Chain: A Dynamic Double Auction Framework for Matching Patient Agents

Abstract

In this paper we present and evaluate a general framework for the design of truthful auctions for matching agents in a dynamic, two-sided market. A single commodity, such as a resource or a task, is bought and sold by multiple buyers and sellers that arrive and depart over time. Our algorithm, Chain, provides the first framework that allows a truthful dynamic double auction (DA) to be constructed from a truthful, single-period (i.e. static) double-auction rule. The pricing and matching method of the Chain construction is unique amongst dynamic-auction rules that adopt the same building block. We examine experimentally the allocative efficiency of Chain when instantiated on various single-period rules, including the canonical McAfee double-auction rule. For a baseline we also consider non-truthful double auctions populated with “zero-intelligence plus”-style learning agents. Chain-based auctions perform well in comparison with other schemes, especially as arrival intensity falls and agent valuations become more volatile.

1 Introduction

Electronic markets are increasingly popular as a method to facilitate increased efficiency in the supply chain, with firms using markets to procure goods and services. Two-sided markets facilitate trade between many buyers and many sellers and find application to trading diverse resources, including bandwidth, securities and pollution rights. Recent years have also brought increased attention to resource allocation in the context of on-demand computing and grid computing. Even within settings of cooperative coordination, such as those of multiple robots, researchers have turned to auctions as methods for task allocation and joint exploration (?, ?, ?).

In this paper we consider a dynamic two-sided market for a single commodity, for instance a unit of a resource (e.g. time on a computer, some quantity of memory chips) or a task to perform (e.g. a standard database query to execute, a location to visit). Each agent, whether buyer or seller, arrives dynamically and needs to be matched within a time interval. Cast as a task-allocation problem, a seller can perform the task when allocated within some time interval and incurs a cost when assigned. A buyer has positive value for the task being assigned (to any seller) within some time interval. The arrival time, acceptable time interval, and value (negative for a seller) for a trade are all private information to an agent. Agents are self-interested and can choose to misrepresent all and any of this information to the market in order to obtain a more desirable price.

The matching problem combines elements of online algorithms and sequential decision making with considerations from mechanism design. Unlike traditional sequential decision making, a protocol for this problem must provide incentives for agents to report truthful information to a match-maker. Unlike traditional mechanism design, this is a dynamic problem with agents that arrive and leave over time. We model this problem as a dynamic double auction (DA) for identical items. The match-maker becomes the auctioneer. Each seller brings a task to be performed during a time window and each buyer brings the capability to perform a single task. The double-auction setting also is of interest in its own right as a protocol for matching in a dynamic business-to-business exchange.

Uncertainty about the future coupled with the two-sided nature of the market leads to an interesting mechanism design problem. For example, consider the scenario where the auctioneer must decide how (and whether) to match a seller with reported cost of $6 at the end of its time interval with a present and unmatched buyer, one of which has a reported value of $8 and one a reported value of $9. Should the auctioneer pair the higher bidder with the seller? What happens if a seller, willing to sell for $4, arrives after the auctioneer acts upon the matching decision? How should the matching algorithm be designed so that no agent can benefit from misstating its earliest arrival, latest departure, or value for a trade?

Chain provides a general framework that allows a truthful dynamic double auction to be constructed from a truthful, single-period (i.e. static) double-auction rule. The auctions constructed by Chain are truthful, in the sense that the dominant strategy for an agent, whatever the future auction dynamics and bids from other agents, is to report its true value for a trade (negative if selling) and true patience (maximal tolerance for trade delay) immediately upon arrival into the market. We also allow for randomized mechanisms and, in this case, require strong truthfulness: the DA should be truthful for all possible random coin flips of the mechanism. One of the DAs in the class of auctions implied by Chain is a dynamic generalization of McAfee’s (?) canonical truthful, no-deficit auction for a single period. Thus, we provide the first examples of truthful, dynamic DAs that allow for dynamic price competition between buyers and sellers.111The closest work in the literature is due to Blum et al. (?), who present a truthful, dynamic DA for our model that matches bids and asks based on a price sampled from some bid-independent distribution. We compare the performance of our schemes with this scheme in Section 6.

The main technical challenge presented by dynamic DAs is to provide truthfulness without incurring a budget deficit, while handling uncertainty about future trade opportunities. Of particular concern is to ensure that an agent does not indirectly affect its price through the effect of its bid on the prices faced by other agents and thus other supply and demand in the market. We need to preclude this because the availability of trades depends on the price faced by other agents. For example, a buyer that is required to pay $4 in the DA to trade might like to decrease the price that a potentially matching seller will receive from $6 to $3 to allow for trade.

Chain is a modular approach to auction design, which takes as a building block a single-period matching rule and provides a method to invoke the rule in each of multiple periods while also providing for truthfulness. We characterize properties that a well-defined single-period matching rule must satisfy in order for Chain to be truthful. We further identify the technical property of strong no-trade, with which we can isolate agents that fail to trade in the current period but can nevertheless survive and be eligible to trade in a future period. An auction designer defines the strong no-trade predicate, in addition to providing a well-defined single-period matching rule. Instances within this class include those constructed in terms of both “price-based” matching rules and “competition-based” matching rules. Both can depend on history and be adaptive, but only the competition-based rules use the active bids and asks to determine the prices in the current period, facilitating a more direct competitive processes.

In proving that Chain, when combined with a well-defined matching rule and a valid strong no-trade predicate, is truthful we leverage a recent price-based characterization for truthful online mechanisms (?). We also show that the pricing and matching rules defined by Chain are unique amongst the family of mechanisms that are constructed with a single-period matching rule as a building block. Throughout our work we assume that a constant limits every buyer and seller’s patience. To motivate this assumption we provide a simple environment in which no truthful, no-deficit DA can implement some constant fraction of the number of the efficient trades, for any constant.

We adopt allocative efficiency as our design objective, which is to say auction protocols that maximize the expected total value from the sequence of trades. We also consider net efficiency, wherein any net outflow of payments to the marketmaker is also accounted for in considering the quality of a design. Experimental results explore the allocative efficiency of Chain when instantiated to various single-period matching rules and for a range of different assumptions about market volatility and maximal patience. For a baseline we consider the efficiency of a standard (non-truthful) open outcry DA populated with simple adaptive trading agents modeled after “zero-intelligence plus” (ZIP) agents (?, ?). We also compare the efficiency of Chain with that of a truthful online DA due to Blum et al. (?), which selects a fixed trading price to guarantee competitiveness in an adversarial model.

