Efficient Nonparametric Conformal Prediction Regions

Abstract

We investigate and extend the conformal prediction method due to Vovk, Gammerman and Shafer (2005) to construct nonparametric prediction regions. These regions have guaranteed distribution free, finite sample coverage, without any assumptions on the distribution or the bandwidth. Explicit convergence rates of the loss function are established for such regions under standard regularity conditions. Approximations for simplifying implementation and data driven bandwidth selection methods are also discussed. The theoretical properties of our method are demonstrated through simulations.

keywords:

[class=AMS]keywords:

math.PR/0000000 \startlocaldefs \endlocaldefs

, and

t1Supported by NSF Grant BCS-0941518. t3Supported by NSF Grant DMS-0806009 and Air Force Grant FA95500910373.

1 Introduction

1.1 Prediction regions and density level sets

Consider the following prediction problem: we observe iid data from a distribution and we want to construct a prediction region such that

| (1.1) |

for fixed where is the product probability measure over the -tuple .111In general, we let denote or depending on the context. This is equivalent to where is the probability mass of the random set . In other words, traps a future independent observation with probability at least . The random set is called a -prediction region or a -tolerance region. In this paper we will use the name “prediction region” for consistency of presentation while “tolerance region” is often used as a synonym in the literature.

Prediction is a major focus of machine learning and statistics although the emphasis is often on point prediction. Prediction regions go beyond merely providing a point prediction and are useful in a variety of applications including quality control and anomaly detection. For example, suppose a sequence of items is being produced or observed. If one item falls out of the prediction region constructed from the previous samples, it indicates that this item is likely to be different from the rest of the sample and some further investigation may be necessary.

Another application of prediction regions is data description and clustering. Given a random sample from a distribution, it is often of interest to ask where most of the probability mass is concentrated. A natural answer to this question is the density level set , where is the density function of . When the distribution is multimodal, a suitably chosen will give a clustering of the underlying distribution (Hartigan, 1975). When is given, consistent estimators of and rates of convergence have been studied in detail, for example, in Polonik (1995); Tsybakov (1997); Baillo, Cuestas-Alberto and Cuevas (2001); Baillo (2003); Cadre (2006); Willett and Nowak (2007); Rigollet and Vert (2009); Rinaldo and Wasserman (2010). It often makes sense to define implicitly using the desired probability coverage :

| (1.2) |

Let denote the Lebesgue measure on . If the contour has zero Lebesgue measure, then it is easily shown that

where the min is over . Therefore, the density based clustering problem can sometimes be formulated as estimation of the minimum volume prediction region.

The study of prediction regions has a long history in statistics; see, for example Wilks (1941); Wald (1943); Fraser and Guttman (1956); Chatterjee and Patra (1980); Di Bucchianico, Einmahl and Mushkudiani (2001); Cadre (2006); Li and Liu (2008). For a thorough introduction to prediction regions, the reader is referred to the books by Guttman (1970) and Aichison and Dunsmore (1975). In this paper we study a newer method due to Vovk, Gammerman and Shafer (2005) which we describe in Section 2.

1.2 Validity and efficiency

Let be a prediction region. There are two natural criteria to measure its quality: validity and efficiency. By validity we mean that has the desired coverage for all , whereas by efficiency we mean that is close to the optimal prediction region .

1.2.1 Validity

By definition, a prediction region is a function of the sample and hence its coverage is a random quantity. To formulate the notion of validity of a prediction region, Fraser and Guttman (1956) defined -prediction regions with -confidence for satisfying

| (1.3) |

However, evaluating the exact probability in the above definition is rarely possible. Most work on nonparametric prediction regions validate their methods using an asymptotic version (Chatterjee and Patra, 1980; Li and Liu, 2008):

On the other hand, if a procedure satisfies (1.1) for every distribution on and every , then we say that is a distribution free prediction region or has finite sample validity.

1.2.2 Efficiency

We measure the efficiency of in terms of its closeness to the optimal region . Recall that if has a density with respect to Lebesgue measure , then the smallest region with probability content at least is

| (1.4) |

where is given by (1.2), provided that the contour has zero measure. Since is unknown, cannot be used as an estimator but only as a benchmark in evaluating the efficiency. We define the loss function of by

| (1.5) |

where denotes the symmetric set difference. Such loss functions have been used, for example, by Chatterjee and Patra (1980) and Li and Liu (2008) in nonparametric prediction region estimation and by Tsybakov (1997); Rigollet and Vert (2009) in density level set estimation. Since,

it follows that the symmetric difference loss gives an upper bound on the excess loss

| (1.6) |

In Chatterjee and Patra (1980) and Li and Liu (2008), a prediction region is called asymptotically minimal if

| (1.7) |

However, such an asymptotic property does not specify the rate of convergence. While convergence rate results are available for density level sets estimation (see Tsybakov, 1997; Rigollet and Vert, 2009; Mason and Polonik, 2009, for example), relatively less is known about prediction regions until recently (Cadre, 2006; Samworth and Wand, 2010).

1.3 This paper

In this paper, we propose an efficient and easy to compute prediction region with finite sample validity and we study the rate of convergence of its loss. To be specific, we construct such that:

-

1.

satisfies (1.1) for all and all under no assumption other than iid.

-

2.

For any , there exist constants and independent of , such that

(1.8) for density satisfying some standard regularity conditions.

