Estimating beta-mixing coefficients via histograms

Abstract

The literature on statistical learning for time series often assumes asymptotic independence or “mixing” of the data-generating process. These mixing assumptions are never tested, nor are there methods for estimating mixing coefficients from data. Additionally, for many common classes of processes (Markov processes, ARMA processes, etc.) general functional forms for various mixing rates are known, but not specific coefficients. We present the first estimator for beta-mixing coefficients based on a single stationary sample path and show that it is risk consistent. Since mixing rates depend on infinite-dimensional dependence, we use a Markov approximation based on only a finite memory length . We present convergence rates for the Markov approximation and show that as , the Markov approximation converges to the true mixing coefficient. Our estimator is constructed using -dimensional histogram density estimates. Allowing asymptotics in the bandwidth as well as the dimension, we prove concentration for the histogram as an intermediate step. Simulations wherein the mixing rates are calculable and a real-data example demonstrate our methodology.

keywords:

1109.5998 \startlocaldefs \newaliascntlemmatheorem \aliascntresetthelemma \newaliascntcortheorem \aliascntresetthecor \newaliascntdeftheorem \aliascntresetthedef \endlocaldefs

and

1 Introduction

The ordinary theory of statistical inference is overwhelmingly concerned with independent observations, but the exact work done by assuming independence is often mis-understood. It is not, despite a common impression, to guarantee that large samples are representative of the underlying population, ensemble, or stochastic source. If that were all that were needed, one could use the ergodic theorem for dependent sources equally well. Rather, assuming independence lets statistical theorists say something about the rate at which growing samples approximate the true distribution. Under statistical independence, every observation is completely unpredictable from every other, and hence provides a completely new piece of information about the source. Consequently, the most common measures of information — including the Kullback-Leibler divergence between probability measures, the Fisher information about parameters, and the joint Shannon entropy of random variables — are all strictly proportional to the number of observations for IID sources. Under dependence, later events are more or less predictable from earlier ones, hence they do not provide completely new observations, and information accumulates more slowly. Assuming ergodicity alone, the convergence of samples on the source can be arbitrarily slow, and statistical theory is crippled. Without more stringent assumptions than ergodicity, one is always effectively in an situation no matter how many observations one has.

To go beyond independence, statistical theory needs assumptions on the data-generating processes which control the rate at which information accumulates. For time series analysis, the most natural replacement for independence is requiring the asymptotic independence of events far apart in time, or mixing. Mixing quantifies the decay in dependence as the future moves farther from the past. There are many definitions of mixing of varying strength with matching dependence coefficients [see 11, 9, 5, for reviews], but many of the results in the statistical literature focus on -mixing or absolute regularity. Roughly speaking (see Section 2.1 below for a precise statement), the -mixing coefficient at lag is the total variation distance between the actual joint distribution of events separated by time steps and the product of their marginal distributions, i.e., the distance from independence.

Much of the theoretical groundwork for the analysis of mixing processes was laid years ago [36, 4, 12, 26, 1, 30, 38, 39], but it remains an active topic in probability, statistics and machine learning. Among the many works on this topic, we may mention the study of non-parametric inference under mixing conditions by Bosq [3], consistent time series forecasting by support vector machines [29], probably approximately correct learning algorithms with mixing inputs [33, 20] and stability-based generalization error bounds [23]. To actually use such results, however, requires knowing the -mixing coefficients, .

Many common time series models are known to be -mixing, and the rates of decay are known up to constant factors given the true parameters of the process. Among the processes for which such results exist are ARMA models [24], GARCH models [6], and certain Markov processes — see Doukhan [11] for an overview of such results. (Fryzlewicz and Subba Rao [15] derive upper bounds for the - and -mixing rates of non-stationary ARCH processes.) With few exceptions, however, these results do not give the actual mapping from parameters to mixing coefficients. For example, it is known that the mixing coefficients of the ARMA process at time lag are for some . While knowledge of the ARMA parameters determine the joint distribution, no one has yet figured out how to map from these parameters to the constants, or even to . To our knowledge, only Nobel [25] approaches a solution to the problem of estimating mixing rates by giving a method to distinguish between different polynomial mixing rate regimes through hypothesis testing. Thus the theoretical results which presume that the mixing coefficients are known cannot actually be applied to assist in the analysis of data, or even of parametric models.

These issues also arise in interpreting the output of Markov chain Monte Carlo (MCMC) algorithms. Even when the Markov chain is in equilibrium, sampling from the desired invariant distribution, the samples are dependent. How much dependence persists across samples is a very important issue for users wishing to control Monte Carlo error, or planning how long a run they need. In some rare cases, theoretical results show that certain MCMC algorithms are rapidly mixing, meaning again roughly that . Such results generally do not give , let alone , which is what users would need.

We present the first method for estimating the -mixing coefficients for stationary time series data given a single sample path. Our methodology can be applied to real data assumed to be generated from some unknown -mixing process. Additionally, it can be used to examine known mixing processes, thereby determining exact mixing rates via simulation. (This includes, but is not limited to, MCMC algorithms.) Section 2 defines the -mixing coefficient, our estimator of it, and states our main results on convergence rates and consistency for the estimator. Section 3 gives an intermediate result on the convergence of the histogram estimator with -mixing inputs which is asymptotic in the dimension of the target distribution in addition to the bandwidth. Some of our results and techniques here are of independent interest for high-dimensional density estimation. Section 4 proves the main results from Section 2. Section 5 demonstrates the performance of our estimator in three simulated examples, providing good recovery of known rates in simple settings as well as providing insight into unknown mixing regimes, and also examines a dataset containing recession indicators for developed economies. Section 6 concludes and lays out some avenues for future research.

2 Estimator and consistency results

In this section, we present one of many equivalent definitions of absolute regularity and state our main results, deferring proof to §4.

To fix notation, let be a sequence of random variables where each is a measurable function from a probability space into with the Borel -field . A block of this random sequence will be given by where and are integers, and either may be infinite. We use similar notation for the sigma fields generated by these blocks. In particular, will denote the sigma field generated by , and the joint distribution of will be denoted . We denote products of marginal distributions as, e.g., .

2.1 Definitions

In this paper, we will consider only the case of stationary data.

Definition \thedef (Stationarity).

A sequence of random variables is stationary when all its finite-dimensional distributions are invariant over time: for all integers and all non-negative integers , the distribution of is the same as that of .

There are many equivalent definitions of -mixing (see for instance [11], or [5] as well as [22] or [39]), however the most intuitive is that given in Doukhan [11].

Definition \thedef (-mixing).

For each , the coefficient of absolute regularity, or -mixing coefficient, , is

| (1) |

where is the total variation norm, and is the joint distribution of the blocks . A stochastic process is said to be absolutely regular, or -mixing, if as .

