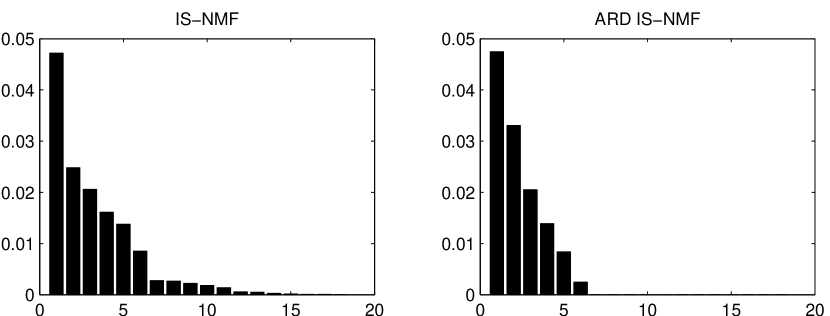

The components produced by IS-NMF were ordered by decreasing value of their standard deviations (computed from the time samples). The components produced by ARD IS-NMF, Mørup & Hansen [18] and Hoffman et al. [21] were ordered by decreasing value of their relevance weights ( or ). Fig. 7 displays the ten first components produced by IS-NMF and ARD IS-NMF. The -axes of the two figures are identical so that the component amplitudes are directly comparable. Fig. 8 displays the histograms of the standard deviation values of all 18 components for IS-NMF, ARD IS-NMF, Mørup & Hansen [18] and Hoffman et al. [21].333The sound files produced by all the approaches are available at http://perso.telecom-paristech.fr/~fevotte/Samples/pami12/soundsamples.zip

The histogram on top right of Fig. 8 indicates that ARD IS-NMF retains 6 components. This is also confirmed by the value of relative relevance (upon convergence of the relevance weights), displayed with the components on Fig. 7, which drops by a factor of about 2000 from component 6 to component 7. The 6 components correspond to expected semantic units of the musical sequence: the first four components extract the individual notes and the next two components extract the sound of hammer hitting the strings and the sound produced by the sustain pedal when it is released. In contrast IS-NMF has a tendency to overfit, in particular the second note of the piece is split into two components ( and ). The histogram on bottom left of Fig. 8 shows that the approach of Mørup & Hansen [18] (with the KL-divergence) retains 11 components. Visual inspection of the reconstructed components reveals inaccuracies in the decomposition and significant overfit (some notes are split in subcomponents). The poorness of the results is in part explained by the inadequacy of the KL-divergence (or Euclidean distance) for factorization of spectrograms, as discussed in [3]. In contrast our approach offers flexibility for ARD NMF where the fit-to-data term can be chosen according to the application by setting to the desired value.

The histogram on bottom right of Fig. 8 shows that the method by Hoffman et al. [21] retains approximately 5 components. The decomposition resembles the expected decomposition more closely than [18], except that the hammer attacks are merged with one of the notes. However it is interesting to note that the distribution of standard deviations does not follow the order of relevance values. This is because the weight parameter is independent of and in the prior. As such, the factors are allowed to take very small values while the weight values are not necessarily small.

Finally, we remark that on this data -ARD IS-NMF performed similarly to -ARD IS-NMF and in both cases the retrieved decompositions were fairly robust to the choice of . We experimented with the same values of as in previous section and the decompositions and their hierarchies were always found correct. We point out that, as with IS-NMF, initialization is an issue, as other runs did not produced the desired decomposition into notes. However, in our experience the best out of 10 runs always output the correct decomposition.

