Properties of Doubly Stochastic Poisson Process with affine intensity

Abstract

This paper discusses properties of a Doubly Stochastic Poisson Process (DSPP) where the intensity process belongs to a class of affine diffusions. For any intensity process from this class we derive an analytical expression for probability distribution functions of the corresponding DSPP. A specification of our results is provided in a particular case where the intensity is given by one-dimensional Feller process and its parameters are estimated by Kalman filtering for high frequency transaction data.

1 Introduction

The Doubly Stochastic Poisson Processes (DSPPs) were introduced by

Cox (1955) by allowing the intensity of the Poisson process to

be described by a positive random variable and not just a

deterministic function. The aim of such a generalization was to

allow the dynamic of a process that is exogenous to the model to

influence transitions in the point process that we are concerned

with. Point processes have applications in several areas of

applications, among which we mention: biostatistics, finance and

reliability theory. In biostatistics they form a theoretical

framework for studying recurrent events, as was done in

Gail et al. (1980), in studies of the size of tumors in rats over a

period of time. In finance, Lando (1998) was the pioneer in using

point processes for describing occurrences of credit events. In

reliability theory, Dalal and McIntosh (1994) work has developed criteria for

determining an optimum stopping time for testing and validating a

software.

It was the seminal work by Cox (1955) which introduced the DSPPs

(also known as the Cox Process). The main work in this field is

Grandell (1976) where the main properties of the DSPPs have been

presented in terms of standard construction of Probability Theory.

Alternatively, in the books of Brémaud (1972) and Daley and Vere-Jones (1988)

the presentation is based in line with the concepts and properties

of Martingales. However, all these sources focus on deriving

general properties of DSPP, without exploring the functional form

of the intensity of the process. Consequently, they attracted a

reduced number of applications.

The study of the DSPPs took a new turn once the functional form

for the intensity of the process has been specified. As a result

it became possible to obtain analytical expressions for

probability density functions for different types of processes. In

this context we can quote may be cited Bouzas et al. (2002) who made

use of truncated normal distribution to describe the intensity of

the process and Bouzas et al. (2006) who generalized the form of

intensity to include the case of a harmonic oscillator. The

contribution of these works was that closed analytical expressions

for density functions of the Cox process have been obtained, as

well as their moments. However, in both cases the authors used

constructions in which the restriction on non-negativity for the

intensity measure was not maintained. In order to get a round of

this limitation, the authors defined a region in the parameter

space where the probability of occurrence of negative values for

the intensity is reduced. With the intent to guarantee the

preservation of the non-negativity condition, Basu and Dassios (2002)

and Kozachenko and Pogorilyak (2008) suggested the adoption of a lognormal model

for the process intensity. A formulation that incorporates the

intensity into a dynamic formulation is developed in

Dassios and Jang (2008) who use the functional form of a process of

the Shot-Noise type which, despite guaranteeing the non-negativity

of intensity, is not in fact a diffusion process. On the other

hand Wei et al. (2002) assumed that the intensity is governed by a

one-dimensional Feller process and

obtained a form of probability density function for the corresponding DSPP.

Feller processes were introduced and established in the financial

literature after Cox et al. (1985). One of the properties is that the

Feller process lives in which guarantees that the

non-negativity condition is fulfilled. In the present work we

assume that the intensity is controlled by a related diffusion

process, as formalized by Duffie and Kan (1996), which incorporates Feller

processes in one or dimensions. In this way, the models from

Wei et al. (2002), Basu and Dassios (2002) and Kozachenko and Pogorilyak (2008)

can be seen as specific examples of the model proposed in the present work.

The use of point processes in finance, especially of DSPPs,

progressed considerably at the end of the 1990s with the

development of models of managing and pricing the credit risk. In

particular, Duffie and Singleton (1999) and Duffie et al. (2003) formalized the construction

of the probability density of the first jump in the process, in a

related context. More precisely, the time to the first jump

represents, in the context of credit risk, the time until the

bankruptcy (default) of a company (and/or a country). Here, once

the absorbing state had been reached, it was unnecessary to study

the further dynamic of the DSPP.

Recently a new area of applications of point processes in finance

has emerged, along with the use of these models for describing the

arrival process of bid and ask orders in an electronic trading

environment. In these models, the arrival process of orders

changes over time; the idea is to characterize the dynamic of

this process and obtain expressions that may be treated

analytically, describing the probability that an order had been

sent in line with a market configuration and was executed before

the price was

altered. See Cont et al. (2010).

