Time Scales in Futures Markets and Applications

Abstract

The probability distribution of log-returns for financial time series, sampled at high frequency, is the basis for any further developments in quantitative finance. In this letter, we present experimental results based on a large set of time series on futures. We show that the t-distribution with gives a nice description of almost all data series considered for a time scale below hour. For hours, the Gaussian regime is reached. A particular focus has been put on the DAX and Euro futures. This appears to be a quite general result that stays robust on a large set of futures, but not on any data sets. In this sense, this is not universal. A technique using factorial moments defined on a sequence of returns is described and similar results for time scales are obtained. Let us note that from a fundamental point of view, there is no clear reason why DAX and Euro futures should present similar behavior with respect to their return distributions. Both are complex markets where many internal and external factors interact at each instant to determine the transaction price. These factors are certainly different for an index on a change parity (Euro) and an index on stocks (DAX). Thus, this is striking that we can identify universal statistical features in price fluctuations of these markets. This is really the advantage of micro-structure analysis to prompt unified approaches of different kinds of markets. Finally, we examine the relation of power law distribution of returns with another scaling behavior of the data encoded into the Hurst exponent. We have obtained for DAX and for Euro futures.

I Introduction

Returns in financial time series are fundamental inputs to quantitative finance. To a certain extend, they provide some insights in the the dynamical content of the market. There are several experimental analysis showing that the probability distributions of returns in a large set of financial markets exhibit power law tails a1 ; a2 ; a3 ; a4 .

Let us consider financial price series, labeled as , from which we extract the log-returns over some time interval . Any statistical analysis can then be conducted on these log-returns . There are evidences that for mature and high liquid markets, in particular futures, both positive and negative tails conform to the so-called inverse cubic law b1 ; b2 ; b3 ; b4 ; b5 ; b6 . It means that if we express the the distribution of returns as a power law

| (1) |

at large values of , we can measure the exponent as it is done in Ref. b5 ; b6 . This is correct for a variety of mature markets, in particular futures. This observation is in contrast to predictions from the Pareto-Levy distribution, and former experimental results, from which we expect c1 . This discrepancy in results shows how the topic is critical and a clear driver for theoretical considerations. There is no universality and the use of large samples of high frequency data is a key point in the understanding of the underlying market dynamics.

Very generally, all experimental investigations confirm that distribution of returns evolve from power law behavior at small time scales (see Eq. (1)) to Gaussian at large time scales. The precise value of the exponent depends on the market under consideration with a tendency for mature and liquid markets to fall outside the Levy stable regime, namely .

In this letter, we consider a few financial series on futures, which correspond to mature markets with high level of liquidity. First, we discuss the universality of the experimental distributions of returns on these financial series. Following Ref. b6 , we extract a parameterization of the log-returns distribution which confirms the previous result, , for small time scales .

Then, we show at which value of the time scale, market dynamics enters into the Gaussian regime. We discuss the universality of this particular scale with respect to a sample of high liquid futures. In a second part, we address the determination of these scales using an analysis technique based on factorial moments d1 . We prove the consistency between the appearance of intermittency and the deviation from the Gaussian regime, as derived in the first part.

From the measurement of the distributions for returns , we can understand how these returns sum up to build the quantity , where is a multiple of . Then, in a thirst part, we discuss the scaling of with . We relate the so-called Hurst exponent to the power law tail .

II Distribution of Returns

II.1 Definitions

From standard quantitative analysis a1 ; a2 ; a3 ; a4 , we know that the distribution of log-returns , namely , can be written quite generally as

| (2) |

where is an objective function and a normalization factor. In particular, it can be shown easily that can be derived by minimizing a generating functional , subject to some constraints on the mean value of the objective function. In Eq. (2) we do not specify the time scale at which returns are derived. When need, we will take this variable into account with the notation . It reads

| (3) |

where is an arbitrary constant.

In addition, the expression given in Eq. (2) for the probability distribution can also be seen as the outcome of an equation of motion for . From Eq. (2) and (3), we can express the stochastic process as a Markovian process of the form a1 ; a2 ; a3 ; a4

| (4) |

where is a Gaussian process satisfying and . In Eq. (4), functions and depends only on . Adopting the Itô convention a1 ; a2 ; a3 ; a4 , the distribution function , associated with this equation of motion (Eq. (4)), is given by the following Fokker-Planck equation

| (5) |

From Eq. (5), we can finally extract the stationary solution for in the form of Eq. (2)

| (6) |

Whether Eq. (4), (5) and (6) can be related to real data on financial markets is not granted. Therefore, we need to compare predictions derived from these equations to real data. As mentioned above, we use financial time series on different futures, using a five minutes sampling.

