On Bidding with Securities: Risk Aversion and Positive Dependence00footnotetext: This work was supported by the National Science Foundation under Grant NSF ECCS 10-28464.

Abstract

DeMarzo et al. (2005) consider auctions in which bids are selected from a completely ordered family of securities whose values are tied to the resource being auctioned. The paper defines a notion of relative steepness of families of securities and shows that a steeper family provides greater expected revenue to the seller. Two assumptions are: the buyers are risk-neutral; the random variables through which values and signals of the buyers are realized are affiliated. We show that this revenue ranking holds for the second price auction in the case of risk-aversion. However, it does not hold if affiliation is relaxed to a less restrictive form of positive dependence, namely first order stochastic dominance (FOSD). We define the relative strong steepness of families of securities and show that it provides a necessary and sufficient condition for comparing two families in the FOSD case. All results extend to the English auction.

JEL classification: D44; D82; G00

1 Introduction

Consider auctioning an asset that is a resource to be developed for profit by the winning buyer. It is common in such auctions to require bids in the form of securities whose values to the seller are tied to the eventual realized value of the asset. As an alternative to simply soliciting cash bids for the asset, for instance, a seller may require buyers to compete in terms of the equity share that the seller retains of the asset’s profits. Other common securities used in bidding include debt and call options. DeMarzo et al. (2005) develop a general theory of bidding with securities in the first price and the second price auctions. Bids are selected from a completely ordered family of securities and the paper focuses on the importance of the choice of the family of securities to the seller’s expected revenue. The paper defines a partial ordering of families based on the notion of steepness (to be made precise in Section 3) and shows that the steeper family of securities provides higher expected revenue to the seller. Two assumptions are made to prove this result: (i) buyers are risk-neutral; (ii) the random variables through which values and signals of the buyers are realized are affiliated. Risk neutrality is a severe restriction for a financial model. Affiliation is an extremely restrictive form of positive dependence.111de Castro (2010) shows that the set of affiliated probability density functions for two random variables is the complement of an open and dense set in the space of continuous probability density functions under an appropriate topology and has zero measure under an appropriate measure.

Our objective in this paper is to explore in the case of the second price auction the dependence of the revenue ranking of families of securities upon these two assumptions.222In addition to the second price auction, DeMarzo et al. (2005) also rank families of securities in the case of the first price auction. An additional restriction on the set of securities and the dependence of values and signals beyond affiliation is required in this analysis (i.e., the log-supermodularity of each buyer’s expected profit, which is Assumption C in the paper). Our interest in this paper is in exploring the effect of relaxing the assumption of affiliation and not restricting it further. We have not been able to carry out the analysis for the first price auction at this level of generality. We do, however, discuss the extension of our results in Section 5 to the commonly used English auction, which is not considered in DeMarzo et al. (2005). We work with a symmetric interdependent values model on the lines of Milgrom and Weber (1982) and risk averse buyers. We consider two additional forms of positive dependence, namely, a monotone likelihood ratio (MLR) property, which is weaker than affiliation;333DeMarzo et al. (2005) assume the MLR property for the case of independent private values and affiliation for the case of interdependent values. For independent private values, the MLR property and affiliation are equivalent. and a first order stochastic dominance (FOSD) property, which is weaker than the MLR property. FOSD captures the idea that the observation by a bidder of a higher signal makes larger values of the other variables more likely. The additional restriction to either MLR or affiliation is attributable to their mathematical value and is typically not motivated in any practical sense. Each of these three positive dependence assumptions has been extensively used in both auction theory and information economics.

Our main results are the following:

-

(i)

A steeper family of securities provides higher expected revenue to the seller even with risk averse buyers and assuming that the values are positively dependent on signals in the MLR sense. We in this sense extend the result of DeMarzo et al. (2005) to the case of risk aversion and a richer informational environment.

-

(ii)

We show with an example that if the notion of positive dependence among values and signals of buyers is relaxed further from MLR to FOSD, then even for risk neutral buyers the revenue ranking of families of securities of DeMarzo et al. (2005) no longer holds.

-

(iii)

We strengthen steepness to a property that we call strong steepness in order to rank families of securities in the case of FOSD and either risk neutral or risk averse buyers. Relative strong steepness is shown to be both necessary and sufficient for comparing two families of securities in this case: one family generates a higher expected revenue for the seller than a second family for all instances of our model satisfying FOSD if and only if it is strongly steeper than the second.

-

(iv)

Finally, we show that the above results extend to the case of the English auction.

It is worth emphasizing that DeMarzo et al. (2005) establish only sufficiency of relative steepness as a condition to rank two families of securities according to the revenue realized by them if affiliation is the notion of positive dependence. By contrast, we show that relative strong steepness is both necessary and sufficient for ranking two families of securities according to the expected revenue realized by them if FOSD is the notion of positive dependence. Furthermore, our proofs are more straightforward than those inDeMarzo et al. (2005) and do not require its strong regularity assumption on the probability density of return conditioned on a buyer’s signal. We accomplish this mainly by exploiting the properties of concave functions, which in particular is what allows the consideration of risk averse buyers in our analysis.

