Introducing the Adaptive Convex Enveloping

Abstract

Convexity, though extremely important in mathematical programming, has not drawn enough attention in the field of dynamic programming. This paper gives conditions for verifying convexity of the cost-to-go functions, and introduces an accurate, fast and reliable algorithm for solving convex dynamic programs with multivariate continuous states and actions, called Adaptive Convex Enveloping. This is a short introduction of the core technique created and used in my dissertation, so it is less formal, and misses some parts, such as literature review and reference, compared to a full journal paper.

Background Story

One of my friends has a small firm that designs electric vehicle battery stations. A battery station works like a gas station: customers arrive to replace their used batteries with full ones and leave, and it is the battery station’s job to charge the batteries in order to serve new customers. However, the electricity price fluctuates during the day. The battery station certainly wants to charge the batteries when the price is low, but it still has to satisfy customer demand. I wanted to help my friend develop an optimal charging policy, which is a typical dynamic program, with multivariate continuous states and actions. However, current ADP methods are not very satisfying when solving this class of problems. For example, algorithms generally require finding the optimal policy under the current approximations of the cost-to-go functions, but the approximations are in general not convex, sometimes very wavy, which makes finding the optimal policy difficult in multivariate problems. Also, even a method is proved to converge under certain conditions, one generally doesn’t know how the current policy compares to the true optimal one. To better solve this class of problems, I devised this new method — Adaptive Convex Enveloping (A.C.E.).

Formulation

Let the time periods be . Let , and be vectors that represent the state, the action and the random information at stage , respectively. Let , , be the cost-to-go function:

| s.t. | (1) |

where is a known function of the cost in period , is a set of constraints on the action , given the current state , and is the state transition function.

Assumptions

-

•

is known and convex;

-

•

The state domain , , is closed, bounded and convex;

-

•

The cost function with fixed, and the constraints , , are jointly convex on ;

-

•

If the constraints are not all linear, then the set must have a relative interior point;

-

•

The transition is linear, i.e., , where and are known matrices; nonlinear transitions are not investigated;

-

•

The distribution of is known, and is independent with and .

Convexity of the Cost-to-go Functions

A convex approximation is only desirable when the target function is convex. So first we have a look at the cost-to-go function. Indeed, the convexity of the cost-to-go functions is a direct extension of the results from Fiacco and Kyparisis’ paper Convexity and Concavity Properties of the Optimal Value Function in Parametric Nonlinear Programming (1986). Note that our action is their decision variable , our state is their parameter , and our cost-to-go function is their optimal value function .

If is convex, then for any realization of , is jointly convex on by our assumptions on and the transition, and so is . Since is a convex set, and constraints , , are jointly convex on , the point-to-set map is convex on by Proposition 2.3 from Fiacco and Kyparisis (1986). Then by their Proposition 2.1, is convex on .

Since is convex, the above argument implies that is convex for all .

Convex Enveloping of the Cost-to-go Functions

Since the cost-to-go functions are convex, we can use supporting hyperplanes as their (outer) approximations. Assume that has been investigated at , where we know the function value , as well as a subgradient (with abuse of the notation). Thus for any point , we know from convexity that

and is approximated as

We now show how to efficiently obtain and to approximate .

Select a sample from the theoretical or the empirical distribution of , and rewrite (1) as

| s.t. | (2) |

If is discrete and the set of it’s possible values is small, we can select all of its possible values as ; otherwise will have to be a sample from the distribution. The error introduced by this sampling will not be considered in this paper, and (2) will be treated as the definition of .

To obtain and at a point , we need to solve an optimization problem. Substitute with its approximation . To simplify the evaluation of , we replace it with a decision variable , and add the supporting hyperplane constraints (linear):

| s.t. | |||

The above formulation allows us to get , but to obtain , we need to change it a bit. We introduce decision variable as a dummy of :

| s.t. | ||||

| (3) |

Solving (3) not only gives us , which is the optimal objective value, but our assumptions also guarantee that there exists a Lagrange multiplier vector associated to the constraint , and that (or , depending on how you write the Lagrangian function) is a subgradient of at . Thus we can obtain for free by looking at the Lagrange multiplier of the constraint .

Note that approximating a function with supporting hyperplanes preserves convexity, thus (3) is a convex program, and any local minimum is also a global minimum.

Adaptive Convex Enveloping

We just showed how to efficiently obtain and to build supporting hyperplanes to approximate , but we haven’t discussed where to build these hyperplanes. From the geometric point of view, the flatter the function in a region, the less supporting hyperplanes needed, vice versa. In principle, we want to be as economical as possible, because each supporting hyperplane will add a number of linear constraints to (3) in stage . Without prior knowledge of , presetting the investigation points could be wasteful in supporting hyperplanes where the function is flat, and insufficient where the function is very curved.