In Eq. (4), (5) and (6), functions and are not specified and any choice can be considered. Obviously, only specific choices will have a chance to get a reasonable agreement with real data. For example, let us consider three cases:

-

(i)

If and , we obtain , and thus we predict a Gaussian shape for the log-returns distribution.

-

(ii)

In the more general case where and is not constant, we obtain

and thus we predict non-Gaussian shape for the log-returns distribution.

-

(iii)

Let us specify the case (ii). Introducing a constant and defining the two functions and as and , we get

(7) In this scenario follows the so-called t-distribution. It depends on one parameter to be fitted on real data, for normalized log-returns. Let us notice that Eq. (7) is equivalent to the q-exponential form of Ref. ts1 ; ts2 ; ts3

(8) where we have conserved the notations of Ref. ts1 ; ts2 ; ts3 . Obviously, Eq. (7) and (8) are directly related by . In particular, is equivalent to .

II.2 Experimental Analysis of

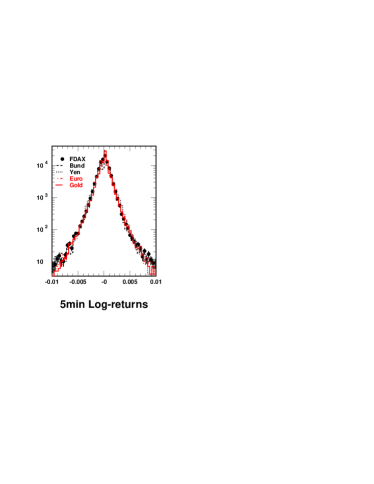

In Fig. 1, we present the log-returns (five minutes sampling) for a large set of futures, with minutes. To make the comparison, we have scaled for all futures to the volatility of the DAX futures (FDAX). All data sets cover the period -. On the left hand side of Fig. 1, we observe that futures on DAX, Bund, Yen, Euro, Gold present the same probability distribution for . Therefore is universal for all these data series once the volatility is normalized to the same value. Note that there are futures on commodities which exhibit some larger tails b6 and we can not claim the universality of this distribution whatever futures. See also Ref. b5 .

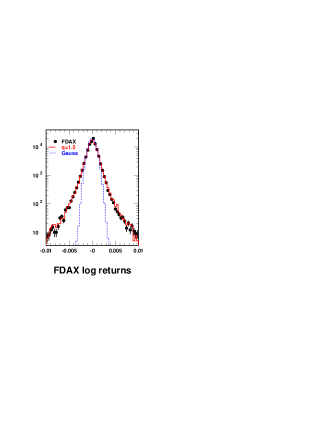

We can use results developed above in order to compare with experimental distributions of Fig. 1 (with fixed minutes). We use predictions exposed in cases (i) and (iii), respectively the Gaussian and the q-exponential forms (or t-distribution). Results are shown in Fig. 2. For data, we only display for DAX futures.

In Fig. 2, we show that the q-exponential probability distribution of Eq. (8), with , gives a good description of the data. Similarly, it corresponds to in the form of the t-distribution of Eq. (7). Also, we observe in Fig. 2 that the Gaussian approximation fails to describe properly the data. On the right hand side of Fig. 2, we observe that when is increased above in Eq. (7), then stands in the middle of the correct probability density and the Gaussian approximation. When tends to infinity, the t-distribution recovers the Gaussian limit.

In summary, from the theory point of view, the probability distribution of log-returns of financial time series, sampled at high frequency, can be expressed quite generally as . In particular, we have shown that a large sample of high liquid futures (with normalized log-returns) are compatible with a distribution of the form

| (9) |

Commodity futures deviate from this shape with larger tails and thus a smaller value of the exponent .

