Calibration of self-decomposable Lévy models

Abstract

We study the nonparametric calibration of exponential Lévy models with infinite jump activity. In particular our analysis applies to self-decomposable processes whose jump density can be characterized by the -function, which is typically nonsmooth at zero. On the one hand the estimation of the drift, of the activity measure and of analogous parameters for the derivatives of the -function are considered and on the other hand we estimate nonparametrically the -function. Minimax convergence rates are derived. Since the rates depend on , we construct estimators adapting to this unknown parameter. Our estimation method is based on spectral representations of the observed option prices and on a regularization by cutting off high frequencies. Finally, the procedure is applied to simulations and real data.

doi:

10.3150/12-BEJ478keywords:

1 Introduction

Since Merton [19] introduced his discontinuous asset price model, stock returns were frequently described by exponentials of Lévy processes. A review of recent pricing and hedging results for these models is given by Tankov [26]. The calibration of the underlying model, that is in the case of Lévy models the estimation of the characteristic triplet , from historical asset prices is mostly studied in parametric models only, consider the survey paper of Eberlein [10] and the references therein. Remarkable exceptions are the nonparametric penalized least squares method by Cont and Tankov [9] and the spectral calibration procedure by Belomestny and Reiß [3]. Both articles concentrate on models of finite jump activity. Our goal is to extend their results to infinite intensity models. A class which attracted much interest in financial modeling is given by self-decomposable Lévy processes, examples are the hyperbolic model (Eberlein, Keller and Prause [11]) or the variance gamma model (Madan and Seneta [18], Madan, Carr and Chang [17]). Moreover, self-decomposable distributions are discussed in the financial investigation using Sato processes (Carr et al. [6], Eberlein and Madan [12]). Our results can be applied in this context, too. The nonparametric calibration of Lévy models is not only relevant for stock prices, for instance, it can be used for the Libor market as well (see Belomestny and Schoenmakers [4]). In the context of Ornstein–Uhlenbeck processes, the nonparametric inference of self-decomposable Lévy processes was considered by Jongbloed, van der Meulen and van der Vaart [14].

Owing to the infinite activity, the features of market prices can be reproduced even without a diffusion part (cf. Carr et al. [5]) and thus we study pure-jump Lévy processes. More precisely, we assume that the jump density satisfies

| (K) |

When increases on and decreases on , it is called -function and the processes is self-decomposable. Further examples which have property (K) are compound Poisson processes and limit distributions of branching processes as considered by Keller-Ressel and Mijatović [16]. Using the bounded variation of , we show that the estimation problem is only mildly ill-posed. While the Blumenthal–Getoor index, which was estimated by Belomestny [1], is zero in our model, the infinite activity can be described on a finer scale by the parameter

Since is typically nonsmooth at zero, we face two estimation problems: First, to give a proper description of at zero, we propose estimators for and its analogs , with , for the derivatives of as well as for the drift , which can be estimated similarly. We prove convergence rates for their mean squared error which turn out to be optimal in minimax sense up to a logarithmic factor. Second, we construct a nonparametric estimator of whose mean integrated squared error converges with nearly optimal rates. Owing to bid-ask spreads and other market frictions, we observe only noisy option prices. The definition of the estimators is based on the relation between these prices and the characteristic function of the driving process established by Carr and Madan [7] and on different spectral representations of the characteristic exponent. Smoothing is done by cutting off all frequencies higher than a certain value depending on a maximal permitted parameter . The whole estimation procedure is computationally efficient and achieves good results in simulations and in real data examples. All estimators converge with a polynomial rate, where the maximal determines the ill-posedness of the problem. Assuming sub-Gaussian error distributions, we provide an estimator with -adaptive rates. The main tool for this result is a concentration inequality for our estimator which might be of independent interest.

This work is organized as follows: In Section 2, we describe the setting of our estimation procedure and derive the necessary representations of the characteristic exponent. The estimators are described in Section 3, where we also determine the convergence rates. The construction of the -adaptive estimator of is contained in Section 4. In view of simulations and real data, we discuss our theoretical results and the implementation of the procedure in Section 5. All proofs are given in Section 6.

2 The model

2.1 Self-decomposable Lévy processes

A real valued random variable X has a self-decomposable law if for any there is an independent random variable such that . Since each self-decomposable distribution is infinitely divisible (see Proposition 15.5 in [21]), we can define the corresponding self-decomposable Lévy process. Self-decomposable laws can be understood as the class of limit distributions of converging scaled sums of independent random variables (Theorem 15.3 in [21]). This characterization is of economical interest. If we understand the price of an asset as an aggregate of small independent influences and release from the scaling, which leads to diffusion models, we automatically end up in a self-decomposable price process.

Sato [21] shows that the jump measure of a self-decomposable distribution is always absolutely continuous with respect to the Lebesgue measure and its density can be characterized through (K) where needs to be increasing on and decreasing on . Note that self-decomposability does not affect the volatility nor the drift of the Lévy process.