6.4 Prediction of stock prices

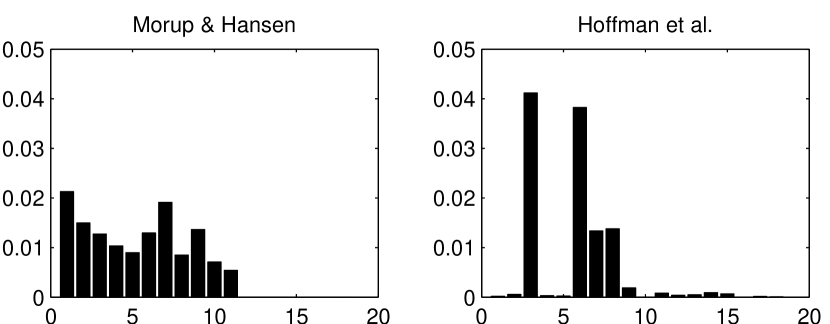

NMF (with the Euclidean and KL costs) has previously been applied on stock data [5] to learn “basis functions” and to cluster companies. In this section, we perform a prediction task on the stock prices of the Dow 30 companies (comprising the Dow Jones Industrial Average). These are major American companies from various sectors of the economy such as services (e.g., Walmart), consumer goods (e.g., General Motors) and healthcare (e.g., Pfizer). The dataset consists of the stock prices of these companies from 3rd Jan 2000 to 27th Jul 2011, a total of trading days.444Stock prices of the Dow 30 companies are provided at the following link: http://www.optiontradingtips.com/resources/historical-data/dow-jones30.html. The raw data consists of 4 stock prices per company per day. The mean of the 4 data points is taken to be the representative of the stock price of that company for that day. The data are displayed in the top left plot of Fig. 9.

In order to test the prediction capabilities of our algorithm, we organized the data into an matrix and removed of the entries at random. For the first set of experiments, we performed standard -NMF with , for different values of , using the observed entries only.555Accounting for the missing data involves applying a binary mask to and , where 0 indicates missing entries [38]. We report results for different non-integer values of in the following. Having performed KL-NMF on the incomplete data, we then estimated the missing entries by multiplying the inferred basis and the activation coefficients to obtain the estimate . The normalized KL-divergence (NKLD) between the true (missing) stock data and their estimates is then computed as

| (45) |

where is the set of missing entries and is the KL-divergence (). The smaller the NKLD, the better the prediction of the missing stock prices and hence the better the decomposition of into and . We then did the same for - and -ARD KL-NMF, for different values of and using . For KL-NMF the criterion for termination is chosen so that it mimics that in Section 4.4. Namely, as is commonly done in the NMF literature, we ensured that the columns of are normalized to unity. Then, we computed the NMF relevance weights . We terminate the algorithm whenever falls below . We averaged the results over 20 random initializations. The NKLDs and the the inferred model orders are displayed in Fig. 9.

In the top right plot of Fig. 9, we observe that there is a general increasing trend; as increases, the inferred model order also increases. In addition, for the same value of , -ARD prunes more components than -ARD due to its sparsifying effect. This was also observed for synthetic data and the swimmer dataset. However, even though -ARD retains almost all the components, the basis and activation coefficients learned model the underlying data better. This is because penalization methods result in coefficients that are more dense and are known to be better for prediction (rather than sparsification) tasks.

From the bottom left plot of Fig. 9, we observe that when is too small, the model is not “rich” enough to model the data and hence the NKLD is large. Conversely, when is too large, the model overfits the data, resulting in a large NKLD. We also observe that -ARD performs spectacularly across a range of values of the hyperparameter , uniformly better than standard KL-NMF. The NKLD for estimating the missing stock prices hovers around 0.2, whereas KL-NMF results in an NKLD of more than 0.23 for all . This shows that -ARD produces a decomposition that is more relevant for modeling missing data. Thus, if one does not know the true model order a priori and chooses to use -ARD with some hyperparameter , the resulting NKLD would be much better than doing KL-NMF even though many components will be retained. In contrast, -ARD does not perform as spectacularly across all values of but even when a small number of components is retained (at , , NKLD for -ARD , NKLD for KL-NMF ), it performs significantly better than KL-NMF. It is plausible that the stock data fits the assumptions of the Half-Normal model better than the Exponential model and hence -ARD performs better.

For comparison, we also implemented a version of the method by Mørup & Hansen [18] that handles missing data. The mean NKLD value returned over ten runs is , and thus it is clearly inferior to the methods in this paper. The data does not fit the model well.