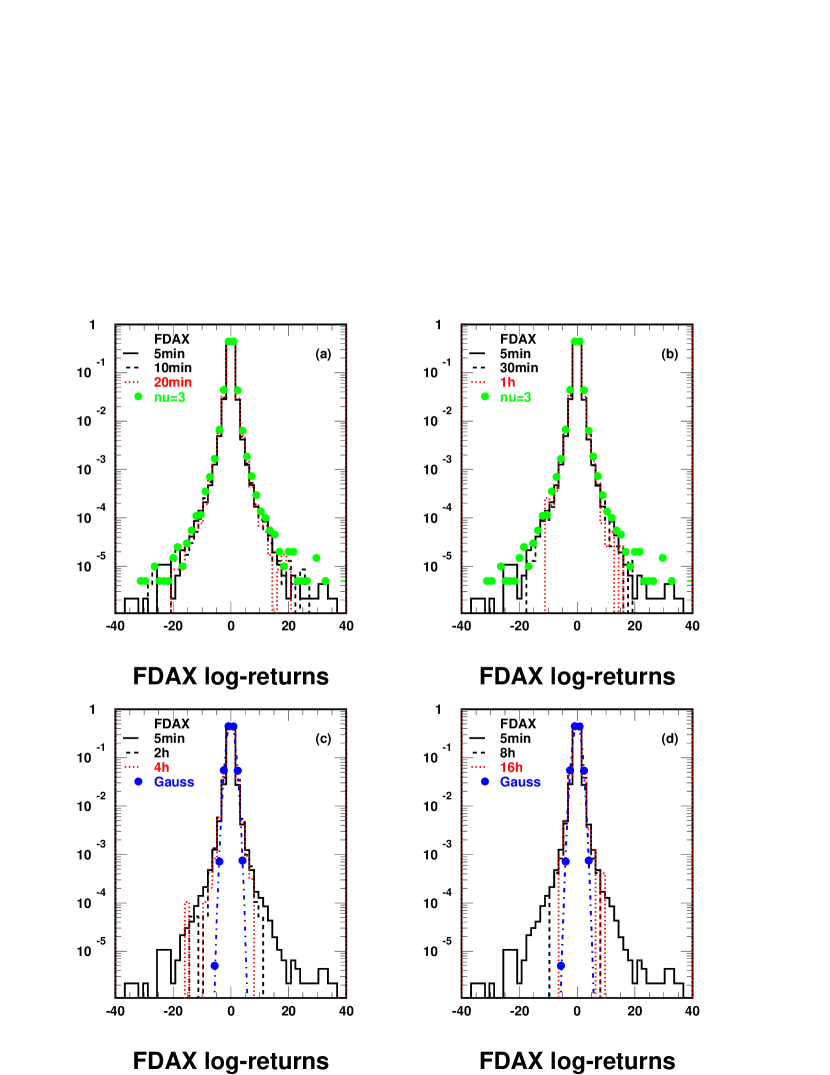

Once Eq. (9) is established, we can examine the validity of this probability distribution as a function of , from minutes to several hours. This is done in Fig. 3 for the DAX futures (FDAX) and Fig. 4 for the Euro futures (EC). As mentioned above, these two data sets cover the period -. In Fig. 3 (a)-(d), we present the normalized log-returns for the FDAX on different time scales (or resolutions) . The normalization is done by changing in where and are the sample mean and variance. This re-definition does not change obviously the tail behavior of .

The basic resolution minutes is displayed in all cases (a)-(d) as a reference. Then, we show the distributions using minutes for Fig. 3 (a), minutes for Fig. 3 (b), hours for Fig. 3 (c) and finally hours for Fig. 3 (d). For small times scales hour, in Fig. 3 (a)-(b), we confirm that the distributions of log-returns follows Eq. (9) with .

When the resolution is increased to hours, Fig. 3 (c), we observe that starts approaching the Gaussian regime. This regime is reached for hours as can be seen on 3 (d).