Assuming and property (K), the process has finite variation and the characteristic function of is given by the Lévy–Khintchine representation

| (2) |

Motivated by a martingale argument, we will suppose the exponential moment condition for all , which yields

| (3) |

In particular, we will impose . In this case, is defined on the strip .

Besides Lévy processes there is another class that is closely related to self-decomposability. Assuming self-similarity, that means , for all and some exponent , instead of stationary increments, is a Sato processes. Sato [20] showed that self-decomposable distributions can be characterized as the laws at unit time of these processes. From the self-similarity and self-decomposability follows for

Since our estimation procedure only depends through equation (2) on the distributional structure of the underlying process, we can apply the estimators directly to Sato processes using and instead of , and . However, we concentrate on Lévy processes in the sequel.

For self-decomposable distributions the parameter captures many of its properties such as the smoothness of the densities of the marginal distributions (Theorem 28.4 in [21]) and the tail behavior of the characteristic function. This holds even for the more general class of Lévy processes that satisfy property (K). Recall that has bounded variation if and only if

In particular, implies . Similarly to deconvolution problems, the stochastic error in our model is driven by and thus we prove the following lemma in the Appendix.

Lemma 2.1

The value as defined in the lemma can be understood as the largest slop of near zero. If the process is self-decomposable than holds and the bounded variation norm equals . Otherwise, we can use and , assuming the derivative exists, is bounded on and integrable on . If either or property (K) is violated, can decay faster than any polynomial order, for example, consider self-decomposable processes with (see [21], Lemma 28.5). Hence, the conditions of Lemma 2.1 are sharp.

2.2 Asset prices and Vanilla options

Let be the risk-less interest rate in the market and denote the initial value of the asset. In an exponential Lévy model the price process is given by

where is a Lévy process described by the characteristic triplet . Throughout these notes, we assume has property (K) and . On the probability space with pricing (or martingale) measure the discounted process is a martingale with respect to its natural filtration . This is equivalent to for all and thus, the martingale condition (3) holds.

At time the risk neutral price of an European call option with underlying , time to maturity and strike price is given by where , and similarly is the price of European put. In terms of the negative log-forward moneyness the prices can be expressed as

Carr and Madan [7] introduced the option function

and set the Fourier transform in relation to the characteristic function through the pricing formula

| (4) |

The properties of were studied further by Belomestny and Reiß [3]. In particular, they showed that the option function is contained in and decays exponentially under the following assumption.

Assumption 1.

We assume that is finite, which is equivalent to the moment condition .

Our observations are given by

| (5) |

where the noise consists of independent, centered random variables with and . The noise levels are assumed to be positive and known. In practice, the uncertainty is due to market frictions such as bid-ask spreads.

2.3 Representation of the characteristic exponent

Using (2) and (4), the shifted characteristic exponent is given by

| (6) | |||||

| (7) |

for . Note that the last line equals zero for because of the martingale condition (3). Throughout, we choose a distinguished logarithm, that is a version of the complex logarithm such that is continuous with . Under the assumption that 111We denote and for . is finite, we can apply Fubini’s theorem to obtain

| (8) |

where the Fourier transform is well defined on . Typically, the and its derivatives are not continuous at zero. Moreover, if the function has a jump at zero in every case. Therefore, the Fourier transform decreases very slowly. Let be smooth on and fulfill an integrability condition which will be important later:

Assumption 2.

Assume with all derivatives having a finite right- and left-hand limit at zero and .

To compensate those discontinuities, we add a linear combination of the functions , for . Since for and all are smooth on , we can find , such that is contained in . This approach yields the following representation. The proof is given in the supplementary article [27].

Proposition 2.2

Let . On Assumption 2, there exist functions and such that is bounded in and it holds

| (9) |

The coefficients are given by especially holds.

Representation (9) allows us to estimate and . A plug-in approach yields estimators for . Since we only apply this representation when is multiplied with weight functions having roots of degree at zero, the poles that appear in (9) do no harm.

Proposition 2.2 covers the case . For we conclude from (7), the martingale condition (3) and Assumption 2

| (10) |

Hence, is a sum of a constant from the integration, the linear drift and a remainder of order , which follows from the decay of the Fourier transform as . Corollary 8 in [27] even shows, that there exists no -consistent estimator of for . Therefore, we concentrate on the case in the sequel.

Equation (10) allows another useful observation. Defining the exponentially scaled -function

we obtain by differentiation

| (11) |

Using this relation, we can define an estimator of .

3 Estimation procedure

3.1 Definition of the estimators and weight functions

Given the observations , we fit a function to these data using linear -splines

and a function with to take care of the jump of :

We choose with support where satisfies . Replacing with in the representations (6) and (11) of and , respectively, allows us to define their empirical versions through

where is a positive function and we apply a trimming function given by

to stabilize for large stochastic errors. A reasonable choice of will be derived below. The function is well defined on the interval on the event

For , we set arbitrarily, for instance equal to zero. The more concentrates around the true function the greater is the probability of . Söhl [23] shows even that in the continuous-time Lévy model with finite jump activity the identity holds.