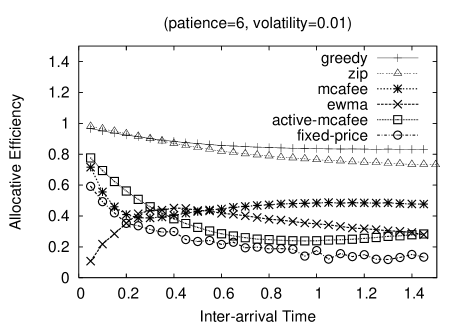

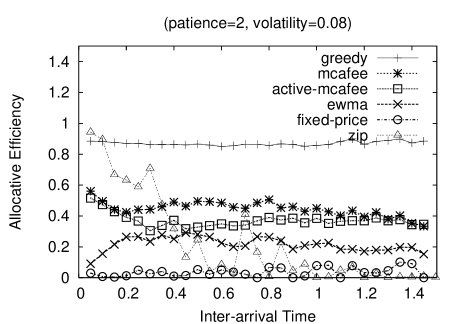

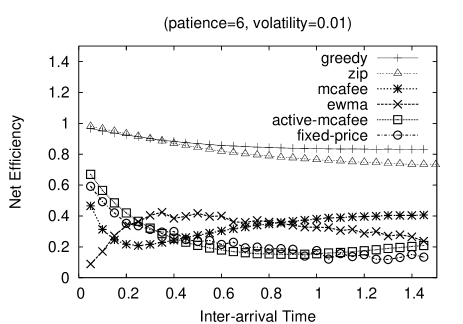

From within the truthful mechanisms we find that adaptive, price-based instantiations of Chain are the most effective for high arrival intensity and low volatility. Even defining a single, well-chosen price that is optimized for the market conditions can be reasonably effective in promoting efficient trades in low volatility environments. On the other hand, for medium to low arrival intensity and medium to high volatility we find that the Chain-based DAs that allow for dynamic price competition, such as the McAfee-based rule, are most efficient. The same qualitative observations hold whether one is interested in allocative efficiency or net efficiency, although the adaptive, price-based methods have better performance in terms of net efficiency. The Blum et al. (?) rule fairs poorly in our tests, which is perhaps unsurprising given that it is optimized for worst-case performance in an adversarial setting. When populated with ZIP agents, we find that non-truthful DAs can provide very good efficiency in low volatility environments but poor performance in high volatility environments. The good performance of the ZIP-based market occurs when agents learn to bid approximately truthfully; i.e., when the market operates as if truthful, but without incurring the stringent cost (e.g., through trading constraints) of imposing truthfulness explicitly. An equilibrium analysis is available only for the truthful DAs; we have no way of knowing how close the ZIP agents are to playing an equilibrium, and note that the ZIP agents do not even consider performing time-based manipulations.

1.1 Outline

Section 2 introduces the dynamic DA model, including our assumptions, and presents desiderata for online DAs and a price-based characterization for the design of truthful dynamic auctions. Section 3 defines the Chain algorithm together with the building block of a well-defined, single-period matching rule and the strong no-trade predicate. Section 4 gives a number of instantiations to both price-based and competition-based matching rules, including a general method to define the strong no-trade predicate given a price-based instantiation. Section 5 proves truthfulness, no-deficit and feasibility of the Chain auctions and also establishes their uniqueness amongst auctions constructed from the same single-period matching-rule building block. The importance of the assumption about maximal agent patience is established. Section 6 presents our empirical analysis, including a description of the simple adaptive agents that we use to populate a non-truthful open-outcry DA and provide a benchmark. Section 7 gives related work. In Section 8 we conclude with a discussion about the merits of truthfulness in markets and present possible extensions.

2 Preliminaries: Basic Definitions

Consider a dynamic auction model with discrete, possibly infinite, time periods , indexed by . The double auction (DA) provides a market for a single commodity. Agents are either buyers or sellers interested in trading a single unit of the commodity. An agent’s type, , where is the set of possible types for agent , defines an arrival , departure , and value for trade. If the agent is a buyer, then . If the agent is a seller, then . We assume a maximal patience , so that for all agents.

The arrival time models the first time at which an agent learns about the market or learns about its value for a trade. Thus, information about its type is not available before period (not even to agent ) and the agent cannot engage in trade before period . The departure time, , models the final period in which a buyer has positive value for a trade, or the final period in which a seller is willing to engage in trade. We model risk-neutral agents with quasi-linear utility, when a trade occurs in and payment is collected (with if the agent is a seller). Agents are rational and self-interested, and act to maximize expected utility. By assumption, sellers have no utility for payments received after their true departure period.

Throughout this paper we adopt bid to refer, generically, to a claim that an agent – either a buyer or a seller – makes to a DA about its type. In addition, when we need to be specific about the distinction between claims made by buyers and claims made by sellers we refer to the bid from a buyer and the ask from a seller.

2.1 Example

Consider the following naive generalization of the (static) trade-reduction DA (?, ?) to this dynamic environment. A bid from an agent is a claim about its type , necessarily made in period . Bids are active while and no trade has occurred.

Then in each period , use the trade-reduction DA to determine which (if any) of the active bids trade and at what price. These trades occur immediately. The trade-reduction DA (tr-DA) works as follows: Let denote the set of bids and denote the set of asks. Insert a dummy bid with value into and a dummy ask with value into . When and then sort and in order of decreasing value. Let and denote the bid and ask values with denoting the dummy bid-ask pair. Let index the last pair of bids and asks to clear in the efficient trade, such that and . When then bids and asks trade and payment is collected from each winning buyer and payment is made to each winning seller.

First consider a static tr-DA with the following bids and asks:

B S 15 -1 10 -1 4 -2 3 -2 -5

The line indicates that bids (1–4) and asks (1–4) could be matched for efficient trade. By the rules of the tr-DA, bids (1–3) and asks (1–3) trade, with payments $3 collected from winning buyers and payment $2 made to winning sellers. The auctioneer earns a profit of $3. The asterisk notation indicates the bids and asks that trade. The tr-DA is truthful, in the sense that it is a dominant-strategy for every agent to report its true value whatever the reports of other agents. For intuition, consider the buy-side. The payment made by winners is independent of their bid price while the losing bidder could only win by bidding more than $4, at which point his payment would be $4 and more than his true value.

Now consider a dynamic variation with buyer types and seller types . When agents are truthful, the dynamic tr-DA plays out as follows:

period 1 period 2 B S B S 15 -1 10 -1 10 -2 4 -2 4 -5 3 -5

In period 1, buyer 1 and seller 1 trade at payments of $10 and $2 respectively. In period 2, buyer 2 and seller 2 trade at payments of $4 and $2 respectively. But now we can construct two kinds of manipulation to show that this dynamic DA is not truthful. First, buyer 1 can do better by delaying his reported arrival until period 2:

period 1 period 2 B S B S 10 -1 15 -1 4 -2 4 -2 -5 3 -5

Now, buyer 2 trades in period 1 and does not set the price to buyer 1 in period 2. Instead, buyer 1 now trades in period 2 and makes payment $4.

Second, buyer 3 can do better by increasing his reported value:

period 1 period 2 B S B S 15 -1 6 -1 10 -2 3 -2 6 -5 -5

Now, buyers 1 and 2 both trade in period 1 and this allows buyer 3 to win (at a price below his true value) in period 2. This is a particularly interesting manipulation because the agent’s manipulation is by increasing its bid above its true value. By doing so, it allows more trades to occur and makes the auction less competitive in the next period.

2.2 Dynamic Double Auctions: Desiderata

We consider only direct-revelation, dynamic DAs that restrict the message that an agent can send to the auctioneer to a single, direct claim about its type. We also consider “closed” auctions so that an agent receives no feedback before reporting its type and cannot condition its strategy on the report of another agent.222The restriction to direct-revelation, online mechanisms is without loss of generality when combined with a simple heart-beat message from an agent to indicate its presence in any period during its reported arrival-departure interval. See the work of Pai and Vohra (?) and Parkes (?).

Given this, let denote the set of agent types reported in period , denote a complete type profile (perhaps unbounded), and denote the type profile restricted to agents with (reported) arrival no later than period . A report represents a commitment to buy (sell) one unit of the commodity in any period for a payment of at most . Thus, if a seller reports a departure time it must commit to complete a trade that occurs after her true departure and even though a seller is modeled as having no utility for payments received after her true departure.

A dynamic DA, , defines an allocation policy and payment policy , where indicates whether or not agent trades in period given reports and indicates a payment made by agent , negative if this is a payment received by the agent. The auction rules can also be stochastic, so that and are random variables. For a dynamic DA to be well defined, it must hold that in at most one period and zero otherwise, and the payment collected from agent is zero except in periods .

In formalizing the desiderata for dynamic DAs, it will be convenient to adopt to denote the complete sequence of allocation decisions given reports , with shorthand and to indicate whether agent trades during its reported arrival-departure interval, and the total payment made by agent , respectively. By a slight abuse of notation, we write to denote that agent reported a type no later than period . Let denote the set of buyers and denote the set of sellers.