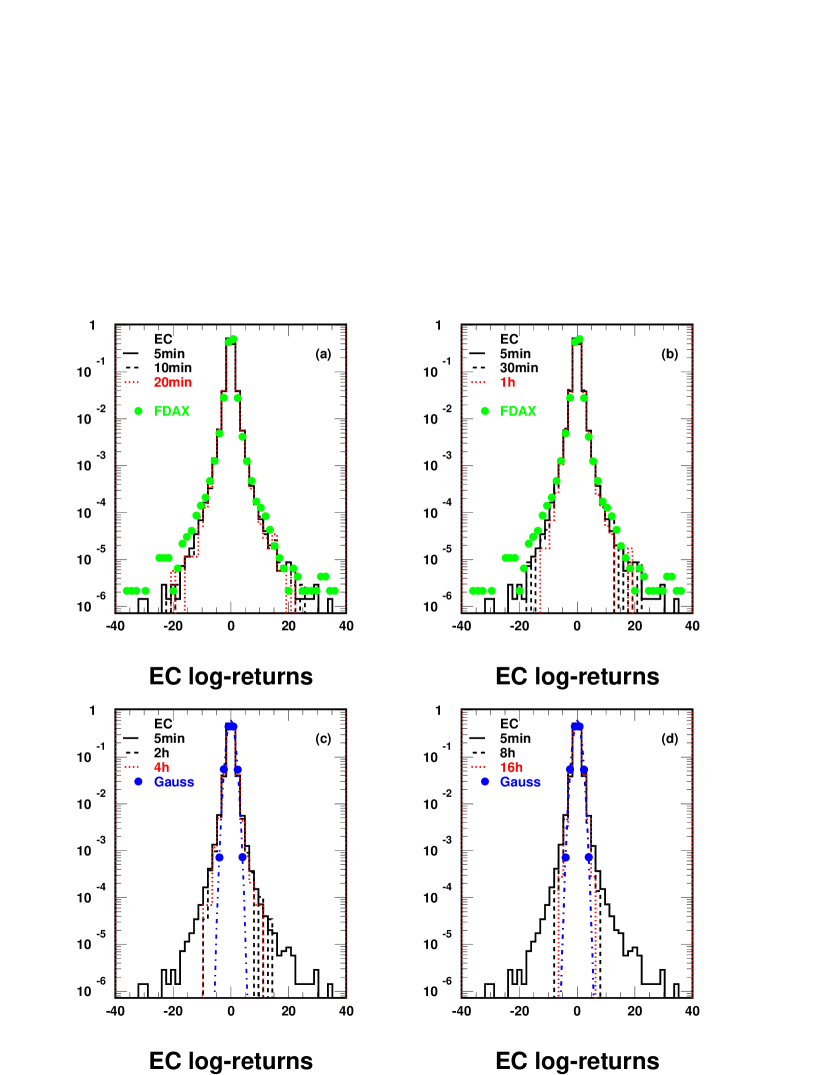

In Fig. 4 (a)-(d), we present similar plots for the Euro futures. Same conclusions can be derived. For small times scales hour, in Fig. 4 (a)-(b), we observe that the distributions of log-returns follows Eq. (9) with . When the resolution is increased to hours, Fig. 4 (c), we observe that starts approaching the Gaussian regime, which is reached for hours (4 (d)).

Identical conclusions are valid also for futures displayed in Fig. 1. This is a reasonable behavior which is compatible with the general statement done in the introduction. evolves from power law at small time scales to Gaussian at large time scales, namely hours. With the above analysis, we have put quantitative estimates on this statement for several high liquid futures.

III Factorial Moment Analysis

III.1 Definitions

In this section, we intend to analyze the dynamics of returns using an alternative technique. The main interest is to show the consistency of all results within different techniques. In the following, we are interested in the multiplicity of positive or negative returns in a given time window . Indeed, sequences of positive and negative returns are much indicative of the statistical nature of fluctuations in the price series. The idea is then to extract a quantitative information from these sequences.

First, we present the situation in nuclear physics. At nuclear or sub-nuclear energies, the number of hadrons created during inelastic collisions varies from one event to another. The distribution of the number of produced hadrons, namely the multiplicity distribution, provides a basic means to characterize the events. The multiplicity distribution contains information about multi-particle correlations in an integrated form, providing a general and sensitive means to probe the dynamics of the interaction. Particle multiplicities can be studied in terms of the normalized factorial moments

| (10) |

for a specified phase-space region of size . The number, , of particles is measured inside and angled brackets denote the average over all events. The factorial moments are convenient tools to characterize the multiplicity distributions when becomes small. For uncorrelated particle production within , Poisson or Gaussian statistics holds and for all . Correlations between particles lead to a broadening of the multiplicity distribution and to dynamical fluctuations. In this case, the normalized factorial moments increase with decreasing . The idea is then to divide the factorial moment defined in Eq. (10) in more and more bins.

We can thus compute the related moment following Eq. (10) as

| (11) |

where is the average number of particles in the full phase space region accepted (), denotes the number of bins in this region and is the multiplicity in -th bin.

The behavior of factorial moments plotted as a function of the number of bins (which means decreasing bin sizes) provides information about the character of multiplicity fluctuations among different bins. Rising of with rising (decreasing bin size) generally signalizes deviation from purely Gaussian distribution of fluctuations. The linear growth of with was defined as intermittency in BiaP . See also Lipa ; Dremin:1993dt ; Dremin:1993ee ; Rames:1994qm . In the following, the term is used for any type of growth of observed.

As a matter of fact, it has been noticed in BiaP that the use of factorial moments allows to extract the dynamical signal from the Poisson noise in the analysis of the multiplicity signal in high energy reactions.