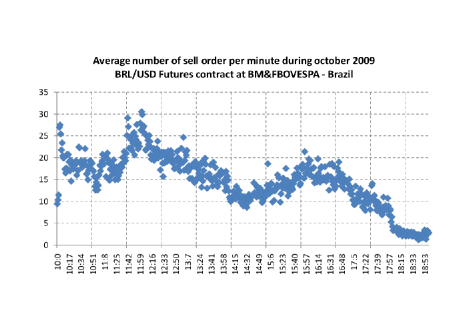

Perhaps the most well known point process is the homogenous Poisson process. For this process the arrival rate is constant. A homogenous Poisson process can therefore be described by a single value . However, in many applications the assumption of a constant arrival rate is not realistic. Indeed, in financial data we tend to observe bursts of trading activity followed by lulls. This feature becomes apparent when looking at the series of actual orders arrivals. Figure 1 presents the average number of sell orders for BRL/USD FX futures submitted to the Brazilian Exchange, BVMF. The plot indicates a non-constant behavior for the average number of submitted orders; the homogenous Poisson model is clearly not suitable for such data.

In fact, the number of bids and asks that getting into the order

book may depend upon a number of factors exogenous to the model.

For example, it may be the level of investors risk aversion on a

given day, or intra-day seasonality, or a disclosure of a piece of

information, or a new technology producing an impact on a certain

sector of the economy. For this reason, in our opinion, the

construction of a model that can be treated analytically and

incorporates endogenously a stochastic behavior of the intensity

of a point process represents a contribution to the literature. In

light of the above topics, the main aim of this article is to

present new results on DSPPs when the intensity

belongs to a family of so-called affine diffusions with potencial application in high frequency trading.

In this situation seems reasonable to focus on a particular class of models and attempt to use the approach based on point processes in order to study their dynamic over time. For this purpose we selected the Affine Term Structure (ATS) models, and our goal is to obtain the form Theorem for the Probability Density Functions for the Cox Process when the intensity belongs to a family of affine diffusion. Additionally, in one particular case when the intensity is governed by an one-dimensional Feller diffusion we obtain more detailed results, such as its moments and the convergence to its stationary distribution. Finally we propose an estimation procedure for point processes with stochastic affine intensity based on Kalman Filter conjugated with quasi-maximum likelihood estimator. Thus, the estimation procedure is applied to high frequency transactional data from FX futures contracts traded in Brazil.

2 The basic structure

Consider the filtered probability space , where is a filtration having the sets with null measure and right continuous.

Definition 1

Let be a non-negative random variable , which is defined on a probability space , such that .

Definition 2

Given a no-decreasing sequence of stopping time , the Point Processes is a (càdlàg) processes defined as:

| (1) |

Definition 3

Define the intensity processes as:

| (2) | ||||

| (3) |

With and .

Where the state variable will be defined below.

Definition 4

Let be

a filtered probability space and let be a

sub-filtration of . We called cumulate

intensity (or Hazard Process) an -adapted,

right-continuous, increasing stochastic process

for with

-a.s. and .

The hazard process plays an important role in the martingale approach to either credit risk or asset pricing because it is the compensator of the associated doubly stochastic Poisson process, see for example Bielecki and Rutkowski (2002). For our purposes, the hazard process will be important to derive the probability density function for the Point Process, . To construct the stopping time with the given intensity, define as in Lando (1998):

| (4) |

where is a unit exponential random variable independent

of i.

Definition 5

Let , be the state variable as solution for the stochastic differential equation SDE:

| (5) |

where: , is the drift; , the diffusion coefficient and, the standard Brownian

Motion defined in . Where will be

properly defined below.

Definition 6 (Duffie and Kan (1996))

Define as an affine processes, if the following condition are simultaneously satisfied for (5):

-

1.

Drift

(6) For and

-

2.

Covariance matrix

(7)

Where is matrix not necessarily symmetric, and is a diagonal matrix with the i-th elements from the diagonal given by:

| (8) |

with a e .

Adopting the construction of Duffie and Kan (1996) and Dai and Singleton (2000) the state variable in its affine form is:

| (9) |

where is the d-dimensional independent standard

Brownian Motion in , and are

matrices which may be nondiagonal and

asymmetric.