In the spirit of Belomestny and Reiß [3], we estimate the parameters and , as coefficients of the different powers of in equation (9). Using a spectral cut-off value , we define

and for

The weight functions and are chosen such that they filter the coefficients of interest. Owing to (11), the nonparametric object can be estimated by

| (12) |

applying a one-sided kernel function with bandwidth since we know that jumps only at zero. The condition on the weights are summarized in the following:

Assumption 3.

We assume:

-

•

fulfills for all odd

-

•

satisfies for all even

-

•

For the weight functions fulfill222For let denote the largest integer which is smaller than .

where and is even for even and odd otherwise. For even we impose additionally

-

•

is of Sobolev smoothness , that is, , has support and fulfills for

Furthermore, we assume continuity and boundedness of the functions for .

The integral conditions can be provided by rescaling: Let satisfy Assumption 3 for and . Since , we can choose . Similarly, a rescaling is possible for :

Therefore, we define and analogously . The continuity condition on in Assumption 3 is set to take advantage of the decay of the remainder . In combination with the rescaling it implies

| (13) |

Throughout, we write if there is a constant independent of all parameters involved such that . In the sequel we assume that the weight functions satisfy Assumption 3 and the property (13).

We reduce the loss of by truncating positive values on and negative ones on . In the self-decomposable framework there are additional shape restrictions of the -function which the proposed estimator does not take into account. The monotonicity can be generated by a rearrangement of the function. To this end let , where we bounded the support with an arbitrary large constant . The rearranged estimator which is increasing on and decreasing on is then given by

| (14) |

Chernozhukov, Fernández-Val and Galichon [8] show that the rearrangement reduces weakly the error for increasing target functions on compact subsets. This result carries over to our estimation problem.

3.2 Convergence rates

To ensure a well-defined procedure, an exponential decay of , the identity (10) and to obtain a lower bound of , we consider the class . Uniform convergence results for the parameters will be derived in the smoothness class .

Definition 3.1.

In the class Lemma 2.1(ii) provides a common lower bound of for . Using , we estimate roughly for :

Hence, the choice

satisfies

| (15) |

where the factor is used for technical reasons. As discussed above, we can restrict our investigation to the case . Since the Lévy process is only identifiable if is known on the whole real line, we consider asymptotics of a growing number of observations with

Taking into account the numerical interpolation error and the stochastic error, we analyze the risk of the estimators in terms of the abstract noise level

Theorem 3.2

Let and assume and . We choose the cut-off value to obtain the uniform convergence rates

As one may expect the rates for become slower as gets closer to its maximal value because the profit from the smoothness of decreases. Note that the cut-off for all estimators is the same. In contrast to we assume Sobolev conditions on in the class in order to apply -Fourier analysis.

Definition 3.3.

Let and . We define as the set of all pairs satisfying additionally , for corresponding Lévy process as well as

In the next theorem the conditions on and are stronger than for the upper bounds of the parameters which is due to the necessity to estimate also the derivative of . However, the estimation of does not lead to a loss in the rate. As seen in (12), we need to estimate .

Theorem 3.4

Let and assume as well as . Using an estimator which satisfies and choosing the cut-off value , we obtain for the risk of the uniform convergence rate

4 Adaptation

The convergence rate of our estimation procedure depends on the bound of the true but unknown . Therefore, we construct an -adaptive estimator. For simplicity we concentrate on the estimation of itself whereas the results can be easily extended to , , and . In this section, we will require the following assumption.

Assumption 4.

Let , and for some maximal . Furthermore, we suppose and .

These conditions only recall the setting in which the convergence rates of our parameter estimators were proven. Given a consistent preestimator of , let be the estimator using the data-driven cut-off value and the trimming parameter

| (16) | |||||

| (17) |

respectively, with . If is sufficiently concentrated around the true value, the adaptation does not lead to losses in the rate as the following proposition shows. Note that the condition is not restrictive since any estimator of can be improved by using instead.

Proposition 4.1

On Assumption 4 let be a consistent estimator which is independent of the data and fulfills for the inequality

| (18) |

with a constant . Furthermore, we suppose almost surely. Then satisfies the asymptotic risk bound

where the expectation is taken with respect to the common distribution of the observations and the preestimator .

To use on an independent sample as preestimator, we establish a concentration result for the proposed procedure. We require to be uniformly sub-Gaussian (see, e.g., van de Geer [28]). That means there are constants such that the following concentration inequality holds for all and

| (19) |

Proposition 4.2

Concentration (20) is stronger than needed in Proposition 4.1. To apply the proposed estimation procedure, let and be two independent samples with noise levels and as well as sample sizes and , respectively. Using for the estimator , we construct adaptively on . We suppose grows at most polynomial in , that is holds for some , cf. [27]. To satisfy (18), it is sufficient if there exists a power , which can be arbitrary small, such that owing to the exponential inequality (20). Using , we estimate

for . Thus, relatively to all available data the necessary number of observations for the preestimator tends to zero.