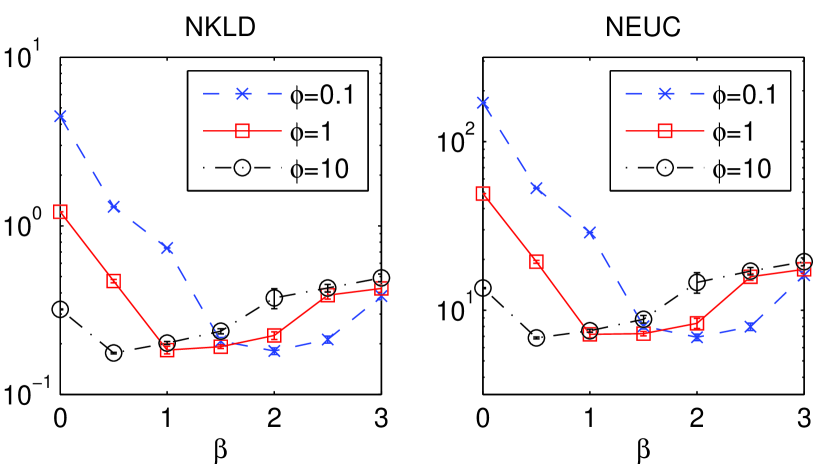

Finally, in Fig. 10 we demonstrate the effect of varying the shape parameter and the dispersion parameter . The distance between the predicted stock prices and the true ones is measured using the NKLD in (45) and the NEUC (the Euclidean analogue of the NKLD). We also computed the NIS (the IS analogue of the NKLD), and noted that the results across all performance metrics are similar so we omit the NIS. We used -ARD, set and calculated using (42). We also chose integer and non-integer values of to demonstrate the flexibility of -ARD. It is observed that gives the best NKLD and NEUC and that performs well across a wide range of values of .

7 Conclusion

In this paper, we proposed a novel statistical model for -NMF where the columns of and rows are tied together through a common scale parameter in their prior, exploiting (and solving) the scale ambiguity between and . MAP estimation reduces to a penalized NMF problem with a group-sparsity inducing regularizing term. A set of MM algorithms accounting for all values of and either - or -norm group-regularization was presented. They ensure the monotonic decrease of the objective function at each iteration and result in multiplicative update rules of linear complexity in and . The updates automatically preserve nonnegativity given positive initializations and are easily implemented. The efficiency of our approach was validated on several synthetic and real-world datasets, with competitive performance w.r.t. the state-of-the-art. At the same time, our proposed methods offer improved flexibility over existing approaches (our approach can deal with various types of observation noise and prior structure in a unified framework). Using the method of moments, an effective strategy for the selection of hyperparemeter given was proposed and, as a general rule of thumb, we recommend to set a small value w.r.t. .

There are several avenues for further research: Here we derived a MAP approach that works efficiently, but more sophisticated inference techniques can be envisaged, such as fully Bayesian inference in the model we proposed in Section 3. Following similar treatments in sparse regression [39, 40] or with other forms of matrix factorization [41], one could seek the maximization of using variational or Markov chain Monte-Carlo inference, and in particular handle hyperparameter estimation in a (more) principled way. Other more direct extensions of this work concern the factorization of tensors and online-based methods akin to [42, 43].

Acknowledgements

The authors would like to acknowledge Francis Bach for discussions related to this work, Y. Kenan Yılmaz and A. Taylan Cemgil for discussions on Tweedie distributions, as well as Morten Mørup and Matt Hoffman for sharing their code. We would also like to thank the reviewers whose comments helped to greatly improve the paper.

References

- [1] P. Paatero and U. Tapper, “Positive matrix factorization : A non-negative factor model with optimal utilization of error estimates of data values,” Environmetrics, vol. 5, pp. 111–126, 1994.

- [2] D. D. Lee and H. S. Seung, “Learning the parts of objects with nonnegative matrix factorization,” Nature, vol. 401, pp. 788–791, 1999.

- [3] C. Févotte, N. Bertin, and J.-L. Durrieu, “Nonnegative matrix factorization with the Itakura-Saito divergence. With application to music analysis,” Neural Computation, vol. 21, pp. 793–830, Mar. 2009.

- [4] D. Guillamet, B. Schiele, and J. Vitri, “Analyzing non-negative matrix factorization for image classification,” in International Conference Pattern Recognition, 2002.

- [5] K. Drakakis, S. Rickard, R. de Frein, and A. Cichocki, “Analysis of financial data using non-negative matrix factorization,” International Journal of Mathematical Sciences, vol. 6, June 2007.

- [6] Y. Gao and G. Church, “Improving molecular cancer class discovery through sparse non-negative matrix factorization,” Bioinformatics, vol. 21, pp. 3970–3975, 2005.

- [7] A. Cichocki, R. Zdunek, and S. Amari, “Csiszar’s divergences for non-negative matrix factorization: Family of new algorithms,” in Proc. 6th International Conference on Independent Component Analysis and Blind Signal Separation (ICA’06), (Charleston SC, USA), pp. 32–39, Mar. 2006.

- [8] M. Nakano, H. Kameoka, J. Le Roux, Y. Kitano, N. Ono, and S. Sagayama, “Convergence-guaranteed multiplicative algorithms for non-negative matrix factorization with beta-divergence,” in Proc. IEEE International Workshop on Machine Learning for Signal Processing (MLSP’2010), Sep. 2010.

- [9] C. Févotte and J. Idier, “Algorithms for nonnegative matrix factorization with the beta-divergence,” Neural Computation, vol. 23, pp. 2421–2456, Sep. 2011.