We shall require that the dynamic DA satisfies no-deficit, feasibility, individual-rationality and truthfulness. No-deficit ensures that the auctioneer has a cash surplus in every period:

Definition 1 (no-deficit)

A dynamic DA, is no-deficit if:

| (1) |

Feasibility ensures that the auctioneer does not need to take a short position in the commodity traded in the market in any period:

Definition 2 (feasible trade)

A dynamic DA, is feasible if:

| (2) |

This definition of feasible trade assumes that the auctioneer can “hold” an item that is matched between a seller-buyer pair, for instance only releasing it to the buyer upon his reported departure. See the remark concluding this section for a discussion of this assumption.

Let denote the value of an agent with type for the allocation decision made by policy given report , i.e. if the agent trades in period and if it trades outside of this interval and is a buyer, or if it trades outside of this interval and is a seller. Individual-rationality requires that agent ’s utility is non-negative when it reports its true type, whatever the reports of other agents:

Definition 3 (individual-rational)

A dynamic DA, is individual-rational (IR) if for all , all .

In order to define truthfulness, we introduce notation for to denote the set of available misreports to an agent with true type . In the standard model adopted in offline mechanism design, it is typical to assume with all misreports available. Here, we shall assume no early-arrival misreports, with . This assumption of limited misreports is adopted in earlier work on online mechanism design (?), and is well-motivated when the arrival time is the first period in which a buyer first decides to acquire an item or the period in which a seller first decides to sell an item.

Definition 4 (truthful)

Dynamic DA, , is dominant-strategy incentive-compatible, or truthful, given limited misreports if:

for all , all , all , all .

This is a robust equilibrium concept: an agent maximizes its utility by reporting its true type whatever the reports of other agents. Truthfulness is useful because it simplifies the decision problem facing bidders: an agent can determine its optimal bidding strategy without a model of either the auction dynamics or the other agents. In the case that the allocation and payment policy is stochastic, then we adopt the requirement of strong truthfulness so that an agent maximizes its utility whatever the random sequence of coin flips within the auction.

Remark.

The flexible definition of feasibility, in which the auctioneer is able to take a long position in the commodity, allows the auctioneer to time trades by receiving the unit sold by a seller in one period but only releasing it to a buyer in a later period. This allows for truthfulness in environments in which bidders can overstate their departure period. In some settings this is an unreasonable requirement, however, for instance when the commodity represents a task that is performed, or because a physical good is being traded in an electronic market.333Note that if the task is a computational task, then tasks can be handled within this model by requiring that the seller performs the task when it is matched but with a commitment to hold onto the result until the matched buyer is ready to depart. In these cases, the definition of feasibility strengthened to require exact trade-balance in every period. The tradeoff is that available misreports must be further restricted, with agents limited to reporting no late-departures in addition to no early-arrivals (?, ?). For the rest of the paper we work in the “relaxed feasibility, no early-arrival” model. The Chain framework can be immediately extended to the “strong-feasibility, no early-arrival and no late-departure” model by executing trades immediately rather than delaying the trade until a buyer’s departure.

3 Chain: A Framework for Truthful Dynamic DAs

Chain provides a general algorithmic framework with which to construct truthful dynamic DAs from well-defined single-period matching rules, such as the tr-DA rules described in the earlier section.

Before introducing Chain we need a few more definitions: Bids reported to Chain are active while (for reported departure period ), and while the bid is unmatched and still eligible to be matched. In each period, a single-period matching rule is used to determine whether any of the active bids will trade and also which (if any) of the bids that do not match will remain active in the next period.

Now we define the building blocks, well-defined single-period matching rules, and introduce the important concept of a strong no-trade predicate, which is defined for a single-period matching rule.

3.1 Building Block: A Single-Period Matching Rule

In defining a matching rule, it is helpful to adopt and to denote the active bids and active asks in period , where there are and bids and asks respectively. The bids and asks that were active in earlier periods but are no longer active form the history in period , denoted where is the size of the history.

A single-period matching rule (hereafter a matching rule), defines an allocation rule and a payment rule . Here, we include random event to allow explicitly for stochastic matching and allocation rules.

Definition 5 (well-defined matching rule)

A matching rule is well-defined when it is strongly truthful, no-deficit, individual-rational, and strong-feasible.

Here, the properties of truthfulness, no-deficit, and individual-rationality are exactly the single-period specializations of those defined in the previous section. For instance, a matching rule is truthful in this sense when the dominant strategy for an agent in a DA defined with this rule, and in a static environment, is to bid truthfully and for all possible random events . Similarly for individual-rationality. No-deficit requires that the total payments are always non-negative. Strong-feasibility requires that exactly the same number of asks are accepted as bids, again for all random events.

One example of a well-defined matching rule is the tr-DA, which is invariant to the history of bids and asks. For an example of a well-defined, adaptive (history-dependent) and price-based matching rule, consider procedure SimpleMatch in Figure 1. The SimpleMatch matching rule computes the mean of the absolute value of the bids and asks in the history and adopts this as the clearing price in the current period. It is a stochastic matching rule because bids and asks are picked from the sets and at random and offered the price. We can reason about the properties of SimpleMatch as follows:

(a) truthful: the price is independent of the bids and the probability that a bid (or ask) is matched is independent of its bid (or ask) price

(b) no-deficit: payment is collected from each matched buyer and made to each matched seller

(c) individual-rational: only bids and asks are accepted.

(d) feasible: bids and asks are introduced to the “matched” set in balanced pairs

3.2 Reasoning about Trade (Im)Possibility

In addition to defining a matching rule , we allow a designer to (optionally) designate a subset of losing bids that satisfy a property of strong no-trade. Bids that satisfy strong no-trade are losing bids for which trade was not possible at any bid price (c.f. ask price for asks), and moreover for which additional independence conditions hold between bids provided with this designation.

We first define the weaker concept of no-trade. In the following, notation indicates the allocation decision made for bid (or ask) when its bid (ask) price is replaced with :

Definition 6 (no-trade)

Given matching rule then the set of agents, , for which no trade is possible in period and given random events are those for which , for every when and for every when .

It can easily happen that no trade is possible, for instance when the agent is a buyer and there are no sellers on the other side of the market. Let denote the set of agents designated with the property of strong no-trade. Unlike the no-trade property, strong no-trade need not be uniquely defined for a matching rule. To be valid, however, the construction offered by a designer for strong no-trade must satisfy the following:

Definition 7 (strong no-trade)

A construction for strong no-trade, , is valid for a matching rule when:

(a) with , whether or not is unchanged for all alternate reports while ,

(b) with , the set is unchanged for all reports while , and independent even of whether or not agent is present in the market.

The strong no-trade conditions must be checked only for agents with a reported departure later than the current period. Condition (a) requires that such an agent in cannot affect whether or not it satisfies the strong no-trade predicate as long as it continues to report a departure later than the current period. Condition (b) is defined recursively, and requires that if such an agent is identified as satisfying strong no-trade, then its own report must not affect the designation of strong no-trade to other agents, with reported departure later than the current period, while it continues to report a departure later than the current period – even if it delays its reported arrival until a later period.

Strong no-trade allows for flexibility in determining whether or not a bid is eligible for matching. Specifically, only those bids that satisfy strong no-trade amongst those that lose in the current period can remain as a candidate for trade in a future period. The property is defined to ensure that such a “surviving” agent does not, and could not, affect the set of other agents against which it competes in future periods.

Example 1

Consider the tr-DA matching rule defined earlier with bids and asks

B S

Bid 1 and ask 1 trade at price and respectively. because bids 2 and 3 could each trade if they had (unilaterally) submitted a bid price of greater than 10. Similarly for asks 2 and 3. Now consider the order book

B S

No trade occurs. In this case, . No trade is possible for any bids, even bids 2 and 3, because . But, trade is possible for asks 2 and 3, because and either ask could trade by submitting a low enough ask price.

Example 2

Consider the tr-DA matching rule and explore possible alternative constructions for strong no-trade.