5 Discussion and application

5.1 Numerical example

We apply the proposed estimation procedure to the variance gamma model. In view of the empirical study [17] we choose the parameters and . the martingale condition (3) yields then . According to the different choices of , we set as maximal value of .

The deterministic design of the sample is distributed normally with mean zero and variance . The observations are computed from the characteristic function using the fast Fourier transform method [7]. The additive noise consists of normal centered random variables with variance for some .

We estimate . Hence, we need , see Corollary 8 in [27]. By self-decomposablity of the model we apply the rearranged estimator given by (14). We use maturity , interest , smoothness , sample size and noise level , which generates values of on average . The results of 1000 Monte Carlo simulations are summarized in Tables 1 and 2.

=270pt 40 20.7998 23.3589 20 5.8362 7.7724 10 1.0505 2.4534 4 0.1729 1.1158

| 0.1408 | 0.0065 | 0.0126 | |

| 10.0000 | 1.0505 | 2.4534 | |

| 32.1016 | 77.5311 | ||

| 0.9556 | 0.4075 | 0.5602 |

In order to apply the estimation procedure, we need to choose the tuning parameters. Owing to the typically unknown smoothness , let the weight functions satisfy Assumption 3 for some large value . The weights for the parameters can be chosen as polynomial whereas is taken as a polynomial times a smooth function with support . The trimming parameter is included mainly for theoretical reasons and is not important to the implementation. The most crucial point is the choice of the cut-off value . For we implement the oracle method and an adaptive estimator based on the construction of Section 4 with sample size for .

5.2 Discussion

Due to the nonparametric setting, our estimators converge more slowly than with rate as in parametric models [10, 11, 17]. Although the studied estimation problem is only mildly ill-posed compared with classical nonparametric regression models and thus the polynomial rates are faster than in nonparametric models with which achieve logarithmic rates only [3]. In order to understand the convergence rate of the estimators for and better, we rewrite equation (11) in the distributional sense, denoting the Dirac distribution at zero by , and differentiate representation (9)

Hence, can be seen as Fourier transform of an s-times weakly differentiable function and estimating from noisy observations of corresponds to a nonparametric regression with regularity s. Since dividing by on the right-hand side of the above equation corresponds to taking the derivative in the spatial domain, the estimation of is similar to the estimation of the th derivative in a regression model. The convergence rate of is in line with the results of Belomestny and Reiß [3] for since their rate equals ours in the compound Poisson case .

For , the degree of ill-posedness is given by . This can be seen analytically by observing that the noise is governed by , which grows with rate . From a statistical point of view a higher value of leads to a more active Lévy process and hence, it is harder to distinguish the small jumps of the process from the additive noise. The influence of the time to maturity on the convergence rates is an interesting deviation from the analysis of Belomestny and Reiß [3]. The simulation shown in Table 1 demonstrates the improvement of the estimation for small the values of . The estimators and provide a complete calibration of the model. Although, estimating the -function at zero is most important and thus additional information through are crucial. Table 2 contains simulation results for the estimators and , , corresponding to oracle and -adaptive cut-off values, respectively. This adaptation to is a first step to a data-driven procedure and should be developed further.

Since the estimating equation (10) holds for all Lévy processes with finite variation, the proposed estimator can be more generally understood as estimator of . Thus, the estimation procedure can be applied to exponential Lévy models with Blumenthal–Getoor index larger than zero, for example, tempered stable processes. However, the analysis of the convergence rates does not carry over to more general Lévy processes since the polynomial decay of the , which is guaranteed by property (K), is essential for our proofs. Moreover, if has no bounded variation the behavior of the Lévy density at zero needs different methods and should be studied further. For instance, Belomestny [1] discusses the estimation of the fractional order for regular Lévy models of exponential type.

Even if the practitioner prefers specific parametric models that might achieve smaller errors and faster rates, the nonparametric method should be used as a goodness-of-fit test against model misspecification. To construct such tests, confidence sets need to be studied which is done by Söhl [24] in the framework of Lévy processes with finite activity. Based on this asymptotic analysis, Söhl and Trabs [25] construct confidence intervals in the self-decomposable model.