Our paper complements recent work concerning the impact of security choice on the seller’s expected profit from auctions. Che and Kim (2010), Kogan and Morgan (2010), and Jun and Wolfstetter (2012) study how the choice of security affects the incentives of the winning bidder in choosing either a level of investment or effort that in turn affects the expected return from the asset. The first case concerns adverse selection while the second concerns moral hazard among bidders. In each case, the ranking of securities based on the seller’s net expected profit does not agree with the ranking according to relative steepness in the sense of DeMarzo et al. (2005). None of these three papers, however, explore the effect of risk aversion or the role of the positive dependence assumption in their assessment of security bids.

This paper is organized as follows. Section 2 outlines our model, notation, and definitions. Section 3 extends the revenue ranking of families of securities of DeMarzo et al. (2005) to risk averse buyers. Section 4 shows that this ranking is not preserved under a more general form of positive dependence, i.e., FOSD. The revenue ranking of families of securities based on strong steepness is then presented. Section 5 provides a brief overview of how the results of Sections 3 and 4 extend to the case of the English auction. We conclude in Section 6.

2 Model, Notation, and Assumptions

Consider buyers competing for a resource that a seller wants to sell. Each buyer has a value for the resource that is unknown to him; however, each buyer has some information (signal) about the value of the resource. The signal of a buyer is known only to him, but it may be informative to other buyers in the sense that it may improve their respective estimates of the value of the resource.

We model this by assuming that the value of the resource to a buyer , denoted by , is a realization of a nonnegative random variable , unknown to him. This is the profit to buyer from developing the resource in the absence of any payments to the seller but after taking into account the variable costs. A buyer privately observes a signal through a realization of a random variable that is correlated with . A winning buyer needs to invest a fixed amount , which is the same for each buyer, to develop the resource. We allow for negative values of ; a negative value represents a subsidy by a third party that goes to the winner to help develop the resource. As in DeMarzo et al. (2005), we assume that the realization of is observed ex-post by the seller and buyer if buyer wins and subsequently uses the resource. The joint cumulative distribution function (CDF) of the random variables ’s and ’s is common knowledge.

Let denote a vector of values and let the random vector be denoted by . A vector of signals and the random vector are defined similarly. We use the standard game theoretic notation of , and similarly for , , and .

Let denote the joint CDF of . It is assumed to have the following symmetry property:

Assumption 1.

The joint CDF of , denoted by , is identical for each and is symmetric in its last arguments (i.e., in the coordinates of ).

Assumption 1 allows for a special dependence between the value of the resource to a buyer and his own signal, while the identities of other buyers are irrelevant to him. The model reduces to the independent private values model if is independent of for all , to the pure common value model if , and includes a continuum of interdependent value models between these two extremes. Because of Assumption 1, the subsequent assumptions and analysis are given from buyer ’s viewpoint.

The set of possible values that each can take is assumed to be an interval and the set of possible values that each can take is assumed to be an interval . Assume that the joint probability density function (pdf) of the random vector , denoted by , exists and is positive for all . By Assumption 1, is symmetric in its arguments. Define the random variable as the largest among , i.e., ; denote a realization of by .

It is commonly assumed in auction theory that the observation of a larger signal corresponds to more favorable estimates of the value of the resource. This is captured by first order stochastic dominance. The specific property that we need in our analysis of the second price auction is as follows:

Definition 1 (FOSD).

The random variable is positively dependent on the random variables in the first order stochastic dominance (FOSD) sense if for any , is nondecreasing in and , where is the CDF of conditioned on and .444With the exception of the discussion of English auctions in Section 5, the properties “FOSD” and “MLR” in this paper specifically concern positive dependence of with respect to

The following characterization of FOSD is well known:

Lemma 1.

FOSD is equivalent to being nondecreasing in and for any nondecreasing function for which the expectation exists.

The monotone likelihood ratio property and affiliation are two more restrictive notions of positive dependence among variables that are also commonly used in auction theory. The versions that we use here are as follows:

Definition 2 (MLR).

Assume that for any and , the pdf of conditioned on and , denoted by , exists and is positive everywhere on . The random variable is positively dependent on the random variables in the monotone likelihood ratio (MLR) sense if is nondecreasing in for any and .

Definition 3 (Affiliation).

Assume that the joint pdf of , denoted by , exists and is positive everywhere on . The random variables are affiliated if

for any and in the support of . Here “” denotes coordinatewise maximum and “” denotes coordinatewise minimum.

Under Assumption 1, the following relationship between affiliation, MLR, and FOSD holds:555Assumption 1 is used in showing that if the random variables are affiliated then so are the random variables ; see Milgrom and Weber (1982). Lemma 2 then follows from the known relationship between affiliation, MLR, and FOSD; see, e.g., Chapter of Shaked and Shanthikumar (2006) and Appendix D of Krishna (2002).