In addition, it has been shown that it is possible to define and compute a multi-fractal dimension, , for the theory of strong interactions DD93 ; OW93

| (12) |

where d is the dimension of the phase space under consideration ( for the whole angular phase space, and if one has integrated over, say the azimuthal angle). In the constant coupling case is well defined and reads

| (13) |

where , is the strong interaction coupling constant, is the gluon color factor DD93 ; OW93 . The choice of the factorial moments as a specific tool in order to study the scaling behavior of the high energy multiplicity distributions is then useful to analyze the underlying dynamics of the processes. In principle, we can extend this last idea to other fields where factorial moments can be defined.

III.2 Generating Function for Factorial Moments

The multiplicity distribution is defined as , where is the cross section of an -particle production process (the so-called topological cross section) and the sum is over all possible values of so that

| (14) |

The generating function can be defined as

| (15) |

which substitutes an analytic function of in place of the set of numbers . Then, we obtain the factorial moment or order as

| (16) |

and the corresponding definition for cumulants

| (17) |

The expression for can then be re-written as

| (18) |

| (19) |

The physical meaning of these moments has been discussed in the previous section. Another interpretation can be seen from the above definitions if they are presented in the form of integrals of correlation functions. Let the single symbol represent all kinematic variables needed to specify the position of each particle in the phase space volume d1 . A sequence of inclusive -particle differential cross sections defines the factorial moments as

| (20) |

Therefore, factorial moments include all correlations within the system of particles under consideration. They represent integral characteristics of any correlation between the particles whereas cumulants of rank represent genuine -particle correlations not reducible to the product of lower order correlations.

III.3 Experimental Analysis

The analogy with returns of financial price series is immediate. If we divide the price series in consecutive time windows of lengths , we define like this a set of events. In each window, we have a certain number of positive returns , where , and similarly of negative returns . If the sequence of returns is purely uncorrelated, following a Gaussian statistics at all scales, we expect for all .

However, correlations between returns may lead to a broadening of the multiplicity distributions ( or or even a combination of both) and to dynamical fluctuations. In this case, the factorial moments may increase with decreasing , or increasing the number of bins that divide , as in Eq. (11). In the following, we consider only the factorial moment of second order . We can write

| (21) |

where is the average number of positive returns in the full time window (), denotes the number of bins in this window and is the number of positive returns in -th bin.

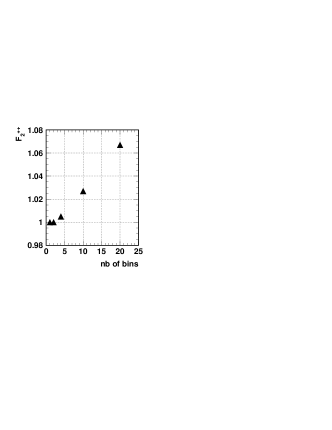

We consider the data series on the Euro futures, sampled in 5 minutes units (same data set as in section II). We present calculations for a time window 200 times units, that we divide in , , , or bins. This means that the time resolution extends from hours to hours. Note that with a time window of 200 time units, we set up an ensemble of more that 3400 events. The statistical precision of the following analysis is then ensured. Results are presented in Fig. 5 (left) for positive returns. Factorial moments are displayed for , , , or bins. As mentioned above, this gives a time resolution ranging from hours for bins till hours for bin. The statistical precision is of %. We can define a systematical uncertainty by shifting the time window of units by or units, which means that we define a different set of events among the price series. Variations in the calculations of are lower that %. Fig. 5 (left) displays the full uncertainty of these quantities.

In Fig. 5 (left), we observe that for and bins segmentation is found to be equal to . As expected, for the larger resolution, positive returns appear as completely uncorrelated. When the number of bins is increased, we observe the phenomenon described in section 1, with an enhanced sensitivity of to non-Gaussian fluctuations. This confirms that correlations between positive returns start to play a role when the resolution is below hours. Thus, Fig. 5 (left) exhibits a clear feature of intermittency. As in nuclear reactions, an increase of the resolution to a certain extend leads to a broadening of the multiplicity distribution and to super-diffusive fluctuations. Let us note that this is a feature that can be approached in the context of non-extensive statistics ts1 ; ts2 ; ts3 .

Similar results can be obtained for , defined for negative returns distribution.

| (22) |

where is the average number of negative returns in the full time window (), denotes the number of bins in this window and is the number of negative returns in -th bin. For all values displayed in Fig. 5 (left) for , we derive the same result for up to %, which makes and indistinguishable.