(i) Dictatorial: in each period , identify an agent that could be present in the period in a way that is oblivious to all agent reports. Let denote the index of this agent. If , then include . Strong no-trade condition (a) is satisfied because whether or not is selected as the “dictator” is agent-independent, and given that it is selected, then whether or not trade is possible is agent-independent. Condition (b) is trivially satisfied because and there is no cross-agent coupling to consider.

(ii) . Consider the order book

B S

Suppose all bids and asks remain in the market for at least one more period. Clearly, . Consider the candidate construction . Strong no-trade condition (a) is satisfied because whether or not is in set is agent-independent. Condition (b) is not satisfied, however. Consider bid 2. If bid 2’s report had been instead of 2 then trade would be possible for bids 1 and 3, and . Thus, whether or not bids 1 and 3 satisfy the strong no-trade predicate depends on the value of bid 2. This is not a valid construction for strong no-trade for the tr-DA matching rule.

(iii) if or , and otherwise. As above, strong no-trade condition (a) is immediately satisfied. Moreover, condition (b) is now satisfied because trade is not possible for any bid or ask irrespective of bid values because there are simply not enough bids or asks to allow for trade with tr-DA (which needs at least 2 bids and at least 2 asks).

Example 3

Consider a variant of the SimpleMatch matching rule, defined with fixed price 9. We can again ask whether is a valid construction for strong no-trade. Throughout this example suppose all bids and asks remain in the market for at least one more period. First consider a bid with and two asks with values and . Here, because the asks cannot trade whatever their price since the bid is not high enough to meet the fixed trading price of 9. Moreover, is a valid construction; strong no-trade condition (a) is satisfied as above and condition (b) is satisfied because whether or not ask 2 is in (and thus ) is independent of the price on ask 1, and vice versa. But consider instead a bid with and an ask with . Now, and is our candidate strong no-trade set. However if bid 1 had declared value 10 instead of 8 then and ask 1 drops out of . Thus, strong no-trade condition (b) is not satisfied.

We see from the above examples that it can be quite delicate to provide a valid, non-trivial construction of strong no-trade. Note, however, that is a (trivial) valid construction for any matching rule. Note also that the strong no-trade conditions (a) and (b) require information about the reported departure period of a bid. Thus, while the matching rules do not use temporal information about bids, this information is used in the construction for strong no-trade.

3.3 Chain: From Matching Rules to Truthful, Dynamic DAs

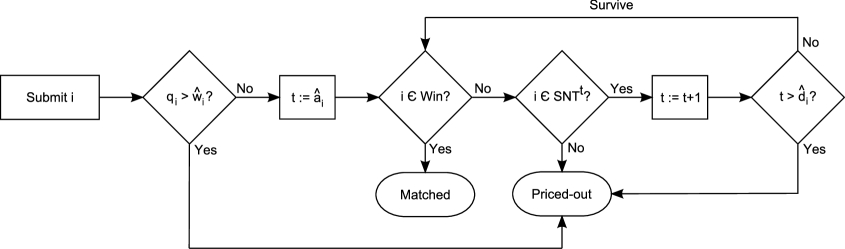

The control flow in Chain is illustrated in Figure 2. Upon arrival of a new bid, an admission decision is made and bid is admitted if its value is at least its admission price . An admitted bid competes in a sequence of matching events, where a matching event simply applies the matching rule to the set of active bids and asks. If a bid fails to match in some period and is not in the strong no-trade set (), then it is priced out and leaves the market without trading. Otherwise, if it is still before its departure time then it is available for matching in the next period.

Each bid is always in one of three states: active, matched or priced-out. Bids are active if they are admitted to the market until , or until they are matched or priced-out. An active bid becomes matched in the first period (if any) when it trades in the single-period matching rule. An active bid is marked as priced-out in the first period in which it loses but is not in the strong no-trade set. As soon as a bid is no longer active, it enters the history, and the information about its bid price can be used in defining matching rules for future periods.

Let denote the set of bids that will expire in the current period. A well-defined matching rule, when coupled with a valid strong no-trade construction, must provide Chain with the following information, given history , active bids and active asks , and expiration set in period :

(a) for each bid or ask, whether it wins or loses

(b) for each winning bid or ask, the payment collected (negative for an ask)

(c) for each losing bid or ask, whether or not it satisfies the strong no-trade condition

Note that the expiration set is only used for the strong no-trade construction. This information is not made available to the matching rule. The following table summarizes the use of this information within Chain. Note that a winning bid cannot be in set :

| Lose | priced-out | survive |

|---|---|---|

| Win | matched | n/a |

We describe Chain by defining the events that occur for a bid upon its arrival into the market, and then in each period in which it remains active:

-

Upon arrival: Consider all possible earlier arrival periods consistent with the reported type. There are no such periods to consider if the bid is maximally patient. If the bid would lose and not be in for any one of these arrival periods then it is not admitted. Otherwise, the bid would win in all periods for which , and define the admission price as:

(3) where is the payment the agent would have made (negative for a seller) in arrival period (as determined by running the myopic matching rule in that period). When the agent would lose in all earlier arrival periods (and so for all ), or the bid is maximally patient, then the admission price defaults to and the bid is admitted.

-

While active: Consider period . If the bid is selected to trade by the myopic matching rule, then mark it as matched and define final payment:

(4) where is the price (negative for a seller) determined by the myopic matching rule in the current period. If this is a buyer, then collect the payment but delay transferring the item until period . If this is a seller, then collect the item but delay making the payment until the reported departure period. If the bid loses and is not in then mark the bid as priced-out.

We illustrate Chain by instantiating it to various matching rules in the next section. In Section 5 we prove that Chain is strongly truthful and no-deficit when coupled with a well-defined matching rule and a valid strong no-trade construction. We will see that the delay in buyer delivery and seller payment ensures truthful revelation of a trader’s departure information. For instance, in the absence of this delay, a buyer might be able to do better by over-reporting departure information, still trading early enough but now for a lower price.

3.4 Comments

We choose not to allow the single-period matching rules to use the reported arrival and departure associated with active bids and asks. This maintains a clean separation between non-temporal considerations (in the matching rules) and temporal considerations (in the wider framework of Chain). This is also for simplicity. The single-period matching rules can be allowed to depend on the reported arrival-departure interval, as long as the (single-period) rules are monotonic in tighter arrival-departure intervals, in the sense that an agent that wins for some continues to win and for an improved price if it instead reports with . However, whether or not trade is possible must be independent of the reported arrival-departure interval and similarly for strong no-trade. Determinations such as these would need to be made with respect to the most patient type given report .

4 Practical Instantiations: Price-Based and Competition-Based Rules

In this section we offer a number of instantiations of the Chain online DA framework. We present two different classes of well-defined matching rules: those that are price-based and compute simple price statistics based on the history which are then used for matching, and those that we refer to as competition-based and leverage the history but also consider direct competition between the active bids and asks in any period. In each case, we establish that the matching rules are well-defined and provide a valid strong no-trade construction.

4.1 Price-Based Matching Rules

Each one of these rules constructs a single price, , in period based on the history of earlier bids and asks that are traded or expired. For this purpose we define variations on a real valued statistic, , that is used to define this price given the history. Generalizing the SimpleMatch procedure, as introduced in Section 5, the price is used to determine the trades in period . We also provide a construction for strong no-trade in this context.

The main concern in setting prices is that they may be too volatile, with price updates driving the admission price higher (via the max operator in the admission rule of Chain) and having the effect of pricing bids and asks out of the market. We describe various forms of smoothing and windowing, all designed to provide adaptivity while dampening short-term variations. In each case, the parameters (e.g. the smoothing factor, or the window size) can be determined empirically through off-line tuning.

We experiment with five price variants:

History-EWMA:

Exponentially-weighted moving average. The bid history, , is used to define price in period , computed as , where is a smoothing constant and is a statistic defined for bids and asks that enter the history in period . Experimentally we find that the mean statistic, of the absolute values of bids and asks that enter the history performs well with of 0.05 or lower for most scenarios that we test. For cases in which is not well-defined because of too few (or zero) new bids or asks, then we set .