According to Duffie and Kan (1996) the coefficient vectors in (8) generate stochastic volatility

unless they are all zero, in which case (9) defines a

Gauss-Markov process. If the volatilities (all or some) are

stochastic, then two questions face up: how to constrain the model

in order to avoid negative volatilities? Under those constraints,

which is the set where the

process can take values?

The open domain implied by nonnegative volatilities

may be defined as:

| (10) |

The following condition of Duffie and Kan (1996) is sufficient for the positiveness of :

Condition A (Duffie and Kan (1996)): For all i:

-

1.

-

2.

, then for

Both parts of Condition A are designed to ensure strictly positive

volatility, and they are both effectively necessary for this

purpose.

A second set of constrains must be imposed to guarantee that the non-negativity condition for is fulfilled. The open domain implied by nonnegative intensities may be defined as:

| (11) |

In this sense, the strongest form of guarantee that (10)

and (11) are simultaneously met it is to impose

. However, it is a very strong

constraint on the state space resulting in a large number of

models excluded.

Using the Canonical Representation developed by Duffie and Singleton (1999) it will

be possible to overcome the non-negativity for . In fact, according to the Canonical Representation,

, where , the state vector

will be split into two subvectors: the first factors vector

, with and the other

group of factors are stacked in .

This way it is also possible to overcome existence and uniqueness

problems for a more general class of affine diffusion than the one

that satisfies (9). In fact the process exists

and is unique, moreover it is autonomous with respect to

. The volatility of , conditionally on

, is given, so there is no uniqueness problem concerning

. Finally, from the Canonical Representation it is known

that the process , when , has Gaussian

Distribution, independent from , with mean and standard deviation .

From the Canonical Representation, we just need to impose an extra

condition to ensure strictly positive of .

Condition B: if we set

| (12) |

it is possible to state that:

Proposition 1

If , then the process is nonnegative almost sure, i.e. .

Proof of Proposition 1

According to the Canonical Representation, the process is Gaussian with mean and standard deviation . Thus it is possible to compute the probability :

| (13) |

where is the cumulative normal distribution function.

| (14) |

where:

Then by requiring that the non-negativity condition for is satisfied almost sure.

We now turn to examples and illustrations of Affine framework.

-

•

Example 1

: Ornstein-Ulhenbeck (Vasicek)

-

•

Example 2

: Feller (or Square Root, Cox-Ingersoll-Ross)

-

•

Example 3

: Geometric Brownian Motion

-

•

Example 4

: Heston (Stochastic Volatility)

-

•

Example 5

: Multivariate CIR

In order to have the no-negative random variable as a stopping time a technical conditions must be imposed over the filtration. So we shall first examine a trivial case where the condition is not respected.

Proposition 2

The hitting time is not a -stopping time with respect to

Proof of proposition 2

Assume, by absurd, that is -stopping time for

, so using the

Martingale Representation Theorem there exist a compensated

process (a -Martingale) which may be represented

as a stochastic integral with respect to the Brownian motion .

Therefore we arrive a contradiction because must jump in

.

Thus the filtration should be enlarge. There are several ways to expand it but we do enlarged just to get as stopping time. Then the proper filtration will be constructed as:

where333:= maximum between A and B

Definition 7

Let be a filtered probability space and a stochastic processes defined on it. Let be a sub-filtration of , then is called a Doubly Stochastic Poisson Process with relation to , if is -measurable and for all and the next condition be satisfied:

| (15) |

where

As a particular case:

| (16) |

Therefore, conditioned to -field the

increments of are independent of the -field

.

Thus, the probability of no occurrences within the interval for the processes with intensity is given by:

| (17) |

2.1 Laplace transform for the process

The Laplace transform of stochastic processes is a key ingredient

to achieve our results. However Laplace transform for integral of

stochastic processes may be obtained in closed form only for a

limited number of processes.

Albanese and Lawi (2004) formalize the criteria to define which processes have a analytic form for its Laplace transform. Thus take a diffusion defined on and consider the Laplace transform defined by:

| (18) |

where , and two Borel functions.

Thus, it is possible to state that:

Result 1 (Albanese and Lawi (2004))

The class of stochastic processes with Laplace transform for its integral is given by:

| (19) |

With additional conditions:

-

1.