Loosely speaking, Section 2.1 says that the coefficient measures the total variation distance between the joint distribution of random variables separated by time units, and the distribution under which random variables separated by time units are independent, . We note that in the most general setting in the literature, , however, this additional generality is unnecessary for stationary random processes , which is the only case we consider here.

As stationarity implies that distributions of blocks of random variables are the same, and we will frequently require notation for these distributions, we will employ the following simplifications: the distribution of a -block will be notated and the joint distribution of two blocks of length separated by timepoints, , will be given by . In particular, will be written as and similarly for the associated sigma-fields when necessary.

2.2 Constructing the estimator

Our result emerges in two stages. First, we recognize that the distribution of a finite sample depends only on finite-dimensional distributions. This leads to an estimator of a finite-dimensional version of . Next, we let the finite-dimension increase to infinity with the size of the observed sample.

For positive integers , and , define

| (2) |

Also, let be the histogram estimator of the joint density of consecutive observations, that is

where is the bin containing and is the indicator function. Similarly, let be the -dimensional histogram estimator of the joint density of two sets of consecutive observations separated by time points, i.e

Note that as we have assumed , in the above definitions, and respectively with . As we assume fixed throughout, we suppress this dependence. We discuss this issue further in a remark following our main result in the next subsection.

We construct an estimator of based on these two histograms.111While it is clearly possible to replace histograms with other choices of density estimators (most notably kernel density estimators), histograms in this case are more convenient theoretically and computationally. See §6 for more details. Define

| (3) |

We will show that, by having grow (slowly) with , this estimator will converge to . This can be seen most clearly by bounding the risk of the estimator with its estimation and approximation errors:

The first term is the error of estimating from a random sample. The second term is the non-stochastic error induced by approximating the infinite dimensional coefficient, , by its -dimensional counterpart, .

2.3 Assumptions and main results

The results of this paper require two main assumptions. The first is that the process is generated by a stationary, -mixing distribution with density . Second, we must place some conditions on the density to ensure that the histogram estimators and will actually converge to the densities and . Specifically, we will assume continuity and regularity conditions as in [13]222We discuss modifications for discrete distributions below, p. 2.3.:

-

1.

and is absolutely continuous on its support, with a.e. partial derivatives

-

2.

and is absolutely continuous on its support, with a.e. partial derivatives

-

3.

for all .

We will presume below that has a bounded domain, but we do not list that as a separate assumption, for two reasons. First, even if has unbounded support, we can always smoothly and invertibly map into (say) , without disturbing any of the assumptions above, and without changing , since total variation distance is invariant under invertible transformations. Second, the unbounded-domain case could be handled by, basically, a remainder argument: the support of the histogram density estimate is effectively set by the empirical range of the , and, with high and growing probability, this includes the overwhelming majority of the probability-mass. Following this through would however needlessly complicate our proofs.

Under these conditions, we can state the two main results of this paper. Our first theorem in this section establishes consistency of as an estimator of for all -mixing processes.

Theorem 1.

Let be a sample from an arbitrary -mixing process satisfying the conditions above. Provided that , , , and as , then for any ,

In this general case, we need doubly asymptotic results about the histogram estimator, that is, the histogram estimators require shrinking bin widths in increasingly higher dimensions. In Section 4, we give appropriate rates for and to achieve the optimal rate of convergence for the estimation error. Of course, with discrete data or Markov models, we may not need doubly asymptotic results since either the maximum number of bins or the memory length of the process is fixed.

For a Markov process of order or less, . In this case, we can give the convergence rate of our estimator.

Theorem 2.

Let be a sample from a Markov process of order no larger than . Then, taking the bandwidths to be for and for ,

| (4) |

Here, is the Lambert function, i.e., the (multivalued) inverse of [7]. As is bigger than but smaller than , our estimator attains nearly parametric convergence rates when the data come from a Markov process of order . Likewise, if we were interested in estimating only the finite dimensional mixing coefficients rather than , Theorem 2 gives the rate of convergence.

The proof of these two theorems requires showing the convergence of the histogram density estimator with -mixing data. We present this result in Section 3. First, we discuss some important details regarding these theorems and provide a method for choosing the number of bins in the histogram.

Remarks on Discrete-Valued Processes

An important special case is that of discrete-valued -mixing processes, including Markov chains in the strict sense. The symbols of any finite alphabet can be represented by points in , and -mixing coefficients are invariant to the choice of representation. Of course, the resulting distributions in will be mixtures of delta functions, and so not absolutely continuous. However, for a finite number of points, there will exist a maximum bin-width below which each bin of the histogram will contain at most one positive-probability point. While the corresponding histogram density estimator is always absolutely continuous, it is easily seen that below this bin-width, the histogram estimator has the same -mixing coefficient as the true distribution. Moreover, the errors of estimation and approximation dealt with in the proofs of our theorems and lemmas are, if anything, even smaller for finite-alphabet processes, making our results somewhat conservative.

Remarks on the interaction between , , and

The interaction between the dimension of the data and the bandwidth of the histogram (equivalently the number of bins used) is important for applications. However, we use to represent more than the “dimension” of the dataset: is the product of the dimension of the range of , , and the length of the Markov approximation. For example, suppose that the data consist of time-series (we will use a data set with in Section 5) which is known to be first-order Markov. Then, for all is sufficient for our estimator to achieve the convergence rate specified in Theorem 2 provided is chosen appropriately. However, if this same dataset is non-Markovian but still -mixing, then in order to estimate consistently, we must use successively larger Markov approximations as . This means taking for an increasing function . Thus, even though the data are of fixed dimension , the dimension over which the histogram is constructed must increase to infinity to give estimation consistency as in Theorem 1. Section 4 shows that if , then there is a polynomial rate for the bandwidth which satisfies the conditions of Theorem 1. Of course for a fixed dataset application, one must choose the bandwidth and potentially the Markov approximation. One could fix the Markov approximation and use cross-validation for the bandwidth selection, but we have found that this procedure tends to choose bandwidths which are too small, resulting in a positive estimation bias. In the remainder of this paper, we suppress and work directly with . In the next section, we present a procedure for choosing the bandwidth for a fixed dimension .

2.4 Choosing the bandwidth

We need some way to pick the bandwidth of our histograms, or, equivalently, the number of bins. If we were doing density estimation for its own sake, the natural thing to do would be some sort of cross-validation with a loss based on the density. However, we do not really care about the density. Instead, we suggest an approach which might be called “calibration with surrogate data”.333“Surrogate data” methods are used extensively in nonlinear time series analysis for hypothesis testing, especially testing the hypothesis that there is some nonlinear deterministic structure [19]. Note that we are using the word “calibration” here in the sense in which measuring instruments are calibrated against standards, not the sense in which it is used in evaluating probabilistic forecasts [16], or the estimation technique from econometrics [18]. In outline, we construct an artificial stochastic process which shares many distributional features with the data, but where is known exactly. This lets us see which bandwidth leads to the most accurate estimation of the reference value of , and this is at least a reasonable guess at the appropriate bandwidth on the data. To flesh this out, we first describe the construction of the surrogate process with known , and then the full bandwidth-selection procedure.

