A Stochastic Approximation for Fully Nonlinear Free Boundary Parabolic Problems

Abstract.

We present a stochastic numerical method for solving fully non-linear free boundary problems of parabolic type and provide a rate of convergence under reasonable conditions on the non-linearity.

Key words and phrases:

Free boundary problems, Monte-Carlo method, fully non-linear PDEs, viscosity solutions, rate of convergence1. Introduction

When the option pricing problem is of several dimensions, e.g. basket options, deterministic methods such as finite difference are almost intractable; because the complexity increases exponentially with the dimension and one almost inevitably needs to use Monte-Carlo simulations. Moreover, many problems in finance, e.g. pricing in incomplete markets and portfolio optimization, lead to fully non-linear PDEs. Only very recently has there been some significant development in numerically solving these non-linear PDEs using Monte Carlo methods, see e.g. [8], [25], [7], [22], [13] and [14]. When the control problem also contains a stopper, e.g. in determining the super hedging price of an American option, see [16], or solving controller-and-stopper games, see [5], the non-linear PDEs have free boundaries.

For solving linear PDEs with free boundaries, i.e. in the problem of American options, Longstaff-Shwartz [21], introduced a stochastic method in which American options are approximated by Bermudan options and least squares approximation is used for doing the backward induction. The major feature in [21] is the tractability of the implementation for the scheme proposed in terms of the CPU time in high dimensional problems. The most important feature of this model that facilitates the speed is that the number of paths simulated is fixed. Simulating the paths corresponds to introducing a stochastic mesh for the space dimension and the Bermudan approximation to American options corresponds to time discretization. Stochastic mesh makes sure that more important points in the state space are used in the computation of the value function, an important feature which increases the speed of convergence. So essentially, this algorithm can be thought of as an explicit finite difference scheme with stochastic mesh. One can in fact prove the convergence rate of the entire “stochastic” explicit finite difference scheme, see [9] for a survey of these results and some improvements to the original methodology of Longstaff-Shwartz.

For semi-linear free boundary problems a similar stochastic scheme is given through Reflected Backward Stochastic Differential Equations (RBSDE) in [22] and rate of convergence is derived to be assuming uniform ellipticity for the problem where the mesh size of the time discretizaton. Here the number of paths, , that one needs to simulate, increases with decreasing and needs to be chosen in a certain way, see e.g. (3.19). This is similar to what we have in classical explicit finite difference schemes. To achieve stability, when we decrease the mesh size for time, we need to decrease the mesh size for the space variable to keep the ratio of time step over space step squared in a certain range. As we discussed above, the Monte-Carlo simulation creates a stochastic mesh. The first result in this direction is due to [22]. Later [7] improved the result of [22] by removing the uniform ellipticity condition. Moreover, they improve the rate of convergence to by assuming more regularity on the obstacle function.

In this paper, we generalize the Longstaff-Schwartz methodology for numerically solving a large class of fully non-linear free boundary problems. We extend the idea in [13] to present a stochastic scheme for fully non-linear Cauchy problems with obstacle. As described in Remark 3.11, our scheme is stochastic, i.e. the outcome is a random variable which converges to the true solution pathwise. The convergence of our scheme follows from the methodology of [4], and the results of [13]. For the convenience of the reader, we sketch the convergence argument in Section 3.2. Under a concavity assumption on the non-linearity and regularity of the coefficients, we obtain a rate of convergence using Krylov’s method of shaking coefficients together with the switching system approximation as in [6], where a rate of approximation is obtained for classical finite difference schemes for elliptic problems with free boundaries. In [10], Cafaralli and Souganidis provide a rate of convergence without a concavity assumption on the non-linearity but they consider elliptic problems with non-linearity that depends only on the Hessian.

Appendix A is provided to establish the comparison, existence and regularity results for a parabolic switching system with free boundary which is needed to provide the estimations in the rate of convergence proof. This appendix generalizes the result of [15] for parabolic obstacle problems to parabolic switching systems with obstacle. Also, it can be considered as the parabolic version of [6] where they study elliptic switching systems with obstacle. Appendix B contains a proof of the technical Lemma 3.9.

The rest of the paper is organized as follows: In Section 2, we present the stochastic numerical scheme. In Section 3, we present the main results, the convergence rate, and its proof. Section 4 is devoted to some numerical results illustrating our theoretical findings. The appendix is devoted to the analysis of non-linear switching systems with obstacles, which is an essential ingredient in the proof of our main result and some technical proofs.

