A new estimator for the tail-dependence coefficient

Marta Ferreira

Department of Mathematics, University of Minho, Portugal

msferreira@math.uminho.pt

Abstract

Recently, the concept of tail dependence has been discussed in financial applications related to market or credit risk. The multivariate extreme value theory is a proper tool to measure and model dependence, for example, of large loss events. A common measure of tail dependence is given by the so-called tail-dependence coefficient. We present a simple estimator of this latter that avoids the drawbacks of the estimation procedure that has been used so far. We prove strong consistency and asymptotic normality and analyze the finite sample behavior through simulation. We illustrate with an application to financial data.

Keywords: extreme value theory, tail-dependence coefficient, stable

tail dependence function

1 Introduction

Modern risk management is highly interested in assessing the amount

of extremal dependence, a growing phenomena in recent time periods

of volatile and bear markets. Correlation itself is not enough to

describe a tail dependence structure and often results in misleading

interpretations (see e.g. Embrechts et al. [3],

2002 for examples).

Multivariate Extreme value theory (EVT) is the natural tool to deal with tail dependence. The so-called tail-dependence coefficient (TDC) has become a popular measure in risk management. It is usually denoted and measures the probability of occurring extreme values for one random variable (r.v.) given that another assumes an extreme value too. More precisely,

| (1) |

where and are the distribution functions (d.f.’s) of

r.v.’s and , respectively. The TDC characterizes the

dependence in the tail of a random pair , in the sense that,

corresponds to tail dependence whose degree is measured

by the value of , and means tail independence.

Due to the emergent importance of this issue, it is not surprising

that the implementation of tail dependence measures and respective

estimation have attracted the attention of investigators. Sibuya

([17], 1960), Tiago de Oliveira ([18], 1962-63),

Ledford and Tawn ([13, 14], 1996, 1997), Joe

([10], 1997), Coles et al. ([2], 1999),

Embrechts et al. ([4], 2003), Frahm et al.

([8], 2005), Schmidt and Stadtmüller

([16], 2006), Ferreira and Ferreira ([6],

2011), are some references on this topic. Curiously, the first tail

dependence concept appearing in literature concerns the TDC, as far

back in the sixties with Sibuya ([17], 1960). More precisely,

for Normal distributed random pairs, Sibuya ([17], 1960) shows

that no matter how high we choose the correlation, if we go far

enough into the tail, extreme

events appear to occur independently in each margin.

Here we shall present an estimator for the TDC based on a new procedure that avoids the main drawback of existing ones. Strong consistency and asymptotic normality are stated and the finite sample behavior is illustrated through simulation. An application to financial data is presented at the end.

2 EVT and tail dependence

The main objective of an extreme value analysis is to estimate the probability of events that are more extreme than any that have already been observed. The tools within EVT, in particular the use of extremal models, enables extrapolations of this type. The central result in univariate Extreme Value Theory (EVT) states that, for an i.i.d. sequence, , having common distribution function (d.f.) , if there are real constants and such that,

| (2) |

for some non degenerate function , then it must be a Generalized Extreme Value function (GEV),

(for , ) and we say that belongs to the max-domain of attraction of , in short, . The parameter , known as the tail index, is a shape parameter as it determines the tail behavior of , being so a crucial issue in EVT. More precisely, if we are in the domain of attraction Fréchet corresponding to a heavy tail, indicates the Weibull domain of attraction of light tails and means a Gumbel domain of attraction and an exponential tail.

Models for dependent or non-identical distributed r.v.’s have also

been developed (see, for instance, Leadbetter [12] 1983 and

Mejzler [15] 1956, respectively).

In a multivariate framework, an extension of the univariate limiting result in (2) is considered and the multivariate maximum corresponds to the vector of component-wise maxima. Let be an i.i.d. sequence of -dimensional random vectors with common d.f. . If there are real vectors of constants and positive such that,

| (3) |

for some non degenerate function , then it must be a multivariate extreme value distribution (MEV), given by

for some -variate function , where , , is the marginal d.f. of . We also say that belongs to the max-domain of attraction of , in short, . The function in (2) is called stable tail dependence function.

Let be the marginal d.f. of . Since a sequence of random vectors can only converge in distribution if the corresponding marginal sequences do, we have, for ,

Hence is a GEV and is in its domain of attraction.