Three second order polyonymous in x: ,,. Such that belongs to the set o e ;

-

2.

The function is a linear combination of hypergeometric functions of the confluent 444A hypergeometric function in its general form may be written as: For been represented using Taylor’s expansion around

From type if and gaussian from type otherwise.

Thus the Laplace Transform is defined by:

| (20) |

Example 6

: As an application from the above result we shall prove that

the Laplace transform of when

the intensity follows a one-dimension Feller process exists.

Thus assume that the polynomials are defined as:

| (21) |

Substituting the polynomial into (19) with a variable change we have:

So in those cases where the Laplace transform exists it is possible to apply the well know result555Details might be found in Karatzas and Shreve (1991):

Result 2 (Feynman-Kac)

Let be a diffusion process with infinitesimal generator . Assume that and is bounded. Then:

| (22) |

it is solution of the partial differential equation (PDE):

| (23) |

and

| (24) |

Furthermore 666We write for trace of a matrix., if solve (23), then .

Taking the Theorem 2 it is possible to state that:

Proposition 3

Let be a diffusion processes satisfying the regularity condition so the solution to (23) has the form:

| (25) |

where the coefficients and are deterministic and satisfying777where ∣ stand for the derivative with respect to .:

| (26) | ||||

| (27) |

with a and .

Proof of Proposition 3

Inserting into the PDE above and grouping the terms in :

Where

| (29) | ||||

| (30) |

Use the separation of variable technique to obtain that and satisfy a Riccati equation with boundary condition e .

3 Distribution of Doubly Stochastic Poisson Process

For a non-homogeneous Poisson processes with intensity , the probability of k occurrences within the interval is given by:

| (31) |

Thus it is possible to state the important result:

Theorem 1

The Probability Distribution Function for a Doubly Stochastic Poisson process, , within at interval when the intensity is an affine diffusion as (9) is given by:

| (32) |

is the k-th derivative of Moment Generating Function for the Hazard Process,

Proof of Theorem 1

Imposing and on the left hand side of equation (22) it may be seen as the Laplace Transform (or Moment Generating Function) for the Hazard Process, .

Thus, using that if is the MGF of , then

| (33) |

and so the result follows.

In a particular case when the intensity follows an one-dimensional Feller process we have:

Theorem 2

The Probability Density Function (PDF) for a non-homogeneous Poisson processes within the interval when the intensity takes the form

| (34) |

is expressed by:

| (35) |

| (36) |

and

| (37) |

| (38) |

| (39) |

Proof of Proposition 2

See appendix A

Since DSPPs processes are essentially Poisson processes, each result for Poisson processes generally has a counterpart for DSPPs processes. The following are some basic properties of a DSPP process driven by . See Brémaud (1972) or Daley and Vere-Jones (1988) for further properties.

Proposition 4

The first two moments of where the intensity is an one-dimensional Feller process are:

1.

| (40) |

The first moment is obtained using the Laplace transform of

:

For the second moment we need an additional result:

| (42) |

Substituting in we obtain the result.

The stochastic nature of the intensity causes the variance of the process to be greater than the variance of a homogeneous Poisson process with the same expected intensity measure. This feature of the DSPPs processes is referred, in the literature on point processes and survival models, as overdispersion.

4 Stationary distribution for

Stationarity is a very important concept in time series analysis.

A stationarity assumption will allow us to estimate parameters

from point processes and make predictions. The characterization of

stationarity for a Point process relying on whether its intensity

process is stationary.

Definition 8

A point process is stationary (or isotropic) if for all e

Thus, the increments of are translation invariant

distribution with respect to any translation .

The definition above can be written in a short form:

Where:

and means equally in distribution.

Proposition 5

The Doubly Stochastic Poisson Process is stationary if its intensity is stationary.

Proof of Proposition 5

The Laplace transform for a point process, , with intensity process is given by:

| (43) |

Thus, taking a with (43):

| (44) |

Therefore, if is stationary such that , so together with (44) we obtain:

| (45) |

In a recent paper Glasserman and Kim (2010) analyze the tail behavior, the range of finite exponential moments, and the convergence to stationarity in affine models, focusing on the class of canonical models defined by Duffie and Singleton (1999). According to Glasserman and Kim (2010) the one-dimensional Feller process has a stationary distribution so the next step is determinate it.