-

3.

For any , the computation cost of evaluating is linear in . In other words, checking to see if a point is in the prediction region, takes linear time.

The convergence rate of efficiency is described by the term . We give explicit formula of constant in terms of the global smoothness and the local behavior of near the contour at level . Its near optimality is discussed for some important special cases.

Our prediction region is obtained by combining the idea of conformal prediction (Vovk, Gammerman and Shafer, 2005) with density estimation. We first construct a conformal prediction region that is closely related to a kernel density estimator. The finite sample validity is inherited from the nature of conformal prediction regions. Then we show that such a region, whose analytical form may be intractable, is sandwiched by two kernel density level sets with carefully tuned cut-off values. Therefore the efficiency of the conformal prediction region can be approximated by those of the two kernel density level sets. As a by-product, we obtain a kernel density level set that always contains the conformal prediction region, and hence also satisfies finite sample validity. This observation means that, most of the time, a kernel density estimator will have near optimal efficiency, finite sample validity, and even lower computational cost at the same time. In the efficiency argument, we refine the rates of convergence for plug-in density level sets first developed in Cadre (2006), which may be of independent interest.

Our method involves one tuning parameter which is the bandwidth in kernel density estimation. We give two practical data driven approaches to choose the bandwidth and demonstrate the performance through simulations.

1.4 Related work

Our main technique for constructing prediction regions is inspired by the conformal prediction method (Vovk, Gammerman and Shafer, 2005; Shafer and Vovk, 2008), a general approach for constructing distribution free, sequential prediction regions using exchangeability. Although in its original appearance, conformal prediction is applied to sequential classification and regression problems (Vovk, Nouretdinov and Gammerman, 2009), it is easy to adapt the method to the prediction task described in (1.1). We describe this general method in Section 2 and our adaptation in Section 3.

In multivariate prediction region estimation, common approaches include methods based on statistical equivalent blocks (Tukey, 1947; Li and Liu, 2008) and plug-in density level sets (Chatterjee and Patra, 1980; Cadre, 2006). In methods based on statistical equivalent blocks, an ordering function taking values in is defined and used to order the data points. Then one-dimensional tolerance interval methods (e.g. Wilks, 1941) can be applied. Such methods usually give accurate coverage but the efficiency is hard to prove. In particular, Li and Liu (2008) proposed an estimator using the multivariate spacing depth as the ordering function. Such a method is completely nonparametric, requiring no tuning parameter, and is adaptive to the shape of the underlying distribution if the density level sets are convex. However, this method requires time to compute the indicator for any given , which is much higher comparing to methods based on plug-in density level sets. Moreover, it is not clear how this method performs when the level sets of underlying distribution are not convex. On the other hand, the methods based on plug-in density level sets (Chatterjee and Patra, 1980) gives provable validity and efficiency in asymptotic sense regardless of the shape of the distribution (Cadre, 2006), while requiring only time to compute the indicator function. The potential of such estimators has been reported empirically in Di Bucchianico, Einmahl and Mushkudiani (2001): “ … in principle the method based on density estimation can perform very well if a proper bandwidth is chosen, …”

Our approach, although originally inspired by conformal prediction, can be viewed as a combination of the ordering based method and the density based method, where the ordering function is given by the estimated density. This agrees with the simple fact that the best ordering function is just the density itself. To the best of our knowledge, this method is the first one with both finite sample validity and explicit convergence rates.

There are other methods for multivariate prediction regions. For example, Di Bucchianico, Einmahl and Mushkudiani (2001) proposed to minimize the volume over a pre-specified class of sets while maintaining a minimum coverage under the empirical distribution. This method works well for common distributions whose level sets can be well approximated by regular shapes such as ellipsoids and rectangles. However, its performance depends crucially on the pre-specified sets which cannot be very rich (must be a Donsker class), and hence cannot be guaranteed for arbitrary distributions. Moreover, the minimization problem may be non-convex and hence computationally intensive.

The rest of this paper is organized as follows. In Section 2 we introduce conformal prediction. In Section 3 we describe a construction of prediction region by combining conformal prediction with kernel density estimator. The approximation result (sandwiching lemma) and asymptotic properties are also discussed in Section 3. Practical methods for choosing the bandwidth are given in Section 4 and simulation results are presented in Section 5. Some closing remarks and possible future works are given in Section 6. Some technical proofs are given in Section 7.

2 Conformal prediction

We can construct a valid prediction region using a method from Vovk, Gammerman and Shafer (2005) and Shafer and Vovk (2008). Although their focus was on sequential prediction with covariates, the same basic idea can be used here. The method is simple: consider a “conformity measure” , which measures the “conformity” or “agreement” of a point with respect to a distribution . Examples of such a function in the multivariate case include data depth (see Liu, Parelius and Singh, 1999, and references therein), and the density function. For other choices of conformity measure, see the book by Vovk, Gammerman and Shafer (2005). Given an independent sample from , we test the hypothesis that using observation for each and invert the test. The test statistic is constructed using with replaced by empirical distribution .

When is a random sample from , let be the corresponding empirical distribution, which is symmetric in the arguments. Let

By symmetry, the sequence of random variables are exchangeable and hence so are . Let

Note that and so . Then, for any ,

| (2.1) |

since there are at least such ’s satisfying .