=200pt

5.3 Real data example

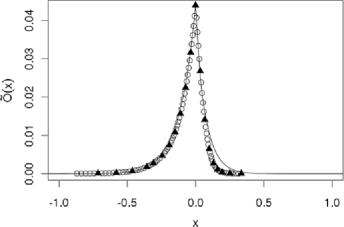

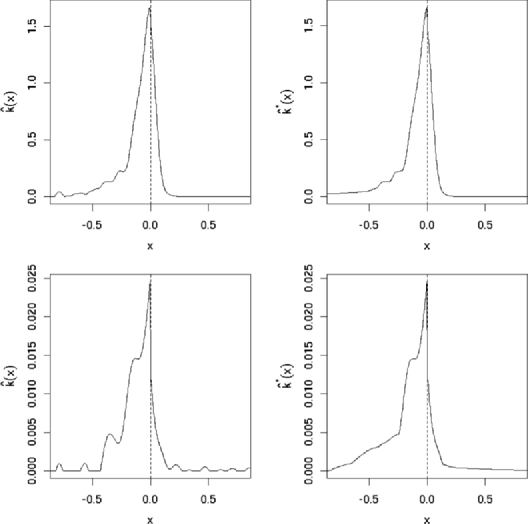

We apply our estimation method to a data set from the Deutsche Börse database Eurex.333Provided through the Collaborative Research Center 649 “Economic Risk”. It consists of settlement prices of put and call options on the DAX index with three and six months to maturity from 29 May 2008. The sample sizes are 101 and 106, respectively. The interest rate is chosen according to the put-call parity. The sub-sample for the preestimator consists of every fifth strike while the main estimation is done from the remaining data points. By a rule of thumb, the bid-ask spread is chosen as 1% of the option prices. Therefore, we get noise levels with values 0.0138 and 0.069 for the two maturities, respectively. Table 3 shows the result of the proposed method. As one would expect, the jump activity is smaller for a longer time to maturity. The estimator as well as the rearranged estimator are presented in Figure 2. In Figure 1, the calibrated model is used to generate the option function in the case of three months to maturity, where the data points used for the preestimator are marked with triangles in the figure. For a comparison of the outcome of our estimation procedure with the spectral calibration of Belomestny and Reiß [3], we refer to Söhl and Trabs [25].

6 Proofs

6.1 Proof of the upper bounds

Let us recall some results of [3]: Because of the -spline interpolation we obtain . Furthermore, the decomposition of the stochastic error in a linearization and a remainder ,

has the following properties.

Proposition 6.1

Upper bound for and (Theorem 3.2)

Since Theorem 3.2 can be proven analogously to Theorem 4.2 in [3], we only sketch the main steps. Note that in we can bound uniformly in representation (9), cf. Lemma 9 in [27]. Let us consider first. The definition of and , the decomposition of and representation (9) yield

Hence, we obtain

where all three summands can be estimated separately. The first one is a deterministic error term. It can be estimated using the decay of and the weight function property (13):

A bias-variance decomposition, with the definition , of the linear error term yields

Using the approximation result in Proposition 6.1, the bound of given by and property (13), we infer the estimate of the bias term

For the variance part, we make use of the properties of the linear spline functions as well as and the independence of . We estimate ()

To estimate the remaining term , we use Proposition 6.1, the property (13) of and the choice of . In addition the independence of and the uniform bound of their fourth moments comes into play.

Therefore, the total risk of is of order

uniformly over . Since the explicit choice of fulfills and holds by assumption, this bound simplifies to

Here balances the trade-off between the first and the second term whereby the third term is asymptotically negligible. We obtain the claimed rate.

For the only difference to the analysis for is the rescaling factor of in (13). Since its square appears in front of every term, we verify

Upper bound for (Theorem 3.4)

Similarly to the uniform bound of the bias of in Proposition 6.1, the following lemma holds true. It can be proved analogously to Proposition 1 in [3] and thus we omit the details.

Lemma 6.2

Assuming , we obtain uniformly over all Lévy triplets satisfying Assumption 1 and .

For convenience, we write and such that . Using for , it is sufficient to consider the loss of on . On one can proceed analogously. We split the risk into a deterministic error, an error caused by and a stochastic error,

The support of yields . The deterministic term can be estimated in the spatial domain, where we use the local smoothness of . For pointwise convergence rates, this was done in [2]. We decompose using

Cauchy–Schwarz’s inequality, the estimate and Fubini’s theorem yield

Using a Taylor expansion, we split in a polynomial part and a remainder:

We estimate by for

With twofold usage of Cauchy–Schwarz and with Fubini’s theorem we obtain

Therefore, we have .

To estimate the stochastic error , we bound the term . Let us introduce the notation

For all where we obtain . For the estimate follows from (15). This yields

Therefore, holds for all . We obtain a similar decomposition as [15],

Since , we have

It follows with Plancherel’s equality

Both terms can be estimated similarly. Thus, we only write it down for , where stronger conditions are needed. Lemma 6.2 and , , yield

Therefore, we have shown . The assertion follows from the asymptotic optimal choice and the assumption on the risk of .