History-median:

Compute price from a statistic over a fixed-size window of the most recent history, where is the window-size, i.e. defining bids introduced to history in periods . Experimentally, we find that the median statistic, of the absolute bid and ask values performs well for the scenarios we test, with the window size depending inversely with the volatility of agents’ valuations. Typically, we observe optimal window sizes of 20 and 150, depending on volatility. For cases in which is not well-defined because of too few (or zero) new bids or asks, then we set .

History-clearing:

Identical to the history-median rule except the statistic is defined as where and are the lowest value pair of trades that would be executed in the efficient (value-maximizing) trade given all bids and asks to enter history in periods . Empirically, we find similar optimal window sizes for history-clearing as for history-median.

History-McAfee:

Define the statistic to represent the McAfee price, defined in Section 4.2, for the bids in had they all simultaneously arrived.

Fixed price:

This simple rule computes a single fixed price for all trading periods, with the price optimized offline to maximize the average-case efficiency of the dynamic DA given Chain and the associated single-period matching rule that leverages price as the candidate trading price.

For each pricing variant, procedure Match (see Figures 3–4) is used to determine which bids win (at price ), which lose, and, of those that lose, which satisfy the strong no-trade predicate. The subroutine used to determine the current price is referred to as determineprice in Match. We provide as input to Match the set in addition to because Match also constructs the strong no-trade set, and is used exclusively for this purpose.

The proof of the following lemma is technical and is postponed until the Appendix.

Lemma 1

Procedure Match defines a valid strong no-trade construction.

Theorem 1

Procedure Match defines a well-defined matching rule and a valid strong no-trade construction.

Proof: No-deficit, feasibility, and individual-rationality are immediate by the construction of Match since bids and asks are added to matched in pairs, with the same payment, and only if the payment is less than or equal to their value. Truthfulness is also easy to see: the order with which a bid (or ask) is selected is independent of its bid price, and the price it faces, when selected, is independent of its bid. If the price is less than or equal to its bid, then whether or not it trades depends only on its order. The rest of the claim follows from Lemma 1.

Example 4

(i) Bid , ask , indexed and price . The outer while loop in Figure 3 terminates with and in Case II. The bid is marked as a loser while . If the bid will depart immediately, then , otherwise .

(ii) Bid , asks , indexed , and price . Suppose that ask 2 is selected before ask 3 in the outer while loop. Then the loop terminates with and in Case II and . Suppose the bid and asks leave the market later than this period. Then because .

(iii) Bid and ask , indexed , price and both the bid and the ask is patient. The outer while loop terminates with and in Case III so that . However, .

4.2 Competition-Based Matching Rules

Each one of these rules determines which bids match in the current period through price competition between the active bids. We present three variations: McAfee, Windowed-McAfee and Active-McAfee. The latter two rules are hybrid rules in that they leverage history of past offers, in smoothing prices generated by the competition-based matching rules.

McAfee:

Use the static DA protocol due to McAfee as the matching rule. Let denote the set of bids and denote the set of asks. If then there is no trade. Otherwise, first insert two dummy bids with value and two dummy asks with value into the set of bids and asks. Let and denote the bid and ask values with denoting dummy pair and denoting dummy pair and ties otherwise broken at random. Let index the last pair of bids and asks to clear in the efficient trade, such that and . When consider the following two cases:

-

•

(Case I) If price and then the first bids and asks trade and payment is collected from each winning buyer and made to each winning seller.

-

•

(Case II) Otherwise, the first bids and asks trade and payment is collected from each winning buyer and payment is made to each winning seller.

To define , replace a bid that does not trade with a bid reporting a very large value and see whether this bid trades. To determine whether trade is possible for an ask that does not trade: replace the ask with an ask reporting value , some small . Say that there is a quorum if and only if there are at least two bids and at least two asks, i.e. . Define strong no-trade as follows: set when there is no quorum and otherwise.

Lemma 2

For any bid in the McAfee matching rule, then for any other bid (or ask) there is some bid that will make trade possible for bid (or ask) when there is a quorum.

Proof: Without loss of generality, suppose there are three bids and three asks. Label the bids and the asks , both ordered from highest to lowest so that is the most competitive bid-ask pair. Proceed by case analysis on bids. The analysis is symmetric for asks and omitted. Let denote whether or not trade is possible for bid , so that . For bid : when then and this inequality can always be satisfied for a large enough a; when then and when then , and both of these inequalities are satisfied for a large enough . For bid : when then and when, in addition, , then and each one of these inequalities are satisfied for a large enough ; similarly when then and when then . Analysis for bid follows from that for bid .

Lemma 3

The construction for strong no-trade is valid and there is no valid strong no-trade construction that includes more than one losing bid or ask that will not depart in the current period for any period in which there is a quorum.

Proof: To see that this is a valid construction, notice that strong no-trade condition (a) holds since any bid (or ask) is always in both and . Similarly, condition (b) trivially holds (with the other bids and asks remaining in even if any bid is not present in the market). To see that this definition is essentially maximal, consider now that . For contradiction, suppose that two losing bids with departure after the current period are designated as strong no-trade. But, strong no-trade condition (b) fails because of Lemma 2 because either bid could have submitted an alternate bid price that would remove the other bid from and thus necessarily also from .

The construction offered for cannot be extended even to include one agent selected at random from the set that will not depart immediately, in the case of a quorum. Such a construction would fail strong no-trade condition (b) when the set contains more than one bid (or ask) that does not depart in the current period, because bid ’s absence from the market would cause some other agent to be (randomly) selected as .

Windowed-McAfee:

This myopic matching rule is parameterized on window size . Augment the active bids and asks with the bids and asks introduced to the history in periods . Run McAfee with this augmented set of bids and asks and determine which of these bids and asks would trade. Denote this candidate set . Some active agents identified as matching in may not be able to trade in this period because can also contain non-active agents.

Let and denote, respectively, the active bids and active asks in set . Windowed-McAfee then proceeds by picking a random subset of bids and asks to trade. When then some bids and asks will not trade.

Define strong no-trade for this matching rule as:

(i) if there are no active asks but active bids, then

(ii) if there are no active bids but active asks, then

(iii) if there are fewer than 2 asks or fewer than 2 bids in the augmented bid set, then ,

and otherwise set . In all cases it should be clear that .

Lemma 4

The strong no-trade construction for windowed-McAfee is valid.

Proof: That this is a valid SNT criteria in case (iii) follows immediately from the validity of the SNT criteria for the standard McAfee matching rule. Consider case (i). Case (ii) is symmetric and omitted. For strong no-trade condition (a), we see that all bids and also , and whether or not they are designated strong no-trade is independent of their own bid price but simply because there are no active asks. Similarly, for strong no-trade condition (b), we see that all bids (and never any asks) are in whatever the bid price of any particular bid (and even whether or not it is present).

Empirically, we find that the efficiency of Windowed-McAfee is sensitive to the size of , but that frequently the best choice is a small window size that includes only the active bids.

Active-McAfee:

Active-McAfee augments the active bids and asks to include all unexpired but traded or priced-out offers. It proceeds as in Windowed-McAfee given this augmented bid set.

4.3 Extended Examples

We next provide two stylized examples to demonstrate the matching performed by Chain using both a price-based and a competition-based matching rule. For both examples, we assume a maximal patience of . Moreover, while we describe when Chain determines that a bid or an ask trades, remember that a winning buyer is not allocated the good until its reported departure and a winning seller does not receive payment until its reported departure.

Example 5

Consider Chain using an adaptive, price-based matching rule. The particular details of how prices are determined are not relevant. Assume that the prices in periods 1 and 2 are and the maximal patience is three periods. Now consider period 3 and suppose that the order book is empty at the end of period 2 and that the bids and asks in Table 1 arrive in period 3.