Notation. For scalars , we write , and . By , we denote the collection of all matrices with real entries. The collection of all symmetric matrices of size is denoted , and its subset of nonnegative symmetric matrices is denoted by . For a matrix , we denote by its transpose. For , we denote . In particular, for , and are vectors of and reduces to the Euclidean scalar product. For a suitably smooth function on , we define

| and |

Finally, by we mean the conditional expectation given for a pre-specified diffusion process .

2. Discretization

We consider the obstacle problem

| (2.1) | |||

| (2.2) |

where

and

is a non–linear map, and are maps from to and , respectively, , . We consider an -valued Brownian motion on a filtered probability space , where the filtration satisfies the usual conditions, and is trivial. For a positive integer , let , , , and consider the one step Euler discretization

| (2.3) |

of the diffusion corresponding to the linear operator . Then the Euler discretization of the process is defined by:

We suggest the following approximation of the value function

| and | (2.4) |

where for a given test function we denote

| (2.5) |

| (2.6) |

where and

provided is invertible. Notice that (2.6) comes from

| (2.7) |

where is a standard Gaussian random variable. The details can be found in Lemma 2.1 of [13].

3. Asymptotics of the discrete-time approximation

In this section, we present the convergence and the rate of convergence result for the scheme introduced in (2.4), and the assumptions needed for these results.

3.1. The main results

The proof of the convergence follows the general methodology of Barles and Souganidis [4], and requires that the nonlinear PDE (2.1) satisfies the comparison principle in viscosity sense.

We recall that an upper-semicontinuous (resp. lower-semicontinuous) function (resp. ) on , is called a viscosity subsolution (resp. supersolution) of (2.1) if for any and any smooth function satisfying

we have:

-

•

if

-

•

if , (resp. ).

Remark 3.1.

Note that the above definition is not symmetric for sub and supersolutions. More precisely, for a subsolution we need to have either

However, for a supersolutions we need to have both

Definition 3.2.

We say that (2.1) has comparison for bounded functions if for any bounded upper semicontinuous subsolution and any bounded lower semicontinuous supersolution on , satisfying , we have .

We denote by , and the partial gradients of with respect to , and , respectively. We also denote by the pseudo-inverse of the non-negative symmetric matrix .

Assumption F

(i) The nonlinearity is Lipschitz-continuous with respect to uniformly in , and for some positive constant ;

(ii) is invertible and .

(iii)

is elliptic and dominated by the diffusion of the linear operator , i.e.

| on | (3.1) |

(iv) and ;

(v)

.

Remark 3.3.

Assumption F(v) is made for the sake of simplicity of the presentation. It implies the monotonicity of the above scheme. If this assumption is not made, one can carry out the analysis in [13, Remark 3.13, Theorem 3.12, and Lemma 3.19] and approximate the solution of the non-monotone scheme with the solution of an appropriate monotone scheme.

Theorem 3.4 (Convergence).

Suppose that Assumption F holds. Also, assume that the fully nonlinear PDE (2.1) has comparison for bounded functions. Then for every bounded function Lipschitz on and Hölder on , there exists a bounded function such that locally uniformly. Moreover, is the unique bounded viscosity solution of problem (2.1)-(2.2).

By imposing the following stronger assumption, we are able to derive a rate of convergence for the fully non–linear PDE.

Assumption HJB The nonlinearity satisfies Assumption F(ii)-(v), and is of the Hamilton-Jacobi-Bellman type:

where functions , , and satisfy:

Assumption HJB+ The nonlinearity satisfies HJB, and for any , there exists a finite set such that for any

Remark 3.5.

Assumption HJB+ is satisfied if is a compact separable topological space and , , and are continuous maps from to , the space of bounded maps which are Lipschitz in and –Hölder in .

Theorem 3.6 (Rate of Convergence).

Assume that the boundary condition is bounded Lipschitz on and Hölder on . Then, there is a constant such that:

-

(i)

under Assumption HJB, we have ,

-

(ii)

under the stronger condition HJB+, we also have .

It is worth mentioning that in the finite difference literature, the rate of convergence is usually stated in terms of the discretization in the space variable, i.e. , and the time step, i.e. equals . In our context, the stochastic numerical scheme (2.4) is only discretized in time with time step . Therefore, the rates of convergence in Theorem 3.6 corresponds to the rates and , respectively.