6.2 Proof of Proposition 4.1

Step 1: Let be a deterministic sequence such that there is a constant with . Let the estimator use the cut-off value and the trimming parameter , with , as defined in (16) and (17). Then we can show the asymptotic risk bound as follows: By construction holds . Hence, fulfills condition (15) for each pair and thus we deduce from Theorem 3.2

| (21) | |||

The first factor has the claimed order, since follows with easy calculations from . Hence, the claim follows once we have bound the sum in the bracket of equation (6.2). For the second term, this is implied by

To estimate the third term, we obtain from and

Step 2: Let . Note that satisfies the condition (15) on the set . Using the independence of and , the almost sure bound and the concentration of , we deduce from step 1:

Since the second term decreases faster then the first one for , we obtain the claimed rate.

6.3 Proof of Proposition 4.2

Recall that the cut-off value of is given by . For we obtain from the definition of the estimator and the decomposition of the stochastic error into linear part and remainder:

We will bound all three probabilities separately. To that end, let be suitable non-negative constants not depending on and .

The event in is deterministic. Hence, the same estimate on the deterministic error as in Theorem 3.2

yields for all .

To bound we infer from the definition of , the linearity of the errors in and from the estimate of the term in Theorem 3.2

where the coefficients are given by for . To apply (19), we deduce from , the weight function property (13) and the assumption

This implies through the concentration inequality of

for all .

It remains to estimate probability . The bound of in Proposition 6.1 ii) yields

The first addend gets small owing to Proposition 6.1(i):

For the second one, we obtain

Thus,

with . Denoting the diagonal term and the cross term as

respectively, we obtain

The first summand vanishes for . To estimate the probabilities on and , we establish the bound

| (22) |

for . Hence,

which yields together with (19)

To derive an exponential inequality for the U-statistic , we apply the martingale idea in [13]. Because of the independence and the centering of the , the process is a martingale with respect to its natural filtration (setting ):

We apply the martingale version of the Bernstein inequality, see Theorem VII.3.6 in [22], which yields for arbitrary

Hence, we consider the increment , for . Denoting , we estimate using (22)

Thus, by Assumption (19) we obtain for all

The quadratic variation of is given by

W.l.o.g. we can assume . Otherwise follows which implies for all and thus . Then would hold for . Hence, we obtain:

To apply inequality (19), we estimate analogous to (6.3) and obtain

We deduce from Bernstein’s inequality (6.3)

By choosing and , we get

For all , we have and hence,

Putting the bounds of and together yields for a constant and all with

Appendix: Proof of Lemma 2.1

Part (i) The martingale condition yields

W.l.o.g. we assume , and because of the symmetry of the cosine.

We split the integral domain into three parts:

| (1) |

Using by assumption and the constant , we estimate

In the second part the dependence on comes into play. Writing , the Taylor series of the exponential function together with dominated convergence yield

To bound the last term in the above display, we proceed as Lemma 53.9 in [21]. By the bounded variation of , we can define a bounded signed measure via . Noting that can be bounded uniformly with a constant , Fubini’s theorem yields

Obtaining for the third part in (1) , we have with as defined in Lemma 2.1

We deduce the estimate for with .

Part (ii) follows immediately from the explicit choice of .

Acknowledgements

The author thanks Markus Reiß and Jakob Söhl for providing many helpful ideas and comments. The research was supported by the Collaborative Research Center 649 “Economic Risk” of the German Research Foundation (Deutsche Forschungsgemeinschaft).

Characteristic exponent and lower risk bounds \slink[doi]10.3150/12-BEJ478SUPP \sdatatype.pdf \sfilenameBEJ478_supp.pdf \sdescriptionFirst, we derive the representation of the characteristic exponent given in Proposition 2.2. Furthermore, we discuss Le Cam’s asymptotic equivalence of our nonparametric regression model to the continuous-time white noise model and show lower bounds in the latter one.

References

- [1] {barticle}[mr] \bauthor\bsnmBelomestny, \bfnmDenis\binitsD. (\byear2010). \btitleSpectral estimation of the fractional order of a Lévy process. \bjournalAnn. Statist. \bvolume38 \bpages317–351. \biddoi=10.1214/09-AOS715, issn=0090-5364, mr=2589324 \bptokimsref \endbibitem

- [2] {barticle}[mr] \bauthor\bsnmBelomestny, \bfnmDenis\binitsD. (\byear2011). \btitleStatistical inference for time-changed Lévy processes via composite characteristic function estimation. \bjournalAnn. Statist. \bvolume39 \bpages2205–2242. \biddoi=10.1214/11-AOS901, issn=0090-5364, mr=2893866 \bptokimsref \endbibitem

- [3] {barticle}[mr] \bauthor\bsnmBelomestny, \bfnmDenis\binitsD. &\bauthor\bsnmReiß, \bfnmMarkus\binitsM. (\byear2006). \btitleSpectral calibration of exponential Lévy models. \bjournalFinance Stoch. \bvolume10 \bpages449–474. \biddoi=10.1007/s00780-006-0021-5, issn=0949-2984, mr=2276314 \bptokimsref \endbibitem