Let

| (2.2) |

where is the random variable evaluated at . Then (2.1) implies that

Based on the above discussion, any conformity measure can be used to construct prediction regions with finite sample validity, with essentially no assumptions on . The only requirement is exchangeability of which is satisfied if the sample is independent.

In this paper we use

| (2.3) |

that is, a density estimate evaluated at . We show that such a choice is closely related to the plug-in density level set estimator and hence can be proved to be asymptotically minimal with explicit rate of convergence.

3 Kernel density estimation

Let . Define the augmented data . Let be some density estimator that is defined for all . For example, could be a parametric estimator or a nonparametric estimator such as a kernel density estimator. The particular algorithm we propose is given in Figure 1.

Algorithm 1: Conformal Prediction with Density Estimation Input: sample , density estimator , and level . For every : (a) Construct from . (b) Compute where for and . (c) Test the null hypothesis by computing the statistic Output: (inverting the test) .

Recall that under the null hypothesis , the ranks of are exchangeable, and hence . Hence, we have:

Lemma 1.

Suppose is an independent random sample from , then

| (3.1) |

for all probability measures and hence is valid.

Remark 2.

Note that the prediction region is valid (has correct finite sample coverage) without any smoothness assumptions on . Indeed, the region is valid even if does not have a density.

3.1 Conformal prediction with kernel density estimation

Now we turn to the combination of conformal prediction with kernel density estimator. For a given bandwidth and kernel function , let

| (3.2) |

be the usual kernel density estimator. For now, we focus on a given bandwidth . The theoretical and practical aspects of choosing will be discussed in Subsection 3.3 and Section 4, respectively. For any given , let and define the augmented density estimator

| (3.3) |

Now we use the conformity measure and the p-value is

The resulting prediction region given by Algorithm 1 is .

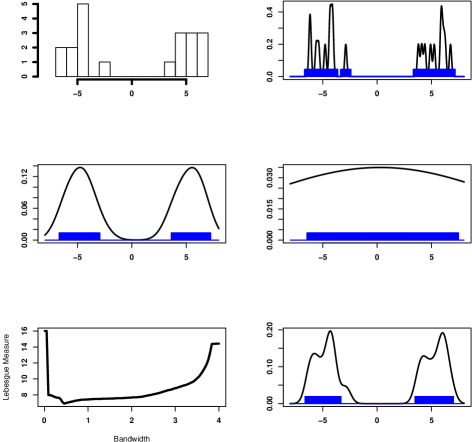

Figure 2 shows a one-dimensional example of the procedure, which we will investigate in detail later. The top left plot shows a histogram of some data of sample size 20 from a two-component Gaussian mixture. The next three plots (top right, middle left, middle right) show three kernel density estimators with increasing bandwidth as well as the conformal prediction regions derived from these estimators with . Every bandwidth leads to a valid region, but undersmoothing and oversmoothing lead to larger regions. The bottom left plot shows the Lebesgue measure of the region as a function of bandwidth. The bottom right plot shows the estimator and prediction region based on the bandwidth whose corresponding conformal prediction region has the minimal Lebesque measure.

3.2 An approximation

The conformal prediction region given by Algorithm 1 is closely related to the kernel density estimator. In this subsection we further investigate this connection and state the main approximation result, the sandwiching lemma, which provides simple characterization of the conformal prediction region in terms of plug-in kernel density level sets. The sandwiching lemma will also be useful in the study of efficiency of the conformal prediction regions.

We first introduce some notation. Define the upper and lower level sets of density at level , respectively:

| (3.4) |

The corresponding level sets of are denoted and , respectively. Let

| (3.5) |

where is the empirical distribution defined by the sample , and is the point mass distribution at . Define functions

The functions , and defined above are the cumulative distribution function (CDF) of and its empirical versions with sample and , respectively.

By (2.2) and Algorithm 1, the conformal prediction region can be written as

| (3.6) |

Let be the reordered data so that are in ascending order. Let , and define the inner and outer sandwiching sets:

and

where . Then we have the following “sandwiching” lemma, whose proof can be found in Subsection 7.1.

Lemma 3 (Sandwiching Lemma).

Assume that , then

| (3.7) |

According to the sandwiching lemma, also guarantees distribution free finite sample coverage and it is easier to analyze. The inner region, , which is not much smaller than when is large, generally does not have finite sample validity. We confirm this through simulations in Section 5. Next we investigate the efficiency of these prediction regions.

3.3 Asymptotic properties

In this subsection we prove asymptotic efficiency of and the sandwiching sets in terms of the convergence rates of their loss.

Recall that the optimal prediction region at level can be written as

| (3.8) |

where is the cut-off value of the density function so that the probability mass in the lower level set is exactly :

| (3.9) |

This holds if we assume is continuous at so that the above equation implies . This is equivalent to assuming that the contour of at value , , has zero measure under .

The inner and outer sandwiching sets and are plug-in estimators of density level sets of the form:

| (3.10) |

where for the inner set and for the outer set . Here we can view as an estimate of . In Cadre, Pelletier and Pudlo (2009) it is shown that, under regularity conditions of the density , the plug-in estimators and using kernel density estimator are consistent with convergence rate for a range of . Here, we refine the results using a set of slightly modified conditions.

Intuitively speaking, for any density estimator and cut-off values , the plug-in density level set is an accurate estimator of if:

-

1.

The estimated density function, , is close to the true density .

-

2.

The true density is not too flat around level .