Lemma 2.

Affiliation implies MLR and MLR implies FOSD.

Our focus is on comparing MLR and FOSD. Lemma 2 implies that results obtained by assuming FOSD hold if MLR is assumed instead, and results obtained by assuming MLR hold if affiliation is assumed instead. It is common in auction theory to justify the assumption of either affiliation or the MLR property by citing either the defining property of FOSD or the property that characterizes it in Lemma 1.666Quoting Milgrom and Weber (1982):“Roughly, this (affiliation) means that a high value of one bidder’s estimate makes high values of the others’ estimates more likely.” This appealing intuition for affiliation, however, suggests the shifting of a probability distribution with the observation of a higher estimate as in first order stochastic dominance and not the inequality that defines affiliation. de Castro (2010) provides some additional examples and references where affiliation is used to obtain important results in economics and finance. The relationship in Lemma 2, however, does not go in the reverse direction: affiliation is strictly stronger than MLR,777In the case of second price auctions, affiliation among and is unnecessary; all that is needed for the analysis of Milgrom and Weber (1982) is affiliation among , , and . Even this weaker form of affiliation, however, is strictly stronger than the MLR property we use in this paper. Affiliation among , , and implies that an MLR ordering property holds for any possible conditioning among these variables, e.g., etc.; the MLR property we use constrains only the conditioning In particular, it does not require that and be affiliated. For example, the MLR property holds under the following assumptions: the signals have any symmetric joint pdf; a common value is assumed (so for all ); is conditionally independent of given where denotes the maximum of the signal values; and the conditional distribution of given is nondecreasing (in the MLR order as a distribution for ) with respect to That is so because is then a nondecreasing function of (namely, ) and, in turn, the conditional distribution of is MLR nondecreasing in and, as discussed further in Section 4, MLR is strictly stronger than FOSD.

The buyers are assumed to be risk averse or risk neutral. Each buyer has the same von Neumann-Morgenstern utility of money, denoted by , which is concave (possibly linear), increasing, and normalized so that . Henceforth, the term risk averse includes risk neutral behavior. The seller is risk neutral. Conditioned on any and , the expected utility of the resource to buyer without any payments is assumed to be positive, i.e., . Thus, the buyers who compete for the resource expect to make a positive profit from utilizing it.

As in DeMarzo et al. (2005), buyers bid with securities from some ordered family. Let be a family of securities parametrized by . A bid of buyer denotes his willingness to pay an amount to the seller if . The interval can be normalized to any arbitrary closed interval, independently of , by translation and rescaling of the parameter in . It is therefore without loss of generality that we assume all families are parametrized by the same interval . The family is assumed to satisfy the following conditions:

Assumption 2.

For any , is continuous and nondecreasing in , and is nondecreasing and nonconstant in .

Assumption 2 implies that the payment made to the seller and the profit of the winning buyer are both nondecreasing in the realized value of the resource.

Assumption 3.

For any and ,

-

(i)

is continuous and decreasing in , nonnegative for , and nonpositive for .

-

(ii)

is continuous and increasing in .

Assumption 3 says that the family of securities is completely ordered from the perspectives of both the winning buyer and the seller, independently of the realized signal vector. Buyers prefer lower security bids and the seller prefers higher security bids. Assumption 3 is satisfied if, e.g., for any , is increasing in . The seller uses the second price auction where the highest bidder wins and pays the security bid of the second highest bidder. As discussed in the next section, continuity together with the boundary conditions in Assumption 3(i) guarantee the existence of a pure strategy equilibrium for the second price auction. Notice that Assumption 3(i) restricts the possible values of , e.g., if for all and then .

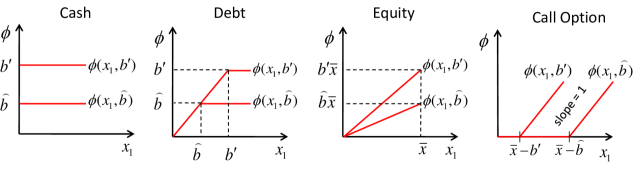

Some common families of securities that satisfy Assumptions 2 and 3 are: cash ; debt ; equity for some small ; and call option . These families of securities are shown in Figure 1.

3 Risk Aversion

This section extends the result of DeMarzo et al. (2005) on revenue ranking of families of securities to risk averse buyers. In a second price auction, a buyer decides how much to bid solely based on his signal . We look for a symmetric equilibrium. We start by defining a function that will be used to characterize the bidding strategies of the buyers:

| (1) |

The uniqueness of in (1) follows from Assumption 3. The value is the security bid that makes buyer indifferent between acquiring and not acquiring the resource given his signal and the highest signal of the other buyers. Notice that the bid corresponds to buyer ’s willingness to pay an amount to the seller if . The next lemma characterizes an important property of the function .