In order to study the dependence structure of a MEV, it is convenient to standardize the margins so that they are all the same. A particular useful choice is the unit Fréchet, (observe that unit Fréchet marginals can be obtained by transformation for ), and the stable tail dependence function in (2) becomes

| (4) |

Thus satisfies an important homogeneity property (of order ) and hence, it is easy to establish that, except for the special case of independence, all bivariate extreme value distributions(BEV) are tail dependent (). Furthermore, we have

| (5) |

Examples of parametric BEV models

-

•

Logistic: , with and parameter ; complete dependence is obtained in the limit as and independence when .

-

•

Asymmetric Logistic: , with and parameters and , j=1,2; when the asymmetric logistic model is equivalent to the logistic model; independence is obtained when either , or . Complete dependence is obtained in the limit when and approaches zero.

-

•

Hüsler-Reiss: , with parameter and where is the standard normal d.f.; complete dependence is obtained as and independence as .

3 Estimation

The -variate stable tail dependence function in (4) can also be formulated as

| (6) |

since, by applying the unit Fréchet marginals, we have successively,

| (13) |

Therefore, based on (5) and (13), the TDC in (1) can be stated like follows:

| (14) |

Huang (1992 [9]), considered the estimator based on (14) by plugging-in the respective empirical counterparts,

| (15) |

where is the empirical d.f. of , . Concerning estimation accuracy, some modifications of this latter may be used, like replacing the denominator by , i.e., considering

(for a discussion on this topic see, for instance, Beirlant et al. [1] 2004). The consistency and asymptotic normality of estimator is derived under the condition that is an intermediate sequence, i.e., and , as . The choose of the value in the sequence that allows the better trade-off between bias and variance is of major difficulty, since small values of come along with a large variance whenever an increasing results in a strong bias. Therefore, simulation studies have been carried out in order to find the best value of that allows this compromise. The other estimators, either for the stable tail dependence function or for the TDC, that have been considered in literature (for a survey, see for instance, respectively, Krajina [11] 2010 and Frahm et al. [8] 2005) are also based on asymptotic results with the same drawback of including an intermediate sequence, already referred above.

The approach that is presented here avoid this problem. It is based on an estimation procedure for the stable tail dependence function only involving a sample mean. More precisely, by Proposition 3.1 in Ferreira and Ferreira ([7], 2011), we have that

| (16) |

Therefore, based on (5) and (16) we propose estimator

| (17) |

where is the sample mean of , i.e.,

| (19) |

Proposition 3.1.

Estimator in (17) is asymptotically normal whenever has continuous marginals and continuous partial derivatives. Moreover it is strong consistent.

Dem. By Fermanian et al. ([5], 2002, Theorem 6), we have that

in distribution in , where the limiting process and are centered Gaussian, and , . The asymptotic normality is now derived from a general version of the Delta Method as considered in Schmidt and Stadtmüller [16] (2006; Theorem 13).

The strong consistency is straightforward from Proposition 3.7 in

Ferreira and Ferreira ([7], 2011).

Remark 3.1.

Observe that, if the marginals , , in (17) are known, the asymptotic normality of is straightforward by the Central Limit Theorem and the usual Delta Method. More precisely,

| (20) |

where

| (22) |

Details of the calculations can be seen in Proposition 3.3 of Ferreira and Ferreira ([7], 2011). The strong consistency is also immediately derived from the sample mean.

3.1 Simulations

We consider independent copies of i.i.d. pseudo-random vectors generated from three different BEV models considered in Section 2: logistic, asymmetric logistic and Hüsler-Reiss. We estimate the TDC through our estimator (). For comparison, we also compute estimator and, the required choice of to balance the variance-bias problem is based on the procedure in Schmidt and Stadtmüller ([16], 2006). The empirical bias and the root mean-squared error (rmse) for all implemented TDC estimations are derived and presented in Table 1. Our estimator clearly outperforms estimator .