-

3.

The estimated cut-off value is an accurate estimate of .

The first condition has been extensively studied in the literature of nonparametric density estimation and sufficient conditions of convergence for kernel density estimators in various forms have been established. The second condition is more specific for density level set estimation. A common condition is the -exponent at level , which is first introduced by Polonik (1995) and has been used by many others (see Tsybakov, 1997; Rigollet and Vert, 2009, for example). The third condition is somewhat opposite to the second one. It essentially requires that the density function cannot be too steep near the true cut-off value. This turns out to be a natural condition whenever the density has bounded derivatives near the contour. We formalize this condition through a “modified -exponent condition” which is detailed in Section 3.3.2.

3.3.1 Hölder Classes of Densities

To study the efficiency of the prediction region, we need some smoothness condition on . The Hölder class is a popular smoothness condition in nonparametric inferences (Tsybakov, 2009, Section 1.2). Here we use the version given in Rigollet and Vert (2009).

Let be a -tuple of non-negative integers and . For any , let and be the differential operator:

Given , for any functions that are times differentiable, denote its Taylor expansion of degree at by

Definition 4 (Hölder class).

For constants , , define the Hölder class to be the set of -times differentiable functions on such that,

| (3.11) |

3.3.2 The -exponent condition

For a density function , and a level , the usual -exponent condition requires that there exists an and such that

| (3.12) |

Condition (3.12) is essentially requiring that the density increases roughly at rate when moves away from the contour by an distance. As a result, a larger value of corresponds to a faster change of the density when moving away from the contour, hence it is easier to estimate the density level set. In this paper, we consider the modified -exponent condition:

Definition 5 (Modified -exponent condition).

We say a density function satisfies the modified -exponent condition at level , if there exist constants and , such that

| (3.13) |

The modified -exponent condition differs from the original definition in three aspects:

-

1.

First, it allows both sides of the interval to change within a neighborhood of , which is stronger than (3.12). It does not allow the contour at level to have positive measure. We note that if the contour at level has positive measure, then the estimated level set has at least a constant loss unless the cut-off value is estimated without error.

-

2.

Second, it does not only require an upper bound on the measure, but also a lower bound. Since the upper bound indicates that the density cannot be too flat around the contour, the lower bound does not allow the density to be too steep. This condition implies that the estimated cut-off value is close to the truth. It usually holds when the density is smooth enough around the contour. For example, when the contour at level is smooth and the density satisfies for all that is away from the contour and all small enough (Tsybakov, 1997).

-

3.

Moreover, in the modified condition, we use the measure induced by , rather than the Lebesgue measure. This is a minor difference since we always have, for all ,

3.3.3 Conditions on the Kernel

A standard condition on the kernel is the notion of -valid kernels.

Definition 6 (-valid kernel).

For any , a function is a -valid kernel if

-

1.

is supported on .

-

2.

.

-

3.

, all .

-

4.

for all .

In the literature, -valid kernels are usually used with Hölder class of functions to derive fast rate of convergence. The existence of univariate -valid kernels can be found in (Tsybakov, 2009, Section 1.2). A multivariate -valid kernel can be obtained by taking direct product of univariate -valid kernels.

3.3.4 Asymptotic properties of estimated density level set

Consider the following assumptions:

Assumption A1:

-

(a)

The density function , where is the class of all density functions that are in the Hölder class .

-

(b)

The density satisfies the modified -exponent condition at level .

-

(c)

The density function is uniformly bounded by a constant .

Assumption A2: The bandwidth satisfies

| (3.14) |

Assumption A3: The kernel is -valid and .

These assumptions extend those in (Cadre, Pelletier and Pudlo, 2009), where is considered. Also A1(b) considered here is a local version.

The next theorem states the quality of cut-off values used in the sandwiching sets and .

Theorem 7.

We give the proof of Theorem 7 in Section 7.2. Theorem 7 is useful for establishing the convergence of the corresponding level set. Observing that , it follows immediately that the cut-off value used in also satisfies (3.15). The next theorem gives the rate of convergence for plug-in level set estimators when the cut-off value satisfies (3.15).

Theorem 8.

Let be a random sequence which satisfies (3.15). Under A1-A3, for any , there exist constants , depending on , and only, such that

By Theorem 7, the cut-off values used in and both satisfy (3.15), so the convergence rate in Theorem 8 holds for and . By Lemma 3, it also holds for .

Corollary 9.

Under A1-A3, for any , there exists constant , depending on , and only, such that, for all ,

| (3.16) |

In the most common case , the term dominates the convergence rate. If we further assume that the level set is star-shaped (or more generally, a union of star-shaped sets), then the rate given by Corollary 9 is near optimal, up to a logarithm term. Indeed, the rate in equation (3.16) is within a logarithm term of the minimax risk for density level set estimation as developed in Tsybakov (1997). But note that the problem considered here is harder than estimating density level set at a fixed level since the cut-off value is not known in advance and needs to be estimated. Indeed, the logarithm term comes from estimating . We also note that the continuity condition on is slightly different than that in Tsybakov (1997) where it is assumed that the density contour at the desired level is in a Hölder class. But the same construction of the lower bound can be used under the global smoothness conditions A1(a) and A1(b).

A minimax risk rate of the plug-in density level set at a fixed level has been developed by Rigollet and Vert (2009). Although the rate is similar as that obtained in this paper, the construction of the lower bound only applies to fixed cut-off values close to 1, and hence has only limited application to the range of values of practical interest.