Lemma 3.

Assuming FOSD, the function is nondecreasing in and .

Proof.

To simplify the analysis in the rest of this paper, we reinforce Lemma 3 with the following additional assumption:

Assumption 4.

The family of securities and the informational environments are such that the function is increasing in .

Assumption 4 simplifies the analysis in this paper by insuring that ties among equilibrium bids (as specified in Lemma 4 below) occur with probability zero. We therefore ignore the possibility of ties in the remainder of the paper, except in footnote 9 later in this paper. Assumption 4 is satisfied in most cases of interest; e.g., since is assumed to be nondecreasing and nonconstant in , if for any , is increasing in , then Assumption 4 is automatically satisfied. The results of this paper hold without Assumption 4 under uniform tie breaking, though the analysis is more complicated.

The next lemma characterizes an equilibrium bidding strategy for the second price auction with bids restricted to the family . The construction of the bidding strategy follows Milgrom and Weber (1982).

Lemma 4.

Let the strategies of the buyers be identical and defined by for all . Assuming FOSD, the strategy vector is a symmetric Bayes-Nash equilibrium of the second price auction with bids restricted to the family .888Our analysis and results are only for the symmetric model and for a symmetric equilibrium that is monotone, as is customary in the auction theory literature. The literature is sparse in the case of asymmetry and the results obtained in the symmetric case need not apply to the asymmetric case; see Chapter of Krishna (2002) for further details.

Proof.

Assume that each buyer except buyer uses the strategy . We will show that the best response for buyer is to use the strategy .

Because of symmetry, the seller’s expected revenue equals the expected payment made by buyer conditioned on him winning. In the symmetric equilibrium given by Lemma 4, the bid of buyer is the highest if and only if his signal is the highest among all the buyers (i.e., ). If buyer wins, his payment is determined by the second highest security bid (i.e., . Thus, the seller’s expected revenue from the second price auction with bids restricted to the family is .999In the absence of Assumption 4, need not be increasing in and ties can occur with positive probability. However, if we assume uniform tie breaking, the seller’s expected revenue can still be shown to be , implying that it is enough to assume uniform tie breaking to preserve all the results in the paper and Assumption 4 can be dropped. To see this, notice that this is indeed the case if ties could be broken in favor of the buyer with the highest signal (which cannot be implemented because the seller cannot infer buyers’ signals from their bids if is not invertible in ). Let be an interval such that is constant for ; let be this constant. The event has the same probability as the event and for any outcome in either of these two events, the winning buyer pays the security bid .

We next reformulate the definition of steepness from DeMarzo et al. (2005) using the concept of quasi-monotonicity, as defined below:

Definition 4 (Quasi-monotone function).

A function is quasi-monotone if for any and such that , if then . A quasi-monotone function therefore crosses zero at most once and from below.

Definition 5 (Steepness).

A family of securities is steeper than another family of securities if for any , is quasi-monotone in .

Notice that call option is steeper than equity and debt, equity is steeper than debt, and all three of these families are steeper than cash (see Figure 1).101010Quasi-monotonicity is not transitive and hence steepness is not transitive. Proposition 1 provides a pairwise revenue ranking for any two families of securities that are ordered under the steepness criteria. This revenue ranking, however, is transitive.

Proposition 1 below states that steepness ordering is a sufficient condition under which two different families of securities can be ranked according to the revenue they generate. The proof is in Appendix A.

Proposition 1.

Let and be two families of securities such that is steeper than . Assuming MLR, the second price auction with bids restricted to generates at least as much expected revenue for the seller as the second price auction with bids restricted to .

A careful review of the proof of Proposition 1 shows that we in fact prove the stronger result that the expected revenue of the seller conditioned on the winning buyer’s signal and the second highest signal is at least as large in the case of the steeper family of securities as with the family . The revenue from the steeper family thus weakly dominates in this ex-post sense, which implies that it is weakly better for the seller ex-ante as stated in the proposition.

The following is an immediate consequence of Proposition 1:

Corollary 1.

Assuming MLR, the expected revenue from the following families of securities can be ranked as: cash debt equity call option.

4 Positive Dependence

This section addresses the role of the positive dependence assumption in the ranking of families of securities. An example is first discussed that shows that the ranking of Proposition 1 does not hold if MLR is relaxed to FOSD.111111Interestingly, the example assumes independent private values among the buyers; it does not rely upon interdependence of values and the problems of inference that it creates, which is commonly the source of problems in models of trading. The pairwise ranking of the three families of securities – debt, equity, and call options – is completely reversed in this example in comparison to the ranking in Corollary 1. If MLR is relaxed to FOSD, the relative steepness condition must be strengthened in order to rank two families of securities. This is accomplished by using the notion of strong steepness that we define below.

Example 1.