Proposition 6

The stationary distribution of one-dimensional Feller process is the Gamma distribution with parameters and

Proof of proposition 6

See Appendix B

Definition 9

Suppose that are locally finite measures defined on , a necessary condition for Vague Convergence of to , in short , is

Where: is a continuous function with compact

support

From the definition 9 we shall present without proof the well know result for convergence of point process:

Result 3

Let defined on be a sequence of Point processes the following results are equivalents:

-

1.

-

2.

-

3.

Theorem 3

For all , suppose that is Poisson process defined on with intensity . If and is locally finite, thus , where is a Poisson process with intensity

Proof of Theorem 3

The Laplace transform for a point processes (43) may be

written as , for

, where . The Theorem

3 establish that , so:

| (46) |

It follows from result 3 that .

From the above results it is possible to determine in a closed form the stationary distribution of . We now turn to one application of this result.

Proposition 7

The stationary distribution of with intensity given by is the negative Binomial distribution.

Proof of Proposition 7

We have determined the stationary distribution for when the intensity is given by an one-dimensional Feller process. Closely related to this result is the determination of the rate of convergence of to its stationary distribution .

Theorem 4

The Cox Process converge to its stationary distribution, , exponentially fast at rate .

Proof of Theorem 4 It is known that the transition density for the process when it follows a Feller process is a non-central -distribution. From proposition 6 we have shown that the process converge to the Gamma distribution. According to Karlin and Taylor (1981), it is possible rewrite both distribution by its spectral representation:

| (47) |

where is the Laguerre polynomial with

parameter , and with the following property . is the Gamma Function.

To describe the stationary distribution by its spectral

representation we just need to set at equation (47).

We decided to evaluate the convergence speed of by looking at the convergence of its density functions written in the spectral form:

| (48) |

Because according to the spectral representation, we have that for , the only term inside the summation involving t is .

Finally, the unconditional version of Cox process gives us:

| (49) |

Therefore,

| (50) |

5 Model Application

In section 2 we developed the requisite theory used to construct the Cox Process as an affine function of the underlying state variables. In every case, this relationship was subject to a given parameter set. Unfortunately, the theory does not tell us anything about the appropriate values that must be specified for this parameter set. We must, therefore, turn to the econometric literature to handle this important issue. Since the seminal paper by Engle and Russell (1998) the modelling of financial point process is an ongoing topic in the area of financial econometrics. The financial point processes are associated with the random arrival of specific financial trading events, such as transactions, quote updates, limit orders or price changes observable based on financial high-frequency data.

Moreover, it has been realized that the timing of trading events,

such as the arrival of particular orders and trades, and the

frequency in which the latter occur have information value for the

state of the market and play an important role in market

microstructure analysis.

Although the literature on the parametric estimation of point

processes (financial Point Process as well) is as large as the

theoretical literature, there is as yet no consensus as to the

best approach. Based on that, we propose a new technique to the

estimation of Cox Processes parameters. The methodology we will be

using, based on the Kalman filter, exploits the theoretical affine

relationship between the Cox Process and the state variables to

subsequently estimate the parameter set. The strength of this

approach is that Kalman filter is an algorithm that acts to

identify the underlying, and unobserved, state variables that

govern the Cox Process dynamics. Once the unobserved component is

filtered the Quasi-Maximum likelihood estimator will be able to

determine the model parameters.

In order to estimate parameters and to extract the unobservable state variables we restrict the equation (35) to deal with the probability of no arrivals, , within the interval . Therefore, the probability of no arrivals for the Cox Process with Feller diffusion is

Additionally it is possible linearize (51):

| (52) |

Thus, the measure equation is log-linear in and it can be written as:

| (53) |

where:

The inclusion of an error term in equation (53) is

motivated by the fact that the underlying intensity process may be

inadequate. If the true factor process is not a Feller process

equation (51) will be functionally misspecified and

estimates of will be inferior. In this case the

probability of no arrivals within the interval implied by

the Feller process will systematically deviate from observed

arrivals. Therefore, in a correctly specified model the errors

should be serially and cross-sectionally uncorrelated

with mean zero.