4 Choosing the bandwidth

As illustrated in Figure 2, the efficiency of depends on the choice of . The size of estimated prediction region can be very large if the bandwidth is either too large or too small. Therefore, in practice it is desirable to choose a good bandwidth in an automatic and data driven manner. In kernel density estimation, the choice of bandwidth has been one of the most important topics and many approaches have been studied; see Loader (1999) and Mammen et al. (2011) and references therein. Intuitively, a good density estimator will likely lead to a good prediction region, and the dependence on of the (near) optimal choice of in Theorem 8 is similar to that in the context of kernel density estimation. However, this is not quite the case (Samworth and Wand, 2010). The intuition is simple: For density estimation, a good bandwidth guarantees the accuracy of estimated density in the whole space, whereas for level sets it suffices to estimate the density accurately near the contour.

We propose two practical methods to choose a good bandwidth from a given candidate set , based on the idea that a good prediction region has small Lebesgue measure; see Figures 3 and 4. The methods introduced here are applicable to any prediction region estimator with finite sample validity. In both approaches, we compute the prediction region for each and choose the one with the smallest volume. To preserve finite sample validity, the first approach, described in Fig 3, uses a Bonferroni correction.

Algorithm 2: Tuning with Bonferroni Correction Input: sample , prediction region estimator , and level . 1. Construct prediction sets each at level , where . 2. Let . 3. Return .

Proposition 10.

If satisfies finite sample validity for any , then the estimated prediction region given by Algorithm 2 also satisfies finite sample validity.

Proof.

Using Bonferroni correction we have

where the last inequality uses the fact that each is a finite sample valid prediction region at level . ∎

When is large, Algorithm 2 tends to be conservative since each single has coverage , which could be much bigger than the ideal region. The algorithm described in Figure 4 uses sample splitting and only sacrifices a constant rate of efficiency regardless of .

Algorithm 3: Tuning With Sample Splitting Input: sample , prediction region estimator , and level 1. Split the sample randomly into two equal sized subsamples, and . 2. Construct prediction regions each at level , using subsample . 3. Let . 4. Return , which is constructed using bandwidth and subsample .

Proposition 11.

If satisfies finite sample validity for all , then , the output of Algorithm 3, also satisfies finite sample validity.

Proof.

Note that is independent of , as a result,

∎

It is easy to see that these methods have small excess loss with high probability since, by construction, , where is the best bandwidth that minimizes the excess loss and is a negligible term, because for dense enough, there exists such that Although minimizing excess loss does not necessarily minimize the symmetric difference loss, a small excess loss itself is a desired property in practice and is also a necessary condition of small symmetric difference loss. However, a more detailed relationship between excess loss and symmetric difference loss requires extra conditions and we leave that for future research.

5 Numerical example

A simple illustration of Algorithm 1 is presented in Figure 2. Here we consider a two-dimensional Gaussian mixture, whose geometric structure allows a better visualization of the results. We also test the bandwidth selectors presented in Section 4. Due to the small value of and limited sample size, we find Algorithm 3 more preferable than Algorithm 2. Thus we only present the results using bandwidth chosen by sample splitting. For example, when , 100 data points are used to select the bandwidth and the other 100 data points are used to construct the prediction region using the selected bandwidth.

Table 1 shows the coverage and Lebesgue measure of the prediction region of level .90 over 1,000 repetitions. The coverage is excellent and the size of the region is close to optimal. Both the conformal region and the outer sandwiching set gives correct coverage regardless of the sample size. It is worth noting that the inner sandwiching set does not give the desired coverage, which suggests that decreasing the cut-off value in is not merely an artifact of proof, but a necessary tuning. The observed excess loss also reflects a rate of convergence that supports our theoretical results on the symmetric difference loss. Taking for example, in Corollary 9 we have , , and

which agrees with the observed drop of average excess loss from 6 to 3 as increased from 200 to 1,000.

| Coverage | Lebesgue Measure | |||

|---|---|---|---|---|

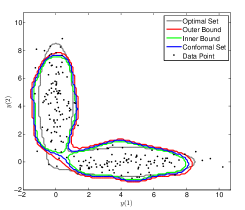

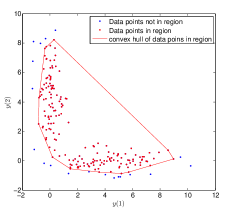

Figure 5 shows a typical realization of the estimators. In both panels, the dots are data points when . The left panel shows the conformal prediction region with sample splitting (blue curve), together with the inner and outer sandwiching sets (red and green curves, respectively). Also plotted is the ideal region (the grey curve). It is clear that all three estimated regions captures the main part of the ideal region, and they are mutually close. On the right panel we plot a realization of the depth based approach from Li and Liu (2008). This approach does not require any tuning parameter. However, it takes time to evaluate for any single . In practice it is recommended to compute the empirical depth only for all the data points and use the convex hull of all data points with high depth as the estimated prediction region. As can be seen on the picture, such a convex hull construction misses the “L” shape of the ideal region. Moreover, the kernel density method is at least 1,000 times faster than the depth based method in our implementation even when .