Consider two risk neutral buyers (i.e., ) with independent private values. Buyer ’s signal is uniformly distributed in the interval . Conditioned on , the random variable , denoting the value of buyer , has the following conditional pdf:

| (2) |

Figure 2 shows the plot of . The pairs are i.i.d. across the buyers. Since there are only two buyers with independent valuations, and . The CDF is given by:

| (3) |

Since for , is increasing in for and is constant in for . Thus, is positively dependent on in the FOSD sense and FOSD is satisfied (in this example, is independent of ). However, for , fails to be nondecreasing in ; the ratio is strictly greater than one for and is equal to one for . Thus, MLR is not satisfied.

Example 1 highlights the distinction between MLR and FOSD in the following sense. If the random variable is positively dependent on the random variable in the MLR sense (i.e., is nondecreasing in for any ), then conditioning on a larger shifts the probability distribution of towards the larger values of everywhere in the interval of possible values of . However, if the random variable is positively dependent on in the FOSD sense (i.e., is nondecreasing in for any ), then the shift of the probability distribution towards the larger values of when conditioned on a larger value of can be localized; in Example 1, a larger value of changes the probability distribution of only in the interval , making the values in close to more likely than the values close to , while the likelihood of the values of in the interval remains unchanged. Proposition 2 below uses this difference between MLR and FOSD to show that Example 1 violates the revenue ranking given by Corollary 1. The proof is in Appendix B.

Proposition 2.

For Example 1, there exists an interval of choices for the investment such that for any realization of the signal vector , the expected revenue to the seller from the second price auction with bids restricted to debt securities is higher than the expected revenue from bids restricted to equity securities.121212This ranking is robust to perturbations of the pdf in the sense so long as the corresponding perturbed CDF satisfies FOSD along with the other assumptions of this paper. A simple family of distributions and investment levels for which the ranking of debt over equity in Proposition 2 holds can be generated as follows. For given by (2), consider convex combinations of the form for and any pdf on . Such a pdf satisfies FOSD and our other assumptions because does not depend upon . It is straightforward to modify the proof of Proposition 2 to show the existence of , such that the ranking of debt over equity holds in the case of and investment for any and any pdf .

Recall that Corollary 1 ranks the revenue from four families of securities in the case of MLR as: cash debt equity call option. Numerical computation for Example 1 with investment results in the following values for the seller’s expected revenue: from cash bids ; from call option ; from equity ; and from debt . Thus, the ranking in Example 1 for is: cash call option equity debt. Notice that (i) cash is last in each ranking, and (ii) compared to Corollary 1, the relative pairwise ranking of debt, equity, and call option are reversed in this example. We show below in Corollary 2 that point (i) holds generally in the case of FOSD, i.e., call option, equity and debt all produce a greater expected revenue for the seller than cash bids in this case. The inferiority of cash bids relative to these other securities thus generalizes from MLR to FOSD. Because the distributions that satisfy MLR form a proper subset of those that satisfy FOSD, the two rankings above show that any ranking of any pair of the three families of securities of debt, equity and call options is possible within the family of distributions that satisfy FOSD. So arriving at a definite ordering among these three families requires restricting the dependence of signals and values beyond FOSD.

The next proposition gives a revenue ranking of families of securities that holds under FOSD with risk averse buyers. This is achieved by strengthening the steepness condition.

Definition 6 (Strong steepness).

A family of securities is strongly steeper than another family of securities if for any such that assumes both negative and positive values over , is nondecreasing in .

Notice that strong steepness implies steepness. Furthermore, debt, equity, and call option are all strongly steeper than cash.

Proposition 3.

The following statements hold:

-

(i)

Let and be two families of securities such that is strongly steeper than . Assuming FOSD, the second price auction with bids restricted to generates at least as much expected revenue for the seller as the second price auction with bids restricted to .

-

(ii)

Let and be two families of securities satisfying the following assumptions:

- (a)

-

(b)

For any , there is a finite set (possibly empty) such that for any and are continuously differentiable, as functions of two variables, in a neighborhood of

Then the family is strongly steeper than the family .

The proof of Proposition 3 is in Appendix C. By Assumption 2, and are differentiable in almost everywhere; and by Assumption 3, and are differentiable in with positive derivatives almost everywhere. The regularity condition (b) above imposes only mild additional smoothness requirements on the securities. In particular, this assumption is satisfied by cash, debt, equity, and call option.

As with Proposition 1, the proof of Proposition 3(i) establishes the stronger result that the seller’s expected revenue conditional on the two highest signals is larger for the strongly steeper family of securities. The following is an immediate consequence of Proposition 3(i):

Corollary 2.

Assuming FOSD, the expected revenue from debt, equity, or call option are at least as large as the expected revenue from cash.