It is known that the exact transition density for the Feller Process is the product of K non-central -densities. Estimation of the unobservable state variables with an approximate Kalman filter in combination with quasi-maximum-likelihood (QML) estimation of the model parameters can be carried out by substituting the exact transition density by a normal density:

where and are defined in such a way that the first two moments of the approximate normal and the exact transition density are equal. The moments are time varying and defined as:

| (54) |

and is diagonal matrix with elements:

| (55) |

Note that once we have represented the Cox Process with Feller intensity into a State Space form we can, according to Harvey (1989), to calculate the quasi log-likelihood:

| (56) |

where is the sample size; is the dimensional of the Feller

process.

6 Empirical Analysis

6.1 Data description

In this section, we apply our estimation technique to some transaction data from the Brazilian Exchange (BM&FBOVESPA)888BM&FBOVESPA is the fourth largest exchange in the word in terms of market capitalization. BM&FBOVESPA has a vertically integrated business model with a trade platform and clearing for equities, derivatives and cash market for currency, government and private bonds. .

The sample is formed by all submitted sell orders for BRL/USD FX

futures contract999Ticker: FUT DOLX08 traded in

BM&FBOVESPA during October 2008 with expiry date of November 1,

2008. This FX contract is one of the most liquid FX contracts in

the emerging markets and the average volume of 300.000 traded

daily is significant even for developed markets. We have a total

of 535 records with trading occurring continuously from 10 am to 6

pm

exclusively through the electronic venue.

The BM&FBOVESPA electronic trade system (GTS) uses the concept of

limit order book, matching orders by price/time priority. Lower

offer price take precedence over higher offers prices, and higher

bid price take precedence over lower bid prices. If there is more

than one bid or offer at same price, earlier bids and offers take

precedence over later bids and offers. The offers are recorded in

milliseconds allowing the highest precision for determination of

precedence criteria. We also observe that no two consecutive

orders arrive in the order book in an intervals smaller than 10

milliseconds, probably due to the internal network latency

While the probability of no arrivals are not themselves directly observable, we can use the empirical frequency of orders arrivals as proxy. To construct the empirical frequency we aggregate orders sent within a same minute for every day during October and the average value is taken. Thus, due to the 10 milliseconds network latency, it is possible, at least theoretically, that 6.000 sells orders could arrive in the order book in 60 seconds.

Therefore, the observable variable is constructed as101010where # is the count measure within the interval :

| (57) |

6.2 Estimation results

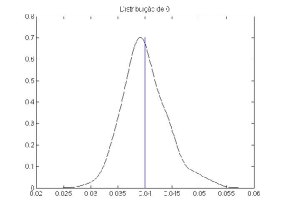

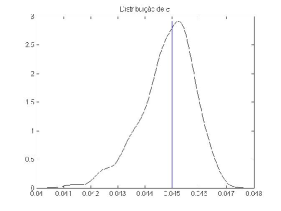

In section we illustrate the properties of the Kalman filter for estimating the parameters of Cox Process with Feller intensity. Table 1 contains the parameter estimates . The estimated standard deviations of errors - the square root of the diagonal elements of H - are also presented in Table 1. Standard errors for the QML estimates are obtained as described in Hamilton (1994, p.389).

| Std. Error | ||||

|---|---|---|---|---|

| Estimates | 0.065 | 0.0043 | 0.00267 | 0.0010 |

| Std Error | 2.6E-05 | 1.7E-05 | 7.47E-08 | 2.68E-09 |

We obtain highly significant parameter estimates (at the 1% level). Additionally, the estimated standard deviation for the measurement error is twice smaller than the diffusion parameter .

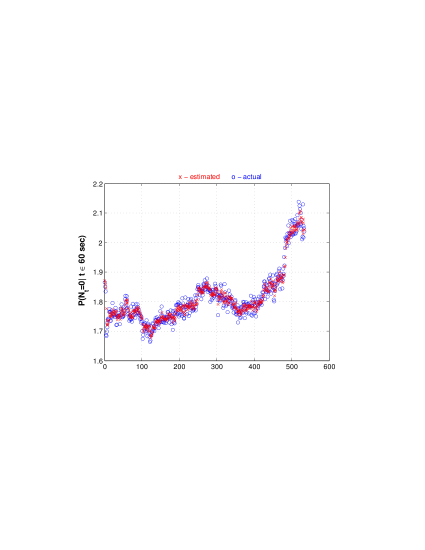

From figure 1 we can see the model flexibility in reacting to different changes in the numbers of orders submitted. In this case, the model seems to fit quite well to actual order flow and the differences between actual and theoretical probability indicate that, on average, the model tends to slightly under-estimate actual occurrence of sell orders. In order to assess the model fitted we conducted a diagnostic checking for possible misspecifications based on the standardized residuals. For a well specified model we need the residuals follows a white noise process.