- [4] {barticle}[mr] \bauthor\bsnmBelomestny, \bfnmDenis\binitsD. &\bauthor\bsnmSchoenmakers, \bfnmJohn\binitsJ. (\byear2011). \btitleA jump-diffusion Libor model and its robust calibration. \bjournalQuant. Finance \bvolume11 \bpages529–546. \biddoi=10.1080/14697680903295176, issn=1469-7688, mr=2784473 \bptokimsref \endbibitem

- [5] {barticle}[author] \bauthor\bsnmCarr, \bfnmPeter\binitsP., \bauthor\bsnmGeman, \bfnmHélyette\binitsH., \bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B. &\bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear2002). \btitleThe fine structure of asset returns: An empirical investigation. \bjournalJ. Bus. \bvolume75 \bpages305–332. \bptokimsref \endbibitem

- [6] {barticle}[mr] \bauthor\bsnmCarr, \bfnmPeter\binitsP., \bauthor\bsnmGeman, \bfnmHélyette\binitsH., \bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B. &\bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear2007). \btitleSelf-decomposability and option pricing. \bjournalMath. Finance \bvolume17 \bpages31–57. \biddoi=10.1111/j.1467-9965.2007.00293.x, issn=0960-1627, mr=2281791 \bptokimsref \endbibitem

- [7] {barticle}[author] \bauthor\bsnmCarr, \bfnmPeter\binitsP. &\bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B. (\byear1999). \btitleOption valuation using the fast Fourier transform. \bjournalJ. Comput. Finance \bvolume2 \bpages61–73. \bptokimsref \endbibitem

- [8] {barticle}[mr] \bauthor\bsnmChernozhukov, \bfnmV.\binitsV., \bauthor\bsnmFernández-Val, \bfnmI.\binitsI. &\bauthor\bsnmGalichon, \bfnmA.\binitsA. (\byear2009). \btitleImproving point and interval estimators of monotone functions by rearrangement. \bjournalBiometrika \bvolume96 \bpages559–575. \biddoi=10.1093/biomet/asp030, issn=0006-3444, mr=2538757 \bptokimsref \endbibitem

- [9] {barticle}[author] \bauthor\bsnmCont, \bfnmRama\binitsR. &\bauthor\bsnmTankov, \bfnmPeter\binitsP. (\byear2004). \btitleNon-parametric calibration of jump-diffusion option pricing models. \bjournalJ. Comput. Finance \bvolume7 \bpages1–49. \bptokimsref \endbibitem

- [10] {bmisc}[author] \bauthor\bsnmEberlein, \bfnmErnst\binitsE. (\byear2012). \bhowpublishedFourier based valuation methods in mathematical finance. Preprint. Univ. Freiburg. \bptokimsref \endbibitem

- [11] {barticle}[author] \bauthor\bsnmEberlein, \bfnmErnst\binitsE., \bauthor\bsnmKeller, \bfnmUlrich\binitsU. &\bauthor\bsnmPrause, \bfnmKarsten\binitsK. (\byear1998). \btitleNew insights into smile, mispricing and value at risk: The hyperbolic model. \bjournalJ. Bus. \bvolume71 \bpages371–406. \bptokimsref \endbibitem

- [12] {barticle}[mr] \bauthor\bsnmEberlein, \bfnmErnst\binitsE. &\bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B. (\byear2009). \btitleSato processes and the valuation of structured products. \bjournalQuant. Finance \bvolume9 \bpages27–42. \biddoi=10.1080/14697680701861419, issn=1469-7688, mr=2504500 \bptokimsref \endbibitem

- [13] {bincollection}[auto] \bauthor\bsnmHoudré, \bfnmChristian\binitsC. &\bauthor\bsnmReynaud-Bouret, \bfnmPatricia\binitsP. (\byear2003). \btitleExponential inqualities, with constants, for -statistics of order two. In \bbooktitleStochastic Inequalities and Applications (\beditor\bfnmEvariste\binitsE. \bsnmGiné, \beditor\bfnmChristian\binitsC. \bsnmHoudré &\beditor\bfnmDavid\binitsD. \bsnmNualart, eds.). \bseriesProgress in Probability \bvolume56 \bpages55–69. \blocationBasel: \bpublisherBirkhäuser. \bptokimsref \endbibitem

- [14] {barticle}[mr] \bauthor\bsnmJongbloed, \bfnmG.\binitsG., \bauthor\bparticlevan der \bsnmMeulen, \bfnmF. H.\binitsF.H. &\bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA.W. (\byear2005). \btitleNonparametric inference for Lévy-driven Ornstein–Uhlenbeck processes. \bjournalBernoulli \bvolume11 \bpages759–791. \biddoi=10.3150/bj/1130077593, issn=1350-7265, mr=2172840 \bptokimsref \endbibitem

- [15] {barticle}[mr] \bauthor\bsnmKappus, \bfnmJohanna\binitsJ. &\bauthor\bsnmReiß, \bfnmMarkus\binitsM. (\byear2010). \btitleEstimation of the characteristics of a Lévy process observed at arbitrary frequency. \bjournalStat. Neerl. \bvolume64 \bpages314–328. \biddoi=10.1111/j.1467-9574.2010.00461.x, issn=0039-0402, mr=2683463 \bptokimsref \endbibitem