- [10] A. Cichocki, S. Cruces, and S. Amari, “Generalized Alpha-Beta divergences and their application to robust nonnegative matrix factorization,” Entropy, vol. 13, pp. 134–170, 2011.

- [11] G. Schwarz, “Estimating the dimension of a model,” Annals of Statistics, vol. 6, pp. 461–464, 1978.

- [12] D. J. C. Mackay, “Probable networks and plausible predictions – a review of practical Bayesian models for supervised neural networks,” Network: Computation in Neural Systems, vol. 6, no. 3, pp. 469–505, 1995.

- [13] C. M. Bishop, “Bayesian PCA,” in Advances in Neural Information Processing Systems (NIPS), pp. 382–388, 1999.

- [14] A. T. Cemgil, “Bayesian inference for nonnegative matrix factorisation models,” Computational Intelligence and Neuroscience, vol. 2009, no. Article ID 785152, p. 17 pages, 2009. doi:10.1155/2009/785152.

- [15] M. N. Schmidt, O. Winther, and L. K. Hansen, “Bayesian non-negative matrix factorization,” in In Proc. 8th Internation conference on Independent Component Analysis and Signal Separation (ICA’09), (Paraty, Brazil), Mar. 2009.

- [16] M. Zhong and M. Girolami, “Reversible jump MCMC for non-negative matrix factorization,” in Proc. International Conference on Artificial Intelligence and Statistics (AISTATS), p. 8, 2009.

- [17] M. N. Schmidt and M. Mørup, “Infinite non-negative matrix factorizations,” in Proc. European Signal Processing Conference (EUSIPCO), 2010.

- [18] M. Mørup and L. K. Hansen, “Tuning pruning in sparse non-negative matrix factorization,” in Proc. 17th European Signal Processing Conference (EUSIPCO’09), (Glasgow, Scotland), Aug. 2009.

- [19] M. Mørup and L. K. Hansen, “Automatic relevance determination for multiway models,” Journal of Chemometrics, vol. 23, no. 7-8, pp. 352–363, 2009.

- [20] Z. Yang, Z. Zhu, and E. Oja, “Automatic rank determination in projective nonnegative matrix factorization,” in Proc. 9th International Conference on Latent Variable Analysis and Signal Separation (ICA), (Saint-Malo, France), pp. 514–521, 2010.

- [21] M. D. Hoffman, D. M. Blei, and P. R. Cook, “Bayesian nonparametric matrix factorization for recorded music,” in International Conference on Machine Learning, 2010.

- [22] V. Y. F. Tan and C. Févotte, “Automatic relevance determination in nonnegative matrix factorization,” in Proc. Workshop on Signal Processing with Adaptative Sparse Structured Representations (SPARS), (St-Malo, France), Apr. 2009.

- [23] A. Basu, I. R. Harris, N. L. Hjort, and M. C. Jones, “Robust and efficient estimation by minimising a density power divergence,” Biometrika, vol. 85, pp. 549–559, Sep. 1998.

- [24] S. Eguchi and Y. Kano, “Robustifying maximum likelihood estimation,” tech. rep., Institute of Statistical Mathematics, June 2001. Research Memo. 802.

- [25] M. Tweedie, “An index which distinguishes between some important exponential families,” in Proc. of the Indian Statistical Institute Golden Jubilee International Conference (J. K. Ghosh and J. Roy, eds.), Statistics: Applications and New Directions, (Calcutta), pp. 579––604, 1984.

- [26] D. R. Hunter and K. Lange, “A tutorial on MM algorithms,” The American Statistician, vol. 58, pp. 30 – 37, 2004.

- [27] A. Cichocki, R. Zdunek, A. H. Phan, and S.-I. Amari, Nonnegative Matrix and Tensor Factorizations:Applications to Exploratory Multi-Way Data Analysis and Blind Source Separation. John Wiley & Sons, 2009.

- [28] Y. K. Yilmaz, Generalized tensor factorization. PhD thesis, Boğaziçi University, Istanbul, Turkey, 2012.

- [29] B. Jørgensen, “Exponential dispersion models,” Journal of the Royal Statistical Society. Series B (Methodological), vol. 49, no. 2, p. 127–162, 1987.

- [30] M. Yuan and Y. Lin, “Model selection and estimation in regression with grouped variables,” Journal of the Royal Statistical Society, Series B, vol. 68, no. 1, pp. 49–67, 2007.

- [31] F. Bach, R. Jenatton, J. Mairal, and G. Obozinski, “Optimization with sparsity-inducing penalties,” Foundations and Trends in Machine Learning, vol. 4, no. 1, pp. 1–106, 2012.