3.2. Proof of the convergence result

The proof Theorem 3.4, similar to the proof of Theorem 3.6 of [13], is based on the result of [4] which requires the scheme to be consistent, monotone and stable. To be consistence with the notation in [4], we define

and then write the scheme (2.4) as =0. Notice that by the discussions in [24] and in Section 3 of [23], the consistency and monotonicity for the scheme (2.4) for obstacle problem follows from the consistency and monotonicity of the scheme without obstacle provided by Lemmas 3.11 and 3.12 of [13]. More precisely, we have

-

(i)

Consistency. Let be a smooth function with bounded derivatives. Then for all :

(3.5) -

(ii)

Monotonicity. Let be two bounded functions. Then:

(3.6)

On the other hand, one can show the stability of the scheme (2.4) in the following Lemma. Throughout this section, Assumption of the Theorem 3.4 are enforced.

Lemma 3.7.

The family defined by (2.4) is bounded, uniformly in .

Proof. Let . By the argument in the proof of Lemma 3.14 in [13], where depends only on constant in assumption F. Therefore,

Using a backward induction one could obtain that for some constant independent of .

The monotonicity, consistency and stability of the scheme result to the following Lemma.

Lemma 3.8.

Observe that thanks to Lemma 3.7, and are well-defined and bounded functions and we readily have . Moreover, functions and are respectively lower semicontinuous and upper semicontinuous. Therefore by the comparison principle for (2.1)-(2.2) and Lemma 3.8, it follows that and the function is a viscosity solution of (2.1)-(2.2) which completes the proof of Theorem 3.4. In addition, uniqueness in the class of bounded functions is a consequence of comparison principle for the problem.

Proof of Lemma 3.8.

We show that and are subsolution and super solution at any arbitrary point . We split the proof into the following steps.

Step 1 (). In this case, we only establish the supersolution property of . The subsolution property of follows from the same line of arguments. Let be a smooth function such that

Since function is bounded, by modifying outside a neighborhood of , one can assume that the is a global strict minimum point. Notice that only the local property of the function matters in the definition of viscosity solution.

Therefore, there exists a sequence , such that , , , and is a global minimum of . (Obtainig this sequesnce is a standard technique in viscosity solution literature. For more details see [4] and the references therein.)

Therefore, . By the monotonicity of the scheme, (3.6), we have

Therefore, by the definition of in (2.4),

We divide both sides by . Letting and using (3.5) we obtain:

Step 2 (Supersolution property when ). Observe that since , we have

which completes the proof of the supersolution argument at terminal time.

Step 3 (Subsolution property when ).

Observe that by the definition of and , we readily have . To complete the subsolution argument, we have to show that . It is sufficient to show that

Lemma 3.9.

For all and , we have

3.3. Derivation of the rate of convergence

The proof of Theorem 3.6 is based on Barles and Jakobsen [3], which uses switching systems approximation and the Krylov method of shaking coefficients [17], [18], [19], and [20]. This has been adapted to classical finite difference schemes for elliptic obstacle (free boundary) problems in [6]. In order to use the method, we need to introduce a comparison principle for the scheme which we will undertake next.

Proposition 3.10.

Let Assumption hold and set . Consider two arbitrary bounded functions and satisfying:

| and | (3.7) |

for some bounded functions and . Then, for every :

| (3.8) |

Proof. This follows from Lemma 2.4 of [15] where it is provided for general monotone schemes for obstacle problems.

3.3.1. Proof of Theorem 3.6 (i)

Under Assumption HJB, we can build a bounded subsolution of the nonlinear PDE, by the method of shaking coefficients, see [3], [6], [20], and the references therein. More precisely, consider the following equations

| (3.9) | |||||

| (3.10) |

By Theorem A.6, there exists a unique bounded solution to (3.9)-(3.10).

Because , is a subsolution to (2.1)-(2.2) at all and by Theorem A.4 (continuous dependence for HJB equations), approximates uniformly, i.e., there exists a positive constant such that

Let be a non-negative function supported in with unit mass, and define

| where | (3.11) |

It follows that . From the concavity of the the nonlinearity , and Lemma A.3 in [1], , is a classical subsolution of (2.1) on . 111This heuristically follows from . Moreover, by Theorem A.7, is Lipschitz in and Hölder continuous in . Thus, by Theorem 2.1 in [19],

| for any | (3.12) |

where , and is some constant. As a consequence of the consistency of , see Lemma 3.22 of [13], we know that

From this estimate together with the subsolution property of , we see that holds true on . In addition, by the regularity properties of , one can see that on . Therefore,

Then, it follows from Proposition 3.10 that

| (3.13) |

Therefore, . Minimizing the right hand-side estimate over , we obtain .