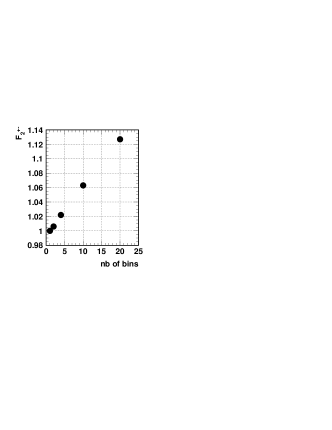

A direct extension of the above study can be obtained if we examine moments for like-sign and unlike-sign combinations of returns separately. The like-sign factorial moment of order is defined by Eq. (21). The unlike-sign can be expressed as

| (23) |

Results are presented in Fig. 5 (right) for . Here again, we observe intermittency, with an increase of as a function of the number of bins. Also, this increase is larger than for like-sign calculations as can be observed when comparing Fig. 5 (left) and 5 (right). The sensitivity to non-Gaussian fluctuations in the returns sequence is thus enhanced with the definition of d to . This is also an effect observed in nuclear interactions Dremin:1993dt ; Dremin:1993ee ; Rames:1994qm .

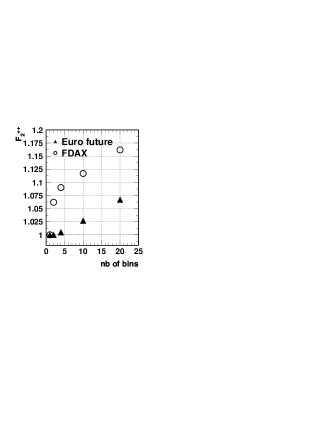

A final comment is in order. This analysis has been illustrated on the Euro futures. However, we have found that a similar intermittent behavior is observed on other futures, like the DAX futures (FDAX). For each series, the values of the like-sign and unlike-sign factorial moments of order vary compared to results exhibited for the Euro future. However the rise of the as a function of the number of bins is an invariant property, with always and equal to unity for a time window of order hours. For some series, like FDAX, the intermittent behavior already prevails for a time scale of order hours, with an increase of from (, h) to (, h). This is shown in Fig. 6. This growth with is faster than the Euro future. However, the key feature is always the same. For a sufficiently fine time scale, more precisely for smaller than to hours depending of the financial product, intermittency is observed.

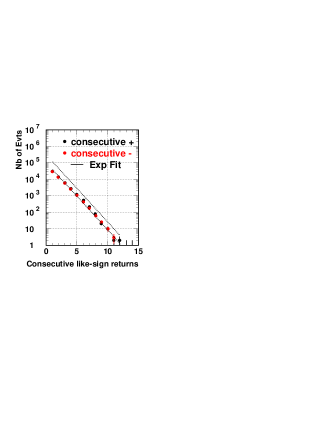

Interestingly, we can use this formalism in order to derive some further statements on correlations of returns. From Eq. (18), we get

which corresponds to the probability to have zero positive (resp. negative) returns in a given time window. This defines a gap in duration for positive (resp. negative) returns. Let us use Eq. (17) to express in another way using cumulants

When we can neglect correlations within a large time window, we have shown , then we conclude

| (24) |

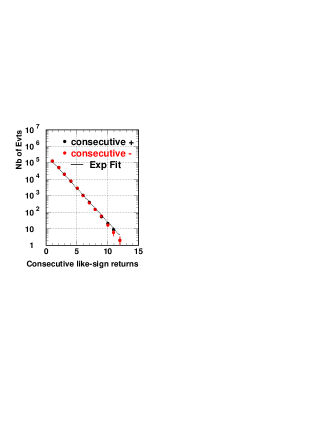

where represents the time scale (time window). This last expression is very simple and instructive. It states that the gap probability is exponentially suppressed with this time scale. This is illustrated in Fig. 7 for the finance case. We observe the distribution of events (probability distribution) as a function of the size of the gap. The gap is defined as the number of consecutive positive returns after a negative return, thus this is a gap in negative return. Inversely for a gap in positive return. This gap is given in number of time units for the financial time series considered. In Fig. 7, we display results for the Euro futures series over 10 years, sampled in two different time units. In both cases we observe effectively an exponential fall of the probability distribution as a function of the gap size. As illustrated also in Fig. 7, this exponential fall does not depend on the sampling. This confirms the prediction of Eq. (24).

IV Further Analysis of Correlations

With factorial moments, we have discussed how the deviation from with the time scale is associated to a broadening of the probability distribution of returns and then to dynamical fluctuations.