The approach used by A.C.E. — the reason why it got the name — is to learn the shape of on the way, adding supporting hyperplanes only where necessary.

Error Control

The supporting hyperplanes give a lower bound of at any , and the convexity of can give an upper bound — together they provide an error bound.

Suppose that our state variable is 1-dimensional and look at Figure 1. We have two tangents added at and , respectively. By convexity, for , must be above the two tangents, and below the segment connecting the two points of tangency. Thus if we use the max of the tangents as the approximation of , the maximum potential error at is the vertical distance from the max of the tangents to the segment connecting the two points of tangency. And the error of any point in the region is bounded by the maximum potential error at the intersection of the two tangents.

In general, suppose that the domain is a -dimensional body, and let be points whose convex hull is also -dimensional. If we add supporting hyperplanes at , (), and use the max of these hyperplanes as the approximation of , then for any , the maximum potential error is the vertical distance from the max of the supporting hyperplanes to the hyperplane defined by the points . The maximum potential error for the region can be found by expressing the point as a convex combination of and solving the following maximization problem:

| s.t. | ||||

| (4) |

There are two facts that may counter one’s intuition when . First, the intersection of the supporting hyperplanes at may not be in ; it may not be in , too, even when . Second, a supporting hyperplane at , , can be an active lower bound, even when . These are the reasons why we need to solve (4) to find the potentially worst point , and why we use all the supporting hyperplanes as constraints.

Recursive Partitioning

Let the optimal solution of (4) be . The point is where the maximum potential error could occur. If this potential error is larger than the tolerance, we can add a supporting hyperplane at to reduce the error, and separate at into smaller convex hulls, each with and points from as vertices (See Figure 2). Then we face subregions whose maximum potential errors can be found by solving (4) again. Note that if is on a facet or an edge of , some of the subregions will be less than -dimensional. We ignore any subregion that is less than -dimensional, as it is covered by the other -dimensional subregions. We can tell if a subregion is -dimensional by looking at .

To initiate the recursive partitioning algorithm, we need to have initial vertices that satisfy two conditions: 1, their convex hull contains ; 2, the feasible action sets , , are nonempty. The first condition is for controlling the error at any point of , while the second condition is needed so that we can build supporting hyperplanes at these vertices. These points are usually not hard to find. For example, if the states have constraints , , one may want to check the intersections of the hyperplanes , , and to see if they satisfy the second condition. However, it’s not guaranteed that these points always exist or are always easy to find. If one really cannot find these points and has no way around it, then one may want to make some compromise and choose that satisfy the second condition and their convex hull covers as much of as possible.

Once we have the initial convex hull to start the algorithm, we separate it into sub-hulls if its maximum potential error exceeds the tolerance. Repeat this procedure recursively to all the sub-hulls, until all of their maximum potential errors are less than or equal to the tolerance.

-

Loop t from T-1 to 1

-

Read supporting hyperplane information from file;

Find initial vertices ;

Add supporting hyperplanes at by solving (3);

Form the first item of the section list with ;

currentMaxError = tolerance + 1;

While (currentMaxError > tolerance)

-

If (list size > Budget)

-

Print ‘‘Budget exceeded.’’;

Break;

End

currentMaxError = 0;

iterator = beginning of the list;

While (iterator != end of the list)

-

Solve (4);

currentMaxError = max(currentMaxError, optimal value of (4));

If (optimal value of (4) < tolerance)

-

iterator++;

Else

-

Solve (3);

Add a new supporting hyperplane at ;

Separate the current section at to subsections;

tmp_iterator = iterator;

iterator++;

Replace tmp_iterator with new subsections;

End

-

End

-

End

Write supporting hyperplane information to file;

Release memory;

-

End

-

Algorithm 1 shows how to solve the dynamic program with recursive partitioning. In the algorithm, we call a convex hull a “section”, and we use a list of sections. The beginning of a list is the list’s first item, while the end of a list is a position beyond the last item. An iterator of a list is like a pointer that points to an item of the list. The “++” operator points the iterator to the next item, but if iterator is the last item of the list, “iterator++” will point it to the end of the list, i.e., a position beyond the last item.

Note that the error we talk about here is the error of relative to . The absolute error of is the error relative to plus the absolute error of .

Approximating by Importance

Theoretically, we can approximate a function to any arbitrary high precision by reducing the tolerance. In practice, however, doing so to a high dimensional function is prohibitive. Meanwhile, pursuing a high precision at every point in could be wasteful, since in many applications the optimal policy tends to guide the process to visit frequently only a small portion of the domain. Therefore it is reasonable to only focus on these more important small portions.