| L | Q(L) | p-value |

|---|---|---|

| 5 | 8.36 | 0.13 |

| 10 | 13.47 | 0.19 |

| 15 | 17 | 0.31 |

Table 2 contains the Ljung-Box111111The Ljung-Box statistic tests the hypothesis that a process is serially uncorrelated. Under the null hypothesis, the Q(L) statistic follows a Qui-Square distribution with L degrees of freedom, where L is the maximum number of temporal lags. statistics up to the lag. The LB test statistic allows us to not reject, at a high significance level, the hypothesis that errors are white noise. In the absence of dependence in errors the Feller process for intensity seems to be a right choice to describe the observed sell orders behavior.

7 Simulation results

In this section, to analyze the performance of our estimation

algorithm we simulate various Cox Process outcomes using a known

parameter set and proceed to estimate the model parameters. This

simulation exercise is intended to indicate how effective this

technique is in terms of identifying parameters. The simulations

for the unobservable state variables have been drawn from the

noncentral Qui-Square distribution121212The samples were drawn

from the Chi-Square distribution with degrees of freedom and

noncentrality parameter, :

, , and the measurement errors have been

simulated as normal random variables with zero means.

The simulation of a sample path for the Cox process with 500 elements, followed by application of the estimation algorithm, is repeated 250 times. The following table summarize the results of the simulation exercise for the Cox Process. The table reports the true values, the mean estimate over the 250 simulations, the Mean Quadratic Error, and the associated standard deviation of the estimates.

| Actual Value | 0.04 | 0.2 | 0.05 |

| Mean estimate | 0.04 | 0.3698 | 0.0448 |

| MQE | 1.5303e-005 | 0.37 | 0.0023 |

| Std. Error | 0.0039 | 0.52 | 0.0001 |

8 Final Remarks

Making use of the theoretical framework developed to model

interest rate term structure allow us to obtain the Probability

Density Function for a Double Stochastic Poisson Process (DSPP)

when the intensity process belong to a family of affine diffusion.

Furthermore, the stationary distribution for DSSP may be found

whenever the intensity process is also stationary. To illustrate

our results in this paper one of most common diffusion in interest

rate dynamics literature is assumed to drive the intensity

process, the one-dimensional Feller process. However the results

derived here are valid for any type of affine diffusion in

d-dimension.

Finally this paper does not have an empirical focus, and these results are primarily illustrative. The empirical analysis was included to highlight that applied papers on estimating the parameter set for the models examined in section 2 are straightforward.

Appendix A Proof of proposition 16

Specifying the form of and into the Theorem 2 we have:

| (58) |

With boundary condition

Using the results from proposition 3 together with (58)131313Where subscript denotes partial derivative:

Plugging the above results into (58):

| (59) |

Since the left hand side is a function of , while the right is independent of it, the following equations must be satisfied:

| (60) |

The first term of (60) is Riccati equation with solution where e are solutions to the following system: 141414 e are functions of and , but is fixed, hence denote the derivative with respect to :

| (61) |

Let , so and the system above may be written as:

| (62) |

From the second term of (62) we have:

| (63) |

Substituting into (62) and rewriting this in terms of -operators:

| (64) |

Taking the roots of the quadratic equation (65) together with the boundary condition allow write the solution as:

| (65) |

Substituting into (63) gives:

| (66) |

Since , the solution of the Riccati equation is obtained from (65) and (66):

| (67) |

Now consider equation (60) with fixed, so is a function of only. Hence:

inserting according to (67) gives:

| (68) |

Appendix B Sketch of the proof of proposition 6

Let be the transition density of , for simplicity assume that at instant . From the Forward Kolmogorov equation:

| (69) |

The stationary distribution must satisfies . When reached the stationary distribution is independent of , so . Combining it together with (69), we have151515A rigorous proof might be found in Pinsky (1995) p. 181 and 219:

| (70) |

Let be the integrating factor, so integrating (70) twice:

| (71) | ||||

| (72) |

Where:

The constants e are determined such that be a probability density function, so

Thus, using the form of and simplifying we have:

In short,

References

- Albanese and Lawi (2004) C. Albanese and S. Lawi. Laplace transforms for integrals of markov processes. Markov Processes and Related Fields, 11:677–724, 2004.