B S SNT? SNT? * 15 4 2 7 7 N -1 4 2 -7 n/a Y * 10 3 1 8 8 N * -3 5 3 -6.5 N 7 3 1 8 n/a N -4 3 1 -7 n/a Y 6 5 3 n/a N * -5 4 2 -7 -6.5 N -10 5 3 n/a Y

Bids and asks are admitted. Bid is priced out because by Eq. (3). Note that and are admitted despite low bids (asks) because they have maximal patience and their admission prices are . Now, suppose that is defined by the matching rule and consider applying Match to the admitted bids and asks.

Suppose that the bids are randomly ordered as and the asks as . Bid is picked first but priced-out because . Bid is tentatively accepted () and then ask is accepted (). Bid is matched with ask , with payment for by Eq. (4) and payment for . Bid is then tentatively accepted () and then matched with ask , which is accepted because . The payments are for and for . Ask expires but asks and survive and are marked in this period because they were never offered the chance to match with any bid. These asks will be active in period 4.

Note the role of the admission price in truthfulness. Had bid delayed arrival until period 4, its admission price would be and its payment in period 4 (if it matches) at least 7. Similarly, had ask delayed arrival, then its admission price would be and the maximal payment it can receive in period 4 is 6.5.

Example 6

Consider Chain using the McAfee-based matching rule with and with the same bids and asks arriving in period 3. Suppose that the prices in periods 1 and 2 that would have been faced by a buyer are and for a seller. These prices are determined by inserting an additional bid (with value ) or an additional ask (with value 0) into the order books in each of periods 1 and 2. We will illustrate this for period 3. Consider now the bids and asks in period 3 in Table 2.

B S SNT? SNT? * 15 4 2 7 7 N * -1 4 2 -6 -4 N * 10 3 1 8 8 N * -3 5 3 -4 N 7 3 1 8 n/a N -4 3 1 -6 n/a N 6 5 3 n/a N -5 4 2 -6 n/a N -10 5 3 n/a N

As before bid is not admitted. The myopic matching rule now runs the (static) McAfee auction rule on bids and asks . Consider bids and asks in decreasing order of value, the last efficient trade is indexed with . But (inserting a dummy bid with value 0 as described in Section 4.2). Price and this trade cannot be executed by McAfee. Instead, buyers trade and face price and sellers trade and face price . Bids and asks are priced-out and do not survive into the next round. Ultimately, payment is collected from buyer and payment is collected from buyer . For sellers, payment and for and respectively.

The prices and that are used in Eq. (3) to define the admission price for bids and asks with arrivals in periods 4 and 5 are determined as follows. For the buy-side price, we introduce an additional bid with bid-price . With this the bid values considered by McAfee would be and the ask values would be , where a dummy bid with value 0 is included on the buy-side. The last efficient pair to trade is with and , which satisfies this bid-ask pair. Therefore the buy-side price, . On the sell-side, we introduce an additional ask with ask-price so that the bid values considered by McAfee are (again, with a dummy bid included) and the ask values are . This time and the last efficient pair to trade is . Now and this price does not satisfy , with and price is adopted. Therefore the sell-side price, .

Again, we can see that bidder 1 cannot improve its price by delaying its entry until period 4. The admission price for the bidder would be and thus its payment in period 4, if it matches, will be at least 7.444We can check that in this case. Suppose that bidder 1 were not present in period 3. Now consider introducing an additional bid with value so that the bids values are (with a dummy bid) with ask values . Then and , which does not support the trade between bid and ask . Instead, is adopted, and we would have . Of course, this is exactly the price determined by McAfee for bid in period 3 when the bidder is truthful. Similarly for ask , which would face admission price and can receive a payment of at most 4 in period 4. We leave it as an exercise for the reader to verify that if ask delays its arrival until period 4 (in comparison, when ask is truthful).

Because the McAfee-based pricing scheme computes a price and clears the order book following every period in which there are at least two bids and two asks, the bid activity periods tend to be short in comparison to the adaptive, price-based rules where orders can be kept active longer when there is an asymmetry in the number of bids and asks in the market. In fact, one interesting artifact that occurs with adaptive, price-based matching rules is that the admission-price and can perpetuate this kind of bid-ask asymmetry. Once the market has more asks than bids, becomes likely for future asks, but not bids. Therefore, bids are much more likely than asks to be immediately priced out of the market by failing to meet the admission price constraint.

5 Theoretical Analysis: Truthfulness, Uniqueness, and Justifying Bounded-Patience

In this section we prove that Chain combined with a well-defined matching rule and a valid strong no-trade construction generates a truthful, no-deficit, feasible and individual-rational dynamic DA. In Section 5.2, we establish that uniqueness of Chain amongst dynamic DAs that are constructed from single-period matching rules as building blocks. In Section 5.3, we establish the importance of the existence of a maximal bound on bidder patience by presenting a simple environment in which no truthful, no-deficit DA can implement even a single trade despite the number of efficient trades can be increased without bound.

5.1 The Chain Mechanism is Strongly Truthful

It will be helpful to adopt a price-based interpretation of a valid single-period matching rule. Given rule , define an agent-independent price, where , such that for all , all bids , all asks , all history , and all random events . We have:

-

(A1) , and

-

(A2) payment if and otherwise

The interpretation is that there is an agent-independent price, , that is at least when the agent loses and no greater than otherwise. In particular, when . Although an agent’s price is only explicit in a matching rule when the agent trades, it is well known that such a price exists for any truthful, single-parameter mechanism; e.g., see works by Archer and Tardos (?) and Goldberg and Hartline (?).555A single-parameter mechanism is one in which the private information of an agent is limited to one number. This fits the single-period matching problem because the arrival and departure information is discarded. Moreover, although there are both buyers and sellers, the problem is effectively single-parameter because no buyer can usefully pretend to be a seller and vice versa. Moving forward we adopt price to characterize the matching rule used as a building block for Chain, and assume without loss of generality properties (A1) and (A2).

Given this, we will now establish the truthfulness of Chain by appeal to a price-based characterization due to Hajiaghayi et al. (?) for truthful, dynamic mechanisms. We state (without proof) a variant on the characterization result that holds for stochastic policies and strong-truthfulness. The theorem that we state is also specialized to our DA environment. We continue to adopt to capture the realization of stochastic events internal to the mechanism:

Theorem 2

(?) A dynamic DA , perhaps stochastic, is strongly truthful for misreports limited to no early-arrivals if and only if, for every agent , all , all , and all random events , there exists a price such that:

-

(B1) the price is independent of agent ’s reported value

-

(B2) the price is monotonic-increasing in tighter

-

(B3) trade whenever and whenever , and the trade is performed for a buyer upon its departure period .

-

(B4) the agent’s payment is when , with otherwise, and the payment is made to a seller upon its departure, .

where random event is independent of the report of agent in as much as it affects the price to agent .

Just as for the single-period, price-based characterization, the price need not always be explicit in Chain. Rather, the theorem states that given any truthful dynamic DA, such as Chain, there exists a well-defined price function with these properties of value-independence (B1) and arrival-departure monotonicity (B2), and such that they define the trade (B3) and the payment (B4).

To establish the truthfulness of Chain, we prove that it is well-defined with respect to the following price function:

| (5) |

where

| (6) |

and

| (9) |

where indicates that for all and otherwise, and where is the first period in which . We refer to this as the decision period. Term denotes the admission price, and is defined on periods before the agent arrives for which had it arrived in that period. Note carefully that the rules of Chain are implicit in defining this price function. For instance, whether or not in some period depends, for example, on the other bids that remain active in that period.

We now establish conditions (B1)–(B4). The proofs of the technical lemmas are deferred until the Appendix. The following lemma is helpful and gets to the heart of the strong no-trade concept.

Lemma 5

The set of active agents (other than ) in period in Chain is independent of ’s report while agent remains active, and would be unchanged if ’s arrival is later than period .

The following result establishes properties (B1) and (B2).