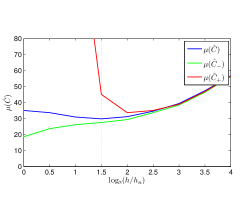

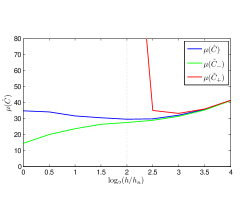

Figure 6 shows the effect of bandwidth on the excess loss based on a typical implementation of conformal prediction, where the axis is the Lebesgue measure of the estimated region. We observe that for the conformal prediction region , the excess loss is stable for a wide range of bandwidth, especially that moderate undersmoothing does not harm the performance very much. An intuitive explanation is that the data near the contour is dense enough to allow for moderate undersmoothing. Similar phenomenon should be expected whenever is not too small. Moreover, the selected bandwidth from the outer sandwiching set is close to that obtained from the conformal region. This observation may be of practical interest since it is usually much faster to compute .

6 Conclusion

We have constructed a distribution free prediction region by combining ideas from density estimation and conformal prediction. It can also be viewed as a combination of the statistically equivalent block methods and the density level set methods. The region is easy to compute and, under regularity conditions, is asymptotically near optimal. Even without the regularity conditions, the region retains its finite sample validity.

The bandwidth tuning algorithm (Algorithm 3) used in our simulation resembles cross-validation, a popular device for kernel density estimators. In Algorithm 3, the comparison between candidate bandwidths is based on a direct evaluation of loss, that is, the Lebesgue measure of the estimated region. This feature yields both conceptually and computationally simple implementation which is also highly stable as observed in our simulation studies. Future topics of research in this aspect include understanding the theoretical properties of such a bandwidth selector, its connection with other approaches in the literature of density and level set estimation, and the performance under both excess loss as well as the symmetric difference loss.

In current work we are studying nonparametric procedures that adapt to smoothness conditions. In principle it is possible to further develop this method to deal with nonparametric prediction with covariates or parametric models.

7 Proofs

7.1 Proof of Lemma 3

Proof of the sandwiching lemma.

The proof is done via a direct characterization of and .

First, for each and , we have

As a result, and hence .

Similarly, for each and we have

Therefore, and hence . ∎

7.2 Proof of Theorem 7

Preliminaries

Recall that is the lower level set of at level : . The bias in the estimated cut-off level can be bounded in terms of two quantities:

and

Here can be viewed as the maximum of the empirical process over a nested class of sets, and is the loss of the density estimator. As a result, can be bounded using the standard empirical process and VC dimension argument, and can be bounded using the smoothness of and kernel with a suitable choice of bandwidth. Formally, we provide upper bounds for these two quantities through the following lemma.

Lemma 12.

Let , be defined as above, then under assumptions A1-A3, for any , there exist constants and depending on only, such that,

and

Proof.

First, it is easy to check that the class of sets are nested with VC (Vapnik-Chervonenkis) dimension 2 and hence by classical empirical process theory (see, for example, van der Vaart and Wellner, 1996, Section 2.14), there exists a constant such that for all

| (7.1) |

Let , we have

| (7.2) |

The first result then follows by choosing .

Next we bound . Let , and

By triangle inequality

Due to a result of Giné and Guillou (2002) (see also equation (49) in Chapter 3 of Prakasa Rao, 1983), under the assumptions A1(c) and A3, there exist constants , and such that have for all ,

| (7.3) |

On the other hand, by assumptions A1(a) and A3, for some constant

| (7.4) |

We note that in the inequalities (7.2), (7.2) and (7.4) the constants , , depend on and only. Hence,

| (7.5) |

which concludes the second part by choosing

∎

Proof of Theorem 7.

Let . We have

Recall that the ideal level can be written as

where the function is the cumulative distribution function of , as defined in Subsection 3.2. By the modified -exponent condition the inverse of is well defined in a small neighborhood of . When is large enough, we can define as

Again, by the modified -exponent,

Therefore, for large enough

| (7.6) |

Equation (7.6) allows us to switch to the problem of bounding .

Recall that . The key of the proof is to observe that

Then it suffices to show that and are close at . In fact, by definition of we have for all :

Applying the empirical measure to each term in the above:

By definition of ,

By definition of and , the above inequality becomes

Let . Suppose is large enough such that

then on the event ,

where the last inequality uses the left side of the modified -exponent condition. Similarly, Hence, for large enough, if then,

| (7.7) |

To conclude the proof, first note that

Then we can find constant such that for all large enough,

| (7.8) |

Let . Combining equations (7.6) and (7.7), on the event

| (7.9) |

we have, for large enough,

| (7.10) |

where the second last inequality is from the definition of and the last inequality is from the choice of . The proof is concluded by observing , a consequence of Lemma 12. ∎

7.3 Proof of Theorem 8

Proof of Theorem 8.