It is instructive to compare the revenue ranking of Proposition 3(i) to the ranking in DeMarzo et al. (2005). Recall Example 1. As noted above, MLR shifts the distribution of across its support as increases while FOSD may only shift this distribution locally. Steepness is fundamentally a local condition that restricts how a security from one family crosses a security from another family (i.e., it crosses at most once and from below). MLR is a global notion of positive dependence that allows this local comparison of two families to determine a ranking based upon the seller’s expected revenue. In moving from MLR to FOSD, however, this ranking no longer holds. Steepness is replaced in Proposition 3(i) by strong steepness that compares two families of securities across the entire support of . DeMarzo et al. (2005) thus apply a local condition on families of securities together with a global condition on positive dependence in order to rank families of securities in terms of expected revenue. When the global condition on positive dependence MLR is weakened to the condition FOSD that may only bind locally, we must strengthen the comparison of the securities to a global condition that holds across the support of in order to be able to rank the families.

Application of Proposition 3(i) is illustrated further by the revenue ranking in Abhishek et al. (2013) of profit sharing securities, which are inspired by spectrum auctions in India. A fraction defines securities as follows. Setting , in the profit-loss security, the winning buyer’s payment to the seller consists of a cash bid along with an share of the return ,

In the profit-only security, the winning buyer’s payment to the seller consists of a cash bid along with an share of the return when it is positive but with no additional payment when it is not,

Let and denote respectively the families of profit-loss and profit-only securities that are determined by and indexed by the range of possible cash bids. It is straightforward to see that: (i) if , then is strongly steeper than and is strongly steeper than ; (ii) for fixed , is strongly steeper than . Proposition 3(i) then implies that the seller’s expected revenue in the second price auction with either profit-loss or profit-only securities is nondecreasing in the share , and for fixed the expected revenue is weakly higher with profit and loss sharing as compared to profit only sharing.

We conclude with intuition on why a strongly steeper family of securities generates a higher expected revenue for the seller in the case of risk neutral buyers. Let and denote two families of securities such that is strongly steeper than . Assume that so buyer wins regardless of whether bids are from or . Buyer in each case pays the bid of the buyer who observed signal . His ex-post payment is equal to if bids are from and the value of the resource is equal to , and the corresponding payment in the case of is . In our symmetric model with risk neutral buyers, and are bids that make buyer indifferent to winning conditioned on :

| (4) |

The seller would thus expect to receive the same revenue from the families and if the highest and the second highest signals are the same, i.e., . Buyer wins the auction, however, when his signal is greater than . His expected payment to the seller is therefore calculated conditioned on . Intuitively, FOSD means that a larger realized signal shifts the distribution of the return from the resource towards its larger values. This shift increases the expected payment to the seller from the strongly steeper family of securities more than that from because the ex-post payment to the seller increases more rapidly as a function of in the case of a steeper security. Compared to for which we have the equality (4), for we have

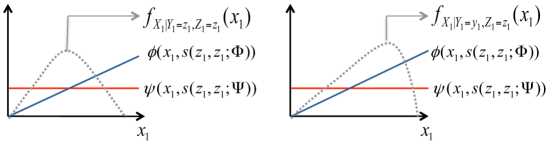

| (5) |

We depict this intuition in Figure 3 for the case in which represents equity shares and represents cash. The lines represent the equilibrium bids in these two families for a given value of . On the left is the density of conditioned on . Relative to this density, the expected value of the payments and are equal. On the right is the density of conditioned on and for . The expected value of exceeds the expected value of relative to this second density, reflecting both the shift of the density given the observation of the larger signal and the relative strong steepness of the two families of securities.

5 The English Auction

We summarize in this section the extension to the case of the English auction of all results from Sections 3 and 4 using strengthened versions of MLR and FOSD. The English auction is an ascending price auction with a continuously increasing price. At each price level, a buyer decides whether to drop out or not. The price level and the number of active buyers are publicly known at any time. The auction ends when the second to last buyer drops out and the winner pays the price at which this happens.

If bids are restricted to a family of securities, then the winning buyer pays the security bid at which the second to last buyer drops out. The security bids at which different buyers drop out allow the remaining buyers to infer the signals of those who have dropped out. A buyer’s bidding strategy thus takes into account the number of active buyers and the inferred signals of the other buyers who have dropped out. This requires modifying MLR and FOSD such that the random variable is positively dependent not only on and but on the entire vector of signals of the other buyers, i.e., on . With this modification, an equilibrium for the English auction with bids restricted to a family of securities can be characterized by following the construction of equilibrium for the English auction with cash bids in Milgrom and Weber (1982).131313See also Abhishek et al. (2013) concerning the English auction with a profit-sharing contract. Using this characterization of equilibrium, all proofs in this paper extend in a straightforward manner to the case of the English auction. In particular, the analysis in Example 1 of Section 4 holds for the English auction as well because it is strategically equivalent to the second price auction in the case of only two buyers.