3.3.2. Proof of Theorem 3.6 (ii)

To prove the lower bound on the rate of convergence, we will use Assumption HJB+ and build a switching system approximation to the solution of the nonlinear obstacle problem (2.1)-(2.2). This proof method has been used for Cauchy problems of [3] and [13]. For obstacle problems, this method is used in the elliptic case by [6] for the classical finite difference schemes. We apply this methodology for parabolic obstacle problems to prove the lower bound for the convergence rate of our stochastic finite difference scheme. We split the proof into the following steps:

- (1)

- (2)

-

(3)

Using Proposition 3.10, the comparison principle for the scheme, to bound the difference of the supersolution obtained in Step 2 and the approximate solution obtained from the scheme.

Step 1. Consider the following switching system:

| (3.14) | ||||

| (3.15) |

where , , is a non-negative constant, ’s, for , are as in assumption HJB+, and .

The above system of equations approximates (2.1)-(2.2). Intuitively speaking, Assumption HJB+ introduces a set of approximating controls in . In the corresponding optimization problem, the maximum cost of restricting controls to the set is proportional to . In addition, the above switching system imposes a switching cost of between controls in the finite set . If goes to zero, then all functions in the solution of problem (3.14)-(3.15) converges to the function , the solution of the problem without switching cost, i.e. (3.9)-(3.10). On the other hand, we have already seen that approximates function , the solution of (2.1)-(2.2).

More rigorously, by Theorem A.6 the viscosity solution to (3.14)-(3.15) exists and by Theorem A.7 is Lipschitz continuous on and -Hölder continuous on . Moreover, by using Assumption HJB+, Theorem A.4 and Remark A.2, one can approximate the solution to (2.1)-(2.2) by the solution to (3.14)-(3.15), see Theorem 3.4 in [6] and the proof of Theorem 2.3 of [3] for more details. More precisely by setting , there exists a positive constant such that

Step 2. Let , where is as in (3.11). As in Lemma 4.2 of [6] and Lemma 3.4 of [3] for , for , the function is a supersolution to

| (3.16) |

Moreover, for any , we have . Therefore, for all we have

Choosing with , one can write

| (3.17) |

Step 3. By the definition of , for any and we have and elsewhere. Therefore, . Moreover, since (3.12) is satisfied by , by Lemma 3.22 of [13], one can conclude that

Therefore due to (3.16), holds true. By Proposition 3.10, one can get

| (3.18) |

By minimizing on , the desired lower bound is obtained.

Remark 3.11 (Stochastic scheme).

Scheme (2.4) produces a deterministic approximate solution. However, in practice, we approximate the expectations in (2.5) based on a randomly generated set of sample paths of the process . As a result, the approximate solution is not deterministic anymore. By following the line of argument in Section 4 of [13], one can show the almost sure convergence of this stochastic approximate solution and even provide the same rate of convergence in .

More precisely, assume that is approximated by where denotes the number of sample paths. Suppose that for some , there exist constants such that for a suitable class of random variables bounded by . By replacing with in the scheme (2.4), one obtains a stochastic approximate solution . Then, if we choose which is chosen to satisfy , then under assumptions of Theorem 3.4

| locally uniformly, |

for almost every where is the unique viscosity solution of (2.1)-(2.2). In addition, if

| (3.19) |

we have that under the assumptions of Theorem 3.6.

4. Numerical results

4.1. Risk neutral pricing of geometric American put option

We consider a geometric American put option on three risky assets each of which follows a Black-Scholes dynamics under risk neutral probability measure. The payoff of the option is given by where and are respectively the strike price and maturity and where

Here is the vector of asset prices, is a 3-dimensional Brownian motion, is the risk free interest rate, and where is the volatility of the th asset.

The price of this option at time and for asset price vector is given by

| (4.1) |

where the supremum is over all stopping times adapted to the filtration generated by the 3-dimensional Brownian motion and is the risk neutral expectation. It is well-known that function satisfies the following differential equation

where . We treat this linear equation as a fully nonlinear one by separating the linear second order operator into two parts. More precisely, for some , we choose the linear and nonlinear parts to be and , respectively. This leads to the choice of diffusion

for the approximation scheme (2.4). On the other hand the approximation of the second order derivatives in (2.6) is given by

where . For the numerical implementation we choose the continuous-time interest rate , volatility of all assets , , , and we evaluate the option at time at .

| Time | |||

|---|---|---|---|

| 5 | 92 | .301173 | .326258 |

| 10 | 234 | .309001 | .334205 |

| 15 | 360 | .312642 | .337974 |

| 20 | 499 | .314978 | .340397 |

| 40 | 1050 | .320354 | .347909 |

| 50 | 1325 | .322115 | .346041 |

The reference value for option price is obtained by applying the binomial tree algorithm to the 1-dimensional optimal stopping problem

on the diffusion satisfying

where is a 1-dimensional Brownian motion. The binomial tree algorithm stabilizes to the value for more than 20000 time steps.