- [32] E. J. Candès, M. B. Wakin, and S. P. Boyd, “Enhancing sparsity by reweighted minimization,” Journal of Fourier Analysis and Applications, vol. 14, pp. 877–905, Dec 2008.

- [33] V. Y. F. Tan and C. Févotte, “Supplementary material for “Automatic relevance determination in nonnegative matrix factorization with the -divergence”,” 2012. http://perso.telecom-paristech.fr/~fevotte/Samples/pami12/suppMat.pdf.

- [34] Z. Yang and E. Oja, “Unified development of multiplicative algorithms for linear and quadratic nonnegative matrix factorization,” IEEE Trans. Neural Networks, in press.

- [35] Z. Yang and E. Oja, “Linear and nonlinear projective nonnegative matrix factorization,” IEEE Transactions on Neural Networks, vol. 21, pp. 734–749, May 2010.

- [36] J. Eggert and E. Körner, “Sparse coding and NMF,” in Proc. IEEE International Joint Conference on Neural Networks, pp. 2529–2533, 2004.

- [37] D. Donoho and V. Stodden, “When does non-negative matrix factorization give a correct decomposition into parts?,” in Advances in Neural Information Processing Systems 16 (S. Thrun, L. Saul, and B. Schölkopf, eds.), Cambridge, MA: MIT Press, 2004.

- [38] N.-D. Ho, Nonnegative matrix factorization algorithms and applications. PhD thesis, Université Catholique de Louvain, 2008.

- [39] M. E. Tipping, “Sparse Bayesian learning and the relevance vector machine,” Journal of Machine Learning Research, vol. 1, pp. 211–244, 2001.

- [40] D. P. Wipf, B. D. Rao, and S. Nagarajan, “Latent variable Bayesian models for promoting sparsity,” IEEE Transactions on Information Theory, vol. 57, pp. 6236–55, Sep 2011.

- [41] R. Salakhutdinov and A. Mnih, “Probabilistic matrix factorization,” in Advances in Neural Information Processing Systems, vol. 19, 2007.

- [42] A. Lefèvre, F. Bach, and C. Févotte, “Online algorithms for nonnegative matrix factorization with the Itakura-Saito divergence,” in Proc. IEEE Workshop on Applications of Signal Processing to Audio and Acoustics (WASPAA), (Mohonk, NY), Oct 2011.

- [43] J. Mairal, F. Bach, J. Ponce, and G. Sapiro, “Online learning for matrix factorization and sparse coding,” Journal of Machine Learning Research, vol. 11, pp. 10–60, 2010.

![[Uncaptioned image]](/html/1111.6085/assets/x16.png) |

Vincent Y. F. Tan did the Electrical and Information Sciences Tripos (EIST) at the University of Cambridge and obtained a B.A. and an M.Eng. degree in 2005. He received a Ph.D. degree in Electrical Engineering and Computer Science from MIT in 2011. After which, he was a postdoctoral researcher at University of Wisconsin-Madison. He is now a scientist at the Institute for Infocomm Research (I2R), Singapore and an adjunct assistant professor at the department of Electrical and Computer Engineering at the National University of Singapore. He held two summer research internships at Microsoft Research during his Ph.D. studies. His research interests include learning and inference in graphical models, statistical signal processing and network information theory. Vincent received the Charles Lamb prize, a Cambridge University Engineering Department prize awarded to the student who demonstrates the greatest proficiency in the EIST. He also received the MIT EECS Jin-Au Kong outstanding doctoral thesis prize and the A*STAR Philip Yeo prize for outstanding achievements in research. |

![[Uncaptioned image]](/html/1111.6085/assets/x17.png) |

Cédric Févotte obtained the State Engineering degree and the PhD degree in Control and Computer Science from École Centrale de Nantes (France) in 2000 and 2003, respectively. As a PhD student he was with the Signal Processing Group at Institut de Recherche en Communication et Cybernétique de Nantes (IRCCyN). From 2003 to 2006 he was a research associate with the Signal Processing Laboratory at University of Cambridge (Engineering Dept). He was then a research engineer with the music editing technology start-up company Mist-Technologies (now Audionamix) in Paris. In Mar. 2007, he joined Télécom ParisTech, first as a research associate and then as a CNRS tenured research scientist in Nov. 2007. His research interests generally concern statistical signal processing and unsupervised machine learning and in particular applications to blind source separation and audio signal processing. He is the scientific leader of project TANGERINE (Theory and applications of nonnegative matrix factorization) funded by the French research funding agency ANR and a member of the IEEE “Machine learning for signal processing” technical committee. |