Correlations between returns can be tested in other ways. One general methodology consists in estimating how a certain fluctuation measurement,labeled generically as , scales with the size of the time window considered. Specific methods, such as the Hurst rescaled range analysis hurst or the Detrended Fluctuation Analysis stanley1 ; jafferson , differ basically on the choice of . If the financial time series is uncorrelated one expects that , as is the case for the standard Brownian motion. On the other hand, if with one then says that the time series has long-term memory. The exponent is generally referred to as the Hurst exponent.

To understand simply the interest of this exponent in describing correlations, we recall that the fractional Brownian motion (FBM) is a Gaussian process with zero mean and stationary increments whose variance and covariance can be written a1 ; a2 ; a3 ; a4

| (25) | |||

| (26) |

where and denotes expected value.

For the process corresponds to the standard Brownian motion, in which case the increments are statistically independent and represent the usual white noise. For the increments display long-range correlation with

| (27) |

where the average is made over and the full time window of the analysis. Thus, if the increments of the FBM are positively correlated and we say that the process exhibits persistence. Likewise, for the increments are negatively correlated and the FBM is said to show anti-persistence a1 ; a2 ; a3 ; a4 .

Let us apply the discussion above on FBM to real price series presented in previous sections. It is well known that the Hurst exponent can be extracted from financial price series using various techniques a1 ; a2 ; a3 ; a4 . In doing so, we need to compute from

| (28) |

in the range of validity of this expression. Obviously, we can write

| (29) |

At this level, we can safely assume that the returns is identically distributed. However, the returns are not independent and thus the central limit theorem does not apply. In order to lead intuition, we shall anyhow make the approximation that we can sum up the sequence of in Eq. (29) using the central limit theorem. Then, there are two cases a1 ; a2 ; a3 ; a4 : (i) if the power tail of the distribution of returns follows , the variance is finite and converges to a Gaussian distribution; (ii) if , the sum in Eq. (29) tends to Levy stable distributions. As we have shown in previous sections for the futures under consideration in this letter, we stand in the case (i). Therefore, following the discussion above, we expect a Hurst exponent of order .

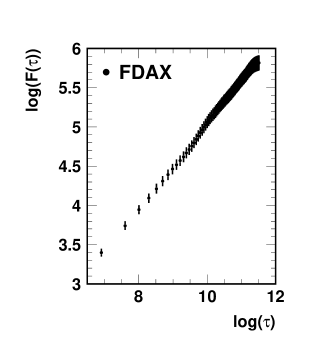

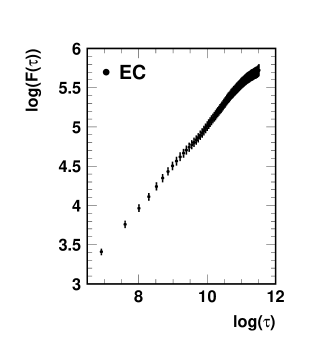

In order to determine the Hurst exponent experimentally, we compute

| (30) |

Results are presented in Fig. 8 for the DAX and Euro futures. Then, the Hurst exponent is extracted with the relation . We get: for FDAX and for EC. These results are well compatible with the value expected from the above discussion. They are also robust within the set of high liquid futures discussed in this letter. Let us note that the uncertainties on are dominated by systematical effects. We have varied the time window for the calculation, the time interval and we have also divided the original data sets over 10 years on periods of 3 years. Also, we have modified the definition of the time average defined in Eq. (30) using an exponential smoothing in order to take into account the fact that the recent past is more important than the remote past. The variations in the determination of the Hurst exponents give the errors quoted above.

Eq. (30) can be extended to higher moments of the distribution of returns as

| (31) |

which leads to the definition of generalized Hurst exponent, namely . Then, processes with independent of are called uni-fractal whereas processes where is not constant are referred to as multi-fractal a1 ; a2 ; a3 ; a4 . When considering all systematic effects listed above, we do not get any experimental sensitivity to the dependence in Eq. (31).

V Conclusion and Outlook

We have presented experimental results based on a large set of time series on futures. When studying the probability distribution of log-returns, we have shown that a t-distribution with gives a nice description of almost all data series for a time scale below hour. For hours, the Gaussian regime is reached. A particular focus has been put on the DAX and Euro futures, which both verify these properties and thus exhibit a similar statistical texture. This appears to be a quite general result that stays robust on a large set of futures, but not on any data sets. In this sense, this is not universal.

A technique using factorial moments defined on returns is described and similar results are obtained. Let us recall that factorial moments are convenient tools in nuclear physics to characterize the multiplicity distributions when phase-space resolution becomes small. In particular, correlations between particles lead to a broadening of the multiplicity distribution and to dynamical fluctuations. In this case, the factorial moments increase above with decreasing resolution. This corresponds to what can be called intermittency. A similar property has been illustrated on financial price series. An intermittent behavior has been extracted for DAX and Euro futures, using moments of order (). This leads to perfectly consistent results with the standard distribution analysis.