In the proof we write for . Observe that

| (7.11) |

Note that

| (7.12) |

and

| (7.13) |

Therefore

| (7.14) |

Suppose is large enough such that

where the constant is defined as in Lemma 12 and is defined as in equation (7.8). Then on the event as defined in equation (7.9), applying Theorem 7 and condition (3.13) on the right hand side of (7.3) yields

| (7.15) |

where , are positive constants depend only on , , and . ∎

References

- Aichison and Dunsmore (1975) {bbook}[author] \bauthor\bsnmAichison, \bfnmJ.\binitsJ. and \bauthor\bsnmDunsmore, \bfnmI. R.\binitsI. R. (\byear1975). \btitleStatistical Prediction Analysis. \bpublisherCambridge Univ. Press. \endbibitem

- Baillo (2003) {barticle}[author] \bauthor\bsnmBaillo, \bfnmA.\binitsA. (\byear2003). \btitleTotal error in a plug-in estimator of level sets. \bjournalStatistics & Probability Letters \bvolume65 \bpages411-417. \endbibitem

- Baillo, Cuestas-Alberto and Cuevas (2001) {barticle}[author] \bauthor\bsnmBaillo, \bfnmA.\binitsA., \bauthor\bsnmCuestas-Alberto, \bfnmJ.\binitsJ. and \bauthor\bsnmCuevas, \bfnmA.\binitsA. (\byear2001). \btitleConvergence rates in nonparametric estimation of level sets. \bjournalStatistics & Probability Letters \bvolume53 \bpages27-35. \endbibitem

- Cadre (2006) {barticle}[author] \bauthor\bsnmCadre, \bfnmBenoît\binitsB. (\byear2006). \btitleKernel estimation of density level sets. \bjournalJournal of multivariate analysis \bvolume97 \bpages999-1023. \endbibitem

- Cadre, Pelletier and Pudlo (2009) {bmisc}[author] \bauthor\bsnmCadre, \bfnmBenoît\binitsB., \bauthor\bsnmPelletier, \bfnmBruno\binitsB. and \bauthor\bsnmPudlo, \bfnmPierre\binitsP. (\byear2009). \btitleClustering by estimation of density level sets at a fixed probability. \bhowpublishedmanuscript. \endbibitem

- Chatterjee and Patra (1980) {barticle}[author] \bauthor\bsnmChatterjee, \bfnmShoutier K.\binitsS. K. and \bauthor\bsnmPatra, \bfnmNishith K.\binitsN. K. (\byear1980). \btitleAsymptotically minimal multivariate tolerance sets. \bjournalCalcutta Statist. Assoc. Bull. \bvolume29 \bpages73-93. \endbibitem

- Di Bucchianico, Einmahl and Mushkudiani (2001) {barticle}[author] \bauthor\bsnmDi Bucchianico, \bfnmAlessandro\binitsA., \bauthor\bsnmEinmahl, \bfnmJohn H.\binitsJ. H. and \bauthor\bsnmMushkudiani, \bfnmNino A.\binitsN. A. (\byear2001). \btitleSmallest nonparametric tolerance regions. \bjournalThe Annals of Statistics \bvolume29 \bpages1320-1343. \endbibitem

- Fraser and Guttman (1956) {barticle}[author] \bauthor\bsnmFraser, \bfnmD. A. S.\binitsD. A. S. and \bauthor\bsnmGuttman, \bfnmIrwin\binitsI. (\byear1956). \btitleTolerance regions. \bjournalThe Annals of Mathematical Statistics \bvolume27 \bpages162-179. \endbibitem

- Giné and Guillou (2002) {barticle}[author] \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmGuillou, \bfnmArmelle\binitsA. (\byear2002). \btitleRates of strong uniform consistency for multivariate kernel density estimators. \bjournalAnnales de l’Institut Henri Poincare (B) Probability and Statistics \bvolume38 \bpages907-921. \endbibitem

- Guttman (1970) {bbook}[author] \bauthor\bsnmGuttman, \bfnmIrwin\binitsI. (\byear1970). \btitleStatistical Tolerance Regions: Classical and Bayesian. \bpublisherGriffin, London. \endbibitem

- Hartigan (1975) {bbook}[author] \bauthor\bsnmHartigan, \bfnmJohn\binitsJ. (\byear1975). \btitleClustering Algorithms. \bpublisherJohn Wiley, New York. \endbibitem

- Li and Liu (2008) {barticle}[author] \bauthor\bsnmLi, \bfnmJun\binitsJ. and \bauthor\bsnmLiu, \bfnmRegina\binitsR. (\byear2008). \btitleMultivariate spacings based on data depth: I. construction of nonparametric multivariate tolerance regions. \bjournalThe Annals of Statistics \bvolume36 \bpages1299-1323. \endbibitem

- Liu, Parelius and Singh (1999) {barticle}[author] \bauthor\bsnmLiu, \bfnmRegina\binitsR., \bauthor\bsnmParelius, \bfnmJesse\binitsJ. and \bauthor\bsnmSingh, \bfnmKesar\binitsK. (\byear1999). \btitleMultivariate analysis by data depth: descriptive statistics, graphics and inference. \bjournalThe Annals of Statistics \bvolume27 \bpages783-858. \endbibitem

- Loader (1999) {barticle}[author] \bauthor\bsnmLoader, \bfnmCliver\binitsC. (\byear1999). \btitleBandwidth selection: classical or plug-in? \bjournalThe Annals of Statistics \bvolume27 \bpages415-438. \endbibitem

- Mammen et al. (2011) {barticle}[author] \bauthor\bsnmMammen, \bfnmEnno\binitsE., \bauthor\bsnmMiranda, \bfnmMar a Dolores Martínez\binitsM. D. M., \bauthor\bsnmNielsen, \bfnmJens Perch\binitsJ. P. and \bauthor\bsnmSperlich, \bfnmStefan\binitsS. (\byear2011). \btitleDo-Validation for kernel density estimation. \bjournalJournal of the American Statistical Association \bvolume106 \bpages651-660. \endbibitem