Lemma 6

The price constructed from admission price and post-arrival price is value-independent and monotonic-increasing when the matching rule in Chain is well-defined, the strong no-trade construction is valid, and agent patience is bounded by .

Having established properties (B1) and (B2) for price function , we just need to establish (B3) and (B4) to show truthfulness. The timing aspect of (B3) and (B4), which requires that the buyer receives an item and the seller receives its payment upon reported departure, is already clear from the definition of Chain.

Theorem 3

The online DA Chain is strongly truthful, no-deficit, feasible and individual-rational when the matching rule is well-defined, the strong no-trade construction is valid, and agent patience is bounded by .

Proof: Properties (B1) and (B2) follow from Lemma 6. The timing aspects of (B3) and (B4) are immediate. To complete the proof, we first consider (B3). If then agent is priced out at admission by Chain because this reflects that in some with , and thus the bid would lose if it arrived in that period (either because it could trade, but for a payment greater than its reported value, or because ). Also, if there is no decision period, then , which is consistent with Chain, because there is no bid price at which a bid will trade when for all periods . Suppose now that there is a decision period and . If then there should be no trade. This is the case in Chain, because the price in is greater than and thus the agent is priced-out. If then the bid should trade and indeed it does, again because the price in that period satisfies (A1) and (A2) with respect to the matching rule. Turning to (B4), it is immediate that the payments collected in Chain are equal to price , because if bid trades then and thus and . The admission price when because price is well-defined by properties (A1) and (A2). Similarly, the payment defined by the matching rule in Chain in the decision period is equal to .

That Chain is individual-rational and feasible follows from inspection. Chain is no-deficit because the payment collected from every agent (whether a buyer or a seller) is at least that defined by a valid matching rule in the decision period (it can be higher when the admission price is higher than this matching price), the matching rules are themselves no-deficit, and because the auctioneer delays making a payment to a seller until its reported departure but collects payment from a buyer immediately upon a match.

We remark that information can be reported to bidders that are not currently participating in the market, for instance to assist in their valuation process. If this information is delayed by at least the maximal patience of a bidder, so that the bid of a current bidder cannot influence the other bids and asks that it faces, then this is without any strategic consequences. Of course, without this constraint, or with bidders that participate in the market multiple times, the effect of such feedback would require careful analysis and bring us outside of the private values framework.

5.2 Chain is Unique amongst Dynamic DAs that are constructed from Myopic Matching Rules

In what follows, we establish that Chain is unique amongst all truthful, dynamic DAs that adopt well-defined, myopic matching rules as simple building blocks. For this, we define the class of canonical, dynamic DAs, which take a well-defined single period matching rule coupled with a valid strong no-trade construction, and satisfy the following requirements:

(i) agents are active until they are matched or priced-out,

(ii) agents participate in the single-period matching rule while active

(iii) agents are matched if and only if they trade in the single-period matching rule.

We think that these restrictions capture the essence of what it means to construct a dynamic DA from single-period matching rules. Notice that a number of design elements are left undefined, including the payment collected from matched bids, when to mark an active bid as priced-out, what rule to use upon admission, and how to use the strong no-trade information within the dynamic DA. In establishing a uniqueness result, we leverage the necessary and sufficient price-based characterization in Theorem 2, and exactly determine the price function to that defined in Eq. (4) and associated with Chain. The proofs for the two technical lemmas are deferred until the Appendix.

Lemma 7

A strongly truthful, canonical dynamic DA must define price where is the decision period for bid (if it exists). Moreover, the bid must be priced-out in period if it is not matched.

Lemma 8

A strongly truthful, canonical and individual-rational dynamic DA must define price , and a bid with must be priced-out upon admission.

Theorem 4

The dynamic DA algorithm Chain uniquely defines a strongly truthful, individual-rational auction among canonical dynamic DAs that only designate bids as priced-out when necessary.

Proof: If there is no decision period, then we must have , by canonical (iii) coupled with (B3). Combining this with Lemmas 7 and 8, we have . We have also established that a bid must be priced-out if its bid value is less than the admission price, or it fails to match in its decision period. Left to show is that the price is exactly as in Chain, and that a bid is admitted when its value and retained as active when it is in the strong no-trade set. The last two control aspects are determined once we choose a rule that “only designates bids as priced-out when necessary.” We prefer to allow a bid to remain active when this does not compromise truthfulness or individual-rationality. Finally, suppose for contradiction that . Then an agent with would prefer to bid and avoid winning – otherwise its payment would be greater than its value.

5.3 Bounded Patience Is Required for Reasonable Efficiency

Chain depends on a maximal bound on patience used to calculate the admission price faced by a bidder on entering the market with Eq. (3). To motivate this assumption about the existence of a maximal patience, we construct a simple environment in which the number of trades implemented by a truthful, no-deficit DA can be made an arbitrarily small fraction of the number of efficient trades with even a small number of bidders having potentially unbounded patience. This illustrates that a bound on bidder patience is required for dynamic DAs with reasonable performance.

In achieving this negative result, we impose the additional requirement of anonymity, This anonymity property is already satisfied by Chain, when coupled with matching rules that satisfy anonymity, as is the case with all the rules presented in Section 4. In defining anonymity, extend the earlier definition of a dynamic DA, , so that allocation policy defines the probability that agent trades in period given reports . Payment, , continues to define the payment by agent in period , and is a random variable when the mechanism is stochastic.

Definition 8 (anonymity)

A dynamic DA, is anonymous if allocation policy defines probability of trade in each period that is independent of identity and invariant to a permutation of and if the payment , contingent on trade by agent , is independent of identity and invariant to a permutation of .

We now consider the following simple environment. Informally, there will be a random number of high-valued phases in which bids and asks have high value and there might be a single bidder with patience that exceeds that of the other bids and asks in the phase. These high-valued phases are then followed by some number, perhaps zero, of low-valued phases with bounded-patience bids and asks. Formally, there are high-valued phases (a random variable, unknown to the auction), each of duration periods, indexed and each with:

-

•

or bids with type ,

-

•

0 or 1 bids with type for some mark-up parameter, and some high-patience parameter, ,

-

•

asks with type ,

followed by some number (perhaps zero) of low-valued phases, also of duration , and indexed , with:

-

•

or bids with type

-

•

asks with type ,

where , , and bid-spread parameter . Note that any phase can be the last phase, with no additional bids or asks arriving in the future.

Definition 9 (reasonable DA)

A dynamic DA is reasonable in this simple environment if there is some parameterization of new bids, and periods-per-phase, , for which it will execute at least one trade between new bids and new asks in each phase, for any choice of high value , low value , bid-spread , mark-up , high patience .

All of the dynamic DAs presented in Section 4 can be parameterized to make them reasonable for a suitably large and , and without the possibility of a bid with an unbounded patience.

Theorem 5

No strongly truthful, individual-rational, no-deficit, feasible, anonymous dynamic DA can be reasonable when a bidder’s patience can be unbounded.

Proof: Fix any , , and for the number of high-valued phases, , set the departure of a high-patience agent to . Keep , , and as variables to be set within the proof. Assume a dynamic DA is reasonable, so that it selects at least one new bid-ask pair to trade in each phase. Consider phase and with agents of types , of type and 1 agent of patient type, . If the patient bid deviates to then the bids are all identical, and with probability at least the bid would win by anonymity and reasonableness. Also, by anonymity, individual-rationality and no-deficit we have that the payment made by any winning bid is the same, and must be . (If the payment had been less than this, the DA would run at a deficit since the sellers require at least this much payment for individual-rationality.) Condition now on the case that the patient bid would win if it deviates and reports . Suppose the bidder is truthful, reports but does not trade in this phase. But, if phase is the last phase with new bids and asks, then the bid will not be able to trade in the future and for strong-truthfulness the DA would need to make a payment of at least in a later phase to prevent the bid having a useful deviation to and winning in phase . But, if:

| (10) |

then the DA cannot make this payment without failing no-deficit (because is an upper-bound on the surplus the auctioneer could extract from bidders in this phase without violating individual-rationality). We will later pick values of and , to satisfy Eq. (10). So, the bid must trade when it reports , in the event that it would win with report , as “insurance” against this being the last phase with new bids and asks. Moreover, it should trade for payment, , to ensure an agent with true type cannot benefit by reporting .