We regard , the order of the Markov approximation, as fixed, and note that, by our error analysis in Theorem 2, the lag should not affect the appropriate bandwidth.444Apart from leading to slight changes to the effective . We thus proceed to construct a process where, for a given , the mixing coefficient has a known value and then try to optimize the variance of our estimator.

To generate the surrogate process, we sample blocks of length from the data . We start with a random -block then repeat that block with probability and resample a new -block with the remaining probability. We continue this process times (rounding up or down as desired) until we have a new sequence of length . Notice that the process has the same marginal distribution as the empirical marginal distribution of . Its higher-dimensional marginal distributions are not guaranteed to match those of the data, because of the abrupt change from one block to the next, and because of the random repetition of blocks. However, if , the -dimensional marginals should be close. Based on this intuition, we present Algorithm 1 for choosing the bandwith in the histograms for continuous data . We then prove two results justifying its use.

The first result presents the exact mixing coefficient for .

Proposition 3.

Suppose that the marginal density of is absolutely continuous. Fix , and let be the set of unique length- sequences appearing in , where sequence appears times. Set

Then for constructed as in Algorithm 1,

Proof.

First, let be the product measure of -blocks and call the joint distribution of -blocks associated to a hypothetical, infinite sequence generated, say, by draws of -blocks from the distribution of rather than its empirical counterpart. The total variation distance between the joint distribution of two identical copies of the same block, and the joint distribution of two independent blocks, is therefore (since the measure of this set is 0).555Requiring any coordinate to be shared between two -vectors and forces the joint distribution to put probability 1 on a lower-dimensional subspace of the product space, which would have measure 0 under the product measure, leading to a total variation distance of 1 from independence. By the same reasoning, two blocks which share some coordinates (even if not in the same positions within a block) have a TV distance of from independence. For the diagonal , we therefore have that while . Thus, the total variation between and is at least . To show that it is no more than , suppose that there was another set where . Without loss of generality, say . (If the inequality went the other way, use .) Then , so must intersect the diagonal ; let . As disjoint sets, , likewise for , so , but and , thus . But , and , so . Therefore, the total variation distance between and is .

Now, observe that is the probability that two independently drawn blocks in will, by chance, happen to be equal. Thus, simplifies to when all the blocks are distinct, as they ought to be when the generating process has an absolutely continuous distribution. The factor corrects for the fact that the empirical distributions we are using put probability on the low-dimensional subspace . ∎

With this result in hand, we will resample many time-series from our data and choose the bandwidth by minimizing the variance over some grid of values (equivalently number of bins). We do not minimize the mean squared error, because the bias of the estimator depends on the mixing coefficient. Minimizing the bias in an attempt to estimate a mixing coefficient near may result in badly biased estimates of coefficients near zero. Our next result calculates the expectation of this estimator and therefore its bias.

Proposition 4.

Suppose that the marginal density of is absolutely continuous. The expected value of based on is given by

where and are the bins for a histogram with bandwidth .

Proof.

By discretizing into histograms, the diagonal is no longer a measure 0 set, and in fact contains more mass than . By construction, the product distribution puts mass on the discretized diagonal while the joint distribution, , puts mass on the discretized diagonal. Therefore, under the histogram with bandwidth , the total variation distance between and is given by

∎

3 convergence of histograms

Convergence of density estimators is thoroughly studied in the statistics and machine learning literature. Early papers on the convergence of kernel density estimators (KDEs) include [37, 2, 28]; Freedman and Diaconis [14] look specifically at histogram estimators, and Yu [38] considers the convergence of KDEs for -mixing data and shows that the optimal IID rates can be attained. Tran [31] proves convergence for histograms under - and -mixing. Devroye and Györfi [10] argue that is a more appropriate metric for studying density estimation, and Tran [30] proves consistency of KDEs under - and -mixing. As far as we are aware, ours is the first proof of convergence for histograms under -mixing.

Our proof requires the method of blocking used in Yu [38, 39] following earlier results such as Eberlein [12], Volkonskii and Rozanov [34] and going back to Bernstein. The idea here is to translate IID results directly to mixing sequences, with corrections that reflect the -coefficients and the length of the process. To do this, one creates an imaginary sequence of independent blocks of data from the original dependent sequence. Ordinary IID results apply to the imaginary sequence, which also approximates the actual dependent sequence, to within a known tolerance.

Consider a sample from a stationary -mixing sequence with density . Let and be positive integers such that . Now imagine dividing into blocks, each of length . Identify the blocks as follows:

for . Let be the entire sequence of odd blocks , and let be the sequence of even blocks . A visual representation is shown in Figure 1. Finally, let be a sequence of blocks which are independent of but such that each block has the same distribution as a block from the original sequence. That is, construct such that

| (5) |

where means the probability law of the argument. The blocks are now an IID block sequence, in that for integers , , so standard results about IID random variables can be applied to these blocks. (See [39] for a more rigorous analysis of blocking.) We now state the main result of this section.

Theorem 5.

Let

| (6) |

be a histogram density estimator based on a sample from a -mixing sequence with stationary density , then for all , and any natural numbers and such that ,

| (7) |

where .

This theorem demonstrates a clear tradeoff between the mixing behavior of the stochastic process and the ability to concentrate the estimator close to the truth. For arbitrary -mixing processes, we cannot actually say much about the quality of this estimator other than that given enough data, it will eventually do well. For this reason, one generally assumes that the mixing coefficients display particular asymptotic behaviors like exponential or polynomial decay.

To prove Theorem 5, we use the blocking method of [39] to transform the dependent -mixing sequence into a sequence of nearly independent blocks. We then apply McDiarmid’s inequality to the blocks to derive asymptotics in the bandwidth of the histogram as well as the dimension of the target density. For completeness, we state a version of Yu’s blocking result and McDiarmid’s inequality before proving the doubly asymptotic histogram convergence for IID data. Combining these lemmas allows us to prove concentration results for histograms based on -mixing inputs.

Lemma \thelemma (Lemma 4.1 in [39]).

Let be an event with respect to the block sequence . Then,

| (8) |

where the first probability is with respect to the dependent block sequence, , and is the -fold product measure created with the marginal distribution of each block , i.e. .

This lemma essentially gives a method of applying IID results to -mixing data. Because the dependence decays as we increase the separation between blocks, widely spaced blocks are nearly independent of each other. In particular, the difference between probabilities of events generated by these nearly independent blocks and probabilities with respect to blocks which are actually independent can be controlled by the -mixing coefficient.