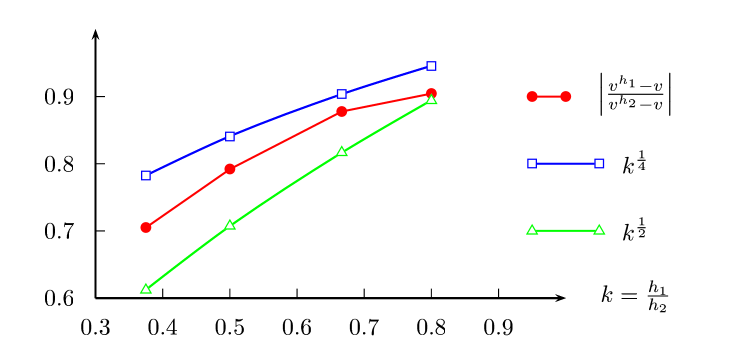

The numerical result as well as the run time of the algorithm 222 Dual core i5 2.5 GHz, 4 GB of RAM is provided in Table 1 for two different choices for . Here we used projection method described in [9] with locally linear basis functions with compact support. Notice that corresponds to the Longstaff-Schwartz algorithm and for , the inequality (3.1) is satisfied. In Figure 1 the red graph is the ratio of error for two consecutive time steps plotted against the ratio of the time steps, while the green graph is the theoretical rate of convergence; i.e. . Because of the analysis in [13, Section 3.4], one expects to have a higher the rate of convergence for the scheme on the linear equations. Therefore, the simulated red plot must lie below the theoretical green plot. On the other hand, due to error of approximation of expectations in the scheme, the rate of convergence will never be obtained in practice.

4.2. Indifference pricing of geometric American put option

We consider a geometric put option on two non-tradable risky assets with Black-Scholes dynamics given by

where is a 2-dimensional Brownian motion, and and are the drift and the volatility of the th asset for , respectively. We assume that there is a portfolio made of a tradable asset with Black-Scholes dynamics and money market with interest rate which satisfies

where is the amount of money in risky asset, is a one dimensional Brownian motion, and and are drift and volatility of the tradable asset, respectively. Here we assume that for . The indifference pricing with exponential utility leads to the controller-stopper problem below

| (4.2) |

which satisfies the fully nonlinear obstacle problem below:

where is a constant and , is the strike price and . To solve the above free boundary problem using scheme (2.4), we choose the linear and nonlinear parts as follow:

| Time | ||||

|---|---|---|---|---|

| 5 | 2 | 34 | -.341675 | -.349489 |

| 10 | 1 | 36 | -.303425 | -.352110 |

| 2 | 76 | -.356332 | -.351678 | |

| 20 | 2 | 180 | -.356126 | -.351659 |

| 3 | 273 | -.351659 | -.356126 | |

| 4 | 372 | -.348773 | -.350201 | |

| 30 | 3 | 422 | -.353311 | -.353088 |

| 40 | 4 | 696 | -.322095 | -.361026 |

Thus, the appropriate diffusion to be used inside (2.4) is

where , , and is a one dimensional Brownian motion independent of .

To find a reference value for the solution, we follow the same idea as in Section 4.1. Since satisfies

we have where the function is the solution of the 2-dimensional controller-stopper problem

| (4.3) |

Neither function nor have closed form solutions, but

we expect that if the scheme converges numerically, it approximates the function more accurately because of the reduction in the dimension. This is because the number of sample paths and time steps for a 2-dimensional problem for can be chosen larger than the 3-dimensional problem for . Therefore, to examine the convergence of scheme, we compare the approximation of these functions by the scheme (2.4).

We set , , , , , , , and for .