Now suppose that this was not the last phase with new bids and asks, and . Now consider what would happen if the patient bid in phase deviated and reported . As before, this bid would win with probability at least by anonymity and reasonableness, but now with some payment . Condition now on the case that the patient bid would win, both with a report of and with a report of . When truthful, it trades in phase with payment at least . If it had reported it would trade in phase for payment at most . For strong truthfulness, the DA must make an additional payment to the patient agent of at least . But, suppose that the high and low values are such that,

| (11) |

Making this payment in this case would violate no-deficit, because is an upper-bound on the surplus the auctioneer can extract from bidders across all phases, including the current phase, without violating individual-rationality. But now we can fix any , and choose to satisfy Eq. (11) and to satisfy Eq. (10). Thus, we have proved that no truthful dynamic DA can choose a bid-ask pair to trade in period . The proof can be readily extended to show a similar problem with choosing a bid-ask pair in any period , by considering truthful type of .

To drive home the negative result: notice that the number of efficient trades can be increased without limit by choosing an arbitrarily large , and that no truthful, dynamic DA with these properties will be able to execute even a single trade in each of these periods. Moreover, we see that only a vanishingly small fraction of high-patience agents is required for this negative result. The proof only requires that at least one patient agent is possible in all of the high-valued phases.

6 Experimental Analysis

In this section, we evaluate in simulation each of the Chain-based DAs introduced in Section 4. We measure the allocative efficiency (total value from the trades), net efficiency (total value discounted for the revenue that flows to the auctioneer), and revenue to the auctioneer. All values are normalized by the total offline value of the optimal matching.

For comparison we also implement several other matching schemes: the truthful, surplus-maximizing matching algorithm presented by Blum et al. (?), an untruthful greedy matching algorithm using truthful bids as input to provide an upper-bound on performance, and an untruthful DA populated with simple adaptive agents that are modeled after the Zero-intelligence Plus trading algorithm that has been leveraged in the study of static DAs (?, ?).

6.1 Experimental Set-up

Traders arrive to the market as a Poisson stream to exchange a single commodity at discrete moments. This is a standard model of arrival in dynamic systems, economic or otherwise. Each trader, equally likely to be a buyer or seller, arrives after the previous with an exponentially distributed delay, with probability density function (pdf):

| (12) |

where represents the arrival intensity in agents per second. Later we present results as the interarrival time, is varied between 0.05 and 1.5; i.e., as the arrival intensity is varied between 20 and . A single trial continues until at least 5,000 buyers and 5,000 sellers have entered the market. In our experiments we vary the maximal patience between 2 and 10. For the distribution on an agent’s activity period (or patience, ), we consider both a uniform distribution with pdf:

| (13) |

and a truncated exponential distribution with pdf:

| (14) |

where so that 95% of the underlying exponential distribution is less than the maximal patience. Both arrival time and activity duration are rounded to the nearest integral time period. A trader who arrives and departs during the same period is assumed to need an immediate trade and is active for only one period.

Each trader’s valuation represents a sample drawn at its arrival from a uniform distribution with spread 20% about the current mean valuation. (The value is positive for a bid and negative for an ask.) To simulate market volatility, we run experiments that vary the average valuation using Brownian motion, a common model for valuation volatility upon which many option pricing models are based (?). At every time period, the mean valuation randomly increases or decreases by a constant multiplier, where is the approximate volatility and varied between 0 and 0.15 in our experiments.

We plot the mean efficiency of 100 runs for each experiment, with the same sets of bids and asks used across all double auctions. All parameters of an auction rule are reoptimized for each market environment; e.g., we can find the optimal fixed price and the optimal smoothing parameters offline given the ability to sample from the market model.

6.2 Chain Implementation

We implement Chain for the five price-based matching rules (history-clearing, history-median, history-McAfee, history-EWMA, and fixed-price) and the three competition-based matching rules (McAfee, active-McAfee, and windowed-McAfee).

The price-based implementations keep a fixed-size set of the most recently expired, traded, or priced-out offers, . Offers priced-out by their admission prices are inserted into prior to computing . The history-clearing metric computes a price to maximize the number of trades to agents represented by had they all been contemporary. The history-median metric chooses the price to be the median of the absolute valuation of the offers in . The history-McAfee method computes the “McAfee price” for the scenario where all agents represented by are simultaneously present. The EWMA metric computes an exponentially-weighted average of bids in the order that they expire, trade, or price out. The simulations initialize the price to the average of the mean buy and sell valuations. If two bids expire during the same period, they are included in arbitrary order to the moving average.

None of the metrics require more than one parameter, which is optimized offline with access to the model of the market environment. Parameter optimization proceeds by uniformly sampling the parameter range, smoothing the result by averaging each result with its immediate neighbors. The optimization repeats twice more over a narrower range about the smoothed maximum, returning the parameter that maximizes (expected) allocative efficiency. None of the price-based methods appeared to be sensitive to small (10%) changes in the size of . With most simulations, the window size was chosen to be about 150 offers. For EWMA, the smoothing factor was usually chosen to be around 0.05 or lower. The windowed-McAfee matching rule, however, was extremely sensitive to window size for simulations with volatile valuations, and the search process frequently converged to suboptimal local maxima.

The admission price in the price-based methods is computed by first determining whether Match would check the value of the bid against bid price if the bid had arrived in some earlier period . Rather than simulate the entire Match procedure, it is sufficient to determine the probability of this event. This is determined by checking the construction of the strong no-trade sets in that earlier period. If contains non-departing buyers (sellers), then the probability that an additional seller (buyer) would be examined is 1 and . Otherwise the probability is equal to the ratio of the number of bids (asks) examined not included in and one more than the total number of bids (asks) present. Finally, with probability the price the agent would have faced in period is defined as ( for sellers), and otherwise it is . Here, is the history-dependent price defined in period .

The competition-based matching rules price out all non-trading bids at the end of each period in which trade occurs (because of the definition of strong no-trade in that context). The admission prices are calculated by considering the price that a bid (ask) would have faced in some period before its reported arrival. In such a period, the price for a bid (ask) is determined by inserting an additional bid (ask) with valuation (0) and applying the competition-based matching rule to that (counterfactual) state. From this we determine whether the agent would win for its reported value, and if so what price it would face.

6.3 Optimal Offline Matching

We use a commercial integer program solver (CPLEX666www.ilog.com) to compute the optimal offline solution, i.e. with complete knowledge about all offers received over time. In determining the offline solution we enforce the constraint that a trade can only be executed if the activity periods of both buyer, and seller, overlap,

| (15) |

An integer-program formulation to maximize total value is:

| (16) | ||||

where is a bid-ask pair that could potentially trade because they have overlapping arrival and departure intervals satisfying Eq. (15). The decision variable indicates that bid matches with ask . This provides the optimal, offline allocative efficiency.

6.4 Greedy Online Matching

We implement a greedy matching algorithm that immediately matches offers that yield non-negative budget surplus. This is a non-truthful matching rule but provides an additional comparison point for the efficiency of the other matching schemes. During each time period, the greedy matching algorithm orders active bids and asks by their valuations, exactly as the McAfee mechanism does, and matches offers until pairs no longer generate positive surplus. The algorithm’s performance allows us to infer the number of offers that the optimal matching defers before matching and the amount of surplus lost by the McAfee method due to trade reduction and due to the additional constraint of admission pricing.

6.5 Worst-Case Optimal Matching

Blum et al. (?) derive a mechanism equivalent to our fixed-price matching mechanism, except that the price used is chosen from the cumulative distribution

| (17) |

where is the fixed point to the equation

| (18) |