Lemma \thelemma (McDiarmid Inequality [21]).

Let be independent random variables, with taking values in a set for each . Suppose that the measurable function satisfies

whenever the vectors and differ only in the coordinate. Then for any ,

Since we will need the dimension of the histograms to grow with , we prove the following lemma which provides the doubly asymptotic convergence of the histogram estimator for IID data. It differs from standard histogram convergence results in the bias calculation. In this case we need to be more careful about the interaction between and .

Lemma \thelemma.

For an IID sample from some density on ,

| (9) | ||||

| (10) |

where is the histogram estimate using a grid with sides of length .

Proof of Section 3.

Let be the probability of falling into the bin . Denote the total number of bins by . Then,

Using a Taylor expansion

where . Therefore, is given by

since the integral of the second term over the bin is zero. This means that for the bin,

Therefore,

Since each bin is bounded, we can sum over all bins. The number of bins is by definition, so

∎

The dimension of the target density is analogous to the order of the Markov approximation. Therefore, the convergence rates we give are asymptotic in the bandwidth which shrinks as increases, but also in the dimension which increases with . Even under these asymptotics, histogram estimation in this sense is not a high dimensional problem. The dimension of the target density considered here is on the order of , a rate somewhere between and .

We can combine the above lemmas to prove the main result of this section. Essentially, we use Section 3 to transform the problem from one about dependent data points to one involving independent blocks, we then apply Section 3 to the blocks to get one-sided concentration inequalities, and finally, we use Section 3 to ensure that certain expectations are bounded.

Proof of Theorem 5.

Let be the loss of the histogram estimator, where is defined in (6). Let , , and be histograms based on the block sequences , , and respectively. Then

Now,

where the equality in the last line (using ) is implicit in the construction of from (5) and . Here,

so by Section 3, as long as for , and , then for all there exists such that for all , . Now applying Section 3 to the event gives

where the probability on the right is for the -field generated by the independent block sequence . Since these blocks are independent, showing that satisfies the bounded differences requirement allows for the application of Section 3 to the blocks. For any two block sequences and with for all , then

Therefore,

∎

4 Proofs of results in Section 2.3

With the structure from the previous section, we can state a concentration inequality for .

Lemma \thelemma.

Consider a sample from a stationary -mixing process. Let and be positive integers such that and . Then

where and .

The proof of Section 4 relies on the triangle inequality and the relationship between total variation distance and the distance between densities.

Proof of Section 4.

For any two probability measures and defined on the same probability space with associated densities and with respect to some dominating measure ,

Recall that is the -dimensional stationary distribution of the -order Markov approximation in the notation of (2), and is the joint distribution of the bivariate random process created by the initial process and itself separated by time steps. By the triangle inequality, we can upper bound for any . Let and be the distributions associated with histogram estimators and respectively. Then,

where is our estimator and the remaining terms are the distance between a density estimator and the target density. Thus,

A similar argument starting from shows that

so we have that

Therefore,

where and . ∎

Proof of Theorem 2.

By Section 4, we have

To balance both terms, one needs . Since for Markov processes, then taking is sufficient. Now, solving

gives giving the result. ∎

The proof of Theorem 1 requires two steps which are given in the following Lemmas. The first specifies the histogram bandwidth and the rate at which (the dimensionality of the target density) goes to infinity. If the dimensionality of the target density were fixed, we could achieve rates of convergence similar to those for histograms based on IID inputs as shown in Theorem 2. However, we wish to allow the dimensionality to grow with , so the rates are much slower as shown in the following lemma.

Lemma \thelemma.

Proof of Section 4.

It is also necessary to show that as grows, we have the nonstochastic convergence . We now prove this result.

Lemma \thelemma.

converges to as .

Proof of Section 4.

We can rewrite Section 2.1 as

and as

| (13) |

As such for all and . We can rewrite (13) in terms of finite-dimensional marginals:

Because of the nested nature of these sigma-fields, we have

for all finite . Therefore, for fixed , is a monotone increasing sequence which is bounded above, and it converges to some limit . To show that requires some additional steps.

Let , which is a signed measure on . Let

which is a signed measure on . Decompose into positive and negative parts as and similarly for . Notice that since is constructed using the marginals of , then for all . Now since is the difference of probability measures, we must have that

| (14) |

for all .

Define . Let . Let be such that

| (15) |

Such a set is guaranteed by the Hahn decomposition theorem (letting be a set which attains the supremum in (13), we can throw away any subsets with negative measure) and (14) assuming without loss of generality that . We can use the field to approximate in the sense that, for all , we can find such that (see Theorem D in Halmos [17, §13] or Lemma A.24 in Schervish [27]). Now,

by (15) since and . Therefore, since , we have

| (16) | ||||

Also,

since and are contained in and . Therefore

Similarly,

since and by (16). Finally,

And since , we have that for all there exists such that for all ,

Thus, we must have that , so that as desired. ∎

5 Performance in examples

To demonstrate the performance of our estimator, we examine three simulated examples and an example using real data.

5.1 Simulations

The first simulation is a simple two-state Markov chain. Thus, its mixing rate is known, only two bins are required in the histogram, and we can use . The second takes this Markov chain as an unobserved input and outputs a non-Markovian binary sequence which remains -mixing, but we must now allow to grow with . Finally, we examine an autoregressive model wherein we can again use as it is Markovian, but there is an uncountable state space.

5.1.1 Markov process

As shown in [8], homogeneous recurrent Markov chains are geometrically -mixing, i.e. for some . In particular, if the Markov chain has stationary distribution and -step transition distribution , then

| (17) |

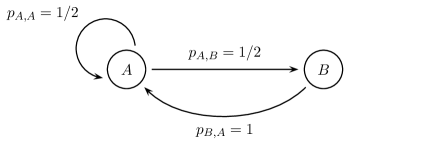

Consider first the two-state Markov chain pictured in Figure 2.