- Basu and Dassios (2002) S. Basu and A. Dassios. A cox process with log-normal intensity. Insurance: Mathematics and Economics, 31:297–302, 2002.

- Bouzas et al. (2002) P.R. Bouzas, M.J. Valderrama, and A.M. Aguilera. Forecasting a class of doubly poisson processes. Statistical Papers, 43:507–523, 2002.

- Bouzas et al. (2006) P.R. Bouzas, M.J. Valderrama, and A.M. Aguilera. On the characteristic functional of a doubly stochastic poisson process: Application to a narrow-band process. Applied Mathematical Modelling, 30:1021–1032, 2006.

- Brémaud (1972) P. Brémaud. Point Processes and Queues: Martingale Dynamics. Springer-Verlag, New York, 1972.

- Cont et al. (2010) R. Cont, S. Stoikov, and R. Talreja. A stochastic model for order book dynamics. Operations Research, no Prelo, 2010.

- Cox (1955) D. R. Cox. Some statistical methods connected with series of events. Journal of Royal Statistical Society B, 17:129–164, 1955.

- Cox et al. (1985) J. Cox, J. Ingersoll, and S. Ross. A theory of the term structure of interest rates. Econometrica, 53:385–408, 1985.

- Dai and Singleton (2000) Q. Dai and K. Singleton. Specification analysis of affine term structure models. The Journal of Finance, LV(5):1943–1978, 2000.

- Dalal and McIntosh (1994) S. Dalal and A. McIntosh. When to stop testing for large software systems with changing code. IEEE Trans. Software Eng, 20:318–323, 1994.

- Daley and Vere-Jones (1988) D.J. Daley and D. Vere-Jones. An Introduction to Theory of Point Processes. Springer-Verlag, New York, 1988.

- Dassios and Jang (2008) A. Dassios and J. Jang. The distribution of the interval between events of a cox process with shot noise intensity. Journal of Applied Mathematics and Stochastic Analysis, 2008.

- Duffie et al. (2003) D. Duffie, D. Filipovic, and W. Schachermayer. Affine processes and applications in finance. Annals of Applied Probability, 13:984–1053, 2003.

- Duffie and Kan (1996) D. Duffie and R. Kan. A yield-factor model of interest rates. Mathematical Finance, 6:379–406, 1996.

- Duffie and Singleton (1999) D. Duffie and K. Singleton. Modeling term structures defautable bonds. Review of Financial Studies, 12:687–720, 1999.

- Gail et al. (1980) M. Gail, T. Santner, and C. Brown. An analysis of comparative carcinogenesis experiments based on multiple times to tumor. Biometrics, 36:255–266, 1980.

- Glasserman and Kim (2010) P. Glasserman and K.K. Kim. Moment explosions and stationary distributions in affine diffusion models. Mathematical Finance, 20:1–33, 2010.

- Grandell (1976) J. Grandell. Doubly Stochastic Process. Springer-Verlan, New York, edition, 1976.

- Harvey (1989) A.C. Harvey. Forecasting, structural time series models and the Kalman Filter. Cambridge University Press, Cambridge, 1989.

- Kallenberg (1986) O. Kallenberg. Random Measures. Academic Press, London, edition, 1986.

- Karatzas and Shreve (1991) I. Karatzas and S. Shreve. Brownian Motion and Stochastic Calculus. Springer-Verlan, New York, edition, 1991.

- Karlin and Taylor (1981) S. Karlin and H. Taylor. A Second Course in Stochastic Process. Academic Press, New York, 1981.

- Kozachenko and Pogorilyak (2008) Yu. V. Kozachenko and O. O. Pogorilyak. A method of modelling log gaussian cox process. Theory of Probability and Mathematical Statistics, 77:91–105, 2008.

- Lando (1998) D. Lando. On cox processes and credit risky securities. Review of Derivatives Research, 2:99–120, 1998.

- Pinsky (1995) R. Pinsky. Positive Harmonic Functions and Diffusions. Cambridge University Press, 1995.

- Wei et al. (2002) G. Wei, P. Clifford, and J. Feng. Population death sequences and cox processes driven by interacting feller diffusions. Journal of Physics A: Mathematical and General, 35:9–31, 2002.