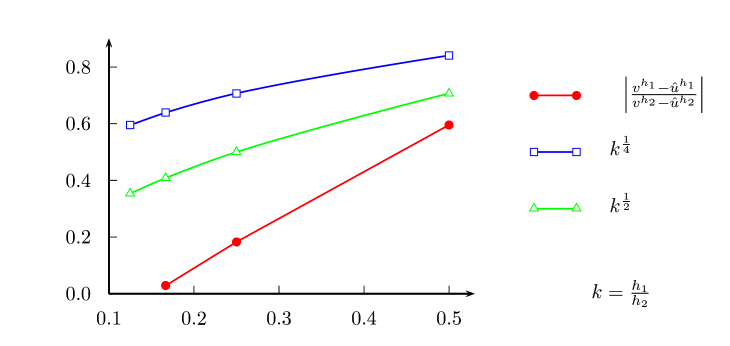

The result of the simulation is summarized in Table 2. In Figure 2, we establish the convergence analysis for the non-linear problem by using the approximations in Table 2 with the largest number of sample paths for each time step.

A. Appendix: A switching system with an obstacle

In this section, we will provide some results needed in the Section 3.3. In particular, we present a continuous dependence result for the switching system with obstacle and as a corollary a comparison result, which provides the uniqueness of the solution. Then, the existence and regularity of the solutions to the switching systems are provided.

Consider the following system of PDEs for :

| (A.1) |

We also need to consider a variant of equation (A.1) as follows:

| (A.2) |

Assumption HJB-S. We assume that in (A.1) and (A.2)

| (A.3) |

, is a non-negative constant, and

Moreover,

and for all , we have .

Remark A.1.

Remark A.2.

For the sake of simplicity in Assumption HJB-S, we only included the nonlinearities of infimum type. However, all the results of this appendix still hold if we assume that

| (A.4) |

and for all and , we have . This remark is also valid if we change the order of and in (A.4).

Lemma A.3.

Let and be respectively the upper semicontinuous subsolution and the lower semicontinuous supersolution of (A.1) and (A.2), and assume that is a smooth function bounded from below. Define

Suppose that there exists an such that and . Then, there exists an such that and

| (A.6) |

Moreover, if in a neighborhood of there are some continuous functions , and such that

then there are and such that

| (A.8) | |||||

| (A.15) |

| (A.16) | ||||

| (A.17) |

Proof. The first part of the proof is similar to those of Lemma A.2 of [2], Lemma A.1 of [6]. The second part follows as a result of Theorem 2.2 of [11].

The following theorem on continuous dependence is used in Section 3.3.2 and in the regularity result, Theorem A.7 below.

Intuitively speaking, continuous dependence result asserts that a slight change in the coefficients of (A.1) changes the solution only slightly.

Theorem A.4 (Continuous dependence).

Proof. Let and define

where are arbitrary constants and constants will be determined later in the proof. We will show that is bounded by a constant which is bounded by mentioned in the theorem as and is set appropriately. Then, it would follow that

Sending , one would then obtain

Note that the above inequality is also valid for by considering as the time interval and by changing to .

Define

where with . Let

| (A.18) |

Since and are bounded, we have . On the other hand, by semicontinuity of and , one can conclude that the supremum in the definition of is attained at some point . In other words, (see Lemma A.3 for the definition of ).

If , then Since

one can conclude that . Therefore, we may assume that . From the definition of , we have . On the other hand, implies . Because if , then which implies

which is a contradiction. So, we have . We continue the proof by considering two different cases.

Case 1: . The supremum in (A.18) is attained at some point with and . Therefore,

On the other hand, since , we have .

Case 2: . In this case, (A.6) is satisfied and by Lemma A.3 and the same line of argument as Theorem A.1 in [15] the result is provided. For the convenience of the reader, we present a sketch of the proof.

By subtracting (A.17) from (A.16), we have

Now, using and together with (A.8)-(A.15), one can obtain the following bound for

where is the constant depending only on in Assumption HJB-S. After we choose in the above and maximize the right hand side with respect to , the proof is complete.

The following result is a straightforward consequence of Theorem A.4, and will be used to establish the existence and the regularity of the solution to (A.1).

Corollary A.5.

Assume that HJB-S holds. Suppose that and are respectively a bounded upper semicontinuous subsolution and a bounded lower semicontinuous supersolution of (A.1). Then, for any , .

Theorem A.6 (Existence).

Assume that HJB-S holds. Then there exists a unique continuous viscosity solution in the class of bounded functions to (A.1).

Proof. We follow Perron’s method (see e.g. Section 4 of [11]). Observe that by Assumption HJB-S, and are respectively sub and supersolutions of (A.1) for a suitable choice of positive constant . Define and

and

It is straight forward that . We want to show that and are respectively a sub and a supersolution to (A.1) which by comparison, Corollary A.5, yields the desired result.

Step 1: Subsolution property of . We start by showing that with

is a supersolution to(A.1) for a suitable positive constant . Observe that since

we have that , and in particular . On the other hand, by simple calculations, one can show that, for an appropriate choice of , we have .