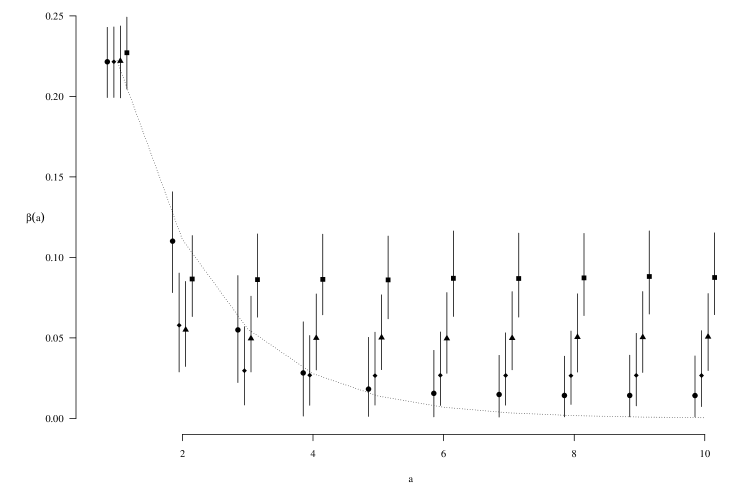

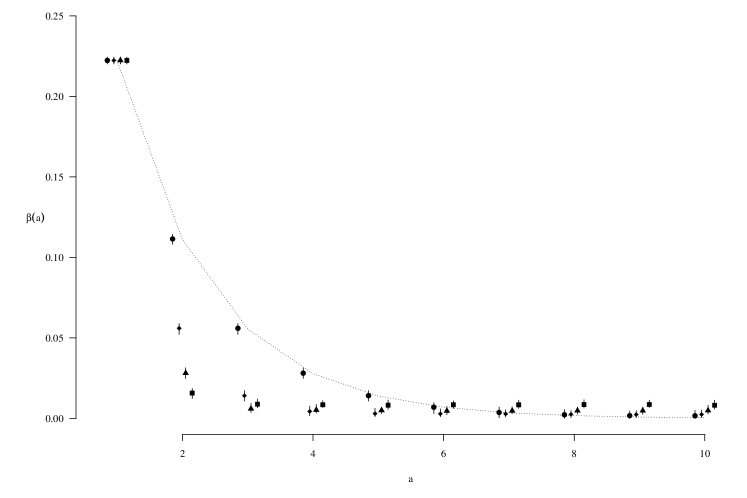

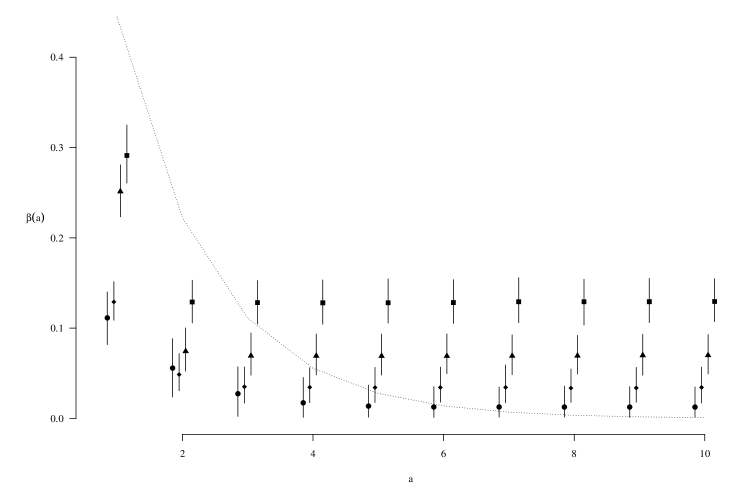

By direct calculation using (17), the mixing coefficients for this process are . We simulated chains of length from this Markov chain. Figure 3 shows the performance of the estimator based on 1000 replications. Here, we have used two bins in all cases (as there are only two states), but we allow the Markov approximation to vary as , even though is exact. The estimator performs well for , but begins to exhibit a positive bias as increases. This is because the estimator is nonnegative, whereas the true mixing rates are quickly approaching zero. The upward bias is exaggerated for larger . This bias goes away as . This is demonstrated in Figure 4 which uses .

5.1.2 Markov chain of order

Before examining a long-memory process, we simulate an intermediate case. We construct a Markov model of order on using the following transition probability:

| with | (18) |

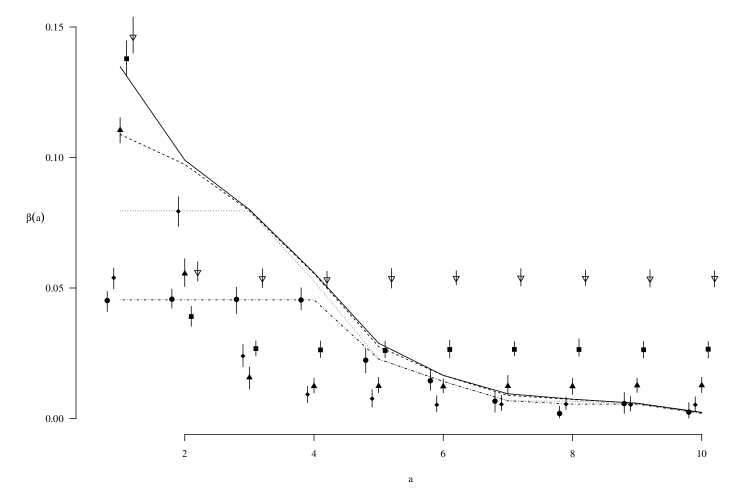

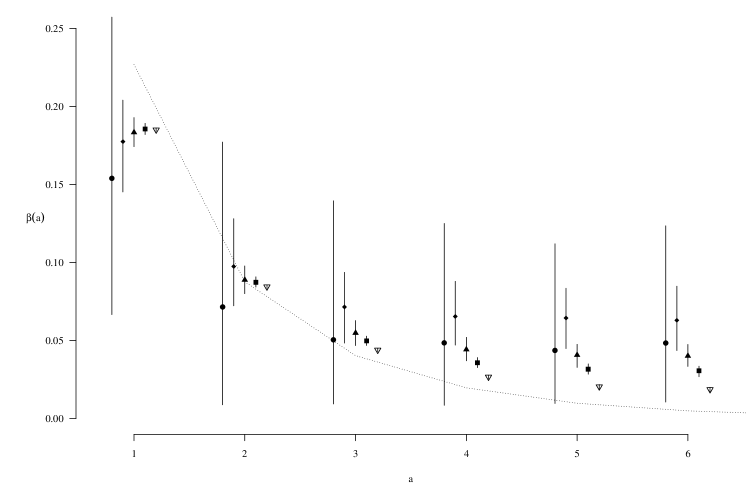

Essentially, this process avoids long strings of ones or zeros. In this case, we have that for all . Therefore, we should be able to estimate well by taking . However, for smaller values of , we will tend to underestimate . In fact, it is possible, using equation (2), to calculate for each . We simulated chains of length from this Markov chain with . Figure 5 shows the performance of the estimator based on 100 replications. Here, we allow the Markov approximation to vary as , even though is exact. As above, the estimator performs well for . Note that, for , we can estimate well as we would expect.

5.1.3 Long-memory discrete process

As an example of a long memory process, we construct, following Weiss [35], a partially observable Markov process which we call the “even process”. Let be the observed sequence which takes as input the Markov process constructed above. We observe

| (19) |

Since is Markovian, the joint process is as well, so we can calculate its mixing rate . The even process must also be -mixing, and at least as fast as the joint process, since it is a measurable function of a mixing process. However, itself is non-Markovian: runs of ones must have even lengths, so we need to know how many ones have been observed to know whether the next observation can be zero or must be a one. Thus, the true mixing coefficients are bounded above, though unknown. Using the same procedure as above, Figure 6 shows the estimated mixing coefficients. Again we observe a bias for large due to the nonnegativity of the estimator.