| Logistic () | ||

|---|---|---|

| bias (rmse) | bias (rmse) | |

| (n=50) | 0.0019 (0.0994) | 0.0395 (0.1962) |

| (n=100) | 0.0052 (0.0711) | 0.0389 (0.1412) |

| (n=500) | 0.0006 (0.0330) | 0.0216 (0.0883) |

| (n=1000) | 0.0002 (0.0232) | 0.0099 (0.1379) |

| Asym. Logistic () | ||

| bias (rmse) | bias (rmse) | |

| (n=50) | 0.0085 (0.1147) | 0.0527 (0.1836) |

| (n=100) | 0.0053 (0.0824) | 0.0635 (0.1363) |

| (n=500) | 0.0020 (0.0389) | 0.0335 (0.0847) |

| (n=1000) | 0.0014 (0.0287) | 0.0038 (0.1193) |

| Hüsler-Reiss() | ||

| bias (rmse) | bias (rmse) | |

| (n=50) | 0.0119 (0.1293) | 0.0729 (0.1893) |

| (n=100) | 0.0077 (0.0838) | 0.0706 (0.1387) |

| (n=500) | 0.0020 (0.0383) | 0.0378 (0.0851) |

| (n=1000) | 0.0020 (0.0293) | 0.0060 (0.1084) |

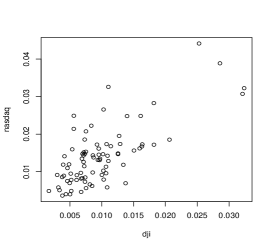

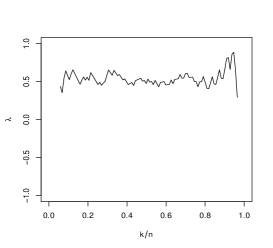

3.2 Application to financial data

We shall see evidence of tail dependence in financial data. We consider the monthly maximum of the negative log-returns of Dow Jones and NASDAQ index for the time period 1994-2004. The corresponding scatter plot and TDC estimate plot of for various (Figure 1) show the presence of tail dependence and the order of magnitude of the tail-dependence coefficient. Moreover, the typical variance-bias problem for various threshold values can be observed, too. In particular, a small k induces a large variance, whereas an increasing k generates a strong bias of the TDC estimate. The threshold choosing procedure of used in Section 3 leads to a TDC estimate of and from our estimator we derive .

|

References

- [1] Beirlant, J., Goegebeur, Y., Segers, J. e Teugels, J. (2004). Statistics of Extremes: Theory and Application. John Wiley.

- [2] Coles, S., Heffernan, J., Tawn, J. (1999). Dependence measures for extreme value analysis, Extremes 2 339-366.

- [3] Embrechts, P., McNeil, A., Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls In: Risk Management: Value at Risk and Beyond, ed. M.A.H. Dempster, Cambridge University Press, Cambridge, pp. 176-223.

- [4] Embrechts, P., Lindskog, F., McNeil, A. (2003). Modelling Dependence with Copulas and Applications to Risk Management, In: Handbook of Heavy Tailed Distibutions in Finance, ed. S. Rachev, Elsevier, Chapter 8: 329-384.

- [5] Fermanian, J.-D., Radulović, D. (2004). Wegkamp, M., Weak convergence of empirical copula processes. Bernoulli 10(5) 847-860.

- [6] Ferreira, H. , Ferreira M.. Tail dependence between order statistics, Journal of Multivariate Analysis (2011), doi:10.1016/j.jmva.2011.09.001.

- [7] Ferreira, H., Ferreira M., Extremal dependence: some contributions (Submitted) (arXiv:1108.1972v1).

- [8] Frahm, G., Junker, M., Schmidt R. (2005). Estimating the tail-dependence coefficient: properties and pitfalls. Insurance Math. Econom. 37 (1) 80-100.

- [9] Huang, X. (1992). Statistics of Bivariate Extreme Values. Ph. D. thesis, Tinbergen Institute Research Series 22, Erasmus University Rotterdam.

- [10] Joe, H. (1997). Multivariate Models and Dependence Concepts, Chapman & Hall, London.

- [11] Krajina, A. (2010). An M-Estimator of Multivariate Tail Dependence. Tilburg: Tilburg University Press.

- [12] Leadbetter, M. R., Lindgren, G. e Rootzén, H. (1983). Extremes and Related Properties of Random Sequences and Processes. Springer-Verlag, New-York, Heidelberg-Berlin.

- [13] Ledford, A., Tawn, J.A. (1996). Statistics for near independence in multivariate extreme values, Biometrika 83 169-187.

- [14] Ledford, A. Tawn, J.A. (1997). Modelling dependence within joint tail regions, J. R. Stat. Soc. Ser. B Stat. Methodol. 59 475-499.

- [15] Mejzler, D. (1956). On the problem of the limit distribution for the maximal term of a variacional series, L’vov Politechn. Inst. Naucn. ZP., 38 90-109.

- [16] Schmidt, R., Stadtmüller, U. (2006). Nonparametric estimation of tail dependence, Scandinavian J. Statist. 33 307-335.

- [17] Sibuya, M. (1960). Bivariate extreme statistics, Ann. Inst. Statist. Math. 11 195-210.

- [18] Tiago de Oliveira, J. (1962-1963). Structure theory of bivariate extremes, extensions, Est. Mat. Estat. Econ. 7 165-195.