Therefore, by comparison, Corollary A.5, for any subsolution , which implies ; specially . Sending and setting , .

Now, for fixed , we suppose and is a test function such that

It follows from the definition of that there exists a sequence with such that is a subsolution to (A.1), , , and is the global strict maximum of . Let . By the subsolution property of , we have

Because , by sending ,

Step 2: Supersolution property of . Since is a subsolution to (A.1), . In particular, . Therefore, we only need to show that

| (A.19) |

on in the viscosity sense. We will prove (A.19) by a contradiction argument. Assume that there are a test function and with such that is the global strict minimum of and but . Then, by continuity of and the equation and lower semicontinuity of , one can find and small enough, such that for we have that and that

| (A.20) |

Define

Since is a subsolution to (A.1) and by (A.20), one can show that is a subsolution to (A.1). By the definition of , we must have , which contradicts the fact that for .

Theorem A.7 (Regularity).

Assume that HJB-S holds. Let be the solution to (A.1). Then, is Lipschitz continuous with respect to and -Hölder continuous with respect to on .

Proof. Lipschitz continuity with respect to : For fixed , is the solution of a switching system obtained from (A.1) by replacing with

with the terminal condition given by . By Theorem A.4, there is a positive constant such that

-Hölder continuity with respect to : For , define to be the solution to

Since is a subsolution of (A.1) on with terminal condition , by comparison result, Corollary A.5, we have . Therefore, . By Theorem A.1 of [3], is -Hölder continuous in which provides

Now, for fixed , define

where , and are positive constants which will be given later and is the same as in Assumption HJB-S. We will show that for an appropriate choice of and , is a supersolution of (A.1) with terminal condition . Then, comparison, Corollary A.5, would then imply that . Therefore,

By setting , we have , where is a positive constant.

Therefore, it remains to show that for and large enough, we have

on . Since , one needs to show that

| and |

Observe that if , by the regularity assumption on , we have

On the other hand,

By choosing and large enough, the right hand side in the above inequality is positive which completes the argument.

B. Appendix: Proof of Lemma 3.9

If holds true, then since function is -Hölder continuous on , the proof is done. So, we assume that

. We introduce the discrete stopping time . Observe that .

Step 1. Let be such that

For all , on the event one can write

where , , , and and are -measurable. We can rewrite the above equality in the following form.

| (B.1) |

Notice that the first term in the right hand side of (B.1) is zero if . We define with and . Observe that is a discrete martingale with respect to . Multiplying (B.1) by , one can write

By summing the above equality over and taking expectation , we have

Observe that here we used by the definition of . Thus, we can write

| (B.2) |

where in the above we used optional stopping theorem for . Our goal is to show that the right hand side of (B.2) is bounded by . First observe that by Assumption F(i), is bounded. Then, because is a positive martingale, we can bounded the second term in (B.2) by :

We continue by bounding the other term in (B.2) in the next step.

Step 2. To bound , we want to apply Itô formula on . But, because is not a function, we first approximate by a smooth function uniformly, i.e . This can be done by where is a family of mollifiers. Because is Lipschitz on and -Hölder on , we have

| (B.3) |

Therefore, we write

Observe that since , one has

| (B.4) |

In the following steps, we find a bound on in terms of and .

Step 3. We apply Itô formula on :

where is the infinitesimal generator for the processe . Thus,

| (B.5) |

We proceed by calculating the term in the above summation for .

| (B.6) |

We first bound the second term in the right hand side in the next step.

Step 4. Since and are measurable, the second term in the right hand side can be written as

where . Notice that we can write . Thus, one can calculate using Itô isometry and the fact that the expected value of stochastic integrals is zero:

Because of (B.4), the first two term in the above are bounded by . The third term can be calculated by using (2.6)

By (2.7), we have which is bounded by . Thus,

Therefore,

Step 5. Because is a martingale and is -measurable, one can write the first term in the right hand side of (B.6) as

Thus, from (B.5) we have

By repeating the argument in Step 3 and Step 4 inductively over , one can write the above as

Specially for (the term containing disappears), we have

Step 6. By using (B.4) and the bound found in Step 5 in (B.2), one has

By choosing , we conclude that

Then, the result follows from -Lipschitz continuity and --Hölder continuity of .

Acknowledgment. The authors are grateful to Xavier Warin and anonymous referees for their helpful comments and suggestions.