5.1.4 Autoregressive process

Finally, we estimate the -mixing coefficients for an AR(1) model

While, this process is Markovian, there is no closed form solution to (17), so we calculate it via numerical integration. Figure 7 shows the performance of the estimator for . Figure 7 shows the performance for varying . We select the bandwidth for each using Algorithm 1. The selected numbers of bins are 2, 8, 17, 44, 90. As grows, the bias shrinks, even for large while the variance of the estimators also shrinks rapidly. However, this figure shows that even with large amounts of data, accurate estimation is difficult.

5.2 Real data

To illustrate the performance of our estimator in applications, we investigate an economic dataset in larger dimensions than in the simulations above. We use a -dimensional macroeconomic time series which tracks recessions in various countries. In particular, we track recession indicators in Canada, Germany, France, Great Britain, Japan, and the United States. We chose this dataset for a number of reasons. First, the data are publicly available from the Federal Reserve Economic Database

| Series ID | Country |

|---|---|

| CANRECDM | Canada |

| DEURECDM | Germany |

| FRARECDM | France |

| GBRRECDM | Great Britain |

| JPNRECDM | Japan |

| USARECDM | United States |

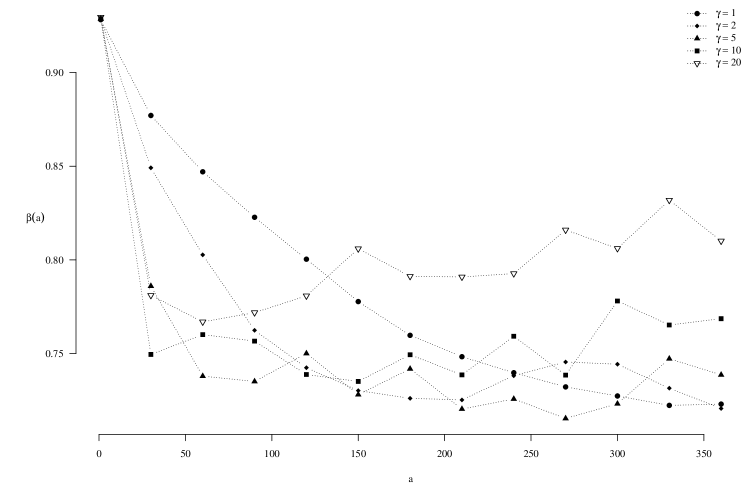

using the series presented in Table 1. Second, the series is long, providing daily observations from December 1, 1961 until September of 2014 for a total of observations. This will enable us to allow to grow quite quickly. Third, the data are binary, so mixing coefficients may be a more reasonable measure of temporal dependence than, say, correlation. It also means we can ignore the issue of bin selection. Fourth, the data likely have high temporal dependence as the indicators are based on a combination of monthly and quarterly macroeconomic aggregates such as gross domestic product, inflation, and unemployment. This means that using both large and very large is necessary. Finally, the data are strongly cross-sectionally dependent since these are all developed countries likely to enter recession or expansion at similar times. This cross-sectional dependence makes it unreasonable to examine each series individually.

With six dimensions, the curse of dimensionality is immediately an issue: with bins along each dimension will have bins when the Markov approximation is of length (that is ). In Figure 8, we present estimated mixing coefficients for between 1 and (giving estimates for 1-month, 2-month, up to 1-year lag dependence) and . As the figure illustrates, these data are highly temporally dependent. The coefficients for decrease smoothly in the lag while the estimates for larger behave less well. However, only the case of seems to exhibit the strong upward bias we might expect if is large relative to . Note that in this case we are estimating the differences in probabilities in bins, although many of these will be empty under both distributions.

6 Discussion

We have shown that our estimator of the -mixing coefficients is consistent for the true coefficients under some conditions on the data-generating process. There are numerous results in the statistics literature which assume knowledge of the -mixing coefficients, yet as far as we know, this is the first estimator for them. An ability to estimate these coefficients will allow researchers to apply existing results to dependent data without the need to arbitrarily assume their values. Additionally, it will allow probabilists to recover unknown mixing coefficients for stochastic processes via simulation. Despite the obvious utility of this estimator, as a consequence of its novelty, it comes with a number of potential extensions which warrant careful exploration as well as some drawbacks.

Several other mixing and weak-dependence coefficients also have a total-variation flavor, perhaps most notably -mixing [11, 9, 5]. None of them have estimators, yet, and the same trick might well work for them, too.

The reader will note that Theorem 1 does not provide a convergence rate. The rate in Theorem 2 applies only to Markov processes or the difference between and . In order to provide a rate in Theorem 1, we would need a better understanding of the non-stochastic convergence of to . It is not immediately clear that this quantity can converge at any well-defined rate. In particular, it seems plausible, but is not proven, that the rate of convergence depends on the tail of the sequence .

The use of histograms rather than kernel density estimators for the joint and marginal densities is surprising and perhaps not ultimately necessary. As mentioned above, Tran [30] proved that KDEs are consistent for estimating the stationary density of a time series with -mixing inputs, so perhaps one could replace the histograms in our estimator with KDEs. However, this would need an analogue of the double asymptotic results proven for histograms in Section 3. In particular, we need to estimate increasingly higher dimensional densities as . This does not cause a problem of small--large- since is chosen as a function of , however it will lead to increasingly higher dimensional integration. For histograms, the integral is always computationally trivial, but in the case of KDEs, the numerical accuracy of the integration algorithm becomes increasingly hard to assure. This issue could swamp any statistical efficiency gains obtained through the use of kernels, though further investigation is warranted.

The main drawback of an estimator based on a density estimate is its complexity. The mixing coefficients are functionals of the joint and marginal distributions derived from the stochastic process , however, it is unsatisfying to estimate densities and calculate integrals in order to estimate a single number. Vapnik’s main principle for solving problems using a restricted amount of information is “When solving a given problem, try to avoid solving a more general problem as an intermediate step [32, p. 30].” However, despite our estimator’s complexity, we are able to obtain nearly parametric rates of convergence to the Markov approximation departing only by logarithmic factors. While the simplicity principle is clearly violated, perhaps our seed will precipitate a more aesthetically pleasing solution.

Acknowledgements

The authors are grateful to Darren Homrighausen for providing useful insights. We also thank two anonymous reviewers for helpful comments on an earlier version of this paper. Finally, we would like to thank the Institute for New Economic Thinking for financial support. In addition, DJM acknowledges support from the NSF (DMS 1407439) and CRS acknowledges support from grants of the NIH (R01 NS047493) and the NSF (DMS 1207759, 1418124).