Let us note that from a fundamental point of view, there is no clear reason why DAX and Euro futures should present similar behavior with respect to their return distributions. Both are complex markets where many internal and external factors interact at each instant to determine the transaction price. These factors are certainly different for an index on a change parity (Euro) and an index on stocks (DAX). Thus, this is striking that we can identify universal statistical features in price fluctuations of these markets. This is really the advantage of micro-structure analysis to prompt unified approaches of different kinds of markets.

Finally, we have discussed that the power law distribution of returns is well consistent with the information encoded into the Hurst exponent. We have obtained for DAX and for Euro futures.

An immediate outlook concerns the use of this knowledge to unfold the sequence of returns into a more controlled sequence of trades. In Ref. lolo , we have proven that it is possible to design such unfolding procedure. Interestingly, the trade durations derived on the DAX and Euro futures lolo correspond perfectly to the time scales derived in this letter. In fact, building a trading strategy is another consistency test of the knowledge we can get from the time series analysis. The broadening of the probability distribution of returns when decreasing the time scale and the associated dynamical fluctuations, as extracted from the factorial moments can serve as a guide in the unfolding procedure.

References

- (1) R. Mantegna and H. E. Stanley, An Introduction to Econophysics, Cambridge Univ. Press, Cambridge, 2000.

- (2) D. Duffie, Dynamic Asset Pricing, 3rd ed., Princeton University Press, Princeton, NJ, 2001.

- (3) J. Voit, The Statistical Mechanics of Financial Markets, Springer, Berlin, 2003.

- (4) see e.g. J.P. Bouchaud, M. Potters, Theory of Financial Risks and Derivative Pricing, Cambridge University Press (2004).

- (5) P. Gopikrishnan et al., Eur. Phys. B 3 (1998) 139-140.

- (6) P. Gopikrishnan et al., Phys. Rev. 60 (1999) 5305-5316.

- (7) G.-F. Gu, W. Chen and W.-X. Zhou, Physica A 387 (2008) 495-502.

- (8) V. Plerou et al., Phys. Rev. 77 (2008) 037101.

- (9) G.-H. Mu and W.-X. Zhou, Phys. Rev. 82 (2010) 066103.

- (10) L. Schoeffel, arXiv:1110.1006.

- (11) B. Mandelbrot, Int. Eco. Rev. 1 79 (1960); J. Business 36 34 (1963).

- (12) L. Schoeffel, arXiv:1108.5596

- (13) C. Tsallis, Braz. J. Phys. 29 (1999) 1.

- (14) D. Prato and C. Tsallis, Phys. Rev. E 60 (1999) 2398.

- (15) A. Rapisarda, A. Pluchino and C. Tsallis, arXiv:cond-mat/0601409.

- (16) A. Bialas and R. Peschanski, Nucl. Phys. B273 (1986) 703; Nucl. Phys. B308 (1986) 857.

- (17) P. Lipa et al., Phys. Lett B285 (1992) 300.

- (18) I. M. Dremin, V. Arena, G. Boca, G. Gianini, S. Malvezzi, M. Merlo, S. P. Ratti, C. Riccardi et al., Phys. Lett. B336 (1994) 119-124. [hep-ex/9405007].

- (19) I. M. Dremin, R. C. Hwa, Phys. Rev. D49 (1994) 5805-5811.

- (20) J. Rames, arXiv:hep-ph/9411349.

- (21) Y.L. Dokshitzer and I.M. Dremin Nuclear Physics B 402 (1993) 139.

- (22) W. Ochs and J. Wosiek, Phys. Lett. B289 (1992) 159, and Phys. Lett. B305 (1993) 144.

- (23) H. E. Hurst, Trans. Am. Soc. Civ. Eng. 116 (1951) 770; H. E. Hurst, R. P. Black, and Y. M. Simaika, Long-Term Storage: An Experimental Study, Constable, London, 1965.

- (24) C.-K Peng, S. V. Buldyrev, S. Havlin, M. Simons, H. E. Stanley, A. L. Goldberger, Phys. Rev. E 49 (1994) 1685.

- (25) J. G. Moreira, J. Kamphorst Leal da Silva, S. Oliffson Kamphorst, J. Phys. A 27 (1994) 8079.

- (26) L. Schoeffel, arXiv:1108.3155, submitted to J. of Inv. Strategies.