6 Conclusions

DeMarzo et al. (2005) identify the relative steepness of two families of securities as the critical factor in determining which of the two families generates the higher expected revenue for the seller in the second price and the first price auctions. For the second price auction, we first generalize this ranking to include the case of risk averse buyers. We then demonstrate the dependence of this ranking on the underlying positive dependence assumption among values and signals. An example is provided in which positive dependence is relaxed from MLR to FOSD. The pairwise revenue ranking of common families of securities – debt, equity, and call options – is reversed in this example from the ranking of DeMarzo et al. (2005). The cause of this reversal is that positive dependence in the MLR sense globally restricts dependence while positive dependence in the FOSD sense may only restrict it locally; while the local condition of relative steepness is sufficient to rank families in the case of MLR, it must be strengthened in order to obtain a ranking under the less restrictive condition of FOSD. We achieve this by identifying relative strong steepness as a necessary and sufficient condition for comparing two families of securities in the case of FOSD. This result is significant because FOSD is the property that is most commonly cited in auction theory to motivate an assumption of positive dependence among values and signals. These results extend to the case of the English auction.

Appendix A Proof of Proposition 1

We start with the following definition:

Definition 7 (Single crossing).

A function single crosses a function from below if there exists such that for and for .

Lemma 5.

Let be a random variable taking values in some interval , and let for be nondecreasing functions with values in some interval . Let single cross from below and be a crossing point. Let be any concave function. Then the following holds:

-

1.

If , then .

-

2.

If and , then .

Proof.

The first claim is from Lemma of Ohlin (1969). We therefore turn to the second claim, the proof of which closely follows the proof of the first claim.

Define , , and let . Clearly, and are probability distributions. If , the event implies the event , hence . Similarly, if , the event implies the event , hence .

Since is concave, it is differentiable almost everywhere (in particular, the right and the left derivatives exist everywhere). Hence, , where can be taken as the right derivative of . For , regard as a random variable with probability measure . The expected value of reduces as follows:

Lemma 6.

Let a function single cross zero from below. Suppose for some and . Assuming MLR, for any .

Proof.

Since conditioning on plays no role in the above claim, for notational convenience define , which omits . Let be the point at which crosses zero from below. Since is increasing in , for , and for , we get

| (10) |

Then,

where the first inequality is from (10). This completes the proof. ∎

We can now prove Proposition 1. The seller’s revenue if bids are restricted to the family is and is if bids are restricted to the family . To prove Proposition 1, it suffices to show that for any ,

| (11) |

From (1), for any ,

| (12) |

If either or for all then (12) would not be true. Hence, and must cross each other as functions of . Since is steeper than , single crosses zero from below. This implies that single crosses from below. This, along with (12), and being concave and increasing, allow for an application of the second part of Lemma 5, and results in the following inequality:

| (13) |

Hence,

| (14) |

Since single crosses zero from below, (14) and Lemma 6 imply

| (15) |

for . This establishes (11) and the proof is complete. ∎

Appendix B Proof of Proposition 2

We first explain how the example was devised. Recall the statement of Lemma 6 from the preceding section. The proof of Proposition 1 is an application of Lemma 6 in which for any value of : (i) , where is a steeper family than ; (ii) equals ; (iii) Lemma 6 is applied to derive inequality (15), which is the conclusion that the expected payment by buyer in the event that he trades is greater with the family of securities than with . Example 1 is constructed with the goal of making this last step false so that the steeper family of securities produces a lower expected payment by buyer . The key observation is that while the function is assumed by Lemma 6 to single cross zero from below, this does not preclude from decreasing for values of below the point at which it crosses zero. In Example 1, a larger value of changes the probability density of only in the interval , making the values in closer to more likely and the values near less likely, while the probability density over remains unaffected. If is decreasing over , then conditioning on a larger value of can decrease the expected value of over and thereby reverse the conclusion of Proposition 1. As we show below, this in fact occurs for a range of values of the investment and for each realization of the signal vector in the case in which is the equity family and is the debt family.

We begin by choosing the investment parameter to ensure that the relevant in the case of debt and equity crosses zero at a value larger than . In the case of debt securities, the optimal bid of buyer when his signal equals zero is determined by the equation

| (16) |

With foresight to the use of below, we wish to ensure that the optimal bid of buyer when his signal equals zero exceeds . The left side of (B) is decreasing in and the right side is nondecreasing in . At and , the left side strictly exceeds the right side. As a consequence, we conclude that there is a value such that for all , the value of that solves (B) strictly exceeds . We therefore fix the investment at some value .

Consider an arbitrary realization of the signal vector such that buyer wins, i.e., . Given , let denote the bid of buyer when he bids with debt securities and his bid when he bids with equity securities. It is sufficient to prove that

| (17) |

where the left hand side denotes the seller’s expected revenue given in the case of equity securities and the right hand side denotes his expected revenue in the case of debt securities. We are using here the fact that is independent of in this example.

Appendix C Proof of Proposition 3

Proof of part (i):

The proof is almost the same as the proof of Proposition 1. The main difference is in how the concluding inequality that ranks the expected payments of the winning buyer under different families of securities is derived using FOSD and strong steepness instead of MLR and steepness.