References

- Athreya and Pantula [1986] {barticle}[author] \bauthor\bsnmAthreya, \bfnmK. B.\binitsK. B. and \bauthor\bsnmPantula, \bfnmS. G.\binitsS. G. (\byear1986). \btitleA note on strong mixing of ARMA processes. \bjournalStatistics & Probability Letters \bvolume4 \bpages187–190. \endbibitem

- Bickel and Rosenblatt [1973] {barticle}[author] \bauthor\bsnmBickel, \bfnmP. J.\binitsP. J. and \bauthor\bsnmRosenblatt, \bfnmM.\binitsM. (\byear1973). \btitleOn Some Global Measures of the Deviations of Density Function Estimates. \bjournalThe Annals of Statistics \bvolume1 \bpages1071–1095. \endbibitem

- Bosq [1998] {bbook}[author] \bauthor\bsnmBosq, \bfnmD.\binitsD. (\byear1998). \btitleNonparametric Statistics for Stochastic Processes: Estimation and Prediction, \bedition2nd ed. \bpublisherSpringer Verlag, \baddressNew York. \endbibitem

- Bradley [1983] {barticle}[author] \bauthor\bsnmBradley, \bfnmR. C.\binitsR. C. (\byear1983). \btitleAbsolute regularity and functions of Markov chains. \bjournalStochastic Processes and their Applications \bvolume14 \bpages67–77. \endbibitem

- Bradley [2005] {barticle}[author] \bauthor\bsnmBradley, \bfnmRichard C.\binitsR. C. (\byear2005). \btitleBasic Properties of Strong Mixing Conditions. A Survey and Some Open Questions. \bjournalProbability Surveys \bvolume2 \bpages107–144. \endbibitem

- Carrasco and Chen [2002] {barticle}[author] \bauthor\bsnmCarrasco, \bfnmM.\binitsM. and \bauthor\bsnmChen, \bfnmX.\binitsX. (\byear2002). \btitleMixing and Moment Properties of Various GARCH and Stochastic Volatility Models. \bjournalEconometric Theory \bvolume18 \bpages17–39. \endbibitem

- Corless et al. [1996] {barticle}[author] \bauthor\bsnmCorless, \bfnmR. M.\binitsR. M., \bauthor\bsnmGonnet, \bfnmG. H.\binitsG. H., \bauthor\bsnmHare, \bfnmD. E. G.\binitsD. E. G., \bauthor\bsnmJeffrey, \bfnmD. J.\binitsD. J. and \bauthor\bsnmKnuth, \bfnmD. E.\binitsD. E. (\byear1996). \btitleOn the Lambert Function. \bjournalAdvances in Computational Mathematics \bvolume5 \bpages329–359. \endbibitem

- Davydov [1973] {barticle}[author] \bauthor\bsnmDavydov, \bfnmY. A.\binitsY. A. (\byear1973). \btitleMixing conditions for Markov chains. \bjournalTheory of Probability and its Applications \bvolume18 \bpages312–328. \endbibitem

- Dedecker et al. [2007] {bbook}[author] \bauthor\bsnmDedecker, \bfnmJ.\binitsJ., \bauthor\bsnmDoukhan, \bfnmP.\binitsP., \bauthor\bsnmLang, \bfnmG.\binitsG., \bauthor\bsnmLeon R., \bfnmJ. R.\binitsJ. R., \bauthor\bsnmLouhichi, \bfnmS.\binitsS. and \bauthor\bsnmPrieur, \bfnmC.\binitsC. (\byear2007). \btitleWeak Dependence: With Examples and Applications. \bpublisherSpringer Verlag, \baddressNew York. \endbibitem

- Devroye and Györfi [1985] {bbook}[author] \bauthor\bsnmDevroye, \bfnmL.\binitsL. and \bauthor\bsnmGyörfi, \bfnmL.\binitsL. (\byear1985). \btitleNonparametric Density Estimation: The View. \bpublisherJohn Wiley & Sons, Inc., \baddressNew York. \endbibitem

- Doukhan [1994] {bbook}[author] \bauthor\bsnmDoukhan, \bfnmPaul\binitsP. (\byear1994). \btitleMixing: Properties and Examples. \bpublisherSpringer Verlag, \baddressNew York. \endbibitem

- Eberlein [1984] {barticle}[author] \bauthor\bsnmEberlein, \bfnmE.\binitsE. (\byear1984). \btitleWeak Convergence of Partial Sums of Absolutely Regular Sequences. \bjournalStatistics & Probability Letters \bvolume2 \bpages291–293. \endbibitem

- Freedman and Diaconis [1981a] {barticle}[author] \bauthor\bsnmFreedman, \bfnmD.\binitsD. and \bauthor\bsnmDiaconis, \bfnmP.\binitsP. (\byear1981a). \btitleOn the Histogram as a Density Estimator: Theory. \bjournalProbability Theory and Related Fields \bvolume57 \bpages453–476. \endbibitem

- Freedman and Diaconis [1981b] {barticle}[author] \bauthor\bsnmFreedman, \bfnmD.\binitsD. and \bauthor\bsnmDiaconis, \bfnmP.\binitsP. (\byear1981b). \btitleOn the Maximum Deviation Between the Histogram and the Underlying Density. \bjournalProbability Theory and Related Fields \bvolume58 \bpages139–167. \endbibitem

- Fryzlewicz and Subba Rao [2011] {barticle}[author] \bauthor\bsnmFryzlewicz, \bfnmP.\binitsP. and \bauthor\bsnmSubba Rao, \bfnmS.\binitsS. (\byear2011). \btitleMixing properties of ARCH and time-varying ARCH processes. \bjournalBernoulli \bvolume17 \bpages320–346. \endbibitem

- Gneiting, Balabdaoui and Raftery [2007] {barticle}[author] \bauthor\bsnmGneiting, \bfnmTilmann\binitsT., \bauthor\bsnmBalabdaoui, \bfnmFadoua\binitsF. and \bauthor\bsnmRaftery, \bfnmAdrian E\binitsA. E. (\byear2007). \btitleProbabilistic forecasts, calibration and sharpness. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume69 \bpages243–268. \endbibitem

- Halmos [1974] {bbook}[author] \bauthor\bsnmHalmos, \bfnmP. R.\binitsP. R. (\byear1974). \btitleMeasure Theory. \bseriesGraduate Texts in Mathematics. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Hansen and Heckman [1996] {barticle}[author] \bauthor\bsnmHansen, \bfnmLars Peter\binitsL. P. and \bauthor\bsnmHeckman, \bfnmJames J\binitsJ. J. (\byear1996). \btitleThe empirical foundations of calibration. \bjournalThe Journal of Economic Perspectives \bpages87–104. \endbibitem