- [16] {barticle}[mr] \bauthor\bsnmKeller-Ressel, \bfnmMartin\binitsM. &\bauthor\bsnmMijatović, \bfnmAleksandar\binitsA. (\byear2012). \btitleOn the limit distributions of continuous-state branching processes with immigration. \bjournalStochastic Process. Appl. \bvolume122 \bpages2329–2345. \biddoi=10.1016/j.spa.2012.03.012, issn=0304-4149, mr=2922631 \bptokimsref \endbibitem

- [17] {barticle}[author] \bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B., \bauthor\bsnmCarr, \bfnmPeter P.\binitsP.P. &\bauthor\bsnmChang, \bfnmEric C.\binitsE.C. (\byear1998). \btitleThe variance gamma process and option pricing. \bjournalEurop. Finance Rev. \bvolume2 \bpages79–105. \bptokimsref \endbibitem

- [18] {barticle}[author] \bauthor\bsnmMadan, \bfnmDilip B.\binitsD.B. &\bauthor\bsnmSeneta, \bfnmEugene\binitsE. (\byear1990). \btitleThe Variance Gamma (VG) model for share market returns. \bjournalJ. Bus. \bvolume63 \bpages511–524. \bptokimsref \endbibitem

- [19] {barticle}[author] \bauthor\bsnmMerton, \bfnmRobert C.\binitsR.C. (\byear1976). \btitleOption pricing when underlying stock returns are discontinuous. \bjournalJ. Finan. Econ. \bvolume3 \bpages125–144. \bptokimsref \endbibitem

- [20] {barticle}[mr] \bauthor\bsnmSato, \bfnmKen-iti\binitsK.i. (\byear1991). \btitleSelf-similar processes with independent increments. \bjournalProbab. Theory Related Fields \bvolume89 \bpages285–300. \biddoi=10.1007/BF01198788, issn=0178-8051, mr=1113220 \bptokimsref \endbibitem

- [21] {bbook}[mr] \bauthor\bsnmSato, \bfnmKen-iti\binitsK.i. (\byear1999). \btitleLévy Processes and Infinitely Divisible Distributions. \bseriesCambridge Studies in Advanced Mathematics \bvolume68. \blocationCambridge: \bpublisherCambridge Univ. Press. \bidmr=1739520 \bptokimsref \endbibitem

- [22] {bbook}[author] \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA.N. (\byear1996). \btitleProbability, \bedition2nd ed. \blocationNew York: \bpublisherSpringer. \bidmr=1368405 \bptokimsref \endbibitem

- [23] {barticle}[mr] \bauthor\bsnmSöhl, \bfnmJakob\binitsJ. (\byear2010). \btitlePolar sets for anisotropic Gaussian random fields. \bjournalStatist. Probab. Lett. \bvolume80 \bpages840–847. \biddoi=10.1016/j.spl.2010.01.018, issn=0167-7152, mr=2608824 \bptokimsref \endbibitem

- [24] {bmisc}[author] \bauthor\bsnmSöhl, \bfnmJakob\binitsJ. (\byear2012). \bhowpublishedConfidence sets in nonparametric calibration of exponential Lévy models. Available at arXiv:\arxivurl1202.6611. \bptokimsref \endbibitem

- [25] {bmisc}[author] \bauthor\bsnmSöhl, \bfnmJakob\binitsJ. &\bauthor\bsnmTrabs, \bfnmMathias\binitsM. (\byear2014). \bhowpublishedOption calibration of exponential Lévy models: Confidence intervals and empirical results. J. Comput. Finance. To appear. \bptokimsref \endbibitem

- [26] {bincollection}[mr] \bauthor\bsnmTankov, \bfnmPeter\binitsP. (\byear2011). \btitlePricing and hedging in exponential Lévy models: Review of recent results. In \bbooktitleParis-Princeton Lectures on Mathematical Finance 2010. \bseriesLecture Notes in Math. \bvolume2003 \bpages319–359. \blocationBerlin: \bpublisherSpringer. \biddoi=10.1007/978-3-642-14660-2_5, mr=2762364 \bptokimsref \endbibitem

- [27] {bmisc}[author] \bauthor\bsnmTrabs, \bfnmMathias\binitsM. (\byear2014). \bhowpublishedSupplement to “Calibration of self-decomposable Lévy models”. DOI:\doiurl10.3150/12-BEJ478. \bptokimsref \endbibitem

- [28] {bbook}[author] \bauthor\bparticlevan de \bsnmGeer, \bfnmSara\binitsS. (\byear2000). \btitleEmpirical Processes in M-estimation. \blocationCambridge: \bpublisherCambridge Univ. Press. \bptokimsref \endbibitem