- Mason and Polonik (2009) {barticle}[author] \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. and \bauthor\bsnmPolonik, \bfnmWolfgang\binitsW. (\byear2009). \btitleAsymptotic normality of plug-in level set estimates. \bjournalThe Annals of Applied Probability \bvolume19 \bpages1108-1142. \endbibitem

- Polonik (1995) {barticle}[author] \bauthor\bsnmPolonik, \bfnmWolfgang\binitsW. (\byear1995). \btitleMeasuring mass concentrations and estimating density contour clusters - an excess mass approach. \bjournalThe Annals of Statistics \bvolume23 \bpages855-881. \endbibitem

- Prakasa Rao (1983) {bbook}[author] \bauthor\bsnmPrakasa Rao, \bfnmB. L. S.\binitsB. L. S. (\byear1983). \btitleNonparametric Functional Estimation. \bpublisherAcademic Press. \endbibitem

- Rigollet and Vert (2009) {barticle}[author] \bauthor\bsnmRigollet, \bfnmPhilippe\binitsP. and \bauthor\bsnmVert, \bfnmRégis\binitsR. (\byear2009). \btitleOptimal rates for plug-in estimators of denslty level sets. \bjournalBernoulli \bvolume14 \bpages1154-1178. \endbibitem

- Rinaldo and Wasserman (2010) {barticle}[author] \bauthor\bsnmRinaldo, \bfnmAlessandro\binitsA. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2010). \btitleGeneralized density clustering. \bjournalThe Annals of Statistics \bvolume38 \bpages2678-2722. \endbibitem

- Samworth and Wand (2010) {barticle}[author] \bauthor\bsnmSamworth, \bfnmRichard J.\binitsR. J. and \bauthor\bsnmWand, \bfnmMatt P.\binitsM. P. (\byear2010). \btitleAsymptotics and optimal bandwidth selection for highest density region estimation. \bjournalThe Annals of Statistics \bvolume38 \bpages1767-1792. \endbibitem

- Shafer and Vovk (2008) {barticle}[author] \bauthor\bsnmShafer, \bfnmGlenn\binitsG. and \bauthor\bsnmVovk, \bfnmVladimir\binitsV. (\byear2008). \btitleA tutorial on conformal prediction. \bjournalJournal of Machine Learning Research \bvolume9 \bpages371-421. \endbibitem

- Tsybakov (1997) {barticle}[author] \bauthor\bsnmTsybakov, \bfnmAlexandre\binitsA. (\byear1997). \btitleOn nonparametric estimation of density level sets. \bjournalThe Annals of Statistics \bvolume25 \bpages948-969. \endbibitem

- Tsybakov (2009) {bbook}[author] \bauthor\bsnmTsybakov, \bfnmAlexandre\binitsA. (\byear2009). \btitleIntroduction to nonparametric estimation. \bpublisherSpringer. \endbibitem

- Tukey (1947) {barticle}[author] \bauthor\bsnmTukey, \bfnmJohn\binitsJ. (\byear1947). \btitleNonparametric estimation, II. Statistical equivalent blocks and multivarate tolerance regions. \bjournalThe Annals of Mathematical Statistics \bvolume18 \bpages529-539. \endbibitem

- van der Vaart and Wellner (1996) {bbook}[author] \bauthor\bsnmvan der Vaart, \bfnmAad W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1996). \btitleWeak Convergence and Empirical Processes. \bpublisherSpringer. \endbibitem

- Vovk, Gammerman and Shafer (2005) {bbook}[author] \bauthor\bsnmVovk, \bfnmVladimir\binitsV., \bauthor\bsnmGammerman, \bfnmAlex\binitsA. and \bauthor\bsnmShafer, \bfnmGlenn\binitsG. (\byear2005). \btitleAlgorithmic Learning in a Random World. \bpublisherSpringer. \endbibitem

- Vovk, Nouretdinov and Gammerman (2009) {barticle}[author] \bauthor\bsnmVovk, \bfnmVladimir\binitsV., \bauthor\bsnmNouretdinov, \bfnmIlia\binitsI. and \bauthor\bsnmGammerman, \bfnmAlex\binitsA. (\byear2009). \btitleOn-line preditive linear regression. \bjournalThe Annals of Statistics \bvolume37 \bpages1566-1590. \endbibitem

- Wald (1943) {barticle}[author] \bauthor\bsnmWald, \bfnmAbraham\binitsA. (\byear1943). \btitleAn extension of Wilks method for setting tolerance limits. \bjournalThe Annals of Mathematical Statistics \bvolume14 \bpages45-55. \endbibitem

- Wilks (1941) {barticle}[author] \bauthor\bsnmWilks, \bfnmSamuel\binitsS. (\byear1941). \btitleDetermination of sample sizes for setting tolerance limits. \bjournalThe Annals of Mathematical Statistics \bvolume12 \bpages91-96. \endbibitem

- Willett and Nowak (2007) {barticle}[author] \bauthor\bsnmWillett, \bfnmR. M.\binitsR. M. and \bauthor\bsnmNowak, \bfnmR. D.\binitsR. D. (\byear2007). \btitleMinimax optimal level-set estimation. \bjournalIEEE Transactions on Image Processing \bvolume16 \bpages2965 - 2979. \endbibitem