We don’t know where these small portions are beforehand, however. What we could do is to use recursive partitioning to obtain affordable and relatively good approximations of the cost-to-go functions, and use simulation to see where the policy guides the process. The following is one possible way to update the approximations by importance.

-

Observe state path under the currect policy;

Loop t from T-1 to 1

-

Find the section that contains ;

If (maximum potential error > tolerance)

-

Add a supporting hyperplane at ;

Separate the current section at ;

End

-

End

-

This refining process can run as long as needed. Note that this recursive partitioning & approximating by importance approach bypasses the exploration vs. exploitation dilemma, which troubles many of today’s popular ADP methods.

Example

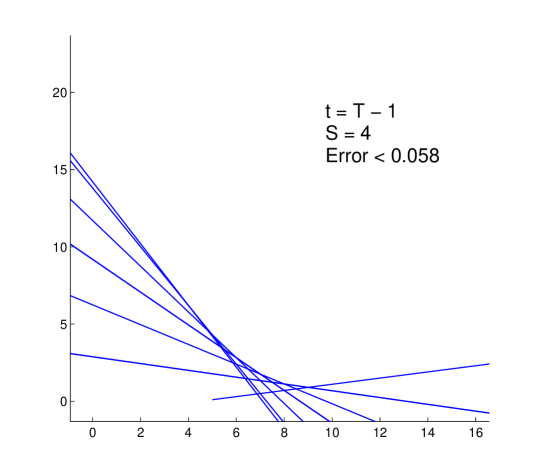

Here is a demonstration that applies A.C.E. to the well-known inventory control problem. Let the purchasing cost, penalty and holding cost be 2.0, 4.0 and 0.2, respectively. Let the demand be uniform on , and let the sample be 0.0, 0.1,,9.9. The cost-to-go function is known to be convex, which also could be confirmed by checking the convexity conditions given at the beginning of this paper. The optimal policy is well known, that is, to order and increase the inventory up to a level , but the value of is not known, and need to be computed numerically.

The following are the approximations given by A.C.E. for , from to , at tolerance = 0.1. is assumed to be zero.

The approximation of is shown by Figure 3. The optimal policy is to order up to . For the region and , we know should be linear, and we see A.C.E. didn’t waste supporting hyperplanes (tangents) there. For the region , it can be shown that is quadratic under a demand from uniform distribution, and the approximation reflects the shape closely. Overall, the approximation has an error less than 0.058 at any point .

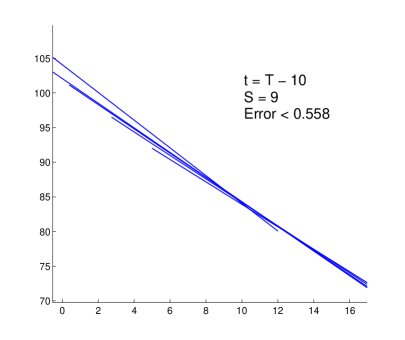

Figure 4 shows the approximations of and . The optimal policy at stage is to order up to . Starting (backwards) from stage , the optimal policy becomes fixed, and we always order up to . The error accumulates. At stage , the error bound for a point is 0.558. But, the cost-to-go accumulates, too, and compared to the scale of this target, the error is pretty small.

The whole process took 0.87 second on my computer. Since this is a simple 1-dimensional example, approximating by importance is not needed.

Features of A.C.E.

-

•

Solves convex DP with multivariate continuous states and actions;

-

•

It is a standardized, general purpose method (no parameter tunning, basis function choosing, kernel designing, etc.);

-

•

No assumption on the form of the cost-to-go functions — the form is learned on the way;

-

•

Implementation of mathematical programming allows large number of action variables;

-

•

The supporting hyperplane approximation preserves convexity of the cost-to-go functions, enabling reliable optimization;

-

•

The supporting hyperplane approximation also “ignores” the state variables that do not add to the nonlinearity of the target function, e.g., approximating is no more difficult than approximating , although the dimension is higher;

-

•

The computation is relatively light since we obtain the subgradients for free from the Lagrange multipliers.

-

•

The supporting hyperplanes are constructed economically by need and importance, further reducing the computation;

- •

-

•

We know an upper bound (not the big- notation) of the error between the approximated and the true cost-to-go functions at any state, thus we know how the policy performs;

-

•

There is no exploration vs. exploitation dilemma;

-

•

Compared to stochastic programming, it stands out when solving problems with long planning horizons, as the CPU time grows linearly in the number of stages, and memory consumption remains the same; plus, it is dynamic.