References

- [1] G. Barles and E. R. Jakobsen. On the convergence rate of approximation schemes for Hamilton-Jacobi-Bellman equations. M2AN Math. Model. Numer. Anal., 36(1):33–54, 2002.

- [2] G. Barles and E. R. Jakobsen. Error bounds for monotone approximation schemes for Hamilton-Jacobi-Bellman equations. SIAM J. Numer. Anal., 43(2):540–558 (electronic), 2005.

- [3] G. Barles and E. R. Jakobsen. Error bounds for monotone approximation schemes for parabolic Hamilton-Jacobi-Bellman equations. Math. Comp., 76(260):1861–1893 (electronic), 2007.

- [4] G. Barles and P. E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal., 4(3):271–283, 1991.

- [5] Erhan Bayraktar and Yu-Jui Huang. On the Multidimensional Controller-and-Stopper Games. SIAM J. Control Optim., 51(2):1263–1297, 2013.

- [6] J. F. Bonnans, S. Maroso, and H. Zidani. Error estimates for stochastic differential games: the adverse stopping case. IMA J. Numer. Anal., 26(1):188–212, 2006.

- [7] B. Bouchard and J.-F. Chassagneux. Discrete-time approximation for continuously and discretely reflected BSDEs. Stochastic Process. Appl., 118(12):2269–2293, 2008.

- [8] B. Bouchard and N. Touzi. Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Process. Appl., 111(2):175–206, 2004.

- [9] B. Bouchard and X. Warin. Monte-Carlo valorisation of American options: facts and new algorithms to improve existing methods. To appear in Numerical Methods in Finance , Springer Proceedings in Mathematics, ed. R. Carmona, P. Del Moral, P. Hu and N. Oudjane, 2011.

- [10] Luis A Caffarelli and Panagiotis E Souganidis. A rate of convergence for monotone finite difference approximations to fully nonlinear, uniformly elliptic pdes. Communications on Pure and Applied Mathematics, 61(1):1–17, 2008.

- [11] M. G. Crandall, H. Ishii, and P.-L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc. (N.S.), 27(1):1–67, 1992.

- [12] A. Fahim. Convergence of a Monte Carlo method for fully non-linear elliptic and parabolic PDEs in some general domains. Preprint, Sep 2011.

- [13] A. Fahim, N. Touzi, and X. Warin. A probabilistic numerical method for fully non–linear parabolic pdes. Annals of Applied Probability, 21(4):1322–1364, 2011.

- [14] Wenjie Guo, Jianfeng Zhang, and Jia Zhuo. A monotone scheme for high dimensional fully nonlinear pdes. arXiv preprint arXiv:1212.0466, 2012.

- [15] E. R. Jakobsen. On the rate of convergence of approximation schemes for Bellman equations associated with optimal stopping time problems. Math. Models Methods Appl. Sci., 13(5):613–644, 2003.

- [16] I. Karatzas and S. G. Kou. Hedging American contingent claims with constrained portfolios. Finance Stoch., 2(3):215–258, 1998.

- [17] N. V. Krylov. On the rate of convergence of finite-difference approximations for Bellman’s equations. Algebra i Analiz, 9(3):245–256, 1997.

- [18] N. V. Krylov. Approximating value functions for controlled degenerate diffusion processes by using piece-wise constant policies. Electron. J. Probab., 4:no. 2, 19 pp. (electronic), 1999.

- [19] N. V. Krylov. On the rate of convergence of finite-difference approximations for Bellman’s equations with variable coefficients. Probab. Theory Related Fields, 117(1):1–16, 2000.

- [20] N. V. Krylov. The rate of convergence of finite-difference approximations for Bellman equations with Lipschitz coefficients. Appl. Math. Optim., 52(3):365–399, 2005.

- [21] F.A. Longstaff and E. S. Schwartz. Valuing American options by simulation: a simple least-squares approach. Review of Financial Studies, 14(1):113–147, 2001.

- [22] J. Ma and J. Zhang. Representations and regularities for solutions to BSDEs with reflections. Stochastic Process. Appl., 115(4):539–569, 2005.

- [23] A. M. Oberman. Convergent difference schemes for degenerate elliptic and parabolic equations: Hamilton-Jacobi equations and free boundary problems. SIAM J. Numer. Anal., 44(2):879–895 (electronic), 2006.

- [24] A. M. Oberman and T. Zariphopoulou. Pricing early exercise contracts in incomplete markets. Computational Management Science, 1(1):75–107, 2003.

- [25] J. Zhang. A numerical scheme for BSDEs. Ann. Appl. Probab., 14(1):459–488, 2004.