- Kantz and Schreiber [2004] {bbook}[author] \bauthor\bsnmKantz, \bfnmHolger\binitsH. and \bauthor\bsnmSchreiber, \bfnmThomas\binitsT. (\byear2004). \btitleNonlinear time series analysis \bvolume7. \bpublisherCambridge university press. \endbibitem

- Karandikar and Vidyasagar [2009] {bunpublished}[author] \bauthor\bsnmKarandikar, \bfnmR. L.\binitsR. L. and \bauthor\bsnmVidyasagar, \bfnmM.\binitsM. (\byear2009). \btitleProbably Approximately Correct Learning with Beta-Mixing Input Sequences. \bnotesubmitted for publication. \endbibitem

- McDiarmid [1989] {bincollection}[author] \bauthor\bsnmMcDiarmid, \bfnmC.\binitsC. (\byear1989). \btitleOn the Method of Bounded Differences. In \bbooktitleSurveys in Combinatorics (\beditor\bfnmJ.\binitsJ. \bsnmSiemons, ed.) \bpages148–188. \bpublisherCambridge University Press. \endbibitem

- Meir [2000] {barticle}[author] \bauthor\bsnmMeir, \bfnmRon\binitsR. (\byear2000). \btitleNonparametric Time Series Prediction Through Adaptive Model Selection. \bjournalMachine Learning \bvolume39 \bpages5–34. \endbibitem

- Mohri and Rostamizadeh [2010] {barticle}[author] \bauthor\bsnmMohri, \bfnmMehryar\binitsM. and \bauthor\bsnmRostamizadeh, \bfnmAfshin\binitsA. (\byear2010). \btitleStability Bounds for Stationary -mixing and -mixing Processes. \bjournalJournal of Machine Learning Research \bvolume11 \bpages789–814. \endbibitem

- Mokkadem [1988] {barticle}[author] \bauthor\bsnmMokkadem, \bfnmA.\binitsA. (\byear1988). \btitleMixing properties of ARMA processes. \bjournalStochastic Processes and their Applications \bvolume29 \bpages309–315. \endbibitem

- Nobel [2006] {barticle}[author] \bauthor\bsnmNobel, \bfnmA. B.\binitsA. B. (\byear2006). \btitleHypothesis Testing for Families of Ergodic Processes. \bjournalBernoulli \bvolume12 \bpages251–269. \endbibitem

- Pham and Tran [1985] {barticle}[author] \bauthor\bsnmPham, \bfnmTuan D.\binitsT. D. and \bauthor\bsnmTran, \bfnmLanh T.\binitsL. T. (\byear1985). \btitleSome Mixing Properties of Time Series Models. \bjournalStochastic processes and their applications \bvolume19 \bpages297–303. \endbibitem

- Schervish [1995] {bbook}[author] \bauthor\bsnmSchervish, \bfnmM. J.\binitsM. J. (\byear1995). \btitleTheory of Statistics. \bseriesSpringer Series in Statistics. \bpublisherSpringer Verlag, \baddressNew York. \endbibitem

- Silverman [1978] {barticle}[author] \bauthor\bsnmSilverman, \bfnmB. W.\binitsB. W. (\byear1978). \btitleWeak and Strong Uniform Consistency of the Kernel Estimate of a Density and its Derivatives. \bjournalThe Annals of Statistics \bvolume6 \bpages177–184. \endbibitem

- Steinwart and Anghel [2009] {barticle}[author] \bauthor\bsnmSteinwart, \bfnmI.\binitsI. and \bauthor\bsnmAnghel, \bfnmM.\binitsM. (\byear2009). \btitleConsistency of support vector machines for forecasting the evolution of an unknown ergodic dynamical system from observations with unknown noise. \bjournalThe Annals of Statistics \bvolume37 \bpages841–875. \endbibitem

- Tran [1989] {barticle}[author] \bauthor\bsnmTran, \bfnmL. T.\binitsL. T. (\byear1989). \btitleThe Convergence of Kernel Density Estimates under Dependence. \bjournalThe Canadian Journal of Statistics/La Revue Canadienne de Statistique \bvolume17 \bpages197–208. \endbibitem

- Tran [1994] {barticle}[author] \bauthor\bsnmTran, \bfnmL. T.\binitsL. T. (\byear1994). \btitleDensity estimation for time series by histograms. \bjournalJournal of statistical planning and inference \bvolume40 \bpages61–79. \endbibitem

- Vapnik [2000] {bbook}[author] \bauthor\bsnmVapnik, \bfnmV. N.\binitsV. N. (\byear2000). \btitleThe Nature of Statistical Learning Theory, \bedition2nd ed. \bpublisherSpringer Verlag, \baddressNew York. \endbibitem

- Vidyasagar [1997] {bbook}[author] \bauthor\bsnmVidyasagar, \bfnmM.\binitsM. (\byear1997). \btitleA Theory of Learning and Generalization: With Applications to Neural Networks and Control Systems. \bpublisherSpringer Verlag, \baddressBerlin. \endbibitem

- Volkonskii and Rozanov [1959] {barticle}[author] \bauthor\bsnmVolkonskii, \bfnmVA\binitsV. and \bauthor\bsnmRozanov, \bfnmY. A.\binitsY. A. (\byear1959). \btitleSome Limit Theorems for Random Functions. I. \bjournalTheory of Probability and its Applications \bvolume4 \bpages178–197. \endbibitem

- Weiss [1973] {barticle}[author] \bauthor\bsnmWeiss, \bfnmB.\binitsB. (\byear1973). \btitleSubshifts of finite type and sofic systems. \bjournalMonatshefte für Mathematik \bvolume77 \bpages462–474. \endbibitem

- Withers [1981] {barticle}[author] \bauthor\bsnmWithers, \bfnmC. S.\binitsC. S. (\byear1981). \btitleConditions for linear processes to be strong-mixing. \bjournalProbability Theory and Related Fields \bvolume57 \bpages477–480. \endbibitem

- Woodroofe [1967] {barticle}[author] \bauthor\bsnmWoodroofe, \bfnmM.\binitsM. (\byear1967). \btitleOn the Maximum Deviation of the Sample Density. \bjournalThe Annals of Mathematical Statistics \bvolume38 \bpages475–481. \endbibitem

- Yu [1993] {barticle}[author] \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear1993). \btitleDensity Estimation in the Norm for Dependent Data with Applications to the Gibbs Sampler. \bjournalAnnals of Statistics \bvolume21 \bpages711–735. \endbibitem

- Yu [1994] {barticle}[author] \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear1994). \btitleRates of Convergence for Empirical Processes of Stationary Mixing Sequences. \bjournalThe Annals of Probability \bvolume22 \bpages94–116. \endbibitem