As in the proof of Proposition 1, it suffices to show that (11) holds for any . The argument in the proof of Proposition 1 implies that must cross as functions of . Strong steepness requires that is nondecreasing in and hence single crosses from below. Inequality (14) then follows by the same argument as before, implying:

The last inequality that proves the result is from an application of Lemma 1, using the fact that is nondecreasing in (i.e., strong steepness) together with FOSD. ∎

Proof of part (ii):

It suffices to consider only the case of two risk neutral buyers and satisfying FOSD such that the pairs for different buyers are independent and identically distributed. We also assume without loss of generality that the ’s are distributed over the interval

Suppose and are two families of securities satisfying conditions (a) and (b) of Proposition 3(ii). Let and be such that assumes both negative and positive values over . Let be a point in and let and . It suffices to prove that

For , let the function be defined by:

| (22) |

Note that

Since assumes both negative and positive values, there exists a pdf over that is continuously differentiable, strictly positive, and such that if random variable has this pdf, then . Define and let .

We describe joint distributions for , parameterized by , using the pdf and the function . The random variable is uniformly distributed over the interval and

| (23) |

In words, the conditional pdf of given is obtained from by shifting a small amount of probability mass, proportional to from just below to just above We shall only consider small enough that the conditional pdf is nonnegative and the rectangular set, (support of )(an open interval containing ), is contained in a set of continuous differentiability of , and the analogous condition holds for and For each such , satisfies FOSD. If , the signals are independent of the values and the pdf of is identical to the pdf of . By construction, . Assumption 3(ii) then implies that for and any , and . By the smoothness conditions in Proposition 3(ii), is continuous in . Hence, for small values of , our choice of and satisfy Assumption 3(i) for family . The same holds true for .

Let denote the expected revenue from the family of securities for parameterized random variables ; define similarly. By the assumed revenue ranking, for all being considered. If , both buyers bidding is the symmetric equilibrium for the family of securities , both buyers bidding is the symmetric equilibrium for the family of securities , and the revenue for each set of securities is . Hence, It will be shown below that the derivative of with respect to at zero satisfies . Similarly, . By the revenue ranking, we must have , implying . It remains to show that .

Consider the family The hypotheses imply that is continuously differentiable in both and for in a neighborhood of zero and in a neighborhood of Moreover,

| (24) | |||

| (25) |

where (25) is obtained by the Taylor series representation of centered at , for a fixed in a small neighborhood of . Here, . Equivalently,

| (26) |

Since the signal and value pairs are independent, the function , defined by (1) for , depends only on ; we write it is as It is characterized by the equation

For a given , (24), (26), and the smoothness conditions of Proposition 3(ii)(b) imply that the partial derivatives of with respect of and are continuous for in some small interval and in a small neighborhood of ; and the partial derivative with respect to is nonzero. By the implicit function theorem, is differentiable in and satisfies:

| (27) |

Notice that at , is independent of , for any , and and are identical in distribution. For notational convenience, define . Then from (26), (27) and continuity of derivatives,

| (28) |

and

| (29) |

Next, notice that

| (30) |

Since is continuously differentiable in and , and is differentiable in , is continuously differentiable in . Additionally, because ’s take values in finite interval , in order to compute the derivative of , we can take the derivative inside the outer expectation in (30).

where the second equality follows from (29). Therefore, as required. ∎

References

- Abhishek et al. (2013) V. Abhishek, B. Hajek, and S. R. Williams. Auctions with a profit sharing contract. Games and Economic Behavior, 77(1):247–270, 2013.

- Che and Kim (2010) Y.-K. Che and J. Kim. Bidding with securities: comment. The American Economic Review, 100(4):1929–1935, 2010.

- de Castro (2010) L. I. de Castro. Affiliation, equilibrium existence and revenue ranking of auctions. Working paper. Kellogg School of Management, Northwestern University, December 2010.

- DeMarzo et al. (2005) P. M. DeMarzo, I. Kremer, and A. Skrzypacz. Bidding with securities: Auctions and security design. American Economic Review, 95(4):936–959, 2005.

- Jun and Wolfstetter (2012) B. H. Jun and E. G. Wolfstetter. Security bid auctions for agency contracts. Working paper, January 2012.

- Kogan and Morgan (2010) S. Kogan and J. Morgan. Securities auctions under moral hazard: An experimental study. Review of Finance, 14(3):477–520, 2010.

- Krishna (2002) V. Krishna. Auction Theory. Academic Press, March 2002.

- Milgrom and Weber (1982) P. R. Milgrom and R. J. Weber. A theory of auctions and competitive bidding. Econometrica, 50(5):1089–1122, 1982.

- Ohlin (1969) J. Ohlin. On a class of measures of dispersion with application to optimal reinsurance. Astin Bulletin, 5:249 –266, 1969.

- Shaked and Shanthikumar (2006) M. Shaked and G. J. Shanthikumar. Stochastic Orders (Springer Series in Statistics). Springer-Verlag, New York, October 2006.